Two proposed wind farms off the New England coast are nearing approval by federal regulators.

The U.S. Bureau of Ocean Energy Management on Feb. 26 announced it had finalized the environmental impact analysis of New England Wind.

Publication of a project’s final environmental impact statement (EIS) typically is followed several weeks later by a record of decision. All six of the decisions BOEM has issued so far have been approvals.

In this case, the EIS is for two wind farms proposed by Avangrid within the 101,590-acre Lease OCS-A 0534: Park City Wind and Commonwealth Wind, neither of which currently has an offtake contract for their combined potential output of more than 2 GW.

Avangrid terminated its power purchase agreements for both projects in 2023 when their terms became financially untenable amid rising construction costs. (See Avangrid Avoids Major Offshore Wind Losses.)

Avangrid has said it still plans to develop the projects, but under profitable terms. There is a chance to pursue this now: Connecticut, Massachusetts and Rhode Island remain eager to decarbonize their grids and are holding a combined offshore wind solicitation for up to 6 GW of capacity, with bids due March 27. (See New England States Delay Offshore Wind Solicitations.)

BOEM published a draft EIS in December 2022 and received 776 public comments in response. It considered multiple scenarios within the final EIS before choosing as the preferred alternative a version of the original plan modified to minimize impacts on complex fisheries habitats.

There is minimal operational data in U.S. waters from which the environmental impact of a given offshore wind proposal can be estimated. The first two utility-scale projects still are under construction.

As with the assessments BOEM has carried out for other proposed wind farms in the New York-New England region, the New England Wind EIS presents a range of possible outcomes good and bad for each assessment category.

Most effects are assessed as minor to moderate beneficial or harmful.

However, the critically endangered North Atlantic right whale; commercial and for-hire recreational fishing; cultural resources; scientific research and surveys; the view from land; and national security and military uses could see “major” negative impacts from New England Wind under BOEM’s preferred scenario, particularly in combination with other underwater energy activities in the region.

One of the EIS appendices indicates an increased potential threat to whales and other marine mammals from vessel strikes and fishing gear entanglement. (See Feds Issue Strategy to Protect Right Whale Amid OSW Push.) This and some of the other effects are potentially “irretrievable.”

But BOEM concludes the majority of marine and onshore environments would return to normal long-term productivity upon decommissioning.

The predicted impacts of the status quo — continued greenhouse gas emissions from fossil power generation, and the resulting climate effects — are judged to be almost as significant in their own way as the potential impacts from construction and operation of New England Wind, an emissions-free power source.

The record of decision is the next milestone for New England and one of the biggest, along with securing contracts for its electricity. Additional reviews and approvals must be secured before construction can start, but a positive record of decision essentially is a green light for a project.

BOEM said in its announcement of the EIS that the record of decision would come in April or later.

Phase 1 of New England Wind is Park City Wind, with one or two offshore substations and up to 62 turbines with combined capacity of at least 804 MW coming online as soon as 2028.

Phase 2 would be Commonwealth Wind, with one to three offshore substations and up to 88 turbines rated at 1,232 to 1,725 MW; full buildout would be dependent on market conditions and offshore wind turbine technology advancement.

In an adjacent lease area, Avangrid and Copenhagen Infrastructure Partners are building Vineyard Wind 1 in a 50-50 joint venture.

WASHINGTON, D.C. ― The year 2023 was record-breaking for sustainable energy in the U.S., according to the Business Council for Sustainable Energy’s 2024 Sustainable Energy Factbook.

Renewables, EVs and the grid, among others, attracted a “record-shattering” $303.3 billion in private investment, while 42 GW of wind, solar and storage were added to the grid and more than 1.4 million new EVs hit the road, the factbook reports.

The challenge is maintaining and then accelerating such levels of growth, said Tom Rowlands-Rees, North America head of research for BloombergNEF, which compiled the factbook’s 69 pages of graphs and charts. Looking at clean energy investments on a global scale, “every country that we tracked, except Japan” had a record-breaking year, Rowlands-Rees said at a press briefing Feb. 20.

Now in its 11th edition, the factbook tracks a U.S. energy transition that is, as advocates like to say, hardwired into the economy but still facing uneven financial and political terrain. The momentum created by the billions of dollars in incentives and tax credits in the Infrastructure Investment and Jobs Act and the Inflation Reduction Act has been tempered by supply chain constraints and the effects of inflation.

High interest rates can have a significant impact on renewable energy projects “because they are [capital expense] heavy compared to alternatives like gas, where so much of the cost is in the fuel itself,” Rowlands-Rees said.

Permitting and interconnection bottlenecks also continue to slow solar, wind and storage deployments. According to the factbook, utility spending on transmission hit a record $30 billion in 2023, but estimates suggest it could remain flat for two more years.

Corporate Contracts and LCOE

Corporate contracts for renewable energy ― a major growth driver ― are also feeling the pinch, falling 15%, from 20.2 GW in 2022 to 17.1 GW in 2023, the first year since 2017 with fewer than 100 deals.

Perhaps the biggest red flag is the levelized cost of electricity ― the all-in, lifetime cost for specific types of generation ― calculated without the IIJA or IRA’s tax credits and other incentives. For the first time since 2017, the LCOE for natural gas is lower than either wind or solar.

Rowlands-Rees sees LCOE as a benchmark of economic competitiveness, underlining the critical role of federal support.

With wind and solar tax credits, renewables “come out substantially cheaper than the alternatives,” he said. But wind and solar won’t “magically” overcome other issues if they are not sitting well economically.

Renewable capacity contracted by corporations (annual and cumulative GW) | BloombergNEF

Emissions and Productivity

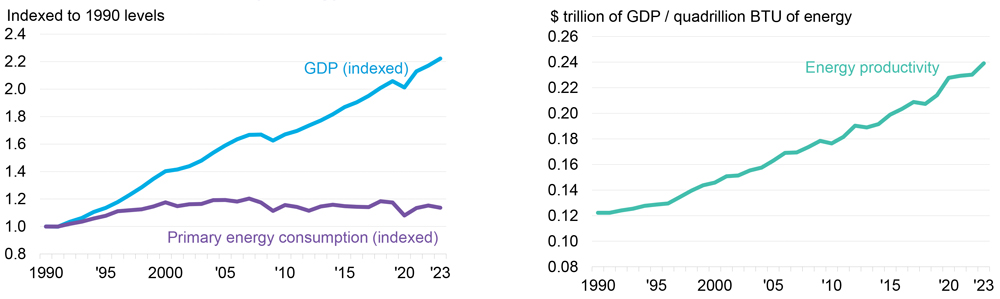

U.S. “energy productivity” has long been a key indicator in the factbook, and since 1990, it has risen steadily as gross domestic product increased while energy consumption stayed relatively flat.

In 2023, GDP was up 2.4%, while energy consumption dropped 1.4%, producing a 4% increase in energy productivity, the factbook says.

These numbers demonstrate “very simply that economic growth and energy consumption are not tied together at the hip,” Rowlands-Rees said. “You can have a thriving economy without a huge growth in energy consumption.”

At the same time, U.S. greenhouse gas emissions dipped 1.8%, signaling a possible downturn following the post-COVID rebound in energy consumption and emissions. The country still must slash emissions to reach its commitment under the 2015 Paris climate accords ― a 50-52% drop in emissions below 2005 levels by 2030 and net zero by 2050 ― but the downward turn is a step in the right direction.

The challenge is that clean energy investments aren’t completely aligned with the main sources of emissions, Rowlands-Rees said. While power, the grid and transportation are the top targets for private investment, industrial emissions now are the second largest source of U.S. GHGs. What’s needed is “to kickstart more investment in reducing industrial emissions,” he said.

U.S. GDP (real) and energy consumption, indexed to 1990 levels | BloombergNEF

Solar

Also speaking at the Feb. 20 briefing, Justin Baca, vice president for markets and research at the Solar Energy Industries Association, pointed to a mismatch between supply chain investments and needs in the solar sector.

The industry is racing to build out a U.S. supply chain to meet domestic content provisions in the IRA and to blunt the June 2024 end of President Biden’s two-year moratorium on tariffs on solar cells and panels from Cambodia, Malaysia, Thailand and Vietnam. The Commerce Department finalized its decisionon the tariffs in August 2023, finding that solar companies in those countries were using Chinese components already subject to tariffs.

While announcements for 34 solar manufacturing projects have been made since passage of the IRA, Baca said, “we have seen over 100 MW worth of solar module factory announcements, then closer to 50 for solar cell [factories] and closer to 20 for solar wafer[s].

“[That] means the further you go up the supply chain … we’re getting more and more constrained,” in an imbalance, he said, that “creates an opportunity for supply chain bottlenecks.”

The supply chain for high-voltage power transformers ― used to step power up and down on the grid ― is equally problematic, Baca said. Worldwide, only a few factories produce this critical equipment, “and we have back orders of about two years,” he said.

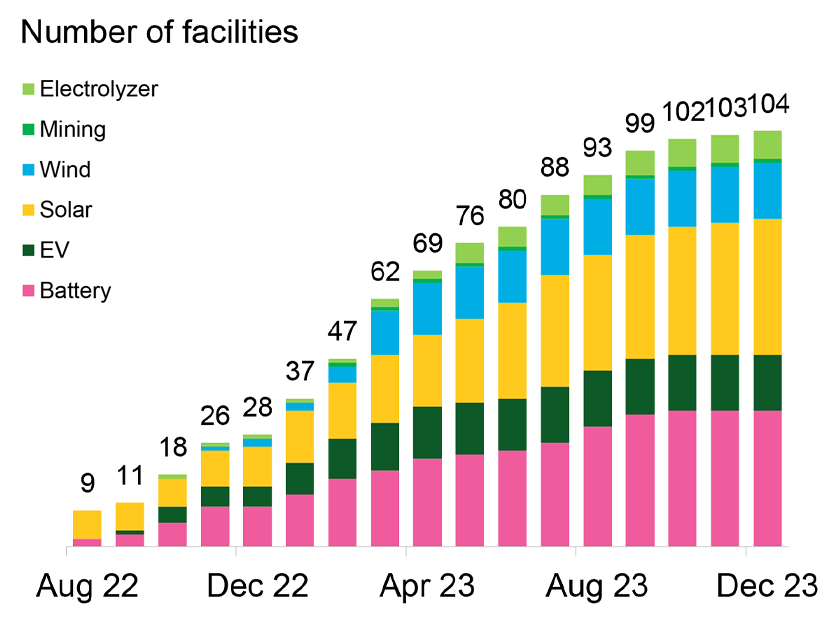

Clean-tech manufacturing investments announcements post-IRA (number of facilities) | BloombergNEF

Energy Efficiency

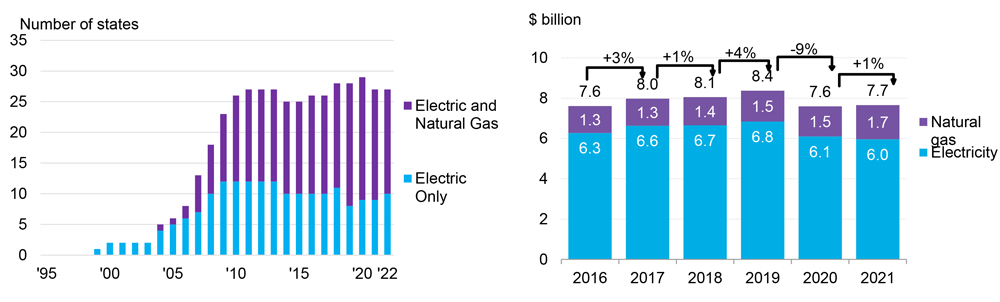

Energy efficiency is another example of potential misalignment of investments. The factbook shows that, as of 2022, more than 25 states have enacted energy efficiency resource standards, for electricity only or for electricity and gas.

But, as of 2021, the most recent figures available, utility investments in energy efficiency had yet to recover from their pandemic drop, from $8.4 billion in 2019 to $7.7 billion in 2021.

The U.S. is one of the 130 nationsthat committed to tripling renewable energy and doubling energy efficiency by 2030 at the United Nations 28th Climate Conference of the Parties in the United Arab Emirates in December 2023. That commitment means energy efficiency must be thought of as a “first fuel, not a secondary thing,” said Paula Glover, president of the Alliance to Save Energy.

Efficiency is vital to keep the curve on energy productivity going up, Glover said. “The more we grow our economy, the more energy we are going to need.” Energy efficiency can mean “less to build and displaces additional demand.”

Referring to the factbook’s energy productivity chart, Glover asked, “What would happen if we actually doubled efficiency? … What would it do to the energy productivity? What would that graph look like?”

Utility energy efficiency spending (in $ billion) | BloombergNEF

Natural Gas and Carbon Capture

Perhaps one of the greatest challenges for clean energy advocates is the role of natural gas in the U.S. energy transition. While coal-fired generation provided less than 16% of U.S. electricity generation in 2023, it has been replaced primarily by natural gas, which now accounts for 43%, up from 40% in 2022.

Overall, power sector and liquid natural gas exports are driving demand, Rowlands-Rees said.

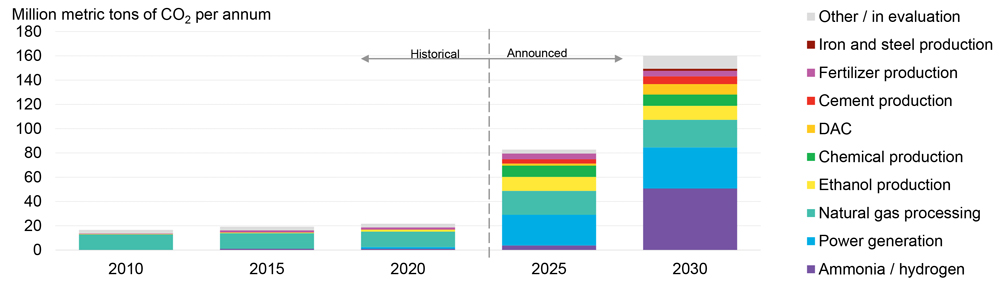

BloombergNEF anticipates that carbon capture, utilization and storage may become a growing factor in both natural gas processing and power generation, again supported by incentives from the IRA, specifically, the 45Q tax credit for carbon and direct air capture.

Carbon capture capacity is set to explode from around 23 million metric tons of CO2 per year in 2020 to 160 MMT per year by 2030 in projects announced. Natural gas processing and power generation could account for more than a quarter of that growth.

But the factbook cautions that, like solar and wind, permitting and other delays could slow growth.

Historical and proposed carbon capture capacity in the U.S. (CO2 MMT per year) | BloombergNEF

EV Tax Credits

Rowlands-Rees downplayed recent negative headlines about EV sales, noting the U.S. has had three record years in a row, and “these are not just record years by a small margin. It’s very substantial,” he said.

Another encouraging sign is that 2023 saw Tesla’s market dominance slip as other automakers introduced more EV models.

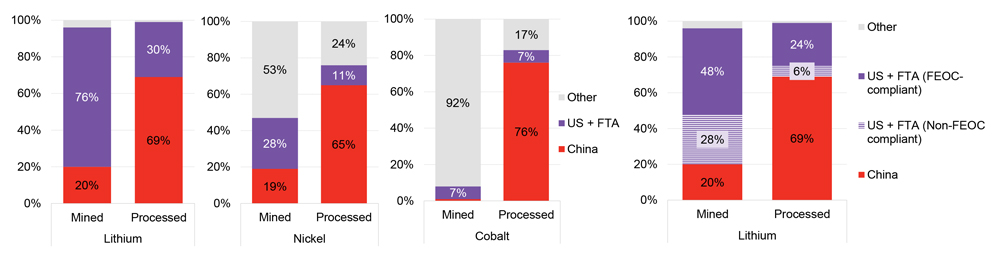

But new Treasury Department rules issued in December have cut the number of EV models that now qualify for the IRA’s top $7,500 tax credit. The new rules terminate tax credits for lithium and other materials mined or processed in China or other “foreign entities of concern” (FEOCs). The factbook shows that only about a quarter of lithium processed will meet the new requirements, with even smaller percentages for nickel (11%) and cobalt (7%).

Share of battery metal supply (left) and lithium supply (right) by location in 2023. | BloombergNEF

The Election

The very large elephant in the room (pun intended) at the briefing is what will happen if Republicans take back the White House and both houses of Congress in the upcoming election, now just over 10 months away.

Former President Donald Trump, the all-but-certain GOP presidential candidate, did all he could to slow the growth of clean energy in his previous term, withdrawing the U.S. from the Paris Agreement and rolling back environmental and emission-reduction measures.

Some Republicans in Congress have called for the repeal of the IRA.

Lisa Jacobson, BCSE president, argues that multiple factors are driving the U.S. energy transition ― customer demand, supportive policy, digitization of the power system, and the growing interest and engagement in communities on being able to make choices about their energy supply and services.

“No one knows where we’ll be a year from now in terms of the makeup of our federal government,” Jacobson said. “But I feel very strongly these [clean energy] investments will go forward … because this is what people and communities want, and we have the technology available to offer improved, modern, efficient and better energy services.”

Other speakers pointed to the flow of IRA dollars into rural areas, red states and Republican-held congressional districts.

According to John Hensley, vice president for markets and policy analysis at the American Clean Power Association, “for the projects we’re tracking at ACP, 80% of those are located in congressional districts that are currently held by Republican representatives. So, there are a lot of reasons to be supportive of these policies, to embrace the investment, the job creation and the economic development benefits they’re bringing.”

CAISO staff and stakeholders are looking to address an inconsistency in how the ISO tests for structural market competitiveness inside and outside of its balancing authority area in the Western Energy Imbalance Market.

The issue was a topic of discussion at a Feb. 21 meeting of the ISO’s Price Formation Enhancements Working Group.

CAISO’s BAA-level Dynamic Competitive Path Assessment (DCPA), which is used to test for structural competitiveness and determine the need for market power mitigation, tests BAAs in isolation and does not consider external supply, ISO staff noted at the meeting.

But within its own BAA, CAISO does consider external supply, creating conditions that could make it easier for the ISO to pass the DCPA and avoid price mitigation.

To address the problem, the ISO has suggested grouping BAAs that are otherwise separated by price differences and testing them together, instead of testing them in isolation and looking only at internal supply relative to internal demand.

“The impact of this problem in the market is that balancing areas in the Western EIM may fail the DCPA, which is the market power mitigation test, more frequently than their actual competitiveness justified, subjecting them to mitigation too often,” said James Friedrich, lead policy developer at CAISO.

However, some stakeholders were concerned that the grouping method would apply the DCPA to two different types of market power — local and BAA-wide.

“It’s almost in our minds like you’re taking aspects of a local market power mitigation test and especially that triggering mechanism and trying to apply it to a BAA-level or system market power condition,” said Kallie Wells, senior consultant at Gridwell Consulting.

Responding to stakeholder concerns about the grouping methodology, Friedrich said he didn’t see a difference between local and BAA-level market power.

“You could define a balancing area as a local area that’s congested from the larger market and the larger system and all of the suppliers within that local area can potentially exert market power. … That’s what the test is for,” he said. “I don’t see why we would have a differentiation between local market power identifying price separated local areas and BAA-level market power. It’s just that the area with which you’re defining is a balancing area and not a single node on the system or a collection of nodes.”

Wells elaborated on stakeholder concerns regarding the differentiation of markets, saying it comes down to demand.

“The demand number that you’re using and that test to figure out if you should actually mitigate resources is different. So, in local market power, that demand is the counterflow,” she said. “But that’s not what you’re using in the BAA-level calculation. … You’re saying we’re going to take this binding transfer constraint as the trigger, and then instead of using the demand for counterflow on that transfer constraint, we’re actually just going to use the demand in the BAA-level area.”

Friedrich said Wells’ explanation helped him think about the issue differently, but that he’d need time to consider how to respond.

DMM Data Demonstrate DCPA Problems

In November, CAISO’s Department of Market Monitoring presented data breaking down how often WEIM BAAs are subject to mitigation and, within that subset, how many times their resources had bids altered.

The data revealed another issue: that because the existing BAA-level market power mitigation uses a transfer constraint-based trigger to test for structural uncompetitiveness, mitigation occurred most frequently in hours inconsistent with when one would expect to need to test, such as in times of high renewable and low load conditions.

“I think because of the mixing and matching of the trigger and the test or the type of market power you’re trying to address, you’re actually seeing that issue pop up in your results,” Wells said.

Dan Williams, principal adviser at The Energy Authority, suggested the ISO examine how transfer constraints materialized for WEIM entities that were using transmission rights to export from the CAISO or another area into their BAA to examine how it affects market power mitigation.

The Price Formation Enhancements Working Group is scheduled to meet again March 18. CAISO also plans to publish an FAQ to address stakeholder questions on issues arising during the Feb. 21 meeting.

VALLEY FORGE, Pa. — A group of demand response providers in PJM proposed adding two hours to the availability window that binds when the resource can be deployed by the RTO at the Markets and Reliability Committee meeting Feb. 22, arguing the current structure may be unfairly limiting DR participation in the capacity market.

The availability window currently confines DR dispatch to between 6 a.m. through 9 p.m. during the winter, which would be expanded to 11 p.m. under the proposal. The summertime availability window of 10 a.m. through 10 p.m. would remain unchanged.

Bruce Campbell of Campbell Energy Advisors said PJM’s assessment of winter risk has changed over the past decade and that there is untapped potential for load to contribute to meeting increased reliability risks identified in winter evenings. The shortcomings of the availability window, Campbell said, were highlighted by the revised risk modeling approach that was proposed out of PJM’s Critical Issue Fast Path (CIFP) process and approved by FERC in January. He argued that limiting DR participation when it can perform could violate FERC Order 719.

The changes were proposed under PJM’s “quick-fix” process, which allows a problem statement, issue charge and solution to be considered concurrently. Campbell said the expedited process is being sought to allow the changes to be in place prior to the commencement of the 2025/26 Base Residual Auction. The proposal is sponsored by CPower, Enel North America, the PJM Industrial Customer Coalition (ICC), NRG Solutions and the Advanced Energy Management Alliance.

Susan Bruce of the PJM ICC said the magnitude of the drop in the effective load-carrying capability (ELCC) class rating for DR following the CIFP changes came as a surprise for industrial participants, some of whom may rethink whether it remains a fit for them. She argued that the diminished ELCC rating, which is a major input in determining resource accreditation, sends market signals that DR’s reliability contributions aren’t needed at a time when PJM staff are sounding long-term resource adequacy concerns. Values that PJM presented during a Feb. 21 Planning Committee meeting showed DR’s ELCC rating going from 95% to 77%.

Manuel Esquivel, Enel’s manager of RTO affairs for the PJM region, said the proposal is not trying to reverse the RTO’s ELCC class ratings after the results have been published. Rather, it is meant to correct an issue that was raised throughout the CIFP process, including during stakeholder deliberations, in communications with the PJM Board of Managers and in comments to FERC on the filings.

Calpine’s David “Scarp” Scarpignato said market changes affecting the ELCC values for one generation class would likely lead to changes for all resources, and with the auction months away, participants need certainty about their assets’ accreditation.

Adam Keech, PJM vice president of market design and economics, said that when the reliability contribution of one resource changes for a single season, the balance risk between summer and winter will shift. Any other resource types that have stronger performance in one season would then see a change in their annual accreditation as their ability to match the risks on the grid varies.

The issue charge also includes a third phase — following education and increasing winter availability — to explore either creating a DR product without an availability window or eliminating it for all DR.

Campbell said there were some discussions about proposing shifting DR to be committable all day, but some providers were concerned about the number of customers that may not have load that can be curtailed at night.

Other MRC Business

PJM’s Zhenyu Fan presented a quick-fix proposal to revise Manual 11 to reflect existing practices for interface pricing points, a mechanism that groups buses together when calculating LMPs for energy imports to, or exports from, external areas. The revisions also would include a recommendation from the Independent Market Monitor to align manual language to reflect the tariff requirement that PJM monitor interfaces at least annually. Fan said the most recent analysis does not suggest that any changes to interface weighing is required.

PJM’s Michele Greening presented proposed revisions to the RTO’s tariff and Operating Agreement endorsed by the Governing Document Enhancement and Clarification Subcommittee (GDECS) mainly focused on clarifications and corrections. But several stakeholders said the recommended changes appeared to be more substantial than they believe is appropriate to implement through the GDECS process. Language that failed to receive unanimous support at the subcommittee include definitions relating to generation interconnection requests and the storage component of hybrid resources.

Members Committee

TOs Considering Handing PJM Transmission Planning Filing Rights

The Transmission Owners Agreement-Administrative Committee (TOA-AC) is considering revising the Consolidated Transmission Owners Agreement (CTOA) to move filing authority over transmission planning from the Operating Agreement to the tariff, which would grant PJM the unilateral right to bring planning matters to FERC.

Ratification of the changes would require agreement of the transmission owners and the PJM Board of Managers.

The proposed revisions also would establish a dispute resolution process under which TOs first would attempt to resolve disputes through meetings with PJM or the board and initiating a nonbinding mediation process overseen by an alternate dispute resolution coordinator if talks were unsuccessful. The mediation process would be followed by regulatory or judicial resolution if necessary.

Presenting the proposal to the Members Committee, Exelon Director of RTO Relations Alex Stern said allowing PJM to make planning-related filings as it sees necessary would bolster the independence of the board, increase PJM’s flexibility in reacting to needs it identifies and facilitate its goals in implementing long-term planning. He said the intent is for PJM to have independent planning authority, with stakeholders providing input. All other RTOs have comparable filing rights, he said.

An example of the type of initiative PJM could undertake with the new authority, Stern said, would be proactively creating a process to plan and construct transmission in support of offshore wind.

Steve Nadel of PPL said it’s highly irregular for the stakeholders to have filing rights under Federal Power Act Section 205 over planning.

“By restoring filing rights to the utility, which is PJM, no one would lose any rightly granted authority,” he said. “This is designed and intended to be a restoration of the correct allocation of authority.”

Reading the unanimous comments of the Organization of PJM States Inc., President Kent Chandler, also chair of the Kentucky Public Service Commission, said the revisions appear overly broad and asked the PJM board to wait until the end of March before making any decision on agreeing to the changes to allow stakeholders to provide fully informed comments.

Speaking for himself, Chandler said the changes would erode the board’s independence, allow TOs to build more costly projects over more efficient routes and would not benefit consumers.

Referencing a provision that would institute an annual meeting between PJM and the CTOA parties to discuss the agreement, the PJM ICC’s Bruce said TOs may retain higher access to the RTO to sway how it uses the proposed filing rights even if all stakeholders are on the same advisory footing under the language.

“We’re not getting the same access, if you will, between PJM and the transmission owners. … We will not have, for example, a state of the union, if you will, meeting,” Bruce said.

While she said consumers often want to see PJM take a more authoritative stance, Bruce said she’s concerned that granting PJM sole Section 205 filing authority could make investors wary of the RTO, as they could lose some control over assets at the intersection of planning and markets.

Vitol’s Jason Barker asked how it can be ensured that proper stakeholder deliberation is held when planning and markets overlap, to which Stern said PJM would have to use the added authority responsibly. Stern acknowledged there is concern associated with affording PJM greater independence from all stakeholders, including TOs. However, the TOs believe those concerns are outweighed by the benefits, Stern said.

John Horstmann, senior director of RTO affairs for Dayton Light and Power, said the TOA-AC is scheduled to discuss the proposal March 15 and could vote on approval that day. He said the CTOA is an agreement between PJM and member TOs, making approval an issue to be decided by the board and TOA-AC rather than the MC.

Jackie Roberts, federal policy adviser to the West Virginia Public Service Commission, questioned the pace of considering approval in the next month and urged the TOs to give members and state commissions more time to understand the implications of the changes.

“I have heard no reason why this is a hair-on-fire must-do-right-now proposal,” she said.

Board Chair Mark Takahashi said he sees value in expanding PJM’s filing rights, speaking as an individual board member, but the board has not considered the details of the proposal yet. He said the board will meet Feb. 28 to discuss it further, adding it will not be rushing to a decision.

“There’s a lot to do here with planning and we really want to work with stakeholders and members,” he said.

The proposed amendments were brought by the American Electric Power Service Corp., AES Ohio, Exelon Corp. and PPL Electric Utilities Corp. In a letter to the TOA-AC, the TOs argued that granting PJM filing authority over planning would give it the independence needed to face new challenges.

“The sponsors also recognize points expressed by PJM states and stakeholders that PJM is too reactive and not able to advance important regional transmission planning reforms. The timing is right to refresh the CTOA to best position PJM, and the region, to meet the challenges of today and tomorrow. These revisions enhance PJM’s independence to conduct regional transmission planning within its existing scope of responsibilities and place PJM on similar footing with other RTOs,” they wrote.

“It is critical that PJM has every tool at its disposal,” Stern said. “With generation deactivations accelerating, energy demands increasing and a portfolio of new generation waiting to interconnect, PJM’s ability to ensure future reliability and affordability for customers is critical and would be enhanced by PJM having Federal Power Act Section 205 rights over the transmission planning protocol.”

SACRAMENTO, Calif. — Construction of the floating offshore wind projects envisioned for the West Coast will require a much more robust supply chain and system of ports, according to industry officials speaking at Oceantic Network’s Floating Offshore Wind Port and Vessel Summit on Feb. 22.

Events of the past year have illuminated the challenges to developing offshore wind (OSW) projects in the U.S., including the need for a stronger supply chain, a greater network of ports and a timelier source of funding from both the public and private sectors. (See Offshore Wind Reset Complete in New York.)

U.S. demand for OSW is growing. Oceantic’s 2024 U.S. Offshore Wind Market Report projects that states will have secured contracts for 20 to 25GW of OSW generation by 2025, growing from 17.6 GW in 2023. And Oceantic CEO Liz Burdock said states could award as much as 15.5 GW of new capacity by December.

But offshore wind developers, port officials and vessel builders will have to address some of the big challenges in building a cost-effective market for offshore wind to meet those goals.

“Obviously, last year, 2023, we experienced some challenges, but we have really risen to meet those challenges. … And I say we collectively, the states and the industry, have come together to create better, smarter, stronger markets for decades to come,” Burdock said.

Inflation and tightening supply chains in 2023 led to the cancellation of offshore wind projects; developers terminated 51% of power contracts in place prior to 2023, including the Empire Wind II, Skipjack and Beacon Wind projects on the East Coast, the report says.

Offtake agreement cancellations substantially impacted supply chain development, causing project delays that left the nation’s 30 GW of clean power by 2030 out of reach.

“With manufacturing investments largely tied to singular projects, the reorganization of the power offtake market nearly froze the development of the supply chain, simultaneously facing skyrocketing inflation and material supply costs,” the report reads. “Factories announced as part of procurements in 2020 and 2021 largely remain in the planning stage. And while there were significant announcements, including a $1 billion investment in a new blade and nacelle facility in New York, on the aggregate, new supply chain investments for manufacturing, ports and vessels slowed modestly in 2023.”

Industry officials at the summit largely grappled with how to address the supply chain issues and develop the ports and vessels needed to advance the state’s expected demand for FOSW.

Supply Chain Issues

John Begala, Oceantic vice president for federal and state policy, highlighted the need for a robust national supply chain.

“What the East Coast has taught us, especially with the cancellation of projects, is that over-reliance on a global supply chain is going to be a challenge,” Begala said during a panel discussion.

“We are not the only country pushing for offshore wind. What I think we need to think about to be successful on the West Coast is to ensure that we create a national and — don’t yell at me — not purely localized multifaceted backbone to support our offshore wind industry. We definitely need to support local interests, but this should be a national effort.”

But Darren McQuillan, who works in global business development at Bardex, which builds ship lifts and mooring technologies, said the supply chain should move to support 100% “local content” built from the bottom up.

McQuillan also noted that lack of standardization coupled with the sheer number of different technologies for offshore wind platforms — around 85, he said — has stalled supply chain development.

Greater standardization requires the identification of common components for offshore wind technologies. While there are three different types of floating platforms — spar buoy, semisubmersible and the tensioned-legs platform (TLP) — they can be developed with the same common components, such as columns and trusses. But the market is “nowhere near standardization,” he said.

“If we’re ever going to make the targets that we want to make by 2030, 2045, we can’t let technology wag the dog,” he said. “As long as technology is wagging the dog, supply chain ends up being a bespoke execution model, and if supply chain locally ends up being a bespoke execution model, of course it’s going to be expensive because they have to constantly retool and change to meet the technology requirement. What that does is it forces the work overseas,” he said.

Begala announced a new Oceantic initiative, the West Coast Supplier Council, which will bring together companies on the front lines of the supply chain, such as equipment manufacturers and construction firms.

“These businesses will serve as the backbone for delivering on that supply chain and create the workforce for offshore wind development,” he said.

Ports and Vessels

An “ecosystem of ports” needs to be developed to support the installation and implementation of floating offshore wind, including staging and integration ports and those that support large vessels, said Michael Magri Overend, senior project manager for Atlas Wind, Equinor’s California FOSW project.

And Jack Haynie, offshore wind and renewables lead at Baird, said the company thinks nearly 100 ports should be built to support the amount of infrastructure needed for the U.S. offshore wind industry, and they’re concerned about where the funding will come from and how quickly.

The Port of Long Beach is leading the way in preparing for offshore wind development. In May, port officials released plans to develop Pier Wind to support the manufacture and assembly of offshore wind turbines; it would be the largest facility at any U.S. seaport specifically designed for these efforts. But planners are asking for financial help from the federal government to support such an ambitious facility.

“We will absolutely bring a significant amount of capital contribution to the development, probably larger than any other port in the nation has done, but in relative value to pure wind cost, it’s not enough,” said Suzanne Plezia, chief harbor engineer at the port.

Plezia is seeking ways to make offshore wind projects “bankable” to avoid the volatile financial patterns of the past.

“How do we de-risk these projects?” she said. “There are smart ways to use public dollars, maybe not just as subsidies, but as a de-risking mechanism, whether it’s a loss reserve or some sort of first-loss position or basic synthetic insurance policy where if you build it and for reasons that are outside of your control demand doesn’t come, then somebody can help absorb that variability.”

Panelists also identified the need for larger vessels that can transport components offshore, which presents another need for significant funding.

During his time as a California assemblymember, San Francisco City Attorney David Chiu authored AB 525, the bill directing the California Energy Commission to study floating offshore wind. Despite the challenges facing the industry, Chiu emphasized the importance of FOSW, highlighting that the state could generate enough energy to power its entire grid with resources located just 20 to 30 miles off the coast.

“Of the 200 or so laws that I have authored in California and in my city of San Francisco, AB 525 from my perspective might be the most impactful thing I was honored to be a part of,” he said. “Every aspect of the state of California should be a part of this.”

And while 2023 was both productive and tumultuous for wind energy, Burdock is confident the market is transforming to support actual implementation of FOSW.

“We’re moving from concepts and pilot projects to commercial development,” she said. “Gone are the days of hypotheticals.”

FERC on Feb. 26 accepted PJM’s request to delay the 2025/26 Base Residual Auction (BRA) from June 12 to July 17 to give stakeholders time to understand new capacity auction rules (ER24-1242).

The commission said PJM acted in good faith and that the request was limited in scope, as it was for the specific purpose of educating market participants on changes to how the RTO will calculate effective load-carrying capability (ELCC) ratings, approved by FERC in January. (See PJM Seeks Waiver to Postpone 2025/26 Capacity Auction.)

“Granting the waiver addresses a concrete problem because it will allow sellers to better understand the implementation of the new ELCC values and modeling methodologies before they are required to submit unit-specific offer caps,” FERC said. “We find that granting the waiver request will not have undesirable consequences, such as harming third parties, because it is a limited to a short delay of one BRA and will facilitate an orderly administration of the auction.”

The commission approved changes to PJM’s risk modeling and accreditation in January but denied a second proposal to revise components of the market seller offer cap in early February. PJM’s Planning Committee has held two special sessions to discuss the changes this month and presented updated class ratings that varied as much as 20% for some resources from preliminary figures shown last year. (See FERC Rejects Changes to PJM Capacity Performance Penalties.)

In comments supporting the delay, LS Power Development argued 35 days is the minimum market participants would need to understand the impact of the new approach to accrediting resources. The company noted it had asked the commission to delay implementation of the ELCC changes to the 2026/27 auction, scheduled for December 2024, because of the tight time frame between PJM’s proposals and the start of preauction activities for the 2025/26 auction.

It also said it “was especially concerned that PJM had released few details of its ELCC methodology to stakeholders and had provided very little information regarding the accredited [capacity values] that would result from the application of that new methodology. LSP Development’s concerns became increasingly pressing as preauction deadlines approached and PJM still had not released necessary information for market participants to make informed business decisions regarding participation in the 2025/2026 BRA.”

Stakeholders also need time to verify the results PJM has presented, LS Power said. The RTO has arrived at “noticeably different” accredited unforced capacity values for two resources located at the same site and with similar characteristics, but members have not received explanation for the reason, it said. “Not only does PJM need to provide ‘additional education,’ but market participants must also have the opportunity to review the underlying data so that any errors in PJM’s accreditation determinations may be corrected.”

The PJM Power Providers Group also submitted comments in support of the delay, arguing the need to ensure accurate accreditation values warrants a delay.

PSEG is urging the U.S. Treasury Department to speedily release rules for the program that could provide Production Tax Credits to support the utility’s three South Jersey nuclear plants, but the effort has yet to yield results, CFO Daniel J. Cregg said in the company’s fourth-quarter earnings call Feb. 26.

Cregg said the utility last spoke two months ago to Treasury officials about the PTC program; it is part of the Inflation Reduction Act, and it awards tax credits of up to $15/mWh for electricity produced by existing nuclear plants. PSEG is the sole owner and operator of the Hope Creek plant and the operator and majority co-owner of Salem 1 and Salem 2 plants.

“We made them aware, as we do every time that we can, that it’s important for them to try to get the rules out sooner rather than later,” Cregg said, referring to Treasury officials. “But as we sit here today, they have not issued a date by which they will provide that guidance. So we are just awaiting their answer.” He said his team nevertheless has “done a lot of work” trying to prepare for the different scenarios so the utility is ready when they’re released.

The utility on Nov. 22 told the New Jersey Board of Public Utilities (BPU) it would withdraw from the state’s Zero Emission Certificate (ZEC) program, which since 2019 has awarded PSEG $300 million a year to ensure its three plants remain operating to help the state meet its clean energy goals. (See NJ Closes Nuclear Subsidy Process as PSEG Looks to Feds.) PSEG said it withdrew to “preserve PSEG’s rights” to federal tax credits.

CEO Ralph LaRossa, responding to a question on the call, said knowing the framework of the tax credits will help shape the utility’s decision-making on economic development plans for the plants. “The PTC rules need to come out, and once all of that comes together, we’ll be able to look at a plan, optimize the revenues from those plants,” he said.

Shifting Customer Use

LaRossa said company initiatives over the past 12 months have aligned with New Jersey’s goals of cutting gas use by 0.75% and electricity use by 2%.

A key element of the effort was PSEG’s $3.1 billion energy efficiency investment program filed with the BPU in December, which, if approved, would run from January 2025 to June 2027. In a second key component of the effort, LaRossa said, the utility in November requested an extension of the current energy efficiency program, which would cost $300 million and run from July 2023 to December.

“Our [energy efficiency] programs continue to create value by lowering customer bills, reducing energy use and emissions, and providing shareholders with a return of, and on, the energy efficiency spending,” he said.

LaRossa added the utility is “proposing new time-of-use rates that will allow customers to save on their bills by shifting usage to off-peak periods, a rate option that can benefit all customers, incentivizing residential customers to charge their electric vehicles during these off-peak hours.” The utility provided no further specifics on the strategy.

PSEG’s fourth-quarter results for 2023 fell short of those in 2022, but the full-year results improved on 2022. The company reported fourth quarter 2023 net income of $546 million ($1.10/share), compared with $788 million ($1.58/share). Non-GAAP operating earnings were $271 million ($0.54/share), compared with $318 million ($0.64/share) in the same period in 2022.

The company reported 2023 net income of $2.563 billion ($5.13/share), up from $1.031 billion ($2.06/share) in 2022. Non-GAAP operating earnings in 2023 were $1.742 billion ($3.48/share), compared to $1.739 billion ($3.37/share) in 2022.

Advanced Energy United has released a scorecard that ranks the seven domestic ISO/RTOs on their generator interconnection processes, finding room for improvement in every one.

Brattle Group and Grid Strategies prepared the Generator Interconnection Scorecard for AEU, as they did for a similar project on transmission planning last year. (See Transmission Report Card Grades MISO “B,” Southeast “F”.)

The scorecard, released Feb. 26, comes after FERC issued Order 2023 and is meant to help track how those and other reforms are implemented, Grid Strategies President and report co-author Rob Gramlich said in an interview. (See FERC Updates Interconnection Queue Process with Order 2023.)

“We’re hopeful that those reforms happen and further reforms get done,” Gramlich said. “And we’re hopeful that in a year or two, if and when we do this again, all of the grades will improve. But the idea was just to kind of take a snapshot at this time.”

The flawed interconnection processes have more than 2 million MW of renewable power and storage waiting to connect to the grid, said Advanced Energy United Managing Director Caitlin Marquis.

“This scorecard confirms what we know about the interconnection process, that grid managers have moved too slowly to adapt to changing market conditions, allowing the process of connecting new electricity to the transmission grid to become dysfunctional,” Marquis said. “Without urgent improvement, the U.S. grid may struggle to keep up with growing energy demands, threatening our ability to keep the lights on and reach our climate goals. Strong implementation of FERC’s recent reforms will be an important first step toward improving the interconnection process, and it’s also clear that additional reforms will be needed.”

None of the ISO/RTOs managed to get an A, but both CAISO and ERCOT got Bs, with Gramlich saying one reason they did better was that they’ve proactively planned their transmission systems to add new resources.

“That has been a little bit less of a case recently in ERCOT,” Gramlich said. “And so ERCOT used to be great from a developer perspective, but they got marked down a little bit because of a lack of transmission. Because you can connect, but there’s a lot of congestion once you connect. California has always done proactive transmission planning pretty consistently … so the grid has been prepared in advance to accommodate more generation.”

Both also scored highly on giving developers a sense of certainty, with ERCOT assigning limited costs to interconnection customers and CAISO being credited with good transparency.

No other market scored above a C- on AEU’s scorecard, which highlights the need for changes to meet rising demand from new large loads, electrification, and state policies and customer demand driving more renewables onto the grid.

“Currently, most of the regions are undergoing significant efforts to reform their interconnection practices and policies in response to stakeholder concerns and FERC Order No. 2023,” the report said. “The scorecard is not an assessment of those ongoing or recently adopted reforms that have not yet impacted the generator interconnection processes.”

The growth of wind, utility-scale solar and storage has resulted in interconnection projects popping up everywhere, Gramlich said.

“Twenty years ago, when the current rules were designed, everybody was building just gas plants,” he added. “They were large and lumpy. You could put them at the intersection of a pipeline and a transmission line. And so, the rules were designed just with one technology in mind.”

The scorecard measures six categories, the first of which is interconnection process and results, which measures an interconnection’s success rate, cost reasonableness and uncertainty. It also grades prequeue information, queue design, assumptions and criteria, availability of interconnection alternatives, and whether transmission planning takes future generation needs into account.

That final category is the only one where the graders looked at rules now in place, which have not impacted the queues yet.

Along with CAISO, MISO scored well there due to the Long-Range Transmission Planning process Tranche 1, with two other tranches being developed. None of those lines have impacted the queue yet, but interconnection customers view them favorably, as one of the benefits studied was transmission projects’ ability to bring the lowest-cost generation to market.

VALLEY FORGE, Pa. — PJM presented the Markets and Reliability Committee with an expedited proposal to revise how it measures and verifies the capacity contribution of energy efficiency (EE) resources, drawing alarm bells from market participants that the RTO is moving too fast and making changes outside the stakeholder process.

The proposed changes shown during the Feb. 22 MRC meeting would focus on how a baseline estimate of energy consumption is determined to measure the load reduction provided by an EE installation. It would require that the providers use the most recent relevant Technical Reference Manual (TRM) published within the past three years when conducting studies of current baseline load or use meter data if standards are not available or applicable. It also would have to be demonstratable that the project was initiated with the goal of wholesale market participation and the equipment being replaced was fully operational and would have continued to be in use.

EE providers also would be required to demonstrate that the installation of the more efficient technology was completed and that they had exclusive rights with end users to enter the installation into the capacity market to prevent double counting.

Pete Langbein, PJM’s manager of demand side response operations, said staff saw value in seeking improvements to the EE measurement and verification processes prior to the next Base Residual Auction, scheduled for June 2024. The proposal was brought under an issue charge at the Market Implementation Committee to broadly look at EE participation in the capacity market and consider if any changes are needed ahead of the next auction. (See “Stakeholders Begin Review of Energy Efficiency Resources,” PJM MIC Briefs: Dec. 6, 2023.)

Equipment replacements that go beyond the standards outlined in TRMs would continue to qualify as EE, but the amount of compensation they receive might change under the proposal, Langbein said.

Several stakeholders argued PJM is bypassing the stakeholder process by introducing a proposal at the MRC without first going through the typical package formation and endorsement process at the MIC. PJM first presented the changes during a Feb. 21 MIC special session.

Luke Fishback, of Affirmed Energy, said the MIC issue charge was brought in part to ensure the definition of EE resources in the manuals reflects tariff language, an effort he does not believe would be advanced by PJM’s proposal. He argued the redlines are hasty and would introduce conflicts between the manuals and governing documents.

Requiring EE providers to enter into contracts with each end user to guarantee that installations are participating in only one program would add a substantial barrier to participation, Fishback said. He agreed with PJM that it’s critical that double counting be prevented, but he said more stakeholder deliberation is needed to find a workable solution, particularly given how little time there is because contracts need to be finalized ahead of the next capacity auction.

Several market participants and state regulators, plus Independent Market Monitor Joseph Bowring, argued the language requiring that installations be dependent on capacity market revenues is unverifiable and questioned what evidence PJM would find acceptable.

Angela Fox, Affirmed Energy’s chief markets officer, said requiring end-use customer information could conflict with privacy laws and obstruct program participation.

Exelon Director of RTO Relations Alex Stern said it’s important that states be informed of the changes being recommended and how they may impact any EE programs in their states. State-sponsored programs may find they are no longer eligible for capacity market revenues, which may impact the ability to continue to offer EE benefits to low-income consumers if those programs use wholesale market revenues to offset the cost to taxpayers.

Asim Haque, PJM senior vice president of governmental and member services, said staff are scheduling a briefing with the states to discuss the changes.

Without a full stakeholder process during the formation of the proposal, CPower Senior Vice President of Regulatory and Government Affairs Ken Schisler said the changes have not been vetted by members and they are not addressing a problem that has previously been articulated. He presented a proposal built off PJM’s redlines which he argued would resolve many of the issues stakeholders identified with the changes.

The CPower proposal would eliminate the requirement that projects be tied to capacity market participation, the end-use consumer data collection language and the three-year requirement for TRMs — instead using the most recent manual.

Highlighting the challenges with PJM’s proposal, Schisler gave the example of an EE project to replace insulation in the home of an individual with a respiratory illness. He argued the dual benefits of reducing electric heating load paired with reducing health risks that may be present could make it difficult to show the causal link between the project and capacity market revenues that PJM’s language would require.

He also stated many of the TRMs in use would be deemed ineligible due to the age of their last update, which would constrain the ability to administer EE programs in many states under PJM’s proposal.

Potential participants in SPP’s Markets+ day-ahead offering endorsed another batch of tariff revisions in preparation for a March filing at FERC.

During a Markets+ Participants Executive Committee meeting Feb. 20, stakeholders approved dozens of pages of revisions related to market monitoring, state greenhouse gas emission programs and transmission usage. Assuming the entire tariff package is approved in March by the Markets+ independent panel of SPP directors and the RTO’s board, it will be submitted to FERC.

MPEC Vice Chair Brian Cole, with Arizona Public Service, praised the “amazing effort” by all involved in the tariff’s development, which began in August 2022. “To get to where we are is amazing. I know we’ve got a long way to go, but to get to a tariff filing is really great,” he said.

The various revisions were approved unanimously against some abstentions. However, a motion to endorse the updated tariff as approved by MPEC and move it to the governing process’ next step for filing at FERC drew four no votes from Western Resources Advocates, the Natural Resources Defense Council, the Sierra Club and the NW Energy Coalition.

“It’s not us saying we do not believe in Markets+,” said Kylah McNabb, speaking for the NRDC. “It’s a product that should go forward. It just needs more work before filing at FERC.”

“Procedurally, we need this vote to move it forward to [the Interim Markets+ Independent Panel],” SPP’s Carrie Simpson, director of western services development, said. “We’ve got the pieces. This is the full package. We need endorsement to get to IMIP.”

“The tariff is notably incomplete. More time is needed,” agreed WRA’s Vijay Satyal, deputy director of regional markets.

McNabb pointed to MPEC’s discussion over the remaining tariff revisions to the greenhouse gas (GHG) market’s design. PowerEx’s Mark Holman suggested language assigning resources to load was “watered down” and asked to strengthen an action item directing the Markets+ Development Working Group (MDWG) and SPP staff to evaluate tools for monitoring and tracking GHG programs.

“We’d like to strengthen it if other participants are supportive because we feel there needs to be a strong push coming out of this phase to develop the ability to attribute resources to load and have the comprehensive reporting that I think ourselves and others have envisioned,” Holman said.

MPEC approved the action item and revisions related to the assignment of resources to load and GHG market design settlements.

SPP staff is surveying Markets+ participants on WRA’s suggestion for an external market monitoring consultant over a three-year period before and after the market’s deployment and to gauge their appetite for a hybrid market monitoring option that could cost an additional $2.5 million. The advocacy group pointed to tariff language that would expand the monitoring structure to include an external adviser to SPP’s Market Monitoring Unit, given the market’s new design approach.

WRA has suggested the developmental phase of the market should include guidance on “areas of focus” by the external consultant. Satyal used a seams and joint operating agreement with CAISO’s Extended Day-Ahead Market (EDAM) as a relevant example.

“The WRA simply feels this is an insurance policy,” he said.

The IMIP meets virtually March 1. It will take up the tariff package and hear any appeals. Assuming IMIP’s approval, the tariff will be considered by the board during a March 25 conference call.

SPP is hoping for FERC approval in October or November and work to begin on Markets+’s implementation early in 2025. That would put the RTO a year behind CAISO’s EDAM, the other competing market offering in the West. The commission approved the EDAM filing in December. (See CAISO Wins (Nearly) Sweeping FERC Approval for EDAM.)

Under SPP’s current timeline, shortened by three months, Markets+ would go live before summer 2027.