In-person stakeholder meetings will resume March 1 at the earliest, and annual sectoral meetings have been pushed back a month to mid-April to allow them to proceed in person as much as possible, NYISO CEO Rich Dewey told the Management Committee on Wednesday.

“We continue to look at infection rates related to the pandemic, and we’re starting to see some declines that we’re hopeful that we’ll be able to get back in person on March 1,” Dewey said.

The sector meetings are an “exceedingly valuable” opportunity to meet with each of the individual sectors, he said, and they constitute the practical kickoff of the ISO’s strategic planning process. The meetings give staff a chance to meet directly with stakeholders according to their line of business or sector for open conversation about what the ISO’s priorities should be, he said.

“Those meetings are far more effective if we can do them in person, so in order to try to maximize or increase the potential that we can actually hold those meetings in person, we’re going to push them back to the early and mid-April time frame,” Dewey said.

Cold Weather Ops Going Fine

Since the second week of January, New York has experienced colder than average weather conditions — but not extreme cold — and the peak so far came in above 23,000 MW, about 97% of the ISO’s forecasted peak winter load, COO Rick Gonzales said.

Natural gas prices during January have been significantly elevated and have ranged from $15 to $25/MMBtu, reaching as high as $35/MMBtu for some of the eastern New York gas hubs, he said.

“That has translated into significantly higher energy clearing prices in eastern New York and even throughout the state. … You might be aware we’ve often seen $200/MWh energy prices and higher throughout eastern New York,” Gonzales said.

New York and New England usually have slightly higher energy prices than neighbors Ontario, Quebec and PJM, he said.

“Quebec is actually almost not an importer to New York during these colder weather periods, but we are actually exporting to Quebec,” Gonzales said. “And Ontario and PJM power transfers are typically into New York, so the market systems are doing what we would expect, but … we are seeing the ties being fully utilized in almost all directions.”

NYISO is continuing to allow certain transmission work to proceed, except for on very cold days, he said.

Consolidated Edison (NYSE: ED) must resolve several regulatory concerns before being authorized to build a new $4 billion substation complex in New York City dedicated to interconnecting offshore wind projects.

Those concerns took shape when the New York Public Service Commission issued a Jan. 20 order directing state solicitations for OSW proposals to require “mesh-ready” transmission plans, part of the broader effort to develop rules implementing the Climate Leadership and Community Protection Act (CLCPA), which requires that 70% of the state’s electricity generation come from renewable resources by 2030 and that generation be 100% carbon-free by 2040.

The PSC also asked Con Edison to supply detailed plans for a wind energy interconnection hub — and specifically one in lower Manhattan allowing the connection of up to 6 GW of OSW projects (Case No. 20-E-0197). (See NYPSC Mandates Meshed Offshore Tx Grids.)

“We look forward to providing more details on the benefits of these projects,” Con Edison spokesman Karl-Erik Stromsta told RTOInsider.

Changing Landscape

“Time is of the essence,” the commission said in its order, noting that the PSC and Con Edison are both aiming at moving targets in their efforts to identify the location for a substation. For example, the Rainey substation, which the state’s three-part power grid study last January identified as a good candidate to integrate OSW, has since been claimed by the Clean Path New York (CPNY) project to bring upstate solar and onshore wind into the city.

“The CPNY project is expected to carry generation associated with up to 1,300 MW of capacity, making it highly unlikely that the same substation can feasibly accommodate an additional 1,250 MW of offshore wind generation as assumed in the base case of the OSW study,” the commission said.

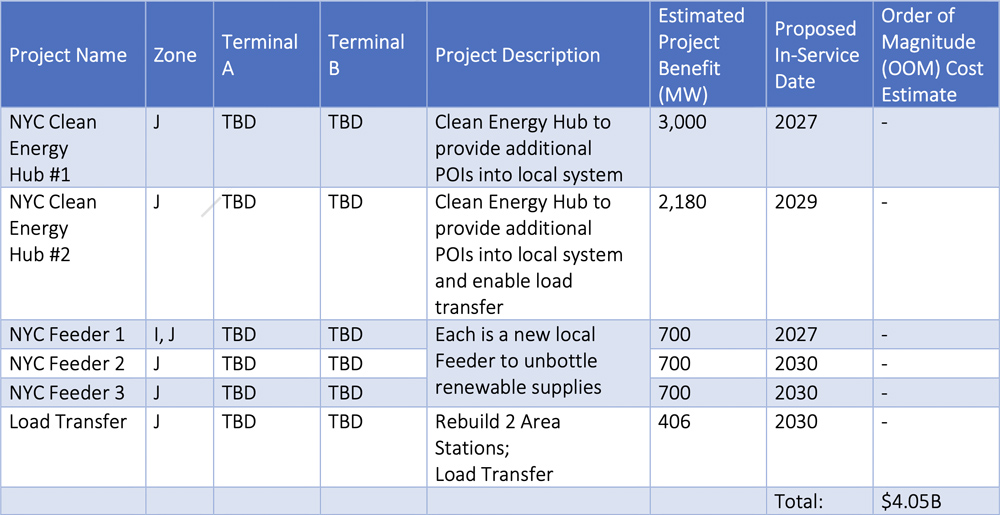

In March 2021 comments on the grid study, Con Edison reiterated earlier proposals for two New York City Clean Energy Hubs.

The first hub would create points of interconnection (POIs) for four 750-MW connections — or 3,000 MW total — and could be placed in commercial operation by summer 2027.

Con Edison estimates from 2020 on approximately $4 billion in Phase 2 projects to bring renewable energy into the city from from both upstate and offshore. | Con Edison

The second hub would create POIs for two new connections for about 1,500 MW total and simultaneously transfer load from three other constrained load pockets on Con Edison’s 138 kV system, relieving transmission constraints and reducing the load’s dependency on local fossil fuel power plants to maintain local system reliability. This project could be placed in commercial operation by summer 2029.

Con Edison first proposed the hubs in a local transmission and distribution report filed by all the state’s utilities in November 2020. The various utilities reported on their T&D status and proposed Phase 1 projects — traditional utility investments that address system reliability or resilience issues — and Phase 2 projects intended primarily for achieving CLCPA goals.

The PSC last April approved $800 million in cost recovery by Con Edison for three Phase 1 projects known collectively as the Transmission Reliability and Clean Energy (TRACE) projects. The projects are needed for reliability in 2023 and 2025 because of the retirement or unavailability of 399 MW of peaking generation made to comply with the state Department of Environmental Conservation’s “peaker rule,” new NOx regulations that go into effect May 1, 2023 (19-E-0065). (See NYPSC OKs $800 Million Tx Cost Recovery for Con Ed.)

Climate Resiliency

Con Edison is also collaborating with the Long Island Power Authority to consider ways to interconnect 9 GW of offshore wind. The grid study and ensuing analysis identified scenarios in which 6,000 MW of interconnections into New York City and 3,000 MW into Long Island minimized onshore transmission system upgrades and involved very limited OSW curtailments. The OSW portion of the study evaluated every New York City area and Long Island substation above 69 kV.

In addition, Con Edison identified the need to construct new feeders to redistribute the renewable energy throughout its local transmission system to both supply local loads and export to upstate load areas to prevent OSW curtailment.

The OSW analysis base case selected four POIs — with their injection capacities — in NYISO’s Zone J (NYC): Farragut (1,400 MW), Rainey (1,250 MW), Mott Haven (1,250 MW), and West 49th St. (1,200 MW). Still unresolved is whether those POIs have the physical space necessary to accommodate the upgrades for the planned injections.

Given the cost and difficulty of finding land for new electrical equipment and operations in lower Manhattan, Con Edison is proposing to build its first hub on land it already owns next to the Farragut substation on the East River in Brooklyn.

The commission is requiring all OSW proposals to include plans for high-voltage direct current (HVDC) transmission to make the best use of limited space available for cables in the Narrows and the harbor. It asked Con Edison for “a reasonable forecast” of where it will put an onshore HVDC converter station and the costs of routing an AC transmission line from there to the hub.

The commission also asked the utility to describe its measures to enhance resiliency, given that the hub would be “geographically concentrating, at a minimum, 3,000 MW of offshore wind interconnections at a single substation that would sit directly adjacent to another large substation (Farragut).”

Specifically, the commission asked for further information on how Con Edison will mitigate the risk of storm damage to the co-located substations; how the substations can be protected from exposure to sea-level rise and static or dynamic flooding; and how the utility will comply with all applicable reliability criteria, including NERC standards for “extreme contingencies” as specified in NERC Standard TPL-001-4.

The PSC also wants the utility to document how it is considering use of advanced technologies in its analysis.

The commission noted comments by LS Power and NextEra Energy Transmission New York in response to the utility study that said despite sufficient detail for regulatory action, Con Edison’s hub proposal should nonetheless be referred to the NYISO public policy planning process because it cannot be considered a local transmission project.

“While the commission expects to address procedural matters following its review of the additional information, the availability of the NYISO process should not interfere with our broad planning authority and review of the options for establishing cost-effective POIs in service of our overarching goal of meeting CLCPA mandates at the least cost to ratepayers,” the commission said in its January 20 order.

The PSC in October 2020 designated the New York Power Authority’s $1 billion Northern New York transmission line as a high priority for meeting the state’s renewable energy goals, bypassing NYISO’s public policy transmission planning process and adopting criteria for identifying other such “priority transmission projects.” (See NYPSC OKs NYPA Project, ‘Priority’ Tx Criteria.)

Xcel Energy said Thursday higher electric and natural gas revenues aided the company in meeting its earnings guidance for the 17th straight year.

Xcel reported year-end earnings of $1.6 billion ($2.96/share), up from 2020’s performance of $1.47 billion ($2.79/share). For the quarter, earnings were $315 million ($0.58/share), compared to $288 million ($0.54/share) in last year’s fourth quarter.

“We had a solid year delivering earnings … and achieving our earnings guidance for the 17th consecutive year. We are well positioned for the future,” CEO Bob Frenzel said in a statement.

Analysts had expected fourth-quarter earnings of 56 to 57 cents/share.

Earnings were partially offset by increases in electric fuel and purchased power, costs of natural gas sold and transported, additional depreciation and lower allowance for funds used during construction.

The Minneapolis-based company reaffirmed its 2022 earnings forecast of $3.10 to $3.20/share.

Xcel is banking on clean energy to meet its guidance. It has filed resource plans in Minnesota and Colorado that it says will accelerate its exit from coal-fired generation in those states by 2030 and 2034, respectively. The company last year said it had reduced carbon emissions by 50% from 2005 levels and is on track to reach an 80% reduction by 2030.

Xcel’s share price closed up Thursday at $68.94, a $1.32 increase from the previous close.

The Bonneville Power Administration will delay its entry into the Western Energy Imbalance Market (WEIM) by two months to work out technical and training issues, the federal power marketing agency said Thursday.

BPA was scheduled to begin trading in the WEIM on March 2 but is now pushing its “go-live” date to May 3, citing customer requests for more testing and training on the computer systems being used to integrate the agency’s operations into the market.

Speaking Thursday during an agency workshop, Chief Business Transformation Officer Nita Zimmerman said the “short delay” provides BPA with additional time “to ensure the most successful go-live outcome” and “to appropriately address some of the remaining functionality needed for some of the systems that we’re still bringing online.”

Zimmerman cited “continued challenges” with metering data, outage management, market settlement allocation and billing among its customer base of publicly owned utilities. Early participants in the WEIM have cautioned potential members on the complexity of integrating into the CAISO-operated market and the high level of “discipline” needed to prepare for joining. (See PacifiCorp Offers Lessons for Future EIM Participants.)

“Building in this additional time does demonstrate the care and rigor that we’re taking — along with our vendors — in bringing this initiative along,” Zimmerman said.

But Zimmerman and EIM Program Manager Roger Bentz both assured BPA customers that the agency is “pedal to the metal” and “continuing full-throttle” in its efforts to meet the May 3 timeline.

Bentz pointed to the progress BPA has made in implementing WEIM systems and practices over the past two months, including commencing parallel operations with the market on Dec. 1. The parallel production environment provides new participants the ability to practice under real market conditions, allowing them to submit bids and base schedules, collect e-tags and learn how to adapt operations to real-time developments.

BPA has also successfully tested end-to-end transfers with two adjacent WEIM entities and finished testing the software that will allow it to “donate” transmission capacity to WEIM operations.

Additionally, the agency has also fully staffed and trained its EIM entity scheduling coordinator and operations desks, Bentz said.

Bentz said he was unsure what impact BPA’s postponement would have on Avista and Tacoma Power, the two other entities slated to join the WEIM on March 2.

“The latest information we have [is] they are likely to stay with their current schedule of March 2,” he said.

“The Tacoma Power team is quickly doing an analysis today and should have more details [Friday],” utility spokesperson Rebekah Anderson told RTO Insider.

Avista did not respond to an inquiry about the effect of BPA’s delay on its WEIM timeline.

If the two utilities stick to their current timelines, BPA will be modeled out of parallel operations early next month and then rejoin in early March, Bentz said.

An impending influx of federal money, a regional partnership in tatters and a pandemic that has drastically changed Americans habits has Massachusetts transportation electrification policymakers’ and advocates’ heads spinning.

But there was optimism and momentum despite uncertainty during a panel hosted by the Northeast Energy and Commerce Association on Wednesday.

An estimated $63 million in formula funding for electric vehicle infrastructure headed to Massachusetts from the Infrastructure Investment and Jobs Act is a “hugely positive story,” said Jake Navarro, director of clean transportation products at National Grid (NYSE: NGG).

But even that money comes with worries about whether it will be spent efficiently.

“It’s really important that those funds get maximized by making them complementary with other programs that other players in the space can offer,” Navarro said.

In addition, the breakdown of the Transportation and Climate Initiative Program (TCI-P) has been frustrating for Daniel Gatti, director of clean transportation policy at the Massachusetts Executive Office of Energy and Environmental Affairs.

“You design a policy for an environment in which no state has any resources to spend on clean transportation … and then it comes time to implement the policy and all of a sudden the price of gas has gone up,” Gatti said. Add big federal funding for transportation to the situation and the circumstances become “challenging” for TCI-P to overcome, he said.

That reality has advocates watching closely to see what will develop in the vacuum.

“TCI-P was pretty central to the administration’s approach to reducing GHGs in the transportation sector,” said Anna Vanderspek, electric vehicle program director at the Green Energy Consumers Alliance. “That is one place where we are taking a really hard look at what is the state’s Plan B in the absence of that stream of revenue?”

Alignment and Opportunity

Participants in the Massachusetts EV sector see a strong landscape despite the market challenges and uncertainties.

“What we don’t really appreciate is the amount of alignment that exists in this state that doesn’t exist in other areas, even in some parts of California,” said James Cater, program lead for EV infrastructure at Eversource (NYSE: ES).

“It’s an amazing thing; I think our alignment enables us to make these really bold steps and make these really bold goals,” Cater said. “I think you are going to see increasingly this be a go-to location for thought leadership, deployment, for business development around this EV universe, and it’s exciting.”

It’s early still in the “adoption curve” for EVs, Navarro said.

“Massachusetts has a goal for 300,000 [EVs, and] … right now we’re at 40,000 to 50,000 vehicles on the road,” he said. “We are at the extreme early end.”

Political circumstances could be favorable to quick government action as Gov. Charlie Baker prepares to exit.

“The last year of the Baker administration, I’m thinking about what we can do in the next 12 months, what we can set up right now,” said Gatti.

One suggestion from Vanderspek: a clearinghouse or “scaffolding” to help consumers understand EVs.

“We’re increasingly getting questions from people saying, ‘I get it, electric school buses; where do I start?’” he said.

PJM is requesting input from stakeholders on a course of action after a member defaulted on its portfolio in the financial transmission rights market, potentially leaving members having to cover millions of dollars.

At Wednesday’s Markets and Reliability Committee meeting PJM’s Chief Risk Officer Nigeria Poole Bloczynski reviewed the timeline of events that led to the default of Hill Energy Resource & Services, a member of the RTO since 2012.

“We are committed to transparency, and we’re just as committed to providing as many opportunities as we can to provide feedback,” Bloczynski said.

Hill Energy’s portfolio value in PJM at the time of default. | PJM

New rules in PJM initiated after the GreenHat Energy default in 2018 were designed to provide more information to members on defaults in the financial markets. GreenHat acquired the largest FTR portfolio in PJM between 2015 and 2018 but defaulted on the portfolio in June 2018, leaving PJM stakeholders to cover more than $179 million in the market. When the company defaulted, GreenHat had only $559,447 in collateral on deposit with PJM. (See Doubling Down — with Other People’s Money.)

Bloczynski said PJM issued an approximate $921,000 margin call on Jan. 10 to Hill because its December positions, which had a positive value, rolled off the RTO’s books. The margin call was due by 4 p.m. on Jan. 11; Hill did not make it and was subsequently declared in default.

PJM withheld payment to Hill of outstanding December and January settlement amounts totaling $735,000 to partially satisfy collateral call. The RTO currently holds $6.1 million in collateral cash from Hill against the defaulted portfolio.

An additional margin call went unmet on Jan. 13, and Hill defaulted on a payment on Monday.

Bloczynski said Hill has been in good standing since it joined the RTO in 2012 and has been adequately collateralized. PJM completed a “Know Your Customer” (KYC) procedure and background check on Hill in 2021 with no adverse findings.

Its FTR portfolio represented 0.3% of PJM’s overall FTR market transactions as of Dec. 31. “It was a relatively small portfolio considering the overall size of the FTR market,” Bloczynski said.

Prior to the Dec. 22 FTR auction, Bloczynski said Hill had a “substantial amount of excess collateral” posted with PJM. After the auction, Hill requested a return of excess collateral, leaving $5.4 million in place against a requirement of $5.1 million. Its portfolio had a positive mark-to-auction value and an FTR credit requirement of $5.1 million, including a $4.1 million FTR requirement and $1 million in additional restricted collateral.

The portfolio goes through May 2025. The company only participated in the FTR market and did not serve any load.

“There were no red flags identified and no previous payment or collateral default history within PJM or what we uncovered through the KYC and background check,” Bloczynski said.

Evaluating the Exposure

Following default, PJM began an analysis of open positions of Hill’s portfolio to assess exposure. The initial analysis showed a subset of the portfolio experiencing “volatile congestion losses” in January because of a short position on the Greys Point-Harmony Village constraint in the Dominion zone. Work started on the line at the beginning of January and is expected to go until December 2023.

As of Monday, PJM had issued about $83 million in collateral calls related to the volatility on the constraint. Approximately 20 impacted companies satisfied the calls, but not Hill. The company’s short position across the constraint path extends from this month through May 2023 for a total of approximately 174 GWh, Bloczynski said, creating risk of “significant degradation” of portfolio value from the December mark-to-auction values. PJM is reviewing other portfolios that may be experiencing losses and issuing collateral calls.

Bloczynski said there are already known losses of $2.8 million from the beginning of the month through Jan. 20 on the defaulted portfolio. Depending on market conditions of day-ahead prices, the final January dollar numbers could be “more or less.”

PJM anticipates an estimated loss of $300,000 from February through May based on the latest February FTR auction for the balance of the planning year and a $4.6 million loss from June through the end of the FTR portfolio in May 2025.

That brings the total of estimated losses to $7.2 million in losses, against the $6.1 million PJM holds in collateral.

“It’s very likely the amount that we have will be inadequate given the unusual congestion patterns we’ve seen so far,” Bloczynski said.

Tim Horger, director of PJM’s forward market operations and performance compliance department, provided some of the options available in the RTO’s “toolbox” to deal with the default, as required under Schedule 1 of the Operating Agreement. They include allowing the positions to go to settlement, or liquidating the positions by offering them for sale in an upcoming auction.

Horger said the January and February positions in the portfolio will go to settlement because of the timing of the default. But “there could be a combination of different ways to handle” the other positions, he said.

Horger said the first option is to allow the positions to go to settlement against day-ahead prices for a certain period or throughout the life of the portfolio through May 2025. He said if the positions are allowed to go to settlement, it could result in a “significant loss” depending on how the congestion on the line in the Dominion zone materializes over the next three years.

“It might not be practical to let them go to settlement for these longer-term positions because at that point the membership will be at risk of potentially higher costs,” Horger said.

The positions can be liquidated in a normal or special FTR auction. Offering the portfolio for sale in a normal FTR auction allows the market to determine the value of the portfolio, Horger said, and it also removes the risk of future exposure because the positions are being taken off the books.

A special auction, Horger said, would be conducted in almost a “silent auction” fashion with only individual paths in the defaulted portfolio being bid on instead of being inserted into the larger FTR market.

Horger said PJM is interested in how much advance notice stakeholders would want before liquidating the portfolio in an auction. “The goal is to minimize losses to members.”

PJM General Counsel Chris O’Hara gave an update on the legal procedure in the default.

The RTO believes Hill was “adequately capitalized” and had “sufficient” capital to satisfy the margin calls, O’Hara said. It filed a complaint and request for expedited discovery against the company and its principal Lijin Chen, who had notified it that the company does not currently have sufficient funds to cover the defaulted portfolio.

O’Hara said PJM filed the court case in Texas to “eliminate personal jurisdiction issues” with Chen. Claims in the lawsuit include breach of contract, taking actions to avoid credit obligations and “piercing the corporate veil/alter ego.” The RTO is pursuing an injunction to “seek to secure funds in the amount of the unsatisfied collateral calls,” he said.

PJM CFO Lisa Drauschak said section 15.2.2 of the OA establishes a default allocation assessment formula to be used at the direction of the board. Ten percent of the default would be charged to every PJM member with a $10,000 annual cap, and 90% of the allocation is based on gross market activity, itself based on three months of gross billings. For the Hill default, the factor would include gross billings from November, December and January.

PJM will discuss the proposed settlement timetable at the Feb. 24 MRC meeting. A special session of the Members Committee is also scheduled for Feb. 2 to further discuss the approach to the default with stakeholders.

Driven by “rising climate ambition and policy action from countries around the world,” investment in low- and no-carbon energy deployment worldwide reached a new high of $755 billion in 2021, said BloombergNEF’s Energy Transition Investment Trends 2022 report issued Thursday.

But to reach global net-zero goals by 2050, clean energy investment will have to triple to an average of almost $2.1 trillion per year between 2022 and 2025, the report says.

“There is another doubling of investments needed thereafter, to an average $4,189 billion per annum over the years 2026-2030,” the report’s executive summary says. “About one to two fifths of the spend is required for next-generation low-carbon technologies, such as hydrogen, [carbon capture and storage] and nuclear.”

The 2021 figure represents a 27% increase over 2020’s high mark of $595 billion, the report says, noting that the figure covers projects with firm financial commitments. The two technologies propelling that growth now and over the coming decade are renewable energy and transportation electrification.

Renewable investments ($366 billion) led electric vehicles and charging infrastructure ($273 billion) in 2021, but with investment in EVs and chargers up 77% over 2020, BNEF predicts the transport sector will overtake renewables this year.

Writing on Bloomberg Green, Nathaniel Bullard, BNEF’s chief content officer, said that investments in electric transportation and energy storage are growing, respectively, at 10 and 8 times the rate of renewables.

At the low end of the scale, global investment in hydrogen, energy storage, sustainable materials and carbon capture and storage (CCS) together totaled $24 billion in 2021, the report says. But, looking ahead, BNEF sees multiple pathways to net-zero, in which potential investment in CCS could rise to $622 billion, while the potential investment for hydrogen could hit $532 billion.

Albert Cheung, head of analysis at BloombergNEF, sees the 2021 figures as a measure of the resilience of the clean energy sector. In a statement on the BNEF website, Cheung said that amid a global supply chain crunch that has raised costs for solar, wind and energy storage, the past year provided “an encouraging sign that investors, governments and businesses are more committed than ever to the low-carbon transition.

“[They] see it as part of the solution for the current turmoil in energy markets,” Cheung said.

No Competition

Overall, the report reflects expectations that rapid deployment of renewables and electric vehicles will be the core technologies needed for near-term greenhouse gas reductions, but getting to net zero in the longer term will require the growth of low- and no-carbon technologies, including nuclear, hydrogen and CCS.

The report anticipates ongoing growth in clean energy markets worldwide; it also shows the U.S. still lagging behind China in overall investments. China’s clean energy investments in 2021 totaled $266 billion versus $114 billion for the U.S.

Similarly, the Americas as a whole were behind both the Asia Pacific and the Europe, Middle East and Africa regions in total investments.

Those figures raised eyebrows on Twitter, where Tim Latimer, CEO of geothermal developer Fervo Energy, was dismayed by China’s overwhelming dominance. “Investment in these technologies will define the future — and it’s not even competitive right now,” he said.

But the U.S. still led other European and Asian countries, with its closest competitor, Germany, taking the No. 3 spot with $47 billion.

Renewables and clean transportation also led investment in what BNEF calls the “climate-tech sector” — the startups and early-stage companies driving innovation in the clean energy transition. Climate-tech investment worldwide totaled $165 billion in 2021, the report says, with 82% of the total going to renewables and transportation.

Drilling down further, BNEF reports that rising climate-tech investments in transportation were, in part, the result of the steep increase in companies going public through reverse mergers with special purpose acquisition companies (SPACs). SPACs are “blank check” or shell companies formed to raise capital to acquire or merge with another company and are being used as an alternative to taking companies public through a traditional IPO.

Transportation startups accounted for two-thirds of climate-tech SPACs in 2021, with total investments of $23 billion.

The U.S. Market

Recent U.S. announcements in the electric transport sector indicate strong growth for the sector going forward. On Tuesday, General Motors made headlines with its announcement of a $6.6 billion investment in the company’s transition to electric vehicles. GM is building a new battery factory and converting an existing plant to produce two electric pickup truck models, the Chevrolet Silverado and the GMC Sierra.

Both facilities are in Michigan and will maintain 1,000 jobs, while creating 4,000 new jobs, GM said in a press release. The $6.6 billion appears to be the first installment of the $35 billion the company committed to electric and automated vehicles in June.

GM’s announcement was followed on Wednesday with Tesla’s earnings call for the fourth quarter of 2021, during which the company reported earnings of $17.6 billion, driven by record deliveries of 300,000 EVs in the last three months of the year. The company also reported increases in its solar and energy storage deployments.

PJM and the New Jersey Board of Public Utilities asked FERC Thursday to approve their plan for using the “state agreement approach” (SAA) to build transmission to deliver the state’s planned 7,500 MW of offshore wind (ER22-902).

Under the proposal, New Jersey would commit to paying 100% of the cost of the transmission but could seek to allocate some costs to other generation projects that use the additional capacity. PJM and the BPU said the SAA agreement, which they asked FERC to approve by April 15, is “an innovative and significant step forward” in meeting New Jersey’s goal of developing offshore wind.

PJM proposed the state agreement approach to comply with Order 1000’s requirement for procedures to address transmission needs driven by public policy requirements in the regional transmission planning process.

As approved by FERC, “the SAA mechanism is not a rigidly defined process in the PJM Operating Agreement,” PJM noted. “Rather, the SAA process is intended to provide the flexibility needed to accommodate the breadth of policies that a state might wish to pursue and to allow that state to select the transmission solution(s) that best addresses its public policy goals.”

The filing is a milestone in a process that began when New Jersey asked PJM on Nov. 18, 2020, to open a competitive window to solicit transmission proposals to connect its OSW. The window, opened last April, closed Sept. 17, 2021. (See PJM, NJ Staff Brief Stakeholders on State Agreement Approach.)

BPU President Joseph L. Fiordaliso called the filing “a critical next step on the pathway for efficient offshore wind interconnection between the approved wind farms and the onshore grid.”

“New Jersey is once again leading the way on offshore wind through this agreement approach, which unlocks the potential for drastically minimizing community impacts while saving money for New Jersey’s ratepayers,” he added.

NJ BPU offshore wind solicitation schedule | PJM

After PJM completes its review of the bids, they will be sent to the BPU to determine which, if any, of the proposed projects the state will agree to fund. According to PJM’s filing, “BPU’s competitive bid evaluation process will review price, risk, environmental and other factors.”

“PJM’s proven competitive process will allow the Board of Public Utilities to select an optimized, comprehensive solution that maintains electric reliability while advancing the state’s energy policy goals,” PJM CEO Manu Asthana said in a statement.

The BPU has awarded more than 3,700 MW of offshore wind generation: Ørsted’s Ocean Wind 1,100-MW project and a combined 2,658 MW for EDF/Shell’s Atlantic Shores Offshore Wind and Ørsted’s Ocean Wind II.

Request

Specifically, PJM asked the commission to approve:

the assignment of transmission capability created by SAA projects to OSW generators selected through New Jersey’s solicitations;

the requirement that OSW generators will be studied through PJM’s interconnection queue;

the granting of any incremental rights, if eligible, associated with any incremental transmission capability created by SAA projects;

New Jersey’s ability to obtain cost sharing from entities other than OSW generators that seek to utilize facilities created as part of an SAA project, including offshore transmission facilities and extensions to the onshore grid; and

the ability of the BPU to assign some or all of the capability created by SAA projects to public policy resources other than OSW generators.

“Importantly, the SAA agreement does not consent to the selection of any SAA project(s), designated entities, or cost allocation methods by which to allocate the costs of any SAA project(s) to New Jersey customers,” PJM said. “Before the NJ BPU can follow through with any of those next steps, it needs to know whether the commission will accept the terms and conditions contained in the SAA agreement. Commission acceptance of the SAA agreement would provide the NJ BPU the regulatory certainty needed to select and sponsor any suitable SAA project.”

Future Filings

If the state selects one or more projects, there would be additional FERC filings specifying the project’s scope, estimated cost, the entity or entities selected to construct it, construction milestones and proposed cost allocation.

PJM said it created the SAA agreement with the BPU “to reflect the complex realities and timelines associated with the development of offshore wind generation and any potential SAA project(s), while at the same time preserving the open access provisions of Order No. 888 and ensuring fair treatment of all other generators in PJM’s interconnection queue.”

“Since New Jersey’s request to inject up to 7,500 MW of offshore wind into New Jersey via an SAA project(s) was known to customers entering the queue after Nov. 18, 2020, such circumstances are appropriately factored into the interconnection study process and may form the basis for assigning the customer new facilities to build or for allocating specific costs to subsequent customers,” PJM said.

“PJM and the NJ BPU urge the commission to recognize the steps they have taken both to preserve fair opportunities for other generators in the queue and open access requirements while, at the same time, ensuring that both the generation and transmission components of the NJ BPU’s SAA proposal can be effectuated on a coordinated and timely basis to meet the state’s public policy goals. PJM urges against efforts to strictly ‘pigeonhole’ each component as being either a part of the interconnection process or the [Regional Transmission Expansion Plan] process without recognizing the important relationship between the two processes under the SAA process, as the failure to do so would render the SAA process meaningless.”

CARMEL, Ind. — MISO this week wrapped up discussion on its plans for sharing the costs of the first group of projects identified under its multistage long-range transmission plan.

The grid operator plans to file its cost allocations for long-range transmission projects with FERC by the end of January. The plan employs a 100% postage stamp allocation to load, limited to either MISO Midwest or MISO South subregions. Projects must have a minimum 100-kV rating, cost at least $20 million, and demonstrate a 1:1 benefit-to-cost ratio.

The cost-allocation design is predicated on the belief that initial projects coming out of the RTO’s first long-range planning cycle are unlikely to produce benefits that seep into MISO South unless MISO increases the capacity of its subregional transmission transfer. (See MISO to Test Long-range Tx Allocation Benefits.)

Currently, MISO can only contractually flow 3,000 MW in the Midwest-to-South direction and 2,500 MW in the South-to-Midwest direction.

The grid operator plans to submit the long-range projects for board approval in mid-June. The first smattering of projects will be limited to Midwestern locations. (See MISO Promises Long-range Tx Project Reveal Soon.)

During a Monday meeting of the Regional Expansion Criteria and Benefits Working Group (RECBWG), MISO’s Jeremiah Doner said the proposal has the support of most of the footprint’s transmission owners.

Brattle: South Benefits Unlikely from Midwest

The Brattle Group, tasked with testing the benefits spread from MISO’s last long-range projects in 2011 to see if they delivered advantages to MISO South, said the region saw only small advantages.

Brattle Group Principal Johannes Pfeifenberger said had members of MISO South — which only dates back to Entergy’s membership in 2013 — been assigned project costs, it would not have met FERC’s roughly commensurate benefit threshold. However, Pfeifenberger recommended that the grid operator keep a systemwide cost-allocation option open for projects that increase transfer capability between the two subregions or are physically located in both.

MISO said it will make a separate filing later to FERC where it will propose an evaluation method testing whether a project’s costs should be shared on a subregional or systemwide basis. The RTO said it will allocate long-range projects’ costs to the entire footprint if systemwide benefits can be proven through analysis.

“We understand that there aren’t zero benefits that can go between the Midwest and South or vice versa,” Doner said.

MISO’s cost-sharing filing will arrive at FERC as multiple Midwestern states are either trying to or have passed rights-of-first-refusal for their incumbent transmission owners. Wisconsin lawmakers this month introduced a bill that would prohibit the grid operator from awarding construction contracts to competitive developers. Michigan, Minnesota and Iowa have already enacted similar legislation.

MISO, meanwhile, is currently accepting applications from transmission developers to become qualified to bid on competitive projects.

Stakeholders: More Meetings on Cost Allocation

In addition to tweaking the long-range plan’s cost allocation, the RECBWG also plans to establish draft allocation designs this year for a possible new MISO and SPP Targeted Market Efficiency Project category and projects stemming from the RTOs’ Joint Targeted Interconnection Study. Those studies are aimed at getting interregional transmission projects built to clear up congestion on both sides of their seam and interconnect new generation.

Multiple stakeholders said they doubted that the RECBWG could accomplish those aims with only eight meetings scheduled in 2022. MISO is debuting a more infrequent stakeholder committee meeting schedule as it charts a return to in-person meetings during the coronavirus pandemic. (See MISO Hosts First In-person Meetings amid Pandemic.)

“Cost-allocations discussions are challenging. I don’t think we have enough meetings on the calendar,” Clean Grid Alliance’s Natalie McIntire said.

“To be blunt, all we accomplished over 14 meetings [last year] was to dust off the [Multi-Value Project] allocation,” WPPI Energy’s Steve Leovy said of proposed long-range allocation. “I’m not confident we’re going to be able to make progress given this calendar.”

Doner said the meeting cadence allows MISO engineers to return to their offices and conduct analyses on and test allocation designs. He said the RTO will discuss the possibility of adding more RECBWG meetings next month.

Staff at the Texas Reliability Entity warned utilities this week that they need to keep working on the systemic weaknesses that led to last year’s Colonial Pipeline shutdown.

The ransomware attack on Colonial led the company to shut down its entire 5,500-mile pipeline network for almost a week. The network transports more than 100 million gallons of petroleum products daily, supplying about 45% of all fuel consumed on the U.S. East Coast. (See Biden Directs Federal Cybersecurity Overhaul.)

Although the hackers — identified by the FBI as the Eastern European cybercrime group DarkSide — did not manage to compromise the company’s operational technology (OT) systems, they did encrypt several computer systems, including the billing system. This led the company to shut down the pipeline because it had no way to bill customers for their fuel. The attackers demanded 75 Bitcoin (then about $4.4 million) in return for a decryption tool; Colonial CEO Joseph Blount authorized paying the ransom, though subsequent media reports alleged that the tool worked so slowly that the company decided to restore its systems from backups instead.

At Thursday’s Talk with Texas RE, William Sanders, a cybersecurity principal at the regional entity, reminded attendees that incidents like the Colonial attack don’t need to involve sophisticated hacking techniques; in many cases, simple carelessness provides plenty of opportunities for hackers to get a foothold in a system. Vulnerabilities such as recycling user names and passwords from one system to another are easy to warn against but can be incredibly hard to eradicate.

“Studies have shown that over half of respondents are reusing passwords … and of those, 44% admitted to reusing passwords between personal and work accounts. So this can be very problematic,” he said.

Password reuse may have enabled DarkSide to first gain entry into the Colonial network. The hackers used the password of an employee to gain access to Colonial’s system on April 29, initially performing reconnaissance before launching their attack several days later. But access alone was not enough to cripple the company, because several other often repeated security recommendations had to be ignored for the gang to infiltrate critical systems.

“We don’t know how the password was acquired, but it has been discovered in a Dark Web leak, so the password is publicly available,” Sanders said. “It’s possible that the Colonial Pipeline employee had reused a password between work and personal accounts, and the Colonial account was no longer in use, but it had not been disabled; it was still enabled and had access to their VPN [virtual private network] … and the VPN did not require multifactor authentication.”

While NERC’s Critical Infrastructure Protection (CIP) reliability standards already require changing passwords at least every 15 months, Sanders observed that this only applies to high- and medium-impact bulk electric system (BES) cyber systems. However, the Colonial incident shows that low-impact systems — even non-OT systems like billing — may also be used to impact an entity’s operations.

For this reason utilities should consider requiring users of other networks to change their passwords frequently too — though changing passwords too often may cause employees to reuse or cycle through credentials, which should also be avoided.

Sanders suggested utilities can consider expanding other CIP requirements that don’t currently apply to low-impact systems, such as disabling accounts that are no longer needed and implementing multifactor authentication wherever feasible.

“Accounts protected with multifactor authentication are 99% less likely to be compromised,” Sanders said. “It’s still possible for them to be compromised, but the level of sophistication and effort [needed] is much greater than [for] those accounts that are only protected with a single-factor password.”