The integration of Markets+ with the Western Resource Adequacy Program (WRAP) would be among a handful of key reliability benefits of SPP’s Western day-ahead offering, according to an “issue alert” published Aug. 13 by 10 entities that backed development of the market.

The alert, sent to the Markets+ States Committee (MSC) on Aug. 13, is the second in a series of seven such notices intended to highlight the purported advantages of Markets+ over CAISO’s Extended Day-Ahead Market (EDAM) and Western Energy Imbalance Market (WEIM). The first covered differences between how the two markets would be governed. (See Governance is ‘Key Consideration’ for West, Markets+ Backers Say.)

The Markets+ Phase 1 Funding Parties include Arizona Public Service, Powerex, Public Service Co. of Colorado, Salt River Project, Tacoma Power, Tri-State Generation and Transmission Association, Tucson Electric Power, and the Chelan, Grant and Snohomish public utility districts of Washington state. The alerts aren’t vetted by the MSC and don’t represent the positions of the committee or of the staff for the Western Interstate Energy Board, which hosts both the MSC and the WEIM’s Body of State Regulators.

“Market design elements that support electric system reliability must be considered prior to joining a market, as reliable service is not only expected by consumers; it is also essential to the safety and wellbeing of the general public,” the alert said. “As evidenced by the impact of extreme weather events over the past several years, reliability risk is elevated.”

The alert contends Markets+ will address that risk because its “robust, stakeholder-driven governance framework” produced a market design with a “strong focus” on reliability. The parties to the notice also point out SPP has a “long track record” as a reliability coordinator in both the Eastern and Western interconnections and through operation of the SPP RTO and Western Energy Imbalance Service (WEIS).

But the integration of Markets+ with the Western Power Pool’s (WPP) WRAP, which SPP operates on behalf of the WPP, gets top billing in the alert. Under the Markets+ tariff, market participants must join the program “because a common and rigorous resource adequacy structure is foundational to reliability and critical to achieving equitable outcomes within a market footprint,” according to the alert.

“WRAP applies a common approach for calculating resource capacity values and determining each participant’s minimum obligation for resource adequacy, which, in the context of Markets+, will prevent market participants from being over-reliant on others’ resources,” the parties wrote, adding that the arrangement will ensure that capacity obligations — and the benefits of regional diversity — are “distributed equitably.”

The parties also contend the WRAP component of Markets+ will provide visibility into how various resources perform during critical hours “in a way that does not currently exist” and enforce resource deliverability requirements that will incentivize development of new transmission, “supporting reliable service to customers and the efficient integration of clean energy resources.”

The alert further said Markets+ “builds upon” WRAP’s forward resource procurement requirement — an explicit commitment to make resources available during a specific time frame — that ensures the market has sufficient generation on hand during real-time intervals through use of a must-offer requirement that can only be satisfied by WRAP supply or other “specified resources.”

“This approach improves reliability in the West by addressing those instances where historically some energy commitments have not been backed by reliable physical supply (and ultimately did not deliver to load),” the alert said.

The WRAP originally was scheduled to begin its “binding” penalty phase in summer 2026, but this spring program stakeholders requested that step be delayed until summer 2027, saying supply chain delays, rapid growth in regional peak load and extreme weather events affect participants’ ability to procure enough capacity to meet RA requirements. (See WRAP ‘Binding’ Phase Delay Finds Stakeholder Support.)

‘Fundamentally Different’

Non-California participants in CAISO’s WEIM and EDAM are not required to participate in a resource adequacy program, but California utilities are subject to one overseen by the state’s Public Utilities Commission. To prevent participants from leaning too heavily on the WEIM/EDAM to meet forecasted demand, CAISO instead administers a resource sufficiency evaluation ahead of each market interval to gauge whether each member is prepared to cover expectations for that interval.

The alert singles out that practice for particular criticism.

“Resource sufficiency tests applied in the operating time frame without the underpinning of a common resource adequacy program are inherently challenging for several reasons,” the alert contended. “These reasons include challenges in accurately applying such a test, insufficient failure consequences to prevent deliberate leaning and insufficient notice of a deficiency due to the late timing of the test.”

The alert called the tests “flawed,” saying there have been “numerous examples of inaccurate outcomes” stemming from differing treatment between WEIM balancing authority areas and the CAISO BAA, although no specific examples were cited.

“This experience has reduced some stakeholders’ confidence that an accurate resource sufficiency test will be applied in the day-ahead time frame for the Extended Day-Ahead Market,” the parties to the alert wrote.

The alert additionally criticizes the WEIM/EDAM approach for resulting in “inadequate consequences.”

“Regardless of whether a resource sufficiency test is applied accurately, a standalone resource sufficiency test does not provide adequate time to resolve supply deficiencies that may be identified,” it said. “As a consequence, such a test necessarily relies on failure consequences that are known ahead of time to create incentives for participants to procure sufficient supply in advance to avoid failing.”

The alert also argues that the lack of a common RA framework in the WEIM/EDAM could reduce liquidity in the day-ahead market because participants might hold back supply “in order to manage unforeseen risks in their individual areas through real-time operations.”

“Such voluntary holdback actions for local reliability further diminish available resources in the market, diminishing the market’s overall reliability and efficiency,” it said.

The alert also cautions that utilities participating in both the WRAP and WEIM/EDAM could incur additional costs for having to meet two “unlinked” requirements: the WRAP’s forward-showing obligation and WEIM’s sufficiency test.

“Ensuring reliability is an essential priority that Markets+ and EDAM seek to address in fundamentally different ways, resulting in material differences in the reliability risk that will prevail in each market,” the alert said.

Two Central Atlantic offshore wind areas drew a combined $92.65 million in high bids Aug. 14 during the region’s first federal wind lease auction in a decade.

The U.S. Bureau of Ocean Energy Management declared Equinor Wind and Dominion Energy the provisional winners among six bidders for the two leases off the Delaware and Virginia coastlines.

Equinor beat out other bidders in multiple rounds of bidding with a $75 million final offer to lease OCS-A 0557. The Norway-based energy company has a worldwide offshore wind portfolio that includes Empire Wind off the New York coast.

OCS-A 0557 totals 101,443 acres with a potential installed generation capacity of 1.2 GW to 2.3 GW.

Dominion, bidding as Virginia Electric and Power Co., submitted the only bid to lease OCS-A 0558 and offered the minimum price: $17.65 million. Dominion currently is building Coastal Virginia Offshore Wind, a 2.6-GW project that is the largest yet approved for construction in U.S. waters.

OCS-A 0558 totals 176,505 acres, with a potential installed generation capacity of 2.1 GW to 4.0 GW.

In a news release, Interior Secretary Deb Haaland noted how far offshore wind has come:

“At the start of the administration, our nation had approved zero offshore wind energy projects. Today, we have nine — enough to power nearly 5 million homes. This is what developing a clean energy transition looks like.”

The U.S. offshore wind sector has grown greatly during the Biden administration yet has struggled mightily with local and global headwinds.

The 2024 Central Atlantic auction attracted far higher bids than the 2023 Gulf of Mexico auction ($5.6 million) but far lower than BOEM’s 2022 auctions in the New York Bight ($4.37 billion), North Carolina ($315 million) and California ($757 million).

BOEM plans offshore wind lease auctions this year off the Oregon coast and in the Gulf of Maine. It canceled a planned Gulf of Mexico auction for lack of competitive interest.

Dominion provisionally won the OCS-A 0558 lease without competition at a substantially lower price than OCS-A 0557 commanded, even though OCS-A 0558 is substantially larger and potentially can site many more wind turbines.

The final sale notice flagged some potential complicating factors for wind energy development in OCS-A 0558, including NASA launch operations and extensive military activity in the region.

BOEM warned prospective bidders, for example, that conflicts with the U.S. Navy’s advanced radar system at Naval Air Station Patuxent River could force up to 1,750 hours of wind turbine curtailment per year.

A third wind energy area in the region presents even more potential conflicts and was removed from consideration for this auction.

A Dominion spokesperson told NetZero Insider it’s too early to say how these restrictions would affect the utility’s planning but that potential future wind energy development would engage all stakeholders.

OCS-A 0558 is 35 nautical miles east of the mouth of the Chesapeake Bay, directly east of and contiguous to OCS-A 0483, which Dominion acquired for $1.6 million in a 2013 auction. It is building Coastal Virginia Offshore Wind (CVOW) there.

Nearby, off the northernmost coast of North Carolina, Dominion has agreed to buy OCS-A 0559 from Avangrid, which had planned to develop it as Kitty Hawk North and ran into local opposition with its plans for an export cable making landfall in Virginia Beach.

A proposal was floated this year to bring competition to offshore wind development in Virginia waters. Senate Bill 578 called for a competitive procurement process in which Dominion could submit bids but not evaluate them or select awardees. The measure was pushed back to the 2025 legislative session.

The provisional winners were happy about the result of the Central Atlantic auction.

Molly Morris, president of Equinor Renewables Americas, said in a news release, “Equinor’s interest in this auction is consistent with our approach to pursue attractive offshore wind opportunities in the United States. The Central Atlantic region has … rapidly growing demand for electricity, with widespread support for adding renewable sources of energy into the power mix.”

Dominion said the move would expand options for an all-of-the-above approach to meeting unprecedented electric demand in Virginia. “Winning this lease area gives us another low-cost option to meet that growing demand while providing our customers with reliable, affordable and increasing clean energy,” CEO Robert Blue said.

Trade association Oceantic Network hailed the auction results and cast an optimistic eye to the future, noting there is bipartisan support in the region for offshore wind even as wind energy foe Donald Trump fights to return to the White House.

“Today’s successful auction demonstrates that offshore wind will continue to play a leading role in the region’s energy future,” Oceantic CEO Liz Burdock said. “The resulting leases will strengthen an emerging manufacturing hub in the mid-Atlantic, creating a dependable pipeline of contracts well into the next decade. Despite the general uncertainty around the upcoming presidential election, this is a vote of confidence for an American industry that has already received more than $2 billion of new supply chain investment in the first half of 2024.”

The Mid-Atlantic Renewable Energy Coalition, a nonprofit advocacy group, hailed the auction results for their impact on the region. Executive Director Evan Vaughan said, “Today’s auction for the right to develop offshore wind farms off the coast of Mid-Atlantic states makes clear that a combination of state policies in Maryland, Delaware, New Jersey and Virginia, along with rising electricity demand, are attracting major interest from our growing industry. MAREC Action congratulates Equinor and Virginia Electric and Power Co. on their winning bids today — consumers will be the ultimate winners of this new source of reliable clean energy.”

The U.S. Department of Energy is looking to supercharge research, development and deployment of advanced and long-duration energy storage (LDES) technologies with the Aug. 13 ribbon cutting at the Grid Storage Launchpad (GSL) ― a high-tech lab and testing facility ― at the Pacific Northwest National Laboratory (PNNL) in Richland, Wash.

The 93,000-square-foot facility includes 30 “specialty” labs where a team of about 100 researchers will use “artificial intelligence to discover new energy storage materials and [test] their performance on the grid using digital twins, smart data models based on physics and high-speed experimentation,” according to the GSL website.

For example, one of the labs will have “pilot-scale prototyping equipment” that will allow researchers to quickly design, produce and test prototypes of emerging storage technologies, while another lab will simulate real-life grid conditions to test the performance of new batteries, first up to 10 kW and then up to 100 kW.

Estimated cost for the GSL is $75 million, with $35 million of the total coming from Washington state, PNNL and Battelle, a science R&D firm that operates the lab for DOE.

Kevin Schneider, a lab fellow and manager for DOE, said having all the research and testing facilities in one building will help accelerate the development of new battery technologies.

“Right now, we have many of these capabilities spread across the [PNNL] campus; so, you complete work in one area, it has to be transported somewhere else. … It takes time and effort,” Schneider said during a phone interview with NetZero Insider. “In the new facility, it’s been laid out in such a way that there are three research corridors, starting with basic chemistry and working its way [to testing], so that there are workflows within the building that allow us to move from one lab to the next very quickly. Those types of structures allow for a surprising kind of increased productivity.”

Schneider also pointed to the lab’s six testing bays, which will test new storage chemistries up to 100 kW, a level specifically requested by industry partners, who told the lab if a technology works at 100 kW, they can begin commercialization.

“So, there’s no need for us to be able to test 1 MW or 10 MW,” Schneider said. “It’s very large and expensive. If it proves out at 100 kW, then they’re ready for deployments.”

The GSL is the only national lab facility with this level of storage testing capability, he said.

Speaking at the ribbon cutting, Sen. Maria Cantwell (D-Wash.) also stressed the importance of the industry partnerships that will be built at the new facility.

“If we want to make the next generation of batteries, we need the energy storage advancements that are here, with the brightest minds at PNNL … just really working together and discovering new and more efficient materials that are faster, cheaper by going from computing, modeling to prototyping to testing and under realistic grid conditions,” Cantwell said.

“This facility will help ensure the advancements in energy storage really do translate to the private sector, creating new innovative battery products as well as dependable manufacturing jobs,” she said.

Geri Richmond, DOE under secretary for science and innovation, spoke of the impact of storage she’s seen while visiting remote tribal communities in Alaska.

“In this job, I’ve had the opportunity to go to places that have been underserved for way too long,” Richmond said. “Having access to storage … allows those tribes in Alaska to not just burn that [fossil] fuel 24/7, that stinks up the town, and it’s loud. I’ve seen what a difference it makes to have storage capacity there. There is so much for us to do and to reach, again, every possible community that we can.”

The facility also will provide technical training for a range of stakeholders, from workers and utility planners to regulators, as well as safety training for first responders.

Cheap, Abundant ‘Local Dirt’

The GSL is a critical part of DOE’s efforts to accelerate the development of new energy storage technologies at commercial scale and at a competitive cost.

The industry’s reliance on lithium-ion batteries has become a political flashpoint due to China’s dominance in the processing of lithium and manufacture of battery cells. The goal for GSL is to develop technologies that use “local dirt,” that is, cheap and abundant materials that come from local sources, Schneider said.

For the United States to achieve its goal of a net-zero economy by 2050, DOE estimates the country will need between 225 GW and 460 GW of LDES, defined as storage with anywhere from 10 hours to more than 160 hours of duration.

Developing these technologies will require more than $330 billion in private investments, while saving $10 billion to $20 billion per year in operating costs and avoided capital spending.

The Energy Storage Grand Challenge was announced in December 2020, with the goal of developing domestic supply chains and manufacturing that could provide all the storage technologies needed to meet U.S. market demand by 2030.

The department launched its Long Duration Storage Shot in 2021, with the goal of reducing the cost of LDES by 90% within a decade. As part of the initiative, DOE awarded $15 million in April to three projects aimed at overcoming technical barriers to the commercialization of long duration storage, such as testing the use of zinc for battery electrodes.

Deployment of grid-scale storage is spreading. As the amount of renewable solar and wind on the grid continues to grow, storage has become vital for time-shifting that intermittent power, storing electricity from mid-day hours, when excess is generated, to be used in the late afternoons and evenings when extra power is needed.

In the past four years, California has deployed 9,000 MW of storage, which has helped CAISO manage extreme heat and high demand, CEO Elliot Mainzer said at a recent online forum sponsored by USEA. (See Demand Growth and Extreme Weather: The Grid’s New Normal.)

Similarly, solar and storage provide ERCOT with the flexible capacity it needs to ride through the late afternoon drop-off of solar energy, CEO Pablo Vegas said at the forum. “This may be the last year that we have real significant risk at solar sunset,” he said. “If we continue to see that trajectory by 2025 into 2026, we could see the summer risk period significantly mitigated because batteries are picking up some of the transition solar ramps as we see the wind come on in the evening.”

But echoing speakers at the GSL ribbon cutting, Schneider said, accelerating the development of new storage technologies remains a high priority. It took decades to develop the lithium-ion batteries powering today’s electric vehicles and grid-scale storage, he said.

“We don’t have another 30 years for the next chemistry to come out,” he said. “We need to be able to do what took 30 years in the next five to 10.”

MISO said its 123-GW collection of projects in the 2023 queue cycle will be subject to another delay into early 2025 as it pauses to see if a tech startup can help it better scale interconnection studies.

In an email to stakeholders Aug. 13, MISO announced it will hold off on starting the definitive planning phase for the 2023 interconnection until February. The RTO said the extra time will allow it to enlist the help of Pittsburgh-based Pearl Street Technologies to better manage interconnection studies.

MISO previously said it solicited help from Pearl Street Technologies to see if the company’s SUGAR (Suite of Unified Grid Analyses with Renewables) software can speed up interconnection studies. Pearl Street has claimed its software can model more generation projects for transmission operators and drastically cut back time spent on engineering analysis.

MISO said the delay in conducting studies ultimately will help it “process more interconnection applications in a timely manner.” It also said it would expand Pearl Street’s assistance from model development to power flow analysis and network upgrade identification.

“MISO would like to take this opportunity to reassure customers that we are committed to processing interconnection requests in a timely manner,” the RTO said to its stakeholders.

In a statement to RTO Insider, MISO said it’s working with Pearl Street to establish some automation in the queue study process that will allow it to complete the first phase of studies more quickly. The RTO said it would begin studies on the 2023 cycle after it can implement automation and after the 2022 cycle of projects clears the first study phase of the three-part interconnection queue.

If it deems all the 2023 applications valid, MISO has said its queue could grow to nearly 350 GW.

MISO told stakeholders more discussion on the 2023 queue class will take place at upcoming meetings of the Planning Advisory Committee and Interconnection Process Working Group.

The 2023 queue cycle already was delayed last year, as MISO sought permission from FERC for steeper penalties, higher fees and more binding proof of land use as a means to get a handle on the sheer number of projects lining up annually for grid treatment. The grid operator ultimately didn’t begin certifying the 2023 class until spring of 2024.

The 2024 cycle also is destined for delays. While it’s unclear if the current software delay will affect when MISO begins processing 2024 entrants, MISO already planned to postpone this year’s cycle while it tries again to win FERC approval of an annual megawatt cap on projects that may enter. (See MISO Sets Sights on 50% Peak MW Cap in Annual Interconnection Queue Cycles.)

MISO said it doesn’t “anticipate closing the window for the next queue cycle until after a cap filing is submitted and accepted by FERC, which is currently on track for 2025.” MISO pointed out it’s currently accepting online applications for the next cycle of interconnection requests, though it’s waiting to kick off any studies.

Meanwhile, clean energy developers’ interest in queueing up appears full steam ahead. Last week, developers Ørsted and Mission Clean Energy announced their intent to join forces to build 1 GW of battery storage in MISO Midwest. Mission Clean Energy plans to submit applications for four projects across MISO’s North and Central regions and give Ørsted the option to buy an ownership stake later in the process.

Ørsted said the storage plans are its first-ever standalone battery storage partnership, in the U.S. or globally.

“Continuing to invest in and build out storage solutions is critical for ensuring a resilient and reliable grid, and this partnership with Mission advances this important goal,” Ørsted Chief Commercial Officer James Giamarino said in a release.

FirstEnergy has reached an agreement with the Ohio Attorney General and the Summit County Prosecutor to resolve all outstanding proceedings on the firm’s bribery scandal.

The $20 million deal with the state and the county prosecutor comes three years after the firm agreed to pay a $230 million fine to the U.S. Department of Justice in a deferred prosecution agreement. (See DOJ Orders $230 Million Fine for FirstEnergy.)

In addition to sinking the careers of leadership at FirstEnergy, its $61 million in bribes and dark money campaign contributions brought down former Ohio House Speaker Larry Householder and former PUCO Chair Sam Randazzo, who committed suicide this year. (See Scandal-ridden Former PUCO Chair Sam Randazzo Found Dead.)

“We are pleased to have reached a resolution with the Ohio Attorney General’s Office and the Office of the Summit County Prosecutor, which recognizes the substantial actions FirstEnergy has taken to establish a highly effective compliance program and instill a culture of ethics and integrity at every level of the organization,” FirstEnergy CEO Brian X. Tierney said in a statement. “FirstEnergy, led by a new Board of Directors and executive team, is a stronger organization today, energized by our commitments to our stakeholders and well positioned for the future.”

The scandal involved trying to get the Ohio Legislature to pass subsidies for nuclear plants FirstEnergy used to own, which it since has spun off into Energy Harbor. That firm was purchased by Vistra Energy in a deal that closed early this year.

FirstEnergy filed the settlement with the Securities & Exchange Commission, which credits the firm with cooperation and says the state will not pursue any charges against it for the conduct covered by the deferred prosecution agreement it signed with DOJ in 2021.

In addition to paying $20 million, FirstEnergy agreed to set up a new Office of Ethics and Compliance and to develop a compliance program designed to prevent violations of U.S. and Ohio regulations and law. The program will include companywide campaigns to get employees and contractors to report any concern about potential violations.

Of the $20 million, $500,000 is set aside to fund the compensation and expenses of an independent consultant to review the efficacy of its compliance programs.

The deal covers only the firm FirstEnergy and specifically does not cover any litigation against former employees or executives. The state has indicted former CEO Charles Jones and former Senior Vice President of External Affairs Michael Dowling. (See Ex-PUCO Chair, Ex-FirstEnergy Execs Indicted in Ohio.)

The U.S. Bureau of Ocean Energy Management has concluded that leasing areas off the Oregon Coast for wind energy development would have no significant environmental impact.

BOEM announced completion of its final environmental assessment Aug. 13. The move paves the way for an auction this year of two areas totaling 195,000 acres with a potential generation capacity of more than 2 GW.

The proposed Brookings Wind Energy Area totals 133,792 acres and sits approximately 18 miles from the southern Oregon shoreline near the California border. The proposed Coos Bay Wind Energy totals 61,203 acres approximately 32 miles offshore, closer to Reedsport and Florence than to Coos Bay.

Both areas are deep enough that floating wind turbine technology would be needed.

The environmental assessment completed by BOEM does not look at the impact of these turbines or their mooring systems and transmission infrastructure. It covers the survey work a leaseholder would conduct while preparing a construction proposal.

And the assessment found this work would have no significant impact on people or the environment.

Mixed support and opposition have greeted the plan to exploit Oregon’s coastal waters for wind power generation, much as plans elsewhere in the U.S. have. (See BOEM Designates Wind Energy Areas off Oregon Coast.)

BOEM has said it took comments into account as it refined the proposed wind energy areas, shrinking the initial call areas from 1.15 million acres and shaping them to reflect concerns voiced in the comment process.

In a news release, BOEM Director Elizabeth Klein said: “BOEM relies on the best available science and information for our decision-making regarding offshore wind activities. Working with Tribes, government partners, ocean users and the public, we gathered a wealth of data, diverse perspectives and valuable insights that shaped our environmental analysis. We remain committed to continuing this close coordination to ensure potential offshore wind energy leasing and any future development in Oregon is done in a way that avoids, reduces or mitigates potential impacts to ocean users and the marine environment.”

BOEM next will publish a final sale notice for the Oregon areas.

President Joe Biden has more than doubled the Section 201 tariff rate quota for imported solar cells, from 5 GW to 12.5 GW per year.

As he imposed new regulations May 16 to protect U.S. solar manufacturers from unfair trade practices, Biden said he might raise the quota if necessary to maintain a supply of cells for U.S. solar module manufacturers as they scale up production through the supply chain.

His administration apparently did conclude this move was necessary: The higher quota was announced Aug. 12, to the praise of an industry group.

The decision affects imports of certain crystalline silicon photovoltaic cells, whether or not they are partly or fully assembled into other products.

The proclamation issued Aug. 12 indicates that a majority of representatives of the U.S. solar industry had requested the change. It reads:

“I have determined that the domestic industry has been making and is continuing to make a positive adjustment to import competition, shown by increased actual and planned module production; various announcements of planned domestic cell production; and improvements in several of the domestic industry’s financial, trade and employment indicators.”

The Solar Energy Industries Association welcomed the move. In a statement, CEO Abigail Ross Hopper said, “SEIA strongly commends President Biden’s decisive action to support American solar module manufacturers by raising the Section 201 tariff rate quota on cells. This move provides an important bridge for module producers to access the supply they need while the United States continues to progress on solar cell manufacturing. This decision will help create a strong, stable module manufacturing sector that can sustain robust cell production in the long run.

“Federal clean energy policies are fueling a surge in domestic manufacturing investments across the country, which are helping us secure our supply chain and uplift American communities. The president’s recent actions are critical for maximizing the impact of these policies and ensuring the long-term success of American solar manufacturing.”

Extensive manufacturing investments have been announced in the United States during his administration, but extensive plans to build solar generation also have been announced, with domestic demand outstripping domestic supply.

Representatives of the U.S. industry in September 2023 said the demand for imports would continue in the near term and petitioned for the tariff rate quota to be raised to 20 GW per year or eliminated altogether.

Eleven months later, they got 12.5 GW.

The new tariff rate quota pertains to products that entered the U.S. after July 31.

Home energy management company Renew Home released a position paper last week arguing that the virtual power plants it creates with aggregations of residential customers can quickly be stood up to help meet growing demand.

As the generation mix shifts ever more toward intermittent renewable resources, the grid needs to be balanced at specific times, which VPPs can help with, Renew Home Executive Vice President Cisco DeVries said in an interview.

“We need to find hundreds of gigawatts of additional capacity in order to meet the challenges faced by the growth in demand for electricity and the management of more intermittent renewables,” DeVries said.

VPPs are going to be key to meeting that demand because they can be stood up around the country much more cost effectively and quickly than other options, including building new natural gas plants, he argued.

“A lot of entities are taking an all-of-the-above approach: looking at natural gas, looking at batteries and looking at VPPs,” DeVries said. “And fundamentally, from an economic perspective, it’s really hard to get there with gas alone, right? Even if you set aside the climate and greenhouse gas impacts, which are significant, you still have an issue of building hundreds of gigawatts of new generation capacity, much of which is only needed for small portions of time in the year.”

Renew Home is a member of Sidewalk Infrastructure Partners, which was formed as an independent entity out of Alphabet, Google’s parent company. The company was created earlier this year by the merger of Google’s Nest Renew service and OhmConnect, and is the largest residential VPP provider in the country, with almost 3 GW under control and plans to expand up to 50 GW by 2030.

Core to that expansion will be growing the number of smart thermostats to cover more of the 82 million homes that have central HVAC systems. Pairing every single HVAC system with a smart thermostat and linking them to a VPP could create 70 GW of load-shifting potential, the company argues in the paper.

Smart thermostats are the quickest way to set up residential VPPs, it says, but electric vehicles and distributed batteries are also part of the plants. The paper forecasts 8 GW worth of EVs and 21 GW of batteries charging by 2030.

VPPs come out of traditional demand response and can still provide that emergency service to the grid when needed, DeVries said, but they are meant to operate more often with less of an impact on the individual customers in an aggregation. They are “designed to run 3 to 5% of the time [and to] have predictable, reliable dispatch in a way that can be just as good as, if not better than, fossil fuel plants.”

They can also do the same work as peaker plants, but even more cheaply without factoring any of the environmental externalities of their competitors, he said.

While most customers are not interested in being a resource that has to respond to changing grid conditions, spreading VPPs out among many customers with smart thermostats can get around and aggregate capacity without too much aggravation.

“We have millions of customers using Nest thermostats who have already given permission to flex their load,” DeVries said. “To say, ‘go ahead, make some modest adjustments in the temperature; pre-cool a little here; let it drift a little there; whatever you want to do. I’m comfortable with it.’”

Renew Home manages their thermostats every day to help customers manage time-of-use rates, save money on their bills and even to use power when the carbon intensity of the grid is lower.

“We have got not only an enormous stranded asset now, as far as gigawatts of existing load that is ready to be controlled today, but there is a near-term pathway to get that into the 50 to 70 GW over the coming few years, and that could transform the reliability of the U.S. grid and also help people actually reduce their energy bills pretty dramatically,” DeVries said.

Electric water heaters could provide another 16 GW in load shifting if connected to smart controllers.

“There are millions and millions of hot water heaters that are put into people’s homes every year, and with a small additional effort, those are all controllable and can be navigated in the same way we do thermostats,” DeVries said. “Customers won’t even notice it’s happening, but their hot water heater will participate, essentially as a thermal battery shifting load around. The capabilities of that are dramatic.”

FERC on Aug. 12 established settlement judge procedures in response to a waiver request from a generator seeking to exit ISO-NE’s inventoried energy program (IEP) and refund the net revenues received from the program (ER24-1407).

The IEP compensates generators for maintaining fuel inventories in the winter and applies to the winters of 2023/24 and 2024/25.

In March, Canal Marketing asked FERC to allow the company to withdraw from the program for the 2023/24 winter period and return the net revenues, plus interest, that it received from its participation in the program.

The company operates a 333-MW gas and oil generator that has been out of service because of a mechanical issue since early 2023. Canal said it initially anticipated the generator would return to service in time for most of the 2023/24 winter, but delays extended the outage through the entire winter.

Canal alerted ISO-NE of the delay in December 2023 and determined the RTO’s tariff does not include provisions that enable “the return of net revenues by a market participant in this particular situation or for a participant to withdraw from the program once its election submission has been accepted by ISO-NE.”

In its request to FERC, Canal said granting the waiver “would not harm any third parties” and that the returned revenues would be “allocated to the market participants that are responsible for the costs of the program.”

Following the request, ISO-NE offered its support for the proposal to return the net revenues. The RTO’s Internal Market Monitor also supported the return of revenues in comments to FERC, while emphasizing the importance of sticking to a “narrow remedy” to the issue.

“Any remedy should be narrowly tailored to preserve the incentives and the design of the program,” the IMM wrote. The market monitor cautioned that any solution must not enable IEP participants in the upcoming winter period to retroactively exit the program if they experience net losses.

“This could create a ‘heads I win, tails you lose’ situation for the upcoming 2024-2025 winter program: a participant that erroneously (or even wrongfully) qualifies for the IEP, could wait-and-see the outcome, and then at the end of the program file for a waiver and return of money if it is in its favor, or not,” the IMM added.

In response comments filed with FERC, Canal disagreed with the IMM’s concerns about broader implications of a waiver, arguing the company communicated to ISO-NE its intention to withdraw from the program and return its net revenues in mid-December 2023, and that it took time to determine the best course of action to remedy the issue.

FERC ordered settlement judge procedures “to permit the parties to seek a settlement to resolve whether and how Canal Marketing should return to ISO-NE the revenues or net revenues.”

The Commission added that “with regard to the IMM’s concerns about future erroneous qualifications for, and late withdrawals from, the IEP, we note that we are establishing settlement judge procedures here based on the unique circumstances and the various arguments raised by parties to this proceeding.”

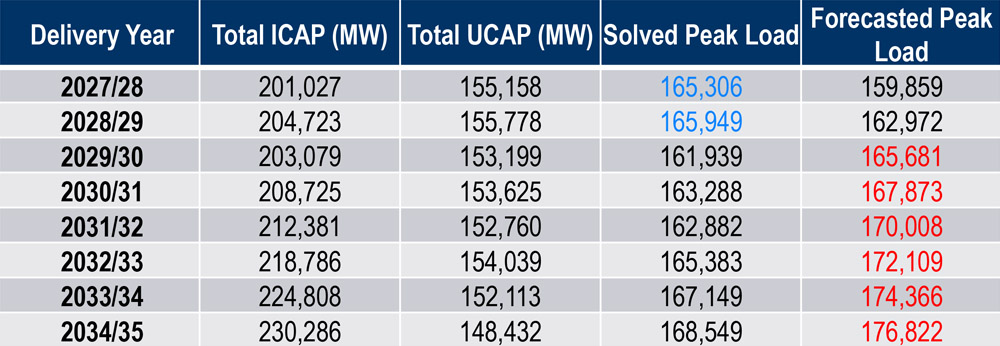

PJM Models Suggest Capacity Shortfall Possible in 2029/30 Delivery Year

PJM could see a growing capacity shortfall starting with the 2029/30 delivery year, the RTO found after running its effective load-carrying capability (ELCC) model on a generation mix forecast through the 2034/35 DY, PJM’s Patricio Rocha Garrido told the PJM Planning Committee during its Aug. 6 meeting.

Rocha Garrido said adjustments to resource accreditation drive a declining forecast pool requirement (FPR) in the analysis, leading to the forecast peak load surpassing the solved peak load.

In other words, the resources PJM expects to come onto the grid will have a declining marginal capacity contribution each year that, paired with generation deactivations, may lead to accredited capacity falling below forecast peak loads.

Rocha Garrido cautioned that the analysis should not be seen as a forecast and is instead the result of applying its ELCC modeling to a resource mix forecast supplied by a PJM vendor, which carries “significant uncertainty.” While the vendor’s assumed resource mix cannot be released publicly, Rocha Garrido said it can be supplied to individuals upon request.

“We’re getting lower reliability value of the additions,” Rocha Garrido said, adding that the declining capacity value is the driving factor “rather than demand-side adjustments.”

If peak loads were driving the imbalance, Rocha Garrido said the FPR would be trending up in the analysis.

PJM analysis found a potential capacity shortfall beginning in the 2029/30 delivery year based on projected resource accreditation ratings and a vendor’s forecast generation mix. | PJM

PJM received deactivation requests for combustion turbines that led to a higher CT rating in the 2026/27 Reserve Requirement Study (RRS) after the analysis was initiated, so they are not reflected in the assumed resource mix. (See PJM Presents Revised Reserve Requirement Study Values.)

Rocha Garrido said a decline in the capacity contribution of demand response resources is due to risk modeling concentrating expected unserved energy in winter hours outside the DR availability window.

Paul Sotkiewicz, president of E-cubed Policy Associates, questioned whether the vendor would readjust the resource mix forecast given the spike in capacity prices in the 2025/26 Base Residual Auction. He said it could make sense for generators to undergo retrofits rather than retire, given the possibility of higher capacity revenues, particularly for coal units that could see upgrades to comply with coal combustion residuals requirements becoming economically viable. (See PJM Capacity Prices Spike 10-fold in 2025/26 Auction.)

Several stakeholders questioned the accuracy of the resource mix forecast and urged PJM to conduct additional sensitivities. Rocha Garrido said more sensitivities would be helpful, but staff did not have time for this analysis while preparing the 2026/27 RRS parameters.

Stakeholders Endorse LAS Charter Revisions

The PC endorsed revisions to the Load Analysis Subcommittee (LAS) charter aimed at reflecting a shift in the group’s function toward reviewing the load forecasts produced by PJM and soliciting stakeholder comments on the forecast inputs.

PJM’s Andrew Gledhill said much of the status quo charter language is a holdover from when transmission owners presented their own forecasts to PJM and stakeholders through the LAS. The proposed changes were approved by the LAS on July 29.

Calpine’s David “Scarp” Scarpignato said stakeholders’ role at the LAS goes beyond reviewing PJM’s load forecasts, which he said was the focus of the original proposed charter revisions. He proposed that PJM’s language be amended to reflect that stakeholders provide substantive comments on how the forecast is prepared.

Gledhill said language in the “responsibilities” section of the charter was intended to reflect stakeholder comments and noted that members do not vote on or approve PJM’s forecasts. He accepted a friendly amendment to the revisions from Scarp to add “and is responsible for soliciting stakeholder input and providing review of PJM reports” to the charter’s mission statement.

Monitor Presents CIR Transfer Proposal

The Independent Market Monitor presented its proposal for an expedited process for transferring capacity interconnection rights (CIRs) held by deactivating generators to planned resources in the interconnection queue. (See “Elevate Reviews CIR Transfer Proposal,” PJM PC/TEAC Briefs: July 9, 2024.)

The biggest distinction between the Monitor’s concept and the four competing designs is that CIRs would not be bilaterally traded between market participants but instead would be made available to the next planned resources that could take advantage of the underlying transmission capability. If PJM identified that a deactivating resource would create transmission violations that would require offering the owner a reliability-must-run (RMR) agreement to keep the plant in operation, PJM would initiate an expedited process where it would assign the CIRs to the next resource in the queue that could address the violations.

If PJM did not identify projects within the interconnection queue that could resolve the transmission violations, it would conduct an auction, or a solicitation could be held for project designs.

Scarp questioned what guarantees can be provided to ensure that generation projects selected by PJM through the expedited process are built if they are meant to replace an RMR contract and constitute reliability projects.

“If you’re doing it for RMR purposes, I’m wondering if you need more of a solid commitment more than what is already in the generator interconnection process,” he said.

PJM, Gabel Associates, MN8 Energy and Elevate Renewables also have sponsored packages, differentiated by the resources that would be eligible to receive transferred CIRs, how potential impacts to the grid would be studied and the standard that would disqualify replacement resources from using transferred CIRs due to identified grid upgrades.

PJM’s Becky Carroll said the proposals are slated to go for first reads and an endorsement during the Sept. 10 PC meeting, but voting could be deferred to the Oct. 8 meeting if substantial changes are made over the next month.

Manual 14B Revisions Include Change to Light Load Model

Stakeholders endorsed revisions to Manual 14B: Region Transmission Planning Process to rework the inputs to PJM’s light load case, which is used in the Regional Transmission Expansion Process (RTEP) load forecast to reflect the growth of load with flat profiles unaffected by weather and season.

The light load case is designed to create an accurate representation of shoulder periods by scaling load down to 50% of the summer forecast peak using bus-level data provided by transmission owners. PJM’s Stan Sliwa said practice has been challenged by the growth of non-scalable load, such as data centers. The revisions would remove non-scalable load from the light load case.

The Manual 14B changes also expand the NERC TPL standards examined during generator deliverability analysis to match current practice, updating the system operating limit (SOL) definition and adding new standards created by NERC.

The language is set to go before the Markets and Reliability Committee for a first read Aug. 21 and an endorsement vote Sept. 25.

Transmission Expansion Advisory Committee

PJM Presents Results of 8-year RTEP Model

PJM has updated the needs in its 2024 RTEP Window 1 solicitation to include a longer eight-year model designed to capture issues that might take longer than the typical five-year cycle to resolve.

The additional three years capture the remainder of the New Jersey offshore wind being interconnected through the State Agreement Approach (SAA), the completion of the Coastal Virginia Offshore Wind (CVOW) project and the 1-GW Chesterfield gas generator near Richmond, Va.

Despite the additions, load growth and resource deactivations are expected to cause Dominion and the West regions to each lose over 1 GW of dispatchable energy in the summer, while the capability in MAAC would grow by 2 GW over the 2029 model. Dominion would lose 2 GW in the winter case, while MAAC and West would both gain around 1 GW. Both MAAC and the West likely would export energy as demand grows in Dominion.

PJM’s Sami Abdulsalam said a conservative approach is taken when considering which planned resources are expected to be available in the RTEP analysis. Both Chesterfield and CVOW have advanced queue positions that provide a strong certainty of them coming online, while the New Jersey SAA projects have commitments to PJM from a state backer.

More than 100 new thermal overloads were identified in the longer model, 76 of which were in the summer, 48 in the winter and 40 in the light load case. Abdulsalam said the analysis is meant to allow transmission owners submitting RTEP solutions to right-size their projects to meet the needs identified in the five-year model with an eye toward long-term needs.

The solicitation window opened July 15 and is set to close Sept. 13, but Abdulsalam noted the new analysis was released after the window opened.

Several ratepayers in Northern Virginia called for alternatives to the series of transmission projects built or that are planned to crisscross the region to supply rapid load growth, with residents particularly interested in the concept of an undergrounded DC line. They also questioned whether higher capacity prices will lead to generation development that could reduce the need for transmission projects.

PJM’s Susan McGill said the RTO’s role is to identify needs and it’s up to developers to propose transmission or generation solutions through the RTEP or interconnection queue.

Supplemental Projects

PPL presented a project to interconnect a 1,980-MW load sited near Hazleton, Pa., for $196.55 million. The customer would be supplied by a new 230-kV switchyard named Tomhicken, which would be cut into the Susquehanna-Harwood double circuit 230-kV line, as well as a new Nescopeck 230-kV switchyard.

Tomhicken would be configured as a six-bay, breaker-and-a-half facility with a 125-MVAR capacitor bank for $45 million, and Nescopeck would be configured as a three-bay breaker and a half switchyard for $29.5 million. Nescopeck would be cut into the Susquehanna-Sunbury 230-kV line with a partial rebuild of the portion between the new facility and Susquehanna to upgrade it to be double circuit for that portion. Additional 230-kV lines would be constructed between Nescopeck, Tomhicken and Harwood.

The customer is expected to come online in 2026 starting with a load of 240 MW, growing to 720 MW in two years, 1,440 MW by 2031 and reaching its full consumption in 2033. The project is in the conceptual phase, with a projected in-service date of June 1, 2027.

Exelon presented a $158 million project to provide service to a customer seeking to bring 378 MW of load to the Elk Grove area in its ComEd zone. The customer would be served by a new 138-kV substation with 16 circuit breakers and in a double ring bus configuration and five 138/34-kV transformers. The facility would be cut into the Elk Grove-Schaumburg line.

The project would require a new 345-kV bus in a breaker-and-a-half configuration to be installed at the Elk Grove substation, including 12 new 345-kV circuit breakers. The bus would be cut into the Des Plaines-Lombard 345-kV double circuit line. Two 345/138-kV autotransformers also would be installed.

The customer expects to bring 117 MW of load in December 2026 and reach 333 MW in 2028. The project is in the conceptual phase, with a projected in-service date of Dec. 31, 2026.

Exelon presented an additional $40.6 million project to serve a customer in the Elk Grove region with 260 MW of load. A new 138-kV substation would be built with 15 circuit breakers in a double ring bus configuration with six 138/34-kV transformers. It would be connected to the Elk Grove East substation with new 1.7-mile, 138-kV lines.

Two 345/138-kV autotransformers would be required at the Itasca substation, as well as two 345-kV and two 138-kV circuit breakers.

The customer anticipates 25 MW of load in June 2027, 87 MW in 2028, growing ultimately to 260 MW. The projected in-service date for the transmission upgrades is Dec. 31, 2027.

FirstEnergy presented a $38.7 million project to replace steel H-frame structures along its Perry-Ashtabula-Erie West 345-kV line, reconductor 7.2 miles of the 20-mile line and replace insulators and related equipment. The line is around 60 years old, and the insulators, H-frames and guying are corroded. The line has experienced seven scheduled outages for repairs and four due to equipment failure since 2014. The project is in the conceptual phase, with a possible in-service date of April 9, 2027.

The utility also presented two projects amounting to $15.5 million to replace obsolete and misoperating relay equipment at its Doubs, Ringgold, Lime Kiln and Montgomery 230-kV substations in the APS zone. The work is in the engineering phase, with an estimated in-service date of Oct. 31, 2026, for Lime Kiln and Montgomery and Dec. 31, 2026, for Doubs and Ringgold.

Dominion presented a $180 million project to address reliability violations along its Fredericksburg-Possum Point 230-kV line, as 3 GW of load is expected to come online served by 13 new substations along its length.

A new Allman switching station would be built north of the Fredericksburg substation, with 10 230-kV line terminals in a breaker-and-a-half configuration. It would cut into 230-kV lines between Fredericksburg and the Cranes Corner, Aquia Harbour and Birchwood substations

About 4.5 miles of the line from Allman to Cranes Corner and 0.7 miles of line from Allman to Hospital Junction would be rebuilt with double circuit structures. The Cranes Corner substation would be expanded to support line realignment. The line to Aquia Harbour would be upgraded to double circuit and rebuilt with vacant arm positions to host two additional 230-kV lines to run from Allman, past Aquia and onto Possum Point on a new 7.1-mile double circuit pole line.

The project is in the conceptual phase, with a possible in-service date of June 1, 2029.

Dominion also presented a $30 million project to power a data center customer in Stafford, Va., with a projected summer 2029 load of 136 MW. A new Centreport switching station in a four-breaker ring bus configuration would be cut into the Spartan-Cranes Corner line with 2.5 miles of new double circuit line.