Performance-based regulation is a way to align utility incentives with the interests of customers and society, according to a new RMI report that seeks to get more states to adopt the practice over traditional cost-of-service regulation.

Traditional regulation has strong financial incentives for utilities to spend more money than needed on infrastructure, leading to affordability concerns as the industry invests to transition to a modern, cleaner grid, said the report, titled “How to Restructure Utility Incentives: The Four Pillars of Comprehensive Performance-Based Regulation.”

“There’s a number of reasons the traditional model just isn’t really well aligned with the challenges today,” report co-author Kaja Rebane, an RMI senior associate, said in an interview. “Affordability is a very big one of those. Right now, we are facing the need to invest a lot of money in the grid [to] modernize it, to deploy new technologies and to just build more capacity to supply clean power to customers.”

Traditional regulation pays utilities for what they build, while performance-based regulation (PBR) focuses on what they achieve, she added. Utilities will consider a number of factors when they make investments, but regulations guaranteeing them a return on capital are a major influence.

“That’s not … well-aligned with what the challenge is today,” Rebane said. “We do need more capital spending that is important, but we need it to be cost-efficient in order to achieve what we want to achieve in an affordable manner.”

Getting the right regulatory incentives sounds easier than it is because a full suite of performance-based regulations requires multiple changes to the cost-of-service model. The report said regulators can do “incremental PBR” and adopt some specific tools onto traditional regulation, or “comprehensive PBR,” adopting the full suite of reforms to get utilities focused on outcomes in ways cost-of-service regulation cannot.

The report lays out four pillars of performance-based regulation: incentivize cost efficiency, remove the throughput incentive, equalize capital and operational spending incentives, and incentivize targeted outcomes.

Cost efficiency can be supported by an array of changes, such as multiyear rate plans, shared savings mechanisms, fuel-cost sharing mechanisms and metrics focused on spending trends.

Revenue decoupling is the main way to remove the throughput incentive, while equalizing returns for capital and operational returns is self-explanatory. Incentivizing targeted outcomes can be accomplished through metrics, scorecards and performance incentive mechanisms (PIMs).

“Although PBR can be powerful, it is not a silver bullet for every regulatory problem,” the report said. “Even a well-designed comprehensive PBR framework will achieve the best results when it is part of a larger basket of synergistic reforms, such as widening opportunities for stakeholder input, adopting innovation policies, updating planning and procurement processes, and expanding regulatory commission authority and responsibilities.”

PBR in Hawaii

The report highlights Hawaii as a jurisdiction that has adopted comprehensive PBR across the four pillars.

“We highlighted Hawaii, in part, because it really has adopted a framework we would consider comprehensive, meaning that all four pillars that we discussed in the report are supported,” Rebane said. “There’s also been a number of forward-looking reforms in Hawaii that are worth highlighting.”

Hawaii has a five-year multiyear rate plan (MRP) with returns pegged to third-party indexes instead of utility forecasts, she added.

To mitigate excessive earnings or losses, the five-year rate plan comes with an earnings-sharing mechanism with a wide symmetrical deadband to ensure cost efficiency, the report said.

“Because of the deadband, which is centered around an allowed ROE of 9.5%, the MRP’s full cost-containment incentive is preserved (i.e., Hawaiian Electric keeps all additional earnings and bears all deficits) when the realized ROE falls between 6.5 and 12.5%,” the report said. “Outside of the deadband, sharing ramps up in a tiered fashion.”

A shared savings mechanism encourages cost efficiency for operational costs not covered by the annual revenue adjustment in the rate plan, which covers fuel for generators, purchased energy and capacity costs, new projects not funded with the rate plan, and other items. A fuel-cost sharing mechanism trues up just 98% of the difference between expected and actual costs — subject to a $2.5 million annual cap, which gives Hawaiian Electric the incentive to operate its generation more efficiently.

Hawaii regulators have also adopted metrics and scorecards that provide visibility into the utility’s cost trends, which include rate base per customer, operations and maintenance cost per customer, and annual revenue growth.

The term performance-based regulation has been around a while, and RMI hopes its report will help regulators better understand what it means and how it can improve outcomes in their jurisdictions, Rebane said.

“We’re trying to give regulators the tools they need to really reform incentives in their jurisdictions to achieve their policy goals,” Rebane said. “We also, of course, in the report provide kind of a relatively basic overview of a number of the key PBR tools that can support each pillar and so, hopefully, that will provide something of a go-to reference for regulators who are interested in these things.”

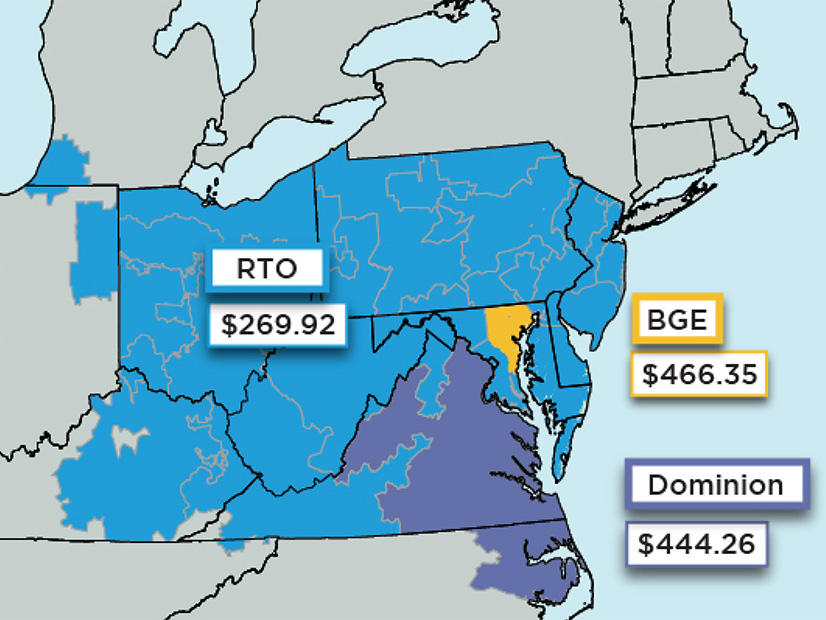

Generation owners point to the nearly 10-fold increase in capacity prices seen in the 2025/26 Base Residual Auction (BRA) results announced July 30 as the price signal they need to invest in new development. Meanwhile, consumer advocates say they worry a compressed auction schedule and backlogged interconnection queue will limit the ability for market participants to react.

The clearing price for most of the RTO jumped to $269.92/MW-day and two regions surged to their price caps, reaching $466.35/MW-day in the Baltimore Gas and Electric (BGE) zone and $444.26/MW-day in the Dominion zone. The “rest-of-RTO” price in the previous auction was $28.92/MW-day. (See related story, PJM Capacity Prices Spike 10-fold in 2025/26 Auction.)

PJM said the increase was driven by tightening supply as generation resources retire, increased demand as data center load is expected to come online and a shift in how PJM forecasts reliability risks and determines the capacity contribution for resources.

Nearly half of the capacity that cleared the auction was supplied by gas generation, at 48%, followed by 21% nuclear and 18% coal. Demand response made up 5% of cleared capacity. Hydro fell to 4% and wind and solar were at 1%.

“The significantly higher prices in this auction confirm our concerns that the supply/demand balance is tightening across the RTO. The market is sending a price signal that should incent investment in resources,” PJM CEO Manu Asthana said in a July 30 announcement of the BRA results.

Consumer Advocates, Enviros: Sluggish Planning and Market Design

Illinois Citizens Utility Board Executive Director Sarah Moskowitz said PJM has been slow to adapt and failed to design a capacity market that sparks new generation investments without creating a windfall for developers.

“The power grid operator’s compressed auction schedules mean generators can’t build and come online quickly enough to respond to prices and bring down costs. Just as concerning, PJM has dragged its feet on interconnection and long-term transmission policy reforms that could speed up its approval process and bring needed clean, affordable energy online more quickly. Similarly, we have concerns about the accuracy of PJM’s load forecasting, as detailed in a recent letter from consumer advocates to PJM,” she said.

Susan Bruce, representing the PJM Industrial Customers Coalition (ICC), said the auction results differ significantly from simulated results PJM presented in the stakeholder process and it remains unclear what led to that gap.

“Regardless, the auction results will have a serious impact on customers. Given the timing of the auction relative to the 2025/2026 delivery year, customers have little to no opportunity to take action to minimize the cost consequences. And with delays in the interconnection queue, there is real concern about what may happen in the next auction,” she said. “Focused and dedicated efforts must be undertaken — post haste — to ensure that PJM market design can both facilitate new entry and retention of resources, without market power being exercised, better accommodate single point load integration, and properly reflect the value of non-weather sensitive customers’ demand response capability.”

Tom Rutigliano, of the Natural Resources Defense Council, said the price jump is the result of a reliance on fossil fuel generation at the expense of designing a market and grid set up to facilitate the development of clean energy. Gas-fired resources in particular, he said, have failed to live up to the promise of delivering reliability at low cost.

“Make no mistake: This was foreseeable and preventable. This is what happens when regulators sideline a wealth of historically affordable clean energy resources waiting at their doorstep and the transmission needed to bring them online. For years, the largest grid operator in the eastern U.S. has all but refused to diversify its resource mix and bring new energy online, and instead opted to depend excessively on an aging fossil fuel fleet while ignoring its reliability failures. This sticker shock is a direct result of recent regulatory changes made to address those reliability failures.”

He argued the cure to high capacity costs lies in the renewable energy projects pending in PJM’s interconnection queue.

“Diverse power grids are critical for reliability, and now we see just how critical they are for affordability. With wind and solar only making up an abysmal 2% of resources in this auction, but the overwhelming majority of PJM’s project queue, it is clearer than ever that PJM needs to rapidly scale up new energy resources to protect customers and resilience,” he said. “The cost of PJM’s interconnection delays has now reached billions of dollars. Leaders in PJM states must demand accountability and solutions from their grid operator before they have to pay billions more in the next auction just five months from now.”

PJM spokesperson Dan Lockwood said the RTO is in the process of implementing a FERC-approved reworking in how it conducts generation interconnection studies, which uses a cluster-based approach to determining any necessary network upgrades and allocating costs. He said that approach is expected to process 72 GW of resources in 2024 and 2025.

“Today, about 38,000 MW of resources that have already cleared PJM’s interconnection process have not been built due to external challenges that have nothing to do with PJM, including financing, supply chain and siting/permitting issues. PJM remains concerned with this slow pace of new generation construction and is considering ways to accelerate those who can successfully overcome those challenges and build,” Lockwood said.

Transmission Owners See Regulated Generation as Solution

During the utility’s July 31 earnings call, FirstEnergy CEO Brian Tierney said the high capacity prices and sluggish resource development suggest state administered capacity procurements may have a part to play in augmenting PJM’s marketplace, pointing to those run by the New York State Energy Research and Development Authority (NYSERDA) and New York Power Authority (NYPA).

The utility has limited ability to own capacity assets in many states. However, conversations about permitting it to develop dispatchable generation with a regulated return could allow it to respond to price signals when other market participants are not. In states where FirstEnergy does own generation, like West Virginia, he said that could take the shape of new combined cycle gas resources, while in Pennsylvania, that would take legislative changes.

“There are people that get upset and say, ‘You’re going back to regulation.’ I don’t think you have to go back to regulation. I think you can still have energy markets. I think you can still have retail choice where you have it today. But I also think you could have constructs like NYSERDA or NYPA where they could buy on behalf of the state’s residents. And that doesn’t have to be an end to competition,” Tierney said. “And they can even have auctions where all people could participate in that: utilities, independent power producers and others. So, for the people that say it has to be one or the other, I just don’t think that’s a valid premise.”

Part of the difficulty Tierney outlined is the disparity between the amount of time it takes to plan and develop new generation resources, compared to how quickly new loads can come onto the grid. He said new resources built in response to the higher prices could take as long as six years to come online, falling toward the end of the period PJM said it’s concerned about resource adequacy in a February 2023 white paper. (See “PJM White Paper Expounds Reliability Concerns,” PJM Board Initiates Fast-track Process to Address Reliability.)

While he said new resources with a regulated return could be part of the solution, Tierney said developing new competitive generation is off the table.

“The thing we wouldn’t be willing to do would be start competitive generation of our own. That’s something that we’ve recently come out of. We paid a heavy price for that. We’ve rebuilt our balance sheet in the wake of that, and that’s not a place that we’re going to be going back to. But other things, other opportunities that could benefit our customers have the capacity that they need be responsive from a price standpoint are all things that are on the table and are all things we’re talking to our states about,” he said.

PJM capacity prices increased nearly tenfold in the 2025/26 Base Residual Auction, with two regions reaching their zonal caps. | PJM

In a statement, Exelon said the results show a need for new generation and transmission assets, particularly within the constrained BGE zone. In its announcement of the auction results, PJM said the higher zonal prices for BGE and Dominion were the result of insufficient generation within the zones and limited transmission to import from other regions.

“The recent PJM auction results underscore a critical need for strategic investments within the Exelon footprint, particularly in our BGE service territory in Maryland. The elevated price levels in this area, as well as others, reflect both a scarcity of resources and transmission constraints. Even with Exelon’s ongoing investments, including $34.5 billion over the next few years to upgrade the energy grid, additional transmission projects are still needed to ensure the strength and reliability of the energy grid now and in the foreseeable future,” the utility said.

During Exelon’s Aug. 1 earnings call, CEO Calvin Butler said all options are being pursued in response to a question asking whether the utility is looking at authorization for including peaker generation in rates.

“We’re working with our commissions on all types of scenarios. We shouldn’t take anything off the table because we need to address this issue and ensure affordability and equity [are] at the forefront of all discussions,” he said.

Generators Say Auction Delivers Needed Investment Signal

Enel North America Head of Energy and Commodity Management Roberto Rosner said the auction tells generation developers that now is the time to build new capacity resources.

“The signal from the auction is unmistakable: PJM needs more clean generation and more flexible demand-side resources. Power producers like Enel are eager for PJM to implement its interconnection reform so we can add more clean, affordable megawatts to the grid. As load forecasts rise from electrification and data center buildout, the value of demand response for maintaining reliability has never been clearer. It’s also clear that the substantial derate of capacity through ELCC ratings had a meaningful impact on the outcome.”

Voltus President Matthew Plante said the results were predictable given the number of generation retirements and PJM’s load forecasts. However, shifts in resource accreditation also had a large impact on the amount of supply able to offer into the auction. PJM’s shift to marginal effective load carrying capability (ELCC) and reworked risk modeling led to the focus on when resources can perform shifting from summer to winter.

“As the grid changes, we’re no longer in a situation where peaks are always during the summer months. In fact, the last time PJM dispatched the emergency load reduction program was December 2022 … so now it’s equally likely that PJM will need these resources in the winter than in the summer,” he said.

For demand response, that led to a 25% derate in the capacity resources could offer, reducing DR supply by about 3,000 MW. Nonetheless, Plante said the high price point is likely to turn around a yearslong decline in DR participation in PJM’s capacity market. Asset-backed DR resources — such as smart thermostats, batteries or anything requiring a capital investment — are especially likely to be buoyed by the high prices.

“It’s hard to find a customer that doesn’t want to take advantage of the value proposition that now exists,” he said.

Technological barriers have limited DR participation in the past, but most of those have been alleviated in recent years, Plante said. PJM and DR providers are working on addressing remaining regulatory barriers. He called the ELCC derate a “sledgehammer solution” and said the whiplash of frequent rule changes could affect market participation.

“I think regulators need to understand that there’s sometimes we change the rules too frequently and are reactive to things, and yes, a whiplash on rules in particular leads to volatility in the number of megawatts enrolled,” he said.

Staff Implement ECRS Changes, Withdraw Related NPRR

ERCOT staff have withdrawn a protocol change and updated control room procedures following the regulatory commission’s rejection of modifications to the grid operator’s new ERCOT contingency reserve service (ECRS) product.

The Public Utility Commission on June 25 rejected the nodal protocol revision request (NPRR1224) by removing the proposed $750/MWh price floor and directing ERCOT to separately implement the revision’s trigger mechanism for the service. (See Texas Commission Rejects ECRS Rule Change.)

“I think my lawyers would say that they did not direct us to do anything, but that they expressed some support for the concept of releasing ECRS when we hit the triggers that were described, so we’re going to roll with that,” ERCOT’s Jeff Billo, director of operations planning, told the Technical Advisory Committee during its July 31 meeting.

Staff and stakeholders had been working since late last year to reach a compromise on NPRR1224. Stakeholders added the price floor for ECRS’s deployment. The trigger mechanism takes effect when there is a 40-MW power balance violation for at least 10 minutes.

ERCOT introduced ECRS last year. It procures capacity resources that can be brought online within 10 minutes and sustained at a specified level for two consecutive hours. The Independent Market Monitor has opposed the new ancillary service, saying it produced “massive” inefficient market costs totaling more than $12 billion in 2023. (See ERCOT Board of Directors Briefs: Dec. 19, 2023.)

Billo said ERCOT has updated its real-time desk procedures to incorporate the trigger mechanism, which became effective Aug. 1.

The grid operator also withdrew NPRR1232, which staff had begun developing during the NPRR1224 negotiations. Billo said after the PUC’s discussion of NPRR1224’s price floor and stakeholders’ concerns over NPRR1232’s implementation and timeline, staff decided to withdraw the latter and its similar price floor concept.

Staff discussed NPRR1232’s withdrawal with the IMM, Billo said. He said he understood the monitor was “agreeable” with the withdrawal.

$29M in Firm Fuel Service

ERCOT staff told TAC it procured 3,319.9 MW of firm fuel supply service (FFSS) capacity with a projected standby cost of $29.88 million between Nov. 15, 2023, and March 15, 2024.

The grid operator contracted with 32 generation resources at $9,000/MW. Three of those either tripped offline during a watch or had mechanical failures unrelated to fuel or cold weather, leading ERCOT to claw back $976,818 from the resources. The clawback was offset partly by $781,342 in fuel replacement costs, resulting in a total FFSS payment of $29.42 million.

The FFSS ancillary service product is a result of legislative requirements and a PUC order to provide additional grid reliability and resiliency during extreme cold weather and compensate generation resources that meet a higher resiliency standard. Under ERCOT protocols, staff will provide a report to TAC when the product is deployed.

The ISO issued a request for proposal for FFSS during the next obligation period (Nov. 15, 2024-March 15, 2025) on July 31.

In other staff reports:

Matt Mereness told TAC that ERCOT’s highly anticipated real-time co-optimization (RTC) and battery project expects to announce a go-live date by the end of September. The project’s tentative go-live date is 2026. In September, staff will simulate RTC, covering data from June 2023 onward, using their simulator for feedback on price formation.

Bill Blevins, who chairs the Large Flexible Load Task Force, said more than 5 GW of load has been authorized and is waiting to be energized. The task force has discussed going into hibernation; members raised concerns over dissolving the group because they value the interconnection queue updates.

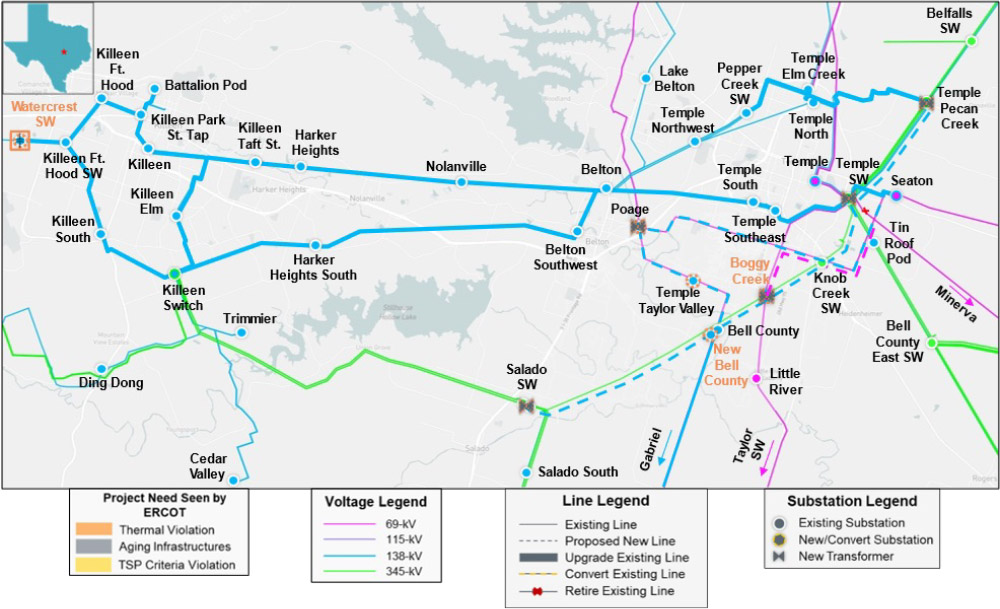

$272.6M Project Endorsed

TAC endorsed a $272.6 million regional project in Central Texas by adding it to the combination ballot. The Tier 1 project, requiring board approval, would address thermal violations in the Temple and Killeen area between Austin and Waco.

ERCOT staff said the Oncor Temple Area Regional Planning Group Project improves long-term load-serving capability, is the least-cost solution and requires the least amount of a certificate of convenience and necessity for the options that meet all ISO and NERC reliability criteria.

The proposed Oncor project in Central Texas | ERCOT

Oncor originally proposed a smaller project, but ERCOT staff’s study found additional thermal and voltage violations and recommended the alternative project after analyzing 11 options. The price tag more than doubles Oncor’s $120.7 million projection.

The project involves converting 69-kV circuits to 138 kV, upgrading more than 65 miles of 138-kV lines, removing existing 138-kV circuits from 345-kV structures, and building a new substation.

Error Forces NPRR’s Withdrawal

ERCOT staff told the committee it has pulled back an NPRR previously approved by TAC over an error in the protocol language that needs to be resolved before it can go to the board.

NPRR1215 clarifies that the day-ahead market energy-only offer credit exposure calculation zeros out negative values. However, ERCOT’s Austin Rosel said an error introduced an unintended change in the E2 credit formula by adding a price variable that wasn’t part of the original system design. Comments will be filed to address the error.

“We think this is the best way to get it back to get it corrected,” Rosel said.

TAC approved the change in June. It originally was scheduled to go before the board in August but will now have to wait until October.

Changes to CDR’s Methodology

Members approved two NPRRs in separate votes. NPRR1219 passed 21-2 with four abstentions; TAC’s consumer segment provided both dissenting votes and both abstentions. It proposes changing the methodologies for the capacity, demand and reserves (CDR) report’s preparation and incorporates a report release schedule. The NPRR also includes new definitions to support the methodology changes and revisions to address outdated terms and add clarity to the methodology descriptions.

Members raised concerns about using effective load-carrying capability (ELCC) for renewable resources and a rushed process and potential implications of changing the reporting methodology. They warned of confusion over differences in the CDR’s reliability metrics and ERCOT’s new reliability standard being developed.

TAC endorsed NPRR1230 23-2, with four abstentions. The four-person cooperative segment cast a dissenting vote and three abstentions over the proposal to establish a shadow price cap for congestion affecting interconnection reliability operating limits.

Members supported the measure because of its market-based approach and operational efficiency. It proposes to manage transmission flows with market mechanisms, rather than manual control room interventions. Cooperatives raised concerns about increased cost to load.

The combo ballot included three other NPRRs, another binding document request and a change to the Verifiable Cost Manual that, if approved by ERCOT’s Board of Directors as required, would:

NPRR1217: Remove the requirement for load resources and emergency response service resources to be deployed with a verbal dispatch instruction (VDI) from ERCOT.

NPRR1231: Provide more clarifications and improvements to the firm fuel supply service.

NPRR1233: Add a flat fee for federally owned generation units and adjust the weatherization inspection fee for transmission service providers.

OBDRR051: Align the methodology for implementing operating reserve demand curve to calculate real-time reserve price adder with system changes required for the emergency pricing program.

VCMRR040: Remove the need for ERCOT to buy an annual coal price index subscription for use in calculating the quarterly coal fuel adder. The VCMRR describes a methodology for a qualified scheduling entity to submit “actual coal fuel adders” similar to the current process for natural gas resources.

New York will convene a summit to address its two-pronged climate goal — accelerating renewable energy buildout while strengthening its economy.

The Future Energy Economy Summit will look at the role next-generation technologies could play in providing solutions to challenges such as deployment of dispatchable emissions-free resources, which are expected to be critical to grid stability as the state relies more heavily on intermittent wind and solar power.

The event also will look at ways new clean energy technologies could support the establishment and expansion of new commercial and industrial enterprises in New York.

State agencies and authorities working to advance the clean energy transition will host the summit Sept. 4-5 in Syracuse. Power producers, technical experts, and labor, environmental and business groups are expected to attend.

New York has some of the most ambitious clean energy goals of any state.

An important focus of the summit will be looking beyond the wind, solar and hydropower generation that constitutes almost all the renewables now being operated or built in New York.

Organizers are looking for input on other technologies, such as next-generation geothermal, advanced nuclear, clean hydrogen and long-duration storage. This will help inform state strategies on using these new resources and using them in a way that fosters economic development.

New York’s clean energy transition has slowed amid soaring costs and lengthy permitting and interconnection processes, and the agencies leading the initiative say the state is on track to miss its first clean energy milepost in 2030, possibly by a wide margin.

The state has responded by allowing developers to rebid projects at higher prices and by attempting to streamline the yearslong review processes facing projects.

Technology development is perhaps a more complicated challenge to solve, but one the state has been tackling for years, including by supporting pilot projects and research.

The state Public Service Commission in mid-2023 began the fraught process of determining what constitutes zero-emissions energy (Case 15-E-0302) for the purposes of complying with the landmark Climate Leadership and Community Protection Act of 2019.

The Future Energy Economy Summit is expected to provide further context for this effort by the PSC.

In her Aug. 5 announcement of the summit, Gov. Kathy Hochul (D) said: “Supporting our historic investments in renewable energy, this summit will bring together the brightest minds to explore how we can accelerate our progress, what potential roles next-generation technologies can play in stimulating economic growth and jobs throughout our state, and how New York’s innovation ecosystem can support these future industries.”

An unusually broad array of stakeholders contributed comments for the news release, reflecting the wide range of industry sectors and advocacy groups affected by the issues at the heart of the summit.

Xcel Energy says it relies on industry best practices and its own experience in beefing up wildfire mitigation plans for its operating companies.

In Colorado, where its affiliate faces nearly 300 lawsuits after the 2021 Marshall fire destroyed more than 1,000 homes, killed two people and caused more than $2 billion in property damage, Xcel recently filed a $1.9 billion wildfire mitigation plan that updates the previous one. It will serve as a template for wildfire mitigation plans in Texas and New Mexico and the company’s other states.

“I’m really proud of what we’re going to accomplish on the operational side to provide the real-time risk reduction that we need today to give us the time to make the necessary enhancements and system resiliency and hardening for our system over time,” Xcel CEO Bob Frenzel told financial analysts during the company’s second-quarter earnings call Aug. 1.

The Colorado plan integrates industry experience, incorporates evolving risk assessment methodologies, adds new technology and expands the scope, pace and scale of programs reducing wildfire risk, Frenzel said. It also benefited from the “hard work of the people that have come in front of us in California,” he said.

“We expect to dramatically reduce our wildfire risk based on their experiences and doing some of the lessons learned from all of those organizations. But that shouldn’t be taken as anything other than a huge focus that we also have in Texas and in [New] Mexico around our plans there,” Frenzel said.

Xcel has been linked to February’s Smokehouse Creek fire in the Texas Panhandle, the largest in state history. It has acknowledged its infrastructure likely started the fire. The company plans to file a resiliency plan in Texas for its Southwestern Public Service subsidiary later this year.

The Minneapolis-based company reported second-quarter earnings of $302 million ($0.54/share), as compared to the same period a year ago of $288 million ($0.52/share). Xcel’s ongoing earnings reflected the recovery of increased infrastructure investments and warmer than normal weather, partially offset by increased depreciation, interest charges and operations and maintenance expenses.

The company reaffirmed its year-end guidance of $3.50-3.60/share. It has met year-end expectations 19 straight years.

Xcel’s share price closed at $59.75, up 2.5% after the earnings release.

CAISO’s own systems may have contributed to a set of “operational surprises” that forced it to declare a series of energy emergency alerts in July 2023, a member of the ISO’s Market Surveillance Committee (MSC) said July 30.

“It is our understanding that CAISO/Western EIM operators were surprised by near-real-time changes in the CAISO/Western EIM supply demand balance on July 20 and July 25, 2023,” MSC member Scott Harvey, a consultant at FTI Consulting, said during a presentation at the MSC’s monthly meeting. “There are also indications that CAISO systems and operator actions may have contributed to operational surprises for Western EIM balancing area operators.”

High levels of self-scheduled exports out of CAISO’s balancing area to support stressed conditions in other parts of the West prompted the ISO to issue an EEA 1 on July 20 and EEA watches on July 25 and 26. (See CAISO DMM: High Exports to Southwest Led to July EEAs.)

On July 20, CAISO was close to being unable to deliver exports that had received hour-ahead awards, though no load was ultimately curtailed. But on July 25, the ISO was unable to award several thousand megawatts of self-scheduled exports.

As a result, CAISO imposed import limits from the WEIM into the CAISO balancing authority area between July 25 and Nov. 16, leading to increased transmission congestion in the 15-minute market and lower prices in the five-minute market, the ISO’s Department of Market Monitoring said in March. (See DMM: CAISO Transfer Limitations During Q3 Heatwaves Led to Price Disparities.)

Although the DMM previously said it was unclear why CAISO chose to implement transfer limits through November, Guillermo Bautista Alderete, CAISO’s director of market performance and advanced analytics, provided additional color by identifying two key market issues. The first, he said, was an inaccurate display of dispatchable capability in the market, where information presented to operators showed an imprecise calculation of storage resources, impacting operators’ ability to take proactive action.

“One of the purposes of that display and that information is to project how the ramp capabilities position for the near future,” Alderete said. “If they see that the ramp capability is getting thinner and thinner, they may start taking action rather than applying load conformance.”

The second was related to scheduling and tagging processes. When clearing transactions in the WEIM between Oregon and California, a change in practice led to double counting, which exacerbated congestion and kept flexible ramping product (FRP) “stranded in the north.”

Additionally, export reductions projected in the hour-ahead scheduling process (HASP) led to uncertainties in the real-time market due to exports not materializing.

“We had about 2,400 megawatts of additional demand that HASP was not projected as having to meet, and now the [real-time dispatch] has to meet that extra obligation in real-time,” Alderete said.

The issues weren’t fully addressed until Nov. 16, when the ISO stopped imposing transfer limits.

MSC Questions Flexiramp, HASP Structure

The “operational surprises” associated with July’s events also included problems identified with HASP and CAISO’s flexible ramping product (flexiramp).

While the role of HASP has “evolved dramatically” since it was implemented in 2014, the structure has not, Harvey said.

The HASP originated as a tool to schedule interchange transactions between CAISO and adjacent balancing areas in conjunction with the scheduling of CAISO balancing area resources. While HASP still serves that role, it “has developed into an hourly spot market for the purchase of capacity to meet the [WEIM’s] resource sufficiency evaluation,” Harvey said.

In 2014, almost all imports and exports scheduled in HASP were with balancing areas that didn’t belong to the WEIM. As of July 2023, nearly all imports and exports scheduled in HASP sourced or sank within the EIM.

As a result, stakeholders questioned the implications of the resource sufficiency evaluation of HASP transactions included in WEIM base schedules but not clear in HASP.

“A core issue is that when CAISO clears HASP to schedule hourly interchange between … CAISO and other Western EIM balancing areas, day-ahead market exports that do not clear in HASP improve the CAISO resource balance relative to the day-ahead market, appearing to increase supply in both … CAISO and the Western EIM,” Harvey’s presentation said.

“However, market exports that do not clear in HASP may be included in the base schedules of EIM entities,” it said. “The current HASP structure models the improvement in CAISO supply when day-ahead exports do not clear but does not model the potential reduction in Western EIM supply. Hence, HASP can appear to show a supply demand balance in the Western EIM when there actually is a large supply gap.”

If WEIM entities find out only after HASP posts that exports included in their base schedules will not flow in real time, they will have less time to take remedial action, as was the case in July.

“It seems that this HASP structure is creating an information problem, that it isn’t set up to tell us the truth for the Western EIM,” Harvey said. “It’s going to tell the truth for what the CAISO needs to do to avoid load shedding in terms of having supply that it can point to, but it isn’t looking necessarily at … the big picture.”

Harvey also questioned the effectiveness of flexiramp and pointed to its potential to create more “operational surprises.” In the case of July’s events, flexiramp product couldn’t reach CAISO’s balancing area due to congestion.

“If we’re going to reduce the load conformance, we have to make sure that the flexiramp is deliverable, and it looks to me like part of the problem on the 20th was that it wasn’t,” Harvey said.

Additionally, flexiramp is designed only to cover net load uncertainty and does not procure capacity in real time to cover all types of supply changes, such as those that occurred in July.

To avoid another emergency event, Alderete highlighted a few ways CAISO could improve.

“We have realized there needs to be better awareness for operators to get a sense of the wider picture, how many transfers they have and potentially give them more confidence of how much of those could be realized,” Alderete said.

Staff also took steps to increase transparency, including using market messages to communicate information on transfer limits.

“We realized that we could have communicated better, and I think we can do better for whenever the next time is going to be,” Alderete said.

SEATTLE — A new Washington program aims to help low- and moderate-income families lease or buy electric vehicles with some of the most generous incentives offered in the U.S.

Gov. Jay Inslee announced the Washington EV Instant Rebates Programat an Aug. 1 press conference in Seattle.

“We know the cost of EVs will come down quite rapidly, but we don’t want to wait,” Inslee said. “Everyone essentially will be able to get one for less than $200 a month” under the program, which will reimburse automakers and dealers who provide point-of-sale rebates to eligible residents leasing or purchasing an EV.

To be eligible, an individual or household must earn no more than 300% of the federal poverty level, said Mike Fong, director of the Washington Department of Commerce.

Fong said it was difficult to pin down precise annual income levels for eligibility but that the threshold would likely range from $45,000 for a single person to $93,000 for a family of four. Roughly 37% of Washington’s households sit below those thresholds.

The program will offer rebates of up to $9,000 for an individual or household obtaining a three-year lease on an EV, $5,000 for a two-year lease and $2,500 for a used EV lease. A $5,000 rebate will be available for the purchase of a new EV and $2,500 for a used EV.

The Washington program is expected to provide rebates to 6,500 to 8,000 residents by June 2025, which is when the $45 million appropriation from the state general fund expires.

A survey of common EVs sold nationwide shows most sell for between $40,000 and $75,000, though a new Nissan Leaf sells for roughly $30,000. A chart at the Aug. 1 press conference showed the monthly lease prices for seven models ranging from $104 to $199. The average monthly payment for gasoline-powered cars is about $700, according to the Washington Department of Commerce.

State officials said 26 EV models are sold in Washington and 122 auto dealers will participate in the program.

Washington’s program appears to offer the biggest EV rebates in the nation. A Kelley Blue Booklistingshows 49 states having either statewide rebates or a hodgepodge of in-state entities offering rebates. Washington’s maximum rebate, $9,000, would be more than double the size of the second-largest rebate.

Washington’s rebates can be used alongside a federal rebate of up to $7,500 for an eligible new EV and up to $4,000 for the purchase of a used vehicle.

More information on the Washington EV rebate program can be found here.

Washington had 194,232 passenger EVs (including both fully electric and plug-in hybrid vehicles) as of June 2024, according to the state’s Department of Licensing. To reach its targets on trimming statewide pollution, the state estimates it needs to have 265,735 passenger EVs on the road by the end of this year to be on pace to hit targets of 1,449,962 by 2030 and 3,135,799 by 2035.

Washington currently has 5,841 public EV charging ports for light-duty vehicles, with 4,546 regular chargers and 1,295 fast chargers. To hit state targets, Washington needs 3,912 regular chargers and 3,030 fast chargers by the end of 2025, according to the state’s Transportation Electrification Strategy.

These targets grow to 8,671 regular chargers and 6,926 fast-charging ports in 2030 and 13,068 regular and 10,522 fast-charging ports in 2035. This is for light-duty vehicles. Additional chargers will be needed for trucks and buses.

Commerce Department spokeswoman Amelia Lamb noted these figures do not include private charging ports for homes, for which current figures are incomplete. The targets for home-charging ports are 1,264,731 by 2030 and 2,944,207 by 2035.

Massachusetts’ 2023/24 legislative session closed in the morning of Aug. 1 without any significant climate or clean energy legislation despite broad agreement on proposed clean energy permitting and siting reforms.

The 19-month session came down to an unsuccessful last-ditch effort to reconcile the differences between separate omnibus climate bills passed by the House and Senate. Lawmakers continued to work into the late hours of the session’s final day but failed to reach a deal.

The separate climate bills passed by the House and Senate contained similar language to streamline and expedite permitting and siting for clean energy generation projects and grid infrastructure. This framework came out of an extended process of negotiations and stakeholder engagement. (See Mass. Commission Issues Recs on Energy Project Siting, Permitting.)

Dan Dolan, president of the New England Power Generators Association, called the failure to pass permitting reform a “huge opportunity missed with agreement among so many of the major elected and industry players.”

Beyond the permitting aspects, the Senate bill contained language intended to enable the state’s transition away from natural gas. It also sought a ban on the practice of competitive electricity supply and would have revamped the state’s clean energy procurement process.

Rep. Jeff Roy (D), the top House negotiator in the conference committee formed to resolve the differences in the climate bills, indicated to reporters that the failure stemmed from the Senate’s ambition to do “too much beyond” the permitting and siting reforms that were common to both bills. Meanwhile, Sen. Mike Barrett (D), the top Senate negotiator, pointed the blame at gas utility lobbyists for blocking common-sense gas reforms.

The Senate bill would have updated the state’s replacement program for leaking gas pipes, adding the option of pipe repairs and retirement. It also would have amended the utilities’ mandate to provide gas service to customers, “enabling the [regulatory] agencies to retire the natural gas system one block at a time when a technology exists to keep that block warm and safe through other means,” Barrett told NetZero Insider.

These proposals echoed the majority recommendations — issued in January — of a stakeholder working group focused on the issue. (See Mass. Gas Working Group Finalizes Recommendations to Legislature.) Within the working group, the gas utilities opposed several of the recommendations, including the proposal to enable the gas utilities to “terminate natural gas service to a customer” if other heating technologies are available.

Barrett said the gas reforms are essential to limiting overall energy costs for Massachusetts residents as grid infrastructure costs increase. He added that legislation addressing gas emissions likely is necessary for the state to meet its climate mandates, which include a 49% reduction in emissions from buildings by 2030.

Rep. Roy did not respond to comment requests in time for publication. He has indicated that permitting and siting reforms were his top issue for the session and appeared to be willing to pass a bill focused just on this issue.

In a statement, Executive Office of Energy and Environmental Affairs Secretary Rebecca Tepper emphasized the importance of permitting and siting reform to meeting the state’s climate mandates.

“We’ll continue conversations with the Legislature to pursue these reforms,” Tepper added.

Meanwhile, climate advocates expressed outrage that the legislature ended the two-year session empty handed.

“I am shocked and appalled that the Legislature has left the building with nothing to show for climate policy,” said Claire-Karl Müller, coordinator of the Mass Power Forward coalition. “Flood and fires and heat waves don’t adjourn for the summer, and this failure of action impacts real people’s lives.”

Larry Chretien, executive director of the Green Energy Consumers Alliance, said the failure to pass gas reforms will threaten the state’s climate goals, pointing to data that indicates building sector emissions in the state increased between 2020 and 2021, and likely increased between 2021 and 2022.

John Walkey of the environmental justice organization GreenRoots expressed dismay that legislators were unable to reach any compromises on climate and pointed the blame at top legislators.

“The way we’ve set up our legislature is such that nothing moves without leadership’s say,” Walkey said. “These folks need to be cutting deals and making things happen … we’re going to be fried to a crisp before our leaders get over their egos.”

Lawmakers have signaled their interest in returning prior to the next session to attempt to pass an economic development bill. Gov. Maura Healey (D) on Aug. 2 urged the legislature to return for a special session, and both the Senate President and the House Speaker have indicated a willingness to do so.

It’s unclear whether a special session would include work on a compromise climate bill. If lawmakers cannot pass the climate bill via special session, the conference committee could continue working while on recess this fall and try to pass a bill when the next session begins in January.

Climate advocates called on lawmakers to pursue a bill as quickly as possible, noting that permitting reforms — even if passed — would take significant time to be established and take effect.

“I think this really is a question of what is your political will to do anything?” Walkey said.

Despite above-average temperatures, the ISO-NE energy market value was down slightly in July 2024 relative to July 2023, ISO-NE COO Vamsi Chadalavada said at the NEPOOL Participants Committee meeting Aug. 1.

Driven by the elevated temperatures, ISO-NE hit its highest peak load of the year July 16 at 24,816 MW, he added.

Chadalavada also provided more information on the capacity scarcity event on the evening of June 18, which lasted about 25 minutes.

The scarcity conditions were caused by about 1,600 MW of generator outages and reductions and a 600-MW generator tripping offline, Chadalavada said. The capacity performance payment rate was $5,455/MWh, and ISO-NE collected $14 million in pay-for-performance charges from underperforming resources.

Votes

The PC voted to approve new data collection requirements for distributed energy resources. The new standards would include information on DER size, location and operating characteristics. Data is currently collected through voluntary submissions. (See NEPOOL Reliability Committee Briefs: July 16, 2024.)

The committee also supported updates to the financial assurance policy to account for the delay of the 19th forward capacity auction.

A recent webinar from Austin, Texas-based analytics firm Aurora Energy Research drew attention to promising and troubling trends alike in MISO’s interconnection queue process, including longer wait times, larger projects, solar’s significance and major transmission’s influence.

Joe Rand, energy policy researcher for Lawrence Berkeley National Laboratory, said the progression from MISO interconnection request to agreement in 2023 has lengthened to about 45 months, with natural gas projects moving the fastest and wind projects moving the slowest.

“The queue duration has become longer and longer,” Aurora researcher Annie Liu agreed during the July 31 presentation. She said while MISO’s approximately 300-GW queue has grown rapidly in the past two years, 40% of active projects in the queue have not begun interconnection studies.

While the wait times have increased, so, too, have the size of projects.

Rand said increasingly bigger solar and storage projects have entered MISO’s queue over the past decade, with the mean capacity of a solar plant entering the queue in 2022 now at 186 MW, up from about 100 MW in 2016. Rand also said the mean size of storage facilities has risen almost 500% in the past 10 years to about 200 MW apiece.

Rand said as of late 2023, 20% of proposed solar projects in MISO’s queue and 6% of proposed wind farms are planned as hybrid configurations with storage on site.

But Rand said the number of projects and capacity withdrawing from MISO’s interconnection queue is on the rise, as it is with other grid operators.

Aurora acknowledged the stronghold solar holds on the MISO queue.

Solar represents most of MISO’s interconnecting capacity at 166 GW; over the past three queue cycles, solar has accounted for 47% of projects, Aurora found.

Liu said that many of the solar and battery projects that entered the 2023 cycle are concentrated in the MISO Central region, which includes Michigan, Wisconsin, Illinois, Indiana and portions of Missouri and Kentucky. Liu said 21 GW of battery storage and 22 GW of solar projects from the 2023 class are vying for locations in MISO Central. But she said MISO South also is attractive to solar developers, with 24 GW of project potential entering 2023 cycle alone.

“There’s a strong developer interest in MISO South, especially in Arkansas and Louisiana,” Liu said.

Interest in storage is shooting up too, researchers said.

Aurora researcher William Eastwick noted that more than 60 GW of standalone battery storage projects have entered the queue in the past three cycles. They tend to select locations near solar hotspots, hoping to leverage a “technologic synergy” between solar and storage, he said.

Eastwick also predicted MISO’s long-range transmission plan (LRTP) portfolios will shape future developer behavior, with many opting to site projects near future lines.

He said while developers have “cooled off” on siting wind projects in Iowa — which now is notorious for curtailments and some of the lowest prices in MISO — MISO’s second, $25 billion LRTP portfolio has the potential to beckon developers again to Iowa, where new LRTP projects can transport wind generation to eastern load centers in Wisconsin and Illinois.

Aurora Energy Research MISO market lead Jose Munoz said developers should be able to make more informed siting decisions for their generation projects after MISO’s Board of Directors votes to approve the second LRTP portfolio at the end of the year. He added the 2023 class of potential capacity has a “strong correlation” with MISO’s first LRTP portfolio.

However, Eastwick said MISO’s recent stepped-up rules requiring more capital upfront and more financial risk have the “potential to affect cashflows” of MISO’s developers.

MISO last year doubled developers’ first milestone fee from $4,000/MW to $8,000/MW and instituted automatic monetary withdrawal penalties. The RTO still is attempting to find a plan that FERC can agree with to cap the number of megawatts it will accept annually into the queue. (See MISO Sets Sights on 50% Peak MW Cap in Annual Interconnection Queue Cycles.)

Munoz said MISO’s higher-stakes financial environment hasn’t deterred developers so far.

“Despite passing a suite of reforms making the interconnection queue process more restrictive, MISO saw the second largest queue cycle size to date, with 115 GW of capacity submitting applications to interconnect,” Munoz said.