FTR Bid Limit Increase Endorsed Under Fast Track Pathway

The PJM Market Implementation Committee on Wednesday endorsed a proposal to increase the maximum number of bids a single corporate entity can place in the RTO’s financial transmission rights auctions from 15,000 to 20,000.

PJM is seeking to make the change under its “quick fix approach” — which allows a proposed solution to be endorsed concurrently with its issue charge and problem statement — with the aim of having the change in place for the April 2023 auction. (See “PJM Considering Increasing FTR Bid Limit of 15,000 per Entity,” PJM MIC Briefs: Dec. 7, 2022.)

The increase is being considered based on requests from market participants and following the transition to weekend on-peak and daily off-peak class types, which effectively required traders to submit two bids to acquire or sell the same number of hours of an FTR as prior to the transition, according to the problem statement.

“We did feel this is sufficient for the type and volume of bids that we are seeing today,” PJM’s Emmy Messina said.

The proposal is set to go before the Markets and Reliability Committee on Jan. 25 for a first read, with a vote on endorsement slated for Feb. 23.

Stakeholders Disagree on Approach to Combined Cycle Modeling

Stakeholders deferred action on an issue charge and problem statement addressing the performance impact of expanding multi-schedule modeling to combined cycle generators in the market clearing engine (MCE).

Committee members were divided over what should be considered in the scope of the proposal, as well as whether the effort should continue before PJM releases a white paper it’s currently drafting outlining the bounds of a technically feasible solution.

PJM has an ongoing MCE software contract with General Electric, which is currently in the process of overhauling the programs it provides based on feedback and goals from the RTO, including the effort to expand multi-schedule modeling to combined cycle units. Currently those generators must mimic their operating characteristics in their offers.

Most of the division centered on PJM expanding the out-of-scope topics in its issue charge to include offer structures in its day-ahead and real-time energy markets and to the three-pivotal-supplier test. Those changes were sought by some stakeholders at the MIC’s December meeting and supported by PJM staff seeking to keep the discussion on a tighter time frame. (See “Feedback on Issue Charge, Problem Statement for Combined Cycle Modeling,” PJM MIC Briefs: Dec. 7, 2022.)

PJM’s Rebecca Carroll said GE is seeking guidance on how to proceed with making changes to the MCE by the third quarter of 2023. If stakeholders have not endorsed a system for multi-schedule modeling of combined cycle units by that point, GE will not proceed, she said. Under the current Next Generation Markets framework, the number of permutations that would have to be modeled for combined cycle units would not be solvable.

Paul Sotkiewicz, president of E-Cubed Policy Associates, who pushed for many of the changes PJM had made to its issue charge, said he would also like to see education from other system operators who have attempted multi-schedule approaches for combined cycle units and abandoned the effort because of the amount of time it would take.

David “Scarp” Scarpignato noted that this has been an issue discussed since PJM created a task force on generator modeling nearly a decade ago. Many of the questions raised in recent meetings have been answered in the materials created there, he said.

The Independent Market Monitor also presented its own proposed issue charge with a scope defined as pertaining to the process where software automatically chooses parameters where resources have local market power or during emergency and hot/cold weather alerts.

Ask 10 experts whether RTO markets and electricity deregulation lead to lower prices and you are liable to get 10 different answers.

Debates around the benefits of restructuring have been going on since the states started unbundling monopoly utilities a quarter century ago. A new skirmish arose on #energytwitter earlier this month in response to a New York Timesarticle provocatively headlined “Why Are Energy Prices So High? Some Experts Blame Deregulation.”

Citing an analysis of Energy Information Administration data by energy researcher Robert McCullough, the article says “California and the 34 other states that have deregulated all or parts of their electricity system tend to have higher rates than the rest of the country.” (See sidebar, A ‘Deregulation’ Debate by the Numbers.)

Rorschach Test

RTO Insider reached out to a range of sources to get their thoughts on whether deregulation and organized wholesale markets have benefited customers.

Competition “is a Rorschach test,” energy consultant Alison Silverstein told RTO Insider. “And you can manipulate numbers, particularly electric rates, to say anything you want to.”

Silverstein’s old boss Pat Wood — who took over as chairman of FERC during the California Energy Crisis and chaired the Texas Public Utility Commission when that state started its journey to a fully deregulated, or restructured, wholesale and retail power market — is firmly in the pro-market camp.

“Competition on its worst day is better than I ever could be as a regulator on my best day,” said Wood, who is now CEO of energy storage developer Hunt Energy Network.

Rate regulation is intended to ensure utilities with monopoly territories earn enough to attract investment while keeping prices affordable. No matter how talented regulators are, Wood said, “there’s no way you can really substitute for the efficiencies and discipline of a market on pricing for customers.”

RTOs were created to lower costs to end-use consumers but have failed to do so, said Public Citizen’s Energy Program Director Tyson Slocum. The states that did restructure started with higher prices to begin with for a variety of reasons.

“But those prices remain just as high or higher today than they did 20 years ago, compared to other states,” Slocum said. “So, what’s clear is that RTOs are failing to deliver the promise of lower prices and that should be of great concern to FERC. If the entire purposes for doing something isn’t happening, then you should probably investigate as to why.”

Severin Borenstein, U.C. Berkeley | U.C. Berkeley

Plenty of others are somewhere in the middle with Severin Borenstein, a professor at the University of California Berkeley’s Haas School of Business and a member of CAISO’s board, whose work has found that it depends on other factors entirely.

“The reality is that if you procure power through a deregulated wholesale market, the marginal supply sets the price,” Borenstein said in an interview. “Now, if gas prices are really low, you end up getting much better prices in a [competitive] wholesale market than you do in a regulated market.”

Natural gas is the most common marginal fuel in ISO/RTO markets around the country, which means that generators burning it most often set the locational marginal price (LMP) for other generators. If gas prices are high, then the vertically integrated states have cheaper prices because their generation is not paid a single price, Borenstein said.

The issue of whether RTOs lead to consumer savings was a hot topic before the shale revolution, when gas prices were trading at $7-8/MMBtu some 15 years ago.

“PJM was in absolute crisis,” said Public Citizen’s Slocum. “There was serious consideration of whether or not it had all failed because gas, which was setting the marginal cost, was punishingly high.”

The RTO model got “bailed out” by cheap natural gas from fracking, said Slocum. But now the markets are under strain again as gas prices were higher last year on average than any year since 2008, according to EIA.

Slocum and others also argue that the markets are under strain as renewables are growing, but many who spoke with RTO Insider argued that RTOs and their abilities to efficiently dispatch generation across a wide footprint are going to be key to making that transition happen affordably and reliably.

Economies of Scale

“I think ISOs have led to huge reductions in cost,” FTI Consulting’s Scott Harvey said in an interview. “Particularly in MISO, SPP and the Western EIM, where there was no power pool before. Having the coordinated dispatch of the ISO allows the region to use all of the transfer capability of the transmission system.”

Under the old rules, the available transfer capability used was a fraction of the total available — not because the people running the old utility balancing authorities were trying to keep the resource themselves, but because they had very limited views of where power was flowing, Harvey said. They had to make worst case assumptions because once the power started flowing, they had very limited abilities to change it even if they need to for reliability.

ISO-NE, NYISO and parts of PJM were already in tight power pools before their ISOs developed, but Harvey said PJM’s expansion has led to major improvements.

“If you think back to the polar vortex of 2014, PJM actually got through it without any load shedding,” Harvey said. “I doubt they could have if it was the old world with a bunch of fractionated utilities in the Midwest and Ohio.”

The benefits of stitched together balancing authorities came up again in the recent cold snap over the Christmas holiday when PJM was again stressed but did not shed load while individual utilities in the Southeast did, Harvey said. (See PJM Gas Generator Failures Eyed in Elliott Storm Review.)

Former FERC commissioner and North Dakota regulator Tony Clark, who is now a senior adviser at Wilkinson Barker Knauer, agreed that a clear benefit of RTOs is that they drive scale, which is hugely important in the electric industry.

Time for a Change in the Pricing Model?

The other common feature that is often credited with driving savings is security constrained economic dispatch, but Clark has doubts about the benefits of the ISO/RTO pricing model.

“LMP pricing was designed around a system where most resources had very similar attributes,” Clark said. “They weren’t exact, but more resources were basically dispatchable, they were basically on demand. They might have longer, or shorter lead times, ramp times, things like that. But they tended to be dispatchable, and they tended to have a fuel cost, which is to say they have marginal costs.”

Weather-dependent renewables are not dispatchable, and they have free fuel so they have no marginal costs. But under the current structure they get paid whatever the most expensive plant needed is paid, which tends to be a natural gas unit.

“Under that scenario, do consumers still benefit?” Clark said. “Or would they benefit from some sort of average cost pricing? It’s a really interesting question.”

The idea of average pricing in wholesale power markets, and any other commodity market, is based on a misunderstanding of how bidding works, said U.C. Berkeley’s Borenstein.

“They wouldn’t bid lower if they knew they were going to be paid their bid,” he said. “They’d try to bid whatever the market clearing price is. The idea that everybody gets paid a uniform price is how commodity markets work, not just for electricity — for natural gas, for gold, for oats, for everything. There’s a market price, and people will get paid that market price because they’re selling a homogeneous good.”

ISO/RTOs Share Some Things in Common, But Have Many Differences

While RTOs have some common characteristics, they also have marked differences. ERCOT also helps administer a fully deregulated wholesale power market, while ISO-NE, NYISO and PJM are dominated by states that have also opened their retail markets, though none have gone as far as Texas.

MISO and SPP are largely dominated by traditionally regulated utilities, while CAISO is somewhere in between with community choice aggregation and capped retail competition for large commercial, industrial and institutional customers.

Beyond those regulatory issues, the markets have very different resources, and that can muddle the studies claiming to find savings or increased costs from ISO/RTOs, said NRG Energy Vice President of Regulatory Affairs Travis Kavulla.

“It wouldn’t matter whether New England was open to competition, or economically regulated at the moment; the fact of the matter is under either of those models it would be substantially exposed to the wholesale gas market,” Kavulla said. “New England happens to be a place where policymakers have decided not to build a lot of gas pipelines to domestic sources of gas, and so they have effectively exposed themselves to the European gas market, the global natural gas LNG market.”

Studies will take those effects and impute them to competition, when it really has more to do with the policies of the New England states, Kavulla said. California is another odd duck to squeeze into studies, he said.

“I don’t think any reasonable person would look at the amount of regulation and the amount of government policy related to the energy sector in California and conclude that it’s quote, unquote deregulated,” he added.

Retail Deregulation

Experts who spoke with RTO Insider were split on the benefits of full “deregulation” — where states have also opened their retail power markets.

Wood, who helped design the ERCOT market, still supports retail competition. The wide-open retail market in most of ERCOT is able to flow through the savings from wholesale competition to end-use customers. But in other states where utilities are still providing default retail service to customers it can be more of a muddle.

“I’ve definitely been on the record for 20 years or so about making sure these default providers don’t suffocate retail competition,” Wood said. “So, you either stick with wholesale competition only and you have a very clear way of passing those benefits of low-cost generation, or lower cost generation, being passed through … or you have robust retail competition, like we have here, where retailers compete with the other ones to get your business, and so, they have to pass through those [lower] costs through.”

In between those two worlds, some middleman is likely to keep a share of any of the purported benefits of competition, he added.

The Natural Resources Defense Council’s Ralph Cavanagh was against the idea of retail competition when California was considering deregulating in the late 90s, and he recalls a debate with an executive at Enron on the issue.

“I asked the question publicly: What is in this for my mother?” Cavanagh told us. “To which his response was, ‘for the first time in history, your mother is going to be able to hedge her fuel price risks in the marketplace.’ Mercifully, people laughed at that.”

Cavanagh said small customers generally do not want to spend the time to learn about fuel price risks, though large commercial, industrial and institutional customers can benefit from such options.

“It is worth recalling that even large, sophisticated customers got swamped by the collapse of the California retail markets in 2000 and 2001,” he added.

Coordination Can Help Green the Grid

But when it comes to wholesale competition, Wood and Cavanagh are on the same page. The elimination of utility monopolies over generation has been going on since the 1970s, and no one is seriously considering reversing that, said Cavanagh.

The West outside of California is one of the two main areas, along with the Southeast, that lack an organized market. But in the former that is changing, and Cavanagh said it must do so to reliably transition the grid to a cleaner future. The West would not have made it through the massive heatwave this past September without major cooperation, where Arizona helped California and California helped Idaho maintain reliability.

“It became obvious to everyone that nobody cared what the political color of the state was,” Cavanagh said. “There’s a common interest to a fully functioning regional grid to which we are all connected.”

The CAISO-run Western Energy Imbalance Market has already expanded to cover most of the Western Interconnection, and it has saved billions of dollars so far.

“The most important thing we have to do now is to get the California legislature to open a path to fully independent governance for the California ISO,” Cavanagh said.

CAISO covers roughly one quarter of the generation and demand for power in the Western grid. Cavanagh said it was the best positioned entity to run the entire interconnection. SPP, however, is also fighting for a role in the Western Interconnection. (See SPP Makes Moves Out of the Southwest.)

The New York Times article that started a fresh round in this old debate spent a lot of time focusing on ballooning transmission and distribution bills that have little to do with markets.

Among the causes the Times cited for the higher prices in “deregulated” states are transmission and distribution costs and power company profits. “Deregulated states may spend more on transmission,” R Street Institute energy adviser Josiah Neeley acknowledged in a rebuttal published in Reason. “But that part of the market is still heavily regulated.”

Of the three big categories that feed into customers’ bills — transmission, distribution and generation — transmission is the smallest of the three. By opening up new resources to serve load, it puts downward pressure on prices, said Cavanagh.

“The entire country is now linked by high voltage interstate transmission, which is regulated on the provision of non-discriminatory access,” he added. “That’s the American model. We’re not divided on that; we’re divided on lots of other things, but not that.”

Transmission and distribution spending will need to increase to ensure the industry can reliably and affordably transition to the kind of cleaner grid needed to avoid the worst impacts of climate change.

“The impact of broader transmission is to create lower wholesale power prices, which is the whole point,” Wood said. “You want to have broader markets to get access to the most cost-effective power, which is a bigger percentage of the customer’s bill than the wires charges are.”

Texas saw the benefits of expanding transmission with its Competitive Renewable Energy Zone lines, which were planned 15 years ago and came with a $7 billion price tag to bring wind from the resource-rich areas of the state to its cities. They wound up producing benefits that were five times their cost, Wood said.

The distribution system is going to need investment as well, to ensure that it can handle all the new sources of demand, such as plug-in vehicles and heat pumps, as well the growing distributed resources such as solar panels and batteries, he added.

Do Markets Help with Greening the Grid?

Silverstein argued that beyond transmission, wholesale competition has helped to weed out old, inefficient coal plants and replaced them with cleaner, more efficient natural gas — and in more recent years, renewable power.

“God forbid, thinking about what we might have had for the rate of climate change and extreme weather if we hadn’t been enabling competition to shut out older and natural gas plants that were emitting even more carbon and were highly inefficient,” she said.

While most experts support the idea that transmitting renewables around a large, centrally managed grid helps, some questioned whether the competitive markets were really helping renewables. Public Citizen’s Slocum argued that the shift to renewables has put the system under strain, as seen with efforts from FERC under the Trump administration to block their impact on the market through the minimum offer price rule.

“Renewables are coming into the system in spite of the market design,” Slocum said. “They’re coming into the system because of regulatory mandates and financial incentives, which are not the markets. And as a result, it’s upending the market-based pricing system.”

CAISO on Friday released a draft report on Western regionalization that is intended to restart talks on the ISO becoming an RTO and bolster a likely legislative effort this year to open its governance to residents of other states.

The report examined 41 regionalization studies in response to last year’s Assembly Concurrence Resolution 188, by State Assemblyman Chris Holden (D), chair of the Assembly Appropriations Committee and a proponent of CAISO expansion. ACR 188 asked the ISO and the state’s eight other balancing authorities to report to the legislature on recent and relevant studies of regional market impacts by Feb. 28.

“It’s time for California to revisit a broader regional market,” Holden said in a message accompanying the bill, which passed unanimously in the State Senate and Assembly.

Prior attempts by Holden in 2017-2018 to allow CAISO to become an RTO failed, but circumstances in California and the West have changed significantly since then. (See Plans Revive to Make CAISO a Western RTO.)

“Expanding CAISO to become a multistate regional transmission organization is an option that ACR 188 calls out specifically,” the report notes.

To avoid appearances of bias, CAISO commissioned the National Renewable Energy Laboratory (NREL) to write the report. “As a national laboratory of the U.S. Department of Energy, NREL is independent of any particular stakeholders and state policies,” the report says.

NREL researchers examined dozens of studies that concluded California and most other Western states would benefit from increased collaboration in terms of cost savings, resource adequacy and meeting climate goals. They included a June 2021 study that found an RTO covering the entire U.S. portion of the Western Interconnection could save the region $2 billion in annual electricity costs by 2030 and cut carbon dioxide emissions by 191 million metric tons.

The study, funded by the U.S. Department of Energy, was led by Utah Gov. Spencer Cox’s Office of Energy Development and energy offices in Colorado, Idaho and Montana. (See Study Shows RTO Could Save West $2B Yearly by 2030.)

A “large, multistate RTO is one of several options,” the report says. “It could provide the largest margin of benefit, including the greatest visibility into operational performance, efficient dispatch and lower-cost reliability. Other forms of enhanced regional cooperation, such as a regional energy market, a regional mechanism for resource adequacy or even the expansion of an RTO to only a few neighboring states, would also provide some measure of cost savings, reliability improvements and reduced carbon emissions for the benefit of all participants.”

However, “some of the technical studies included in this review suggest that the benefits of more comprehensive forms of regional cooperation might not be spread evenly across participating states and their utilities,” the report said. A section detailing the “distribution of benefits among states” in one or more Western RTOs is still being drafted.

“The CAISO is working with NREL to expand this section to be responsive to the legislation,” the report says.

The state-led study found “that a single RTO would provide California and all other states greater capacity savings than two Western RTOs. For a day-ahead market, all states except Colorado would see greater capacity savings with one market rather than two.”

A separate study conducted by the Colorado Public Utilities Commission at the behest of Colorado lawmakers determined that the state would benefit more if there were two RTOs: one led by CAISO, and another by SPP that includes most utilities in Colorado and some in Wyoming.

“This study found significant cost savings to Colorado if its utilities were to join a regional RTO,” the report says. “Interestingly, the benefits were slightly greater for joining SPP: a 9% savings in total system costs over the status quo reference case, compared to 8% for a [WECC-wide] RTO and 7% splitting Colorado between SPP and a WECC RTO.”

If Colorado participates in a WECC-wide RTO, “higher power prices in the West [especially California] lead to slightly higher prices in Colorado,” it said. “The marginal cost of serving demand in Colorado under a WECC RTO was about 16% higher than it would be if Colorado utilities were in SPP. Colorado also retired more coal capacity under the SPP RTO.”

In the past two years, a handful of Colorado utilities decided to join SPP’s real-time Western Energy Imbalance Service instead of CAISO’s larger Western Energy Imbalance Market, with some exploring membership in SPP’s RTO. (See Colorado Utilities Choose WEIS over WEIM.)

The ACR 188 report comes as CAISO and SPP continue to vie for Western market share in a region primed for one or more organized electricity markets.

SPP plans to launch its Markets+ offering with many of the services of an RTO and later to introduce a Western version of its Eastern RTO called RTO West. CAISO intends to add a day-ahead market to its successful real-time WEIM, which could eventually develop into an RTO. The Western Power Pool (formerly the Northwest Power Pool) is seeking FERC approval for its Western Resource Adequacy Program, a possible RTO launchpad. And Colorado and Nevada have ordered transmission-owning utilities to join an RTO by 2030.

The retirement of coal generation and increase in wind and solar resources in remote parts of the West is a major factor driving the need for regional transmission planning, the report notes. Strained grid conditions during heat waves have shown the need for better a resource adequacy framework, and a growing number of states are adopting clean-energy goals, requiring more interstate transactions, it said.

CAISO has scheduled a stakeholder call for this Friday to discuss the report.

“The ISO values stakeholder input on this preliminary draft and plans to incorporate feedback received during the Jan. 20 stakeholder call, and in written comments submitted by the deadline on Feb. 3, into future iterations to ensure the accuracy and value of the final report,” the ISO said last Friday in a message to stakeholders.

PORTLAND, Ore. — When energy economist Robert McCullough greeted this reporter at a wine shop and deli in our shared Southeast Portland neighborhood, he joked about recently contributing to “quite a stir” in the electricity industry.

McCullough was referring to a high-profile article published in TheNew York Times Jan. 4 under the headline “Why Are Energy Prices So High? Some Experts Blame Deregulation,” which set off a wave of criticism from industry insiders — much of it on #energytwitter.

“On average, residents living in a deregulated market pay $40 more per month for electricity than those in the states that let individual utilities control most or all parts of the grid. Deregulated areas have had higher prices as far back as 1998,” the Times said.

Times Article Misses the Mark, Critics Say

Critics faulted the Times for conflating “deregulation” with organized RTO/ISO wholesale markets.

While 13 states and the District of Columbia allow most of their electric customers to choose their electric supplier, the Times appeared to be including as “deregulated” 21 states whose utilities participate in organized wholesale markets but do not allow retail choice, said R Street Institute energy adviser Josiah Neeley in a rebuttal published in Reason.

The Times “seems to say that the label ‘deregulation’ applies even in places like Minnesota, where no customer exercises a choice in provider, and where the industry simply has been restructured to be part of a larger grid with two different regulators (FERC and the state),” tweeted former Montana regulator Travis Kavulla.

Kavulla, now vice president of regulatory affairs for NRG Energy (NYSE:NRG) also rejected the characterization of California as “deregulated,” saying it “stands as the foremost example of a jurisdiction where policymakers treat utility balance sheets as playthings for various policy ends.

“There is no such thing as ‘deregulation’ or a ‘free market’ in this industry anywhere — which remains regulated everywhere,” Kavulla added.

A power and gas trader who tweets under the name “King of Power” called the piece a “master class in how not to do power market analysis,” adding that “the article is so full of bad methodology and blatant falsehoods that it would make a utility blush.”

Other critics pointed to a lack of supporting data in the piece.

McCullough, who was prominently quoted by Times reporter Ivan Penn, also produced the data that was cited in the article but conspicuously absent from it. In an interview with RTO Insider, McCullough acknowledged that omission, but said he thought the piece was “generally a good article” that just required more “column inches” to do the subject justice. He said he may have “overwhelmed” Penn “on this whole question of competition.”

“Of course, one of the evocative things about electricity — evocative in that it attracts a lot of confusion — is it is complicated, and so it’s very hard to get some of the concepts across,” McCullough said.

Penn did not respond to a request for comment.

Some of that confusion may have stemmed from the article’s use of the term “deregulated.” In our interview, McCullough said the analysis he provided the Times wasn’t really a comparison of retail electricity prices in deregulated versus regulated states, but between states operating inside and outside of organized markets.

McCullough’s staff sourced the price and volume data from the U.S. Energy Information Administration’s Electric Power Monthly reports, and calculated weighted price averages to show differentials between RTO and non-RTO states.

“Is that exact? No, because of course, some of the states are split between two [markets]. But was it honest? Yeah — it’s a pretty straightforward calculation,” McCullough said.

The data does not control for differences in fuel costs or resources across regions, because, McCullough said, the Times only requested retail price numbers. A spreadsheet he provided to RTO Insider includes a retail price data series covering January 1998 to October 2022, showing average monthly prices and total electricity consumption by state. That data is then distilled into a comparison of prices between RTO and non-RTO states over the entire period.

The first entry, January 1998, before widespread implementation of retail choice, shows an average retail price of 6.33 cents/kWh in non-RTO states and 7.41 cents/kWh for states that would eventually join RTO states. During the Western energy crisis in 2001, the spread increased sharply, with non-RTO states averaging of 6.47 cents/kWh and RTO states 9.35 cents/kWh.

During a period of relatively high natural gas prices from 2002 to 2009, retail prices averaged 8.35 cents/kWh in non-RTO states versus 9.99 cents/kWh in RTOs. In the 2012-15 period of lower gas prices, average non-RTO and RTO state prices were 9.52 and 10.47 cents/kWh, respectively.

A graph included with the data illustrates trends across the time series, with callouts for events in which RTO price spikes outpaced those in non-RTO areas. The events include the commodities price bubble of 2008, the ERCOT outages accompanying February 2021’s winter storm and Russia’s invasion of Ukraine in February 2022.

McCullough contends that prices in RTO areas can be more sensitive to such events because RTOs rely on the single market clearing price mechanism to set prices, as opposed to the “price-as-bid” nature of the traditional utility model.

“For states served at the market clearing price — ERCOT comes to mind — the swings are greater because the entire market is priced at the market clearing price,” he said. “And, of course, for ERCOT the reserve margin price adjustment, as well as the ERCOT-administered emergency price cap, creates quite a ‘bump.’ A peculiarity of the ERCOT rolling outages is that the prices crossed the ERCOT border and extended all the way north to North Dakota in the SPP market. This is somewhat peculiar given the limited transmission, but [it] did affect retail rates.”

McCullough was among the first industry watchers to identify the manipulation that sparked the Western energy crisis of 2000-01, when energy traders such as Enron exploited adverse market conditions and design flaws in California’s organized electricity market to drive up wholesale prices. Their actions caused rolling blackouts, bankrupted Pacific Gas & Electric and nearly sunk Southern California Edison. He has long been a vocal critic of RTOs and ISOs, which he refers to as “administered” markets, compared with what he calls the “competitive” bilateral wholesale markets that still predominate in most of the West.

“Northwest power markets are large and competitive and low-price, but we don’t have a central administrator to tell us what to do. How valuable is the central administrator on energy markets and prescheduled energy markets? I suspect the answeris: pretty irrelevant,” he said.

McCullough thinks the Northwest has “maintained a very successful, large, efficient market for many years … with very few abuses, no blackouts, [and] guys who actually call each other on the phone and buy and sell.

“Exceedingly transparent. Far more transparent than in the California ISO because you know everyone’s prices every day,” he said.

Impact of Markups

R Street’s Neeley also challenged the Times’ contention that competition leads to higher prices because of “profits taken in by energy suppliers.”

“Based on reading the Times article, you might be surprised to learn that monopoly utilities also make profits,” Neeley wrote. “Indeed, utility rates are typically set to give the utility a set percentage of profit based on their past investments. This, needless to say, does not encourage utilities to find ways to lower costs.”

The Times article might have strengthened its thesis if it gave more than passing mention to a Harvard working paper published last month that does in fact focus on the impact of electricity deregulation on ratepayers.

The authors of the paper, Alexander MacKay, assistant professor of business administration at Harvard Business School, and Ignacia Mercadal, assistant professor of economics at University of Florida,say their work seeks to fill a gap in the academic discussion on electricity restructuring by addressing the question of whether deregulation of wholesale (as opposed to retail) markets has resulted in lower electricity prices for end consumers.

Their findings suggest the opposite: that consumers in markets subject to wholesale deregulation have seen greater increases in retail prices compared with those in fully regulated environments.

“The goal of our analysis is to evaluate the effect of electricity restructuring on markups and prices. For this, we compare utilities in restructured states to those that remained vertically integrated and regulated, and we examine the evolution of costs, wholesale prices, and retail prices over time,” MacKay and Mercadal explain in the paper.

While the study does not specifically focus on differentials based on RTO markets, it does address the influence of those markets on price outcomes, in part because nearly every retail choice state featured in the study — except Oregon — participates in an RTO or ISO. That study also relies on EIA retail price data sets.

The study examines the period between 1994 and 2016, using 1999 as the “baseline” for retail prices and relying on a “difference-in-differences” approach that measures the price movements in deregulated states relative to the those in the “control” group of states that did not implement retail choice. It finds that states that unbundled their monopoly utilities started with a higher baseline for retail prices (averaging $79/MWh — or 7.9 cents/kWh) than those in the control group ($59/MWh), which is attributed to higher fuel prices in the deregulated states at the time.

From 1994 to 1997, the analysis showed prices were stable for both groups, followed by a convergence over 1998-2000 as prices in deregulated states declined while those in control states held steady. “Starting in 2001, prices in both states began to rise. Deregulated prices outpaced control prices until 2005, when the gap between the two widened further,” the authors write.

From 2000 to 2005, deregulated utilities saw average price increases of $3.90/MWh, followed by a sharper rise of $12.60/MWh from 2006 to 2016 (a 16% increase from the baseline), for an average increase of $7.60/MWh over 2000-2016.

“We reiterate that these changes are difference-in-differences effects, i.e., increases above and beyond the price trends occurring in control utilities,” the authors wrote.

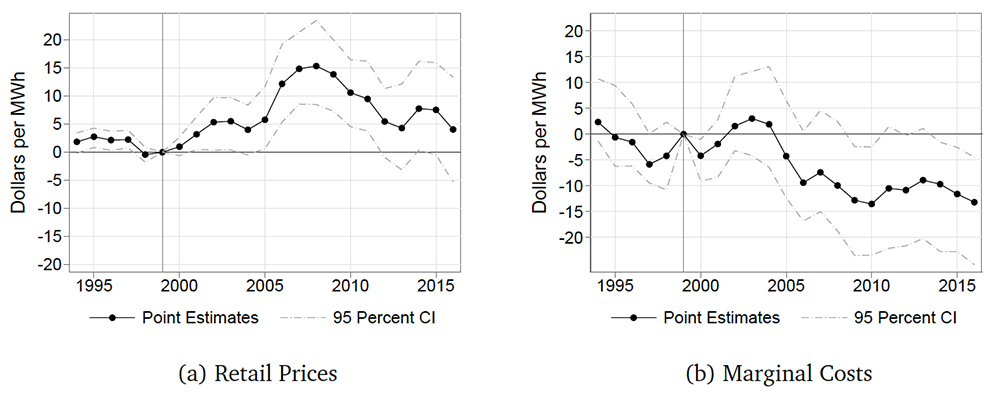

Another key finding: while retail prices rose in deregulated markets, generation costs declined, with average fuel prices falling by $6.90/MWh over the study period. The authors say that indicates generators were earning higher “markups” for their power — the difference between the selling price for power and the cost for generating it. The study finds that markups were “modest” from 2000 to 2005, but spiked to $20/MWh over 2006-2011 (See graph).

Figure displays difference-in-differences matching estimates of changes in (a) retail prices and (b) fuel costs for deregulated utilities. Each deregulated utility is matched to a set of three control utilities based on 1994 characteristics. The estimated effects are indexed to 1999, which is the year prior to the first substantial deregulation measures. The dashed lines indicate 95 confidence intervals, which are constructed via subsampling. | Alexander MacKay and Ignacia Mercadal

MacKay and Mercadal attribute that development to a combination of factors present in deregulated markets, including an increased concentration of power suppliers and a larger pool of buyers that now includes utilities, power marketers and industrial customers. They contend that when the wholesale price caps that states implemented to smooth the transition to deregulation began to expire around 2005, bargaining power for distribution utilities declined while the market power of generators increased.

“For a utility, obtaining electricity from the wholesale market was more expensive than [providing its own generation], as wholesale prices reflect a markup. … With deregulation, utilities effectively paid a market-based markup to generation facilities that they had previously owned,” they say.

At the same time, incumbent utilities increased their regulated retail rates to reimburse average variable costs, which “went up due to the introduction of this markup.”

The study also contends that the specific characteristics of electricity make wholesale markets “particularly prone to market power.”

“Both demand and supply are inelastic, yet supply must meet demand at every moment since large amounts of electricity cannot be stored efficiently. Transportation is expensive, constraining the degree to which generators compete across local markets. Entry is limited due to large sunk investments, long planning horizons, and high risk. As a result of these factors, only a few generators are typically competing to serve demand for a certain area at a particular moment, and the relative scarcity can give them substantial market power. Deregulation did not fundamentally change these factors,” the authors say.

Tyson Slocum, director of Public Citizen’s energy program, said the Harvard study indicates that the efficiency gains from wholesale markets “are all being vacuumed up by these sophisticated traders and other market participants” who exploit arbitrages and take the profits, leaving no savings to end consumers.

“It’s a who’s who of sophisticated financial traders,” Slocum said. “Those guys are parked in those markets, not because, you know, ‘Gosh, we need to work every day to deliver value to end users.’ They’re like: ‘We’re going to be heavily in these markets to exploit the arbitrage and make enormous and unregulated profits.’ That’s what’s driving RTO activity.”

‘Likely Wrong’

But criticism of the study came from a different corner, setting off an exchange that illustrates the difficulty of reaching consensus on the impacts of electric restructuring.

Scott Harvey, an energy consultant with FTI Consulting and member of CAISO’s Market Surveillance Committee, picked apart the paper in an email to RTO Insider. Among other complaints, Harvey contended that its finding of declining fuel costs for generators from 2002 to 2015 was “incomprehensible” and that there must be something “fundamentally flawed” in how those costs were measured.

He also argued that the wholesale electricity prices used in the paper do not reflect prices in the spot markets, but the higher prices since 1994 for various types of contracts, including those for securing renewables to meet state environmental mandates.

“Hence the fuel cost measure is wrong and the wholesale price measure is wrong. All of the results in the paper are likely wrong,” Harvey wrote.

MacKay and Mercadal defended their approach for measuring fuel costs and noted that their analysis checked for variables such as environmental regulations.

Mercadal also said it would’ve been incorrect to just focus on spot prices in their analysis.

“A big point of our paper is that most of the purchased electricity (>80%) comes from contracts (not spot markets), and these prices are indeed often higher. We can’t just ignore these prices … they really do matter for the prices that consumers pay!” she wrote.

“We would be happy to see evidence supporting other explanations for our findings. We tried competing hypotheses but were not supported by the data,” Mercadal said.

ALBANY, N.Y. — The New York State Legislature has started its 2023 session and is poised to take up many bills that build on the Climate Leadership and Community Protection Act (CLCPA).

Both Senate and Assembly committees will soon hold hearings on bills seeking to improve economic conditions for ratepayers, establish market rules that comply with the CLCPA and protect New York’s natural resources. The bills, among hundreds of others already in front of the legislature, include:

S334, to update requirements for electricity bills;

S404 and S402, to develop more residential advanced metering and microgrid energy storage;

S737, to provide net revenue from renewable generators to low-income customers;

S1487, to mandate that the governor alone select the two candidates for the locally nominated seats on the state Board on Electric Generation Siting and the Environment;

S1275, to increase the number of trustees on the New York Power Authority by two, and mandate that the new seats be held by a resident of Niagara County and of St. Lawrence County; and

S374 and S592, to add conditions for transmission approvals and renewable siting.

Other bills target environmental conservation through creating carbon dioxide pricing mechanisms; establishing a public water justice act; authorizing forest rangers to train search-and-rescue volunteers; and requiring annual climate expenditure reports (S732, S238, S28, S288).

Republican Priorities

Senate Minority Leader Robert G. Ortt last week outlined Republicans’ “Rescue New York” agenda, which includes calls for increasing energy affordability, stemming the flow of capital from the state, enacting climate policies that ensure affordable and reliable energy, and eliminating burdensome regulations.

In an email to RTO Insider, Ortt argued that “everyone agrees we need to move toward a clean energy future, but we need to do so by supporting common-sense energy policies that work.”

“The unachievable goals and radical policies set out by the Climate Action Council will only continue to drive New York residents and businesses elsewhere,” Ortt said. Republicans have “repeatedly requested a cost-analysis because we must understand the real implications that are going to land on the backs of New York’s ratepayers.”

The Republican agenda includes opposing proposed bans for natural gas hookups, requiring independent cost studies of all the CAC’s proposals and supporting burgeoning technologies, such as advanced nuclear and hydrogen.

One of the bills Ortt is sponsoring, S592, would prohibit siting wind farms within 40 miles of military installations. It is in response Apex Clean Energy’s proposed Lighthouse Wind Project in the towns of Yates and Somerset. The Niagara Falls Air Reserve Station is about 30 miles away from Somerset.

“The Niagara Falls Air Reserve Station is too much of an asset to Niagara County and our entire region to put its future at jeopardy with this proposed project,” Ortt said. “We cannot risk hindering the air base’s operations, security and potential new missions.”

Democratic Outlook

Assemblymember Didi Barrett (D), the newly elected chair of the Assembly’s Energy Committee, told RTO Insider that she plans on “supporting innovative energy generation practices and technologies, and working with state, local and community leaders to develop and to support the siting of renewable energy in an equitable and sustainable manner.”

Barrett said she will “develop thoughtful legislation that will help us meet our goals through a just energy transition.” The CLCPA emphasizes “the important balance between reaching our ambitious climate goals while protecting communities across New York.”

She also said she does not believe energy is a partisan issue, highlighting how she has “sponsored and passed numerous bills on a range of issues with bipartisan support” and “stands ready to work with colleagues in both parties and both houses to forge a path forward.”

Despite differences on what actions need to be take, which issues should be prioritized or what policies will be most effective, Barrett said legislators align on the fact that New York is at a critical stage and that actions taken this year will have a massive impact on the future.

The New York League of Conservation Voters’ (NYLCV) recently released 2023 legislative priorities call for more offshore wind development, the creation of a clean fuel standard, more investment in green jobs and education, enhancement of coastal resilience, more funding for agencies charged with energy resources, and improvements to the access and quality of natural resources.

In an email to RTO Insider, NYLCV Policy Director Patrick McClellan said, “No silver bullet exists to solve the climate crisis overnight, or even in a couple years, but if we make the right decisions now, New York will be better prepared to withstand the impacts of climate change in the coming years.”

McClellan believes “it’s imperative that the state increase its offshore wind capacity through the timely procurement, responsible siting, government permitting and the transmission of 9 GW of offshore wind by 2035, while increasing our offshore wind goal to 20 GW by 2050.”

The Alliance for Clean Energy New York’s (ACE NY) 2023 legislative agenda closely aligns with legislation the organization supported previously.

It calls for bills that help renewable projects overcome construction barriers, codify state operations being powered entirely by renewables, promote clean transportation and buildings efforts and exempt energy storage resources from the sales tax.

ACE NY “supports legislation that enhances market opportunities for large-scale, grid-connected renewables; for smaller-scale distributed renewable energy; for energy efficiency; and the electrification of transportation.” It opposes bills that “would unduly or unfairly restrict clean energy development in New York state.”

Alan Gooding, co-founder of the United Kingdom’s Smarter Grid Solutions software company, told MISO stakeholders Thursday that distributed energy resources are going to be a “very large part of the energy mix going forward” with emerging technologies that are already affecting the system.

Speaking during a conference call with the RTO’s DER task force, Gooding said large customers are drawn to DERs for price security and as a hedge against global energy scarcity. He said with the industry facing electrification’s increased demand to fuel “heat, transport, cooling and industrial processes,” companies will have to reimagine and retool the grid as part of a massive infrastructure development.

“All of that increased demand, four, five times the demand … will have to be supplied by green energy at the point of use. We’re talking about having to do this within my lifetime,” Gooding said.

He said utilities will need to create DER management systems (DERMS) to access the resources’ full value. DERs need autonomous systems that produce demand and generation forecasts and form dispatch plans, he said.

Gooding said a “maturing sector understanding of DERMS is creating increased confidence to act,” with many DERMS’ requirements quickly becoming standardized. He also said utilities face a range of DER integration challenges that include managing congested interconnection queues, staffing issues, digitalization challenges, data security, grid modernization, and adapting business models.

“We see every utility is going to be on its own DERMS journey,” Gooding said. “We think there’s still quite a journey to go here. Regulations are going to have to catch up with what these assets can technically provide.”

The industry has “so, so much to go” in how DERs interconnect and how the markets adapt, Gooding said. He said DERMS will be key to creating an “integrated ‘ecosystem’ of new and existing systems.”

He also said utilities want to understand how the software works and are no longer looking for their vendors to provide a “black box piece of technology.”

MISO plans to host another DER guest speaker in April. It tentatively plans to gain perspective from a nonprofit DER registry.

MISO held an informational meeting last week on its second request for proposals coming out of its $10 billion long-range transmission portfolio (LRTP).

The newest project up for bids is a 345-kV project crossing the Iowa-Missouri state border. Proposals are due by May 19 with a developer to be selected by Oct. 31, staff told stakeholders during a Thursday teleconference.

The $161 million Fairport-Denny project involves construction of a 345-kV substation in Iowa and two 345-kV transmission lines to Fairport, Mo. In MISO, prequalified transmission developers may submit multiple proposals in response to a RFP, though each submittal requires a $100,000 deposit. That’s on top of the $20,000 application fee they must pay to become a qualified transmission developer able to bid on competitive projects. MISO expects the project to be in service in June 2030.

The RTO’s Board of Directors approved the 18-project LRTP package of 345-kV lines in July. Only about 10% of the portfolio will be competitively bid because of existing right-of-first-refusal laws and upgrade work. (See MISO Board Approves $10B in Long-range Tx Projects.)

The Fairport-Denny RFP is the fourth MISO has issued and is the first it will manage and evaluate simultaneously with other open RFPs.

The grid operator in September released an RFP for a $254 million 345-kV project on the Indiana-Michigan state border. It expects to announce a developer for that work on May 11.

MISO will release its third RFP on March 6 for a $556 million 345-kV project that will link up with the Fairport-Denny project. Developers have until February to become certified to bid on the line.

Brian Pedersen, senior manager of competitive transmission services, said two other RFPs will be released in July. MISO plans to open bidding periods for a $12 million, 345-kV project in Wisconsin on July 11 and a $23 million, 345-kV segment from the Iowa-Illinois border to an Illinois substation on July 24.

For transparency’s sake, MISO has instructed stakeholders to send all questions regarding the competitive process to TDQS@misoenergy.org instead of individual personnel. The RTO also prohibits stakeholders from directing questions about competitive projects to interconnecting incumbent transmission owners while an RFP is active.

Stakeholders last week requested MISO take a second look at its recommendation for expedited transmission projects in Michigan.

During a series of technical study task force meetings, the RTO said it would recommend five expedited projects in its 2023 Transmission Expansion Plan (MTEP23). However, stakeholders said a $63 million package of a proposed substation and line work in Michigan could use more evaluation.

ITC subsidiary Michigan Electric Transmission Co. (METC) proposed that it construct a new 138-kV substation, build 1.5 miles of new 138-kV line and rebuild more than 25 miles of 138-kV lines near Big Rapids, Mich., to serve a new large industrial customer. METC said approvals cannot wait on the December deadline for the MTEP approval. The project has a March 2025 in-service date and is backed by the Michigan Economic Development Corporation.

During a Wednesday task force meeting, Wolverine Power Supply Cooperative’s Tom King said his utility’s planned upgrade of nearby 69-kV and 138-kV lines by 2024 could help alleviate the need for some of the METC project’s elements.

Thompson Adu, MISO’s senior manager of transmission expansion planning, said staff will evaluate Wolverine’s suggestion further. He said MISO could either consider the alternative for the second half of the project or recommend the as-is expedited request at the Jan. 25 Planning Advisory Committee.

During the meeting, stakeholders also asked whether they could propose alternative projects for the solutions outlined in expedited project requests. Adu said MISO can examine alternatives but that expedited projects are sometimes urgently needed and don’t allow time for in-depth study.

The grid operator has recently fielded a steady clip of expedited project reviews to primarily accommodate new industrial load. A series of expedited project recommendations last year in MISO South led some stakeholders to question whether staff is engaging in thorough and cost-effective transmission planning and exploring alternatives. (See Stakeholders Doubt MISO Study of Alternative Tx Projects.)

Another expedited request from Michigan also produced concern. MISO said it found no issues with ITC’s $5.5 million, 120-kV underground cable relocation to allow the Michigan Department of Transportation to begin freeway construction.

Thompson said MISO would conduct further closed-door discussions on the project details of the expedited request.

The RTO did clear Henderson Municipal Power and Light’s proposed 161-kV line reroute to make way for a new recycled paper mill in Kentucky. The $160,000 tap project is necessary to accommodate Big Rivers Electric’s previously approved $20 million transmission project to accommodate the mill’s new load. That project was also an expedited request under MTEP 22.

MISO also said it found no reliability issues with Arkansas Electric Cooperative’s plans to add 50 MW of capability to a pair of Mississippi County Electric Cooperative substations.

MISO CEO John Bear will helm two international energy industry associations this year, the grid operator said Thursday.

The RTO said that Bear was appointed chair of the ISO/RTO Council (IRC) and also elected president of GO15, an international association of 15 grid operators that collectively manage more than half the world’s electricity demand.

Bear succeeds Stefano Donnarumma, CEO of Terna, Italy’s national transmission service operator, at GO15 and CAISO CEO Elliot Mainzer at IRC. The council includes representatives from the seven U.S. and two Canadian system operators. The IRC chair’s role rotates annually among current IRC Board members.

“There is a need for continued collaboration and idea sharing when it comes to operating the power grid and planning for the future,” Bear said in a press release. “Our collective problem solving enables us to keep the power flowing reliably and efficiently. That’s true whether we are working locally, regionally, nationally or even globally.”

Bear said he will focus on “major strategic and technical issues” affecting power systems during his GO15 term, including grid decarbonization and digitalization and the resilience of electricity infrastructure.

Winter storms that dumped heavy, wet snow on Northern Nevada knocked out power to almost 124,000 NV Energy customers over the New Year’s holiday weekend, according to a report from the utility.

The outages reached a peak around 8 p.m. on Dec. 31, when 89,378 customers were without power, NV Energy said in a report filed with the Public Utilities Commission of Nevada. And 8,000 customers still didn’t have power on Jan. 3, according to PUCN.

NV Energy filed the report on Wednesday in response to an order from PUCN. The commission opened a docket on Jan. 3 to investigate the causes of the outages and the utility’s response.

In its report, NV Energy said “extreme weather” caused the outages.

“The storm was a very long-duration, atmospheric river storm that affected the entire region of Northern Nevada with heavy precipitation in the form of heavy, wet snow,” the report said.

Storm-related damage occurred across most western Nevada valleys and at Lake Tahoe, as tree branches snapped and snow piled up on power lines and equipment.

NV Energy dealt with 765 separate outages impacting an estimated 123,879 customers from Dec. 30 to Jan. 5. Twenty-nine of the outages were momentary, and the remainder were prolonged.

The outages mainly involved the distribution system and were caused by blown fuses, downed wires, broken poles, and damaged transformers and pole line hardware. In addition, downed wires and damaged structures caused some transmission-level outages, the utility said.

NV Energy worked to first address outages affecting the largest number of customers. As power was restored to many customers, the focus shifted to customers who had been without power for the longest time.

On Jan. 4, NV Energy made direct calls to 614 residential customers who had been without power for more than 48 hours, offering free lodging at a local hotel and checking to see if they needed water for livestock.

The utility also communicated with customers through the news media, its website and social media.

NV Energy initially dispatched four of its own crews to repair the outages on Dec. 31. Additional crews were then brought in from other parts of the state, along with seven contract crews, for a total of 18 crews on Jan. 2. A typical crew consists of four or five linemen.

In addition to the crews, the response included troubleshooters, fire crews for snow and debris removal, and NV Energy’s crisis and incident management teams.

Paul Sotkiewicz, E-Cubed Policy Associates | © RTO Insider LLC

Paul Sotkiewicz, E-Cubed Policy Associates | © RTO Insider LLC