SPP, MISO Applying for DOE Funds to Help with JTIQ Portfolio

OKLAHOMA CITY — SPP told its members last week that it will apply for grants from the U.S. Department of Energy to help fund transmission projects recently identified with MISO along their seam that could unclog their generation interconnection queues.

David Kelley, SPP | © RTO Insider LLC

David Kelley, SPP | © RTO Insider LLC

David Kelley, the RTO’s newly minted vice president of engineering, said DOE’s $10.5 billion Grid Resilience and Innovation Partnerships (GRIP) program aligns neatly with SPP’s Joint Targeted Interconnection Queue (JTIQ) study with MISO.

GRIP, authorized under the Infrastructure Investment and Jobs Act, is designed to accelerate the deployment of “transformative” projects that improve the grid’s flexibility and resilience against the growing threats of extreme weather and climate change. It includes a focus on interregional projects, investments that accelerate the interconnection of clean energy generation, and using distribution assets to provide backup power and reduce transmission requirements. (See DOE Opens Applications for $6B in Grid Funding.)

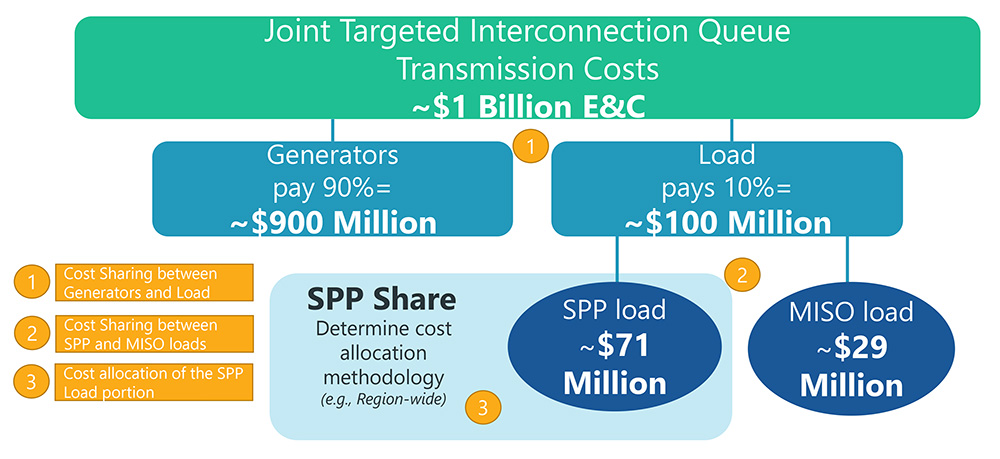

The JTIQ study resulted in five projects on the MISO-SPP seam that should help reduce congestion and allow additional resources, primarily wind farms, to interconnect with the RTOs’ systems. Their staffs have proposed a cost allocation that assigns most of the portfolio’s $1.06 billion in costs to generation. (See MISO, SPP Propose 90-10 Cost Split for JTIQ Projects.)

“We have still yet to find the magic unicorn of developing transmission along the seams,” Kelley said. “When we looked at [the GRIP] program and what it was intended to do, it almost reads as if it was written for something like what JTIQ was trying to do. It was kind of a no-brainer for us to seek to receive some of this money on behalf of our members.”

Kelley said an initial concept paper has already been filed with the program’s administrators, meeting a Jan. 13 deadline. DOE will review the applications to determine whether they are worthy of full applications, providing that feedback to applicants. Final applications will be due May 19.

Under DOE’s Grid Innovation Program, applications must come from a state or a group of states, regulatory commissions or tribal or local governments. That has led SPP and MISO to collaborate with the Minnesota Department of Commerce and the Great Plains Institute (GPI) on the effort. The state of Minnesota, as a potential eligible recipient of the funds, made the filing. The institute is coordinating the effort by holding discussions with utilities that will build the projects and those utilities and states that will be affected.

“Our job has been to facilitate all potentially affected folks to kind of vet the DOE requirements,” Matt Prorok, GPI’s senior policy manager, told RTO Insider. “How might those be fulfilled? Are [the JTIQ] projects a good fit for this funding bucket?”

The proposed cost allocation for JTIQ projects. | SPP

The proposed cost allocation for JTIQ projects. | SPP

Kelley pointed out that the GRIP program is a partnership involving federal and private dollars.

“We feel pretty good about it. We’ve talked to DOE a number of times, and they were very interested in what we’re doing here,” Kelley said. “We are being encouraged by what we’re hearing. But again, because this is a partnership, we do think it’s important that we lay the groundwork that not only are we pursuing DOE funds, but that we also have a commitment from SPP, MISO and our customers in our membership that we have the other half of this bill covered.”

Under the staffs’ proposed JTIQ cost-sharing methodology, generators will pay 90% of the portfolio’s cost and load will pay 10%. SPP load will pay about $71 million and MISO load about $29 million, without the DOE funding.

As with any discussion about allocating costs, several stakeholders raised concerns.

Steve Gaw, APA | © RTO Insider LLC

Steve Gaw, APA | © RTO Insider LLC

“I think all of us are seeing this DOE funding opportunity as a way to facilitate mitigating some of the concerns the stakeholders are expressing and the opportunity for that mitigation to really help make this a success,” the Advanced Power Alliance’s Steve Gaw said. “The second round of that application process, if the application makes it there, will be a very opportune time for additional comments of endorsement.”

The Cost Allocation Working Group (CAWG) on Friday unanimously endorsed and recommended that the Regional State Committee approve the 90-10 allocation. It also recommended that:

- the 10% load portion of the JTIQ’s annual transmission revenue requirement (ATRR) be based upon adjusted production costs, as outlined by the RTOs’ joint operating agreement;

- the load portion of the portfolio’s ATRR be regionally allocated on a load-ratio share basis consistent with previous RSC policies;

- each building transmission owner recover the non-capital cost component allocable to generation interconnection customers through a formula rate template in the building TO’s region; and

- SPP’s load share in the current portfolio and for the next study of the southern party of the MISO-SPP seam be regionally allocated on a load-ratio share basis consistent with previous RSC policies.

The motions all passed unanimously except for the last one, which Louisiana, North Dakota and Oklahoma opposed.

The RSC meets Jan. 30. Kelley said SPP plans to make the appropriate filings after the April round of governance meetings.

“We have to ensure we’re in lock-step with MISO and its processes,” he said.

GI Queue Continues to Expand

The JTIQ work will only result in more generation interconnection requests as SPP staff continue to work on reducing the backlog of requests in its queue.

Kelley said the SPP and MISO queues have grown since the JTIQ work began, with no end in sight.

“While we’ve made significant progress in clearing our existing backlog, there continues to be significant interest in developing new generation, both within the SPP footprint as well as MISO’s,” he said.

The backlog, which once stood at 651 requests and nearly 120 GW, had been reduced to 370 and 68.2 GW, respectively, in mid-December. However, the 2022 study cluster that closed in early January added 53.8 GW of requests, pushing the backlog to about 122 GW.

Many of those requests have yet to be validated by staff, leaving the active queue at 463 requests and just over 88 GW.

“It’ll take a couple of months to evaluate the impact of this cluster. It’s really, really big,” SPP’s Juliano Freitas told members, noting that the 2022 cluster exceeded forecasts by about 10 GW.

He said the new cluster is about 50% solar and 25% wind, in line with the active queue. Solar requests (39.2 GW) account for almost half the queue, with wind requests at 23.1 GW and storage at 12.9 GW.

SPP currently only has about 250 MW of installed solar capacity, said Casey Cathey, director of system planning. “That is kind of our next frontier.”

Freitas said that considering only about 40% of GI requests result in signed interconnection agreements, SPP could add more than 45 GW of capacity by 2028. The grid operator has added 27.7 GW of capacity since January 2017, executing 143 GI agreements.

Members Defer on PRM Deficiency RRs

The committee deferred action on a pair of revision requests related to deficiency penalties by load-responsible entities unable to meet the grid operator’s new 15% planning reserve margin (PRM).

Following late changes to the two requests by stakeholder groups the night before the MOPC meeting began, committee members agreed to wait until a special conference call Friday to consider the change requests. That will give additional time to several stakeholder groups who have yet to approve the proposed revisions; the committee will then be able to endorse a recommendation for the RSC and the Board of Directors when they meet next week.

SPP is hopeful FERC will approve the revision requests in time to accredit resources for the summer.

Staff have been working on the mitigation strategy at the board’s direction since July. It became necessary when the board increased the PRM from 12% to 15%, effective next year, which left some members complaining they would not have enough time to meet the requirements. (See SPP Board of Directors Briefs: Dec. 6, 2022.)

COO Lanny Nickell has said the mitigation concepts include reducing the deficiency payment charge, extending the timeline to cure deficiencies and adding mechanisms to assure capacity.

MOPC’s leadership for 2023: Chair Alan Myers, ITC Holdings; staff secretary Lanny Nickell, SPP; and vice chair Joe Lang, Omaha Public Power District. | © RTO Insider LLC

RR536, proposed by SPP’s Market Monitoring Unit, would replace the sufficiency valuation methodology’s current penalty framework with a sufficiency valuation curve similar to the curve that NYISO uses to value capacity in its market. The curve starts at twice the cost of new entry (CONE) until regional accreditation reaches the sum of total noncoincident peak loads, then slopes downward to a net CONE value when regional accreditation reaches the PRM.

When accreditation exceeds the PRM, the curve continues its downward slope until it reaches $0 when regional accreditation reaches 1.15 times the PRM. By focusing on how valuable excess accredited capacity is to the market given the regional level of accredited capacity, this methodology shifts from a punitive approach to a tool that manages the current deficiency and properly rewards LREs with excess accredited capacity.

Staff worked with the MMU on RR536 and also drafted RR537, which clarifies that an LRE making the deficiency payment will be sufficient for this year’s resource adequacy requirement. It also says that any entity receiving a deficiency payment cannot subsequently sell any of the excess capacity during the applicable calendar year.

“I think we’re getting closer. Today is too soon, given the language was only provided last night,” Evergy’s Mo Awad said. “I would like to take some time and review the language.”

Staff drew up a number of issues for stakeholder consideration, including clarifying that the waiver process is only in effect when the PRM increases; the timing of when generation must be committed to SPP, based on a deficiency megawatt amount; how the cost of new entry is broken into seasonal components; and simplifying megawatt allocation for the MMU’s CONE process.

The Supply Adequacy and Regional Tariff working groups will take up the revision requests on Tuesday and Thursday, respectively. The CAWG met Friday but did not vote on them; it has scheduled a special meeting for Wednesday.

December Storm Raises Same Issues

Staff told the committee that the December winter storm, while less severe than the February 2021 storm that forced the grid operator to shed load for the first time, still highlighted some of the same issues from two years ago.

C.J. Brown, director of system operations, said constricted fuel supplies and extreme cold weather-related outages led to some generation unavailability as surface temperatures in the SPP footprint were up to 25 degrees Celsius below historical averages.

Staff began receiving notifications on Dec. 20 from natural gas suppliers that non-firm usage of pipelines would be limited through Dec. 28. Ice floes on the Missouri River threatened several gigawatts of hydro generation, and the RTO’s main control room operated on backup power during the event after the facility’s transformer malfunctioned.

Empire Electric District and City Utilities of Springfield, Mo., near the Missouri-Arkansas border, experienced extremely low voltages on Dec. 23 caused by resource trips, lack of deliverability and parallel system flows. Empire had to shed about 25 MW of load for 15 minutes on Dec. 22.

Still, SPP was able to meet a peak demand of 47.2 GW on Dec. 22, a winter record.

Brown said that if the worst weather conditions had shifted to Dec. 23 or Dec. 24, SPP would have had 2 to 5 GW of capacity at risk.

“It doesn’t mean we would have had load shed,” he said, noting that the RTO could have reached energy emergency alert levels. “None of us want to be in a headline that says we shed load over Christmas. We need to get better information” from gas suppliers.

Midwest Energy’s Bill Dowling cautioned SPP about taking comfort in the amount of gas generation it committed before the cold front blew in.

“It’s one thing to know that [a gas unit] is committed a couple or three days in advance; … it’s something else to get the gas,” he said. “If the gas producers aren’t producing and it doesn’t show up in interstate pipeline, you’re not going to get it, I don’t care how much you paid for it.”

Josh Phillips, who represents SPP at the North American Energy Standards Board, said the board’s Gas-Electric Harmonization Forum is preparing a report on three main areas of concern during extreme weather events: fuel delivery assurance, communication practices and gas reliability.

Power generators and load-serving entities are underrepresented on the forum, Phillips said. He urged more industry participation as the final report delves into whether there’s a need to require every gas generator to have firm gas supply and transportation contracts.

Dowling said that whenever he listens to discussions between the electric and gas sectors, “it ends up, ‘This is your problem, electricity, so you have to change to meet our requirements.’”

“If [gas suppliers] declare force majeure, you just don’t get your gas,” said long-time MOPC member Bill Grant, now consulting for XO Energy. “The NAESB agreement needs teeth if they don’t perform, that’s the answer.”

Brown said staff will complete its post-event review and gather lessons learned, while also participating in the FERC-NERC joint inquiry on the storm. They will continue to support resource adequacy efforts through the RSC and other stakeholder groups.

Members Endorse ITP Scope, STEP

The committee endorsed two stakeholder groups’ recommendation to approve the 2024 Integrated Transmission Plan’s scope, which includes assumptions not standardized by the ITP manual.

SPP’s Casey Cathey (left) catches up with long-time MOPC member Bill Grant, who represents XO Energy on the committee. Grant retired last June after 40 years with Xcel Energy, 16 of those on MOPC. | © RTO Insider LLC

SPP’s Casey Cathey (left) catches up with long-time MOPC member Bill Grant, who represents XO Energy on the committee. Grant retired last June after 40 years with Xcel Energy, 16 of those on MOPC. | © RTO Insider LLC

The assessment will study two futures — a reference case and an emerging technologies case — that assume between 49.9 and 54.9 GW of wind resources and between 14 and 22 GW of solar resources by Year 10. SPP currently has 32.5 GW of installed wind capacity and 14,000 turbines on its system, but only about 250 MW of solar, Cathey said.

The scope also includes peak and energy increases in both futures to account for electric vehicle growth and an approved methodology for retirements based on participants’ resource plans. Staff used those plans to also determine wind, solar and storage capacity amounts. The study scenarios will assume all companies meet the PRM.

“We believe the two futures capture the necessary scenarios for building out the transmission system,” Cathey said.

The committee also endorsed the SPP Transmission Expansion Plan (STEP), a comprehensive list of all transmission projects over a 20-year planning horizon. The report indicates that SPP members completed eight upgrade projects costing more than $40 million from last April to year-end. SPP issued 76 notifications to construct (NTCs) for $822 million during the same period; 12 NTCs were withdrawn.

Cathey reminded the committee that the 2022 ITP assessment was a reliability-only study, thus resulting in a smaller portfolio.

RAS Scheme Passes

The committee unanimously approved a consent agenda that included eight revision requests; an extension of the Transmission Owner Selection Process Task Force’s sunset to Jan. 31, 2024; a waiver request to include the 2023 ITP needs assessment’s market powerflow models (MPMs) and consider the 2023 ITP MPM violations in the 2024 ITP; and a sponsored upgrade study of NextEra Energy’s proposal to add a 345/138-kV transformer at Oklahoma Gas & Electric’s Cimarron substation.

Nebraska Public Power District had RR505 pulled off the agenda for a separate vote, over concerns that the remedial action scheme (RAS) criteria would lead to unintended consequences. The change would supplant the need for approval conditions and clarifies RASes’ appropriate uses. Members approved the revision request with a 95% vote.

Five other RRs, if approved by the Board of Directors next week, would:

- RR519: formalize the SPP operating criteria’s requirement to perform an annual resource real-time availability evaluation and report findings and recommendations to appropriate stakeholder groups.

- RR522: clarify the use of the word “separately” (“Each facility must be registered separately with SPP…”) to direct parties in the agreement to register each facility separately when they have multiple resources involved with the pseudo-tie agreement.

- RR523: modify existing pro forma generator interconnection agreements and language to provide a clearer indemnification standard with clearer language. The changes are modeled on PJM’s interconnection service agreement.

- RR526: specify that a resource or an aggregation must be able to maintain a response of at least 0.1 MW for at least an hour to participate in the Integrated Marketplace; if the anticipated response drops below 0.1 MW, the resource must set its commitment status to “outage,” consistent with recent FERC orders and SPP’s current process.

- RR528: clean up Business Practice 7060 by using “evaluation” rather than “study” for projects that have been issued an NTC, aligning the term with how it is used when an NTC is re-evaluated through the ITP.

The consent agenda also included two other RRs that don’t require board approval and go into effect immediately:

- RR525: deletes Business Practices 7100 (Designated Transmission Owner Qualification Process) and 7150 (Transmission Owner Selection when a Designated Transmission Owner Rejects a Notification to Construct), which became obsolete with the implementation of SPP’s competitive transmission selection process.

- RR529: the annual cleanup to correct grammar, punctuation and acronyms in the production and/or forward looking protocols.