FERC has established settlement judge procedures to consider the validity of rate schedules filed by Talen Energy to continue operating its Brandon Shores and H.A. Wagner generators past their retirement date (ER24-1787, ER24-1790). (See PJM Requests 2nd Talen Generator Delay Retirement.)

The commission’s June 17 order states that the proposed rate schedules may not be just and reasonable because of the calculation of the filings’ valuations of the two generators. It also took issue with adjusting fixed operating and maintenance expenses for inflation using an escalation index, along with the proposed monthly project investment tracker payment and performance requirements.

“While we are setting these matters for a trial-type evidentiary hearing, we encourage the parties to make every effort to reach settlement before hearing procedures commence,” the order states.

The filings requested annual fixed costs of around $175 million to keep Brandon Shores’ 1,273-MW coal-fired generator online from June 1, 2025, through Dec. 31, 2028, as well as variable costs such as fuel and $29.9 million in project investments. The Wagner filing requests $40.3 million annually to keep two of Wagner’s oil-fired units, amounting to 702 MW, online for the same period and $4.5 million in additional investments.

The reliability-must-run (RMR) agreement is intended to keep the generators online to avoid reliability violations identified throughout the Baltimore region while transmission reinforcements are constructed that would allow the units to deactivate without issue. (See FERC Approves Cost Allocation for $5 Billion in PJM Transmission Expansion.)

The proposed rates were opposed by the Independent Market Monitor and the Maryland Public Service Commission, who argued the rate schedules would improperly include sunk costs incurred prior to the start of the RMR term and unrelated to the going-forward costs of keeping the facilities operational.

The Monitor argued that including sunk costs that have already been reported as impaired assets would ask ratepayers to make investors whole for past losses.

The June 17 order accepted the rate schedules, suspended them and initiated the settlement judge procedures with the possibility of evidentiary hearings if that avenue does not yield a consensus.

Maryland Deputy People’s Counsel William Fields said sunk costs make up a significant portion of the proposed rates and the Office of People’s Counsel is preparing an analysis on how the RMR could affect state ratepayers. He said the office is pleased with the commission’s decision to open settlement judge procedures and plans to fully participate.

“We don’t view those as costs that are related to going forward with operations of the plant.”

Fields said he believes PJM’s backlogged generation interconnection process leaves few alternatives to expensive RMR contracts to keep retiring resources online while major grid reinforcements are constructed.

“We’ve got a few concerns with that approach or reliance on the market response here, and one is that this happens very quickly. You’re talking months, and that is very, very quick for any kind of significant market response to a significant, pretty big retirement. Trying to respond to that with a lot of megawatts is going to be difficult in any circumstance, and right now, the PJM queue process is working through its backlog, and that makes it even more difficult for some kind of new resource to get through and get online on a time frame that’s going to help the situation at all,” he said.

Protesters also disputed the filings’ methodology for determining the value of Brandon Shores and Wagner, depreciation and the amount of risk the company faces in continuing to operate the generators.

Monitor Joe Bowring said opportunity costs similar to those Talen is seeking to include in the rates have been rejected by the commission in past RMR filings.

The Brandon Shores filing also notes it’s subject to a settlement agreement with the Sierra Club requiring that coal combustion at the site cease by the end of 2025. It states that it will seek changes to those terms to allow the generator to keep operating for the RMR term.

Casey Roberts of the Sierra Club said the organization is willing to engage with Talen on the agreement, but “additional protections for the local community and consumers, and longer-term reforms to avoid similar predicaments in the future, must all be on the table.”

The club’s protest of the rate schedule also urged the commission to not approve an RMR agreement that would pay for Brandon Shores to remain online until the agreement has been modified to allow the generator to operate.

“Thus, it appears on the face of the CORS [continuing operations rate schedules] that Talen intends not to operate Brandon Shores under the CORS unless its settlement agreement with Sierra Club is modified, notwithstanding the hundreds of millions of dollars in fixed monthly payments that Talen would receive even if it never generates a single megawatt hour. FERC cannot approve such an arrangement, particularly on the expedited basis that Talen seeks in this proceeding,” the Sierra Club wrote.

Both the Sierra Club and Maryland Public Service Commission argued that the proposed rates lack performance requirements and would require load to pay significant sums to keep the two generators operational with no guarantee they would respond if dispatched by PJM.

Maryland PSC spokesperson Tori Leonard said the commission supports FERC’s directive opening the settlement judge proceedings.

“FERC’s preliminary analysis confirmed that both the Brandon Shores rate schedule and Wagner rate schedule have not been shown to be just and reasonable and may be unjust, unreasonable, unduly discriminatory or preferential, or otherwise unlawful,” Leonard wrote in an email. “This commission is pleased that FERC granted our request (as well as the request of the Maryland Office of People’s Counsel), to set the matter for settlement judge procedures. The commission will continue to advocate for a reasonable resolution of the Brandon Shores and Wagner RMR filings that will minimize impacts to ratepayers, while preserving the reliability of the bulk electric power system to serve Maryland’s needs.”

The economic forecasts for both New York state and the U.S. are reasonably healthy, stakeholders learned at NYISO’s annual Spring Economic Conference on June 17.

“The track that we’re on is pretty sustainable,” said Adam Kamins, senior director of Moody’s Analytics. “It doesn’t look like there’s any sort of recession imminent.”

Nationally, 200,000 to 250,000 new jobs were created every month in the fourth quarter of 2023 and first quarter of 2024. This was ahead of expectations and “far stronger than expected,” Kamins said.

Kamins anticipates that while new jobs should level off nationally to closer to 100,000 per month, this is unlikely to cause additional inflation. Kamins attributed this to immigration, both documented and undocumented. New families are taking otherwise-unfilled jobs and growing the population.

“We’ve had a surge of immigrants come in and fill all of these jobs and continue to contribute to 250,000 jobs per month,” Kamins said. “But it’s not created this sort of inflationary pressure that we thought it would have if we took the census numbers at face value.”

Later in the presentation, Kamins showed that New York state was among the top destinations for new immigrants, highlighting data from immigration court filings. Many were coming to New York City, but growth could also be seen in other metro areas of Albany, Rochester and Buffalo.

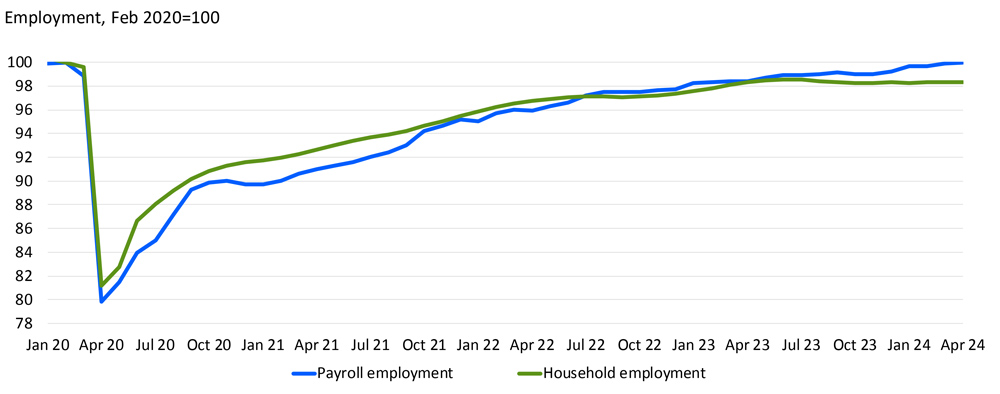

Job growth in New York recovered slowly from the shock it endured during the pandemic, but it has recovered, Kamins said. He pointed to New York City as the primary driver.

This graph shows the recovery of jobs for both the Bureau of Labor Statistics Payroll (blue) and Household (green) surveys of job creation for New York State. While there is a discrepancy between the two rates of growth, they show New York approaching pre-pandemic employment levels. | Moody’s Analytics

“It’s not being driven by the traditional kinds of jobs of the New York City economy. This is not runaway growth in Wall Street jobs,” Kamins said. He explained that this was mostly consumer-facing jobs, driven by tourism and health care services.

The rest of the state has not recovered nearly as well, but Kamins said the outlook was pretty good for markets like Syracuse, Buffalo and Albany.

“Syracuse is clearly outgrowing the U.S. and is actually the second fastest-growing metro area in the region,” Kamins said.

He went on to highlight a “chip corridor” through the Capital Region and Central New York that extends into part of the Southern Tier and the Rochester area. This area is benefiting from the Biden administration’s increased investment in computer chip production as new facilities come online.

“The bigger picture in New York is that, with all of the investment in chip production that’s happened, Upstate New York is really becoming, if not the chip production capital of the U.S., [then] one of two or three [important] areas. … There’s a huge opportunity here.”

This “regional cluster” of chip production and similar high-tech industries could lead to substantial, sustainable growth, unlike the beleaguered Tesla electric vehicle facility in Buffalo, Kamins said.

At the same time, inflation seems to have slowed down such that it is back to the Federal Reserve’s target of 2% per year. Rent growth has slowed nationally, and wage growth is catching back up to price growth. Kamins said Moody’s anticipates the Federal Reserve will cut interest rates this year.

‘Scars Remain’

Kamins cautioned that despite the stronger-than-anticipated economic picture, there were very real problems faced by consumers that have led to decreased confidence in the economy.

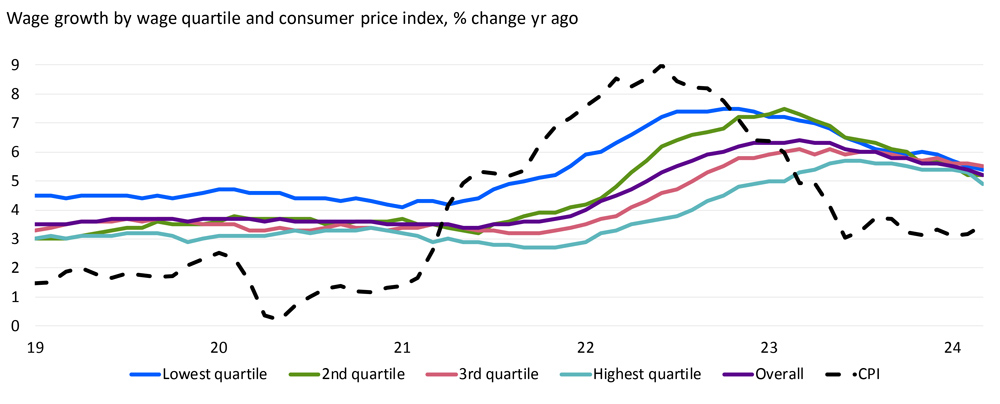

The past few years of inflation have outpaced wage growth, leading to an overall decrease in real wages.

“All these income quartiles, including the lowest earners, saw wage growth not keep up with inflation, meaning they’re experiencing real wage declines,” Kamins said. “That doesn’t feel good for people, and the pain is very broad.”

Wage growth moves back ahead of inflation, but scars remain | Moody’s Analytics

Kamins said this was particularly felt in lower wage earners who were already struggling to make ends meet prior to the increase in inflation. While the recovery in wage growth has begun, it hasn’t made it to where it needs to be.

“We will need another year or so of wage growth exceeding growth in inflation, which we think will happen,” Kamins said.

Another major constraint on the economy is housing. Kamins said that nationwide, including New York, lack of supply is driving increased home prices. He said that while the rate of house price growth was slowing, it wasn’t at all close to declining. Builders just aren’t building enough housing to meaningfully curtail prices. This is particularly pronounced in Buffalo.

High housing costs are partly responsible for New Yorkers migrating outward. While that has slowed in recent years, it’s still persistent. Both young professionals and retirees are leaving the state for the Carolinas, Tennessee, Florida, Connecticut and New Jersey.

Novel Emission Considerations

The conference also featured two presentations about optimizing for carbon emissions impact on both the generation and consumption sides.

Lee Taylor, CEO of clean energy advisory firm REsurety, explained the problem of local marginal emissions, the emissions rate of a particular node of the electrical grid. This is the carbon-accounting version of LMP. As load and generation change hour by hour, the ratio of renewables to fossil fuels can change depending on weather, load demand and transmission bottlenecks.

“You have a highly impactful carbon footprint of the projects that are close to the city,” Taylor said. “As you move up into the area toward the Canadian border, you get farther from the load, [and] the impact of the generation profile gets lower and lower in terms of its carbon offset.”

This means that if a renewable energy project is sited far away from the point of delivery, it has less ability to reduce emissions near that point. Taylor noted wind projects close to Canada run often but are often either curtailed or end up competing with other renewables because the power they produce can’t get to where the load is.

Taylor said the renewable energy industry was starting to take this into account when determining where to build, optimizing for cheap emission reductions rather than simply building where it is cheapest.

“A project that is 50% more expensive to build but 70% more carbon-abative is actually cheaper when your goal is to spend the least amount of money to impact the highest amount of carbon, which is, ultimately, the goal of most voluntary carbon actors,” Taylor said.

In addition to siting renewable projects in places where they would have the most emissions impact, large load customers are increasingly taking this into account when considering where to build their facilities.

“Businesses are cost optimizing,” Taylor said. “They’re looking for where does that go the furthest in dollar per ton of carbon.”

On the demand side of things, Gavin McCormick, executive director of nonprofit research group WattTime, said many companies were moving to smart load shifting to offset their emissions.

“We’ve just hit, as of today, 700 million devices worldwide that are optimizing every five minutes their consumption of electricity to reduce emissions,” McCormick said. “All signs point towards sort of roughly a doubling per year for the next four or five years.”

McCormick said this meant that about 20% of smart devices were committed, via software, to implementing this emissions-reduction strategy worldwide. While most of these devices are currently smart phones, McCormick listed several EV manufacturers, including Toyota, Honda and General Motors, as committing to this strategy.

McCormick said the impact of this load shifting on emissions wasn’t clear yet. He said his organization had joined several universities, tech companies and grid operators to attempt to empirically research the impact of this kind of mass, distributed load shifting on emissions.

“We would be very interested in speaking with ISOs about whether we are measuring emissions correctly [and whether] the effects of this [is] what we believe them to be,” McCormick said. “There’s so much corporate interest in shifting load to the cleanest time that I think it should be recognized.”

Contentious NPRR Revising ECRS Passes over Monitor’s Objections

ERCOT’s Board of Directors took up two contentious protocol changes during its June 18 meeting that have divided staff and stakeholders, tabling one it had previously remanded and approving the other over objections from consumer interests and the Independent Market Monitor.

Potomac Economics President David Patton made his second appearance in less than six months before board members to press his case against the grid operator’s heavy use of ERCOT contingency reserve service (ECRS).

Patton, whose firm holds ERCOT’s IMM contract, said he was “very disappointed” with the board’s approval of the protocol change (NPRR1224). The rule change sets a price floor of $750/MWh for the product, which procures capacity resources that can be brought online within 10 minutes and sustained at a specified level for two consecutive hours.

“This is the first time I’ve seen [a grid operator] advocate for such a proposal that is designed to undermine the competitive performance of its market — reducing reliability to artificially inflate its real-time prices,” Patton told RTO Insider.

The Monitor last year said the ECRS product, ERCOT’s first new ancillary service in 20 years, created artificial supply shortages that produced “massive” inefficient market costs totaling about $12 billion during the year. The service was first deployed in June. (See ERCOT Board of Directors Briefs: Dec. 19, 2023.)

“I think this is one of the most important votes to approve something that you’ll ever take,” Patton told the board’s Reliability and Markets Committee on June 17. “The key objectives of any competitive, deregulated wholesale markets is that they produce efficient and competitive outcomes that maintain the reliability. NPR1224 violates all three of those objectives.”

In his presentation to the committee, Patton said NPRR1224 will effectively have ERCOT administer a withholding framework where key economic units are physically withheld from the real-time market until they are deployed. He said it economically withholds the resources after deployment by attaching the $750 offer floor, “for which there is no competitive basis.”

Because ERCOT doesn’t yet co-optimize energy and ancillary services in real time (that is scheduled to come online in 2026), ECRS is quarantined from the real-time market. The Monitor projects that if conditions this year are similar to 2023’s, the NPRR will generate “inefficient and anticompetitive” costs exceeding $5.7 billion. Patton recommended staff instead develop procedures that would anticipate a security-constrained economic dispatch (SCED) shortage and then deploy ECRS.

Attorney Katie Coleman, who represents Texas Industrial Energy Consumers, advocated for a $100 price floor but supported 1224 as an interim step before real-time co-optimization (RTC) is added to the market.

“We are concerned that with the $750 price floor, we are not making much progress relative to last summer’s experience,” she said. “We do support a stopgap between now and real-time co-optimization to insulate the market from those effects, but we believe that the $100 floor is the appropriate level.”

ERCOT staff said they had drafted another protocol change (NPRR1232) as a follow-up to NPRR1224. It would introduce a mechanism to make some ECRS available to SCED every hour, assuming the latter NPRR’s price floor is codified into the protocols. Staff said the price floor represents the opportunity cost of depleting available reserves for use in the real-time market.

Staff said ECRS has been deployed 52 times through May 2024, with 43 of those occasions providing frequency recovery or to cover net load ramps. ERCOT CEO Pablo Vegas used that data point in supporting NPRR1224, which he said is intended to provide some benefits during the summer.

NPPR1224 “represents an improvement over what we saw last year in terms of lowering the price,” Vegas said. “The [Technical Advisory Committee] has worked together to try to find a pathway that addresses some of the cost implications that we saw last summer. It preserves the unique characteristics of ECRS and what we’re able to do under manual deployments today with our control room. It represents the first step in a series of … steps that are going to track us towards RTC.

“I would recommend we move forward with the work that TAC has done and take this first step to see the benefit this summer. We’ll be able to take continued lessons learned into 1232 as we set up the automation of the release of ECRS. We’re going to have to get comfortable as a committee and as a board dealing with issues where there are strong pros and strong cons. We’re not going to be able to necessarily find the middle ground that makes everybody happy on these kinds of issues.”

The R&M Committee, divided over the deliberative stakeholder process and a lack of transparency into the price floor, voted 3-1 to approve NPRR1224. The Office of Public Utility Counsel’s CEO, Courtney Hjaltman, cast the dissenting vote over concerns the price floor is too high. She abstained from the full board’s unanimous vote.

NOGRR245 Bifurcated, Delayed

The board also agreed with staff’s recommendation to table a revision to the Nodal Operating Guide (NOGRR245) that has been bandied back and forth between stakeholders and staff since late last year. The proposed rule change would impose voltage ride-through requirements on inverter-based resources.

Staff said tabling the measure will give them additional time to hammer out an agreement with some stakeholders by bifurcating or decoupling parts of the exemptions and extension process for legacy assets unable to meet ride-through requirements.

“ERCOT believes one more opportunity to work with joint commenters is appropriate to potentially give regulatory certainty,” staff said.

Chad Seely, ERCOT | ERCOT

General Counsel Chad Seely said ERCOT will work to schedule a special board meeting before the regular Aug. 19-20 bimonthly meetings to take up NOGRR245’s exemptions and extension process issues. He said that will allow staff to quickly hand off the measure to the Texas Public Utility Commission for policy discussions. The measure’s reliability assessment process and criteria for hardware upgrades necessary to meet its requirements will go through the normal stakeholder process, with a December target to go before the board.

“This is a critical reliability issue for the grid. It’s time to move this forward and hand this off to the commission as expeditiously as possible,” Seely said, expressing optimism that staff will be able to “effectively bifurcate” the issue.

TAC endorsed the rule change June 7 after several months of trading and reviewing comments with ERCOT, gaining staff’s support in the process. The committee inserted gray-box language with potential modifications that wouldn’t become effective until March 2025. The language was aimed at those entities for which upgrade costs are less than 40% of the full, in-kind replacement cost of a plant’s inverters or turbines and converters. (See ERCOT TAC Endorses Rule for Inverter-based Resources.)

However, the joint commenters — primarily renewable developers — protested the change and threatened to file a complaint at the PUC, saying TAC attempted to defer issues around hardware changes by placing them in the gray-box language. They urged the board to ensure that the ride-through standards “do not have the unintended consequences of harming reliability by eliminating existing generation and harming future investment in infrastructure in the ERCOT market.” (See Renewable Developers Oppose Proposed ERCOT IBR Rule.)

The NOGRR is meant to align the grid operator’s protocols with NERC reliability guidelines and the most relevant parts of the Institute of Electrical and Electronics Engineers’ standard for IBRs interconnecting with the grid. The board in April remanded the NOGRR back to TAC, directing that the language be modified to address ERCOT’s reliability concerns.

ECRS Slows Energy Prices’ Drop

ERCOT IMM Director Jeff McDonald said that while he wasn’t going to focus on ECRS in briefing the board, the ancillary service had a profound effect on the market last year.

“I know it comes up repeatedly in the report … but you will see it is the focus in certain areas in the report because it had a fairly profound effect on energy prices and overall cost,” he said in sharing the Monitor’s annual State of the Market report.

McDonald said the load-weighted average energy prices were down about 13% to roughly $65/MWh in 2023 from the year before, even though natural gas prices declined more than 60% during the same period. The report attributes that difference to the “adverse” effects of ECRS’ implementation, noting that real-time prices drive those in the day-ahead and forward markets.

“Electricity prices will be correlated with natural gas prices in a well-functioning market because fuel costs represent the majority of most suppliers’ marginal production costs, and natural gas units are generally on the margin in ERCOT,” the report says.

ECRS’ effect on real-time prices was largely confined to the hotter months of June through September, McDonald said. “So, it did roughly double the real-time energy price during that period.”

McDonald said the IMM spent a “fair amount” of time looking at the market’s competitiveness, finding it to be competitive with little evidence that suppliers exercised market power. He said that while the market has provided sufficient revenues to signal the need for more generation in four of the past six years, he was unable to explain why it took the subsidization of gas plants’ construction through the Texas Energy Fund to make that more of a reality. (See Vistra Joins Rush for Dispatchable Generation Loans.)

“As a project developer, you need to see a series of revenues in the market that would support your investment before you undertake it,” he theorized. “In the investment world, policy risk is a big factor, especially for large capital … investments. So I’ll be spending more time trying to find a satisfactory answers to your question.”

ERCOT: Another Hot Summer

Dan Woodfin, ERCOT’s vice president of system operations, told the board that staff meteorologists expect this summer to be among the hottest on record, as have the past few summers.

“Probably not as hot as last summer, where we just had lots and lots of hot temperatures,” he said. “We’ve actually had quite a few of the summers within the last few years that have been well above normal, and so we expect this summer to fit in with that. Given what we’ve seen in June, I think that we’re trending that way.”

“We’re seeing a pretty significant little bit higher growth during the summer period than what we’ve seen in some of the other seasons,” CEO Vegas said. “It’s a little bit higher than what we’ve seen across other seasons over that same period, and it’s likely due to the very hot summers recently that we’ve just had. So we’ve seen some very recent high weather that has helped to boost some of the demand growth.”

According to a recent University of California, Berkeley study, the state’s average temperature has risen by about 2.7 degrees Fahrenheit since the dawn of the industrial age. However, the heat index has been as many as 11 degrees higher during that same period.

The past two summers have been the second- and third-hottest on record, and four of the 10 hottest summers have come in the past six years, Vegas said. September 2023 was the hottest September on record and included ERCOT’s first energy emergency since the disastrous February 2021 winter storm.

ERCOT set a new demand market record last August of 85.5 GW during a summer in which it issued 17 weather watches, voluntary conservation notices or conservations appeals. As of June 20, it was projecting more than 80 GW of demand on June 26, marking the first 80-GW day of the season. The June record for peak demand came last year at 80.8 GW.

“We are prepared for this summer,” Vegas said, citing weatherization inspections, “meaningful” growth in generation resources and tabletop exercises.

2nd DR RFP Canceled

Vegas said ERCOT is canceling a request for four-hour demand response after it received three offers with less than 10 MW.

A request for 3,000 MW of six-hour DR last fall was canceled when the grid operator received 11.1 MW of potential eligible capacity.

“It is clear from the two recent experiences with capacity [requests for proposals] … that we need to modify the approach for developing the next set of demand response capabilities in the ERCOT market,” Vegas said, echoing similar comments he made last year. (See ERCOT Cancels RFP for Additional Winter Capacity.)

IMM’s David Patton argue against ECRS’ use. | ERCOT

He added that he is confident there is “significant potential” in both residential and commercial and industrial demand response classes. “We need to take a more in-depth approach working with market participants to develop a demand response product that will be additive to the reliability capabilities at an ERCOT market level,” Vegas said.

ERCOT staff are working with PUC staff on a study Vegas said “shows meaningful potential for incremental demand response.” Texas A&M University is nearing completion of the study in advance of next year’s Texas legislative session, PUC Commissioner Kathleen Jackson said.

“Our stretch goal is that we want to look at the lay of the land and come up with recommendations that hopefully we can bring forth during the next legislative session,” Jackson said.

Board Approves $1.12B Project

The board approved ERCOT’s recommended $1.12 billion project to rebuild 345-kV infrastructure in West Texas that will address thermal overloads and petroleum production load-growth issues in the region. The project was also unanimously endorsed by TAC.

Oncor, the transmission provider, will disconnect existing 345- and 138-kV transmission lines before rebuilding about 245 miles of new line and switches. It will also build a new substation and upgrade terminal equipment. The utility plans to complete the work by summer 2028.

The board’s consent agenda included seven NPPRs, two NOGRRs and three revisions to the Planning Guide (PGRRs):

NPRR1198, NOGRR258 and PGRR113: add an extended action plan as a constraint-management plan suitable to managing congestion resolvable by SCED.

NPRR1212 and PGRR114: clarify a distribution service provider’s obligation to provide an electronic service identifier for a resource site that consumes load other than wholesale storage and is not behind a non-opt-in entity tie meter.

NPRR1218: updates the state’s renewable energy credit trading program to clarify that it only applies to solar renewable energy.

NPRR1220: modifies the market’s restart process to require board and TAC approval and provide an alternative mechanism to board approval under certain circumstances.

NPRR1223: updates a protocol form to require transmission and/or distribution service providers to provide contact information to ERCOT.

NPRR1228: decreases the number of firm fuel supply service obligation periods awarded in a procurement from two to one.

NOGRR255: establishes high-resolution data requirements.

PGRR112: sets requirements for interconnecting entities to submit dynamic data models and for transmission service providers to submit final full interconnection studies for approval at least 30 business days before the quarterly stability assessment deadline.

Sunrise Wind has received final federal approval of its construction and operations plan and expects to begin seabed preparations off the New England coast this year.

The Bureau of Ocean Energy Management announced the decision June 21. BOEM had formally greenlighted the project with its record of decision March 26, but other pieces of the review process remained.

BOEM’s final approval clears the way for offshore construction of the 924-MW project, which will be the second offshore wind farm to feed into the New York grid and the third project begun by the Ørsted/Eversource partnership. Sunrise’s onshore transmission infrastructure preparations have been underway for months and now will accelerate.

The June 21 announcement was BOEM’s third offshore wind update in four days.

BOEM said June 20 it had determined its plan to lease parts of the Gulf of Maine for wind energy development would have minimal environmental impact, and on June 18, it issued a call for input as it begins to consider a wind lease auction off the coast of a U.S. territory, tentatively targeted for 2028.

Sunrise Wind

The announcements that Sunrise Wind could and would begin construction complete a turnaround from a remarkably bad year for that project and for most other wind farms planned along the Northeast U.S. coast, as soaring costs made offtake contracts negotiated years earlier untenable.

New York state rejected Sunrise’s request for more money in late 2023 but invited a rebid in a rush solicitation. Sunrise submitted a new bid with much higher costs, and New York announced a new contract June 4.

Along the way, Ørsted and Eversource recorded billions of dollars in impairments and losses from their joint venture. There also were some high points: This year, the partners completed South Fork Wind, the first utility-scale wind farm in U.S. waters, and started construction on Revolution Wind.

The two companies are in the late stages of terminating their partnership — Eversource has decided to limit its work in the offshore wind sector to onshore transmission infrastructure. It has reached deals to sell its share of Sunrise to Ørsted and its share of South Fork and Revolution to Global Infrastructure Partners.

“Sunrise Wind is a centerpiece of New York’s clean energy vision, and with this final federal approval, we can officially put the construction phase in motion,” Ørsted Americas CEO David Hardy said in a news release. “BOEM’s approval is an important milestone not just for New York, but also for America’s domestic energy sector.”

Sunrise Wind is to be built in lease area OCS-A 0487, which is 109,952 acres situated more than 30 miles east of the eastern tip of Long Island, closer to Massachusetts and Rhode Island than to New York.

Sunrise is targeted to come online in 2026. Its export cable will stretch about 100 miles to Holbrook on the south shore of Long Island. Port Jefferson Harbor, on the north shore, will host the operations and maintenance hub.

Gulf of Maine

The Gulf of Maine draft environmental analysis announced June 20 is a preparatory step for the auction of up to eight lease areas totaling nearly 1 million acres and holding the potential for up to 15 GW of wind generation capacity.

The Department of the Interior announced in April it is targeting such an auction for 2024. Also this year, it hopes to auction leases in Central Atlantic, Gulf of Mexico and Oregon regions.

The water is so deep in the Gulf of Maine and Oregon lease areas that wind power development there would rely on floating technology, which still is being developed.

The draft environmental assessment does not examine the environmental impact of installing and operating thousands of floating wind turbines off the Maine, New Hampshire and Massachusetts coasts.

It assesses only the reasonably foreseeable consequences of site characterization and site assessment activities that would occur as developers conduct the research that would form the basis of their construction and operation plans.

The draft analysis concludes this work would have negligible or negligible-to-minor impacts.

BOEM has been advancing the Biden administration’s offshore wind goals vigorously. While so far it has fended off legal challenges from wind power opponents, it has given consideration to feedback from stakeholders and the public.

BOEM reduced the number of turbines in the Sunrise Wind plan, for example, and reduced the size of the Gulf of Maine Wind Energy Area, both in response to concerns raised in public comment periods.

Before it finalizes the Gulf of Maine environmental analysis, BOEM once again is seeking feedback. A 30-day public comment period on the draft will run through July 22.

US Territories

On June 18, BOEM issued a request for suggestions for baseline environmental and socioeconomic studies that will shape its decisions about potential offshore wind development near U.S. territories.

BOEM also is looking for local entities that could carry out studies and environmental monitoring.

“BOEM develops, funds and manages rigorous scientific research to ensure our decisions are informed by the best science and Indigenous knowledge available,” Rodney Cluck, chief of BOEM’s Environmental Studies Program, said in a news release. “Additional research focused on the U.S. territories will increase our understanding of these important areas, and the potential impacts of offshore wind energy development on their residents and resources.”

The U.S. has territories in both the Caribbean Sea and Pacific Ocean, and BOEM’s request for letters of information references both regions.

The regulator is considering a wide range of study subjects, including sea turtles, whales, workforce capabilities, public values, submerged archaeological sites and larval dispersal.

BOSTON — Offshore wind executives and government officials expressed tentative optimism at an offshore wind conference about the industry’s rebound from last year’s spate of contract cancellations.

With construction underway on Vineyard Wind, Revolution Wind and Coastal Virginia Offshore Wind and several earlier-stage projects back under contract or rebid in ongoing state solicitations, the industry is building a foundation heading into the uncertainty of the 2024 election, several speakers emphasized at the June 17-18 Reuters event.

Walter Musial, chief engineer of offshore wind energy at the National Renewable Energy Laboratory, said recent project cancellations have delayed offshore wind’s growth in the U.S. but do not seem likely to have a major impact on its long-term outlook.

Most indicators “generally support the long-term viability of the industry,” Musial said.

Heading into the election, “something that we have not done well enough as an industry is selling the job creation story,” said Teddy Muhlfelder, head of Empire Wind for Equinor.

“It’s a truly exciting story for the U.S., which hasn’t seen new major manufacturing in a long time,” Muhlfelder added. “This impacts red states and blue states.”

Despite the recent rebound, the nascent industry remains reliant on federal and state governments as it scales up. A recent report by the Global Wind Energy Council projected 410 GW of additional global offshore wind capacity to be installed over the next decade, contingent on continued policy support. (See Decade of Strong Growth Forecast in Offshore Wind Sector.)

While the Biden administration has approved eight commercial-scale offshore wind projects, former President Donald Trump did not issue a single offshore wind permit during his presidency and has expressed his disdain for offshore wind on the campaign trail.

Speaking about the Atlantic Shores project at a rally in May, Trump said “we’re going to make sure that that ends on day one — I’m going to write it out in an executive order.”

“We must not take a day for granted,” said Daniel Runyan, head of offshore wind development at Invenergy.

Runyan stressed the need to continue building up the domestic supply chain, noting that “we have the opportunity to see some major investment throughout the United States” that would provide job and economic development benefits “beyond just the megawatt hours.”

Despite the uncertainty at the federal level, speakers applauded the Northeast states’ continued commitment to offshore wind amid the recent rocky waters.

David Ortiz, head of government affairs and market strategy at Ørsted, praised the ongoing coordinated procurement of Connecticut, Massachusetts and Rhode Island. The combined solicitation of up to 6,000 MW received 5,454 MW in bids in March, with winning bids set to be announced Aug. 7. (See New England States’ OSW Procurement Receives 5,454 MW in Bids.)

“We think that this coordinated procurement is a really strong step in the right direction and is really leading this industry,” Ortiz said. “Other states should look this way and follow.”

The coordinated procurement is intended to unlock economies of scale and enable the more efficient use of regional supply chains and ports to reduce overall costs to ratepayers.

Ortiz said the Northeast states could further improve their procurement processes by more closely aligning the commercial operations date requirements and inflation index mechanisms of the three state requests for proposals.

Speakers at the conference also called for permitting improvements to help reduce costs and timelines.

“Permitting needs to be accelerated for offshore wind and every other infrastructure project in the U.S,” said Sy Oytan, COO of offshore wind for Avangrid Renewables. He noted that allocating more resources and funding to relevant government agencies could be one way to speed up timelines.

Beyond just permitting speed, “clarity of time frame is absolutely critical,” said Diane Leopold, COO of Dominion Energy. Leopold said uncertainty regarding the length of the permitting process can directly increase costs, particularly for booking contractors.

Muhlfelder of Equinor also stressed the importance of timeline certainty, calling offshore wind a “schedule-driven” industry.

“You’re forecasting eight years out when a vessel’s going to arrive in a four-month window,” Muhlfelder said. “Having a really good understanding of your schedule is going to be key.”

Below is a summary of the agenda items scheduled to be brought to a vote at the PJM Markets and Reliability Committee and Members Committee meetings. Each item is listed by agenda number, description and projected time of discussion, followed by a summary of the issue and links to prior coverage in RTO Insider.

RTO Insider will be covering the discussions and votes. See next week’s newsletter for a full report.

Markets and Reliability Committee

Consent Agenda (9:05-9:10)

B. Endorse proposed revisions to Manual 18: PJM Capacity Market to reflect redesigns drafted through the Critical Issue Fast Path (CIFP) process and approved by the commission in January (ER24-99). The changes expand the use of effective load-carrying capability in the accreditation of all generation classes, require that planned resources notify PJM of their intent to participation in auctions at least 90 days in advance and change how unforced capacity (UCAP) values are calculated. (See “Stakeholders Endorse Manual Revisions to Implement CIFP Changes to Capacity Market,” PJM MIC Briefs: May 1, 2024.)

C. Endorse proposed revisions to Manuals 14B: PJM Region Transmission Planning Process; 20: PJM Resource Adequacy Analysis; 20A: Resource Adequacy Analysis; 21: Rules and Procedures for Determination of Generating Capability; 21A: Determination of Accredited UCAP Using Effective Load Carrying Capability Analysis; and 21B: Rules and Procedures for Determination of Generating Capability drafted through the CIFP process and accepted by the commission in ER24-99. The new language details PJM’s new approach to risk modeling, how it simulates resource outputs and the definition of the capacity emergency transfer objective (CETO). (See “CIFP Manual Revisions Endorsed,” PJM PC/TEAC Briefs: June 4, 2024.)

B. Endorse proposed tariff and Reliability Assurance Agreement (RAA) revisions addressing how capacity obligations arising from forecasted large load adjustments are assigned. (See “New Approach to Large Load Addition Capacity Assignments Endorsed,” PJM MRC Briefs: May 22, 2024.)

MISO’s second, mostly 765-kV long-range transmission plan could tip past $25 billion with the addition of more projects, stakeholders have learned.

RTO staff said its “near-final” second long-range transmission plan (LRTP) stands between $23 billion and $27 billion, up from the original range of $17 billion to $23 billion. The grid operator plans to submit the portfolio to its Board of Directors for approval in early December.

“That is currently where we’ll think we will land, including underbuilds,” Director of Economic and Policy Planning Christina Drake said of the cost during a teleconference June 21. The proposed portfolio will require “underbuilding,” or secondary, lower-voltage transmission upgrades to support a 765-kV network in the Midwest region. MISO is still finalizing its list of underbuild projects. It also has yet to translate its reliability and economic analyses into a business case for the second LRTP portfolio.

MISO last month said it would add seven 765- or 345-kV projects in the Dakotas, Minnesota, Michigan, Indiana and Iowa and replace an original 765-kV project in Missouri and Iowa with segments of 345-kV line in the St. Louis metropolitan area. (See “MISO Undeterred, Plans More LRTP Projects,” MISO IMM Knocks LRTP Benefit Calculations; RTO Poised to Add More Projects.)

“We’re in some of the final stages here of economic and reliability robustness testing,” Drake said.

MISO’s analyses so far indicate that with the second, expanded portfolio, its Midwest region reduces curtailments by 8.5% annually — or by 20.4 million MWh — by 2042. Reductions in curtailments should assist fleet evolution, the RTO said. They should also reduce adjusted production costs by allowing the dispatch of the most economical units.

RTO staff said the portfolio would allow more generation dispatch from its West region to flow east to population centers. MISO’s analyses showed the portfolio “enables and incentivizes” energy deliveries from renewable sources in Minnesota, the Dakotas and Wisconsin, which will cut down on price separation in the Midwest region.

MISO said it expects LRTP II to overall reduce the cost to serve load in the Midwest by the early 2040s. While the Central region could save $2.20/MWh and the East region $.70/MWh, costs could rise at times in the West region, which will export more often.

The RTO also said the portfolio would reduce congestion to improve existing transmission limits, especially in its Central and East planning regions.

Some stakeholders said the savings seemed underwhelming for the scale of the proposed 765-kV network.

MISO Senior Expansion Planning Engineer James Slegers cautioned stakeholders that when more generators can deliver output, the greater volumes will likely aggravate congestion on other flowgates. The RTO said it plans to address congestion shifts through the underbuild process or through its next LRTP portfolio.

The RTO is planning to debut a second part of the portfolio that proposes more projects for MISO Midwest.

Drake said MISO is aware that the $25 billion portfolio would not enable all new deliveries of generation the RTO expects in the next 20 years.

“That’s why we’re taking this in two slices,” Drake said. She said the second part will be considered a separate portfolio and able to stand on its own merits.

WEC Energy Group’s Chris Plante challenged MISO’s characterization of the second LRTP being a standalone portfolio. He likened the system to a car that needs major repairs in addition to several secondary issues.

“We need to look at all the problems of the vehicle. I appreciate MISO saying that it’s standalone, but that’s a red herring. Just say what it is: It doesn’t address all of the constraints. Let’s be honest,” Plante said.

MISO Executive Director of Transmission Planning Laura Rauch said that despite not proposing to solve all system issues with this portfolio, MISO is nonetheless demonstrating that it provides value and sustains reliability.

Drake said that without the second LRTP, curtailments, overloads and price separation will proliferate, and new resources will be prevented from connecting to an already strapped system.

The LRTP portfolio would resolve most impending thermal violations on 200-kV and above facilities in the Midwest, MISO said. But for facilities under 200 kV, it said, the second LRTP appears to solve thermal violations less consistently. Staff said some of the remaining violations are better addressed through MISO’s routine annual transmission planning or through network upgrades assigned to generators trying to complete the interconnection queue.

New York has approved a framework to reach its 6-GW energy storage goal by 2030 and will take steps to ease factors that have limited its deployment to barely 400 MW of operational capacity so far (18-E-0130).

The Public Service Commission’s vote June 20 on a 6-GW roadmap is the culmination of a lengthy period of planning and review after Gov. Kathy Hochul doubled the goal from 3 GW.

If successfully executed as planned, the roadmap would create infrastructure that would reduce future investments needed in the grid, replace more of the high-emissions peaker plants and potentially meet at least 20% of the state’s peak load.

Storage is an indispensable part of the grid New York wants to build, in which intermittent wind and solar generation provide an increasingly large portion of the power portfolio. Department of Public Service staff estimate a need for 12 GW of storage by 2040, when the state reaches its statutory deadline for a zero-emissions grid, and the 2030 goal is seen as an important market signal needed to build momentum toward this.

The PSC order establishes an interim goal of 1.5 GW of storage by 2025.

Revenue uncertainty and rising costs have limited the storage buildout in the state. As of April 1, approximately 396 MW of storage was operational in New York; 581 MW was under contract; and 300 MW has been procured but not under contract.

The PSC’s order attempts to address this. Among the highlights of the roadmap:

3 GW of new short-duration (up to four hours) bulk storage will be procured through a new competitive index storage credit mechanism.

5 GW of new retail storage (up to four hours) and 200 MW of new residential storage (up to two hours) will be supported through expansion of existing regional incentive programs through the New York State Energy Research and Development Authority.

At least 35% of program funds will support projects that benefit disadvantaged communities by targeting fossil fuel peaker plant emissions reductions; there will be specific carve-outs for the New York City region because of the concentration of peaker plants and disadvantaged communities there.

Electric utilities must study the potential for storage projects to provide cost-effective transmission and distribution services not available through existing markets.

Investment will be prioritized in the development of reliable, long-duration storage technologies.

Prevailing wages will be a programmatic requirement for energy storage projects with a capacity of 1 MW or greater.

Contract duration will be a maximum of 15 years for bulk lithium-ion battery projects and 25 years for other technology.

A one-time inflation adjustment will be allowed.

Retail storage projects will be capped at 20 MWh.

The New York Battery and Energy Storage Technology Consortium (NY-BEST) welcomed the news.

“The roadmap represents the largest investment in energy storage in the nation, with proposed investments estimated between $1.2 billion and $1.9 billion, distributed across bulk, retail and residential programs,” Executive Director William Acker said.

The trade group Alliance for Clean Energy New York also celebrated the move.

“This is an important milestone in our clean energy progress,” Executive Director Marguerite Wells said. “Battery energy storage plays a pivotal role in improving grid reliability, stabilizing electricity prices, harnessing the full power of renewable energy, reducing New York’s reliance on fossil fuels and transitioning to a modernized electric grid, and is an important part of reaching our clean energy and climate goals.”

“Long-duration energy storage is a vital resource in meeting peak loads as traditional peaking plants retire due to the” Climate Leadership and Community Protection Act, the Independent Power Producers of New York said. “However, batteries, as load modifiers, and not generators themselves, are risky due to the need to decide when to charge and when to discharge into the system. However, we still need new dispatchable resources in the future, whatever qualifies as net zero under the CLCPA, to keep the grid running during events like the heat we have had this week.”

The PSC vote was not unanimous. Commissioner Denise Sheehan, who previously was associated with NY-BEST, recused herself, and Commissioner John Maggiore concurred rather than vote to approve.

“Advancing the energy storage sector through this program once again positions New York as a leader for others to follow. That said, I’m skeptical about how we’re funding this program,” Maggiore said.

He specifically faulted the roadmap for relying on funding through utility bills and for benefiting some disadvantaged communities at the expense of others through the downstate carveouts.

The analysis performed for the roadmap estimates the total cost of the incentive program at $1.29 billion to $2.01 billion, a very wide range because of the uncertainty of wholesale energy and capacity payments.

It estimates 6 GW of storage by 2030 would have a net value in averted grid expenditures of $1.94 billion in net present value through increased delivery of renewables and decreased reliance on more expensive firm capacity. It did not attempt to quantify further societal benefits such as improved air quality.

In 2030, when the program cost is expected to be highest, monthly bill impact of the retail/residential storage incentives is estimated to range from an average of $1.07 for residential ratepayers to $22.43 for commercial ratepayers to $2,307.50 for industrial high-load factor ratepayers.

On top of that would be the bulk storage program impacts: $1.05, $22.14 and $2,277.13 per month for the same three classes of customers, respectively.

Two weeks after visiting Georgia to celebrate the completion of two new reactors at the Vogtle nuclear power plant, Energy Secretary Jennifer Granholm was on stage at the American Nuclear Society (ANS) Conference in Las Vegas, announcing $900 million in federal funding to support the buildout of a pipeline of new, smaller-scale nuclear plants.

The Westinghouse AP1000 reactors now producing power at Vogtle were the first new nuclear plants built in the U.S. since 2016 and came online seven years behind schedule and cost more than double the original estimate of $14 billion. The new federal funding, authorized in the Infrastructure Investment and Jobs Act, is aimed at building market confidence that the U.S. industry will be able to incorporate the lessons learned at Vogtle to deliver a new round of safer, more efficient small modular reactors (SMRs) on time and on budget.

According to a notice of intent (NOI) the Department of Energy issued June 17 ― following Granholm’s announcement in Las Vegas ― the IIJA dollars will be split into two “tiers.” The First Mover Team Support tier will provide up to $800 million for two next-generation light-water SMRs, or GenIII+ SMRs, being developed by teams that include a utility, the reactor manufacturer, a construction company and end users or off-takers.

The teams must have signed contracts in hand and must be committed “to deploying a first plant while at the same time facilitating a multireactor GenIII+ SMR orderbook,” the NOI says.

The Fast Follower Deployment Support tier will split the remaining $100 million between three types of projects that together could help streamline and accelerate project development. The three “sub-tiers” include:

siting initiatives that “lead to multireactor orderbooks of advanced SMRs”

initiatives to support the buildout of a cost-competitive nuclear supply chain

initiatives that help GenIII+ SMR projects set and meet their time and cost targets

The NOI also sets out a tentative schedule, beginning with an informational “Industry Day” and meetings with prospective applicants this summer, followed by the opening of the application process. The deadline for applications could be by year’s end, and awards could be announced by summer 2025.

The federal support is intended to “ensure nuclear power ― the nation’s largest source of carbon-free electricity ― continues to serve as a key pillar of our nation’s transition to a safe and secure clean energy future,” Granholm said in a DOE press release. The goal is to “support early movers in the nuclear sector as we seek to scale up nuclear power and reinforce America’s leadership in the nuclear industry.”

But U.S. leadership in nuclear development ― at home and abroad ― has waned as the cost and time overruns of Vogtle have cast a pall over the market, creating a “commercial stalemate,” according to the NOI. “Utilities and end users/off-takers recognize the benefits of and need for nuclear power, but perceived risks of cost and timeline overruns and project abandonment have limited committed orders for new reactors.”

Anticipated growth in power demand could help break that stalemate, said Patrick White, research director of the Nuclear Innovation Alliance.

DOE’s efforts to build an SMR pipeline is “part of a larger conversation about how different energy end users are going to think about trying to meet their clean energy targets,” White said. “I think we’re seeing a lot of conversations about what does it take for a utility to reach net zero? What does it take for things like tech companies that have increasing energy requirements from data centers, from AI computing?” he said.

“There are more and more conversations about how a Generation III+ SMR could help meet those energy needs. So, I think this is another piece of the puzzle of trying to align all the different stakeholders so we can have a reactor technology ready when a project developer, a constructor and an end user are ready to commit to a project and move forward.”

State of the Stalemate

The new Vogtle reactors ― referred to as Units 3 and 4 ― are classified as GenIII+ reactors, which is industry shorthand for the generation of nuclear reactors developed since the mid-1990s, White said. The first generation of reactors was developed in the 1950s and ‘60s, and the second generation ― many of which still are online today ― in the ‘70s and ‘80s.

But the 1,000-MW size of the AP1000 “might limit its application for some utilities … and that total cost of the project might be prohibitive for some smaller utilities,” he said. “And so there was a recognition by advanced reactor developers and by companies that there might be a niche here for using that Generation III+ technology, but on a smaller scale.”

DOE has been funding other advanced SMRs through its Advanced Reactor Demonstration Program (ARDP), which has provided $2.5 billion in IIJA funds to two projects using new technologies. TerraPower’s 345-MW Natrium reactor is designed to be a sodium-cooled fast reactor. The Bill Gates-funded company broke ground on the project June 10 at a site in Wyoming, near a soon-to-retire coal plant owned by PacifiCorp, which is planned to be the primary off-taker for the Natrium plant.

X-energy’s Xe-100 reactors are designed as high-temperature, gas-cooled generators. X-energy is working with Dow Chemical, which plans to install four of the reactors at its Seadrift plant in Texas.

A key difference between the ARDP projects and the GenIII+ SMRs is the fuel they use. GenIII+ SMRs use the same low-enriched uranium (LEU) that powers existing reactors. But both Natrium and the Xe-100 are designed to use high-assay, low-enriched uranium (HALEU), which has a higher concentration of uranium-235, close to 20% versus 3% to 5% for the LEU that fuels most commercial reactors.

Until recently, Russia was the only source of uranium for HALEU, but the war in Ukraine has spurred DOE efforts to develop domestic supplies. A demonstration plant was opened in Ohio in November of 2023, with the goal of eventually producing enough HALEU for both ARDP projects, which are not expected to come online until the end of the decade.

The GenIII+ SMRs now available or in development in the U.S. are mostly sized at 300 MW: for example, the Westinghouse AP300, a smaller version of the AP1000, and GE Hitachi’s BWRX 300. Holtec also is developing a 300-MW GenIII+ SMR, with plans to deploy two of the reactors at its Palisades plant in Michigan, which is in the process of restarting.

But, as DOE notes, the pipeline of committed projects is thin. Billed as the first GenIII+ SMR deployment in North America, the Province of Ontario and Ontario Power Generation (OPG) plan to install four GE Hitachi BWRX 300s at an existing OPG nuclear plant.

The Tennessee Valley Authority also says it wants to install a BWRX 300 at its Clinch River site. CEO Jeff Lyash has spoken about developing a fleet of up to 20 reactors by 2050. (See Making the Case for Nuclear at NARUC.)

Nuclear Capacity Needed

In addition to Vogtle Units 3 and 4, the 93 nuclear reactors in operation across the U.S. provide close to 18% of the nation’s electricity and 45.5% of its carbon-free power, according to the Nuclear Energy Institute, an industry trade group.

In its recent Pathways to Commercial Liftoff: Advanced Nuclear report, DOE estimated that to meet President Joe Biden’s goal of a net-zero economy by 2050, the U.S. will need 550 GW to 770 GW of clean, firm power by 2050. Advanced nuclear could provide 300 GW of that total if the industry can triple its fleet’s 100-GW capacity, the report says.

While some environmental groups, such as the Sierra Club and Greenpeace, remain opposed to the development of any new reactors, nuclear energy has become a rare point of common ground for Democrats and Republicans in Congress. A new bill aimed at streamlining and accelerating nuclear permitting (S. 870) cleared the Senate by a vote of 88-2 on June 18 and is on the way to President Biden. The House passed the bill in May with a strong 393-13 vote.

But will DOE’s $900 million be enough to provide the momentum needed to overcome the legacy of Vogtle and activate the pipeline of orders the NOI envisions?

Again, drawing on the lessons of Vogtle, DOE will prioritize projects that are reliable, licensable and commercially viable, according to the NOI. Teams also must be able to show they’ve agreed on a “preferred reactor technology with a replicable design.”

Catherine Prat, a nuclear engineer and member of ANS, cautioned: “I don’t know if anyone in the design phase of a mega-project would say that any finite amount of money is enough. It certainly helps offset some of the risks, but still requires significant investment from utilities and reactor vendors to develop and deploy the technology.

“It is a significant step for DOE to recognize that some level of government support is necessary, and I think it’s fair to say the industry is appreciative of that,” Prat said in an email. “Let’s not let perfection (enough money) be the enemy of good (some money [and] movement in the right direction).”

Getting a pipeline of projects over the post-Vogtle hump will require “really trying to align the business models and business requirements for all the different commercial players that are going to need to work together,” White said.

DOE “is trying to help kind of create a framework or a way to have incentives for these different companies to come together and say, ‘What is a business model that makes sense for these first movers and for fast followers?’ Does providing this additional funding help them to retire risk related to design, related to siting, related to licensing, related to supply chain, or is it a way to just help maybe reach alignment faster?

“How do you get to five reactors? How do you get to 10 reactors that really help lower the cost of all the technologies overall?”

New York launched its eighth large-scale renewable energy solicitation June 20, seeking proposals for land-based projects to help the state meet its emission-reduction goals.

The New York State Energy Research and Development Authority (NYSERDA) said eligibility applications are due July 15; bid proposals are due Aug. ; and initial award notifications are expected by Sept. 30.

The 2024 Renewable Energy Standard request for proposals — RESRFP24-1 — will result in NYSERDA procuring Tier 1 renewable energy certificates from renewables that enter commercial operation before Nov. 30, 2026, with a possible deadline extension to Nov. 30, 2029.

A productive RFP would help NYSERDA continue to refill the state’s renewable energy pipeline, which suffered a major setback in late 2023 as 81 projects canceled Tier 1 contracts totaling 7.5 GW of nameplate capacity because of rising costs that made it financially untenable to proceed to construction.

As the pipeline collapsed and chances of the state reaching its goal of 70% renewable energy by 2030 grew increasingly remote, NYSERDA launched RESRFP23-1 on Nov. 30, 2023.

On April 29, it announced the 2023 solicitation had yielded tentative contracts for 24 projects totaling 2.4 GW of capacity, all of them mature proposals and many of them party to previously canceled contracts.

For RESRFP24-1, NYSERDA is encouraging all project developers to submit proposals, including new market entrants. The solicitation includes the inflation-indexing provisions that have been included in other recent renewable solicitations in the era of spiraling costs.

It also includes requirements to ensure the state’s societal goals beyond climate protection are addressed, including labor provisions, stakeholder engagement requirements, disadvantaged community commitments and agricultural land preservation.

“Private renewable energy developers are ready and willing to invest billions of dollars into New York, providing jobs and tax revenue for our local municipalities,” Marguerite Wells, executive director of the Alliance for Clean Energy New York, said in the state’s announcement of RESRFP24-1. “We expect numerous quality responses to this RFP, and we look forward to NYSERDA awarding projects that will be built expeditiously to bring benefits to New Yorkers as soon as possible.”