The Department of Energy and FERC already have enough authority to site necessary transmission lines under existing laws even without additional congressional action, the authors of a paper on the subject said in a webinar Monday.

Two of its authors, Isabel Carey, an associate at Marten Law, and Justin Gundlach, an attorney at the Building Decarbonization Coalition, spoke during the webinar hosted by ELI and the law school.

The article was published just as the national conversation around transmission was starting to shift, Gundlach said.

“Failing to develop more regional and interregional transmission capacity would mean leaving the power sector’s shoelaces tied together and constraining burgeoning efforts to build clean energy capacity,” he said. “This was true when we started writing our article years ago. But it is even more true now.”

The Inflation Reduction Act offers voluminous incentives to clean energy that are expected to accelerate the pace of renewable development, but ensuring that happens requires grid expansion, he said.

The Biden administration is aware of that, and the paper’s other two co-authors are now working at the U.S. Department of Energy: Sam Walsh is the agency’s general counsel and Avi Zevin is a deputy general counsel for energy policy.

The federal government has had backstop siting authority since the Energy Policy Act of 2005, but that tool had been collecting dust on the shelf for years until recently. The law allowed DOE to designate National Interest Electric Transmission Corridors (NIETCS), and FERC was given authority for backstop siting in the absence of state action.

The first attempt to implement the policy drew very wide corridors covering huge swaths of Southern California and the entire Mid-Atlantic, said Carey.

The U.S. 9th Circuit Court of Appeals found in California Wilderness Coalition v. U.S. Department of Energy that the agency had insufficiently coordinated with the states in determining the broad NIETCs. The court also said DOE failed to study the NIETCs’ environmental impacts as required by the National Environmental Policy Act, Carey said.

“Both of these were procedural errors that could have been fixed with additional time and resource devotion,” Carey said. “But DOE abandoned any attempt to re-designate the two quarters and has not attempted any designations since.”

The 4th Circuit limited FERC’s authority in a 2009 decision in Piedmont Environmental Council v. FERC, which found the commission could not overturn a state’s denial of a transmission line in an NIETC. That was fixed in the Infrastructure Investment and Jobs Act of 2021, which reversed the court’s finding and gave FERC the authority to approve national interest lines rejected by state regulators, said Carey.

FERC cannot act until states have a year to review transmission, but it is able to review proposals at the same time as states, which is a much more efficient process, she added.

“To address one of the problems that the failed corridor designations faced, our paper suggested that national corridors should be designated more narrowly, ideally with specific projects in mind,” Carey said. “By focusing the designated corridors, we could better tee up projects to apply for citing permits.”

AUSTIN, Texas — Infocast’s 11th ERCOT Market Summit last week attracted about 600 attendees, primarily financiers and developers, eager to gain insight into the Texas grid operator’s new products and services addressing reliability, the state’s increasing load, and emerging policy and market challenges.

Given the potential changes to how providing power is rewarded, much of the discussion centered on the performance credit mechanism (PCM), the Texas Public Utility Commission’s preferred market redesign for ERCOT.

The PCM would reward generators in ERCOT’s energy-only market with credits based on their performance during a determined number of scarcity hours. Those credits must either be bought by load-serving entities or exchanged between them and generators in a voluntary forward market. (See Texas PUC Submits Reliability Plan to Legislature.)

Most speakers expressed opposition to the construct. Others offered support.

Asked how he could be sure the untested PCM would incent gas-fired generation, as favored by the state’s lawmakers and regulators, ERCOT CEO Pablo Vegas said the market mechanism is really nothing new.

“The PCM is actually a fairly well understood set of tools that the ERCOT market and its participants have been using in different forms for many, many years,” he said, noting it can be broken down into three main components: a forward auction, a supply-and-demand curve and a backward settlement for performance during the performance period.

“We’re taking those three components and we’re putting that together. So, I think the argument that it’s too novel is really not well founded,” Vegas said. “Texas has created some of the most novel concepts in the history of energy markets. The energy-only market created back in 2000 was the first of its kind and continues to be one of the most innovative markets in the world. We have experience doing things that are completely new and different and seeing success from it.

“I think it will be well understood. I think it will incentivize generation because markets work. We have the history of knowing the markets work, when there are significant distortions that change the way those markets work, and you see issues on the market. And that’s what we’re dealing with today. Markets will work if they’re designed in a way that can be understandable.”

Campbell Faulkner, a senior vice president with over-the-counter energy commodity broker OTC Global Holdings, was asked whether the PCM market would turn into a capacity market, as some fear. He said the construct is unlikely to result in an optimum solution for everyone.

“You’re trying to marshal the quasi-governmental aspects of ERCOT with the state legislature and the end-use constituents. … It’s going to end up being filtered through the state representatives … to determine are you willing to pay more for a liability or a preference to paying less but having more frequent outages,” he said.

“Capacity markets, in general, are complicated. You’re essentially trying to ensure that you not only have fleet reliability, but you have dispatch reliability and often you have congestion reliability. The ERCOT system worked exceptionally well for most of its design life, largely because it did have a relatively high price cap. There are economic arguments that say there shouldn’t be a price cap at all to generate every single marginal megawatt. These things are all going to basically have to be relitigated.”

“If you look at other capacity market constructs … there are price mechanisms and price structures that help support debt financing for projects,” EIG Partners’ Shalin Parikh said. “When you look at the way the PCM has been proposed, I don’t foresee it being a structure that will support or that lenders will underwrite to.”

Parikh said capacity markets are “largely based on creating availability, covering your fixed costs and potentially servicing some of that financing that you have raised to build those projects.”

“From that standpoint, I would say ERCOT likely will not be viewed as a capacity market construct, even if that is the intention of the mechanism,” he said.

Katie Coleman, an attorney who represents industrial consumers, was asked what reliability problem the PCM is trying to solve as part of the PUC’s Phase II market redesign. Phase I included weatherization requirements, revisions to the operating reserve demand curve and additional ancillary services in the aftermath of the February 2021 winter storm.

“I view Phase II as an effort to try to exert more control over what investment decisions are made in a deregulated market,” she said. “This is at least the fourth time that we’ve been through this argument about whether we should impose a capacity construct on the market. I think when you are sitting in the seat as a regulator or a legislator who has responsibility for reliability, it is very attractive to try to impact market outcomes through administrative measures.

“We do believe that there are mounting operational issues in ERCOT that need to be addressed in a more tailored way,” Coleman added. “And my clients believe that it’s worth spending more money to do that, but they do believe that additional services and tools are needed to manage particularly renewable variability.”

Shell Energy North America’s Resmi Surendran said U.S. Energy Information Administration data on resource retirements and investment shows ERCOT’s energy-only market is sending the right signals to the financial community. She said the capacity markets in PJM and MISO have resulted in a combined 140 GW of investment against 77 GW of retirements, according to the EIA data.

“ERCOT has had 48 GW of investment in thermal resources in the last 20 years, but only 18 GW of retirement. That means ERCOT has load growth that is incentivizing generation,” she said. “The energy market is sending the signal that is needed for investment.”

Emily Jolly, associate general counsel for the Lower Colorado River Authority, listened to her fellow panelists and said she was noting the issues they raised and thinking about how to respond to them.

“I think the problems that we’re looking to solve in the market are, we don’t need payday loans. We don’t have a problem getting financing for the additional capital construction,” she said. “I think it’s important for us to look at the revenues that dispatchable generators are actually receiving in the ancillary services markets today. We’ve seen a lot of short-duration battery storage participating in those markets and getting increasing shares of those revenues. Those are not the kinds of resources that are going to get us through another multihour, multiday event, but I think that’s a tradeoff that we all need to be aware of.”

Study: PCM a ‘Major’ Market Overhaul

Aurora Energy Research’s Oliver Kerr shared his firm’s analysis of the PCM, saying it represents a “pretty major overhaul of the market” and that all its versions lead to a “pretty substantial shift away from scarcity value towards PCM credit.”

“I don’t think it’s an exaggeration to say that the PCM actually represents a pretty fundamental paradigm shift in how assets are remunerated in Texas,” he said. “You’re really seeing a pretty key shift away from revenues driven by energy scarcity value towards reliance on capacity payments.”

Aurora studied an illustrative PCM implemented in 2027, with credits paid for the 20 highest hours of peak net load. The firm modeled four scenarios based on renewables eligibility and the top 20 reliability hours determined seasonally versus annually. All the scenarios led to an increase in capacity, with more added when renewables were not eligible, Kerr said.

The researchers determined that excluding renewables leads to more new build capacity because fewer credits are generated. That increases the credits’ price and leads to the buildout of more peakers and batteries. Aurora found the PCM does benefit solar in all scenarios in that it sees increased capacity relative to the base case because of higher battery buildout; batteries increase solar gross margins by charging during solar production.

“All scenarios that we modeled led to an increase, a significant increase, actually, in dispatchable generation or capacity across the board,” Kerr said. “Fewer renewables means fewer credits are generated, which means that the price per credit is high as it grows to other technologies.”

Vegas Says ERCOT at Crossroads

Juliana Sersen, a 10-year veteran of ERCOT’s legal department and now a partner in the Baker Botts law firm, introduced CEO Vegas’ keynote speech by telling the audience, “I can tell you what ERCOT used to be like, but here’s someone who knows what it will be like in the future.”

“We find ourselves today at a crossroads. Facing us are a series of choices that could lead us into a prolonged season of stagnation and frustration, or continue ERCOT on a trajectory of innovation, competition and economic growth,” Vegas said in his opening comments. “As [Texas] legislators revisit the laws that they passed in 2021 and they debate the nature of their ongoing implementation going forward, I can’t think of a more important conversation or more significant way for us to spend our time today.”

Labeling ERCOT as “the nation’s only independent state grid,” he said the deregulated market’s track record is “unmatched” and its competitive edge and opportunity is “enormous.”

Vegas referred to the “false binary of renewables-only strategies” as he discussed the need for more dispatchable generation. ERCOT has seen more than 27 GW of thermal generation retire since 2000 and added more than 52 GW of renewable generation during that same time. The grid operator’s peak load exceeded 80 GW last year, more than a 5-GW jump in three years, he said.

“Are we doing what it takes to add the generation that we need before Mother Nature decides to test us again?” Vegas asked.

He assured his listeners that renewable energy remains a part of the mix as he answered a question about whether they should be excluded from the PCM.

“I think that we need to have performance criteria that creates a very dependable, responsive set of generating assets that can deliver earnings in that market,” Vegas said. PCM “is a separate market. … The energy-only market continues to operate the way it does today. All the benefits that renewables get today under the current energy on the market are going to continue to exist, so I think renewables will continue to have all the incentives that they have had historically to continue to develop.”

Political Influence Concerns Developers

A panel on ERCOT’s “new normal” in a future of volatile gas prices, increasing renewable penetration and exponential load growth debated the heavy hand of politicians following the February 2021 winter storm. The PUC commissioners at the time are all gone, replaced by Gov. Greg Abbott appointees, and the ERCOT board has replaced market representation with independent directors selected by a political committee.

The current market redesign work has only heightened fears of renewable developers that wind and solar will face stiff headwinds.

“I’ve been working in solar and ERCOT for a number of years now, and it definitely feels like it’s changing,” Lightsource BP’s Helen Brauner said. “The demand thankfully is greater than it’s ever been, so that’s a very positive trend and change. It’s a great market for solar, but it kind of feels like there’s additional pressures afoot.”

Brauner said that while ERCOT is on track to add 8 GW of solar-powered capacity this year and Texas is expected to overtake California as the No. 1 state for solar power, she is noticing political pushback against renewable energy. Referring to a recent bill filed at the legislature “with some really egregious time terms,” she said, “That just didn’t happen before, so I’m a little nervous about seeing things like that.”

Julia Harvey, vice president of government relations and regulatory affairs for Texas Electric Cooperatives, agreed with Brauner.

“I’m not the first to observe this, but maybe the trend towards politicization of the stakeholder process has always somewhat been the case because of the unique nature of electricity. You can’t just design a market purely based on economic ideals,” Harvey said. “There’s always other motivations, but since the [2021] winter storm, I think there’s been a more pronounced movement away from this kind of stakeholder-driven, more sort of technocratic policymaking to something that’s more top down, and I think that can create some sense of instability for market participants.”

“I feel like things are getting kind of political, and that concerns me,” Brauner added. “All these different generation resources have different pros and cons to them, and I just don’t want ERCOT or the politicians to pick and choose generation. Just lay out what we need, and let the resources figure out what they need to make money. That’s how it’s always been. … I just hope that continues.”

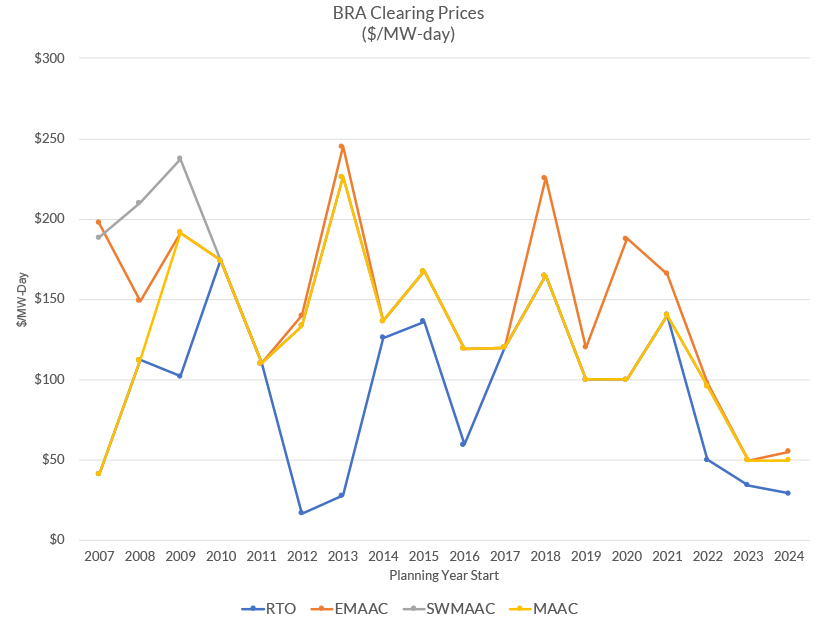

PJM capacity prices dropped in much of the RTO for delivery year 2024/25, but ratepayers in five regions will face increases due to locational constraints.

PJM said its overall capacity bill will be unchanged at $2.2 billion as prices in the “rest-of-RTO” dropped 18% to $28.92/MW-day from $34.13 for 2023/24. But prices in the Base Residual Auction were considerably higher in five regions, an increase from three regions that saw price separation in the previous auction:

DEOK (Duke Energy Ohio and Duke Energy Kentucky): $96.24;

DPL-South (Delmarva Power south of Chesapeake & Delaware Canal): $90.64;

MAAC (Met Ed, Penelec, Pepco, PPL): $49.49;

Eastern MAAC (Atlantic City Electric, Delmarva Power North, Jersey Central Power & Light, PECO, PSE&G, and Rockland Electric): $54.95; and

BGE (Baltimore Gas and Electric): $73.

Constrained LDAs

“We continue to see indications that … some locational deliverability areas are increasingly constrained,” PJM Senior Vice President of Market Services Stu Bresler said in a press conference after the results were released Monday afternoon.

“The congestion is really due to the combination of the available transmission into the locational deliverability area, along with the available resources and the offer prices of those resources in those constrained LDAs,” Bresler said. “It’s really an indication that we need to commit higher cost resources there than we did in the rest of … the RTO, in order to maintain reliability. So it’s not necessarily an indication that we are or will be short, in that area. Certainly none of these LDAs got anywhere close to the maximum price on the demand curve.”

While none of the LDAs were near the maximum price cap in each of the zones’ variable resource rate (VRR) curve, the report notes that all five had less than 5% supply offered in excess of the megawatts that cleared the auction.

PJM said prices in DPL-South would have been four times higher had FERC not accepted the RTO’s proposal to address a “mismatch” between the resources included in the calculation of the LDA’s reliability requirement and those that entered the auction.

Supporters of the proposal, largely public utilities and state advocates, said it protected ratepayers while keeping the market in line with supply and demand, while generation owners decried the order as undermining confidence in the markets and a violation of rules against retroactive ratemaking. (See FERC OKs PJM Proposal to Revise Capacity Auction Rules.)

‘Healthy’ Margin vs. Retirement Concerns

Although the RTO said it will maintain a “healthy” reserve margin at 20.4%, officials expressed concern at a 2,198-MW drop in offered capacity, the third year in a row that saw a reduction. Bresler said the reduction in offered supply was almost all comprised of fossil fuel units, mostly coal-fired generation, which saw a 2,050-MW decrease in offers. Demand response, hydro and wind saw more modest declines.

“If this trend continues, it represents a potential concern for long-term resource adequacy, depending on the rate of replacement of these resources,” PJM said.

A white paper published by PJM last week warned of reliability problems within a few years if the pace of generation interconnections does not increase to match deactivations. The report states that approximately 40 GW of generation is expected to retire by 2030, while as little as 15 GW is projected to be installed at the current trajectory. The PJM Board of Managers concurrently announced that it has initiated a fast-track rulemaking process to find solutions to address the reliability concerns. (See PJM Board Initiates Fast-track Process to Address Reliability.)

Energy Market Impact

Bresler said the reduced prices in rest-of-RTO reflected higher energy market revenues driven by higher gas, oil and coal prices.

“So you would expect to see lower capacity market offers,” he said. “But we do remain concerned about market sellers’ ability to include risk in their capacity market offers, particularly learning from the events of December 23rd and 24th, where there were … quite a few performance assessment intervals, and therefore penalties that will apply to capacity resources that failed to perform.” (See PJM Gas Generator Failures Eyed in Elliott Storm Review.)

The auction results may have also been impacted by a “marginally higher” net cost of new entry used to determine the VRR curve, according to PJM’s auction report. The figure rose from 6.2% to 7.2% in the 2024/25 BRA. The RTO’s reliability requirement also increased by 236 MW up to 132,056, although the report notes there were “significant” changes to the requirement for LDAs.

“While the auction’s low capacity clearing price represents savings for customers in the short term, we continue to sound the alarm when it comes to the reality that critical generation resources needed to secure reliable electricity … are at risk of retirement,” the Electric Power Supply Association (EPSA) said in a statement after the results were announced. “The market must be designed properly and avoid rule changes intended to accommodate specific preferred resources or technologies. EPSA has long called on PJM leadership, policymakers, and regulators to address the serious foundational issues at hand, and we stand ready to continue to provide recommendations and work collaboratively to forge a solution.”

Winners, Losers

PJM procured 140,416 MW of capacity, excluding energy efficiency resources, whose impact is reflected in a lower load forecast. Fixed resource requirement (FRR) capacity plans — load-serving entities that choose to provide their own resources outside of the BRA — added 32,545 MW for a total of 172,961 MW.

Including FRR resources, PJM saw increases in cleared capacity for natural gas (+1,615 MW) and solar (+1,297 MW). Energy efficiency cleared or committed in an FRR plan increased by 2,198 MW.

In contrast, demand response (-451 MW), nuclear (-331 MW), coal (-278 MW), hydro (-237 MW) and oil (-230 MW) cleared less than in the prior auction.

New generation cleared 328.5 MW in the BRA, while an additional 173.8 MW capacity was procured from uprates to existing or planned generation, which Bresler said was a “fairly significant reduction in offers from new or upgraded generation” compared with the approximately 3,000 MW that cleared in the previous auction.

The RTO as a whole failed the three-pivotal supplier test, resulting in market power mitigation being applied to all existing generation capacity resources, resulting in the RTO utilizing the lower of the resources’ market seller offer cap or the submitted offer price when determining the resource’s RPM clearing.

In the 2023/24 BRA, prices in most of the MAAC region dropped nearly 50%, while those in rest-of-RTO fell nearly one-third. (See PJM Capacity Prices Crater.)

VALLEY FORGE, Pa. — The PJM Markets and Reliability Committee last week endorsed an RTO proposal to increase the maximum number of bids a single corporate entity can enter into financial transmission rights auctions from 15,000 to 20,000.

Market participants had complained that the transition from weekend on-peak and daily off-peak class types made it take a larger volume of bids to buy and sell the same number of hours of an FTR, according to the problem statement adopted by the Market Implementation Committee in December. The change was pursued through the RTO’s “quick fix” process, which allows a proposal to be endorsed concurrently with its issue charge and problem statement. (See “FTR Bid Limit Increase Endorsed Under Fast Track Pathway,” PJM MIC Briefs: Jan. 11, 2023.)

During the MRC’s first read of the proposal, Senior Engineer Emmy Messina said the 20,000 figure was viewed as a balance between the usage of the class types and bid submission performance. The approved manual changes will be effective for the auction occurring in March.

Updated Default CONE and ACR Figures

PJM presented a first read of the updated default gross cost of new entry (CONE) and avoidable-cost rate (ACR) formed through its Quadrennial Review.

Following advisory votes at the MRC and Members Committee, PJM is set to submit a filing with the parameters to FERC. If approved, the values will be in place for the 2026/27 delivery year.

The gross CONE for all resource types, except storage, would increase, which PJM’s Skyler Marzewski said was expected given the tendency for costs to rise, the Inflation Reduction Act’s changes to the investment tax credit and different reference resources for combined cycle and onshore wind facilities.

Stakeholders questioned the nine-fold difference between the proposed net CONE values for fixed solar panels versus those with tracking technology, which Marzewski said is attributed to the higher energy and ancillary services revenues and effective load-carrying capability rating for tracking panels.

The most significant changes to the gross ACRs proposed are the introduction of steam oil and gas as a new resource type, refined property tax and insurance costs, and expanded data from the Nuclear Energy Institute on resource costs. Single-unit nuclear generators would be the only resources to see their default ACR decrease under the proposal.

Members Committee

PJM Board to Review Monitor Contract

PJM Board of Managers Member Paula Conboy | PJM

PJM Manager Paula Conboy told the MC that the Board of Managers plans to review the RTO’s contract with its Independent Market Monitor, Monitoring Analytics.

The contract is up for renewal at the end of 2025. Responding to stakeholder questions, Conboy said that the review is to look at terms and conditions, as well as any areas that may need clarification.

“This is about the terms and conditions of the contract; this isn’t about the IMM [Joe Bowring] himself,” she told the committee. “With the evolving market and so many things changing, we just want to make sure we’re all on the same page about what’s in the contract.”

PJM General Counsel Chris O’Hara said the RTO has not engaged in a pre-emptive review or redline of the contract.

PJM’s Board of Managers is opening an accelerated stakeholder process to address rising reliability concerns about the RTO’s capacity market.

The effort includes last week’s release of a PJM white paper detailing a potential imbalance between deactivating resources and new development if interconnections do not speed up.

“Notwithstanding the efforts to date, given recent events and analyses, the Board believes near-term changes to the Reliability Pricing Model (RPM) are necessary to ensure that PJM can maintain resource adequacy into the future,” the board said in a letter to stakeholders Friday. “The Board also continues to value robust stakeholder review, input and challenge to help solve complex problems such as this.”

In invoking PJM’s Critical Issue Fast Path process, the board aims to submit a FERC filing by Oct. 1 to address many of the issues stakeholders have been deliberating in recent months. The letter also noted that FERC recently announced the opening of a forum to examine PJM’s capacity market, saying the commission’s interest underlines the need for the fast-track process and could provide a venue to vet potential solutions ahead of the potential October filing. (See FERC OKs PJM Proposal to Revise Capacity Auction Rules.)

The scope of the fast-track process includes revising the capacity performance model and how penalty risks can be accounted for in capacity offers; improving resource accreditation to ensure that reliability contributions are accounted for and compensated; and enhancing risk modeling to improve understanding of winter risk and correlated outages. The board also aims to align the RPM and fixed resource requirement rules to ensure that supply and demand are held to comparable standards.

The board will be exploring whether any potential changes it proposes should be applicable to auctions prior to the 2027/28 Base Residual Auction, which could require delays to future auctions. It has directed staff to draft possible alternative auction schedules.

“For the first time in recent history, PJM could face decreasing reserve margins … should these trends — high load growth, increasing rates of generator retirements, and slower entry of new resources — continue,” the paper states.

About 40 GW of generation is expected to retire by 2030, representing 21% of the current installed capacity, while one of the scenarios PJM identified would see only 15 GW of new resources installed. The RTO could fall below its target reserve margin by the 2026/27 delivery year and continue declining through the rest of the decade.

PJM also found that increasing data center growth and the electrification of vehicles and home heating could exacerbate the decreasing amount of capacity available by pushing its long-term load forecasts higher.

“Along with the energy transition, PJM is witnessing a large growth in data center activity. Importantly, the PJM footprint is home to Data Center Alley in Loudoun County, Va., the largest concentration of data centers in the world … In 2022, the [load analysis subcommittee] began a review of data center load growth and identified growth rates over 300% in some instances,” the white paper states. (See Policymakers Working to Meet Spiking Demand of Data Centers in Virginia.)

PJM’s estimates for new generation are based on existing projects in the interconnection queue and the historical rate for resources to reach commercial status, paired with a series of projections through 2030 from S&P Global. The low-entry scenario is based on the current rate of approximately 5% of projects entering the interconnection queue reaching commercial operation, while the high-entry alternative includes a “fast transition” model assuming “carbon net neutrality by 2050 through the IRA and additional policies.”

The pairing of the accelerating electrification projection and low-entry scenario could result in a reserve margin of 3% by 2030, while pairing that projection with the high-entry model would see a 12% margin. According to the PJM Independent Market Monitor’s third quarter State of the Market Report, the 2023 installed reserve margin target is 14.8%, far exceeded by the projected reserve of 21.6%.

PJM said the reliability risks underline the need to continue its work on changes to its capacity market, interconnection process and clean energy procurement, while embarking on “combined actions to de-risk the future of resource adequacy while striving to facilitate the energy policies in the PJM footprint.”

The 40 GW of deactivations is largely attributed to government and private sector policies, with an estimated 25 GW due to various on-the-book and proposed policies. A further 12 GW of retirements are either underway or announced over the next few years and another 3 GW is estimated to be due to economic reasons.

Monitor Joseph Bowring said he agrees with PJM’s assessment of the scale of policy deactivations and pace of resource development; however, he believes PJM is underestimating the likely number of economic retirements by understating the avoidable cost rate he believes generators are likely to face.

He also believes PJM is overstating the amount of capacity available by including demand response and by using an inaccurate approach to calculating the capacity provided by renewable resources.

“An essential part of addressing expected reliability issues is to identify the expected sources of new generation. That resource mix will include both renewables and gas-fired generation, but PJM needs to focus on exactly how new generation will meet peak loads,” Bowring said. “There are a lot of resources in the queue, but the question is whether they will provide reliability when it is most needed, including the expected performance of renewables and the adequacy of firm gas supply.”

Bowring believes the first step PJM must take is to modify the current capacity market design, including eliminating extreme penalties from the capacity market, relying on energy market incentives and adding firm fuel and testing requirements to ensure reliability during cold- or hot-weather emergencies. To support the first recommendation, he pointed to the $1-$2 billion estimate of the capacity performance penalties generators are facing from the Dec. 23 winter storm.

“The extreme penalties in the current capacity market design create an administrative process that adds unacceptable uncertainty to the process and that can never approach the effectiveness of the energy market in providing price signals and timely settlement,” he said. “There is no reason that in a rational market design, less than 24 hours of cold weather would result in a crisis and a level of administrative complexity that threatens to undermine the incentives to invest in existing and new supply resources at a time when those resources are needed. The current capacity market design undermines incentives rather than creating positive incentives to invest and perform.”

While he’s glad to see PJM directly discussing future reliability more often, Bowring said he does not believe the best approach is to take the response out of stakeholders’ hands through the board’s fast-track process.

Tom Rutigliano, senior advocate with the Natural Resources Defense Council, said the report shows that new resource development is key in addressing a critical risk a few years away.

“To be clear: the problem for 2030 is PJM’s project completion rate for new renewables and transmission, not the retirement of polluting, high-emitting plants,” Rutigliano said. “It is PJM’s responsibility to identify worst-case scenarios with time to avoid them, and this report highlights the urgent need to remove barriers to new supply in PJM. PJM and states now must work together to rapidly speed interconnection, get needed transmission upgrades built, and fix rules that keep supply from other regions and new technologies from supporting reliability.”

PJM Power Providers (P3) President Glen Thomas said recent actions by PJM and FERC have undermined both the capacity market and the reliability it’s meant to provide. In particular, he said the commission’s order last week accepting PJM’s proposal to revise the reliability requirement of locational delivery zones under specific circumstances follows a pattern that is “not only unsupportive of competition, but directly damaging to markets and market participants’ confidence in them.”

“The results of the report are not surprising,” Thomas said. “Reliability will be compromised when demand is increasing and state and federal policies are actively promoting the retirement of resources that are needed to maintain reliability. Not mentioned in the report is the significant impact that PJM and FERC actions to undermine the capacity market, PJM’s tool for ensuring reliability, have had to drive investors away from PJM. That represents a direct threat to reliability and will cost consumers more money than they should be paying for that reliable supply of power. PJM is headed toward a bad spot, and it’s going to take a collective effort to make sure we don’t get there.”

SPP said Monday it has selected Deborah Sterzing, who has more than 20 years of experience in finance and electric industry financial planning, as its new CFO. She replaces Tom Dunn, who retired in December after 21 years with the RTO. (See “CFO Dunn Retires,” SPP Board/Members Committee Briefs: Oct. 25, 2022.)

Sterzing will be responsible for developing and executing SPP’s overall financial strategy, aligning it with the RTO’s vision and objectives. She previously served as CFO of Wind Energy Transmission Texas and has also held financial roles at Citigroup, High Bridge Energy Development, Skaia Energy, Green Mountain Energy and General Electric.

“[Sterzing’s] strategic, financial and regulatory expertise will ensure SPP has the organizational readiness necessary to lead our industry to a brighter future,” SPP CEO Barbara Sugg said.

Compromise bills that will change how utility rates are regulated in Virginia sailed through both chambers of the General Assembly during the last day of its session Saturday.

The legislation, which was passed nearly unanimously, is backed by Gov. Glenn Youngkin (R) and the state’s largest utility, Dominion Energy (NYSE:D).

The legislation removes some rate riders and will set Dominion’s return on equity at 9.7%, which is about halfway between the current 9.3% and the 10.03% in an earlier version of the bill. That rate will be in effect later this year until 2025, when the State Corporation Commission will set its rates, freed from basing them on a peer group of its fellow Southern utilities that had been the practice in Virginia for more than a decade.

“I applaud the legislators who took the lead on writing and negotiating this landmark bill, which will save customers money on their monthly bills, restore the independent oversight of the State Corporation Commission and support the long-term stability of Virginia’s largest electric utility,” Youngkin said. “Today, the General Assembly came together and put Virginians first.”

Senate Majority Leader Richard Saslaw (D) | Virginia Senate

The companion bills — SB 1265, introduced by Senate Majority Leader Richard Saslaw (D), and HB 1770, introduced by Del. Terry Kilgore (R) — cleared the Senate unanimously in votes Saturday and only drew one opposing vote in the House of Delegates from Del. Dave LaRock (R).

“What we got here today, though, finally is a good, well rounded deal,” Kilgore said. “A deal that’s good first and foremost, for Virginians. And a deal that’s good for Dominion, a utility whose health that we need to deliver energy reliably.”

The bill shifts $350 million from rate adjustment clauses into the base rates and spreads $1.7 billion in fuel costs that Dominion has incurred because of recent price rises over 10 years, Saslaw told his fellow senators as they debated the bill on the floor.

“Instead of getting a $17/month increase on July 1, it won’t happen,” Saslaw said. “It’ll be pennies more to the average bill as a result of being able to spread it out like that.”

Getting rid of the rate adjustment clauses will save the average customer between $6.50 and $7/month, he added.

The bill also includes changes to Dominion’s “rate collar,” so that if the utility over-collects by more than 70 basis points on its ROE, 85% of the excess will return to customers; if it over-collects by 150 points, all of it goes back to consumers.

“We’re going to vote on a bill that was not dictated to us by Dominion Power, but rather it was people working together from different viewpoints: the ratepayer viewpoints, the power company viewpoint, the industrial consumer viewpoint, even environmentalist viewpoint,” Sen. John Chapman Petersen (D) said. “Not everybody got what they wanted. But you didn’t have one entity dominating the conversation.”

Senate Minority Leader Thomas Norment (R) pushed back on the notion that Dominion dictates the commonwealth’s electricity policies, noting that major corporations were behind the push to deregulate the electric industry more than two decades ago; years later, many of them also supported legislation stopping retail deregulation from going into effect.

How the law gets implemented is ultimately up to the SCC, but it only has one member now, and the legislature did not address the two vacancies, Sen. Scott Surovell (D) said. Currently the SCC only has Jehmal Hudson serving as a commissioner after Judith Jagdmann stepped down, and the legislature did not reappoint Angela Navarro, who had finished out Mark Christie’s term after he left to join FERC.

Surovell had introduced SB 1482, which would have added a fourth commissioner to the SCC, then eliminated that position when the next vacancy occurred, in an effort to break the logjam at the legislature.

“In order for somebody to be looking out for the little guy, we have to have a regulator that’s ready to follow through on all the discretion that’s been given under this bill,” Surovell said. “And right now, there’s only one commissioner sitting on the SCC and there’s two vacancies. And that’s not getting resolved today.”

Dominion welcomed the legislation’s passage, calling it a win for consumers and regulatory oversight.

“It will lower electricity bills for our customers, reduce the impact of rising fuel costs and strengthen SCC oversight,” a utility spokesman said in a statement. “We appreciate the leadership of the patrons, Gov. Youngkin, Attorney General [Jason] Miyares and lawmakers from both parties in getting this bipartisan legislation across the finish line.”

One of the early drivers in the effort to site floating power generation off the U.S. coast outlined a plan last week to continue its early work, enlarging its economy and shrinking its carbon footprint in the process.

The Maine Offshore Wind Roadmap is the result of 18 months’ work by 96 committee members studying the concept from every angle.

Much of the roadmap boils down to core concepts: gathering data; collaborating on plans to use the data; communicating those plans; minimizing adverse impacts and maximizing benefits of those plans; and ensuring those benefits are shared equitably.

Bringing those concepts to fruition is where the challenges and disagreements will crop up, and the roadmap seeks to prevent as many of them as possible.

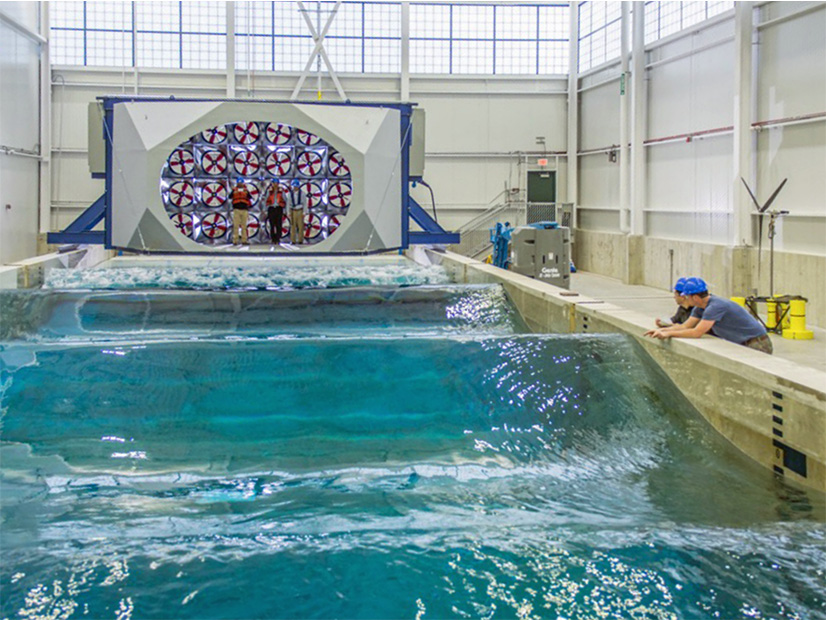

Speaking to the U.S. Department of Energy’s Floating Offshore Wind Shot Summit on Thursday, after her Energy Office released the roadmap, Gov. Janet Mills cited all the groundwork Maine has done to prepare for the effort, including placement of the first test turbine in U.S. waters.

The University of Maine…s Alfond W2 Wind-Wave Ocean Engineering Laboratory is shown. | University of Maine

“Maine has the tremendous potential to become a global leader in offshore wind, and that means more good paying jobs, cleaner energy and a healthier environment,” she said. “We’ve already started the work to get us here as well.”

With its strong and sustained winds, the Gulf of Maine is considered one of the best potential U.S. sources of offshore wind energy. But it is too deep for wind turbines with rigid sea-floor foundations, so development there will rely on floating turbines, a concept still in development.

Meanwhile, a large part of Maine’s economy is linked to its oceanfront and fishing industry, which are anxious to avoid harm from placement of wind power arrays. In response, Mills in 2021 signed into law a 10-year moratorium on offshore wind development in state waters, pushing the nascent industry farther out into federal waters.

Outsized Plans

Large states such as California, New York and New Jersey have been one-upping each other with high-megawatt offshore wind goals, but small states such as Maine and Rhode Island (whose combined population is one-eighth New York’s) are also contributing to the growth of the sector.

The first few fixed-base offshore wind turbines in the U.S., in Rhode Island waters, have yielded empirical knowledge that can be incorporated into future projects, and Maine has been researching floating offshore wind (FOSW) technology for more than a decade.

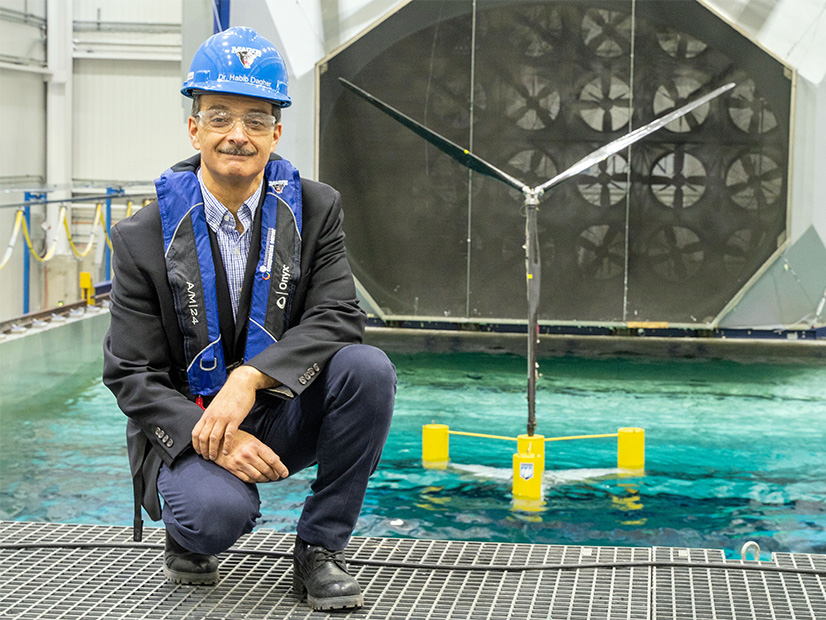

The University of Maine’s Advanced Structures & Composite Center has developed VolturnUS, a semisubmersible concrete hull for FOSW applications, and hopes to commercialize it. The center’s executive director, Habib Dagher, told the FOSW summit Thursday that it shares technology with bridge construction and can be manufactured in local communities. A decade ago, the university placed a 1:8 scale test turbine off the coast at Castine.

Habib Dagher, executive director of the Advanced Structures and Composites Center at the University of Maine, poses at the Alfond W2 Wind-Wave Ocean Engineering Laboratory. | University of Maine

In 2024 the university and its partners plan to anchor a single 11-MW floating turbine near Monhegan Island. This will pave the way for a planned research array of 10 to 12 FOSW turbines, with a capacity of up to 144 MW, farther out to sea. Maine hopes to gain U.S. Bureau of Ocean Energy Management approval in 2023 for the project. (See BOEM Continues Planning Process for Maine OSW.)

The university also has reported advances in floating light detection and ranging technology, synthetic mooring lines and 3D printer fabrication of components. It has built a wind-and-wave test basin, expanded its FOSW engineering team to 45 people and added graduate student concentrations in offshore wind.

Maine is known for harsh winters, and its residents are more dependent on heating oil than any other state. The state’s decarbonization efforts and Mills’ goal of 100% clean energy by 2040 are expected to double the state’s power demand.

Against this backdrop, the state considers FOSW a source of both new energy and economic stimulus: Nearly 80 Maine firms already are engaged in or are poised to enter the offshore wind industry, and 117 occupations would be involved to some degree in a buildout, the roadmap states.

Objectives and Strategies

The roadmap and the supporting technical reports are posted on the Maine Offshore Wind Initiative website. The roadmap breaks out five broad objectives and suggests several strategies for achieving each:

boost offshore wind supply chain, infrastructure and workforce investments by creating opportunity for Maine businesses; investing in port and manufacturing infrastructure; attracting workforce; ensuring workforce opportunity and inclusivity; and developing export opportunities for businesses and research institutions.

harness renewable energy to control costs and fight climate change by establishing a FOSW procurement and coordinating it regionally for cost effectiveness; pursuing regional transmission strategies; ensuring a stable and predictable investment environment; and advocating for federal leasing mechanisms that support Maine’s goals.

advance Maine-based innovation to compete nationally and globally in offshore wind by continuing development of FOSW demonstration projects; commercializing the state’s R&D capabilities; establishing an in-state FOSW innovation hub; leveraging and expanding in-state capabilities in artificial intelligence, data science and robotics; and researching complementary technology such as energy storage and clean fuels.

support Maine’s seafood industries and coastal communities by seeking engagement and integrating technical feedback from fishers and residents; promoting open research and data-gathering; learning from information yielded by research turbines; seeking to avoid or minimize conflicts by prioritizing development outside key lobster and fishing areas; designing wind farms to ensure safe navigation; and promoting fair and equitable benefits.

protect the environment, wildlife and fisheries ecosystem in the Gulf of Maine by collecting high-quality data in cooperation with fishers, scientists and others; proactively reducing conflicts and minimizing impacts while facilitating timely permitting; strengthening Maine’s policy framework, including through the review authority conferred by the federal Coastal Zone Management Act; enhancing collaboration with other states in the gulf; continuing state funding and pursuing federal funding; facilitating open engagement and integration of technical advice; and promoting and advancing new technologies, then allowing for their integration into planning.

Texas politicians are making a last-ditch push to avoid the retirement of a 37-year-old coal plant in East Texas that they say has another 22 years of useful life.

However, there may be little they can do.

The plant in question, Southwestern Electric Power Co.’s (SWEPCO) (NASDAQ:AEP) Pirkey Plant, was scheduled for retirement in 2020 to comply with environmental regulations. The plant, a 580-MW coal-fired unit in SPP’s eastern Texas footprint, went into operation in 1985 and will cease operations in March.

In a letter to the Texas Public Utility Commission earlier this year, 13 state senators called on the commissioners to delay approving SWEPCO’s pending rate-increase request for renewable generation until they can determine whether there is a “legitimate” reason for Pirkey’s early retirement.

The lawmakers said that the analysis SWEPCO relied upon in deciding to retire the plant was “seriously outdated and … seriously flawed.” They cited testimony in the utility’s rate case docket that “called into question” the economic and environmental regulatory assumptions used to make the decision (53625).

Sen. Bryan Hughes (R), who signed the letter, chairs the State Affairs Committee that held a hearing on Pirkey last year, and his district includes the plant’s site. He made an impassioned plea for its survival during a surprise appearance at the PUC’s most recent open meeting.

He said the lawmakers’ ask of the commission was very simple: to consider their letter and intervene in the proceeding.

“We want to make sure this decision is being made in the best interest of Texas and Texas ratepayers and folks who need that electricity,” Hughes said. “These folks happen to be outside of ERCOT, but they’re inside Texas. You have much more authority outside of ERCOT as far as regulating these companies.

“Slow this process down. You have the power to do it. And if you don’t, it’ll be too late,” he added.

PUC Chair Peter Lake thanked Hughes for his attendance and “highlighting the urgency of the issue,” but he offered no other support. The commissioners did not discuss the issue during the open meeting.

Texas State Sen. Bryan Hughes makes his case before the PUC. | AdminMonitor

PUC spokesperson Ellie Breed declined to speculate on the commission’s decision. “Staff is reviewing the situation and the concerns raised by Sen. Hughes,” she said.

Hughes’ appearance before the PUC caught some by surprise.

“It kind of came out of left field. … We were all a little bit caught off guard by it coming up in a discussion about ERCOT market design,” said Katie Coleman, who represents Texas Industrial Energy Consumers, an intervenor in the SWEPCO docket. “I’m not sure who he had talked with in advance of that, but I think that the narrative around the need for dispatchable resources caught [Hughes’] attention.”

In their letter, the senators say the State Affairs hearing “uncovered evidence about the coercive ‘manage-down-to-zero’ [environmental, social and governance] practices” of American Electric Power’s top three shareholders. AEP is the parent company of SWEPCO, which also services portions of Arkansas and Louisiana. According to Bob Eccles, an ESG expert, Vanguard Group, BlackRock and State Street own a collective 20.5% of the organization.

“AEP is the picture of woke capitalism and ESG virtue-signaling to the detriment of stockholders and, in this case, ratepayers. We believe that’s exactly what’s driving this decision,” Hughes told the PUC.

AEP has been open about its plans to transition to cleaner-burning fuels. It has retired or sold nearly 13.5 GW of coal-fueled generation in the last decade and has committed to achieving net-zero emissions by 2045 and an 80% reduction relative to 2005 levels by 2030.

The Columbus, Ohio-based company said it decided to shutter Pirkey and stop burning coal at the nearby Welsh Plant to comply with EPA’s coal combustion residuals rule. AEP said its actions would save customers an estimated $740 million to $1.2 billion by avoiding compliance costs and higher ongoing operating and fuel costs.

“Pirkey’s fuel costs have been rising for more than 15 years and were expected to remain higher than other similar SWEPCO plants,” spokesman Scott Blake said in an email to RTO Insider.

He said the more than 200 employees at the two plants have since elected to retire or found work elsewhere, many within the AEP system. Pirkey’s closure will also shut down Sabine Mining’s lignite mine that fuels the plant and its 130 jobs; many of its employees have also found work elsewhere.

Blake said the company followed SPP’s notification process for retiring units. The RTO requires at least a 12-month heads-up of a unit’s pending shutdown. It does not approve or reject the retirements but does conduct a study to determine whether its absence would create a reliability issue that needs a short-term mitigation or transmission solution.

“From our perspective, AEP’s plans may continue,” said Casey Cathey, SPP director of grid asset utilization.

Energy consultant Alison Silverstein, a former PUC staffer, said SPP’s opinion “is what matters for closure,” noting that the grid operator did not consider the cost impacts to SWEPCO or its customers, or “the market impacts of having that production available.”

“The whole point of being in a regional market with adequate generation and transmission capacity and a competitive market is that a utility can buy its energy from other producers in the region, rather than just having to own all of its power plants,” Silverstein said. “SPP is highly competitive and has lots of generation and transmission. The fact that they approved the Pirkey closure means they think it’s not needed for long-term grid reliability, and presumably that replacement power from the region is deliverable into the SWEPCO footprint.”

Not surprisingly, the plant’s retirement and the loss of local jobs and tax revenue have created a regional uproar. Eccles wrote a tongue-in-cheek piece for Forbes about the State Affairs hearing and Texas’ dichotomy as a state rich in renewables, yet eager to add dispatchable (i.e., thermal) generation.

In February, Wayne Christian, a member of the Railroad Commission — which regulates Texas’ intrastate gas and petroleum industry but not railroads — keynoted the annual Republican Lincoln Day Dinner in Harrison County, where Pirkey is located.

“AEP bought the thing and decided it was going to shut it down regardless,” Christian was quoted as saying in a local newspaper. “Thirty years of this plant here in Hallsville, got 30 years in reliable generation of electricity, and we’re tearing that sucker down because it ain’t working. It doesn’t fit into the [environmental] religion.”

“I don’t blame legislators for wanting to protect the local utility, local jobs, local communities and tax base by resisting the closure of a coal plant and coal mine,” Silverstein said in an email. “The Pirkey plant … is a great source of ongoing revenue for SWEPCO, so the fact that the integrated utility wants to shut it down before the end of its useful life indicates that they are looking ahead at favorable energy replacement costs, the likely high costs of meeting upcoming EPA coal emissions requirements and potential rate base replacements.

“But this coal plant and coal mine are imposing significant costs on the communities and on all SWEPCO customers, and it appears that they could save money for everyone if they shut down the Pirkey plant and replaced it with SPP region-sourced energy alternatives,” she said, noting the Inflation Reduction Act contains “big incentives to reinvest in communities to ‘retool, repower, repurpose or replace’ fossil infrastructure and recover transition costs.”

“It’s likely that the communities these legislators represent could come out ahead in terms of jobs and utility bills within a few years if the legislators work with SWEPCO for a smart energy transition, rather than trying to protect an old coal plant,” Silverstein added.

Coleman said that SWEPCO being outside ERCOT offers a “different paradigm” and leaves the PUC with few options.

The commission’s next open meeting is March 5, leaving it little time to change AEP’s course.

DTE Energy executives warned Thursday that the utility needs to continue its investments in grid reliability and cleaner generation, investments that won’t come cheap.

CEO Jerry Norcia said during DTE’s (NYSE:DTE) year-end conference call with financial analysts that the utility didn’t request base rate increases during the COVID-19 pandemic to keep rates affordable. He said DTE now needs to reflect investments in “system reliability, grid modernization and cleaner generation.”

“Since 2020, we invested more than $8 billion in DTE electric system while keeping base rates nearly flat,” Norcia said. “After four years of essentially no base rate increases, we are requesting an increase that would go into effect at the end of 2023. This request supports investments in Michigan to improve reliability and deliver clean energy while maintaining affordable rates.”

The utility last month filed a $622 million annual rate increase with the Michigan Public Service Commission that would begin at the end of this year. The commission in 2022 reduced DTE’s request for a $388 million rate increase to $30.5 million, disputing projections of declining residential consumption. The PSC said residential use was on the upswing in 2020 and again in 2021.

“Although there were a lot of positive aspects to the outcome for which we are very grateful … we were disappointed by the projected residential sales volume in the final order,” Norcia said.

He said DTE is refreshing residential sales volume projections in the rate case. The utility also has requested an infrastructure recovery mechanism to allow it to recover the cost of grid investments between the rate cases.

“[DTE is] committed to working with all interested parties to pursue a settlement that strikes the right balance between continuing to increase reliability and providing cleaner energy for our customers, all the while maintaining affordability,” Norcia said.

CFO David Ruud said that because the PSC allowed only a modest increase, DTE will enact “one-time cost reductions that are not sustainable over the long term,” including delaying hiring, reducing the contractor workforce, deferring near-term maintenance work, and limiting overtime.

“These initiatives are all in areas where we have achieved success in the past like during the start of the pandemic, and during the last recession,” Ruud said. “[W]e remain confident that we will achieve our financial goals for the year without sacrificing safety, reliability or customer service.”

Despite the smaller-than-expected rate recovery, DTE reported earnings of $1.1 billion ($5.52/diluted share) for the year, compared to 2021’s earnings of $907 million ($4.67/diluted share).

For the quarter, earnings were $265 million ($1.31/diluted share). Earnings were $306 million ($1.57/diluted share) the year prior.

Norcia said 2022 was a record year for grid reliability and renewable energy investments, with the utility investing more than $1 billion in its grid last year to help improve reliability. He said the system operated reliably 99.9% of the time last year, with 21% fewer power outages than 2021. Average outage-duration times were reduced by more than 40%, he said.

“In communities where DTE completed some of our most focused work on a grid’s more challenged infrastructure, customers experienced up to a 70% improvement in reliability,” Norcia said. “2022 was a record year for investment in our grid, and the result was stronger reliability.”

DTE conducted the earnings call while working to restore service to about 400,000 customers after ice storms rolled through the service territory Wednesday.

Norcia said DTE needs to continue reinforcing the grid for more “violent weather” and the added strain of electric vehicle load growth.

The utility has increased its five-year capital plan by 20%, $3.5 billion more than last year’s plan, owing to “infrastructure renewal and cleaner generation,” Norcia said.

He noted that DTE in 2022 secured contracts with Ford Motor Co. and automaker Stellantis under its voluntary renewable energy program, MIGreenPower. The company said it currently has 900 businesses and 85,000 residential customers enrolled in the 2.25-GW program.

“[I]t continues to grow daily and exceed expectations,” Norcia said.

He said DTE’s five-year plan for cleaner generation includes spending $1 billion on its voluntary renewable program and $1 billion for solar generation development.

The utility retired two coal plants last year. DTE called it a “milestone” in its efforts to achieve net zero emissions by 2050. In the interim, it is targeting an 85% reduction in emissions by 2035 and 90% by 2040.