A study conducted for the California Public Utilities Commission finds that without mitigation, the distribution grids of the state’s three large investor-owned utilities will require up to $50 billion in upgrades by 2035, mainly to accommodate electric vehicle charging.

The Electrification Impacts Study, performed by energy analytics firm Kevala, was commissioned by CPUC as part of its High Distributed Energy Resources Grid Planning rulemaking, which is intended to prepare the state for large-scale transportation and building electrification.

California law requires that all new vehicles sold in-state be zero-emitting by 2035, and the state Air Resources Board is weighing a ban on sales of new natural gas-powered space and water heaters for residential and commercial use. (See Calif. Considers Zero-emission Appliance Rules.)

The study takes these high-electrification scenarios into account. Kevala and CPUC released the findings from its first part May 9 and plan to review the results in a public workshop May 17.

The findings provide preliminary estimates of the impact of widespread transportation electrification on the grids of Pacific Gas and Electric (PG&E), Southern California Edison (SCE) and San Diego Gas & Electric (SDG&E) using a “highly granular load forecast” for more than 12 million homes.

“It is important to highlight that this Part 1 analysis was conducted under unmitigated planning scenarios, which assume only traditional utility distribution infrastructure investments,” the study says. The study also assumed that existing time-of-use rates and behind-the-meter solar tariffs would be in place throughout the study period.

“It did not consider alternatives or future potential mitigation strategies such as alternative time-variant rates or dynamic rates and flexible load management strategies,” the study says.

“Across these unmitigated load scenarios, Kevala estimates up to $50 billion in traditional electricity distribution grid infrastructure investments by 2035,” it says. “This estimate reflects distribution grid needs across the PG&E, SCE and SDG&E service territories under the policy assumptions used in this report.”

Two high transportation electrification scenarios would require the utilities to nearly double their current spending on feeder lines, transformer banks and substations, it says.

“Secondary transformer and service upgrades alone … [comprise] an estimated $15 billion of the $50 billion … and are currently not accounted for” in the investor-owned utilities’ annual assessments of grid needs, it says.

“PG&E’s distribution circuits are projected to reach capacity sooner than SCE and SDG&E,” it says. “SDG&E is expected to have the least number of feeders reaching full capacity by 2035, with 22% compared to SCE’s 36% and PG&E’s 48% of feeders.”

The study forecasts that peak load will increase on the utilities’ distribution systems an average of 56% from 2025 to 2035 under all high-electrification and base-case scenarios.

“This dramatic increase in peak load … is primarily due to transportation electrification impacts, with over 60% of this demand coming from light-duty vehicles,” it says. “The average percent change in peak load from 2025 to 2035 for the high transportation electrification scenarios is more dramatic for PG&E (69%), followed by SDG&E (53%) and SCE (44%).”

Among the study’s recommendations is that the utilities increase their distribution planning horizons to align with those of CAISO and the California Energy Commission, which stretch from 10 to 20 years. That would help them prepare more efficiently for a distribution grid that can incorporate DERs and manage load, it says.

“The substantial difference between the estimated capacity expansion costs, in the several tens of billions of dollars, in this study and the recent filings by the [utilities] suggest there is a disconnect between the data and the current planning process,” it says.

Another recommendation is for the utilities to better incorporate the state’s policy goals in their distribution planning.

A second part of the study will build on the first part’s findings, including by developing scenarios that reflect state policy goals, state agency targets and the Energy Commission’s demand forecast.

The U.S. Department of Agriculture has announced $10.7 billion in funding from the Inflation Reduction Act to help rural electric cooperatives across the country stand up clean energy, zero-emission and carbon capture projects.

Agriculture Secretary Tom Vilsack described the funding, announced Tuesday, as “the single largest investment in rural electrification since the Rural Electrification Act of 1936.” That law, signed by President Franklin Delano Roosevelt, provided critical loans to farmers and rural communities forming electric cooperatives during the Depression.

The new funding “continues an ongoing effort to ensure that rural America is a full participant in this clean energy economy,” Vilsack said during an advance press briefing on Monday.

The largest chunk of the IRA dollars — $9.7 billion — will go to the Empowering Rural America (New ERA) program, offering “a mix of loans grants and loan modifications to support the purchase or ownership of renewable energy systems, zero-emissions and carbon capture systems,” Vilsack said.

Funding will be “exclusively for rural electric cooperatives,” he said, adding that the IRA allows for “stacking of benefits.” That means projects also can take advantage of production tax credits and investment tax credits in the IRA.

As nonprofit organizations, electric co-ops have previously not been able to take advantage of the ITC but are now able to under the IRA’s direct payment provisions.

The second program, with $1 billion in funding, is the Powering Affordable Clean Energy (PACE) program which will “provide loans — a portion of which can be forgiven — in connection with development of renewable energy projects or energy storage,” Vilsack said. These loans will be open to a broader range of applicants, including corporations, municipalities, co-ops and tribes, he said.

There are three categories of loan forgiveness, ranging from 20% to 60%, depending on where the project is located, Vilsack said. For example, projects in Puerto Rico, Micronesia, the Marshall Islands, Palau and tribal communities will be eligible for 60% forgiveness, according to the USDA announcement.

Micronesia, the Marshall Islands and Palau are island nations that together total more than 2,300 small islands, with loose affiliations with the U.S.

The goal of the program is “to make clean energy affordable for vulnerable, disadvantaged, tribal and energy communities to heat their homes, run their businesses and power their cars, schools [and] hospitals,” the announcement said.

Figuring in repayment of loans over time, Vilsack said, the $1 billion could be stretched to provide $2.7 billion in loans.

Letters of interest for New ERA are due between July 31 and Aug. 31, while letters of interest for PACE will be accepted from June 30 to Sept. 29, according to the USDA.

Jim Matheson, CEO of the National Rural Electric Cooperative Association (NRECA), was quick to praise the new programs as “an exciting and transformative opportunity for co-ops and their local communities, particularly as we look toward a future that depends on electricity to power more of the economy.”

Matheson called the programs “smartly structured … in a way that will help electric co-ops leverage new tools to reduce costs and keep energy affordable while meeting the future energy needs of their rural communities.”

He also noted that the wide range of eligible projects — including carbon capture, renewable energy, storage, nuclear, and generation and transmission efficiency improvements — will allow individual co-ops to tailor programs to their circumstances.

‘Proven Driver of Economic Growth’

At present more than 900 electric co-ops serve customers in 48 states, with service territories covering 56% of the continental U.S. land mass, including 92% of “persistent poverty counties,” according to the NRECA website.

Co-ops can range from several hundred members to tens of thousands, and because they are largely not regulated, some have been able to adopt aggressive and innovative clean energy programs. The Kit Carson Electric Cooperative in Taos, N.M., has been sourcing 100% of its daytime power from solar since June of 2022 and is exploring the feasibility of using its excess solar to produce green hydrogen to provide night-time power.

Holy Cross Energy, a Colorado co-op, has set a goal of providing 100% renewable power to its members by 2030 and offsetting all emissions to net zero by 2035.

As of 2021, renewable energy constituted about 22% of the power provided by co-ops across the country, while coal and natural gas accounts for 61% and nuclear 15%, according to NRECA.

With financing still a hurdle for many co-ops in rural areas, National Climate Advisor Ali Zaidi called renewable energy “a proven driver of economic growth” in rural communities. Citing an analysis from the nonprofit news site Stateline, Zaidi said that seven of the 10 counties nationwide with the highest increase in gross domestic product between 2019 and 2021 “had revenue that came from wind farm construction.”

The New ERA and PACE programs are “designed to begin the process of allowing the rural electric cooperatives to essentially reach parity, if you will, with the privately owned utility companies that have already begun significant investments” in clean energy, Vilsack said. The funding will “make it a little bit easier for [co-ops] to be able to accelerate plans they may have to transition away from fossil fuel[s].”

VALLEY FORGE, Pa. — PJM plans to allocate more than 2,000 MW of transmission headroom to generators that requested additional capacity interconnection rights (CIRs) under a transitional process as the RTO shifts to a new methodology for calculating CIRs for effective load carrying capability (ELCC) resources. (See FERC Approves Revisions to PJM’s ELCC Accreditation Model.)

Existing generators or those with signed ISAs may request higher accreditation through the transitional study process, which assigns a portion of available headroom on the grid to those resources. PJM’s Jonathan Kern said about 7,000 MW was eligible to participate in the studies, of which 2,073 MW was awarded, with the remaining 5,000 MW largely denied due to not being available for the upcoming delivery year. Those generators denied can receive access to headroom in future years once they are online.

“It’s just for this particular Base Residual Auction (BRA) that they didn’t achieve the particular milestones to participate,” he said.

The higher accreditation will be added onto resources’ CIRs when running calculations for the 2025/26 BRA and future auctions until the transitional period has ended. Should FERC grant PJM’s request to delay that auction — currently scheduled for next month — Kern said many of the figures calculated could change significantly, including headroom allocations. (See PJM Seeks to Delay Capacity Auctions Through 2028 Delivery Year.)

Most resources received either no increase in their accreditation or the full amount they asked for, with some receiving in between based on locational factors. Kern said there was no queue-based determination in the headroom allocation.

Stakeholders Seek Discussion on CIR Transfers

Denise Foster Cronin, of the East Kentucky Power Cooperative, and Tonja Wicks, of Elevate Renewable Energy, presented a problem statement and issue charge to open a discussion on streamlining the process of transferring CIRs from a deactivating generator to a replacement resource.

“Our motivation to bringing this forward is to add some certainty to something that is currently uncertain,” Cronin said.

The current rules allow CIRs to be used at a resource seeking to interconnect at the same site as the retiring generator or at a different point of interconnection. Transferring CIRs also requires a study of the grid upgrades that may be necessary to support the capacity offered by the new generator, part of the interconnection queue process.

The status quo process assumes studies can be completed relatively quickly, but the queue is backlogged as PJM transitions to a new process meant to complete studies quicker, potentially creating a “timing misalignment.” The problem statement says resources seeking to retire between 2023 and 2026 may expect a delay of four years before they’re able to transfer CIRs to new resources, affecting reliability and cost.

“Inefficiency in the CIR transfer process results in unnecessary additional cost to customers served by these generation capacity resources. Load serving entities may need to seek alternatives and may find inadequate hedges to mitigate market price exposure should CIR transfers not be efficiently executed,” the problem statement reads. “Also, the inefficiency could result in PJM needing to rely on [reliability-must-run] agreements and/or the transmission reinforcements to address reliability issues resulting from generation deactivation that otherwise would not be necessary if CIR transfers could be more efficient. These measures result in cost to load, and the allocation of such costs may extend beyond the zone in which the deactivating generation is located.”

The problem statement also calls for clarifying the resources the CIR transfer rules apply to, noting the status quo language refers to “generation capacity resources.” The document states that more explicit inclusion of energy storage or hybrid resources may be warranted.

The issue charge states that any changes to the current process for transferring CIRs to a replacement resource located at a different interconnection site would be considered out of scope. The sponsors’ presentation said the new standard interconnection process would not be affected.

Stakeholders asked questions on the implementation timeline and expressed concerns regarding possible queue jumping, generators being able to avoid grid upgrade cost allocations and any impact to generators already in the interconnection queue should resources receiving CIR transfers be studied first.

Reliability Requirement Study to Use New Software

PJM plans to use new software to conduct the 2023 Reserve Requirement Study (RRS), the annual process that resets the forecast pool requirement (FPR) and the installed reserve margin (IRM) for the following three delivery years and establishes an initial value for the fourth year out, 2027/28 in this case. The study will also set the winter weekly reserve target for the 2023/24 delivery year. (See “Stakeholders Endorse 2022 Reserve Requirement Study Results,” PJM PC/TEAC Briefs: Oct. 4, 2022.)

Past studies were conducted with the PRISM modeling software, but PJM’s Patricio Rocha Garrido said this year the software developed for the hourly loss-of-load modeling used for the ELCC study will be used in parallel with PRISM. Two separate sets of assumptions will be generated to correspond with the different approaches, and both sets of results will be presented to stakeholders after the study is done, with PJM planning to recommend one of the results for endorsement. PJM plans to ultimately shift to using the hourly loss-of-load modeling software by default in the future.

PJM will also be including data from the 2014 polar vortex based on experience gathered through the December 2022 winter storm. Previously, the polar vortex had been replaced with other data. The capacity benefit of ties will also be averaged over the past several years, rather than using annual data, due to value volatility.

The PC is slated to vote on the RRS approach at its June meeting.

Advocates Push for More Transmission Cost Details

State consumer advocates are seeking more insight into the development of cost estimates for supplemental transmission projects when they are presented to the Transmission Expansion Advisory Committee (TEAC). A presentation by the Consumer Advocates of PJM States (CAPS) said questions to transmission owners about their proposals have not yielded substantive information. (See “CAPS Pushes for More Transmission Upgrade Data,” PJM PC/TEAC Briefs: April 11, 2023.)

For the 22 projects presented at the April TEAC, the presentation said transmission owners were asked how they developed the estimated cost, to provide a breakdown of the project budget and if the relevant state utility commission would have planning oversight. None of the responses regarding project budgets provided a breakdown, instead pointing to processes for receive cost breakdowns after the work is done. None of the responses specifically addressed the question of oversight, the presentation said.

Exelon’s Alex Stern rejected CAPS’ complaint.

“We have enhanced the planning process, and the TOs are providing more transparency in a timely manner than anywhere else in the country,” he said. “We’re also providing the best, most accurate cost estimates that we can based on industry experience when we bring solutions to needs forward followed by cost updates posted on pjm.com quarterly from project inception to project completion.”

The estimates provided to TEAC can significantly change before a project goes to development and is completed based on state and local siting processes, Stern added.

Tom Schmidt of Buckeye Power said the nuances of each state’s oversight provisions can make providing a yes or no answer “very, very difficult,” giving Ohio as an example of a state where oversight depends on specific voltages and project length.

Transmission Expansion Advisory Committee

Data Center Growth in Ohio Contributing to Nearly $600 Million in Transmission Upgrades

American Electric Power presented about $579.5 million in transmission upgrades throughout Ohio to accommodate several new load interconnection requests. AEP’s Nicolas Koehler told the Transmission Expansion Advisory Committee (TEAC) that much of the load stems from a surge in plans to construct data centers, with new announcements over the past few months estimated to consume around 3,000 MW.

The bulk of the expense would be direct connection costs at $498 million, while the remaining $81.6 million are system upgrade costs.

Responding to stakeholders who questioned why the AEP projects weren’t following the same competitive process as the data center alley in Northern Virginia, PJM’s Dave Souder said the Virginia load growth has necessitated upgrades to the regional 500-kV transmission system. PJM has opened a third window to its 2022 Regional Transmission Expansion Plan (RTEP) to address “unprecedented growth” from data centers. (See “Load Forecast for Northern Virginia Data Centers Continues to Climb,” PJM PC/TEAC Briefs: Jan. 10, 2023.)

The largest portion of the Ohio work would involve significantly expanding the grid in the New Albany region and adding about a dozen new substations:

The existing Corridor — the Conesville 345-kV line would have two new substations, Curleys and Bermuda, and it would be rerouted to tie into the existing Innovation substation, which would be upgraded to handle both the new 345-kV capability and its current 138-kV lines. The Curleys facility would serve an ultimate load of 968 MW and would come with a $55.2 million price tag, while the Bermuda substation would serve an ultimate demand of 337 MW and would cost around $60.3 million.

The Corridor — the Jug Street 138-kV line would have four substations added along its run: Souder, which would serve a projected future load of around 100 MW at a $14.3 million cost estimate; Fiesta (up to 300 MW/$22.3 million); Horizon (200 MW/$11 million); and Badger (290 MW/$18 million).

The Green Chapel — the Innovation 138-kV line would be cut and extended around 0.75 miles to connect to the new Tasjan substation, which would serve an ultimate load of 150 MW. The work would cost around $19 million.

The Innovation — the Kirk 138-kV line would be cut with two single-circuit lines terminating around 0.35 miles at the new Jorden substation, which would serve a 270-MW load. The project would cost an estimated $12.5 million. A new line would be constructed from the Innovation facility to the Brie substation with around 1.75 miles of double-circuit 138-kV line. New equipment would be installed at the Brie site, addressing potential load drop and overload risks at a $10.8 million expense.

The existing Innovation substation in the New Albany area would receive $53.7 million in upgrades to serve 247 MW of additional load. The proposed project includes cutting into the Corridor-Conesville 345-kV circuit and building a new 345-kV ring bus at the site.

Additional substations would be built in the area of Union County and Columbus:

The Cyprus substation outside Columbus would be upgraded with 345-kV infrastructure, in addition to the existing 138-kV equipment, and cut into the Beatty-Bixby 345-kV line at a $46.9 expense.

The proposal would build the new 138-kV and 345-kV Celtic substation in Union County to serve 461 MW of load at an estimated $60 million. The substation would cut into the Hayden-Hyatt 345-kV line and the Amlin-Hyatt 138-kV line and would also include a new 138-kV line to the existing Kileville line.

The Beacon substation would be built for $40 million to supply an ultimate load of 328 MW in the Columbus area. The facility would cut into the Hayden-Roberts 345-kV circuit.

The Jerome substation in Plain City would serve an initial load of 106 MW, which could grow as high as 203 MW at a $30 million price tag. The facility would connect to the proposed Celtic substation and the existing Hyatt-Amlin line via new 138-kV lines.

Several Generators Announce Deactivation

PJM’s Phil Yum presented an update on the status of deactivating generators, highlighting seven facilities that have recently requested to go offline.

The new deactivations include the 1,884-MW Homer City coal plant in Pennsylvania, the 1,282-MW Brandon Shores coal plant near Baltimore, and the 167-MW Vienna oil-fired generator in Maryland.

The PJM Board of Managers referenced the Homer City deactivation request in a May 1 letter responding to environmental groups that said the RTO’s analysis of future resource adequacy concerns overstated the issue.

“In performing the analysis discussed in this study, the PJM team made assumptions it believes are conservative, meaning that PJM did not try to overstate resource retirements … In fact, just recently, the largest Pennsylvania coal-fired generating plant, Homer City, announced its retirement. Homer City was not included in our retirement assumptions because the policy drivers underlying its retirement were not known at the time of the study,” the board wrote.

Changes to NJ Offshore Wind Transmission Add $128 Million

Several portions of the transmission planned to connect 6,400 MW of offshore wind to the PJM grid have been changed since the approval of the State Agreement Approach, leading to a $128 million increase in the expected project cost from $1.064 billion to $1.192 billion.

The scope of the work in the Jersey Central Power & Light (JCPL) zone has increased to include the removal of existing equipment to accommodate new lines for $17.47 million, while updated cost projections for previously expected JCPL work has increased by $31.71 million. Work in the Public Service Enterprise Group (PSEG) region has increased by $12.25 million, while a case correction in the PECO zone has reduced cost estimates by $5.6 million.

The expected construction cost for the Larrabee Collector Station, as well as procuring and preparing land adjacent to the site, has increased from $121.1 million to $193.3 million, with the new figures including costs that were explicitly excluded from the original estimate but have been determined to be required for the project.

Kern said additional work was identified after the approval of the project and will require the approval of the PJM Board of Managers. The New Jersey Board of Public Utilities is also aware of the changes.

VALLEY FORGE, Pa. — PJM last week proposed creation of a new cost of new entry (CONE) area for the Commonwealth Edison (ComEd) zone during discussions about how to account for local factors in calculating net CONE.

PJM’s Gary Helm said the discussion arose out of concerns raised in the RTO’s quadrennial review filing at FERC about the impact of the Illinois Climate and Equitable Jobs Act on net CONE. An issue charge and problem statement were adopted following the approval of that filing to evaluate how asset life and net CONE are determined. (See “Amortization Period,” FERC Approves PJM Quadrennial Review.)

“What we are looking at proposing here in this package is addressing that specific item through making ComEd, that [locational deliverability area], its own CONE area. So we currently have four CONE areas; this would be a fifth,” Helm said. He added that PJM is also considering what other areas could be impacted by approved state and local legislation or other localized factors.

Stakeholders Continue Discussion on Co-located Load Packages

Several packages seeking to create new rules for generators with co-located load were discussed by the Market Implementation Committee during its May 10 meeting. PJM’s Tim Horger worked with package sponsors to create a comparison of the five current proposals. (See “Discussion on Co-located Load Packages,” PJM MIC Briefs: April. 12, 2023.)

Much of the ongoing discussion of the proposals has centered on configurations in which the co-located load isn’t directly connected with the grid and whether those loads should be considered FERC jurisdictional or falling under state regulation. The discussion has also focused on whether generators should be permitted to retain their full capacity interconnection rights (CIRs) for the balance of their output consumed by the load and what service fees, if any, should be allocated to the load or generator.

The Independent Market Monitor proposal would follow the status quo of requiring generators to reduce their CIRs corresponding to the co-located load consumption, while the other four would not. The PJM, Constellation/Brookfield and Exelon packages specify that CIRs can be retained so long as the load is capable and willing to curtail within 10 minutes and that output be able to shift over to the grid.

The Advanced Energy Management Alliance (AEMA) package considers all co-located load to be FERC jurisdictional and as taking services from the grid. It would permit generators to retain their full CIRs.

The Constellation/Brookfield proposal is the only one to not charge any grid services to the configuration. The PJM package would assess regulation, reserve and black start fees to the entire load by assigning them to the generator. Exelon’s would consider the generator to be a load-serving entity for the co-located load and levy all LSE credits and charges. The Monitor proposal would include charges for regulation, reactive power, frequency control, reserves and black start via the generator, and the AEMA proposal includes all firm point-to-point transmission charges.

All proposals except the Monitor’s would permit the inclusion of curtailment costs in their market-based energy market offers, but not their cost-based offers. The monitor would not permit any inclusion.

The Constellation/Brookfield and Exelon proposals are silent on configurations in which the load is receiving service from the grid, while the AEMA proposal has the same rules for all configurations.

Under configurations with grid service, both the PJM and Monitor proposals would require CIRs to be reduced and consider the load to be FERC-jurisdictional. The Monitor also applies all LSE charges and credits, while PJM does not.

Exelon presented minor changes to its proposal since its last presentation, clarifying that the co-located load could participate as either demand response or price-responsive demand, incorporating PJM feedback to lengthen the initial public notice to 10 days and adding a provision to grandfather PJM’s market rules for co-located load configurations that were approved by the relevant electric retail regulatory authority prior to 2024.

MIC Chair Foluso Afelumo said the committee will likely be continuing first reads at the June meeting to accommodate a data center developer that plans to present an additional package at that meeting. Voting on endorsement could begin at the July meeting.

PJM will also give additional thought to how voting will be structured, as four of the proposals have separate provisions for co-located load with and without service from the grid, while the AEMA proposal addresses both.

Other MIC Business

The committee endorsed by acclamation a PJM problem statement, issue charge and proposal to clarify that smoothened supply curves will only be generated after Base Residual Auctions and not Incremental Auctions. Tariff revisions will move on for consideration at the Markets and Reliability Committee and the Members Committee. The proposal was brought under the quick fix process, allowing solutions to be voted on simultaneous with the problem statement and issue charge. (See “First Read on Smooth Supply Curve Quick Fix,” PJM MIC Briefs: April. 12, 2023.)

Stakeholders endorsed revisions to Manual 11 to allow PJM to reduce the Transmission Constraint Penalty Factor under a set of circumstances when it is believed the penalty cannot incentivize actions that would reduce constraints. The proposal codifies a package previously approved by stakeholders and a FERC order in March. (See FERC Approves PJM Proposal to Reduce Congestion Penalty During Grid Upgrades.)

The MIC endorsed revisions to Manuals 11, 27 and 28 to add market rules for hybrid resources. The proposal will go before the MRC for endorsement on May 31, followed by a FERC filing with a requested effective date of June 1.

Stakeholders endorsed revisions to Manual 15, which PJM’s Glen Boyle described as minor updates to clarify current processes related to heat input guidelines and the IMM Opportunity Cost Calculator.

The Consumer Advocates for PJM States gave a first read on a proposal to amend the issue charge for the Reactive Power Compensation Task force, reducing the items considered out-of-scope to permit discussion of “any existing FERC approved or pending reactive service rates.”

ALBANY, N.Y. — The Independent Power Producers of New York’s (IPPNY) annual Spring Conference on Wednesday highlighted the challenges New York faces as it decarbonizes.

Some prominent figures in the industry shared their thoughts on how New York can achieve its ambitious energy and climate goals.

“We are literally experiencing this transition in every way across our economy every day,” said Doreen Harris, president of the New York State Energy Research and Development Authority. “We got our work cut out for us” because “when it comes to climate action and clean energy, all eyes are on New York. …

“But I am truly optimistic about the ways we can achieve [New York’s] goals and build a truly inclusive energy economy that sets the example for others to follow,” she added.

“We’re entering the period in our transition when it feels like a marathon,” New York Public Service Commissioner Diane Burman said, so in the near term, the state must “focus on being prepared and getting the right resources in place.”

“We need to look at every technology, because wind and solar aren’t going to get the job done,” State Sen. Mario Mattera (R) said. Constituents must demand more answers from their policymakers “about how this transition will get done and paid for” because “we want to make sure we’re creating jobs, not losing them.”

New York State Assemblymember Didi Barrett (D) agreed, saying, “This [transition] cannot be done on the back of ratepayers,” adding that the state “needs to be open to new technology opportunities” while “educating the public about the realities they’ll face.”

Keynote speaker Alexis Glick, CEO of biomethane producer Nature Energy, discussed the benefits from biofuels, saying, “We need an all-of-the-above approach because it’s what New Yorkers do really well.” They “recognize that innovation, investment, fresh thinking and an inclusive approach is critical to our combined success.”

Bart Franey, vice president of clean energy development at National Grid, noted the benefits from energy storage resources and how they can enable New York to connect other renewables to the grid at scale without the need to make as many transmission and distribution system upgrades.

Rudy Wynter, president of National Grid, commented on the importance of workforce training and development, saying, “We want to make sure that all the jobs that will be created during the energy transition are secure, because we know in previous [historical] transitions communities have been left behind … so [National Grid] works directly with communities to make sure they understand that those jobs are coming, and we help them get prepared for those jobs.” (See In Climate Leader NY, Energy Workforce Rising from Ground Up.)

Zach Smith, NYISO vice president of system and resource planning, commented on how dispatchable emissions-free resources are “not some unicorn technology.” New York can attract future resources with certain desirable attributes by sending the right price and market signals that encourage investment in new technologies.

In reference to the increasing risks posed by extreme weather events, Chris Wentlent, chair of the New York State Reliability Council’s Executive Committee, said the state needs to understand how every grid resource is impacted and correlated to natural disasters because without this knowledge, the state will struggle to successfully transition.

Aaron Markham, NYISO vice president of operations, said, “We need to keep our eyes open to how [New York’s] transition is progressing” because there is a concern that as the state decarbonizes, its energy supplies could become compromised and the ISO will find itself unable to reliably meet growing electricity demands.

Eastern Generation CEO Mark Sudbey said, “We need to be realistic to people about decarbonization’s timelines because I am concerned that our goals are too aspirational” and, in attempting to transition too quickly, the state may end “up doing something foolish.”

IPPNY President Gavin Donohue closed out the meeting by saying the challenge for New York will be to transition in a reasonable manner while ensuring that innovation is not compromised, investments are not discouraged and that environmental justice concerns are still considered.

ALBANY, N.Y. — There was no shortage of ideas on how to overcome the well known challenges to carrying out New York’s clean energy transition last week at the Independent Power Producers of New York’s 37th Spring Conference.

Much of the conference built on themes discussed last year, such as how to best implement New York’s climate legislation, the need to expand the grid without compromising reliability or hurting ratepayers, and that everyone needs to be involved in the transition. (See Overheard at IPPNY 2022 Spring Conference.)

Since New York passed the 2019 Climate Leadership and Community Protection Act (CLCPA), the state has set itself on an aggressive decarbonization timeline: 70% renewable electricity by 2030, 100% zero-emission electricity by 2040 and net-zero emissions statewide by 2050. The Climate Action Council (CAC) recently approved a Scoping Plan that laid out a roadmap for how New York can meet CLCPA goals. (See New York Climate Scoping Plan OK’d.)

These deadlines are fast approaching, and panelists agreed that New York needs to act quickly, but methodically. Many of New York’s fossil fuel plants are due to retire soon, and if the state has not installed enough reliable renewable capacity to replace that baseload generation, then those emissions-producing plants may need to stay online, which means that the state will not meet its objectives.

IPPNY President Gavin Donohue opened the meeting saying, “The purpose of this conference is to work together to identify innovative technologies that are zero-emitting and, ultimately, are going to bolster both reliability and affordability.”

Common refrains heard during the conference were that New York needs to encourage more collaboration and be more open to innovative ideas or resources because this will better position the state to achieve its mandates.

Corinne DiDomenico, director of regulatory affairs at NextEra Energy Resources, said “the state has very discrete goals with very rigid timelines” and as those deadlines approach, “things start to get messy, and so with that in mind, we need flexibility to address incoming challenges.”

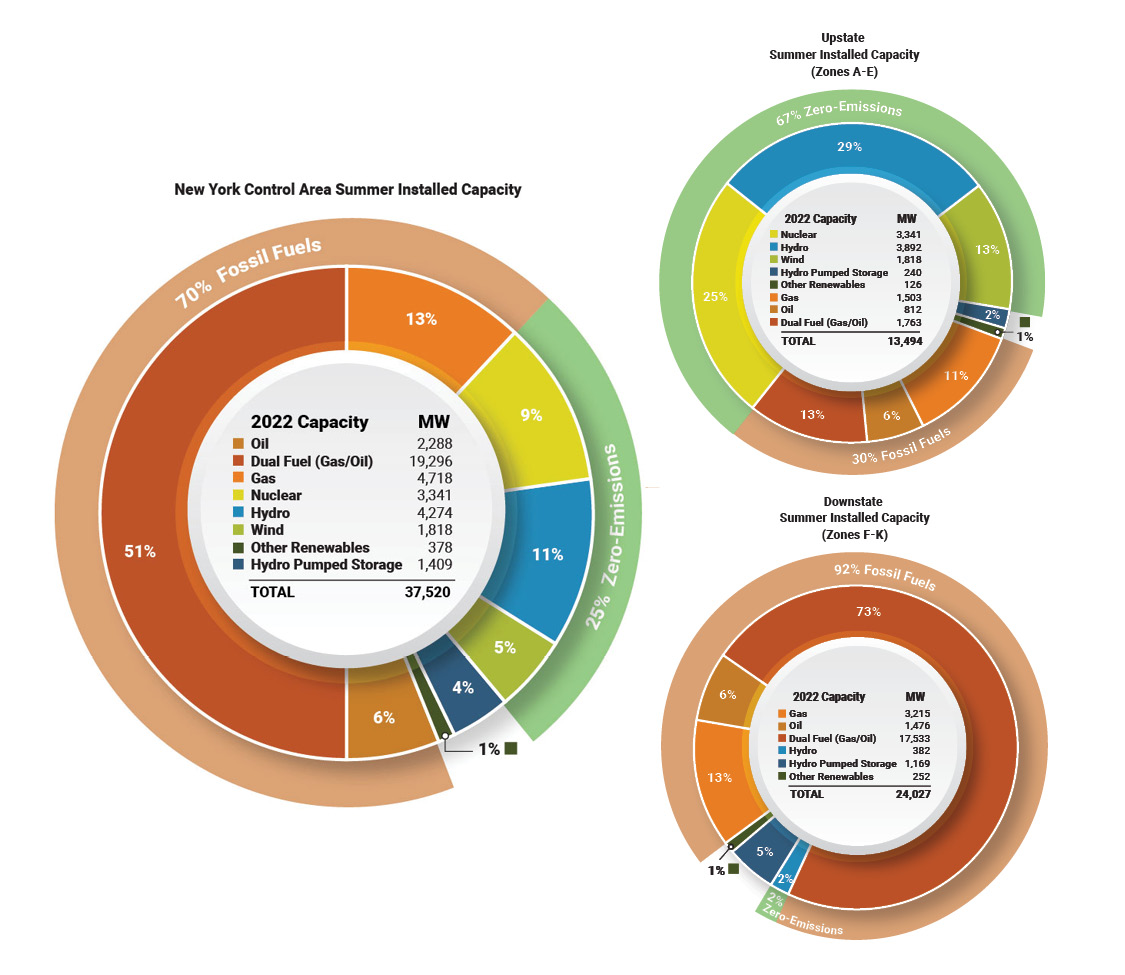

The state’s grid currently has 37,520 MW of total installed capacity, according to NYISO, and about 70% of that capacity is fossil fuel, the majority of which are dual-fuel systems for downstate zones; many will retire soon.

NYISO’s 2022 Reliability Needs Assessment found that these retirements are leading to tightening transmission security and resource adequacy margins that could become deficient by 2025 if critical emissions-free projects — such as the Champlain Hudson Power Express, an immense transmission project to import hydroelectric power from Quebec to New York City — experience delays. (See Champlain Hudson Power Project Receives Landmark Delivery.)

New York is walking a tightrope between its lofty aspirations and reality on the ground.

“We need to be able to adapt to the changes we see every day because, as exemplified by COVID, markets need to be able to react and respond,” DiDomenico said. “The state also needs a lot more coordination to happen to address the world changing around us.”

A desire for flexibility was also seen in a panel about climate change, resilience and reliability during extreme weather events, where natural gas was seen as critical to meeting current energy needs, particularly during emergencies like the December winter storm.

“We’ve had a surplus of fossil fuel resources, and that surplus not only offers flexibility and resiliency, but lets [NYISO] manage the grid as reliably as you see … and we don’t want to risk that,” said Aaron Markham, NYISO vice president of operations. “In New York there remain incentives to maintain dual-fuel capabilities because, particularly during high demands in the winter, we have to have fuel on site that can provide resiliency in case there is an emergency.”

The panel was supportive of renewable development but agreed that gas has a role in the transition.

“ISOs need be thoughtful about retiring [natural gas plants] too soon, because we don’t want to impact loads during the transition to a renewable future because we want to make sure we have sufficient resources available to meet resource adequacy needs,” Stephen George of ISO-NE said.

Chris Wentlent, chair of the New York State Reliability Council (NYSRC) Executive Committee, agreed. “Fortunately we went into this winter with a great fuel diversity that provided benefits when we started moving into the extremes for load,” he said.

This flexibility and desire for New York to think more creatively was best expressed by William Acker, executive director of the New York Battery and Energy Storage Technology Consortium, and Bart Franey, vice president of clean energy development at National Grid, during a panel on “The Future of the Electric Grid.”

“There are a lot of tools in our toolbox that can optimize [New York’s] transition going forward,” Acker said.

New York “needs to think about different kinds of solutions and be more flexible, and not always be applying standard practices to its transition,” Franey added.

Flexibility was not the only thing on panelists’ minds, and frequently, they cited the need for greater cooperation.

Franey said the state “needs to do a better job coordinating land use very purposefully” and engage with communities directly because New York does not have vast tracts of land to install large-scale renewable projects.

This call for greater cooperation was most observable during the fireside chat between State Sen. Mario Mattera (R) and Assemblymember Didi Barrett (D).

Mattera, the ranking minority member on the Senate’s Energy and Telecommunications Committee, said that “when I’ve worked with developers, they always come up to me saying that we need to get the local community involved, that we need to have open forums, and we need to involve everyone, because when you don’t do that, that’s when you have problems.”

Barrett, chair of the Assembly’s Energy Committee, concurred. “We’re not going to get to our goals by bullying people, by shaming people, by calling people names or lying, so my goal is to make sure that we do bring all of our communities, all of our producers and all of our businesses together, since they are important to our decarbonization”

Some still expressed skepticism about New York accomplishing its near- to medium-term goals, though they thought it was not too late to learn from any early mistakes and change course.

“I think New York has an aggressive but appropriate climate agenda,” Franey said, but he added that “with regards to 2030 goals, we got caught flatfooted, and to make sure 2040’s goals become real, we need to start thinking about planning and infrastructure that will be needed to address affordability and reliability concerns.”

Public Service Commissioner Diane Burman, agreed, saying, “We have to be clear that our near-term opportunities are not necessarily all going to be a done deal and that there will be significant challenges. …

“This transition does have fundamental risks, and we need to be open and transparent about that and work through those challenges together to figure out solutions,” she added.

Doreen Harris, president of the New York State Energy Research and Development Authority (NYSERDA), was more optimistic, saying, “We each have a critical role to play in this effort, and I believe change is not easy, but it is realizable. …

“This mid-transition point will have some messy spots on the way,” she added, but “I believe we are coming together in ways that not only get us from here to there but make our state the better in doing so.”

Panelists offered specific recommendations about how New York could be more flexible in its approach or better coordinate the transition.

NYISO’s Markham called for greater interregional cooperation among the RTOs/ISOs, saying, “Coordination amongst all [our neighbors] and state agencies as new polices are developed is critical to ensure there is an ability in those polices to keep resources around for reliability if necessary, because, in my opinion, that will minimize disruptions.”

Wentlent cited the NYSRC’s recent creation of an Extreme Weather Working Group, which was tasked with understanding how the grid is impacted by increasingly frequent and devastating disasters.

“We, and NYISO, are only at the cusp of understanding these [extreme weather events],” he said. He advised that New York study how every resource is correlated and impacted by these events because “until we understand all these pieces, we’re just at the beginning.”

Franey recommended that NYISO “could gain a lot of interesting efficiencies if [they] integrate storage with transmission … and, in some cases, could become more economical and efficient.”

“We have to make sure that we can be creative in our transmission-distribution system buildout, and that means looking at other technologies and not just traditional transmission technologies, since we want to make this as cost-effective as possible,” he said.

More than One Way to Skin a Cat

For decades New York’s clean energy sector has been dominated by nuclear and hydroelectric power, yet they do not produce nearly enough energy to achieve CLCPA mandates, speakers said.

That emissions-free generation has been bolstered recently, particularly by wind, which will soon make up a large part of New York’s total energy production once offshore projects being planned along the coast are connected. But still more renewables are needed if CLCPA goals are to be met.

The state’s future success will also heavily rely on distributed energy resources and dispatchable emissions-free resources, both of which are nowhere near at scale to meet the energy demands being asked of them and, to many observers at the conference, have yet to be fully fleshed out.

In that context, many panelists called for a more inclusive approach to New York’s decarbonization.

Mattera was one of the most vocal, saying, “It seems like we’re not doing enough to consider other energy technologies,” citing the perceived lack of research into hydrogen, geothermal, carbon capture, storage or wastewater heating technologies.

Keynote speaker Alexis Glick, CEO of biomethane producer Nature Energy, called for greater usage of biofuels. She pointed to the EU as evidence for how there are many ways to reach net zero, noting how it was forced to think creatively about its transition after Russia’s invasion of Ukraine caused gas shortages and embrace renewable natural gas (RNG).

“RNG is seen as a key ingredient to [Europe’s] clean energy future,” Glick said. The union, via the RePowerEU program, has committed to annually produce 35 million cubic meters of biomethane to displace Russian gas by 2030. “I believe RNG needs to play a critical role in our energy transition to achieve our mutual goals,” she said.

New York currently uses 50 trillion BTU of RNG per year, according to an April 2022 report from NYSERDA, and bioenergy accounts for less than 2% of the state’s electric generation, according to the agency. Biofuels were one of the most contentious topics as the CAC was developing the Scoping Plan, as members disagreed on its environmental benefits and role in the transition. (See Natural Gas Debate Heats up Hearing on CAC Scoping Plan.)

The Scoping Plan would recognize these resources as ways to reduce state emissions, but it still faces stiff activist resistance, which is why hydrogen was also discussed during the conference and offered as alternative to fossil fuels.

During an industry fireside chat, panelists such as Tim Cortes, chief technology officer at Plug Power, which develops hydrogen fuel cell systems, noted that hydrogen can be an important piece to the transition puzzle.

“Because we are still in the early stages of this transition, it is critical that we not take any viable solutions that could decarbonize the economy off the table,” he said.

“In the long run, hydrogen gives us the ability to be part of the solution by lowering emissions while keeping generating facilities that would’ve been retired around for a longer period of time,” said Mark Sudbey, CEO of Eastern Generation.

Referencing the risks posed by the early retirement of many fossil fuels generators, Rudy Wynter, New York president of National Grid, said, “We’re going to need a lot of solutions to achieve our goals, and so we should keep an open mind to the many pathways to decarbonization. …

“Hydrogen can play a role in this transition, especially if you’re operating off natural gas distribution networks because it will help to decarbonize those fossil fuels,” he said. Furthermore, RNG and hydrogen “can help us decarbonize [natural gas] molecules, because let’s be clear, not everyone is going to be able to afford to electrify, and some customers may have a harder time finding alternative decarbonization fuels.”

There was some reluctance about hydrogen’s potential, however.

“I think it’s still pretty early to judge [hydrogen’s] effectiveness in New York,” Markham said, because the “the challenge is that, No. 1, we still need the infrastructure to support not only the production and transportation of hydrogen, but also the storage; and secondly, what will the cost of that hydrogen be? Because the costs vary wildly.”

Hydrogen’s fluctuating costs can be partially attributed to its many forms, where the price of blue hydrogen, which is produced from fossil fuels, and green hydrogen, which comes from the electrolysis of water to produce zero emissions, are dependent on the price of the resource that they are derived from.

More important, there is a hard push to develop technology to generate green hydrogen much more cheaply, and the degree to which it is successful will be a critical determinant of green hydrogen’s prospects for large-scale adoption as a fuel.

NYSERDA’s Harris, however, cited hydrogen as an example of the collaboration the transition can create, referring to the seven-state Northeast Regional Clean Hydrogen Hub that was led by New York but pooled everyone’s expertise. (See Vermont Joins Northeast Clean Hydrogen Hub.)

“I believe we put together not only a winning proposal, but one in which we can continue to think about this resource and the ways it can help us achieve decarbonization,” she said.

“We have to catch our breath and recognize that we’re all in this together,” Commissioner Burman concluded. “We need to keep focused on what can be helpful as we move forward and how do we accomplish our transition in a way that is helpful, and not just rip off the Band-Aid saying, ‘We got this,’ because we may not, and we cannot risk reliability, affordability or safety.”

New Jersey’s largest planned offshore wind farm would have a “major” effect on commercial fisheries and “scenic and visual resources,” but only a moderate impact in 13 other categories, the Bureau of Ocean Energy Management said Monday in its an environmental impact statement (EIS) for the Atlantic Shores project.

The 900-page draft report on the 1,510-MW project concluded that the wind farm would have “moderate to major” impact on navigation and vessel traffic and a “major” impact on visual aspects of the sea and on cultural resources, such as historic, archeological and geographically significant areas.

The project would also have “negligible to moderate” impact on most mammals, including the endangered North American right whale, the report found. But the cumulative impact of nearby OSW projects and non-wind projects, and Atlantic Shores itself, including decommissioning of the turbines, would be “negligible to major,” the EIS reported. It said adverse impacts would “result mainly from pile-driving noise, vessel noise and presence of structures.”

The impact of OSW projects on whales has emerged as a significant issue in recent months, after several dead whales washed up on the Jersey Shore. Project opponents and two area congressmen have questioned whether the deaths were linked to preliminary marine study work underway for the projects and called for a halt to the projects while the issue is investigated.

Federal and state authorities say there is no evidence that the deaths had anything to do with OSW projects. But poll results released Thursday by Fairleigh Dickinson University suggest the unfounded reports are having an impact on public opinion.

The poll found that when the whale deaths were mentioned in the question, 35% of New Jersey residents said they favored continued offshore wind development, while 39% said development should be halted. When the whales were not mentioned in the question, 42% of those polled were in favor and 33% opposed.

The BOEM report says the impact to the whales of not approving the projects would be “negligible to major,” the same as if the projects go ahead because of issues such as “coastal and offshore development, marine transportation, fisheries use and climate change,” with a warmer ocean and strong storms affecting the sea mammals.

BOEM has scheduled two public hearing to solicit public comments on the draft on June 26 at 1 p.m. and June 28 at 5 p.m., with a 45-day comment period that ends on July 3.

Assessing Impacts

The New Jersey Board of Public Utilities picked the Atlantic Shores project in the state’s second OSW solicitation in 2021, when it also backed the 1,148-MW Ocean Wind II project being developed by Denmark-based Ørsted. The BPU picked Ørsted’s Ocean Wind I project in the state’s first solicitation in 2019. (See NJ Awards Two Offshore Wind Projects.)

The Atlantic Shores EIS covers the project’s first phase, which has been approved by the BPU, and a second phase for an additional 1,327 MW, which has not. Together, the two projects would involve installation of 200 wind turbines.

The draft EIS for Atlantic Shores, a joint venture between EDF Renewables North America and Shell New Energies US, assesses the potential biological, socioeconomic, physical, cultural and other impacts of the project, which at its closest is 8.7 miles from the Jersey shoreline.

The study assesses impacts of six different scenarios if the project is approved. These included approval of the entire proposal, along with several scenarios in which the project is modified, including a reduction in the number of turbines and offshore substations to minimize the impact on certain habitats; a reduction of the number of turbines to reduce the visual impact; modification of the project to create a “setback” between the project and neighboring Ocean Wind I; and an adjustment in the type of monopoles used in the foundation to reduce the impact.

The draft EIS then assesses the impact of each scenario and defines them as negligible, minor, moderate or major.

The EIS, for example, concluded in all the scenarios that the impact was either moderate or lower for air; water; birds, coastal habitats and fauna; fish, invertebrates and essential fish habitat; sea turtles; wetlands; demographics, employment, economics; environmental justice; land use and coastal infrastructure; and recreation and tourism.

Increased Vessel Traffic

The study found that the commercial and recreational fishing sectors would be impacted by increased anchoring of boats working on the turbines, marine disturbance caused by cable emplacement and maintenance, and the additional noise generated by construction. Those factors could disrupt fishing trips and make it difficult to fish, as well as prompting some commercial companies to avoid fishing in certain areas — all of which could reduce revenue, the report said.

The effect might also be to push all commercial fishing operations into the same, smaller fishing area, resulting in smaller catches, the report concluded.

“BOEM expects that increased vessel traffic associated with the proposed action would cause long-term, localized, moderate impacts on commercial and for-hire recreational fisheries,” the report concluded. BOEM also found that the overall impact on commercial fishing operations could be “major” in many scenarios.

The study found that the area’s cultural resources would be affected whether BOEM approved the wind projects or not and labeled the impact in the long term “major” in all scenarios, but only “moderate” if the projects were not approved.

“The primary sources of onshore impacts from ongoing activities include ground-disturbing activities and the introduction of intrusive visual elements, while the primary source of offshore impacts includes activities that disturb the seafloor,” the report found. “While long-term and permanent impacts may occur as a result of offshore wind development, impacts would be reduced” through a consultation process to reduce the effects on historic properties, the study concluded.

Navigation and Visual Impacts

The study found that navigation and vessel traffic would experience moderate impact regardless of whether the projects went ahead, in part because of rising traffic in the area and also traffic generated by other offshore wind projects. New Jersey’s OSW projects, if approved, would have a moderate to major impact when added to the cumulative impact of vessel traffic from nearby OSW projects and general water transportation traffic.

“Impacts from the proposed action alone would include increased vessel traffic in and near the project area and on the approach to ports used” by the OSW vessels, the report found. Vessels in the area would also experience “obstructions to navigation” caused by the projects.

During construction, the project would cause “short-term increase in project-related construction vessel traffic, short-term presence of partially installed structures, and short-term safety zone implementation,” the study found.

“Impacts on navigation and vessel traffic would also include changes to navigational patterns and to the effectiveness of marine radar and other navigation tools,” the report said. “This could result in delays within or approaching ports, increased navigational complexity, detours to offshore travel or port approaches.”

The study found that scenic and visual resources would suffer a “major” impact in the longer term, whether the New Jersey wind farms were built or not, because of other wind farms nearby being built and as a result of other marine activities, such as dredging and port improvements, marine minerals extraction and marine transportation, the report found.

If the state’s OSW projects don’t go ahead, “the character of the coastal landscape would change in the short term and long term through natural processes and planned activities that would continue to shape onshore features, character, and viewer experience,” BOEM said.

“Ongoing activities in the geographic analysis area that contribute to visual impacts include construction activities and vessel traffic, which lead to increased nighttime lighting, visible congestion, and the introduction of new structures,” the report concluded. The cumulative impact of other OSW projects and general marine activities would create a “major” impact, the study said. As a result, the cumulative effects of the projects and others in the area would be “appreciable,” the study concluded.

“The main drivers for this impact rating are the major visual impacts associated with the presence of structures, lighting and vessel traffic,” the study found.

VALLEY FORGE, Pa. — PJM has doubled its synchronized reserve requirement to account for diminished performance since the implementation of the reserve market overhaul in October.

Donnie Bielak, PJM senior dispatch manager, told the Operating Committee that reserve performance has been approximately 50% since the RTO implemented reserve price formation last year, which consolidated reserves into one product, lowered the offer cap from $7.50/MWh to 2 cents and expanded resources subject to the must-offer requirement. (See Synchronized Reserve Pricing Falls in PJM Markets After Overhaul.)

The higher reserve requirement, announced to members Thursday morning, went into effect for the day-ahead market for Friday and was in place starting at midnight. The increase amounts to an additional 1,588 MW procured, equal to the single largest expected contingency.

“This is meant to be an immediate, albeit temporary measure,” Bielak said. “We are doing this to make sure we have reliable and uninterrupted service to the load.”

Several stakeholders questioned the timing and the immediacy of the decision, asking why there was not more notice. Bielak told RTO Insider that following stakeholders’ decision to initiate a quick-fix process to address reserve rates last month, PJM staff determined a more immediate solution was needed going into the summer months.

Generator performance during the December 2022 winter storm may have led to a violation of NERC’s disturbance control performance (DCS) standard by potentially taking 52 seconds longer than the permitted 15 minutes to alleviate a contingency event recovery period on Dec. 23.

Independent Market Monitor Joseph Bowring said PJM hasn’t provided any evidence of a reliability issue or that there is a risk of violating the DCS standard. After the operating reserve rule change on Oct. 1, 2022, the must-offer requirement for synchronized reserve significantly increased the amount of reserves available, he said, noting also that there have been no issues with violating the NERC DCS standards. Bowring also asked PJM to explain why it thinks it has the authority to unilaterally double the reserve requirement.

Bielak said PJM thinks it has been able to procure adequate synchronized reserves because some generators are continuing to operate under the old ruleset, despite not receiving revenue for doing so. As that reality becomes clear for market participants, the RTO may not receive the same response to its calls to generators. (See PJM MIC Briefs: April. 12, 2023.)

PJM Projects Adequate Supply This Summer

The 2023 Summer Study found that the RTO will have enough installed capacity, 186.5 GW, to meet its 90/10 load forecast of 162.7 GW. The non-diversified peak demand is expected to be 156.1 GW.

“PJM works diligently throughout the year to coordinate and plan for peak load operations, with reliability as our top priority,” PJM CEO Manu Asthana said in an announcement of the study on Thursday. “We’re not saying these extreme conditions will happen, but the last few years have taught us to prepare for events we have never seen.”

No reliability issues were identified; however, re-dispatch and switching could be required in some areas to avoid thermal or voltage violations.

Demand response may need to be implemented in the event of “extraordinary electricity demand and high generator outages,” with around 7.5 GW in pre-emergency load management found to be available in the study.

The study found that PJM should have resources to cover the outage scenarios historically seen in the summer months. It also draws on lessons learned from the February 2021 winter storm to incorporate the possibility of extreme conditions without precedent.

“We have learned through experience to expand the set of possibilities we prepare for,” Senior Vice President of Operations Mike Bryson said in the announcement. “We will continue to work with our utility partners and stakeholders to refine our planning, analysis and communications of the risks presented by new and challenging weather patterns and other variables.”

About 15.4 GW of discrete generator outages are expected in the study, as well as 4 GW being lost through net interchange. Under the largest gas-electric contingency, which is expected to take 4.8 GW off the grid, PJM would have an additional reserve margin of 4.1 GW. The no-wind and low-solar scenario would reduce available capacity by 5.6 GW, producing a margin of 3.4 GW.

Last year’s study presented the largest contingency and the low-renewables scenario together; however, PJM spokesperson Jeff Shields said it would be unlikely for those conditions to overlap. (See PJM Summer Forecast Reports Sufficient Supply.)

“We didn’t feel that stacking all the contingencies together made for a plausible scenario,” he said. “We wanted to emphasize that with high generator outage failures and high load, combined with either of the unlikely scenarios of almost no sun in peak summer conditions or major pipeline failure, we would have to call on demand response.”

Discussion Continues on Transmission Outage Coordination Proposals

A joint package from PJM, DC Energy and Public Service Enterprise Group (NYSE:PEG) would involve coordination between utilities and RTO staff to identify any extended outages that may be required, evaluate the impact of those outages and expand outage information shared by PJM. Upgrades to facilities may be considered if outages are expected to cause significant operational issues.

The Monitor’s proposal would consider requests to reschedule an outage as a new request and classify it as a late submission if the request comes too close to the scheduled date. The language also would aim to reduce or eliminate approval of outage requests after FTR bidding opens and prevent TOs from bypassing rules for long-duration outages by breaking them into smaller segments.

Bowring said the Monitor’s proposal wouldn’t change existing processes, but it would more clearly define when outages should be considered late and provide market participants with more information about outages.

“We’re not trying to change the way outages are scheduled. We’re just trying to ensure they’re labeled correctly,” Bowring said. “… The goal is to make it easier to understand why the system is behaving the way it is.”

PJM’s Paul Dajewski said the status quo rules allow for outages submitted on time to be rescheduled regardless of their duration, which provides TOs with flexibility when scheduling their outages. He said the ability to reschedule is necessary to account for circumstances such as delays in equipment availability or weather.

Bowring responded that he understood that outages have to be scheduled well in advance and include flexibility but said the Monitor’s proposal wouldn’t change market mechanisms or how outages are scheduled, instead providing more information for other market participants.

Other OC Business:

Stakeholders approved revisions to manuals 3 and 36 under each document’s periodic review. In both cases, the changes were updating the manuals with new information, as well as clarifying language in Manual 3.

PJM’s Steve McElwee provided a cybersecurity update, saying that a recent attack on Dragos displays the need to stay vigilant against “social engineering” hacks being used to gain access to sensitive systems. (See Cancel: Dragos Breach Did Not Compromise E-ISAC.) He said if a member’s email systems were compromised, it would be difficult for PJM to determine that a breach had occurred unless it had been detected by that organization.

The OC voted by acclamation to sunset the Synchronized Reserve Deployment Task Force due to an inability to determine a path forward since FERC rejected PJM’s intelligent reserve deployment in August 2022. Task force facilitator Vijay Shah said its issue charge has limited the ability to discuss the concerns the commission raised in its order and there has been limited discourse and no proposals currently before the group. Shah noted that PJM’s Adam Keech said during the Annual Meeting that RTO staff plan to bring a new problem statement and issue charge this summer.

WASHINGTON — Much of the focus at the Energy Bar Association’s Annual Meeting last week was on the grid’s transition from fossil fuels — specifically matching carbon-free electricity to demand curves.

“For many of you, it may feel like the goalposts are moving, complicating business risks,” NorthBridge Group Partner Neil Fisher said. “And what was considered the gold standard five years ago may not be acceptable in the near future.”

While retiring renewable energy credits from wind farms far from the customer was seen as good enough in the past, now many large, sophisticated customers want to match their load with 24/7 clean energy.

The federal government — the largest buyer of electricity in the country, at about 54 TWh per year —historically only tried to comply with the Energy Policy Act of 2005, which required 7.5% of that come from renewables, said White House Council on Environmental Quality Director of Clean Energy Tanuj Deora.

But President Biden has upped that with a goal of getting the federal government to 100% carbon-free electricity by 2030.

“We know it’s very ambitious, right?” Deora said. “So, we are looking actively to figure out how we get there because not only is it ambitious, but it is absolutely necessary. I think we all know that we’re living the consequences of climate change, and the impact on the environment here real time, and so there’s no time to waste.”

Today the grid is already at 40% carbon-free power so the federal government procurements will take that into account.

Deora said the government would not seek to supply its facilities exclusively with the output from existing zero-emissions facilities. Instead, the procurements will focus on new resources. And the government is hedging its bets because it is still unclear exactly which technologies will prove economical and scalable among advanced nuclear, virtual power plants, carbon capture and storage, clean hydrogen and others.

The federal government is not alone in trying to procure more green power. Voluntary commitments from corporate buyers helped to build about 40% of new clean energy resources in recent years, Deora said.

Google (NASDAQ:GOOGL) has aggressive clean energy goals and a total load of 18 TWh annually that is growing because of computing power demands from new technologies like artificial intelligence, the firm’s Brian George said. Google says it has met its entire demand with renewable energy since 2017.

“Even as we do that, there are periods during the day where we still rely on fossil energy to serve our data center demand,” George said. “In 2021, around the world … our data centers consumed about 66% of carbon-free energy on an hourly basis.”

Like the federal government, Google wants to increase that to 100% by 2030, which will require it getting new resources built where they can directly serve its data centers. Focusing on 100% carbon-free electricity can help send the signals that are needed to build out the new technologies required to reach an emissions-free grid, he added.

“Our systems are not set up to recognize and reward customers for what they are already doing just from paying their electric bills, much less … be tailored to the actions that the Googles of the world want to be taking to be driving change,” said Constellation Energy (NASDAQ:CEG) Senior Vice President of Public Policy Mason Emnett. “And so, we’re spending a lot of time working with our customers in terms of the product development, the commercialization of these types of products.”

While wind and solar are the cheapest options now, over time the more they get built the less the power produced matches up with demand every hour. Emnett said once they hit about 50% of demand that split starts to grow. Once you get to 100% annual match with renewables, the grid is still relying on balancing resources for about 25% of its total needs, he added.

Interregional Transmission

Another EBA panel focused on getting more interregional transmission lines built.

The experiences of Texas and its neighboring grids in SPP and MISO during the 2021 winter storm are one of the main reasons former FERC Chair Richard Glick wants to see interregional transmission built. ERCOT lacked major connections with the outside, and it was short on power for days, leading to hundreds of deaths, while the nearby sections of the Eastern Interconnection were able to import power from farther afield and avoided the worst.

“There is a lot of consensus out there that much more is needed in terms of connections between these regions,” Glick said.

Many in Texas might still be skeptical about linking up with the rest of the grid. But in other regions, even state regulators have indicated that they support addressing the barriers to interregional transmission.

“We do know, with regard to interregional transmission in particular, that there are multiple benefits,” Glick said. “And part of the problem — some are very easy to quantify, like probably production cost reductions — … but some of the benefits, whether it be resilience, whether it be achieving public policy goals … are more difficult to quantify.”

Figuring out a way to quantify those benefits is going to be necessary to make progress and deal with the very tricky issue of cost allocation, he added.

“Whenever we talk about transmission, it always does come down to cost allocation,” Glick said. “There’s a lot of other issues. There’s always barriers, but cost allocation is the big one.”

While interregional transmission can produce benefits, the conversation around expanding it has not been very refined, said Edison Electric Institute Managing Director Kevin Huyler.

“When I look at some of the proposals that are out there for driving interregional transmission investment, I don’t see a lot of nuance, which sometimes isn’t surprising, particularly if it’s a legislative proposal,” Huyler said.

Some have suggested that regions should be able to get a 30% minimum transfer requirement, but Huyler said nobody really knows what the right number is, and getting accurate figures is vital to proper transmission planning.

“It can’t be entirely precise,” he added. “But I think there has to be an effort made … to have customers and stakeholders [understand] why that much is being built.”

Invenergy is pursuing merchant interregional projects around the country, along with the development of new renewable resources and that makes it come at the issue with a sense of urgency, said its Executive Vice President of Public Affairs Kelly Speakes-Backman.

“I don’t want to turn this into a whole climate discussion, but it’s real and it’s here, and we’ve got not a lot of time to fix this,” Speakes-Backman said. “Frankly, the planning and the work that goes into it takes a really long time. And this is part of why we’re in the transmission business itself — to help with the urgency.”

Invenergy can make it easier to get transmission by investing its capital to get new lines constructed. But it does need to get paid for the benefits of such investments to make it work economically, she added.

SACRAMENTO, Calif. — West Coast states need to work together on transmission, ports and industrial infrastructure to achieve their goals for floating offshore wind, speakers at this year’s Pacific Offshore Wind Summit said.

The two-day event, hosted by Offshore Wind California, drew 700 attendees to the SAFE Credit Union Convention Center in downtown Sacramento on May 9-10.

Panelists encouraging collaboration cited lessons learned, both positive and negative, from the East Coast’s experience developing offshore wind projects and infrastructure.

“What we have learned is that there’s great power in bringing the states together,” said Travis Douville, who leads wind energy grid integration research at the Pacific Northwest National Laboratory.

“There already are models of substance in play,” Douville said during a panel on offshore wind transmission. For example, the New England States Transmission Initiative “is showing real promise, and the idea here is that states can come together and develop a shared transmission plan that serves all of their needs at the state level.”

Last year, five New England states — Connecticut, Massachusetts, Maine, New Hampshire and Rhode Island — announced their joint initiative to explore investment in the transmission infrastructure they need to integrate offshore wind and other clean energy resources while improving grid reliability.

One of their proposals, the Joint State Innovation Partnership for Offshore Wind, would “proactively plan, identify and select a portfolio of transmission projects needed to unlock the region’s significant offshore wind potential, improve grid reliability and resiliency, and invest in job growth and quality.”

California, Oregon and Washington could benefit from similar arrangements, Douville said.

‘Pacific Coast Scale’

The West Coast states have nearly 300 GW of potential capacity from floating offshore wind turbines, the National Renewable Energy Laboratory estimated in a study last year. California has 88 GW of potential capacity. Oregon has 150 GW, and Washington has 59, NREL said.

The states, federal government and private industry are planning to develop that capacity, starting south and working north.

The Bureau of Ocean Energy Management (BOEM) held the first West Coast wind auction Dec. 7, when five lease areas off the California coast, with 4.5 GW of total capacity, brought more than $757 million in winning bids. (See First West Coast Offshore Wind Auction Fetches $757M.)

Three of the lease areas are in the Morro Bay Wind Energy Area off the coast of Central California, and two are in the Humboldt Wind Energy Area off the coast of Northern California.

The auction was crucial to achieving the Biden administration’s goal of deploying 15 GW of floating offshore wind in deep waters by 2035, the Interior Department said. The California Energy Commission has proposed offshore wind goals of 25 GW by 2045. (See California Boosts Offshore Wind Goals.)

Off the coast of Oregon, BOEM has identified three call areas with 17 GW of capacity, one of which, the Brookings Call Area, is 60 miles north of California’s Humboldt Wind Energy Area. The proximity quickly prompted discussion of collaboration between the West Coast states.

“The growing Pacific Coast scale of this … sets in motion a whole set of speculation about coordination across the region,” Adam Stern, executive director of Offshore Wind California, told an Energy Bar Association meeting shortly after BOEM announced the Oregon call areas Feb. 24, 2022. (See Energy Bar Weighs OSW in Oregon, California.)

In Washington, BOEM has received two unsolicited bids for floating wind farms but has yet to identify any call areas.

Washington has moved more slowly on offshore wind, in part because of its vast supply of hydroelectric power, said Ryan Calkins, a Port of Seattle commissioner and part of a panel on West Coast collaboration.

“We have such an abundant source of renewable energy in hydro that I think we didn’t get off the starting blocks very quickly,” Calkins said. “However, I think we’re starting to see some real progress.”

The state has an energy strategy that includes 3 GW of offshore wind by 2045, and “oftentimes you’ll hear our state officials talk about ‘it’s not if, but when’ we will get into offshore wind,” he said.

The state is expecting to learn from California’s experience with offshore wind, including its effects on fisheries, coastal communities and Native American tribes, he said.

“When we join California in a few years with our own plans for offshore wind, I welcome the inputs of California ports and supply chains to help us meet our targets,” Calkins said. “I think it just makes sense for us to have a systemwide approach to this.”