Intense heat coupled with this summer’s early and active fire season likely will increase the need for public safety power shutoffs (PSPS) this year, according to utilities presenting at a California Public Utilities Commission workshop Aug. 7-8.

Southern California Edison COO Jill Anderson spoke about the “relentless heat waves” and “months of wildfires” that have hit the state this summer.

“We’ve been setting records, certainly in SCE’s service area and other places, and all of that for us is a reminder of how critical it is that we are ready with all the tools at our disposal to make sure that we can be managing and responding to extreme weather,” Anderson said. “We know that one of those tools — what we consider a last resort tool — is PSPS.”

PSPS allow utilities to temporarily shut off power in certain areas to reduce the risk of fires caused by electric infrastructure. Several utilities, including SCE, Pacific Gas and Electric, PacifiCorp, and San Diego Gas and Electric, discussed the summer forecast in their service territories, PSPS predictions, and methods of implementing and preventing power shutoff events.

The transition to the La Niña weather pattern, associated with decreased rainfall in California, could extend high fire danger conditions later into fall and winter and increase the number of PSPS events, the utilities noted.

“We’re concerned about the La Niña weather pattern because it historically correlates with more offshore wind days and also less precipitation, and these are not good markers for PSPS,” said Tom Brady, principal manager of business resiliency at SCE.

But that correlation isn’t always the case, Brady noted. In some instances, meteorologists have seen rains come early during La Niña weather patterns. Climate change also could weaken the relationship between La Niña and precipitation in Southern California, Brady said.

The utilities highlighted that above-normal precipitation this past winter and in the past few years contributed to the vegetation growth that is fueling wildfires across the state.

“August fuel levels are now at critical levels, and any moisture benefit from 2024 has mainly elapsed,” Brady said. “We’re in PSPS season, and in fact, we’re activated today for a small event with localized impacts on the border of Kern and Los Angeles counties. We can begin to expect larger events to begin occurring when weather patterns shift and we have more widespread high winds across our service territory.”

PG&E painted a similar picture, highlighting extreme weather conditions that have increased the likelihood of PSPS events.

Scott Strenfel, PG&E senior director of meteorology operations and fire science, said historically high temperatures have rapidly dried the fuels and “set the stage for what’s already been a very challenging fire season.”

“It is more probable than not that this will be a more active PSPS season compared to the last two years, just because of the danger of fuel,” Strenfel said. “But all of that is going to depend on how many wind events we get and the timing of rainfall that could occur before or after those dry wind events that we get from the northeast.”

Conditions are similar in SDG&E’s service territory, with hot temperatures, increased vegetation and high fire risk.

“It’s certainly not the forecast that a lot of us want to see going into the fall, but it is one that our situational awareness is very focused on, and we’re very prepared,” said Brian D’Agostino, vice president of wildfire and climate science at SDG&E.

‘Positive Trend’

The utilities all highlighted ways they’ve worked to prevent PSPS events through system hardening, undergrounding, sectionalizing devices and transmission switches, and using cameras and weather stations.

In 2023, SDG&E completed 72 miles of undergrounding, trimmed and removed 13,000 trees, conducted 15,000 drone inspections, implemented 60 miles of covered conductors and more. In 2024, the utility aims to implement 40 more miles of covered conductors, 125 miles of undergrounding, trimming and removing 11,000 more trees, and conducting 17,000 detailed asset inspections.

PG&E completed 664 miles of undergrounding between 2019 and 2023, hardened 1,664 miles of power lines, and installed 602 cameras and 1,424 weather stations. The utility plans to underground 250 more miles, harden 280 more miles, enable the use of AI for the cameras and continue to optimize the weather stations.

PacifiCorp has made similar progress, replacing over 95 miles of bare conductor with insulated covered conductor in 2023, undergrounding five miles of line, upgrading more than 35 reclosers, relays and circuit breakers, and installing over 4,000 non-expulsion fuses. The utility also implemented the FireSight model to identify areas of heightened fire risk, which led it to identify a new high fire-risk area. In total, high fire-threat districts encompass approximately 1,700 overhead line miles and 54% of PacifiCorp’s territory in California.

SCE implemented about 5,900 miles of covered conductor and 26 miles of undergrounding, trimmed or removed over 2 million trees, installed or replaced over 14,200 fast-acting fuses and 160 remote-controlled sectionalizing devices, and conducted over 1 million equipment inspections.

The utilities also highlighted the importance of artificial intelligence and machine learning in their modeling, forecasting and preparedness for PSPS events. For example, SDG&E is using machine learning at each of its 222 weather stations to train AI models to predict exactly which areas could experience a shutoff, allowing the utility to more accurately target notifications.

SDG&E also relies on three primary AI-based tools to enhance its PSPS response: gridded AI-based fuel models that provide a holistic look at fuel moisture content, machine learning wind gust models and AI smoke detection. The utilities also rely on enhanced powerline safety settings (EPSS), which allows powerlines to automatically turn off power within one-tenth of a second.

PG&E relies on outage and ignition probability weather models, as well as a fire potential index, to calculate the need for PSPS.

CPUC President Alice Reynolds expressed optimism despite predictions for increased PSPS events.

“I’m really pleased to see the progress that has been made on PSPS events over the last several years,” Reynolds said, noting that PSPS customer notifications across all utilities declined from 5.8 million in 2019 to about 500,000 in 2023.

“There’s a positive trend for the number of customers that have been de-energized … so clearly significant improvements,” Reynolds said.

VALLEY FORGE, Pa. — The Market Implementation Committee endorsed a PJMproposal to revise how the capacity offered by energy efficiency resources is measured and verified, rejecting competing proposals from EE providers and the Independent Market Monitor. The package passed with 65.5% support during the Aug. 7 MIC meeting. (See PJM Hears Proposals to Redesign EE Participation in Capacity Market.)

The proposal requires that EE providers demonstrate that capacity market revenues were the only factor in allowing a project to come to fruition and that it would not have occurred otherwise. The package also would reduce the period for which an EE project can participate in the capacity market from three years to one year after completion, which would address a possible delay in load-serving entity cost savings on lower peak load contributions (PLC).

Any EE megawatts that did clear the Base Residual Auction (BRA) under PJM’s proposal would continue to be tacked onto the load forecast in a process known as the addback, which is meant to ensure that EE cannot act on both the supply and demand side. A withdrawn proposal from CPower included language that would have opened a separate problem statement and issue charge to consider the continued role of the addback, which also is the subject of a FERC complaint filed by three state consumer advocates (EL24-118). (See PJM Consumer Advocates File Complaint on EE Market Design.)

The ability for EE to participate in fixed resource requirement (FRR) plans also would be eliminated on the grounds that the option has not been used and would be redundant, as cleared EE would be added back to the FRR obligation.

“It’s a complicated package, but if members choose and they want to keep energy efficiency as a market product, we think this package can help put those checks and balances in there,” PJM’s Tim Horger said while presenting the proposal Aug. 7.

The resource has been the focus of stakeholder attention over the past year, as PJM contends that under the current framework, EE providers have not demonstrated the capacity market revenues they receive have a causal link with reduced load and should not receive capacity market revenues until that link can be demonstrated. Several complaints have been filed at FERC during that time, alleging PJM’s market structure discriminates against EE, its treatment of market participants is unfair and EE resources have not demonstrated they meet the Reliability Pricing Model (RPM) participation requirements.

Presenting PJM’s first read of the proposal during the July 24 Markets and Reliability Committee meeting, PJM’s Pete Langbein said he believes there’s a large amount of “naturally occurring” EE from consumers wanting to reduce their carbon footprint or energy bills by buying more efficient devices. He argued those installations should not be eligible for BRA revenues.

PJM CEO Manu Asthana gave the example of a recent washing machine purchase he made, where the deciding factor was appliance features rather than the efficiency of the device. He said it’s possible it had a lower load than competing models and therefore would qualify for mid- or upstream EE programs that seek to use capacity market revenues to discount the purchase price, even though the purchase would have occurred regardless. While in aggregate EE programs may be successful in shifting consumer behavior in favor of reducing capacity needs, he said the capacity market isn’t entirely designed for that kind of cost allocation.

Several stakeholders said the causal link sets an impossible standard for EE providers to meet and would result in all programs being eliminated from the market.

Market participants proposed competing visions of how the accuracy of market participating EE could be improved. Affirmed Energy proposed a standardized approach for the measurement and verification (M&V) methodologies providers submit, an EE registration process akin to the rules around demand response, and third-party review for PJM’s verification. Mid- and upstream EE programs that use capacity market revenues to discount efficient devices in an effort to incentivize their purchase would not be required to obtain contracts with each consumer to offer the capacity associated with the energy savings into PJM’s market.

The Affirmed proposal initially sought to eliminate the addback by increasing the amount of EE data PJM incorporates into its load forecast. That component was dropped as the number of complaints pending at FERC regarding EE market design multiplied. The proposal received 2.2% support.

Greg Poulos, executive director of the Consumer Advocates of the PJM States (CAPS), said there’s a concern the addback leads to capacity market payments going to EE providers without any corresponding increase in reliability.

A proposal from Exelon aimed to preserve the ability for utilities administering EE programs on behalf of their states to enter savings into the capacity market by positing that programs run “under the direction, authorization and/or supervision of state public utility regulatory authorities are de facto qualified as EE capacity market products.”

The proposal also would differentiate the state directed, authorized and supervised programs from those offered by third-party EE providers with respect to the approval of M&V plans. Those plans outline how the EE provider intends to demonstrate the amount of capacity it will offer and validate that figure, as well as PJM’s evaluation of post-installation measurement and verification (PIMV) reports, where providers describe how they put those methodologies into practice.

Exelon’s Alex Stern said the utility believes that if PJM approves a M&V plan, it should not reject PIMV reports that accurately follow through on the described approach that has been reviewed and accepted by the states. The proposal received 37.2% support.

Stern said for as long as the states want their programs to have the ability to participate in the PJM capacity market, a distinction should exist between the rigor and regulatory scrutiny states already exercise over utility-run EE programs and EE that is bid into the capacity market by other EE market participants.

“We certainly don’t oppose other energy efficiency market participants … so long as the rules are fair. And by fair, I mean allowing opportunities for all, but [respecting] that the state programs are different in regard to measurement and verification,” he said.

The Independent Market Monitor proposal would go the furthest by removing EE from the capacity construct entirely, arguing that the energy savings have been incorporated in PJM’s load forecast since the 2016/17 delivery year and there is no basis in the tariff for keeping them in the market. Though the package received 54% support over the status quo, it failed to receive endorsement with a tie.

“The IMM’s proposal is the only one to recognize the current reality. EE is factually not a capacity resource under the tariff, EE is not in the capacity market, and PJM has not treated EE as a capacity resource since 2016. It is not PJM’s role to choose to subsidize EE outside the market. The lack of credible measurement and verification and the absence of causality make the subsidies even more unsupportable,” Monitor Joe Bowring told RTO Insider in an email.

He noted that the votes were not on a sector-weighted basis and the results of PJM’s proposal and the IMM’s proposal in a sector-weighted vote could be quite different, whereas rejection of the other packages likely would not have changed with sector weighting.

CPower withdrew its proposal during the Aug. 7 meeting, which focused on standardizing M&V and creating a separate process to reconsider the addback. It threw its weight behind the Exelon package while urging stakeholders to vote against the proposals from PJM and the Monitor.

“The Market Monitor’s proposal would by definition eliminate [EE] from the market … and as others have noted as well … the PJM proposal would de facto eliminate it because it continues to include this unmeetable 100% causality test,” CPower’s Aaron Breidenbaugh said.

CPower Complaint on PJM Guidance Ahead of 2025/26 Auction

In a July 17 complaint to FERC, CPower argued PJM has improperly taken a step toward implementing some of those changes, in contravention of the reigning tariff and manual language. It did so by issuing a guidance document on June 13 that informed EE market participants that it was limiting the project installation years eligible to participate in the 2025/26 BRA to the 2023/24 and 2024/25 delivery years.

The document also revised how PJM determines the standard baseline used for measuring EE savings for lightbulbs, requested documentation showing that providers hold exclusive capacity rights, and added a process where the Monitor can review PIMV plans to provide comments and recommendations to PJM (EL24-128).

The complaint asks FERC to allow CPower to participate in the Incremental Auctions (IAs) for the 2025/26 delivery year under the status quo rules and establish a settlement process or an administrative law judge to mediate disputes around PJM’s market rules for EE in the 2025/26 BRA. The amount of EE that cleared in the 2025/26 auction fell to 1,459.8 MW from 7,668.7 MW for the prior year.

CPower argued that the PJM tariff and the 2010 FERC order establishing EE participation in the RPM hold that resources can offer into four auctions and that limiting that period would constrain participants’ ability to use past projects as replacement capacity to cover any shortfalls caused by new installations not being completed by the start of the delivery year.

The change to the standard baseline resulted in LED lightbulbs being set as the standard practice for consumer behavior. The standard baseline determines the device that more efficient devices included in EE plans are measured against. CPower argued that the shift was made with little evidence that it reflects typical consumer behavior, stating that a memo sent from Apex Analytics to Rutgers University staff was the basis for the change.

“PJM does not offer any robust sets of studies or analyses about standard practice. It conducted no stakeholder process to seek input on standard practice. Allowing PJM to issue edicts about what standard practice is throughout the region with alleged support as flimsy as the Apex memo would set damaging precedent and allow PJM to wield an inordinate amount of power outside of the commission’s just and reasonableness FPA [Federal Power Act] review process, both as to EE and beyond,” the company wrote in its complaint.

The company took issue with including the Monitor in the approval of PIMV reports on the grounds that complaints have been filed against EE providers by the Monitor, calling into question whether it can be impartial and independent when reviewing reports submitted by those parties. CPower said it received two letters from the Monitor on June 26 stating it would recommend PJM not approve its M&V plan for the 2025/26 delivery year unless the company provided several items to the Monitor, including its justification for opposing PJM’s June 13 guidance.

“PJM is thus effectively denying CPower’s ability to withhold from the IMM what amounts to discovery outside of a commission-mandated process. Given the consequences of not providing the information, which included precluding its participation in the upcoming BRA, CPower had no real choice but to provide it to the IMM, despite its legal objections,” CPower said.

PJM responded on Aug. 5, stating that the tariff language provides that EE may participate in the auction for four delivery years but does not mandate it. It also argued that the M&V review is within the Monitor’s scope and responding to its inquiries is a condition of PJM membership.

“CPower unreasonably claims it is entitled to a four-year installation period for EE projects that clear a BRA even under a compressed auction schedule when two of the delivery years have already been completed and the load forecast reflects those efficiency projects as having already been installed. CPower’s position is irrational from an economic or operational perspective and is grounded in a gross misinterpretation of the tariff, RAA and PJM Manual 18B,” PJM said.

PJM Argues Addback Necessary to Implement EE

PJM has responded to a complaint filed by the New Jersey Division of Rate Counsel, Maryland Office of People’s Counsel and Illinois Citizens Utility Board arguing that the RTO’s use of the addback deprives consumers of the reliability benefits EE can offer while still requiring them to pay market participants. Given the significance of the addback, they also state that it should be enshrined in the governing documents, rather than business manuals, and be subject to FERC review.

In a July 10 response, PJM said the addback is necessary to avoid contravening tariff language prohibiting the double counting of EE resources as a capacity resource while also reducing peak load forecasts. PJM argued that the addback is envisioned by the tariff and can be accomplished through the manuals under the “rule of reason” as a mechanism to implement tariff language. Without the addback, it said the reliability requirement for the 2024/25 BRA would have been 142,973 MW, short of the 151,631-MW peak summer load requirement.

“The addback was designed to address changes in the methodology for determining the PJM load forecast to preserve the ability of EE resources to qualify for capacity payments as they had under the previous load forecast methodology. Thus, far from being a ‘fundamental change’ that undermined the participation of EE resources in RPM auctions, as complainants argue, the introduction of the addback preserved the status quo for EE resources seeking to receive capacity commitments,” PJM wrote.

Both Advanced Energy United and the PJM Power Providers submitted comments supporting the consumers’ call for FERC to convene a technical conference to consider the addback and EE market design more thoroughly.

In its July 10 complaint against PJM, the Monitor also argued that PJM’s implementation of the addback violates the tariff, stating that EE is permitted to offer capacity only for savings that are “not reflected in the peak load forecast prepared for the delivery year for which the energy efficiency resource is proposed.” The complaint says PJM should have eliminated EE from the capacity construct once it revised its load forecast approach to include EE data produced by the Energy Information Administration’s Annual Energy Outlook (EL24-126).

“When EE was added to the forecast and EE was removed from the capacity market, PJM should have simply followed the tariff, recognized that EE was not capacity, recognized EE resources do not meet the definition of EE resources in the filed tariff and eliminated payment to EE resources. Instead, PJM recognized that EE resources are not capacity, stopped including EE resources in the capacity auction, and began to pay EE resources an uplift payment equal to the capacity market clearing price without making any provision for such payments in the filed tariff,” the Monitor wrote.

PJM responded that the addback is permitted under the rule of reason and that it cannot change the results of the 2024/25 BRA because of the filed rate doctrine, citing a March 2024 3rd U.S. Circuit Court of Appeals decision rejecting a post-auction change to a regional reliability requirement. (See 3rd Circuit Rejects PJM’s Post-auction Change as Retroactive Ratemaking.)

The New Jersey Board of Public Utilities asked FERC to reject the Monitor’s request to cease EE payments, consolidate the remainder of the complaint with the consumer advocates’ filing and convene a technical conference centered on EE’s role in the capacity market.

“The New Jersey BPU supports a holistic review of [energy efficiency resource] eligibility and discussions around whether including EE in the market clearing mechanism is preferable to the EE addback. However, this decision must be the result of a process that allows for participation and input from all relevant stakeholders,” the board wrote.

PJM Responds to Monitor Complaint Against EE Providers

In a July 3 response to a complaint filed by the Monitor alleging that several EE market participants have not demonstrated they were eligible to participate in the 2024/25 and subsequent capacity auctions, PJM defended its approach to reviewing PIMV reports and said the Monitor proposed an unworkable approach to determining what qualifies as EE (EL24-113). (See Monitor Alleges EE Resources Ineligible to Participate in PJM Capacity Market.)

The complaint argued that EE mid- and upstream programs must be able to demonstrate that the more efficient products purchased with EE rebates actually were installed and are being operated within the PJM footprint. It asks the commission to either bar the EE providers from receiving capacity revenues in the 2024/25 delivery year or open an investigation to determine eligibility.

“For instance, short of conducting on-site audits for every location where EE is claimed right before the start of each delivery year, it is unclear whether any other methodology or estimate would satisfy the Market Monitor’s allegation that the post-installation M&V reports fail to establish that the indicated energy efficiency sellers have actually installed the resources in homes or businesses,” PJM wrote. “However, such an approach would clearly [be neither] feasible nor cost-effective given that 7,716 MW of EE resources cleared the capacity auction for the 2024/2025 delivery year alone, which could include tens of thousands, or even hundreds of thousands, of individual end-use customer sites that would need to be audited.”

While PJM agreed that improvements should be made to measurement and verifications, it said that should be done through the stakeholder process instead and indicated it plans to file M&V changes within the coming months. It also stated it intends to solicit an independent third party with expertise in EE to review the PIMV reports submitted for the 2024/25 delivery year.

“These audits will confirm or amend the final nominated EE value and capacity performance value for the EE resources that comprise the indicated energy efficiency sellers’ portfolios for the 2024/25 delivery year,” PJM said.

The American Council for an Energy Efficient Economy commented that a technical conference would be the proper forum to resolve the dispute and that the approaches favored by PJM and the Monitor would constrain EE’s ability to participate in the capacity market.

“ACEEE believes that PJM and IMM are not appropriately assessing the benefits of energy efficiency, not assigning it its deserved value and trying to kill its role in capacity markets to the detriment of electricity consumers. Energy efficiency with appropriate evaluation belongs in the capacity system, both to benefit consumers and to ease growing demand for new electric generation,” the trade group wrote.

The Environmental Law and Policy Center argued that the Monitor’s complaint is a collateral attack on past FERC orders mandating the ability for EE to offer capacity.

Echoing policies he laid out early in his administration, Nevada Gov. Joe Lombardo released a climate plan that calls for keeping natural gas in the state’s energy mix.

Lombardo on Aug. 8 announced the release of the Nevada Climate Innovation Plan, which “seeks to mitigate the changing patterns of the environment, while also considering economic realities and national security,” according to a release.

The plan said Nevada needs to find ways to maintain energy reliability while also “potentially decreasing emissions … over a sensible time frame.” That means an approach that includes natural gas, solar, geothermal, hydroelectric, wind, hydrogen, energy efficiency and energy storage projects.

“Nevada can’t persist with the mentality that everything must transition to sustainable energy overnight,” the plan said.

Statements in the new plan are consistent with what the Republican governor said in a March 2023 executive order that called for “diverse energy options” in the state, including natural gas and renewables. (See New Governor Seeks Shift in Nevada Energy Policy.)

Lombardo’s goal of having an energy portfolio that includes natural gas prompted the governor to pull Nevada from the U.S. Climate Alliance last year. (See Nevada Exits US Climate Alliance.)

Nevada’s new climate plan stands in contrast to the state’s 2020 Climate Strategy, developed under previous Gov. Steve Sisolak (D), which called for transitioning away from natural gas to meet the state’s 2050 net-zero emissions goal.

Minerals, Rangeland

The new Climate Innovation Plan sets broad goals in areas such as regulatory reform and economic and educational opportunities.

One objective is to modernize the state’s energy infrastructure — a goal that comes with a caveat.

“With the undeniable effects of inflation occurring across the nation, we must be mindful of cost,” the plan said.

Another section of the plan, focused on rangeland management, lists wildfire prevention strategies such as controlled burns, strategic grazing and invasive species removal.

The plan points to critical mineral production in Nevada, as well as the state’s “Lithium Loop” — a U.S. Economic Development Administration-designated technology hub. The hub plans to grow technology across the full lifecycle of lithium batteries, from lithium extraction and processing to battery manufacturing and recycling.

The EDA last month recommended the tech hub for $21 million in grant funding.

The climate plan criticizes the federal government for taking actions including national monument designations that have blocked access to critical mineral assets in the state. More than 80% of Nevada land is federally controlled, the plan noted.

In March 2023, Lombardo blasted the Biden administration for its designation of the Avi Kwa Ame national monument, which the governor said would disrupt rare earth mineral mining in Southern Nevada.

“The federal confiscation of 506,814 acres of Nevada land is a historic mistake that will cost Nevadans for generations to come,” Lombardo said in a statement at the time.

Climate Actions Underway

More than 20 pages of the 33-page Climate Innovation Plan are devoted to climate initiatives already underway within various state departments.

Among the programs listed is an incentive for residents to replace older wood-burning stoves with cleaner-burning models. In the Governor’s Office of Energy, the Renewable Energy Tax Abatement (RETA) program gives sales- and property-tax breaks to eligible renewable energy projects.

The Nevada Division of Environmental Protection received a $3 million planning grant from the U.S. EPA to develop a short-term Priority Climate Action Plan (PCAP) and a more in-depth Comprehensive Climate Action Plan (CCAP). (See Nevada Draft Climate Plan Outlines GHG-reduction Priorities.)

The PCAP was completed this year. The CCAP is due in July 2025.

Board Approves 36% PRM for Winter over Stakeholder Objections

ST. LOUIS — SPP directors and state regulators have approved the grid operator’s first winter planning reserve margin, endorsing a base PRM that is 3 percentage points higher than many of its utilities wanted.

The Board of Directors during its Aug. 6 meeting approved a 36% PRM for the winter season and a 16% margin for the summer season, effective 2026/27 and 2026, respectively. In doing so, the board sided with the Regional State Committee’s recommendation over that of the Market and Operations Policy Committee, which endorsed a 33% winter PRM.

The approval of the tariff change (RR622) capped months of discussions and deliberations by several stakeholder groups, including the Resource Energy and Adequacy Leadership (REAL) Team that is responsible for resource adequacy issues. (See SPP Markets and Operations Policy Committee Briefs: July 16-17, 2024.)

“I’m very disappointed that we did not agree to common ground with implementing the PRM,” SPP CEO Barbara Sugg said after the vote. “There are things I want to focus on that we all agree with. We agree that we have to get more steel in the ground, and we can’t do that fast enough. We agree nobody wants to explain why we have to shed load or why we’ve been turning away load. Nobody wants to tell customers why the rates are going up. It goes without saying nobody wants to find themselves paying for [RA] deficiencies.

“Again, I’m disappointed when we can’t reach consensus. It’s not who we are. But I know we all want the same thing. We want a reliable, affordable system. We have more work to do to achieve that.”

SPP said the action marks the first time a winter PRM requirement has been defined separately from the summer requirement and was necessary to ensure member utilities acquire enough generating capacity for both seasons. The RTO’s load-responsible entities must have access to enough generating capacity to meet their peak consumption by at least a 36% margin during the winter and at least 16% margin during summer.

The grid operator says severe extreme weather has become “increasingly common” in recent years. The February 2021 winter storm forced SPP to shed load for the first time in its then-80 years of operation. During the December 2022 winter storm, the RTO’s staff was forced to curtail almost 6.5% of demand to prevent uncontrolled outages after a higher-than-expected level of coal-fired generator outages and derates.

“Winter is becoming our trouble season,” RSC President John Tuma said.

SPP’s 2023 loss-of-load study, the first to directly analyze seasonal risk beyond summer, found that a 15% PRM would not meet a 1-in-10 loss-of-load expectation in either season.

The grid operator’s Market Monitoring Unit said it saw 36% as a minimum threshold. It preferred a 37% PRM to allow for extra maintenance outages during winter.

Tuma likened SPP’s quest for the appropriate resource adequacy requirements to a fellowship’s travails straight out of fantasy novels.

“It’s a long journey that we’re on here at SPP … We’re at one of those points where you have a difficult lift,” he said. “You see that the trail turns ahead of you, and you don’t know exactly where it goes. This is difficult stuff. We understand that, but it’s unclear what’s coming around the corner, and we still need to go forward.”

“I wish someone would put together a trajectory that was giving us a pathway to growth and future … so that we know how much water to pack,” American Electric Power’s Richard Ross said. “I don’t want to get down that target and find out we’re going another 20 miles and not having enough water. Let’s not go on that trail and not be prepared.”

Ross was one of 12 Members Committee representatives to oppose the 36% PRM in the committee’s advisory vote for the board, with eight in favor and three abstentions. He said MOPC’s 33% recommendation “strikes the proper balance between what is needed to maintain reliability in the system and what is actually achievable, given the situations that we have.”

“What we really need to do, though, is figure out what we’re going to do for the long term, so we don’t yet again repeat this exact same conversation where SPP is cranking up the reserve margin,” Ross said. “I think you’ve heard from everyone that it takes five to six years to bring a resource online.”

“At 36%, the region as a whole has enough capacity to meet that requirement, but in all likelihood, the reality is a number of LREs [load-responsible entities] would be short in the near term,” said MOPC Chair Alan Myers, with ITC Holdings.

However, Xcel Energy has issued a request for proposals as it faces the need for more than 3 GW of accredited capacity in its Southwestern Public Service (SPS) footprint. Arkansas Electric Cooperative Corp. CEO Buddy Hasten has said the organization will have to spend $2 billion on new dispatchable generating capacity to meet the requirements.

Tuma agreed that staff, the REAL Team and several stakeholder groups recognize the need for “critical, long-vision steps” beyond the current path.

“We’re soberly going into this knowing that there’s a lot more work in front of us. SPP is on an industrial transition, and it’s not going to be cheap,” he said. “We need to take this back to our commissions, take it back to our state leaders. It will cost money, but we need to do it smartly and wisely. If we don’t do it as part of SPP or MISO, it will be more costly. This is where reliability happens.”

Texas Public Utility Commissioner Lori Cobos cast one of two dissenting RSC votes against the 36% requirement, expressing concern over rising rates and supply chain issues that have increased construction costs.

“The challenge that I have on my end is trying to get to a place where I believe my LREs can feasibly work on these reserve margins that are coming in the next several years in a feasible but also affordable manner,” she said.

The board and RSC also approved a fuel assurance policy (RR621) that SPP says will further strengthen RA policies by placing additional emphasis on conventional resources’ performance during the season’s most critical hours and reduce the PRM’s socialization of capacity allocation.

The MC unanimously endorsed the change, with the Natural Resources Defense Council abstaining.

Rate Cap Increased 10.8%

The directors and members both approved the Finance Committee’s recommendation for a 10.8% increase in SPP’s rate cap, from the 46.5 cents/MWh set in 2021 to 51.5 cents/MWh, effective next year.

FC Chair Stuart Solomon said the bump in the rate cap is in line with previous increases that have averaged 11.2% every three years and will serve as a bridge between the current cap and projected expenses through 2028. He said the compound annual growth of inflation has outpaced the billing units and net revenue requirement (NRR) from 2018-2024.

SPP calculates its rate cap by dividing the budgeted NRR, including a true-up from prior periods, by the estimated amount of transmission service to be provided under the tariff in the coming calendar year.

“The rate cap is a longer-term planning measure that provides predictability for planning purposes,” Solomon said. “SPP has shown the cost-control over time, from 2018 to the present day, as the services increased very significantly over that period.”

More services mean additional staff, but Solomon noted the RTO’s staff ran a “whole lot” of model runs, all of which indicated a need to increase the cap.

The MC endorsed the increase with a 19-4 vote. AEP, Google, Oklahoma Gas & Electric and SPS all voted against the measure. Several members said they will support the rate increases but will focus more closely on the budget, which will be brought before stakeholders and the board in October.

“I am sympathetic [that] FERC’s continuing orders are getting more and more responsibility into the hands of the RTO. More and more compliance,” said Denise Buffington, Evergy’s director of federal regulatory affairs. “I just encourage the organization to continue their focus on their core mission. It’s nice to have staff, but really, how do we get steel in the ground, how do we get generation connected, how do we get transmission planned in an appropriate way? I will be looking at the budget very closely.”

GI Waivers to be Filed

The board approved staff’s proposal to file two waiver requests with FERC following a unanimous vote by the MC that will help SPP clear the backlog in its generator interconnection queue.

The first waiver would allow SPP to delay the 2024 definitive interconnection system impact study (DISIS) cluster’s first phase. The phase would begin after the 2023 DISIS second phase’s restudy is completed and posted in August 2025; without the waiver, the phase would start before the second phase of the 2022 and 2023 clusters and likely lead to unplanned restudies, staff said.

The second waiver would pause the opening of the 2025 DISIS cluster. Together, staff say they will ease conflicts with their effort to clear the GI queue’s backlog and transition to a new planning process. (See “DISIS Waivers Endorsed,” SPP Markets and Operations Policy Committee Briefs: July 16-17, 2024.)

“This really just reflects the reality of the situation that we’re in, in terms of the sheer magnitude and our customers’ generation figures that we’re seeing in the restudies that are resulting from that,” said Natasha Henderson, senior director of grid asset use for SPP.

“I know efforts to clear the queue are challenging … but it’s not fast enough,” Buffington said. “I still have a lot of concerns about the timing. We’re just asking you to be creative about how we can get the process moving more quickly. There’s a lot of concern about alleged queue jumping, but at some point, we’ve got to cut out speculative developers and get a concrete study and concrete development.”

SPP plans to transition to the consolidated planning process (CPP) in late 2026 after a transition period. Opening the 2025 DISIS would mean the cluster’s generation would “significantly” overlap with the CPP’s transition study and first annual assessment.

FERC’s approval of the waivers would enable the timely completion of backlog studies and allow time to further develop CPP. The grid operator has 416 requests in the GI queue totaling about 84 GW in proposed capacity, down from the original backlog of 1,139 requests for 221 GW of capacity.

SPP Responds to Deficiency Letter

CEO Sugg said staff are working to address FERC’s questions about the Markets+ tariff filing and “some of its nuances, particularly transmission usage.”

The commission on July 31 filed a deficiency letter asking the RTO to address 16 issues with its proposed day-ahead market offering in the Western Interconnection. FERC gave SPP 60 days to respond. (See FERC Finds SPP Markets+ Tariff ‘Deficient’ in Several Areas.)

“We’ve been working on formulating a response,” Sugg said. “We anticipate filing the response to those questions in the deficiency letter within the next 60 days.”

The Markets+ Participant Executive Committee has set aside an hour during its Aug. 13 meeting in Westminster, Colo., to discuss the deficiency letter with SPP legal staff.

OCC’s Hiett Leaves RSC

Oklahoma Corporation Commissioner Todd Hiett was a no-show for the RSC meeting Aug. 5, two days before he would give up his seat on the committee to seek treatment for alcoholism.

OCC staffer Jason Chaplin represented the state in Hiett’s absence.

Hiett, the RSC’s vice president, also stepped down as the OCC’s chair Aug. 7 but remains on the commission. Some lawmakers have asked for a special session to impeach Hiett. His fellow commissioners have called for his resignation and an independent investigation following two instances of public drunkenness and allegations of sexual misconduct. Hiett has refused to resign but offered to step down as chair.

The OCC elected Vice Chair Kim David as its new chair, and she will replace Hiett on the RSC.

The allegations against Hiett were first publicized last month by The Oklahoman, which reported that one incident occurred June 9 in the lobby of the hotel where the Mid-America Regulatory Conference was being held in Minneapolis. Hiett acknowledged to the newspaper that he had had too much to drink but could not remember any of his alleged actions.

In an additional piece of business, the RSC selected an “F Troop” as its Nominating Committee: Kansas’ Andrew French, Louisiana’s Mike Francis and South Dakota’s Kristie Fiegen. They will be responsible for selecting the committee’s 2025 term leadership.

2025 Operating Plan Endorsed

The board’s approval of its consent agenda included SPP’s 2025 operating plan, as recommended by the Finance and Strategic Planning Committees.

The plan is meant to provide a reference point for the highest priorities that will drive “significant” long-term gains for SPP and its members.

The consent agenda also contained recommended in-service date changes for a pair of competitive project certificates of convenience and necessity (CCNs) recently awarded to NextEra Energy Transmission Southwest (NEET SW). Staff urged approval of the transmission developer’s new in-service dates for its 345-kV Wolf Creek-Blackberry project in Missouri and Kansas and the 345-kV Minco-Draper line in Oklahoma, from Jan. 1, 2025, to July 15, 2025, and from July 1, 2024, to Jan. 31, 2025, respectively.

Staff also recommended new language for Evergy Kansas’ 345-kV Wolf-Creek-Waverly line to include re-termination at Wolf Creek, allowing NEET SW’s Wolf Creek-Blackberry project to progress without crossing the two lines.

The consent agenda additionally included: Emeka Anyanwu’s (the CEO of Lincoln Electric System) nomination to fill a vacant transmission-using member’s seat on the Human Resources Committee; cost increases for a 138-kV Western Farmers project and Omaha Public Power District upgrades; a sponsored upgrade study for terminal equipment at several Western Area Power Administration substations; and the withdrawal of NTCs for Western Farmers substation work and SPS 115-kV terminal upgrades.

Finally, the agenda had two tariff changes that:

RR602: add process structure, tracking and improved criteria for evaluating potential transmission reconfigurations.

RR619: add application programming interfaces as an acceptable submittal process.

California energy agency heads appearing before state lawmakers Aug. 6 pitched the proposed CAISO governance changes being developed by the West-Wide Governance Pathways Initiative, saying that expanding the ISO’s electricity market will provide for increased reliability and cost benefits for state residents.

Though the initiative has been in the works since last year, the state Senate Energy, Utilities and Communications Committee discussed the topic for the first time during an oversight hearing on electricity reliability. Representatives from CAISO, the California Energy Commission (CEC) and the California Public Utilities Commission (CPUC) participated.

The agency leaders outlined the purported advantages of giving the Western Energy Markets (WEM) Governing Body increased authority over CAISO’s Western Energy Imbalance Market (WEIM) and Extended Day-Ahead Market (EDAM). They also touched on the Pathways Initiative’s evolving plan to establish an independent Western “regional organization” (RO) that eventually would assume more of the ISO’s market functions. (See New Western ‘Regional Organization’ Could be Folsom-based.)

Electricity markets in the West are “very fragmented,” Alice Reynolds, president of CPUC, told the committee. “So, this effort is really thinking about the benefits of a larger market, meaning, think about a market with a footprint that is larger than any one weather event.”

Reynolds said a shared market would allow stakeholders to optimize resources for reliability and tackle different weather events while also maximizing cost savings for ratepayers. However, she noted that proposed changes under the Pathways Initiative would not involve alterations to CAISO’s balancing authority area, a key concern for California labor groups that blocked previous legislative efforts to “regionalize” the ISO and now say they support a bill to enact the Pathways plan. (See California Labor Groups Affirm Support for Pathways Proposal.)

Sen. Henry Stern (D) asked what additional economic benefits California ratepayers could expect from the state’s participation in the EDAM compared with those currently seen in the WEIM, which provided its participants $365 million in estimated benefits during the second quarter of 2024, according to CAISO. (See WEIM Yields $365M in Q2 Benefits with Hot Start to Summer.)

CAISO CEO Elliot Mainzer said EDAM could double those benefits “on just the economic side” but emphasized the impact of an expanded market on reliability.

“The reliability element is becoming increasingly important. I think as you see the reduction in the number of energy emergency alerts, that’s our goal,” Mainzer said. “We want to keep the system calm. We want to have that wide area of visibility. We want to understand not only what’s happening in California, but what’s happening in the broader West, so that on a day-ahead basis, we’ll have the ability to move power to where it’s most needed, given the capabilities of the transmission system.”

‘Really Good Proposal’

On May 31, the initiative’s Launch Committee unanimously endorsed Step 1 of the “stepwise” proposal issued in April. The Launch Committee presented CAISO with the proposal on June 5, which would revise CAISO’s WEIM charter to elevate the oversight position of the market’s Governing Body over WEIM/EDAM matters to “primary” authority, rather than the “joint” authority it currently shares with the ISO’s Board of Governors.

CEC Vice Chair Siva Gunda said the proposal focuses on furthering the independence of CAISO’s governance structure “to have more people feel confident and comfortable to join the EDAM.”

He noted the proposal also clarified the dual filing — or “jump ball” — process that would occur if the CAISO board disagrees with a market rule filing approved by the WEM Governing Body and submits a parallel filing with FERC.

“There will be a dispute resolution if the boards don’t agree,” Gunda said. But “if the dispute resolution did not bring the two boards together, there is a jump ball filing to FERC, meaning both boards can put their proposal to FERC.”

The CAISO board is expected to vote on the first step of the proposal during a joint meeting with the WEM Governing Body later this month.

Gunda told the senators the Pathways Launch Committee expects to issue a proposal on the effort’s next steps in the fall. (The committee is targeting a Nov. 15 release.) Not explicitly described by Gunda but widely understood by industry stakeholders is that the Step 2 proposal will cover the changes to California law needed to migrate some of CAISO’s market functions to the RO, give the RO sole authority over the WEIM/EDAM and allow the ISO to participate in the new entity.

“I just hope you take the next step,” Stern said. “I think you put a really good proposal on the table.”

However, Sen. Kelly Seyarto (R) questioned whether there has been enough outreach to inform the public about the initiative’s implications, saying, “this is the first time I’ve even seen this.”

“I don’t know what our outreach is to the public and when those meetings are, but this is something important for people to understand,” Seyarto said.

“If it’s something that is just kind of part of a box to check off, ‘oh yeah, we did public meetings, we did this, and now we’re doing this,’ you’re going to have a lot of pushback from the public. Because anything that they think might raise their rate right now — they’re hypersensitive to it,” Seyarto added.

Keeping trees near electric wires trimmed back may not save those wires from damage in a hurricane or tropical storm if branches are flying and trees are uprooted outside a utility’s right-of-way, said ERCOT CEO Pablo Vegas.

A big storm, with wind and rain, “can create an environment where trees can fall from outside of the right-of-way into it and create just as much damage,” Vegas said during an Aug. 7 online briefing on the grid impacts of extreme weather, hosted by the U.S. Energy Association.

When Tropical Storm Beryl recently roared through Texas, “there was a lot of the vegetation outside of the utilities’ right-of-way that came into play,” Vegas said, “We’re starting to have conversations about ― how do we work more closely with homeowners who can see risky vegetation that could be compromising the electric infrastructure that happens to be outside the right-of-way?”

Driven by increasingly frequent and disruptive weather intensified by climate change, discussions of grid reliability and resilience ― defined as the ability to bounce back after such events ― have become industry imperatives, regularly included at conferences and online forums like the USEA briefing.

What’s new, according to Vegas and other speakers at the Aug. 7 event, is the growing power demand from data centers, and the opportunities and challenges it creates, all of which must be factored into plans for extreme weather.

Rather than seeing data centers as passive load requiring firm, baseload power, Vegas looks at the massive new installations as potential grid assets that could help maintain equitable access to electricity for all customers.

Backup generation at data centers, critical for ensuring 24/7 power, could be used for emergency demand management, he said. “We could lean on those customers and say, ‘Hey, we need you to disconnect from the grid for a short period of time. We need to you to use your local generation to alleviate the pressure, so that those who don’t have [backup power] will have adequate capacity to serve during this time of scarcity.”

Andrea Staid, principal technical lead at the Electric Power Research Institute (EPRI), talked about the need to expand ideas about what “extreme weather” might mean as climate change affects all forms of power generation.

“Extreme from a weather perspective might no longer be extreme from a system stress perspective when you’re thinking about the grid with increasing renewables,” Staid said. “Wind lulls and solar droughts … are extreme from a resource adequacy perspective, but not so much from a pure weather perspective.”

EPRI researchers look at interregional transmission as one possible solution as renewable “resources become uncorrelated across larger spatial regions,” she said. “It comes down to data … just having a sufficient amount of data to really capture the [impacts] of these distributions when you’re looking at rare occurrences of both wind and solar droughts.”

But Ravi Seethapathy, executive chair of Biosirus, an industry consultant based in Canada, countered that different approaches and strategies may be needed when a specific area is hit repeatedly with severe storms. “I’m not quite sure whether that interconnection all over the United States will actually help that area,” Seethapathy said.

Resilience will need to be multilevel, he said, isolating and protecting certain sections of the transmission grid, using non-wires solutions, such as microgrids, for local reliability, topped off with better public awareness and education.

“We have not been able to condition the public to take certain quick measures to manage [those storms],” Seethapathy said. “We are constantly on a 24/7, 365, by-the-minute kind of time frame … and maybe all these events are telling us, ‘You now need to be a little more resilient, by way of [changing] your daily practices.’ …

“That’s the approach we’re advocating.”

Managing Costs

The pace and cost of extreme weather events continue to rise, according to industry veteran David Owens, formerly executive vice president of the Edison Electric Institute. In the past three years, the U.S. has seen 66 major weather events causing more than $1 billion in damages. The total price tag, from 1980 to today, is $2.8 trillion, he said.

Owens deftly summarized the challenges for utilities, regulators, grid operators and other industry stakeholders: “How do we mitigate the risk? And how do we, at the same time, not expose electric consumers to exorbitant costs? What are some of the technologies that we can employ?”

Meeting future load growth will be expensive, “regardless of what happens with climate and extreme weather,” Staid said. Integrating extreme weather resilience into long-term planning for load growth could result in “only a small adder on top of a very big cost to make sure you can ride through these extreme heat events, these extreme cold events.”

“We absolutely need to keep this extreme weather and climate change in mind, but if we plan ahead of time, it shouldn’t drive the cost up significantly,” she said.

Seethapathy again said a shift in thinking and in relations between utilities and regulators may be needed.

“We have got a system where the regulator [and] the utility have got a relationship and things are moving very slowly. Why are the costs so high? It’s because we are using the methodologies of 50 years ago,” he said.

For example, undergrounding of transmission or distribution lines need not mean burying them four feet deep, Seethapathy said. “Cable protection” can be laid at ground level or “just shallow, below ground,” he said. Existing standards “are just out of whack with today’s times.”

Lessons Learned

Joining Vegas on the USEA panel, CAISO CEO Elliot Mainzer and MISO Senior Vice President Todd Hillman talked about the lessons learned from previously unprecedented weather events like the 2021 winter storm in Texas, commonly called Uri, and the 2020 August heat waves and rolling blackouts in California.

In the wake of 2020, California tackled resource adequacy ― ensuring it has enough power on reserve to cover emergencies ― with a vengeance. The state has kept existing generation online ― in particular, the Diablo Canyon nuclear power plant ― while adding more than 20,000 MW of new generation to the grid and “a pretty amazing fleet of lithium-ion batteries, now over 9,000 MW, managing that evening peak in tandem with solar,” Mainzer said.

CAISO also leans on its Energy Imbalance Market, Mainzer said, “taking advantage of transmission connectivity across broad geographies.” EIM is expanding with new lines into New Mexico and Wyoming, and implementation of its voluntary day-ahead market ― expected to come online in 2026 ― will “offer even greater optimization,” he said.

“The economics are very compelling, but it’s going to be the reliability benefits ― by reducing the need for energy emergency alerts, calming down the system and taking advantage of wide-area dispatch ― that I think ultimately will provide the greatest customer value,” Mainzer said.

Hillman said MISO is following an “all-of-the-above” strategy, including its Joint Transmission Interconnection Queue with SPP, aimed at providing more interregional transfer capacity. The $1.8 billion package of projects is expected to go to FERC for approval “very soon,” he said.

Like CAISO, MISO also seeks to beef up its generation, with some of the 350 GW of projects ― mostly wind and solar ― in its interconnection queue, Hillman said. However, MISO’s attempts to set an annual cap on interconnection capacity were turned down at FERC in 2023, and the grid operator has delayed opening the queue for new 2024 applications until it sends a revised proposal to the commission. (See MISO: New Interconnection Queue Cycle to Wait on MW Cap Filing.)

Hillman also spoke about a shift in thinking about risk parameters under way at MISO. With operations covering 15 states, “we’re looking at any and all resources, that they can stay online as long as they possibly can, despite the pressures on the system. But we’re also looking at what the real value of each asset is worth, what’s called accreditation. So, really, what are those values when you get into a risk situation?”

The dayslong power outages of Uri notwithstanding, ERCOT has yet to focus on developing more interregional transmission lines. Rather, Vegas said, “we’re starting to look at other steps of voltage in our transmission system, stepping up from what we have today across Texas, a 345-kV system. [We are] starting to evaluate, could a 500- or 765-kV system with a strong backbone network built across the state provide added resiliency should we have isolated areas of intense issues that could come from things like weather events?

“We think that there’s a lot of potential value to that kind of an infrastructure investment that not only supports resiliency but can also support the tremendous load growth that we’re all talking about too.” A new surge of solar and storage on the system also could help ERCOT ride through the traditionally high-risk times when solar power drops off the system during summer sunsets, Vegas said.

“This may be the last year that we have real significant risk at solar sunset,” he said. “If we continue to see that trajectory by 2025 into 2026, we could see the summer risk period significantly mitigated because batteries are picking up some of the transition solar ramps as we see the wind come on in the evening.”

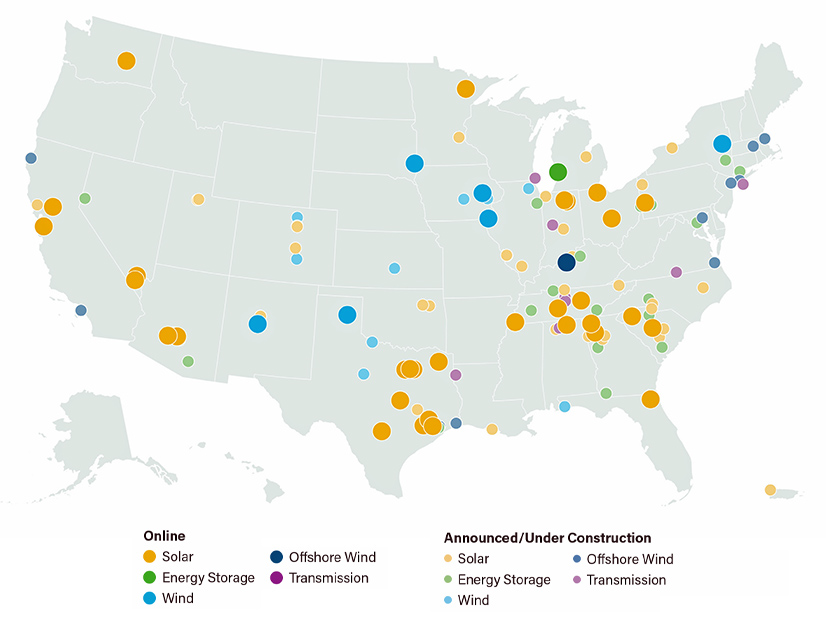

The American Clean Power Association reports that U.S. clean energy investments announced over the past two years have reached a half-trillion dollars.

That money would pay for at least 161 new manufacturing facilities, with the potential for more than 100,000 new manufacturing jobs and more than 300 GW of new emissions-free power generation.

Most of the spending and much of the resulting infrastructure are in the future, but the commitments are significant enough for ACP to declare it a manufacturing renaissance in “Clean Energy Investing in America,” the report it issued Aug. 7.

“These historic investments are providing a powerful engine for job creation across the nation,” ACP CEO Jason Grumet said in a news release. “As demand for electricity continues to rise, clean power is answering the call and propelling a new era for American manufacturing.”

The two-year period in the report overlaps a historic infusion of federal funding intended to encourage exactly what the report quantifies: clean energy development and the creation of a domestic manufacturing base to supply it.

The Inflation Reduction Act, signed into law by President Biden in August 2022, has provided billions to encourage the changes the ACP report highlights.

A geographic look at clean-energy-related manufacturing facilities that were announced or came online after August 2022. | American Clean Power

In the latest example, a day after the report was released, the Department of Energy’s Loan Programs Office announced a $1.45 billion conditional loan guarantee for Qcells to set up what is expected to be the largest solar ingot and wafer factory ever built in the United States.

The LPO said the Georgia facility would be the first vertically integrated U.S. solar factory in more than a decade and would re-establish critical parts of the domestic supply chain for photovoltaics.

Grumet said that while headline numbers in the ACP report are remarkable, they are only part of the clean energy transition: “Our ability to deploy new capacity with adequate speed and scale requires dramatic efficiency improvements in federal, state and local decision making. ACP is encouraged by recent bipartisan progress to confront barriers to modernizing America’s energy economy.”

The report’s statistics run through June 30, 2024. At that point, most of the benefits cited in the report were yet to come:

$500 billion in investments had been announced, but only $75 billion had been made.

Construction or expansion of at least 161 manufacturing facilities had been announced, but at least 119 of the projects were in development.

Only 20,000 of the anticipated 100,000 new manufacturing jobs had been created.

Only about 55 GW of the announced 300 GW of new clean energy generating capacity had become operational.

Breaking down the numbers:

Solar leads the way in new generation, with 33 GW of new capacity built, at a cost of $42 billion. Onshore wind (11.6 GW, $20 billion) and storage (10 GW, $12 billion) are a distant second and third.

New generation projects totaling $363 billion account for the bulk of the announced $500 billion of investment, followed by manufacturing ($61 billion), supply agreements ($47 billion) and other sectors ($28 billion).

ACP’s report intersperses the project lists and dollar counts with vignettes diving deeper into some of the new manufacturing created in the past two years:

Form Energy built the first factory for its iron-air, 100-hour battery system in Weirton, W.Va., on the site of a demolished steel mill that was the economic and cultural heart of that community for generations.

GE Vernova announced a $50 million expansion and 200 new jobs at its Schenectady, N.Y., facility, where it produces the largest land-based wind turbine in the United States.

Illuminate USA announced, built and opened a massive plant in Pataskala, Ohio, to produce advanced solar panels. Its workforce already exceeds 800 “illuminators,” and the company expects to surpass 1,200 by the end of 2024.

Vestas, which already invested more than $1 billion in Colorado factories that produce wind turbine blades and nacelles, announced a $40 million expansion of the two facilities and plans to hire upward of 1,000 people.

Grumet said much more is possible — the nation can be a global leader in clean energy: “If we combine innovations in technology and governing, it is possible to achieve an energy system that is reliable, affordable, secure and clean.”

Governance should be a “key consideration” for the West in the competition between day-ahead electricity markets because the outcome potentially affects $25 billion a year in energy transactions, according to an “issue alert” issued Aug. 7 by 10 entities that helped develop the SPP Markets+ tariff.

The “governance” alert, addressed to the Markets+ States Committee, is intended to be the first of seven such notices published in coming months by the “Markets+ Phase 1 Funding Parties.”

The contributing parties include Arizona Public Service, Chelan County Public Utility District (PUD), Grant County PUD, Powerex, Public Service Co. of Colorado, Salt River Project, Snohomish PUD, Tacoma Power, Tri-State Generation and Transmission Association, and Tucson Electric Power.

Those entities, along with the Bonneville Power Administration, which did not sign on to the alert, represent some of the strongest supporters of Markets+ in its competition for participants with CAISO’s Extended Day-Ahead Market (EDAM), designed to extend the capabilities of the Western Energy Imbalance Market (WEIM).

In April, BPA staff issued a “leaning” that cited CAISO’s state-run governance as one of the top reasons the agency should choose Markets+ over EDAM. (See BPA Staff Recommends Markets+ over EDAM.)

In their Aug. 7 alert, the Funding Parties noted the “considerable industry dialogue focused on the market seams that will exist between EDAM/EIM and Markets+, as well as the EDAM/EIM governance enhancements being pursued through” the West-Wide Governance Pathways Initiative, a multistate effort launched last year to create the framework for an independent organization to oversee those markets.

“While both topics are important, the Markets+ Phase 1 Funding Parties believe this dialogue is incomplete without also considering the numerous governance and market design differences between Markets+ and EDAM/EIM that are driving continued support for Markets+,” they said.

The parties derived their $25 billion annual impact estimate from the assumption that transitioning to a full day-ahead and real-time market likely will replace much of the region’s bilateral transactions still occurring “while also impacting forward transactions and the utilization of the Western transmission grid.”

“Sound governance is a foundational requirement for a day-ahead organized market to provide the benefits of increased efficiency and enhanced reliability while also ensuring equitable outcomes for all participants and all Western subregions,” they said.

That entails having a “durable, effective and independent governance structure” that fairly represents all market stakeholders, who would “initiate, develop and own outcomes,” they said.

According to the alert, the Markets+ governance framework “fully achieves” those requirements by having:

a “geographically diverse” board that is independent of market participants and has authority over “all aspects” of the market;

a “transparent and consensus-based market development process” that is led by stakeholders, who have voting rights to determine whether market design proposals advance;

a “fully independent and impartial market operator that does not also act as one of the participating balancing authorities with its own interests”; and

a stakeholder framework in which “all generators, load and BAAs are participating in the same manner with equivalent rules, rights and responsibilities.”

The alert additionally notes that the Markets+ governance framework already is up and running, having underpinned the decision-making in developing the market’s tariff, which last week received a deficiency notice from FERC. (See FERC Finds SPP Markets+ Tariff ‘Deficient’ in Several Areas.)

They expressed additional skepticism that Pathways would create a governance framework “comparable to” Markets+, saying the initiative’s starting point is an EDAM/WEIM tariff designed under CAISO’s existing governance model, and that Pathways has not proposed to replace it with a “stakeholder-driven design.”

The parties also contended that Pathways has not addressed the fact that “EDAM and EIM were built as extensions of a legacy institutional framework with embedded dependencies on, and obligations to, California state agencies” and has not ensured that CAISO, as the operator of the markets, “will balance the interests of all stakeholders and avoid undue influence from California interests.”

They also argued the stakeholder-driven Markets+ process has produced a market design “substantially different” from EDAM in “several key respects,” which will be the subject of future alerts. Design differences can influence the level of participation in a market, “while also encouraging or discouraging generation and transmission investments,” they said.

“For example, a market that inaccurately suppresses peak prices will discourage flexible generation and storage solutions. Similarly, a market that misallocates congestion costs will generally lead to less economically efficient transmission investments,” the parties said, touching on two issues particularly important to entities in the Northwest, the latter sparking especially sharp controversy after a January 2024 cold snap left the region severely short of energy. (See NW Cold Snap Dispute Reflects Divisions over Western Markets.)

The parties concluded by touting the benefit of competition — in this case between markets.

“Experience in the East demonstrates that the ongoing existence of two or more competing organized markets provides the opportunity for participants to continuously evaluate which organized market provides the best value for its customers. This places ongoing competitive pressure on each organized market to continuously evolve to deliver value to all of its participants and all of its subregions, driving immeasurable value for consumers while also reducing risk.”

Five years ago, load growth from transportation electrification was a major issue for policy makers, according to speakers at a WECC webinar. Now the focus has shifted to data centers.

“Over the last year or so, the data center growth has become one of the major challenges for this industry,” said Branden Sudduth, WECC’s vice president of reliability planning and performance analysis, who noted the centers can consume as much as 3 GW of energy.

“That’s just massive loads that we’re not accustomed to seeing come onto the grid,” Sudduth said.

The discussion came during a WECC webinar Aug. 7 on emerging risks to reliability in the West.

In its 2023 Western Assessment of Resource Adequacy, WECC projected the region’s demand would increase 16.8% over the next decade, nearly double the 9.6% growth predicted in its 2022 assessment. The 2023 assessment said the biggest driver of the increased demand is the expansion of data centers, especially in the Northwest.

Data center growth also is expected in other parts of the Western Interconnection. In its integrated resource plan filed in May, NV Energy said more than 3,000 acres of industrial land had been purchased in Northern Nevada last year for data center development.

In addition to needing large amounts of energy to process data, data centers require significant cooling, which further increases load.

New Generation Lagging

During the WECC webinar, Sudduth said the data centers can come online as quickly as 18 months, or even sooner if infrastructure is in place.

“What we know for sure is that generation doesn’t get built that quickly,” said Kris Raper, WECC’s vice president of strategic engagement and external affairs.

Although an increasing amount of generation is being planned each year, much of that is not materializing, Sudduth said.

For example, he said, 14 GW of new energy resources were expected to come online in the Western Interconnection in the first half of 2023. But by the end of 2023, only 55% of those resources had been added.

Projections of new resources for the following two years were even greater: 17 GW in 2024 and 28 GW in 2025, said Sudduth, who noted the figures were near-term forecasts for resources close to or in the construction phase.

“We’re getting more and more aggressive with the amount of generation that we’re expecting to bring online,” Sudduth said. “But up to this point, we don’t seem to be able to keep up with that aggressive growth.”

Sudduth attributed the delays to supply chain issues, which are making it difficult to get equipment such as transformers. And increasing costs are “forcing people to rethink when and if they’re going to build certain resources,” he said.

One way the generation gap is being filled is through resource retirement delays, Sudduth added.

EV Concerns

Raper, who noted that data centers had taken over from transportation electrification as a hot topic among policymakers, said both sources of load growth remained on WECC’s radar screen.

“We’re trying to watch all of it,” Raper said. “Because all of the things are going to have an impact on reliability to the grid.”

Sudduth said one aspect of EV adoption that makes him nervous is long-haul trucking.

“[Truck drivers] are not going to want to sit around all day and charge their vehicle, and so it’s going to require massive amounts of power to get those long-haul trucks charged quickly,” he said. “What does that do to load forecasts?”

SPP CEO Barbara Sugg announced Aug. 8 that she will retire from the RTO on April 1, 2025, after 35 years of service.

Sugg was appointed to the RTO’s top position in 2020, replacing longtime CEO Nick Brown. Under her guidance, SPP has earned designations as one of the best places to work in Arkansas the past three years; expanded its service offerings and territory into the Western Interconnection with RTO West, Markets+ and other services; and garnered consistently high stakeholder satisfaction ratings.

During her tenure, the RTO has navigated historic challenges that included the COVID-19 pandemic and resulting changes to workplace norms; increasing extreme weather that has affected regional electric reliability; and the ongoing growth in demand for electricity and challenges to resource adequacy.

Sugg said in an email to RTO Insider that she has “bittersweet, mixed emotions” about her planned retirement during an “exciting and rewarding time to be part of the electric utility industry.”

“I have no doubt that SPP’s future is as bright as ever,” she said.

Golden Spread Electric Cooperative’s Mike Wise, one of SPP’s more senior and involved members, noted Sugg’s career has virtually matched his. He commended her for bringing out the best in people and encouraging them to grow.

“Barbara’s leadership and vision guided the SPP through some very difficult times,” Wise told RTO Insider, alluding to the COVID-19 pandemic that hit just after she was named CEO. “She had to create a new corporate culture around remote work and still maintain effective RTO operations. Then she was forced to navigate the highly destructive Winter Storm Uri as an RTO which faced circumstances never seen before in the region.

“She exhibited amazing strength of character and never wavered from her strong belief in the exceptionalism of her employees and the committed stakeholders in the SPP. A big three cheers for a good friend and great leader.”

Joe Lang, Omaha Public Power District’s director of generation strategy and origination and vice chair of the stakeholder-led Markets and Operations Policy Committee, wished the best for Sugg and congratulated her on a “fulfilling” career.

“Barbara has been a strong leader as SPP’s CEO through significant challenges in the electric power industry,” he said. “Barbara will be remembered for her leadership that guided SPP through the pandemic, generation interconnection backlog efforts, navigating resource adequacy constraints during extreme weather events, as well as successes expanding into the West.”

“Barbara’s dedication, passion and support of SPP’s mission and people have been evident throughout her tenure,” John Cupparo, chair of the Board of Directors, said in a news release. “Her impact as a CEO will be felt for years to come, and the board joins SPP’s stakeholders in thanking her for the high standard of leadership she’s set.”

The board plans to name a new CEO before Sugg’s departure, and it has engaged search firm Heidrick & Struggles to assess internal and external candidates as her potential replacement.

“I’m not done until I’m done. I still have much work to do,” she said, crediting SPP’s “dedicated” staff and “diverse” stakeholders. “For now, I remain energized, committed and focused on ensuring SPP’s success and partnering closely with my replacement to ensure she or he is prepared to take the reins.”

Sugg joined SPP in 1997 after eight years with Louisiana Energy and Power Authority. Because LEPA, which comprises 20 municipal power systems, was an SPP member at the time and new hires from members were able to bridge their service years, Sugg is credited with 35 years with the grid operator.

Her career has spanned every level of the RTO’s leadership, including roles as senior vice president of information technology and chief security officer.

Michael Deselle, SPP’s chief compliance and administrative officer, also has announced his retirement, effective at year-end. He joined the RTO in 2006 after 14 years at Central and South West and American Electric Power.