NV Energy will commit to joining CAISO’s Extended Day-Ahead Market (EDAM), sources have told RTO Insider, a move that will end months of speculation among Western electricity sector stakeholders about whether the Nevada utility would choose EDAM over SPP’s Markets+.

The utility plans to make its intent public May 31 when it files an integrated resource plan with the Public Utilities Commission of Nevada, multiple sources closely involved with market developments in the West said.

NV Energy did not respond to a request for comment on the matter, a topic of increasing interest in the region, with multiple sources recently telling RTO Insider that the utility has been revealing its decision in favor of EDAM in private meetings. An NV Energy executive offered the clearest public signal yet on the utility’s leaning during a May 22 joint session of the CAISO Board of Governors and Western Energy Imbalance Market (WEIM) Governing Body. (See Is NV Energy Leaning to CAISO’s EDAM?)

The selection still must be approved by the PUCN. A 2021 Nevada law requires the utility to join an RTO by 2030, with the decision subject to approval by the commission, which has been hosting workshops exploring the two day-ahead market options in the West as part of its RTO proceeding. (See Nevada RTO Proceeding Examines EDAM, Markets+ Design.)

At one of those workshops, the Brattle Group presented data showing NV Energy stood to gain $62 million to $149 million in annual economic benefits from joining the EDAM, while it stood to lose as much as $100 million from withdrawing from CAISO’s Western Energy Imbalance Market (WEIM). The results of joining Markets+ ranged from a loss of $17 million compared with the status quo to a benefit of $16 million. (See Nev. RTO Effort Turns Focus to NV Energy Day-ahead Studies.)

Big Win for EDAM

NV Energy’s decision spells a major victory for the EDAM in its ongoing competition for members with SPP’s Markets+ day-ahead offering.

The utility serves the majority of Nevada’s electricity users and is the balancing authority for the state. Its control area occupies a central position in the WEIM, functioning as the primary wheel-through point for energy transfers between the WEIM’s California participants — including the ISO — and PacifiCorp’s sprawling balancing authority area in the inland West.

PacifiCorp in April became the first entity to agree to sign an implementation agreement for the EDAM, sealing its participation in the market. (See PacifiCorp Fully Commits to CAISO’s EDAM.)

NV Energy’s membership in EDAM also would be consequential for Markets+ because the utility’s BAA sits between the territories of the entities that have shown the most interest in joining the SPP-run market, including the Bonneville Power Administration and Puget Sound Energy in the Northwest, and Arizona Public Service, Salt River Project and Tucson Electric Power in the Desert Southwest. The inclusion of Nevada’s transmission network in EDAM would limit the ability of those entities to transfer energy among each other in a geographically divided Markets+.

The decision also is significant for the West-Wide Governance Pathways Initiative. Backers of that effort in April issued a proposal to make stepwise changes to the governance of the WEIM/EDAM, with the objective of eventually putting the market under the authority of an independent “regional organization” after seeking changes to California law related to CAISO. (See Pathways Initiative to Act Fast on ‘Stepwise’ Governance Plan.)

But step 1 in that proposal entails elevating the “joint” authority the WEIM’s Governing Body currently shares with CAISO’s Board of Governors over WEIM matters to “primary” authority. Under the plan, the ISO would pursue that change with FERC only after the EDAM secures implementation agreements with a “set of geographically diverse” WEIM participants representing load equal to or greater than 70% of CAISO BAA annual load in 2022. With commitments from PacifiCorp, Balancing Authority of Northern California, Idaho Power, Los Angeles Department of Water and Power, and Portland General Electric, NV Energy has been cited by Pathways supporters as the entity needed to trigger that move.

NV Energy’s filing with the PUCN on May 31 will coincide with a monthly meeting of the Pathways Initiative’s Launch Committee, at which the committee is expected to vote on adopting step 1 of the governance proposal.

The CAISO Board of Governors and Western Energy Imbalance Market (WEIM) Governing Body voted unanimously May 22 to approve an expedited proposal to increase the ISO’s soft offer cap from $1,000/MWh to $2,000.

CAISO staff and stakeholders participating in the ISO’s Price Formation Enhancements (PFE) Working Group quickly crafted the plan as part of a strategy to improve the bidding prospects of energy-limited resources — such as battery storage and hydroelectric resources — ahead of late summer.

The ISO hopes to win FERC approval for the proposal by Aug. 1, the date that typically marks the start of the most challenging period for grid operations in the West because of declining hydro availability and the onset of what usually are the warmest conditions of the year in California’s load centers.

Grid operators across the region are preparing for the prospect of tight supplies this summer based on low water conditions in the Northwestern U.S. and the Canadian province of British Columbia.

“I see these changes as urgent, given the difficult hydro conditions in the Pacific Northwest. The market will benefit if more hydro resources are fully in the market as much as they can be,” Governing Body Chair Andrew Campbell said during the body’s joint session with the ISO’s board. “There’s urgency for batteries too. There’s so many batteries online this summer, and I support relying more on the market to manage charge and discharge rather than market operator directives.”

The two-part proposal is designed to allow energy-limited resources with “intraday opportunity costs” — specifically batteries and hydro — to factor those costs into their default energy bids (DEBs), but the new rules will apply to gas-fired generation as well. The ISO has emphasized that all resources will still need to justify the costs behind their bids. (See CAISO Moves for Expedited Change to Soft Offer Cap.)

Those opportunity costs arise on stressed days for the grid when supplies become tight, usually from extreme weather. In those circumstances, an energy-limited resource committed to the market at the $1,000/MWh soft offer cap can find itself dispatched at high prices occurring relatively early in the day, leaving it unable to provide energy later when prices are even higher.

To address the issue, the proposal seeks to revise CAISO’s rules related to FERCOrder 831, the 2016 directive that required RTOs and ISOs to limit the market bids of energy resources to the higher of either a soft offer cap of $1,000/MWh or a cost-based offer already verified by the market operator, up to a hard cap of $2,000 MWh.

‘Loud and Clear’

The proposal had solid backing from many industry stakeholders, including hydro-heavy WEIM participants Bonneville Power Administration and Seattle City Light, and was endorsed by CAISO’s Market Surveillance Committee (MSC) during its May 15 meeting.

Some stakeholders, such as BPA and the Western Power Trading Forum, expressed concern about a last-minute change to the proposal that limits storage resources to bidding above the $1,000/MWh cap only in the real-time market — and not in the day-ahead market — made in response to the MSC’s opinion that the ISO’s integrated forward market process already solves the opportunity cost issue for storage in the day-ahead.

Opponents included the California Public Utilities Commission and its Public Advocates Office, both of which raised concerns about the potential costs to ratepayers from increasing the cap and the speed with which the plan moved through CAISO’s stakeholder process.

Supporters among stakeholders and the CAISO and WEIM oversight bodies emphasized the measures should be considered only a temporary remedy. Some said the PFE Working Group should come up with a more complete solution before summer 2025, one that would more completely address the bidding requirements for storage and take up the needs of hybrid and demand response resources as well.

After expressing gratitude for the quick efforts by CAISO staff and stakeholders on the proposal, ISO Board Chair Jan Schori acknowledged how much more needs to be done on the matter.

“I am hearing loud and clear, from all the comments that we’ve received, that we simply have to do a lot more work on batteries and storage, and particularly fixing the [bid-cost recovery] rules,” Schori said. “But [batteries] are unique; they are different; and we need to probably come up with a set of rules that really works to match that resource and enable us to both have it be a long-term resource for the industry and for customers, but also to make sure it’s deployed at the time that we need it available to us to address the reliability issues that we may be confronting.”

New Approach to Large Load Addition Capacity Assignments Endorsed

The PJM Markets and Reliability Committee endorsed a proposal to revise how capacity obligations for serving large load additions (LLAs) are calculated to limit capacity assignments to areas where LLAs are forecast to interconnect.

The MRC did not vote on an alternative motion offered by American Municipal Power (AMP) under the committee’s truncated voting structure. (See “Changes to Capacity Assignments for Large Load Additions Contemplated,” PJM MRC Briefs: April 25, 2024.)

When bringing the issue charge in October 2023, American Electric Power (AEP) and Dominion Energy said the current capacity obligation assignments spreads PJM-approved LLAs across transmission zones, meaning an increased load forecast by an electric distribution company (EDC) participating in the reliability pricing model (RPM) could compel a fixed resource requirement (FRR) entity to procure capacity for load it will not serve.

In February, FERC granted AEP a waiver to alter the capacity obligation calculation for four of its vertically integrated utilities to not include forecast LLAs outside their territories. (See FERC Grants AEP Utilities Waiver of Capacity Obligation.)

The tariff and Reliability Assurance Agreement (RAA) revisions would rework how PJM calculates capacity obligation assignments to exclude LLAs included in Table B-9 of the load forecast from base zonal scaling factors and add those LLAs back when determining the obligation peak load input.

The AMP alternative sought to add a definition of large load additions to the Reliability Assurance Agreement (RAA) to clarify how they can result in capacity obligations for LSEs. The proposed redlines also rewrote a section of the “threshold quantity” definition pertaining to the preliminary forecast peak load for FRR entities in a transmission zone alongside RPM participants to remove the phrase “the FRR Entity’s Obligation Peak Load last determined prior to the Base Residual Auction for such Delivery Year, times the Base FRR Scaling Factor.” It will instead point to the relevant RAA section.

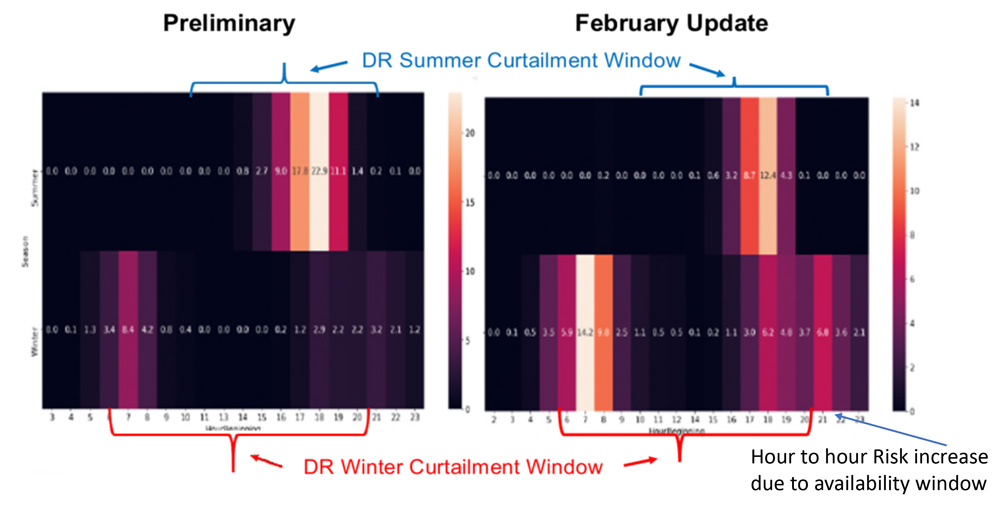

DR Availability Issue Charge Approved, Quick Fix Proposal Rejected

Stakeholders endorsed an issue charge to investigate modifying the availability of demand response resources, but they rejected a quick fix proposal to expand the winter availability window by two hours. The issue charge passed with 59% sector-weighted support; however, the proposal failed to carry the two-thirds threshold required at 54% support.

The issue charge and quick fix proposal were sponsored by the Advanced Energy Management Alliance (AEMA), PJM Industrial Customer Coalition (ICC), CPower, Enel and NRG Curtailment Solutions. (See “Demand Response Providers Seek Expanded Availability,” PJM MRC/MC Briefs: Feb. 22, 2024.)

Bruce Campbell, of Campbell Energy Advisors, said the revised risk modeling approach PJM adopted following the critical issues fast path (CIFP) process conducted last year led to the wintertime hours the model has found hold elevated reliability risks being expanded well into the night. However, the DR availability window was not expanded beyond the status quo 6 a.m. to 9 p.m., preventing dispatchers from using DR to address the full risks the RTO has identified. The proposal would extend the window in which DR is dispatchable by two hours to end at 11 p.m. (See FERC Approves 1st PJM Proposal out of CIFP.)

Several demand response providers argued that PJM’s wintertime risk projections, shown on two heat maps, justify expanding the DR availability window. | PJM

Campbell argued the longer availability window would not negatively affect the reliability contribution of DR resources, as most participants are industrial load that consumes power at a steady rate throughout the day irrespective of season.

Independent Market Monitor Joseph Bowring said the change would affect the effective load carrying capability (ELCC) rating for DR resources, a calculation tied into the ELCC ratings of all resources. Making a change to one resource would require recalculating all resource class ELCC values, which he said would be difficult and inappropriate to do with the original targeted implementation for the 2025/26 delivery year.

“PJM calculates the contribution of DR resources to reliability for ELCC purposes using an assumed maximum level of response rather than actual data on DR response during the winter. PJM uses actual data for generation resources. The result is that the ELCC of DR is significantly overstated,” Bowring told RTO Insider in an email. “Actual DR performance/load reduction during Winter Storm Elliott was well below 50% of the stated capacity values. A one-off administrative change to the rules that would arbitrarily increase payments to DR resources and reduce payments to other resources without a comprehensive review of the DR ELCC would be inappropriate.”

During the May 22 meeting, Campbell worked with other package sponsors to revise the issue charge to delay the targeted implementation of the quick fix portion of the issue charge to the 2026/27 Base Residual Auction (BRA). The issue charge was also revised to shift implementation of the third key work activity (KWA) — which seeks to eliminate the window outright or create an additional DR classification that would be available all day — to the 2027/28 delivery year. But this alternate version was rendered moot by endorsement of the original package.

PJM Director of Stakeholder Affairs David Anders said with the vote on the expanded availability window failing, the KWA is now considered complete and future stakeholder discussions will focus on the other work areas.

The proposal would add three intraday resource commitment runs to the day-ahead market, lining up with the North American Energy Standards Board’s (NAESB) gas nomination cycle deadlines. Gas generators would be notified that they are being committed with adequate time for them to nominate for fuel in the subsequent cycle and generators would be asked to voluntarily “use every reasonable effort to notify” PJM if they have procured fuel or expect to do so in time to be scheduled. The manual revisions also say PJM may perform additional resource commitment runs when necessitated by load forecasts, updated resource parameters or changing system conditions.

The proposed revisions to Manual 11 stress that the request for generators to notify PJM if they have or intend to procure fuel is voluntary and does not come with penalties for those who do not provide an update. Gas resources that do not procure fuel necessary to meet their day-ahead or reserve commitments are required to notify dispatchers by adjusting their availability or parameters in Markets Gateway, submitting an eDART ticket and by calling PJM dispatch. The changes include a note stating that keeping dispatchers informed about fuel availability during critical conditions “is essential to providing optimal situational awareness of generator availability to PJM Operations.”

Dominion Energy’s Jim Davis said the proposal is another step building on real-time values to increase operational certainty around the alignment of the electric and gas markets. The package was sponsored at the EGCSTF by PJM, Dominion and Gabel Associates.

First Read of CIFP Manual Revisions

PJM’s Skyler Marzewski presented a set of manual revisions implementing capacity market changes drafted through the CIFP process and approved by FERC in January, including several changes to reflect stakeholder feedback received since it was endorsed by the Market Implementation Committee on May 1.

The manual revisions would phase out Manuals 20, 21 and 21A and replace them with new Manuals 20A and 21B, as well as “cleaning up” Manuals 18 and 14B. (See “Stakeholders Endorse Manual Revisions to Implement CIFP Changes to Capacity Market,” PJM MIC Briefs: May 1, 2024.)

The changes to the Manual 18 language include spelling out a formula that helps determine unforced capacity (UCAP) values for load management resources and clarifying that existing FRR entities may terminate their election to participate in FRR rather than the RPM through “and including” the 2028/29 delivery year without being penalizes.

If endorsed, the capacity market changes would expand the use ELCC analysis for accrediting all generation types, require that planned resources notify PJM of their intent to participate in a Base Residual Auction (BRA) at least 90 days in advance and change how generation UCAP values are calculated. The MRC manual revisions are set to be voted on by the MRC during its June 27 meeting.

The revisions to Manuals 20, 21 and 21A — which focus on the planning side of the CIFP proposal — would establish a new approach to capacity accreditation, reliability risk modeling and BRA procurement targets. The PC is set to vote on the revisions on June 4 and would be included alongside the Manual 18 revisions at the MRC if approved. (See “First Read on CIFP Manual Revisions,” PJM PC/TEAC Briefs: April 30, 2024.)

Consumer Advocates Intend to Propose Wider DESTF Scope

Maryland and Illinois consumer advocates plan to propose revisions that would widen the scope of the Deactivation Enhancements Senior Task Force (DESTF) to include finding resources that could replace retiring generators and and have PJM consider alternatives to maintaining costly reliability-must-run (RMR) contracts while traditional transmission expansions are constructed to resolve any reliability violations prompted by the deactivation. The current issue charge is focused on how RMR compensation is determined, when generation owners need to notify PJM of their intent to deactivate and improving transparency.

Clara Summers, of the Illinois Citizens Utility Board (CUB), said the intent is to supplement the work of the DESTF, which is discussing proposals from the Monitor and PJM, rather than supplant those efforts.

Phil Sussler, of the Maryland Office of People’s Counsel (OPC), said there are multiple stakeholder discussions looking at generation deactivation siloed between the DESTF and other groups, such as the Interconnection Process Subcommittee’s work on how capacity interconnection rights (CIRs) may be transferred from a deactivating generator to a replacement resource at the same point of interconnection. Harmonizing those efforts raises the odds of a solution that allows the interconnection process to better react to a deactivation request, he said.

Vistra’s Erik Heinle said a balance is needed to ensure discussions do not become so broad that they collapse in on themselves.

“Each of these issues is an important one … but we also want to make sure we don’t get stuck and have the weight of multiple interests preventing us from getting to a solution as expeditiously as possible,” he said.

The call for harmonization mirrored comments at the May 8 Public Interest and Environmental Organization User Group (PIEOUG) meeting, where advocates said siloed processes make it difficult for offices with limited resources to track numerous discussions and limits the solutions on the table. (See “Consumer Advocates Call for More Holistic Thinking at PJM,” Consumer Advocates, Environmentalists Urge Holistic Thinking at PJM.)

AUSTIN, Texas — ERCOT stakeholders plumbed the depths of Robert’s Rules of Order and amended motions before endorsing a rule change May 22 that allows the grid operator to manually release ERCOT contingency reserve service (ECRS) from economically dispatched resources after repeated violations of the system power balance constraint.

Following multiple failed attempts, the Technical Advisory Committee finally met the two-thirds threshold for approval by lowering the nodal protocol revision request’s (NPRR1224) offer floor from the originally proposed $1,000/MWh to $750/MWh. The measure passed 20-10, opposed by the consumer and retail segments over concerns of price increases.

The change introduces a trigger that ERCOT can use to manually release ECRS from security-constrained economic dispatch (SCED)-dispatchable resources when the amount of the power balance violation is at least 40 MW for 10 consecutive minutes. With TAC’s modification, it would also require that energy offer curves for capacity assigned to ECRS be offered at the new floor.

ERCOT staff and the Independent Market Monitor have been collaborating on the issue since late 2023 after ancillary service methodology discussions for this year at TAC and the Board of Directors. The board directed staff to review the processes used to compute the minimum quantities of ECRS and identify potential alternatives by May.

The grid operator has been operating under a conservative posture since the 2022 summer. It has been procuring huge quantities of ancillary services to ensure it has enough operating reserves to account for intermittent solar and wind resources.

However, that has increased costs in ERCOT’s energy-only market. The Monitor says ECRS, the newest ancillary product, created artificial supply shortages that produced “massive” inefficient market costs totaling about $12.5 billion last year through Nov. 27. (See ERCOT Board of Directors Briefs: Dec. 19, 2023.)

The Monitor suggested the deployment trigger to avoid sequestering large quantities of ECRS out of SCED that it said caused the mechanism to perceive shortages that weren’t real and set energy prices much higher than their true marginal reliability value. It also proposed a re-evaluation of the ECRS procurement quantities and eliminating the $1,000/MWh offer floor.

“Such a provision would retain a significant portion of the artificial shortage pricing that we documented in 2023, mitigating only those prices that exceeded $1,000/MWh,” the Monitor said in its comments. “While this may be in the economic interest of suppliers in the short term, setting prices that are not based on market fundamentals … will undermine the credibility of the ERCOT markets over the longer term.”

Generation owners, led by Michele Richmond, executive director of Texas Competitive Power Advocates, and Lower Colorado River Authority’s Blake Holt and ENGIE’s Bob Helton, disputed the IMM’s valuation of ancillary service reserves.

After first jokingly suggesting that the issue be placed on TAC’s combination ballot, Luminant’s Ned Bonskowski reminded members that ECRS was originally intended to be deployed with real-time co-optimization, which is still two years away.

“It’s a tough problem where we’re trying to bridge two worlds,” he said. “We’ve got a lot of folks that are thinking about the extreme heat and scarcity that we had last summer and reacting to that, whereas I think the joint commenters looked at this and said, ‘Well, while we may not agree that the way ECRS is currently operated is the problem, we recognize that there is a concern, and so as a step towards compromise, let’s try to align whatever it is in NPRR2024.’”

Bonskowski shared data that he said indicated releasing 500 MW of ECRS has a value “well above” the level recommended by the Monitor. He said the Protocol Revision Subcommittee’s (PRS) $1,000/MWh proposal falls “somewhere reasonably” in the middle.

ERCOT’s Jeff Billo, director of operations planning, said the grid operator agrees with the concept of a floor and that it needs to be done correctly “regardless of the quantity.”

“Then we can continue to work on what is the right methodology for determining the quantity,” he said. “We’re coming at this with different viewpoints on the offer floor.”

TAC’s first attempt to endorse NPRR1224, as amended by the Monitor’s comments, fell flat at 10-18 with two abstentions. Its only support came from the consumer and retail segments.

A second motion to endorse the change with the offer floor set at $500/MWh met the same fate by an identical vote. The retail segment was joined by the municipal segment.

A third attempt at passage, this time as originally proposed by the PRS, also failed, at 15-11, with four abstentions. It was opposed by the consumer and retail segments.

Finally, on its fourth attempt, TAC endorsed the measure. It must still be approved by the board and Texas Public Utility Commission, but it has been assigned urgent status so it can be effective this summer.

TAC Endorses $1.2B Project

TAC endorsed the ERCOT Regional Planning Group’s recommended $1.2 billion project to rebuild 345-kV infrastructure in West Texas that will address thermal overloads and petroleum production load-growth issues in the region.

The project easily cleared the $100 million threshold to be classified as a Tier 1 project, necessitating board approval.

Assuming the rebuild is approved, Oncor, the transmission provider, will disconnect existing 345- and 138-kV transmission lines before rebuilding about 245 miles of new transmission lines and switches. It will also build a new substation and upgrade terminal equipment.

The project was first identified in the grid operator’s 2021 Permian Basin Load Interconnection Study. Staff conducted a subsynchronous resonance (SSR) screening for the rebuild. They found no adverse SSR effects to the existing and planned generation resources and also determined the project did not cause new congestion within the area.

The utility plans to complete the work by summer 2028.

Plaque Honors Brad Jones

ERCOT has installed a plaque across from the board room memorializing former interim CEO Brad Jones, who died last year.

Jones took over the grid operator’s reins in the wake of the disastrous and deadly February 2021 winter storm. He worked to raise public confidence in ERCOT and steady the ship before handing the helm to current CEO Pablo Vegas. (See Brad Jones, Former ERCOT, NYISO CEO, Dies at 60.)

The plaque includes a quote from Teddy Roosevelt, Jones’ favorite president. It reads: “‘Far and away the best prize that life has to offer is the chance to work hard at work worth doing.’ I know the work we do here at ERCOT is, indeed, the best prize.”

Staff have also planted a tree in his memory outside ERCOT’s operations center in nearby Taylor.

Theme of the Month

The meeting got off to a rocky start when ENGIE’s Helton attempted to submit a friendly amendment to the phrase of the month brought forward by American Electric Power’s Richard Ross.

Ross, who provides a monthly theme for both ERCOT and SPP stakeholder meetings, called in to say May’s was “words matter.”

“It’s been used quite well this week at SPP meetings,” Ross said. “I’m quite confident you guys can pull it off.”

He resisted Helton’s suggestion to add “innovation” as a nod to the ERCOT Innovation Summit the day before.

“I hate to be difficult, but it’s my phrase of the month,” Ross said as members erupted in laughter.

2 Combo Ballots Pass

TAC members approved a separate combined ballot containing NPRR1198 and related changes to the Planning Guide (PGRR113) and Nodal Operating Guide (NOGRR258) that adds an extended action plan as a constraint-management plan suitable to managing congestion resolvable by SCED.

Calpine, CenterPoint Energy, Jupiter Power and South Texas Electric Cooperative abstained from the unanimous vote, with Calpine’s Bryan Sams saying his company prefers SCED solutions.

EDF Renewables’ Alexandra Miller, the NPRR’s sponsor, said her group included all input and requests to ensure transparency was consistent throughout the changes.

“This is not something that is done outside of SCED, and it is a change to the system configuration. … Scalability is allowing transmission owners to operate and choose what to respond with,” she said.

TAC unanimously endorsed its combo ballot and the withdrawal of a Planning Guide revision request (PGRR105) that would have added DC ties to the list of resources that must meet minimum deliverability conditions. ERCOT staff said the PGRR was contrary to a recent PUC decision and that it raises a policy issue that is best suited for the commission.

The ballot also included the Real-time Co-optimization Battery Task Force’s recommended mitigated offer cap for all hydro resources and five NPRRs that, if approved by the ERCOT board, would:

NPRR1218: update the state’s renewable energy credit trading program to clarify that it only applies to solar renewable energy.

NPRR1220: modify the market’s restart process to require board and TAC approval and provide an alternative mechanism to board approval under certain circumstances.

FERC on May 23 upheld the contract termination payment (CTP) rules for Tri-State Generation and Transmission Association it approved last year, though it modified some of its original order in response to requests for clarification (ER21-2818-002, et al.).

Tri-State is a wholesale generation and transmission cooperative that serves members in Colorado, Nebraska, New Mexico and Wyoming with long-term, full-requirement wholesale electric service contracts.

FERC’s preferred balanced approach was initially proposed by one of Tri-State’s members. The co-op argued for its preferred accounting methods on rehearing, but FERC declined to overhaul its December order.

“We continue to find that the adopted BSA is consistent with principles of cost causation and with the purpose of an exit fee,” FERC said. “The presiding judge correctly explained that the BSA appropriately aligns costs and benefits to Tri-State members by declining to assign generation-related debt to Tri-State’s members located in the Eastern Interconnection, whose loads are supplied entirely through power purchase agreements.”

FERC also continued to find the BSA’s treatment of PPAs is just and reasonable because it requires that members pay their pro rata share of those that are actually used to serve load.

Tri-State argued that assigning the costs of dozens of PPAs to departing members would be unworkable, which did not persuade FERC. The commission said the co-op does not need to provide members with their exact share of PPA costs before they make a final decision on departure.

FERC granted requests for clarification from Tri-State and Mountain Parks Electric on the amortization term for the transmission credit. It should be amortized over the remaining term for the depreciation rates in effect for the assets to which the debt payment relates, the commission said.

It also clarified that the amortization term for the credit is determined based on the average remaining life of depreciable transmission plant base as determined by Tri-State’s most recent Form No. 1 filing at the time a member withdraws.

The commission sustained the overall transmission crediting approach, finding the prepayment and back-crediting of transmission-related debt in the adopted BSA strikes a reasonable balance between ensuring the debt-related costs of Tri-State’s transmission assets are recovered through the CTP and ensuring the withdrawing member reaps the full benefit of these costs while minimizing cost shifts.

“The payment of transmission-related debt as part of the CTP is intended to compensate Tri-State for the transmission-related debt it incurred to serve withdrawing members,” FERC said. “To prevent shifting costs onto remaining members, the withdrawing member must compensate Tri-State for this debt whether it uses Tri-State’s system or not.”

VAIL, Colo. — “Uncertainty” was a recurring theme at the annual meeting of the Western Conference of Public Service Commissioners on May 19-22, where participants grappled with how to account for the growing number of unknowns in resource adequacy modeling in a future with less predictable weather patterns and unprecedented load growth.

Some speakers at the meeting said the issue requires the electricity sector to fundamentally change its approach to load forecasting.

“There’s a lot of climate and economic uncertainties,” Siva Gunda, vice chair at the California Energy Commission, said during a panel May 20. “Do we really understand the climate data, and are we incorporating it into the forecast? Most of our work has been historically given — historic insights, historic weather patterns; obviously that’s not true anymore.”

The theme of uncertainty dominated conversations about RA, as industry experts shared both a fear of how changing conditions will affect the grid and an inspiration to address the unknown.

“The operational conditions on the system have become a challenge, and the need to harness the collective integration, diversity and power of the grid has never been more true,” said Sarah Edmonds, CEO of Western Power Pool. “Several years ago, utilities … observed that we are, for lots of reasons, headed toward a real reliability pinch in the West.”

Load growth was essentially flat for over a decade compared with today’s “astronomical” load growth projections stemming from new data centers, widespread electrification, and other trends in technology, policy and economics, said FERC Commissioner Mark Christie.

These “macro drivers” should be considered in modeling and forecasting, rather than relying solely on historical data, according to Jeremy Hargreaves, principal at Evolved Energy Research. Other macro drivers include state emissions targets, decarbonization and electrification policies, artificial intelligence sector growth, and crypto markets.

“The question is how to proactively plan in the face of uncertainty. We want to be finding these no-regrets actions that we can take that are informed by these macro drivers, recognizing there’s a lot of uncertainty in how these will play out,” Hargreaves said. “We need more complex modeling approaches to try and estimate what kind of impacts they’ll have.”

Gunda emphasized the importance of adequate forecasting to address uncertainty and maintain reliability.

“Forecasting has a direct implication on affordability; it has a direct implication on reliability; it has direct implications on economic and industrial processes. And so, what we’re doing right or wrong will directly affect the entire system,” Gunda said.

Forecasting should evolve to keep up with changing conditions and uncertainty, and Hargreaves and other industry analysts suggested supporting the grid with bottom-up forecasting and end-use forecasting, which looks at individual customer load geographically.

“My argument is that our historical approach to planning is not going to do,” said Ry Horsey, researcher and software engineer at National Renewable Energy Laboratory. “Forecasts should inform planning and decision-making.”

Evolved Energy Research has looked at a variety of different sectors and developed a load-growth taxonomy that reflects different loads and how they impact people over time, and Hargreaves suggested more widespread implementation of this model in forecasting.

Robert Kenney, president of Xcel Energy’s Colorado division, summed up both the fear of uncertainty and the actions being taken to address it.

“I don’t think there’s any disagreement that we’re retiring resources more quickly … we have load showing up in ways that we haven’t seen in 20 years,” Kenney said. “We should be freaked out, but only to the extent that it drives creativity and action.”

CARROLL, N.H. — Angst over looming load growth, cost increases and reliability headaches headlined the 76th annual New England Conference of Public Utilities Commissioners (NECPUC) Symposium, held May 20-21 at the Mount Washington Hotel.

“I think it is a laudable goal to want to get rid of any greenhouse gas-emitting source, but we’re going to have to do this at pace,” said Charles Dickerson, CEO of the Northeast Power Coordinating Council. He said that as policymakers push for “100% reliable, 100% renewable and 100% really cheap [power], I just don’t think those three [aspects] can exist in one space at one time.”

Dickerson called on regulators to work to encourage innovation and be “a little less rigid” around cost recovery for utilities experimenting with new solutions.

“If we take the same approach to regulation that we’ve taken over the past 100 years, it’s probably going to take us 100 years to solve this,” Dickerson said, adding that regulators should try to approach the looming challenges with “a little bit more risk tolerance and a lot more creativity.”

Vineyard Offshore CEO Alicia Barton pushed back with a more optimistic tone.

“Respectfully, I do disagree — actually pretty strongly — that we can’t do all three,” said Barton, former CEO of the New York State Energy Research and Development Authority. She emphasized that changes to the power purchase agreement model, including tweaks to contract lengths and inflation-adjustment mechanisms, could help bring costs down.

“You can actually get better costs if you leverage some of these choices,” Barton said.

Richard Levitan of Levitan & Associates recommended that public utility commissions “embrace principles of transparency, honesty and realism” when weighing competing priorities.

“I don’t think in the pursuit of clean, reliable and affordable [that] there are easy tradeoffs,” Levitan said. “There is no one unassailable answer; there’s no quick solution; but constructive debate with prominent stakeholders — possibly through the ISO, but at the state level too — should inspire awareness, and I think that’s a laudable goal.”

One way to limit costs would be to maximize the potential of high-performance conductors and grid-enhancing technologies (GETs) like dynamic line ratings, advanced-power flow control and topology optimization, said Rob Gramlich, president of Grid Strategies.

Gramlich noted that the deployment of GETs in the U.S. has lagged behind other countries.

“You just have to wonder whether the cost-of-service regulatory model — which rewards large capital investments — is a disincentive for getting senior management at utilities to really deploy these things,” Gramlich said. “I think we’re at the place nationally with GETs where there’s a need for some independent expert who has access to all the information to identify where the right technology could apply.”

Tiffany Menhorn, principal at the Menhorn Group, said GETs often can provide ancillary grid resilience benefits and give utilities “eyes on your line like never … before.”

Along with better real-time awareness, predictive analytics could provide significant insights into asset health and help to identify anomalies, Menhorn added.

Speakers also highlighted retail demand response as an area for improvement that could significantly reduce the overall costs associated with the clean energy transition.

ISO-NE CEO Gordon van Welie said activating DR at the retail level remains “a work in progress.”

In February, NECPUC launched a yearlong working group to look at how retail DR can help address peak load and resource adequacy challenges.

“What I hope for is a standardized approach to doing demand response in the region,” van Welie said, adding that deploying automation, sending the right price signals and incorporating retail DR into the wholesale markets will be essential. As winter risks increase, longer-duration DR that can extend over multiday periods will become increasingly valuable. “That’s a much more complicated type of demand response, and I think it’s an opportunity for us to innovate as a region.”

The Role of Natural Gas

Several of the speakers presented significantly different visions for the role natural gas and gas pipelines will play in the coming decades.

“I hope that states don’t get away from … everything that we’re doing to ensure the safety and reliability of that infrastructure,” said Georgia Public Service Commissioner Tricia Pridemore, who is also first vice president of the National Association of Regulatory Utility Commissioners.

“I’m a pro-gas commissioner,” Pridemore said. She noted a report by the National Petroleum Council that found that “the pipeline infrastructure is going to be with us for a long time,” arguing that alternative fuels like hydrogen and renewable natural gas (RNG) will rely on the gas system as states decarbonize.

Marc Brown of the Consumer Energy Alliance, an advocacy group whose members include a wide range of industrial end users and fossil fuel companies, called natural gas “part of the solution” and argued that the most significant decarbonization gains over the past two decades have come from the proliferation of natural gas.

He said environmental progress and decarbonization “is going to take people accepting the fact that natural gas is going to continue to play an important role in affordability, reliability and emissions reductions in the near- and midterm future.”

In contrast, Emily Green, senior attorney at the Conservation Law Foundation, said states should engage in long-term planning efforts to transition off fossil fuels, including natural gas. She highlighted the significant warming effects of methane leaks from the gas system, which are typically underestimated by state and national greenhouse gas inventories.

“We’re going to be paying for today’s investments in gas for decades to come, both in terms of emissions and ratepayer impacts,” Green said. “It’s low-income consumers that are going to be left holding the bag.”

Green also called on regulators “to be very wary of utilities looking to maintain or even upgrade pipelines on the future promise of biomethane or hydrogen.”

In the Massachusetts Department of Public Utilities’ final rule on its multiyear “Future of Gas” investigation, it found that efforts to blend hydrogen and RNG into the gas network should not be funded through the general rate base (20-80-B).

“The department is uncertain about the viability of hybrid heating and hydrogen technologies and their potential as economical long-term solutions for ratepayers,” the DPU wrote, adding that “RNG and the use of hydrogen as a fuel are emerging technologies that have not yet been proven to lead to a net reduction in GHG emissions.”

FERC has denied a rehearing request and partly adopted a clarification request by Constellation Energy related to a challenge to the fixed costs associated with the Mystic cost-of-service agreement (COSA) (ER18-1639-028).

Initially signed in 2018, Mystic’s COSA between Constellation and ISO-NE delayed the retirement of the Mystic Generating Station by two years to help provide fuel security to the region. The agreement is set to expire — and Mystic to retire — at the end of May.

As part of the COSA, Constellation is required to submit annual informational filings related to the costs of the agreement. Relevant stakeholders are allowed to request more information and ultimately challenge the filings with FERC.

The May 23 FERC ruling stems from an October 2022 series of challenges by a group of municipal utilities to an informational filing submitted that year.

In December 2023, FERC granted several of the municipal utilities’ challenges, determining “that the challenges raised issues of material fact that could not be resolved on the record before the commission, and thus established hearing and settlement judge procedures.”

In January 2024, Constellation requested rehearing on three of the order’s rulings and clarification on two rulings — while also requesting rehearing on the latter two rulings if not granted the clarifications.

“The relief sought herein is aimed at avoiding unnecessary litigation in a case that has seen too much already,” the company wrote.

In its ruling May 23, FERC dismissed the rehearing requests on the basis that the challenge order was not a final decision and therefore not subject to rehearing.

FERC did grant Constellation’s clarification request regarding projected 2023 capital expenditures at the Everett LNG import facility, which also is owned by Constellation and provides the fuel for Mystic via a fuel supply agreement.

A 2022 settlement agreement among Constellation, the New England states and ISO-NE “resulted in the Mystic Agreement no longer providing recovery for any Everett 2023 [reliability-must-run capital expenditures],” FERC wrote.

“Accordingly, we grant Mystic’s requested clarification and determine that there is nothing further to litigate” regarding this aspect of the informational filing, FERC ruled.

Meanwhile, FERC affirmed its 2023 ruling to “set for hearing and settlement judge procedures” the three other formal challenges to the informational filings, which relate to the calculations of Mystic and Everett’s rate bases prior to the agreement.

PJM on May 20 announced that it had completed the first phase of studies for 306 generation interconnection requests sorted into the first cycle in the transition to its new interconnection process, a cluster-based study approach intended to reduce how long it takes the RTO to bring generators online.

“This is another critical milestone for PJM’s widely supported interconnection process reform,” said Aftab Khan, executive vice president of operations, planning and security. “New service requests for generation resources are moving through our process as designed and promised, with more than 200,000 MW of projects to be studied over the next two years to help states advance their energy policy goals.”

Developers with projects in Transition Cycle 1 (TC1) will have 30 days to review the system impact studies and decide whether to move forward with their projects to the facility study phase. PJM said those that complete the process will be ready for construction by mid-2025. (See PJM Initiates Transitional Interconnection Queue.)

Another 306 projects expected to require minimal network upgrades are being studied through an Expedited Process “fast lane” that is expected to yield final interconnection service agreements (ISAs) throughout this year. PJM also plans to initiate Transition Cycle 2 on June 20, with a likely application deadline by Dec. 16.

PJM said about 72 GW are expected to clear the queue by mid-2025 and 230 GW over the next three years, more than 90% of which is renewable energy or storage.

The cluster-based approach groups projects together on a first-ready, first-served approach to identify any grid upgrades and assign costs. It also includes increasingly large readiness deposits to be made throughout the study process, with the aim of discouraging speculative or uncertain projects from taking focus away from others. PJM said 118 projects have dropped out of the queue or failed to post deposits, out of 734 eligible. (See FERC Approves PJM Plan to Speed Interconnection Queue.)

Environmental organizations said the milestone is a welcome first step but that more change is needed.

“PJM worries there’s not enough new power coming online, but it’s still only approving projects proposed four to six years ago,” said Tom Rutigliano, of the Natural Resources Defense Council. “This is a step forward, but PJM’s current process is not enough to get these new clean energy projects connected to the grid as quickly as they’re needed.”

Christine Powell, deputy managing attorney at Earthjustice, said the amount of time it has taken for PJM to get to this stage has already resulted in projects stalling or withdrawing from the queue. “While PJM’s shift to a cluster study process is a positive development for the hundreds of clean energy projects waiting to interconnect to the power grid, PJM continues to lag behind other RTOs,” she said.

Katie Siegner of RMI pointed to a study released in February that found that incorporating grid-enhancing technologies (GETs) into how PJM conducts transmission planning could optimize the use of existing infrastructure to reduce upgrades needed for new projects and speed interconnection studies. The study estimated that about $1 billion in annual production costs could be avoided through 2033 by expanding use of GETs. (See RMI Report: GETs Could Speed Renewable Development, Save Consumers Billions.)

PJM’s “clearest opportunity for improvement is bringing its interconnection process into compliance with Order 2023, particularly through serious consideration of alternative transmission technologies that could provide faster and cheaper network upgrade alternatives,” Siegner said. “The fact that no grid-enhancing technologies have been identified or used as network upgrades to date suggests PJM has more work to do in incorporating these fast, flexible transmission tools into its study methodologies.”

PJM spokesperson Jeff Shields told RTO Insider the RTO allows and welcomes GETs as components of proposals for its Regional Transmission Expansion Plan and laid out how it will fully comply with Order 2023’s requirements around their facilitation in its May 16 compliance filing (ER24-2045).

“All of the enumerated [GETs] already are considered and studied as necessary, if merit exists in the use of such technologies, in the course of interconnection studies in the PJM region,” Shields said. “This incorporation of new and emerging technology is consistent with the objectives of the final rule, which requires transmission providers to evaluate certain GETs in each and every one of its interconnection studies.”

Shields said PJM agrees there is more progress to be made in improving generator interconnection and development, both at the RTO and removing external obstacles. “We are working with stakeholders within the PJM stakeholder process, as well as entities outside of the PJM membership, to accomplish this.”

Responding to a rehearing request by Advanced Energy United over FERC’s partial acceptance of ISO-NE’s third Order 2222 compliance filing, FERC has directed ISO-NE to submit an additional filing to specify its metering and telemetry practices for distributed energy resource aggregations (DERAs) (ER22-983-006).

Order 2222, which requires RTOs to update their tariffs to enable DERAs to participate in wholesale markets, has led to a long series of compliance filings and rehearing requests related to ISO-NE’s compliance.

On May 23, FERC issued an order on rehearing responding to Advanced Energy United’s challenge of ISO-NE’s third compliance filing, which FERC accepted Nov. 2, 2023. (See FERC Accepts ISO-NE Order 2222 Compliance Filing.)

“We sustain three of the four findings AEU [Advanced Energy United] challenges,” FERC ruled.

Responding to the trade association’s argument that ISO-NE’s three metering options for DERAs — “retail delivery point metering, submetering with reconstitution and parallel metering” — are unnecessarily prohibitive, FERC affirmed its finding that these options “do not pose an unnecessary or undue barrier to individual DERs joining an aggregation.”

FERC upheld its acceptance of ISO-NE’s proposal to apply the requirements of the “binary storage facility” and “continuous storage facility” participation models for DERAs to provide withdrawal service. FERC also continued to find that the ISO-NE properly explained the steps it took to “avoid imposing unnecessarily burdensome costs on DER aggregators and individual resources in DERAs.”

However, FERC set aside its prior ruling that ISO-NE adequately described its metering requirements for DERAs.

“Specifically, we set aside our finding that, for those DERAs containing behind-the-meter DERs, ISO-NE’s tariff includes a basic description of the metering practices for DERAs with references to specific documents that contain further technical details for metering and telemetry practices,” FERC wrote.

“ISO-NE’s basic description of its metering practices for DERAs is incomplete because its tariff does not include submetering requirements for DERAs participating as submetered Alternative Technology Regulation Resources,” FERC added.

FERC directed ISO-NE to submit an additional compliance filing to specify these submetering requirements. FERC also set aside its ruling that ISO-NE’s proposal to extend “existing requirements for Alternative Technology Regulation Resources to DERAs” is just and reasonable, writing that it will reassess these requirements after the RTO submits its additional compliance filing.

Caitlin Marquis of Advanced Energy United said FERC’s directive “sends ISO back to the table to resolve one metering barrier for DERs seeking to provide regulation service, which is welcome and important.”

“However, as New England and the rest of the country face rising demand, rising electricity prices and reliability threats, much work remains to ensure the region is taking full advantage of DERs,” Marquis added.

Commissioner Mark Christie concurred with the parts of the order that accepted ISO-NE’s filing and dissented “to the rest.”

Christie decried Order 2222’s “seemingly never-ending and avoidable rounds of compliance filings” and called the compliance saga a waste of time and money.