South Korea’s SK On, Ford to End U.S. Battery Joint Venture

South Korean battery maker SK On has ended its joint venture with Ford Motor for their battery factories in the U.S. as part of a business overhaul to focus on other growth areas.

SK On, a subsidiary of SK Innovation that supplies automakers including Hyundai Motor and Kia, said a Ford subsidiary will take full ownership of the battery plants in Kentucky, while SK On will assume full ownership and operate the Tennessee plant. In 2022, the companies invested $11.4 billion to build the plants.

Fervo Nabs $462M to Complete Next-gen Geothermal Project

Fervo Energy has raised an additional $462 million to build the next generation of geothermal power plants in the U.S.

The company announced it has closed a Series E funding round led by a new investor, B Capital, a global venture capital firm started by Facebook cofounder Eduardo Saverin. With the latest announcement, Fervo says it has raised about $1.5 billion overall since 2017 as it develops what could become the world’s largest “enhanced geothermal system” in Utah.

EPA Planning to Delay Enforcing Biden Vehicle Pollution Rule

The EPA plans to delay enforcement of a Biden-era regulation requiring significant cuts in air pollution from vehicles, according to a senior agency official.

In April 2024, the EPA finalized a rule requiring significant reductions in “criteria pollutants” emitted from passenger and commercial vehicles from the 2027 through 2032 model years. As part of a planned delay, the EPA is considering keeping the 2026 standard in place for two more years to give the agency time to reconsider the Biden-era standards and how the agency sets standards, the official added.

EPA Administrator Lee Zeldin in March announced the plan to reconsider the 2024 rules that would cut passenger vehicle fleetwide tailpipe emissions by nearly 50% by 2032 compared with 2027 projected levels.

The U.S. solar industry installed 11.7 GW of new solar capacity in the third quarter, a jump of 49%, according to a study by the Solar Energy Industries Association and Wood Mackenzie. The report said solar accounted for 58% of all new electricity-generating capacity added to the grid through the third quarter, with more than 30 GW installed.

Since the start of 2025, nearly 2,000 power projects, or 266 GW of new capacity, have been canceled in the U.S., according to data from clean energy analytics platform Cleanview. The overwhelming majority of those were clean energy projects, with utility-scale solar accounting for 86 GW, energy storage 79 GW and wind 54 GW.

ReliabilityFirst expects “normal risk” for the upcoming winter season thanks to positive developments across its territory, one of the regional entity’s engineers assured listeners during a webinar hosted by the organization.

Tim Fryfogle, RF’s principal engineer for resources, engineering and system performance, joined the Dec. 15 webinar to discuss the results of RF’s Winter Reliability Assessment, which the RE released Dec. 10 as a companion to NERC’sWRA.

The assessment is intended to provide a closer look at reliability risks in the RF footprint during the winter months of December through February, based on data from PJM and MISO; parts of both RTOs are in the RE’s service area.

NERC’s WRA found “pockets of elevated risk” across North America, indicating a “potential for insufficient operating reserves in above-normal conditions.”

However, the WRA left PJM and MISO out of this group, assessing both areas under the “normal” classification. This means they possessed sufficient generating capacity to meet demand under both the ERO’s 50/50 load forecast, which denotes a 50% chance the actual load will be higher or lower than predicted, and the 90/10 forecast, meaning a 10% chance that the actual load is higher than predicted. (See NERC Winter Reliability Assessment Finds Many Regions Facing Elevated Risk.)

Fryfogle observed that RF’s assessment came to the same conclusion, despite using different analyses. Both assessments use the same data drawn from NERC’s Generating Availability Data System, which collects performance information from conventional, wind and solar plants.

The difference, Fryfogle said, is that RF’s analysis is based on historical GADS data covering December through February over a rolling five-year period, while NERC uses the average forced outages for weekdays in the same months over the past three years. Fryfogle did not describe either approach as superior but said the fact they reached similar conclusions is “a great way to provide some verification and validation with regards to the end result.”

Fryfogle observed that the assessment of MISO and PJM represents a significant change from last winter, when NERC’s WRA found both MISO and PJM faced elevated risk during extreme weather scenarios. He cited several reasons for the shift.

First, he pointed out that the 2024/25 winter risk determination factored in the impact of litigation over the Transco Regional Energy Access gas pipeline and potential constraints on its use. FERC’s reinstatement of the pipeline’s certification allowed the risk to be downgraded, Fryfogle said. Second, since last year’s assessment MISO has implemented a seasonal resource adequacy construct and unit accreditation, allowing the region to better assess resource availability.

The changes mean PJM has a less than 1% chance of being unable to serve load even in the 90/10 scenario, Fryfogle said, while MISO’s likelihood of being unable to serve its load under the same conditions is about 3%. However, he urged listeners to remain cautious because severe weather could develop quickly. He suggested utilities make use of resources such as RF’s winterization assistance visits. (See RF Presenter Plugs Winterization Assist Visits.)

“We have a great team that … will help you pinpoint any issues … but please continue to do your due diligence [and] please share best practices,” Fryfogle said. “We are continuously getting better, but that’s because of outreach, everyone sharing great ideas and thoughts on how to weather these cold winter storms.”

Texas regulators have approved two more applications under the Texas Energy Fund’s completion-bonus program, making the generation resources eligible for more than $100 million in grants.

During its Dec. 12 open meeting, the Public Utility Commission sided with staff’s recommendation to issue eligibility notices to Calpine and NRG Energy for their projects that add 916 MW of dispatchable gas-fired capacity to the ERCOT grid. The companies can execute grant agreements with the PUC upon the generation’s “timely and successful” interconnection (57937).

Both projects already have been awarded 20-year loans at 3% interest under the fund’s In-ERCOT Generation Loan Program and are expected to come online before summer 2026.

Calpine, which was granted a $278.3 million loan in October, now is eligible for $55.2 million in performance-dependent TEF funds over a 10-year period for its 460-MW Pin Oak Creek peaker. NRG could receive as much as $54.7 million in grants for two gas turbines, totaling 456 MW, at its TH Wharton plant. The units were awarded a 20-year loan of up to $216 million in August. (See NRG Energy Secures $216M Loan from TEF.)

The Completion Bonus Program is one of four under the fund. Applications must meet a set of nine criteria that include market participation and whether they provide dispatchable energy or are a non-storage facility.

The commission also approved staff’s recommendation to extend timelines for the first disbursement of loans to seven applicants in the In-ERCOT program (56896). Under a recently enacted state law, the first loan payments were due to be disbursed before January.

Staff said each loan applicant had multiple market factors outside their control and had taken “reasonable steps to mitigate the delays caused by these factors.” They cited global demand for transformers and turbines, cost and availability of contractors, construction and permitting delays, and economic constraints.

“A confluence of market forces … make it unlikely that the commission could timely enter into a loan agreement with the applicants,” PUC staffer Susan Nance told commissioners.

With the extensions, the PUC now faces deadlines of June 30, July 31, Sept. 30 and Dec. 31 in 2026 to disburse the first loan payments. Together, the applicants’ 10 projects amount to 4,063 MW in nameplate capacity.

Entergy 500-kV Line Approved

The PUC approved an administrative law judge’s decision allowing Entergy Texas to build a 500-kV, 41-mile single-circuit transmission line in Southeast Texas (58136).

Entergy said the Cypress-Legend project is necessary to address load growth from new and expanded industrial facilities and an increase in residential and commercial demand in Texas’ Golden Triangle. The region’s load is expected to grow by about 40% in the next five years.

MISO identified Entergy’s proposal as a baseline reliability project. It has an estimated cost of $398.7 million.

However, PUC Chair Thomas Gleeson moved to grant the rehearing for the “limited purpose” of including additional findings and explanation. He said the chosen route “best meets the transmission line routing factors the commission must consider.”

The Western Transmission Expansion Coalition plans to publish its 10-year outlook for Western transmission needs in February 2026 and has begun outlining the 20-year plan, according to Energy Strategies, which is developing the report.

The WestTEC effort, jointly facilitated by the Western Power Pool (WPP) and WECC, will address long-term interregional transmission needs across the Western Interconnection. The goal is to produce transmission portfolios for 10- and 20-year planning horizons. (See WestTEC Tx Study on Track Despite Delays.)

The 10-year outlook is slated for release in February 2026, pending approval from the WestTEC Steering Committee, said John Muhs, senior consultant with Energy Strategies, during a WestTEC Regional Engagement Committee meeting Dec. 11.

The 10-year report will include a six-page summary, a 20-page report and technical appendices with supplemental data and methodology, according to presentation slides.

“The study work itself is largely done pending approval,” Muhs said. “But the 20-year is further behind — it’s earlier on in the study process.”

The goal for the 20-year plan is to have a report in front of the WestTEC Steering Committee by September 2026, Muhs said.

The consulting firm has begun developing the 20-year reference case nodal models and hypothesis map. Energy Strategies is using the 10-year models as a starting point to develop the production cost model and system reliability assessment, according to the slides.

Energy and Environmental Economics (E3) will provide data on expected electricity demand by 2045, which Energy Strategies will use to develop area-level load profiles for the 20-year reference case with feedback from the WestTEC Assessment and Technical Taskforce (WATT).

Based on data from E3 and the 10-year outlook, Energy Strategies is mapping out how the transmission system could look in 20 years, according to the slides.

The main objective of WestTEC is to create an “actionable” transmission study by conducting integrated planning analysis across the Western Interconnection.

The study horizons focus on evaluating transmission requirements in 2035 and 2045, with the goal of prioritizing “flexible and scalable transmission solutions for nearer-term needs to help better position the system for efficient long-run expansion,” the study plan reads.

The effort has support from stakeholders across the Western region. For example, WATT members include representatives from the Bonneville Power Administration, Western Area Power Administration, Powerex, Northwest Power and Conservation Council, and more.

In June, CAISO cited WestTEC as one of the factors influencing its interregional transmission planning, saying it will use the information to help identify opportunities it will emphasize, either by itself or in collaboration with other entities. (See Inland Wind, WestTEC to Guide CAISO Interregional Planning.)

Energy Strategies will present “a much more finalized version and set of results” of the 20-year outlook during WPP’s all-committee meeting in January, Muhs said.

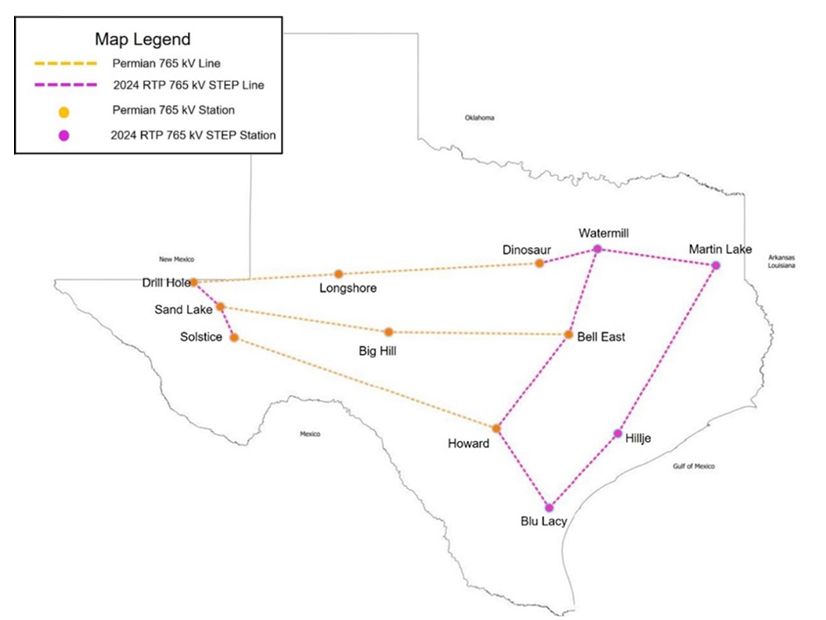

ERCOT’s Board of Directors has approved staff’s proposed 765-kV Eastern Backbone project and its $9.4 billion capital cost price tag, making it the most expensive project in the grid operator’s history.

The 1,100-mile project, a subset of the 2024 765-kV Strategic Transmission Expansion Plan (STEP), will address Texas’ significant load growth and reliability needs, ERCOT said. Much of that demand is driven by more than 233 GW of interconnection requests by data centers, cryptocurrency miners and other large loads, and the electrification of the state’s oil and gas industry.

“We see the need for this infrastructure to be able to reliably serve the future demand on the system,” Kristi Hobbs, vice president of system planning and weatherization, told the board during its Dec. 8-9 meeting.

Incumbent transmission providers American Electric Power — an industry leader in building and operating 765-kV lines since the 1960s — CenterPoint Energy, CPS Energy and Oncor will build the project’s seven segments of extra-high-voltage transmission lines, four 765-kV substations, 11 765/345-kV transformers, and 69 765- or 345-kV circuit breakers.

Hobbs said recent transmission plans have indicated a need to incorporate 765-kV facilities in meeting staggering demand increases.

“We realized we cannot keep planning the system the way we always had,” she said.

The new approach won’t come cheaply. ERCOT’s 2024 345-kV Regional Transmission Plan and the 765-kV STEP both expect about $5 billion per year of investment over a six-year planning horizon. Staff say a 765-kV network will enable power to flow more efficiently through long-distance transmission to urban load centers.

Hobbs and Thomas Gleeson, chair of the Texas Public Utility Commission, assured questioning board members that their respective staffs have a firm grip on escalating costs. ERCOT used a 20% adder for mileage estimates to account for right-of-way issues, Hobbs said.

Gleeson told the board he joined the PUC as staff during the Competitive Renewable Energy Zone process, which was completed in 2014 at a cost of $6.9 billion, $2 billion over projections. However, the project resulted in 3,600 miles of 345-kV CREZ lines that freed up over 23 GW of wind capacity in West Texas.

ERCOT’s Eastern Backbone project and EHV paths into the Permian Basin | ERCOT

“I’m very aware of the public’s desire to know cost overruns if the schedule slips,” he said. “I think it’s important, given the magnitude of this and the cost, that we are transparent about any cost overruns and slips in schedules. We will do everything we can at the commission to make sure that that information is public so that everyone from the governor to the legislature to the public at large knows what’s going on with this project.”

The board approved two other transmission projects with a combined cost of $852.8 million, pushing the total estimated value of endorsed infrastructure to $10.3 billion:

Oncor and AEP’s proposed 104-mile, single-circuit 765-kV project in West Texas that closes the western end of ERCOT’s EHV backbone. The Drill Hole-Solstice project has a projected capital price tag of $742.2 million.

Oncor upgrades to a 345/138-kV switch and 9 miles of 138-kV line, and 13 new miles of 345-kV lines in far West Texas. The project has an estimated capital cost of $110.6 million and completion date in December 2026.

All three projects will require construction permits from the PUC.

Vegas Sets Lofty Goal

CEO Pablo Vegas told the board that ERCOT has updated its vision, mission and core values that see the grid operator as the “most reliable and innovative grid in the world.”

“Not just in Texas, not just in the United States, but in the world,” he said. “We are one [of the best], if not the leading, grids globally when it comes to operational and technical complexities. To be successful, we need to be a clear leader on a stage that represents the entirety of this planet.”

The vision builds on the ERCOT 4.0 construct that Vegas unveiled earlier in 2025. At the time, he said ERCOT 4.0 was a “strategic lens to look at the priorities and the initiatives that we’re going to be investing in to make sure that we continue to deliver on our mission, which is getting more complex and more dynamic every year.” (See ERCOT Board of Directors Briefs: June 23-24, 2025.)

“It represents a transition in our market that is characterized by high and very rapid growth of intermittent and short-duration supply resources,” Vegas told the board Dec. 9. “It’s characterized by a rapidly changing customer base that includes price-responsive loads like cryptominers, rapidly growing large-scale data centers and continued penetration of distributed energy resources. … It represents an opportunity to create a more resilient and cost-effective grid.

“To achieve this vision, we will ensure a reliable grid with competitive and cost-effective electricity markets,” he added.

NPRR1309 and its associated Nodal Operating Guide revision (NOGRR283) address stakeholder feedback that DRRS procurements be co-optimized with obtaining energy and other ancillary services. The protocol change is the third iteration of DRRS’ design, which began development in 2023 as a subset on non-spinning reserve service. The PUC has set DRRS as a key commission priority.

In designating DRRS as a board priority, the directors also ordered TAC to bring the measures, structured to meet statutory requirements, to the June board meeting for consideration.

ERCOT has withdrawn NPRR1235, which would have developed DRRS as a standalone ancillary service.

The IBR measures granted priority status were NPRR1308 and its associated change to the Nodal Operating Guide, NOGRR282.

NPRR 1308 defines a large electronic load (LEL) as exceeding 75 MW, in which 50% or more of the site’s demand is computational load from a data center or cryptomining facility. NOGRR282 establishes frequency and voltage ride-through requirements for LELs.

Staff said the inability of LELs to ride through disturbances on the grid poses a growing reliability risk for ERCOT. They have identified 26 LEL ride-through events since the beginning of 2023. ERCOT says it is determining whether additional ride-through requirements are needed for other large loads.

ERCOT says the draft’s release will help improve the final product’s quality and strengthen the transparency of the data and associated processing steps. Staff have added additional scenarios that look at the effects of assumptions based off new rules for large-load curtailment and projects approved for Texas Energy Fund loans.

“Getting input from the stakeholders throughout the process has been beneficial,” Hobbs said.

The CDR gives a five-year look ahead at generation that has met certain requirements for connecting to the grid in the future. It also includes forecast demand received from utilities.

The report predicts a summer peak load hour of 138 GW and a net peak load hour of 126 GW in 2030. (Net peak load subtracts renewable energy generation.) It also forecasts 60 GW of additional generation by the summer of 2030, with solar and storage accounting for 86% (52.3 GW) of that total.

Real-time Price Correction

The board approved another real-time market price correction with more than $812,000 in impact, representing almost 4% of settlements for the Oct. 14 operating day.

Staff said a software issue led to an “inappropriate” effect on generation dispatch values. The issue was not discovered within the two-business-day deadline, meeting the criteria for a board-approved correction. ERCOT said the software bug’s cause has been identified and a fix deployed.

The board also rubber-stamped three staff recommendations to approve requests from market participants:

BHER Power Resources’ bid for a permanent site-specific exemption from complying with metering protocols by placing it on the combination ballot. The company said its Falcon Seaboard facility in Big Spring was built in such a way that it can’t meet a 500-kW maximum load limit requirement for auxiliary distribution factors. The facility has operated for 35 years.

Lamar Electric Cooperative’s request to transfer about 60 MW of peak load from the Rayburn Country Electric Cooperative load zone to the competitive North LZ. The transfer will go into effect January 2030.

The committee will welcome three new members, including AEP’s Erin Rasmussen, who replaces long-time TAC member Richard Ross. The other new members are CenterPoint Energy’s Ebby John and Garland Power & Light’s Curtis Campo.

The directors also approved 11 NPRRs, two NOGRRs, a Planning Guide revision (PGRR) and a system change request (SCR):

NPRR1263: remove the accuracy testing requirements for coupling capacitor voltage transformers.

NPRR1274: update the estimated capital cost for the tier-classification rules used in the Regional Planning Group (RPG).

NPRR1280: establish an RPG review process for proposals to permanently bypass an existing series capacitor or un-bypass a series capacitor previously designated as permanently bypassed.

NPRR1285: expand the current reliability unit commitment opt-out window to incent self-commitment, increasing capacity available to the market at lower expense and reducing RUCs and associated costs.

NPRR1287: replace the defined term “Maximum Daily Resource Planned Outage Capacity” with “Resource Planned Outage Limit” (RPOL) to align with the actual calculated RPOL; add the maximum duration of a proposed transmission outage with a described lead time to align with current outage-coordination practices; define conditions under which ERCOT can accept an outage request if it could exceed the planned outage limit; and clarify that energy storage resources submit outages.

NPRR1293: clarify the “Update Network Operations Model Production Environment’s” milestone dates.

NPRR1294: incorporate the other binding document “Demand Response Data Definitions and Technical Specifications” into the protocols, standardizing the approval process.

NPRR1298: require comments on proposed rule changes to be delivered to ERCOT within 14 days of the revision request’s posting. Comments posted after the 14-day comment period can be considered at the Protocol Revision Subcommittee’s discretion.

NPRR1299: clarify and clean up language related to the emergency response service program, including a data file produced at the end of the procurement process using code managed entirely within ERCOT’s Demand Integration group. The file is manually produced and must be posted manually, which is affected by weekends and holidays.

NPRR1300: implement Senate Bill 1877 by including the Texas Office of Public Utility Counsel as an entity permitted to receive protected information or ERCOT critical energy infrastructure information without violating the protocols.

NPRR1303: revise language to change the method for submitting and receiving declaration of natural gas pipeline coordination from a physical form to an electronic format.

NOGRR279: modify the monitoring equipment installation deadlines established by NOGRR255 (High Resolution Data Requirements) to Jan. 1, 2029, consistent with NERC standard PRC-028-01 (Disturbance Monitoring and Reporting Requirements for Inverter-Based Resources), and clarify that synchronized resources with standard generation interconnection agreements executed prior to July 25, 2024, have 12 months after their commercial operations date to comply with the new equipment standards.

NOGRR280: remove language governing communication path requirements for CREZ circuits and stations.

PGRR131: implement mandatory reporting requirements for transmission service providers’ and ERCOT’s interconnection-cost reporting, and delete gray-box language superseded by the requirements.

SCR831: modify the network model management system, operational data management system, topology processor and the modeling-on-demand system to incorporate short-circuit modeling data for maintaining models built by the System Protection Working Group.

When the Western Area Power Administration decided to reconductor a transmission line in North Dakota, it made “perfect sense on paper,” according to WAPA’s former CEO.

But the switch from a 230-kV line to a 345-kV line equipped with the latest technology had cascading impacts, Mark Gabriel told the Colorado Public Utilities Commission on Dec. 11.

“The reality was a number of the downstream small co-ops and municipal entities were negatively impacted, because it required changing out transformers, changing out reclosers and reconfiguring the system moving down,” said Gabriel, who now is CEO of Colorado electric cooperative United Power.

The upgrade ended up costing those entities hundreds of thousands of dollars, he added.

Gabriel was one of several speakers at a PUC informational meeting on reconductoring. The presentations were organized by the Colorado Electric Transmission Authority (CETA).

Reconductoring involves replacing the wires between existing transmission towers, leaving those structures in place. It’s typically faster and cheaper than new construction or a rebuild, the speakers said. Because existing right-of-way is used, environmental hurdles and permitting challenges may be reduced.

An Idaho National Laboratory (INL) report found that reconductoring with advanced conductors can double the capacity of existing lines at a cost about one-third that of building new lines. Advanced conductors use modern materials to withstand the high temperatures of heavy loads while managing sag. Power flow can be increased.

The INL study found that 118,821 miles of existing transmission lines — out of around 600,000 miles of transmission across the U.S. — would benefit from reconductoring with advanced conductors.

Reconductoring Pitfalls

Reconductoring is getting the attention of state lawmakers, including those in California. Gov. Gavin Newsom in 2024 signed Senate Bill 1006, which requires utilities to study the feasibility of using advanced reconductoring and other grid-enhancing technologies. They must submit reports to CAISO, which will review the findings as part of its annual transmission planning. (See California GETs Bill Gets Newsom’s Signature.)

Still, there are situations where reconductoring may not be the best option, such as when transmission structures need replacing.

“If you’ve got 70-year-old wooden poles in a fire-prone area, [it] might not be the best opportunity to go back and put up new conductor on top of those,” said Joe Coffey, vice president of transmission at Prysmian, a conductor manufacturer. Coffey worked on the INL reconductoring report.

Coffey noted that reconductoring wouldn’t necessarily remove bottlenecks at substations or other places on the grid.

Gabriel of United Power said reconductoring isn’t the only solution. He pointed to other grid-enhancing technologies such as dynamic thermal circuit rating. The technology, also known as dynamic line rating, adjusts a transmission line’s rating based on local conditions rather than using static rating assumptions, potentially boosting the line’s capacity.

“Reconductoring is … a great alternative in some situations,” Tom Green, director at Energy Strategies, told the PUC. “There are limits to what that can do.”

Reconductoring might not remove the need for new transmission that’s necessary for resilience, Green noted.

Meeting Transmission Needs

Green worked on a report for CETA titled “Transmission Capacity Expansion Study for Colorado.” The study found that planned transmission wouldn’t be sufficient to accommodate the 15 GW of renewable energy that Colorado needs to achieve its clean energy goals. More than $4.5 billion in new transmission investment is needed over the next 20 years.

Increasing the capacity of existing lines through reconductoring projects accounted for nearly 80% of the line miles identified in the study but only 28% of the cost.

“The benefits of reconductoring seem pretty straightforward and common-sensical,” CETA Executive Director Maury Galbraith said during the PUC meeting.

Galbraith said CETA is talking with transmission developers about potential partnerships. He’s interested to see if there’s a role for CETA to play in reconductoring.

CETA can issue revenue bonds to help finance transmission construction. The authority will host a study session on Jan. 7 to review findings of a whitepaper on the strategic use of public financing to accelerate transmission development.

CAISO continues to work to revise the rules around how congestion revenues will be allocated to participants in the ISO’s Extended Day-Ahead Market, which will be launched in spring 2026.

The ISO published a proposed set of design principles that would help eliminate or reduce self-schedule incentives in its approved congestion revenue allocation design. Self-scheduling incentives could lead to significant unintended cost shifts, experts cautioned earlier in 2025.

CAISO early in 2025 prioritized EDAM congestion revenue allocation, specifically under parallel — or loop — flows, after Powerex published a paper contending the EDAM model contained a “design flaw” with potentially $1 billion in unjustifiable charges at stake. (See Powerex Paper Sparks Dispute over EDAM ‘Design Flaw’.)

But the approved design stoked concerns among some stakeholders, and CAISO decided to make the design “transitional” for EDAM’s opening in May 2026.

“[The initial design] is transitional to allow us room to further additional enhancements in this second phase, as well as evaluating a more long-term design,” said Milos Bosanac, CAISO regional markets manager, at a Dec. 11 workshop on the subject.

The initial design creates incentives for energy resources to self-schedule in order to receive the congestion rebate, CAISO’s Market Surveillance Committee said in a June letter. Other RTOs/ISOs use financial rights designs to hedge congestion to avoid similar self-scheduling and below-cost bidding incentives, they said.

The MSC cautioned that self-scheduling incentives potentially reduce the benefits of coordinating unit commitment and dispatch across multiple balancing areas that EDAM is intended to provide and could cause cost shifting among participants.

“The potential negative consequences we describe may not be material, particularly in year one given the limited scope of EDAM, but we have not seen enough empirical evidence for us to conclude that this will definitely be the case,” the MSC said. “We recommend that the CAISO seek to transition to financial congestion hedges for future years. How material these self-scheduling incentives and impacts will be during near-term year one EDAM operations with PacifiCorp is uncertain.”

CAISO then started “Phase 2” of its effort to improve the design of congestion revenue allocations.

Phase 2 will study two primary issues: how to eliminate or reduce self-schedule incentives and how to ensure symmetry in allocation of parallel flow congestion revenues for CAISO balancing areas.

ISO staff presented the new design principles at a Dec. 11 stakeholder workshop and they state that:

Congestion revenues should be allocated in an equitable manner to avoid undue cost shifts.

A revised design should support the ability of transmission customers with firm transmission rights or congestion revenue rights (CRRs) to manage and hedge congestion risk exposure considering grid conditions and feasibility of flow.

A revised design should support continued administration of CRRs in the CAISO balancing area and continued sale of OATT transmission rights.

The proposed design principles “provide a starting point for consideration but certainly won’t be the universe of design [principles] we will consider,” Bosanac said.

The revised design also should provide a comparable allocation method for the CAISO balancing area with a CRR construct and for EDAM balancing areas that sell firm OATT transmission, CAISO said. Doing so should enable symmetry in allocation between CAISO and EDAM balancing areas.

CAISO requested stakeholder comments on the design principles by Jan. 16. The ISO plans to present a full proposal for approval in the fourth quarter of 2026.

PJM staff plan to recommend an $11.6 billion package of transmission projects intended to address rising load growth in the east of the RTO’s footprint.

PJM Director of Transmission Planning Sami Abdulsalam said the first window of the 2025 Regional Transmission Expansion Plan is one of the largest iterations of the planning process the RTO has undertaken, if not the largest. It includes constructing a greenfield 765-kV corridor from West Virginia to central Pennsylvania; an HVDC line in Virginia from Brunswick County to Loudoun County; and upgrades to the 765- and 345-kV networks around Columbus, Ohio. (See PJM Presents Shortlist of RTEP Projects.)

The need is being driven by 8 to 12 GW of load growth expected in the PPL and Mid-Atlantic Area Council (MAAC) regions, along with the risk of capacity resource deactivations and significant delays in offshore wind development, Abdulsalam said.

The window was broken into three clusters — west, MAAC and south — as well as $2.3 billion of in-zone projects and $18.5 million in short-circuit upgrades. Independent cost estimates procured by PJM put the total for the clusters, without the in-zone projects, at $10.2 billion.

Additional upgrades could be required along the 765-kV corridor between PJM’s northwestern region and the AEP zone, depending on how generation planned in ComEd and the northwest is constructed.

A set of seven-year scenarios was included in the analysis to properly size the projects to be able to address long-term needs and offer expandability.

Southern Cluster

The southern cluster of projects includes a new 185-mile undergrounded HVDC line between converter stations to be constructed at the Heritage and Mosby substations. It also includes a new 500-kV line between the existing Elmont substation and planned Kraken substation, and rebuilding several 500-kV lines across Dominion Energy’s territory. The package was proposed by Dominion at a $4.8 billion cost, with an independent estimate at just over $5 billion.

The cluster is intended to improve transfer capacity from the southern region of PJM up to Data Center Alley in Northern Virginia, around Dulles Airport.

Several Virginia and Maryland ratepayers spoke in support of the HVDC project on the basis that the subterranean cables would minimize disturbance to surrounding residents compared to the overhead 765-kV alternatives.

Abdulsalam said there are technical benefits to HVDC as well, as the Dominion proposal offers between 500 MW and 1 GW of additional transfer capability over the AC options, and it would not contribute to short-circuit issues that have been growing in Dominion.

The runner-up in PJM’s analysis was a $2.9 billion Transource Energy project to construct a pair of 765-kV lines, one from Heritage to Vontay and the other between Joshua Falls and Morrisville.

Western Cluster

Load growth in Columbus and to its west contributed to thermal overloads and voltage issues across the region. About 1.7 GW are expected to be added between 2029 and 2030, followed by an additional 3 GW in the subsequent two years.

PJM determined a $2.8 billion Transource and FirstEnergy Transmission project to construct several 765-kV lines around the city is the technically superior option and has an independent cost estimate $600 million lower than a joint NextEra Energy and Exelon proposal the RTO evaluated.

The package includes a 765-kV line spanning 172 miles between the Greentown and Marysville substations, with a new 765-kV substation named Teddy to be built around 35 miles west of Marysville. A 32-mile 765-kV line would be built to connect the expanded Conesville substation to the Guernsey facility, and a 38-mile 765-kV line would link the Adkins substation to West Millersport, which also would be expanded. Conesville and West Millersport would be connected with a new 49.1-mile 765-kV line.

MAAC Cluster

The need in MAAC is driven by about 5 GW of additional load growth identified in the 2025 Load Forecast expected by 2030 and delays in the development of 7.5 GW of offshore wind in New Jersey. Staff selected a $1.7 billion NextEra/Exelon proposal to construct a 222-mile, 765-kV line from the Kammer substation in West Virginia to Juniata in Pennsylvania. Two 765/500-kV substations would be built along the line: Buttermilk Falls would be 114 miles east of Kammer and loop into the 500-kV Keystone-Conemaugh line, and Mountain Stone would be constructed near Juniata.

Several stakeholders questioned whether PJM’s medium-high assessment of the land acquisition and right-of-way risks for the proposal are overly optimistic given the amount of greenfield development needed to construct the line.

Abdulsalam said almost half of the route proposed by FirstEnergy overlaps with the NextEra/Exelon corridor, demonstrating that three entities looked at the needs and determined the ideal solution is to use the corridor. The joint proposal offers the greatest transfer capability of all the packages in the cluster.

Below is a summary of the agenda items scheduled to be brought to a vote at the PJM Markets and Reliability Committee and Members Committee meetings Dec. 17. Each item is listed by agenda number, description and projected time of discussion, followed by a summary of the issue and links to prior coverage in RTO Insider.

RTO Insider will cover the discussions and votes.

Markets and Reliability Committee

Consent Agenda (9:05-9:10)

As part of its consent agenda, the committee will be asked to:

B. Endorse proposed revisions to Manual 14B: PJM Region Transmission Planning Process drafted through its periodic review. The changes would allow transmission owners to choose having the ambient ratings for their lines modeled at 59 or 60 degrees Fahrenheit in the light-load case used in the Regional Transmission Expansion Plan. References to phase angle regulators were added throughout the document when referencing phase-shifting transformers to improve consistency. (See “Planning Manual Revisions Endorsed,” PJM Stakeholders Endorse Manual Revisions for Modeling DERs.)

C. Endorse proposed revisions to Manual 14D: Generation Operational Requirements proposed as part of its periodic review. The language would require generation owners to notify PJM of any issues that may affect their units’ ability to start during a cold weather advisory and add detail to the cold weather operating limit data requests and cold weather advisory drill. (See “Manual 14D Revisions Endorsed,” PJM Monitor Presents Spin Event Performance.)

D. Endorse proposed revisions to Manual 14D to rework the rules for generation owners seeking to deactivate units. The FERC-approved changes would require a one-year notice before a resource can be retired and increase the amount of information publicly posted, including the reliability-must-run revenue allocation zonal rate for areas assigned part of the cost associated with agreements to keep units online past their desired deactivation date (ER25-1501). The deactivation avoidable cost credit would be tweaked to remove a $2 million limit on project investments, limit the yearly adder on investments to 10% and remove the trigger causing the daily deficiency rate to be used in lieu of the deactivation avoidable cost rate. (See “Stakeholders Endorse Changes to Generator Deactivation Requirements,” PJM MRC/MC Briefs: Jan. 23, 2025.)

E. Endorse proposed revisions to Manual 19: Load Forecasting and Analysis drafted through the document’s periodic review. The language would reflect the forecast horizon being extended from 15 years to 20 and correct printing issues with formulas included in the manual.

F. Endorse proposed revisions to Manual 18: PJM Capacity Market, Manual 20A: Resource Adequacy Analysis and Manual 21B: PJM Rules and Procedures for Determination of Generating Capability to conform with FERC Order 2222 and detail how distributed energy resources will participate in the 2028/29 Base Residual Auction. The language would eliminate the availability window for demand response and rework the calculation of the winter peak load for participants to be determined at the system’s coincident peak, rather than individual participants’ peaks. (See PJM Stakeholders Endorse Manual Revisions for Modeling DERs.)

B. The Energy Co-op Executive Director Divya Desai will present proposed amendments to the proposal to revise how the minimum tangible net worth would be calculated under the main motion.

The committee will be asked to endorse the proposed solution and corresponding tariff revisions.

As part of its consent agenda, the committee will be asked to:

C. Endorse and approve proposed revisions to the tariff, Reliability Assurance Agreement and Operating Agreement drafted by the Governing Document Enhancement and Clarification Subcommittee.

Endorsements (10:35-10:45)

1. Elections (10:35-10:45)

PJM’s Michele Greening will review the proposed sector representatives to serve on the Finance Committee in 2026, as well as sector whips and the MC’s vice chair for the year. The committee will be asked to elect the proposed representatives.