California-based TAE Technologies on Tuesday said its research reactor had achieved and maintained control of plasma in the heart of a fusion reactor at a temperature of 75 million degrees Celsius (135 million degrees Fahrenheit) in a self-created magnetic field.

The company’s target temperature is 100 million C (180 million F), which it believes it can control to initiate sustained fusion and build a commercial reactor by the end of the decade.

TAE is among a half dozen startup research companies, including one in Seattle, working to develop a working fusion reactor to create energy by fusing atoms rather than splitting them as conventional nuclear power plants do. (See Fusion Company Gets $500 million.) Fission creates radiation in the process and leaves behind radioactive waste, some of which will be dangerous for millions of years. Fusion reactors do not produce long-term radioactive waste.

Unlike competing fusion research companies that have been working to fuse hydrogen from heavy elements and can be slightly radioactive while operating, TAE has been working since 1998 with hydrogen and boron, a common element found in cleaning products.

TAE’s rector creates enormous amounts of heat by fusing the nuclei of hydrogen atoms with those of boron atoms in a radiation-free process that also creates helium, an inert gas. Boron is ubiquitous on Earth, and the company estimates a 100,000-year global supply.

The research reactor is a fifth-generation test machine, dubbed “Norman” in honor of TAE co-founder Norman Rostoker, a Canadian plasma physicist who died in 2014. The reactor began operating in 2017.

The company credited Norman’s success to sophisticated control technologies it developed with Google since partnering with it in 2014.

“Through successful training of Norman’s state-of-the-art control system, paired with proprietary power-management technology and extensive optimization of our machine-learning algorithms, we have achieved a scale of control at an unparalleled level of integrated complexity,” TAE CEO Michl Binderbauer said in a statement.

The success of the Norman reactor has enabled TAE to secure $250 million in new funding for a larger test reactor, which it has named Copernicus. Since its founding it has received $1.2 billion in private investment and received more than 1,100 patents related to its technology.

The most recent investors include Chevron, Google, Reimagined Ventures, Sumitomo and Tiff Investment Management, as well as a large pension fund and a mutual fund manager, both unidentified.

“The caliber and interest of our investors validates our significant technical progress and supports our goal to begin commercialization of fusion by the end of this decade,” Binderbauer said. “Global electricity demand is growing exponentially, and we have a moral obligation to do our utmost to develop a baseload power solution that is safe, carbon-free and economically viable.”

The company characterized its hydrogen-boron technology as “the cleanest, safest, most economical terrestrial fuel cycle for fusion, with no geopolitical concerns or proliferation risks.”

The company’s announcement includes little detail on the “balance of plant” technologies that it will need to harness the enormous amounts of energy created by the fusion. In a FAQ document accompanying the announcement, there is a reference to a “steam generator.”

“Just as you feel warmth when sunlight hits your skin, in a power plant, the containment vessel wall will heat up from energetic light emanating from the plasma. The wall will be cooled through a network of pipes, which have working fluid streaming through them to pick up the heat and transport it to a steam generator,” the FAQ explains.

“The steam spins a turbine that then drives an electric generator, similar to what happens in operating power plants today. TAE’s unique fusion core supplies a superior and environmentally benign heat source for future power plants.”

Oregon officials are grappling with how the natural gas sector will fit into the state’s decarbonization strategy, with industry players seeing a clear role in a clean energy future and skeptics seeking a sharply reduced position for gas companies.

The two sides pitched their perspectives at a virtual public hearing hosted by the Oregon Public Utility Commission (OPUC) on July 12. The commission called the hearing to solicit input on its draft Natural Gas Fact Finding report, issued in April. A final version of the report is due to be released Aug. 12.

The hearing also cast light on the uncertainty utility regulators in Oregon — and elsewhere — face as they’re forced to balance their roles as economic supervisors with the growing need to factor environmental mandates and the decisions of sister agencies into their own decision-making and long-term planning.

According to the draft report, Oregon’s three natural gas utilities in 2019 earned $810 million in revenues while delivering about 1.6 billion therms of gas. Residential customers accounted for about 59% of those revenues, followed by “firm” commercial and industrial customers at 33%. Pipeline transport customers — who acquire their gas from other sources — accounted for just under 5% of revenues but more than 40% gas utility deliveries.

The Climate Protection Program (CPP) adopted last year by Oregon’s Department of Environmental Quality requires gas utilities to reduce greenhouse gas emissions by 50% by 2035 and 90% by 2050. All gas deliveries will be subject to the declining caps, including those for transport-only customers.

The fact-finding is intended to serve two purposes, the PUC said: to analyze the ratepayer impact of limiting gas utility GHG emissions under the CPP; and to “identify appropriate regulatory tools to mitigate potential customer impacts and accommodate utility action.”

At last week’s hearing, OPUC Utility Strategy and Planning Manager Kim Herb told hearing participants that the draft report points to the “strong and divergent opinions about how the natural gas industry decarbonization will come about.”

Even so, Herb acknowledged, some groups complained the draft report failed to capture their input. Environmental, community groups and “grassroots” commenters contended that the report focused on the financial costs of complying with the CPP while downplaying the societal benefits of climate-related policies and investments.

Those commenters advocated for a policy of halting the further expansion of the gas system in Oregon, which would entail prohibiting new gas hookups for new construction in favor of building electrification. Builders would instead be steered to heat pump technology for space heating, which would provide the added benefit of cooling in the warmer months.

Greer Ryan, Oregon clean buildings policy manager for Climate Solutions, said the organization was “extremely concerned” by the draft report.

“We’d like to see more benefits captured. When we’re talking about programs that are meant to address the climate crisis in Oregon, it’s not just about short-term costs, but we think about longer-term costs of inaction and the benefits that communities receive from these kinds of investments,” Greer said. The draft also “failed to incorporate the bulk of community groups’ feedback, and in some cases misrepresents alignment between nonprofit and community-based organizations and the utility and industry groups.”

Climate Solutions is calling for the PUC to immediately discontinue gas companies’ “line extension allowances,” ratepayer-based subsidies that permit the connection of new customers at no cost. Any subsidies should be directed to support “a clean and renewable energy economy,” especially for low-income and environmental justice communities, Greer said.

She also said the PUC’s final report should “not give credence” to gas industry arguments that the system must be expanded “to protect communities.”

“This argument is reflective of the gas industry co-opting legitimate community concerns without taking into account actual community-based organizations and ratepayer advocate feedback,” she said.

Zach Kravitz, director of rates and regulatory affairs at NW Natural, Oregon’s largest gas provider, said the company “respectfully” disagreed with “some stakeholders’ approaches, which we view as morphing this fact-finding around the CPP into a binary policy choice about the future of natural gas.”

Kravitz said NW Natural believes that it can decarbonize its system and comply with the CPP at a “reasonable cost.” The energy delivered by the company’s gas system cannot be easily replaced, he said, adding that during a cold winter morning, it delivers about twice as much energy as the electric system.

“Our modeling indicates that our compliance with the CPP carbon-reduction targets is achievable through a combination of increased energy efficiency, conservation [and] installation of low-use appliances like dual-fuel or hybrid heating systems or gas heat pumps; reduced intensity of our gas supply; and the use of community climate investments [CCIs],” Kravitz said. Under the CPP, energy providers will be allowed to offset a portion of their emissions with CCIs.

The company wants the PUC to implement a process of joint system planning among gas and electric utilities, he said.

“We can’t look at gas and electric in silos anymore. And we can really leverage each other going forward, whether it’s hydrogen, where we can utilize excess renewables and store it on the gas system, or even hybrid heating, which NW Natural is open to and wants to explore further and which can really help address resource adequacy on the power grid [by] having gas utilities meet space heating demand during those peak periods,” Kravitz said.

Lori Blattner, director of regulatory affairs for Cascade Natural Gas, voiced concern that the fact-finding is moving in an “anti-gas direction.”

“Cascade encourages the commission to instead continue to encourage innovation throughout the natural gas distribution system that will allow natural gas utilities to make carbon-reduction goals, while still providing customers all the benefits of energy diversity, including reliability and affordability,” Blattner said.

‘Unique Opportunity’

Commissioner Mark Thompson mused that PUC might be confronting two competing paradigms. In the first, the agency must fulfill its duty to protect utility customers financially as an economic regulator amid sweeping change. In the second, the commission would have to expand the notion of protecting customers to considering the most cost-effective way to decarbonize the gas system — and the energy industry — as a whole.

“How do you think we ought to balance and understand that our role in this environment?” Thompson asked Climate Solutions’ Greer.

“I think that as economic regulators being tasked with having the least-cost and reduced-risk criteria in mind, you can absolutely take into account costs and risks of inaction on climate. And there’s more and more precedent for this and other state commissions,” Greer said.

Commissioner Letha Tawney ticked off some of the lingering uncertainties that come with decarbonizing an electricity sector expected to replace gas. She named the impact of transportation electrification, the difficulty in siting new transmission, offshore wind controversy and the reliability concerns that come with fossil fuel plant retirements.

“I’m curious how you’re thinking about sort of the large-scale risks of the vision you’re putting forward,” Tawney asked Greer.

“My two cents, right now, is that this transition is not happening overnight. I think gas utilities and other fossil fuel companies try to use the tactic of spreading fear by saying, ‘If you do this transition, we won’t be able to afford it. People will be without power because we have reliability issues.’ But the fact of the matter is, it’s going to take some time to curb the gas system. We can have strategic planning conversations.”

Thompson wondered whether the PUC was facing a “Y” in the road, in which one path led to gas companies achieving decarbonization through use of renewable gas and hydrogen without having to worry about depreciation and a shrinking system — and actually investing in new assets — while the other path leads to gas companies shrinking, the elimination of the line-extension policy and a push for electrification.

“I don’t actually agree that it’s a ‘Y,’ and you’ve got a choice to either go down one path or the other,” said Bob Jenks, executive director of the Oregon Citizens’ Utility Board.

Jenks said it won’t come down to the PUC deciding which path to choose. Rather, different government agencies and hundreds of individual customers will be deciding whether they want fossil fuel coming into their homes.

“Do they want the most efficient cooling system that they can get — an electric heat pump? And with that comes efficient heat,” he said.

Mark Gamba — mayor of Milwaukie, a suburb of Portland — said “rational people” must confront the fact that the world is confronting “climate chaos.”

“Methane, greenwashed as natural gas, is one of the most powerful greenhouse gases in the world; it’s 86 times more powerful than CO2,” Gamba said, adding that burning natural gas inside a home also impacts human health.

“You have a unique opportunity to start to make actual changes so that … when it becomes abundantly clear to everyone that we need to be moving away from methane, it’s not a sudden and catastrophic switch,” he said.

NEW YORK — The ABB FIA Formula E World Championship’s New York City E-Prix returned to Brooklyn on Saturday with a race that started in sunshine and ended abruptly with a rainout and a dramatic multicar crash.

Twenty-two of the championship’s second-generation (Gen2) open-wheeled, single seater electric cars took to the track in the lead up to the Season 8 finale in Seoul, South Korea, in August. The Gen2 cars will retire officially after this season’s championship, and the next generation (Gen3) will debut for the 2023 season.

The Formula E race cars are not as loud as their fossil-fueled counterparts, but they still quicken the pulse up close with a high-pitch whine and top speeds of 200 mph. The 45-minute race Saturday came to a halt with seven minutes remaining when the cars entered a sudden downpour, which caused the two lead cars to hydroplane in quick succession into a wall followed by the fourth-place car.

The crash led to a red flag, stopping the race. While drivers were on standby, officials determined that the race would not continue because of safety concerns and called the winners based on the drivers’ standing in the lap prior to the red flag. Nick Cassidy (No. 37) of Envision Racing, the winner of the race, and second-place winner Lucas di Grassi (No. 11) of ROKiT Venturi Racing, had crashed, while third-place winner Robin Frijns (#4) of Envision survived the slick conditions without incident and took over the lead.

“We had a really nice fight,” Cassidy said at a press conference after the race. “It got slippery; it got fun; and then ultimately, it was a bit too much.”

Di Grassi expressed gratitude for the cars’ safety features.

“This was the biggest crash of my Formula career,” he said. “I’m without any problems, but the car is pretty much destroyed, and that shows how safe these cars are.”

Di Grassi was going about 62 mph when it crashed, he said.

Frijns said visibility was low coming up on the crash site, but he managed to break early enough to make the turn that the lead cars in front of him had missed.

“When the rain came, I saw Lucas in a 90-degree angle in front of me, which is never good,” Frijns said. He added that although he had thought he won the race, he believed the final ruling was “a good one.”

Gen3

The International Automobile Federation (FIA) and Formula E introduced the Gen3 car in April, calling it the “pinnacle of high performance, efficiency and sustainability.”

Seven auto manufacturers have agreed to race under the Gen3 standards next year. They include DS Automobiles, Jaguar, Mahindra Racing, Maserati, NIO 333 Racing, Nissan and Porsche.

The new standards call for a top speed of about 200 mph, which will push the vehicles closer to the traditional Formula One car’s top speed of about 230 mph. On the charging front, the cars will produce about 40% of the energy used in a race through regenerative braking. And it will have ultra-high speed charging capability of 600 kW, or almost double most current commercial chargers, according to FIA.

Among the updated sustainability standards for Gen3 will be the first ever use of linen along with recycled carbon fiber from the Gen2 cars for the new car bodies. FIA said the recycled materials will reduce the carbon footprint of the Gen3 body construction by 10%.

Tires for the new season will include 26% natural rubber and recycled fibers, and all tires will be recycled after use.

In designing the Gen3 car, FIA tracked all the carbon-reduction measures that will reduce the cars’ impact, while carbon offsets will address all remaining emissions.

RCAR III Shows Dramatic Improvements in all Tx Zones

WESTMINSTER, Colo. — SPP’s third Regional Cost Allocation Review (RCAR) of the regional and zonal allocation methodology’s reasonableness left several members dinged by the first two reports in a cautious, yet celebratory mood during last week’s Markets and Operations Policy Committee meeting.

“We’re not popping the champagne yet,” said Jeff Knottek, director of system planning and compliance for City Utilities of Springfield (Mo.). He was among several members who have requested meetings with the RTO’s staff to better understand how the new numbers were derived.

CUS was the only utility below a benefit-to-cost ratio threshold of 0.80 in its transmission zone after the first RCAR in 2012. It was joined by five other utilities who failed to meet the 40-year present values of the estimated benefit metrics and costs in 2016’s RCAR II.

However, the preliminary RCAR III review pegged CUS’ ratio at 10.65, third among all pricing zones.

“It feels pretty good to be a winner,” said Empire District Electric’s Aaron Doll, whose zone went from a 0.60 to a 6.04 in the last two RCARs. “Empire would be interested in meeting with SPP staff to understand how our B/C ratio increased tenfold with little to no investment. … We’re a little bit skeptical the increase was so substantial without the investments commensurate with that.”

SPP General Counsel Paul Suskie said the Regional Allocation Review Task Force, comprising SPP regulators and members, took a hybrid approach to RCAR III. Staff used actual market runs with and without highway/byway transmission and took a planning-based approach for approved upgrades not in service for at least two years.

The review’s preliminary operational results show significant B/C results for the region and all pricing zones. Staff used 538 of 741 highway/byway upgrades, totaling $4.6 billion of $6.4 billion in upgrade costs. They said it is unlikely any remedies will be needed.

Suskie said the real-life models were a contrast to the first two RCARs, which were more “theoretical, what we thought the system would look like.” That resulted in lower B/C ratios for CUS, Empire and others.

“For instance, we said in 2020 [that] we would have 17 GW of wind in 2022. Today, we have 31 GW,” Suskie said. He pointed out that the recent run-up in natural gas prices also created higher ratios.

MOPC endorsed the RARTF’s recommendation to direct staff to finalize the report based solely on operational results. When the report is brought back to the committee in October, members can then determine if the full planning process is needed to supplement the operational result.

MOPC Keeps SPS’ Tx Alternatives Alive

Committee members endorsed two projects as potential solutions for a 345-kV double-circuit transmission line in eastern New Mexico’s Permian Basin region.

They sided with staff’s recommendation to issue a notification to construct following further evaluation of Southwestern Public Service’s proposed Crossroads-Phantom project, a 150-mile line estimated to cost $410 million.

MOPC also endorsed a NextEra Energy Resources’ motion that Crossroads-Phantom would be a viable alternative to another proposed project line in the same region, the 143-mile, 345-kV double-circuit Crossroads-Hobbs-Roadrunner line. The $395 million project was approved as an alternative by both the Transmission and Economic Studies working groups over its operational flexibility and lower cost to SPS.

Comparisons between the Crossroads-Phantom and Crossroads-Hobbs-Roadrunner projects. | SPP

The votes served as a compromise following a discussion over whether to vote on the two different projects separately or together, and whether to even conduct the vote. That left some members frustrated enough to suggest MOPC should just tell the Board of Directors to decide for it.

“We’re abdicating our responsibility,” Midwest Energy’s Bill Dowling said.

The original proposal received 80% support, while NextEra’s suggestion barely cleared the 67% threshold.

“At the end of the day, NextEra and other want to see steel in the ground,” NextEra’s Matt Pawlowski said.

Jarred Cooley, SPS’ director of strategic planning, called in to the meeting to throw his company’s support behind the Crossroads-Roadrunner option. He said adding a substation at Hobbs gives direct access to reactive reserves for the load pocket and offers voltage support on the pocket’s north and south sides.

“Apples to apples, it has slightly better economics; it’s a slightly cheaper line; and routing the line through the Hobbs substation breaks up an extremely long, 150 mile transmission line that would span pretty much the entire New Mexico territory,” he said. “This will help our area operationally grow as the system continues to grow in that area.”

The Crossroads-Phantom project was originally part of the 2021 Integrated Transmission Planning (ITP) report that was approved in January. However, MOPC pulled the project out of the portfolio when two stakeholder groups said load-projection errors had been discovered late in the planning process. (See SPP Markets and Operations Policy Committee Briefs: Jan. 10-11, 2022.)

Questions to Engineers Require Care

Golden Spread Electric Cooperative’s Natasha Henderson learned the hard way not to ask a group of engineers a question with a literal answer.

Fresh off a Hawaiian vacation that was sandwiched between SPP meetings and focused on the three presentations she was about to deliver to MOPC, Henderson entered the meeting room looking for her seat. She walked up to a group of fellow stakeholders and jokingly asked where she was.

The group was more than happy to help.

“You’re right here!” responded one. “You’re with us!” another said.

Henderson eventually found her seat on her own.

NRDC Becomes SPP’s 113th Member

MOPC welcomed to the table Natural Resources Defense Council’s Christy Walsh, director of federal energy markets, who represented the organization as it became SPP’s 113th member. The RTO eliminated its exit fee for non-transmission owners several years ago, opening the door to environmental groups and other nonprofit organizations. (See FERC Tells SPP to End Exit Fee for Non-TOs.)

Walsh, a FERC staffer for almost 20 years, is only serving until the environmental advocacy group can hire a fulltime staffer to represent it before RTOs.

Changes for Tx Evaluations

MOPC endorsed a revision request (RR452) from the Transmission Working Group that adds a standardized process for evaluating projects proposed by TOs for reasons other than meeting SPP regional criteria or meeting a limited subset of local planning criteria evaluated in the ITP.

The change will allow TOs to perform their own analysis and provide it to staff for review. If SPP performs the studies, TOs must sign an agreement, pay a deposit and cover all study costs.

The more “robust” process also includes the implementation of zonal planning criteria recently approved by FERC. The revision establishes an annual process for each transmission pricing zone to develop a single set of uniform zonal criteria to evaluate zonal reliability upgrades in regional planning. (See FERC Accepts SPP’s 2nd Try at Zonal Planning Criteria.)

Members also unanimously approved a consent agenda included three RRs:

RR484: includes surety bonds as a form of “financial security” within the tariff to secure all types of financial transactions, including transmission congestion rights and virtual energy. Surety bonds can provide a lower cost entry point for creditworthy customers as compared to a letter of credit.

RR489: identifies business practice and ITP manual changes to ensure that transmission service and ITP base reliability models’ dispatch are accounting for the granted amount of interconnection service or surplus interconnection service to multiple resources behind the same point of interconnection. The RR also identifies an ITP base reliability dispatch approach for batteries that have been granted transmission service for charging purposes.

RR496: adds minor and non-substantive missing language, primarily modifying settlements, that are necessary to accurately implement RR449.

The committee also approved four sponsored upgrade studies. SPP reliability assessments found no system impacts on:

NextEra Energy Resources’ upgrade of terminal equipment on two 161-kV lines near Warrensburg, Mo.;

Invenergy’s proposal to build a 345-kV line between two substations in West Texas;

Invenergy’s upgrade of two 345/230-kV transformers in South Dakota to a 581-MVA rating; and

Oklahoma Gas & Electric’s reconductoring of a transmission line to increase their normal and emergency ratings of the lines while replacing aging assets.

WESTMINSTER, Colo. — An ad hoc group of SPP stakeholders and staff addressing crypto miners and other “non-standard” loads told the Strategic Planning Committee last week that the additional demand could aggravate resource adequacy concerns, yet also serve beneficial functions as well.

“If we really put our heads together and work through the process, there’s probably a solution,” said NextEra Energy Resource’s Matt Pawlowski, a member of the self-labeled “non-task force.”

The group has drafted a preliminary report but will let SPP staff assemble a strawman that will be brought back to the SPC in October to identify gaps between the loads and current system processes. Those proposals will likely get farmed out to the Markets and Operations Policy Committee and its working groups.

“This has to be vetted. It’s a huge policy issue,” Golden Spread Electric Cooperative’s Mike Wise said. “These policy implications need to be debated at the SPC.”

SPP defines non-standard loads as very large, potentially interruptible loads such as crypto miners, data centers, biofuel and alternative fuel manufacturers, and cannabis grow houses. The loads can be broken down into firm and non-firm load, some of which will be behind the meter.

Since June 21, the grid operator has received 56 requests from such loads to change delivery points, ranging in size from 3 to 1,300 MW and totaling 7.1 GW.

“More of this is likely coming,” SPP’s chief compliance and administrative officer Michael Desselle said. “If these kinds of loads seeking to locate in low LMP zones concentrate in one particular zone, that only exacerbates resource adequacy concerns.”

Desselle said members have expressed concerns that the loads’ transient nature could leave the RTO with stranded transmission investments.

However, non-standard loads could also provide demand response if controls allow them to respond adequately, the group said in its draft report.

SPC in April created the ad hoc group to advise it on the issues associated with non-standard load wanting to connect to SPP and its members. (See “Ad Hoc Group to Look at Cryptos,” SPP Strategic Planning Committee Briefs: April 13, 2022.)

Energy Storage Group to be Retired

The SPC approved the Energy Storage Resource Steering Committee’s (ESRSC) retirement and the group’s recommendation that multi-use ESR initiatives remain on hold until at least January 2024 and be managed through the normal course of business.

Evergy’s Denise Buffington, who chaired the committee, said 25 of 38 initiatives that the ESRSC was responsible for have been completed. The other 13 have been assigned to primary working groups, with most be to be completed by 2025.

The SPC last year recommended staff and stakeholders continue developing rules that allow ESRs sited as generation resources and as transmission-only assets (SATOA). It also said rulemaking and policy for SATOAs should be completed before finalizing evaluations for multi-use ESRs in what has been labeled a “walk-before-run approach.”

Multi-use ESRs are on hold, pending SATOA implementation and additional production experience.

American Electric Power’s Richard Ross, a critic of task forces, marked the ESRSC’s retirement by presenting one of his coveted Gold Stars of Excellence to Buffington — “With a certificate of authenticity,” he said — for closing down the steering committee.

Counterflow Optimization Work Continues

SPP’s Micha Bailey told the committee that staff’s latest effort to add counterflow optimization (CFO) to the market will continue with a stakeholder workshop this fall to review stakeholder input and best practices from other ISOs and RTOs.

“Some of the stuff they’re doing we actually like,” Bailey said. “We want to bring that back to workshop for stakeholder feedback.”

“Those conversations are really helpful. That’s going to potentially lead to some better practices here,” Pawlowski said, noting that his company operates in every other organized market.

Staff will also share results of the survey it conducted in May of several stakeholder groups on CFO and other congestion-hedging proposals. The workshop will be conducted before the October set of governance meetings.

The Holistic Integrated Tariff Team recommended three years ago that counterflow optimization, limited to excess auction revenue, be added to SPP’s market mechanism that hedges load against congestion charges. The process, which keeps system transmission flows between two points in balance, was meant to address concerns about how congestion rights instruments are awarded and the current process’s efficiency.

Competitive Project Improvements OK’d

The SPC approved five process-improvement recommendations from the task force working to improve SPP’s transmission owner selection process (TOSP) under FERC Order 1000.

The recommendations are:

Requiring addendums to reconciliation invoices to clarify true-up cost calculations and the invoices;

Adopting a cost/cap/guarantee disclosure table to improve their transparency and impacts to quarterly tracking;

Adding a scoring methodology table applicable to all scoring categories and sub-categories;

Preventing the industry expert panel (IEP) scoring competitive bids from awarding additional points for early in-service dates or guarantees; and

Requiring the IEP’s public report be posted no later than 21 calendar days prior to the Board of Directors meeting considering the competitive project’s approval.

The TOSP Task Force has made other process improvements after each of SPP’s competitive project solicitations. The RTO’s board has awarded four competitive projects since 2016, the most recent coming in April when NextEra Energy Transmission won a bid for a $55 million, 345-kV facility in Oklahoma. (See SPP Board of Directors/Markets Committee Briefs: April 26, 2022.)

The task force will draft the tariff revision requests’ language and work to gain the appropriate stakeholder and governance approvals, with the October meetings as a target. It will also continue working on the remaining 11 improvement items.

A group of Connecticut lawmakers urged ISO-NE last week to take action in the wake of the Supreme Court’s June 30 ruling barring the EPA from requiring generation shifting to reduce carbon emissions. (See Supreme Court Rejects EPA Generation Shifting.)

In a letter to CEO Gordon van Welie, the legislators asked ISO-NE to “move more aggressively to adopt market reforms that will increase our reliance on renewable energy sources and establish carbon emission standards for power plants.”

The letter is the latest development in the continuous back and forth between ISO-NE and the New England states over the right approach and appropriate jurisdiction for greening the region’s electricity markets. (See NE States, ISO-NE Start to Wrestle with Next Steps on Pathways.)

The Connecticut lawmakers pointed to work they’ve already done as a state, such as power purchase agreements, and a region, such as the Regional Greenhouse Gas Initiative, but said it’s not enough.

“The Supreme Court’s decision puts the ISOs and RTOs in the driver’s seat when it comes to shifting how this country procures energy,” the letter says. “The time to act is now. And it is our hope that ISO-NE will be our partners in that process.”

The letter was led by House Majority Leader Jason Rojas (D) and Energy and Technology Committee Chair David Arconti (D), with 44 other state representatives signing on.

NYISO on Monday filed a request with FERC for a 90-day extension of the Aug. 16 compliance deadline for Order 2222 and a separate request for clarification or rehearing regarding the order’s requirements for operating reserves (ER21-2460).

In response to NYISO’s original compliance filing, the commission June 17 directed the ISO to make more than 30 tariff revisions related to utility opt-in provisions and interconnection procedures, and to propose an effective date in the fourth quarter. (See FERC Partially Accepts NYISO Order 2222 Compliance.) Issued in September 2020, Order 2222 directed all commission-jurisdictional RTOs and ISOs to revise their tariffs to allow participation of distributed energy resource aggregations in their markets.

“Several of the required tariff modifications are extensive, require significant resources to develop and time to coordinate with the appropriate stakeholders,” the ISO said. It said it must work with New York’s distribution utilities to develop protocols that can be consistently applied by each utility, evaluate the burdens of the proposal against other options and work with stakeholders to resolve any outstanding concerns.

Extending the compliance filing deadline to Nov. 14 would result in rules that are fully compliant with Order 2222, the ISO said.

NYISO initially planned to implement its DER participation model, devised independently by the ISO in 2019, by the fourth quarter. But it “has faced several challenges in developing the databases, workflows and software automation necessary for DER implementation,” it told FERC. “The complexity of the software, combined with staffing resource limitations, has led to significant delays to the 2019 DER project, which impacts the NYISO’s ability to move forward with designing and developing the software necessary for compliance with Order No. 2222.”

Heterogenous Aggregations

NYISO also requested clarification or, in the alternative, rehearing of a specific directive in FERC’s June 17 order that addresses the provision of ancillary services by heterogenous DER aggregations — those consisting of different types of resources.

FERC had said that “so long as some of the DERs in the aggregation can satisfy the relevant requirements to provide certain ancillary services … we find that those DERs should be able to provide those ancillary services through aggregation.” It directed NYISO to file a proposed effective date “by which it will allow DERs in heterogeneous aggregations to provide all of the ancillary services that they are technically capable of providing through aggregation.”

NYISO argued that the directive would require it to incorporate the operation of individual DERs into its real-time commitment and dispatch solution in a manner that is inconsistent with the accepted parts of its DER market design.

That could also compromise reliability, as it would require the ISO’s “real-time commitment and real-time dispatch to solve a host of new constraints” and “could delay the timely posting of real-time dispatch instructions,” it argued.

NYISO said its accepted DER market design does not require it to consider the operational status of each individual DER; instead, it is the aggregator’s responsibility to dispatch its set of DER consistent with the composite offer it submits for the aggregation and the instructions the ISO issues to the aggregation.

VALLEY FORGE, Pa. — PJM’s Operating Committee last week conducted a second first read on RTO and Independent Market Monitor proposals to address the management of remaining run hours for coal and other generating resources limited by fuel shortages or environmental restrictions.

The proposals would change PJM operating procedures for generators in “maximum emergency” status, used to conserve remaining run hours.

Manual 13 currently limits generators on maximum emergency status to a 32-hour remaining run time for steam units, and 16 hours for combustion turbines.

Denise Foster Cronin, representing the East Kentucky Power Cooperative, which owns the coal-fired H.L. Spurlock Station near Maysville and John Sherman Cooper Station near Somerset, said 32 hours is not sufficient. “PJM needs more flexibility than current rules provide,” she said during the meeting Thursday.

The session featured a briefing on the current coal supply shortage on behalf of EKPC and America’s Power. Seth Schwartz of Energy Ventures Analysis showed slides illustrating a 200 million ton drop in coal burn in the U.S. from 2018 to 2020, a reduction of one-third, before rebounding by 65.6 million tons in 2021.

In PJM, coal plant capacity factors dropped from 70% to 33% between 2007 and 2020 before jumping to more than 45% in the first quarter of 2022.

Many coal plants are dispatched after gas combined cycle plants and are run for reliability, Schwartz said.

The uncertainty makes it difficult for coal plants to maintain adequate fuel inventories. Coal suppliers need longer-term contracts to support investments to increase production, Schwartz said, and railroads often require annual contracts with take-or-pay penalties.

PJM’s Chris Pilong said resources in maximum emergency status are not excused from performance assessment intervals.

The RTO proposed allowing coal units only to qualify for maximum emergency with between 32 and 240 remaining run hours. Use of the status would be barred under hot or cold weather alerts, or when conservative operations have been declared. PJM also could deny use of maximum emergency for “any reason,” including potential thermal or voltage violations, black start concerns or extreme weather.

PJM proposed notifications be made via eDart and Markets Gateway with verbal notification to generation dispatch. “Dispatchers are looking at a lot of data,” Pilong explained.

David “Scarp” Scarpignato of Calpine said it could be “overkill” to require the notification in so many different channels, with the risk that one might be missed.

“We don’t want to create a compliance trap,” Pilong said.

Monitoring Analytics’ Joel Luna offered the Independent Market Monitor’s alternative proposal, saying “we don’t want to expand ‘MaxE’ without some consequences.”

The Monitor’s proposal would create a new availability status for “fuel conservation.” That would allow any committed capacity resource with 10 days or less of inventory that does not qualify for the maximum emergency fuel limit (e.g., not beyond the owner’s control, not a temporary interruption, not the result of limited on-site storage) to be made unavailable for economic dispatch.

The catch: Units would forfeit their daily capacity revenues during that status.

Luna said the new availability status is needed because PJM’s proposal doesn’t change the requirement that the maximum emergency status be the result of physical causes.

“The disruption in the coal market, those are not physical events,” Luna said. “Those are decisions plant owners make based on the future. We don’t think it warrants the current definition of MaxE.

“We believe our option is better. … Otherwise we still have the same situation with MaxE being driven by physical events — bridges, barges — not a contractual, procurement decision. This allows both PJM and the market seller to allocate that energy when it’s needed the most,” Luna said.

Becky Robinson of Vistra asked whether units under the IMM’s option would see their equivalent demand forced outage rate (EFORd) reduced for future capacity auctions. “If we’re not doing that, we’re pretending we have more capacity than we do.”

“That’s a really good point, on how to represent these megawatts in the future,” responded Luna.

Tom Hyzinski of GT Power Group said he disagreed with the IMM’s proposed penalties “because there is no failure to meet one’s capacity obligation — one is still subject to CP penalties, and PJM can deny MaxE status and call the unit for reliability at any time.”

Hyzinski said it would be “retroactive ratemaking” to apply the new rules to resources with existing capacity obligations. “If the [Base Residual Auction] has not cleared, and the IMM proposal is in place for that delivery year, then I understand that before I sell the capacity,” he wrote in a WebEx message to other meeting participants.

The committee will be asked to choose between the two proposals at its next meeting.

You young’uns don’t know, but back in the Middle Ages of the 1970s there was a famous commercial for Fram oil filters: You could pay the Fram guy $4 for an oil filter now or pay hundreds for engine repairs later.[1]

Having slightly less pizzazz is the question of how consumers pay for transmission project costs during the pre-construction and construction phases, i.e., before they are completed and placed in service. Consumers can pay a transmission owner’s return (aka cost of capital, aka carrying charge) on such costs on a current basis before and during construction (pay now) or start to pay that return when the project is completed (pay later). The former is often called the “construction work in progress” or CWIP approach, and the latter is often called the “allowance for funds used during construction” or AFUDC approach.[2]

Are you with me so far? Let me give a simple example of the difference. A transmission owner spends $100 million on a project in year 1, and let’s assume an annual return of 9%. Under the CWIP approach the transmission owner charges consumers $9 million in (or shortly after) year 1. Under the AFUDC approach the transmission owners books the $9 million and adds it to the capital cost (aka rate base) of the project, to be charged to consumers starting when the project goes into service (or is abandoned).

When consumers pay that transmission owner return — now or later — is a timing question. There is no obvious answer to which is better for consumers.

Time Value of Money

All else equal, the answer turns on the time value of money — an esoteric concept that compares what someone would take in the future for not having a given sum today. So, for example, if someone would be indifferent to receiving $105 a year from now versus having $100 today, we would say that person has a time value of money with a 5% “discount rate.” In the context we’re considering, the question is whether the consumer would rather pay the transmission owner now or pay a higher amount later.

We can take a shot at estimating this. There’s about $18 trillion in bank accounts averaging 0.1% interest,[3] so that might be a decent estimate of consumers’ discount rate. If someone would accept $100.10 a year from now on his/her $100 today then there’s a really low discount rate.

At the other end of the spectrum are consumers with credit card debt paying 16% interest, implicitly choosing (or having to pay) a 16% discount rate.[4] If they don’t pay the transmission owner that $100 up front, instead paying down credit card debt by that amount, they could save $16 in credit card interest. But there’s around $840 billion in aggregate credit card debt,[5] versus $18 trillion in bank accounts, so there’s a rough ratio of 20-1 for a low discount rate of 0.10% versus a high discount rate of 16%.

I hope I haven’t lost you because we still need to compare consumers’ discount rate with an estimate of what the transmission owner charges consumers for the time value of money. It’s roughly 9% using current allowed returns (weighted average cost of capital including income tax allowance).[6]

Based on the foregoing, the vast bulk of consumers would rather pay now than pay later. For every $100, forego $0.10 now versus pay $9 a year from now. Conceptually most consumers would take $100 from a bank account, foregoing $0.10 in annual interest, in order to pay a transmission owner that would otherwise charge an extra $9 a year later.

Cut to the April NOPR

Now we can cut to FERC’s April Notice of Proposed Rulemaking, which suggests the opposite — that consumers overall would rather pay later. The NOPR says: “… we are concerned that the CWIP Incentive, if made available for Long-Term Regional Transmission Facilities, may shift too much risk to consumers to the benefit of public utility transmission providers in a manner that renders commission-jurisdictional rates unjust and unreasonable.”[7]

There’s no analysis supporting this conclusion — it’s just asserted. As I pointed out above, the transmission owner charges consumers for its return under either approach; it’s just pay me now or pay me later. And most consumers would rather pay now because of their low discount rate, as well as to avoid what the commission has called “rate shock” if the return on large projects is deferred and accumulated until the project goes into service.[8]

Perhaps the NOPR’s focus is on situations when the project is abandoned instead of going into service. The NOPR says: “Should the regional transmission facilities not be placed in service, then ratepayers will have financed the construction of such facilities that were not used and useful, while ultimately receiving no benefits from such facilities.”[9]

There are problems with this focus. First, abandoned project costs are a small percent of total transmission costs because the vast majority of projects are not abandoned and because abandoned projects are abandoned in the pre-construction phase where relatively few dollars have been expended. So, to have abandoned project costs decide the overall CWIP v. AFUDC issue is to have the tail wag the dog.

Second, under commission precedent, consumers generally pay that transmission owner return even for abandoned projects that provide consumers no benefit.[10] The NOPR seems to assume that it would spare consumers from this cost of abandoned projects when the commission’s own rules and precedent are the opposite.

The NOPR doesn’t propose to change the commission’s rules and precedent on this (although Commissioner Mark Christie’s concurrence seems to suggest it does[11]). And the commission seems unlikely to change the rules given the inevitable transmission owner objections that this would discourage the big transmission projects that the commission wants to promote.

And let me add that even if recovery of abandoned project costs were to be disallowed then transmission owners would argue for a higher rate of return because of increased investment risk — another wrinkle on pay me now or pay me later. Consumers seem unlikely to win that tradeoff against transmission owner lawyers and consultants (who consumers pay for[12]). And a risk of disallowance might skew a transmission owner’s incentive against abandoning a project that ought to be abandoned.

Wrapping Up

OK, I’ll wrap this up by saying I would love to be wrong — that somehow consumers would be better with the AFUDC pay-later approach. But that doesn’t seem possible for projects that go into service. And as for abandoned projects, consumers might be better off but only if return on capital were actually denied instead of deferred and billed to consumers later.

P.S. errata note, in my last column on transmission competition the references to $136,070,000 should have said $128,750,000. Import unchanged. I regret the error.

Columnist Steve Huntoon, principal of Energy Counsel LLP, and a former president of the Energy Bar Association, has been practicing energy law for more than 30 years.

[2] These terms can be confusing. Sometimes the return/carrying charge amount is referred to as AFUDC, which is added to the CWIP balance. Also I should note that generally under both the AFUDC and CWIP approaches, the amount in question is return on capital, not return of capital. In both approaches the capital costs of construction are treated the same – recovery from consumers is deferred until the project goes into service (or is abandoned).

[6] For illustrative purposes take last year’s settlement of a rate complaint against PPL Electric Utilities, a PJM transmission owner, with an allowed common equity return of 10.4% and allowed equity/debt ratio of 56%/44%, https://elibrary.ferc.gov/eLibrary/filedownload?fileid=F83FB3CC-1092-CA7D-87C8-7B6442400000. Grossing up the equity return for a 21% federal income tax rate yields a pretax equity return of 13.2%. Applying the equity/debt proportions to that equity return and to a long-term debt cost of 3.6% from data in PPL’s Form 1 yields a weighted average cost of capital of 9.0%. Your mileage may vary.

[7]Building for the Future Through Electric Regional Transmission Planning and Cost Allocation and Generator Interconnection, Notice of Proposed Rulemaking, 179 FERC ¶ 61,028 (April 21, 2022) (“NOPR”), at P 332.

[8]Potomac-Appalachian Transmission Highline, L.L.C., 122 FERC ¶ 61,188, at P 42 (2008).

[10] Order No. 679, 116 FERC ¶ 61,057 at P 163 (2006); MidAmerican Central California Transco, LLC, 168 FERC ¶ 61,197 at P 3 (2019); GridLiance West Transco LLC, 164 FERC ¶ 61,049, at P 19-20 (2018); Potomac-Appalachian Transmission Highline, L.L.C., Opinion No. 554, 158 FERC ¶ 61,050, at P 5, fn. 10 (2017) (“PATH”); Xcel Energy Services, Inc., 121 FERC ¶ 61,284 at P 62 (2007).

[11] Commissioner Christie concurring, at P 5 and 15. If the Commission actually intends what Commissioner Christie suggests it does, then a Final Rule should make that clear.

Rule on Variable Environmental Costs and Credits Advances

VALLEY FORGE , Pa. — The PJM Market Implementation Committee last week approved a joint RTO-Independent Market Monitor proposal to update rules governing variable environmental charges and credits and their inclusion in cost-based energy offers.

Under the proposal, generation units receiving the production tax credit (PTC) or renewable energy credits (RECs) would have to reflect them in their fuel-cost policies (FCP) when submitting non-zero cost-based offers in the energy market.

The package includes changes to Manual 15 and Schedule 2 of the Operating Agreement. Under the changes, the review of emissions rates would be reduced from annual to every three years to align with the FCP review process. Emissions rates should not change drastically year to year, said PJM’s Melissa Pilong. The market seller is responsible for updating rates to ensure their accuracy.

The new rules would also add transparency on the information required from market sellers.

The IMM’s Joel Luna told the committee that RECs and PTCs must be included in cost-based offers under the same standards as fuel costs, and must be “accurate, verifiable and systematic.”

“In plain terms, it cannot be made up,” Luna said.

RECs can be based on the actual transaction price (inventory cost or contract-based) or spot price (replacement cost). If the actual price is used, the FCP must say how often the price will be updated and the period for the price (e.g., last year). If a spot price is chosen, the FCP must identify the source (e.g., broker/publication), data point used (e.g., midpoint/settled) and update frequency (e.g., weekly).

Units with bundled power purchase agreements making non-zero cost offers can use the actual REC price or spot REC price.

PTC rates are defined by the Internal Revenue Service and grossed up based on the effective corporate tax rate. For a company with a 21% tax rate, the $27/MWh PTC converts to $34.18/MWh ($27/(1-0.21)).

Jeff Whitehead of GT Power Group questioned why the RTO is including out-of-market revenue, saying it’s at odds with the effective elimination of the minimum offer price rule.

“We have a couple of ‘no’ votes [because of] the policy implications,” he said. “We’re wondering if we’re going the wrong direction with this policy.”

“Having the net cost reflects the true marginal cost of the units,” said Luna. Without such considerations, “you’ll be sending [solar and wind generators] a signal to curtail, and they will not respond.”

The proposal passed 180-39 (82%) with five abstentions. Stakeholders said they preferred the new rule over the status quo by 178-32, with 21 abstentions. It will receive a first read at this week’s Markets and Reliability Committee meeting.

Market Suspension Rules OK’d

Members also approved a revised PJM/IMM package of changes to the treatment of long-term market suspensions.

The changes are intended to address a gap in tariff language regarding how to settle the real-time market if prices can’t be determined. They would set separate rules for suspensions of less than and more than 24 hours.

Under a compromise, the intermediate suspension category was eliminated, and the “short term” suspension was expanded to 24 hours from six.

The changes apply to the real-time market when dispatch is unable to provide zonal economic dispatch results for at least seven five-minute intervals within a market hour. For suspensions up to 24 hours, PJM would substitute the missing prices with the average real-time price of those from the preceding and subsequent hours.

Suspensions longer than 24 hours would use day-ahead prices, if available. If not available, energy LMPs would be priced hourly based on an aggregate supply curve from available offers (including available resources not running), with actual generation megawatts serving as the proxy for demand. Loss LMPs and congestion LMPs would be set to $0.

The change included a friendly amendment by Shell Energy’s Sean Chang that stated if the suspension is greater than six hours but less than 24 hours, PJM would use day-ahead prices for corresponding hours.

The changes do not affect suspensions of the day-ahead market, which will continue to use real-time prices as defined in tariff section 1.10.8(d).

Tom Hyzinsky of GT Power Group expressed concern with the changes, saying “day-ahead and real-time can be two completely different markets.”

PJM’s Tim Horger said 90 to 95% of load clears in the day-ahead market. “That’s why I feel confident using it for six to 24 hours.”

The changes were approved by acclimation with no objections or abstentions.

Initiative Approved on Weather-sensitive Load Compliance Rules

Members approved an issue charge proposed by Sharon Midgley, of Exelon (NASDAQ:EXC) and subsidiary Baltimore Gas and Electric (BGE), to explore an alternative demand response/price-responsive demand (PRD) compliance construct for weather-sensitive load, such as residential demand impacted by summer air conditioning.

Midgley said the current rules compare metered load under prevailing weather conditions to the peak load contribution (PLC) based on weather-normalized peak weather conditions. Capacity compliance for DR and PRD is currently based on the firm service level (FSL), calculated as the PLC minus the amount of installed capacity that the DR/PRD resource cleared in the capacity auction. Compliance is achieved if metered load is at or below the FSL.

Over the summers of 2018-2021, the actual peak load for BGE’s weather-sensitive residential customers averaged 13% higher than the weather-normalized peak load. The disparity was the largest in 2019, with weather-normalized load 22% lower than actual load.

The discrepancy means DR and PRD providers may not be able to offer the full capability of their programs into the capacity market because of unachievable FSL, Midgley said.

Midgley revised the issue charge to make out-of-scope changes to the current compliance construct’s ruleset, which caps monetization to the customer’s PLC.

Monitor Joe Bowring opposed addressing the issue separately from ongoing discussions at the Resource Adequacy Senior Task Force. “We don’t think this is a narrow issue, and we don’t think it should be carved out from the RASTF,” he said.

Midgley said the RASTF’s work plan didn’t envision “getting to that level of detail.”

“I don’t see this as asking for special treatment,” she added.

The issue charge was approved with one objection for 22 members.

First Read on Day-ahead Zonal Load Bus Distribution Factors

PJM’s Amanda Martin gave a first read of a problem statement and issue charge addressing day-ahead zonal load bus distribution factors.

This example shows the July 14 DA nodal load (left scale) is consistently 13% of the zonal load (right scale), while the July 7 RT load is only 6% of the zonal load. | PJM

The RTO’s current rules state that the default distribution of load buses for a zone in the day-ahead energy market is the state estimator distribution of load for that zone at 8 a.m. one week prior to the operating day. That means the share of the zonal load attributed to each node remains constant for all 24 hours, even though the node’s share of total load may vary throughout the day because of nonconforming loads, such as behind-the-meter solar and data centers. This can cause a mismatch between the day-ahead nodal loads and real-time state-estimated load.

“This seems overly simplistic given the data we have,” said consultant Roy Shanker. “I’m surprised we’re doing it this way.”

The committee will be asked to approve the issue charge at its next meeting under the “CBIR Lite” (Consensus Based Issue Resolution) process. The work is expected to take four months, with changes to tariff section 31.7c(i) and updates to Manual 11 and Manual 28.

IMM Balks at New Capacity Options for Generation with Co-located Load

Bowring expressed concern over proposals to change how PJM treats capacity offers from generation with co-located load.

According to the problem statement proposed by Brookfield Renewable Trading and Marketing and Constellation Energy — and approved by stakeholders in January — PJM’s current rules do not allow capacity offers for the full output of generating units that are contracted to physically serve co-located loads, instead requiring owners to retire a portion of their capacity to serve such loads.

The companies said large commercial customers with fast-response curtailment capability (less than 10 minutes) are seeking physical supply options for loads that are directly interconnected behind carbon-free generation resources such as hydro and nuclear.

Changing the rules would provide customers more options and give PJM the ability to call on the generators serving such interruptible customers, backers say. The initiative could result in modifications to capacity market rules, cost-based offer rules and relevant manual provisions to account for co-located load configurations.

“We have lots of large loads that can drop at any time on the system,” said Shanker. “Operationally, I don’t think this is anything new.” He added, however, that the magnitude could be increasing.

But Bowring said the proposal is a “significant change” that removes, rather than adds, flexibility. He said it could mean that a large nuclear power plant will no longer provide its energy to PJM in most hours but will be paid as if it is a capacity resource.

Discussing the impact of an unexpected drop in the behind-the-generator load, he said, “It’s not just a load drop. It’s a sudden increase in generation. … Everyone needs more details about this to be convinced it’s business as usual.”

He also said the impact of the proposed change on the provision of reactive power and frequency control by the generator must be explicitly defined.

Constellation Energy’s Jason Barker asked Bowring to be specific about the analysis he seeks, saying he wanted to avoid his request from “unduly delay[ing] consideration of this process.”

“The process has worked in the past to adjust interconnection service agreements,” Barker said.

PJM’s Jeff Bastian said the RTO currently operates the system prepared for the loss of its largest units. “If you lose a 300-MW load behind the meter of a generator, the system is going to react the same as if you lose a 300-MW paper mill or any other kind of load that’s connected to the system. So I’m not sure I understand the concern,” he said.

PJM’s Lisa Morelli said she will continue discussions outside of the MIC “to make sure we’re not talking past each other.”

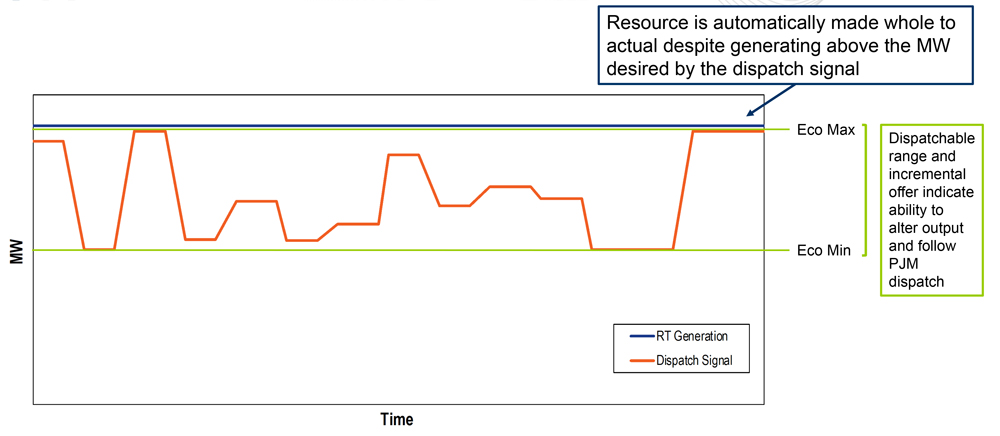

CT Make-whole Loophole Discussed

Members discussed a proposal to close a loophole that allows combustion turbines to ignore PJM dispatch without financial consequences.

Under PJM rules, most resources are made whole to the lesser of their actual megawatt output or the RTO’s desired output. But CTs are always made whole to their actual megawatts, regardless of how well they follow dispatch, Morelli explained.

The distance between the orange (dispatch) line and blue (actual operation) line represents excess MWs for which the combustion turbine can receive make-whole payments under current PJM rules. | PJM

PJM and the Monitor said the special treatment made sense before the implementation of Capacity Performance, when CTs were not required to have a dispatchable range. Most CTs now share similar dispatchability to the rest of the fleet, they said.

Flexible CTs received 72% of all balancing operating reserve credits in 2021, “so changes to this rule can be quite meaningful,” said Morelli.

PJM reran the highest uplift days for CTs from summer 2021 and found that with the CT exception eliminated, uplift payments to CTs would drop from $13.4 million to $12.2 million over the eight days — a reduction of $1.3 million (10%).

“$1.3 million for eight days is pretty significant, so that would grow over a whole year,” Morelli said. “I think it does make a strong case for removing the CT rule.”

She called the change “low-hanging fruit,” although she acknowledged, “we realize some CTs are not flexible.”

Timing of ARR/FTR Market Task Force Talks at Issue

PJM backed off from a recommendation to delay additional work on new seasonal auction revenue rights (ARRs) and financial transmission rights (FTR) products in the face of opposition by DC Energy.

In a poll of 129 members of the ARR/FTR Market Task Force, 98% answered “yes” to the question: “Should the annual ARR/FTR products be retained and seasonal products be added (recognizing that fewer rounds would be required)?”

Almost two-thirds (64%) of those polled also supported “pursuing any other ARR/FTR market reforms at this time.”

A much smaller majority (57%) supported retention of the annual ARR/FTR products. “So no real conclusory evidence there on where people want us to go,” said task force facilitator Dave Anders.

Asked what process changes the task force should pursue to simplify auctions to allow additional products, 60% favored adjusting the structure of the annual auction (e.g., number of rounds), and 83% supported modifications to overlapping periods and/or class types.

In contrast, “adjustments to the annual ARR allocation process” drew only 26% support.

After reviewing the poll results, Anders recommended that the task force delay discussions on new products until late 2023 or early 2024 to allow the September 2022 Phase I (new FTR product type) and February 2023 Phase II (ARR changes) be implemented first. Those changes were approved by FERC on March 11 (ER22-797).

“Let’s make sure we’ve got some stability before we make additional changes,” he said.

Anders also proposed revising the task force’s issue charge to “narrow the focus down to, what do we want to accomplish going forward?”

“The issue charge was exceptionally wide open,” said Anders. “Being able to say the task force is done is an important thing.”

“Where did this recommendation come from?” asked Bruce Bleiweis of DC Energy. “It wasn’t discussed.”

“As facilitator of the task force, this is my recommendation,” responded Anders.

Bleiweis said he agreed with revising the charter, but he said he would oppose waiting “another year and a half to begin those discussions.”

“I don’t think we need to wait for the implementation of the new products and class types, because they’re different from what we’re recommending” he said.

“This is just my recommendation,” Anders responded. “We’ll go whatever direction the stakeholders want to go.”

Anders said he would return to the group with “a more definitive path forward.”

Separately, the MIC endorsed changes to Manual 6: Financial Transmission Rights as part of the periodic review and to make changes conforming with FERC’s March order. The changes include definitions of new FTR class types and clarification of the remaining time frame for existing off-peak classes. Also added was a new rule on the minimum price for clearing options. The first of the changes will be effective Sept. 1 and be applied first to the October 2022 auction, which opens in mid-September.

Wolf’s Appeal Reinstates RGGI Costs in Pa. — for Now

On July 11, Pennsylvania Gov. Tom Wolf’s administration appealed the Commonwealth Court’s injunction blocking the state from entering the Regional Greenhouse Gas Initiative (RGGI), effectively lifting the injunction. (See Court Blocks Pa. from Joining RGGI.)

“As a result, generators can include RGGI costs in their cost‐based offers per their approved fuel-cost policies beginning on July 13 for July 14, unless and until the injunction is reinstated, if it is,” the Monitor advised in a notice.

Manual Revisions Approved

Members also endorsed revisions to:

Manual 18: PJM Capacity Market to conform with FERC’s July 12 order regarding hybrid resources (ER22-1420). A hybrid is defined as a single generator plus a single storage facility operating as a composite. The change adds hybrid resources to the exemption from the capacity market must-offer rule currently applied to intermittent resources and capacity storage resources.

Manual 28: Operating Agreement Accounting to support the start-up cost offer development proposal the MRC approved in May. It clarifies what intervals are included in segments for determination of balancing operating reserve credits.