Energy storage resources bailed out the ERCOT grid May 8, providing a record amount of energy to help the Texas grid operator through the first tight conditions of the maintenance season.

Discharging batteries provided 3,195 MW at 8:05 p.m. CT, according to Grid Status, meeting 5% of demand for the first time and smashing the previous record by more than 1 GW.

“The future is here!” former FERC Chair Pat Wood, now Hunt Energy Network’s CEO, said on social media.

The old mark came Sept. 6 when ESRs provided 2,172 MW of energy after a voltage drop forced ERCOT into emergency operations for the first time since Winter Storm Uri. (See ERCOT Voltage Drop Leads to EEA Level 2.)

ERCOT began the year with 3.3 GW of storage capacity. That is expected to double by the end of the year, but an additional 145 GW of storage capacity is in the interconnection queue.

The ISO had issued a weather watch for the day because of “unseasonably” high temperatures, high levels of expected maintenance outages and the potential for lower reserves. Weather watches are not calls for conservation, ERCOT says.

The heat index at DFW Airport reached 103 degrees Fahrenheit.

The grid operator’s May resource adequacy forecast, distributed in March, assumed 14.7 GW of thermal assets would be offline during the month. Instead, 24.7 GW of the resources were offline May 8, according to the ERCOT dashboard. The same forecast also predicted 2 GW of energy storage availability.

Peak load averaged 68.9 GW during the hour ending at 5 p.m. ERCOT’s record is 85.5 GW, set last August.

Prices neared their $5,000 cap during the interval ending at 8:15 p.m.

ERCOT on May 3 issued a request for proposal for 500 MW of demand response, primarily in the San Antonio area. The grid operator has established a generic transmission constraint south of the city to address power flow limitations over transmission lines.

Canada’s pension board and a private equity firm intend to buy Duluth, Minn.-based energy company Allete for $6.2 billion, which appears to make some Minnesota regulators apprehensive.

Allete announced May 6 that it entered into an agreement to be acquired by Canada Pension Plan Investment Board (CPP Investments) and Global Infrastructure Partners (GIP). The two would disperse $67/share to shareholders and assume Allete’s debt.

Following the acquisition, Allete would become a private company, no longer traded on the New York Stock Exchange. The sale is scheduled to close next year and requires approvals from shareholders, Minnesota and Wisconsin regulators, FERC, the Federal Trade Commission, and possibly others.

In a press release, Allete CEO Bethany Owen said the transaction would grant Allete “access to the capital we need” to serve customers and hit clean energy targets as the fleet transitions.

“CPP Investments and GIP have a successful track record of long-term partnerships with infrastructure businesses, and they recognize the important role our Allete companies serve in our communities as well as our nation’s energy future,” Owen said. “Together, we will continue to invest in the clean energy transition and build on our 100-plus-year history of providing safe, reliable, affordable energy to our customers.”

Allete CEO Bethany Owen | Allete

Allete’s Minnesota Power, which serves about 150,000 residents and industrial customers across 15 municipalities, must reach Minnesota’s 100% carbon-free electricity mandate by 2040.

Allete also boasts clean energy developer Allete Clean Energy and North Dakota-based wind operator Allete Renewable Resources in addition to BNI Energy in North Dakota; Superior Water, Light and Power in Superior, Wis.; and distributed solar energy developer New Energy Equity.

Owen framed the transition to private ownership as a positive development, allowing Allete to draw on its owners’ financial resources instead of having to issue equity in the markets. She said, “strong partners will not only limit our exposure to volatile financial markets, it also will ensure Allete has access to the significant capital needed for our planned investments now and over the long term.”

CPP Investment Board has about $591 billion Canadian dollars (about $432 billion USD) in assets; it oversees the retirement funds for approximately 21 million Canadians. GIP manages $112 billion with a focus on energy, transportation, digital infrastructure, and water and waste management. GIP is set to provide 60% of the equity to purchase Allete, with CPP Investments providing the remaining equity.

Earlier this year, BlackRock announced it plans to acquire GIP for $3 billion of cash and approximately 12 million shares of BlackRock common stock. That negotiated deal hasn’t been finalized and is awaiting FERC approval (EC24-58). BlackRock already owns 13.55% of Allete.

Minnesota regulators appeared apprehensive of Allete’s reclassification as a private company owned by investment firms during a special planning meeting May 9 discussing the possible sale.

There, Owen emphasized the acquisition wouldn’t mean a change in day-to-day operations or customer rates. In the press release, Allete said its headquarters, leadership, workforce, compensation and charitable contributions would remain undisturbed.

“Allete is a relatively small company doing big, important things,” Owen told regulators, adding that becoming a privately held company will help it raise more than double its current, roughly $3.4 billion market value for new infrastructure projects.

Owen said Allete will file a petition for approval of the sale with the Minnesota PUC and the Public Service Commission of Wisconsin sometime in July.

GIP founding partner Jonathan Bram said he’s certain regulators will thoroughly evaluate the acquisition’s details.

“There haven’t been a lot of acquisitions like this in front of the commission,” Minnesota Public Utilities Commission Chair Katie Sieben said. She asked how the sale would affect Allete’s transparency.

Minnesota Power Vice President of Regulatory and Legislative Affairs Jennifer Cady said even though Minnesota Power wouldn’t have to make SEC filings going forward, transparency would continue through rate cases and FERC Form 1 filings, alongside other FERC filings. Cady also said the PUC could require more reporting as a condition of the sale.

Katherine Hinderlie, manager of the Residential Utilities Division at the Minnesota Office of the Attorney General, said the likely amount of protected data in the sale means there’s a good chance it will become a contested proceeding.

Commissioner Hwikwon Ham said he worried that investor firms could lobby to weaken Minnesota’s “strong” regulatory model.

GIP representatives said they’re happy with Minnesota’s regulatory model and don’t plan to influence changes.

Allete has said that Minnesota Power and Superior Water, Light and Power will continue as “independently operated, locally managed, regulated utilities.”

Minnesota Power is partial owner in a proposal to build the gas-fired Nemadji Trail Energy Center in Wisconsin. Plans for the plant hit a snag in April when the city council of Superior, Wis., didn’t allow necessary zoning changes for construction to begin. (See City Council Vote Stalls Planned Wisconsin Gas-fired Plant.)

After announcing its sale, Allete canceled its first-quarter earnings call, scheduled for May 9.

In the press release, GIP CEO Bayo Ogunlesi said it and CPP Investments “look forward to partnering to provide Allete with additional capital so they can continue to decarbonize their business to benefit the customers and communities they serve.”

“Bringing together Allete, with its demonstrated commitment to clean energy, with GIP, one of the world’s premier developers of renewable power, furthers our commitment to serve growing market needs for affordable, carbon-free and more secure sources of energy,” Bayo said.

Concerns over the BlackRock Connection

The announcement doesn’t sit well with a nonprofit consumer advocate. Public Citizen Energy Program Director Tyson Slocum said the pending sale of GIP to BlackRock means that BlackRock — “a totally different animal” — would be the one to acquire Allete.

Public Citizen said it plans to lodge a protest with FERC over BlackRock’s takeover of GIP considering the Allete deal.

Allete would “lose significant transparency” under its new ownership, Slocum predicted, and could be “consumed into BlackRock’s black box” if the world’s largest asset manager successfully obtains GIP.

Slocum said he expects GIP and CPP Investments to agree to short-term commitments along the lines of reducing rates, shielding customers from transaction costs and possibly decarbonizing Allete’s fleet faster. However, he said impacts in the long run are murkier and entirely up to the new owners.

“The long-term issue of the utility going private can’t be undone. That’s the big issue here,” Slocum said in an interview with RTO Insider. “If BlackRock is ultimately the owner, they can do whatever they want with their asset. This is a really, really serious move by BlackRock. Whatever assurances the companies are giving, you’re losing transparency at the holding company level.”

Slocum said SEC filings are not on par with FERC Form 1 filings, with the former occurring at the holding company level while the latter are at the franchised utility level. Comparing detailed SEC disclosures to FERC and state filings is a “tired talking point that is factually inaccurate,” he said.

Slocum said nothing is stopping the new ownership from creating numerous LLCs to obscure investment decisions. It could have state commissioners playing “whack-a-mole” trying to regulate financial activities, he said.

Slocum said he worried that investor firm ownership would trade the existing influence of everyday shareholders to the “wealthiest 1% of the planet.” He noted only a handful of utilities with captive service areas are privately controlled, including Puget Sound Energy, El Paso Electric, Cleco and Duquesne Light Co.

“Missing at that conference today was BlackRock,” he said of the PUC’s special planning meeting. “It looks like state regulators haven’t wrapped their heads around this. Whatever hearing Minnesota has next, they must have BlackRock there.”

BlackRock thus far has styled itself to FERC as a passive minority holder of utilities, Slocum said, and ownership of GIP would change that. He said federal agencies might consider splitting BlackRock in two so it can maintain both passive and active ownership of utilities.

“I have no idea how you navigate that unless you force a divesture,” Slocum said.

Slocum also said BlackRock should abstain from the shareholder vote for GIP and CPP Investments to acquire Allete. Although BlackRock currently owns shares, participating in the vote would constitute a “clear conflict of interest” given its expected purchase of GIP.

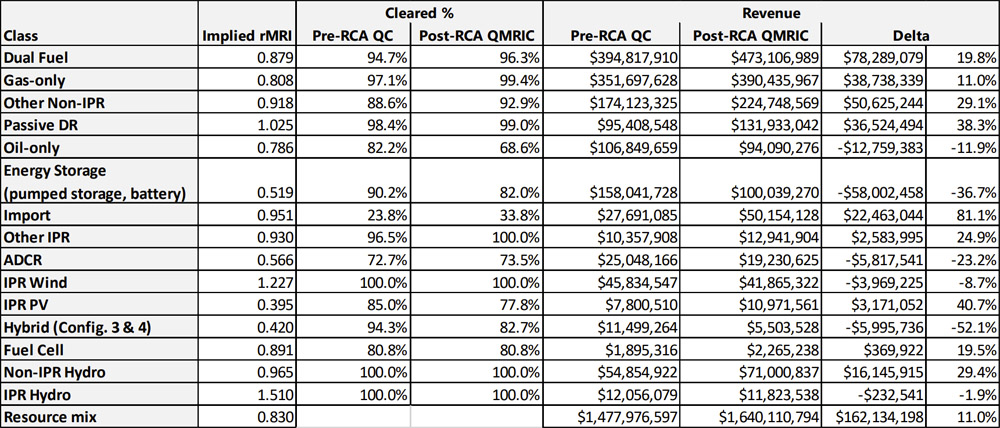

ISO-NE’s proposed resource capacity accreditation (RCA) updates would result in an estimated 11% increase in capacity market revenues, the RTO told the NEPOOL Markets Committee on May 7.

Despite the overall increase, ISO-NE projects revenues to vary significantly based on resource class. The modeling showed that compensation for gas, dual fuel, energy efficiency, solar and imports would increase, while revenues for oil, energy storage, active demand response, wind and hybrid resources would decrease.

The RTO also estimated that the RCA updates would reduce the loss-of-load expectation by about 38%.

Initially introduced in 2021, the RCA project is intended to better align ISO-NE’s capacity market with the reliability contributions that different resources provide to the grid. Accreditation values would be based on a given resource’s expected output during the hours of greatest reliability risk.

The RTO emphasized that the revenue results are dependent on the modeling assumptions and are likely to change as the resource mix and seasonal risk profile shifts. The RTO’s modeling indicates that near-term reliability risks are concentrated in the summer, and it projects that winter reliability risks will rise dramatically as heating electrification intensifies and winter peak loads will surpass summer peaks in the mid-2030s.

The seasonal risk balance likely significantly affects the revenues projected for gas-only resources. While one of the main drivers of the RCA project was to better account for gas constraints during winter months, ISO-NE projects that the changes will increase gas-only resources’ revenues by 11% (coincidentally). This increase is attributed in part to the concentration of risks in the summer, when gas resources face minimal constraints, ISO-NE said. As winter reliability contributions become more important, gas constraints will have a greater impact on capacity accreditation, likely reducing revenues.

The design of the capacity auction could also significantly change before the RCA updates are implemented.

ISO-NE is proposing to shift its capacity auction from a forward annual design, with the auction for each yearlong capacity commitment period (CCP) held over three years in advance, to a prompt seasonal design, with auctions held much closer to the CCP, which would be broken up into seasonal segments.

If FERC accepts ISO-NE’s proposal to delay Forward Capacity Auction 19 an additional two years, the RTO “will focus on evaluating scope and phasing of work for a combined accreditation design with a seasonal/prompt capacity market to implement for CCP 19 and would target discussing initial scope considerations with the MC in July,” said the RTO’s principal analyst, Dane Schiro.

Despite the uncertainties, the RTO’s presentation provides the most detailed look to date at how the changes will ultimately impact resource compensation.

ISO-NE projects dual-fuel resources to have the largest increase in total revenue, about $78.3 million (19.8%), followed by a class of non-intermittent resources including coal, nuclear and wood-burning generators at $50.6 million (29.1%); gas-only resources at $38.7 million; energy efficiency at $36.5 million (38.3%); imports at $22.5 million (81.1%, the largest percentage increase); and non-intermittent hydro at $16.1 million (29.4%).

RCA revenue results by resource class | ISO-NE

Meanwhile, ISO-NE estimated that energy storage (including both batteries and pumped hydro) would have the most significant decrease in revenue, about $58 million (36.7%), followed by oil-only resources at $12.8 million (11.9%), hybrid resources at $6 million (52.1%, the largest percentage decrease), active demand response at $5.8 million (23.2%) and wind at $4 million (8.7%).

Alex Chaplin of New Leaf Energy told RTO Insider the company is concerned that the projected revenues indicate the updated accreditation methodology may undervalue storage resources.

“Some New England states have energy storage goals and have implemented (or are working to implement) incentive programs for storage to help address the ‘missing money’ problem batteries face,” Chaplin wrote in an email. “We fear that a significant reduction in capacity revenues will worsen the missing money problem and negatively impact storage deployments in the region.”

Aleks Mitreski of Brookfield Renewable expressed perplexity about why storage resources experienced such a significant reduction in capacity revenues relative to fossil resources, adding that the differences may stem from how ISO-NE models the physical parameters of various resource classes.

“Pumped storage resources that operate every day receive a sizable capacity payment reduction of 36%, while oil units that run a few days of the year only get a 12% payment reduction,” Mitreski told RTO Insider.

Constellation Energy Corp. is looking at squeezing more megawatts out of existing reactors, extending their operational lifespans and building new generation beside existing facilities.

Constellation CEO Joe Dominguez said the company continues to believe nuclear fission is the most reliable and therefore best option for emissions-free electricity, and as long as policy support continues, Constellation will seek to supply more of it.

“Our country needs what we have — clean and dependable power generation to drive economic growth [and] support our national security and our environmental goals,” he said during a May 9 conference call with financial analysts to discuss first-quarter results.

“We intend that Constellation will be a leader in adding new clean, reliable megawatts to the grid to meet the needs of American families and businesses.”

Dominguez identified three strategies the company will pursue to accomplish this:

Keeping existing reactors in service into the 2060s would limit the need to build new full-size reactors, a costly and lengthy process. Constellation has sought and/or received license extensions for five facilities and will seek more if supportive policies remain in place, Dominguez said. This by itself would create “more clean energy than all of the renewables ever built in this country,” he said.

Upgrading existing reactors would maximize their output — previously announced updates at the Byron and Braidwood generating stations will yield 160 MW in the next few years, Dominguez said. “We’re looking at many opportunities to do that at other plants. We believe that the opportunities will add up to 1,000 MW, or perhaps more,” he said.

“Third, we’re looking to partner with others to locate new technologies, including new nuclear, at our existing sites,” Dominguez said. The existing nuclear facilities enjoy community support and have the capability to support expansion, he said, making them the logical place to add new capacity.

Dominguez opened the call with a tribute to Chris Crane, who died in April at 65. As CEO of Exelon, Crane paved the way for the spinoff Constellation to shine as the largest U.S. operator of nuclear power generation, Dominguez said.

“He was an all-of-the-above energy thinker who cared about nuclear because he was sure that you could not run a full-time clean energy economy just on part-time power,” Dominguez said.

This idea of full-time power is central to Constellation’s business plan as state and national leaders press the clean energy transition: Nuclear generates electricity when the sun is not shining and the wind is not blowing, and in nearly every other circumstance. Output from photovoltaic panels and wind turbines is intermittent.

Constellation’s nuclear fleet had a 93.3% capacity factor in the first quarter of 2024, and that was at the lower end of performance recorded in the previous eight quarters.

The U.S. Energy Information Administration reports the capacity factor for land-based wind generation reached an all-time high of 35.9% in 2022. The highest capacity factor for solar in the past 10 years was 25.6% nationally. Both clean energy technologies vary greatly by region and season.

Nuclear power still has many critics, due to the exorbitant cost of new construction and radiation hazards, but it has gained support on both sides of the aisle for this ability to steadily produce electricity without also producing carbon dioxide.

“State legislatures have 130 bills out there to support nuclear energy this year, compared to five to 10 historically,” Dominguez said. “They’re removing barriers to nuclear by repealing moratoriums on building new nuclear, and they’re developing regulations to support new development in the states. And six states, red and blue, have created incentives in their state budgets to attract nuclear to their state.”

Constellation’s GAAP net income was $2.78 per share in the first quarter of 2024, and its adjusted (non-GAAP) income was $1.82. This compares with $0.29 and $0.78 in the first quarter of 2023.

Constellation’s stock price has increased 176% in the past year and 426% since it began trading in January 2022. It closed 3.8% higher May 9.

Previewing NERC’s Summer Reliability Assessment at the ERO’s quarterly technical session May 8, Director of Reliability Assessment and Performance Analysis John Moura warned that the organization expects significant challenges to grid reliability during periods of extreme heat.

NERC publishes the assessment annually to identify potential regional reliability issues and topics of concern in the June-to-September time frame. According to the timeline Moura presented at the technical session, the report has been submitted to CEO Jim Robb for approval and will be sent to the Board of Trustees later this week. The organization plans to publish the assessment May 15.

Hot conditions are likely across the U.S. and Canada this summer, Moura said; the National Weather Service predicts a greater than 50% chance that New England and most of the Southwest will experience above-normal temperatures, and at least a 1-in-3 chance in the rest of the U.S. Canada also forecasts a high probability of above-normal temperatures across all provinces.

The report also noted the risk of drought across large areas of North America, with abnormally dry conditions predicted in the Northwest U.S. and eastern Canada, and moderate to extreme drought in the Southwest and western Canada. Drought conditions could lead to higher wildfire risk, along with reduced hydropower output.

Moura emphasized the ERO expects all regions to “have an adequate electricity supply for normal peak conditions,” just as it did when it issued last summer’s assessment. (See NERC Warns of Summer Reliability Risks Across North America.) This comes despite 12 of the 20 assessment areas projecting a higher peak demand than in past summers; Alberta and British Columbia lead the pack with predicted increases of 8.9% and 7.4%, respectively, while Quebec’s expected growth is the lowest at 0.3%.

Reserve margins in many areas also are expected to be higher than last year thanks to the addition of new resources and demand response. For example, the Western Interconnection is adding solar and battery capacity; Ontario authorities have rescheduled maintenance activities to make more nuclear generation available; SERC Central has added natural gas and solar generators; and multiple areas have lined up firm imports.

But while normal conditions are not a major concern, Moura said extreme scenarios are a different story. Long periods of widespread high temperatures raising demand across multiple regions could limit the ability of individual assessment areas to import power, because neighbors likely will have similar demands. The ERO also foresees difficulty for areas with high levels of wind, solar or hydropower to meet their needs when those resources run low.

Moura said the published assessment will provide several recommendations for industry, including that reliability coordinators, balancing authorities and transmission owners in areas with elevated risk review their operating plans and protocols for supply shortfalls. He also said NERC will ask owners of solar generation resources to implement the recommendations in the Level 2 alert for inverter-based resources the ERO issued last year.

ISO-NE predicts New England’s peak load will increase by about 10%, and electricity consumption by 17%, by 2033, according to its 2024 Capacity, Energy, Loads and Transmission (CELT) report, released May 1.

The increasing peak load forecast is driven by increasing transportation and building electrification, ISO-NE said. The estimate is a slight decrease from the peak load projections in the 2023 CELT report. (See ISO-NE Decreases Its 10-year Peak Load Forecast.)

While the New England grid currently peaks in the summer, ISO-NE projects the winter peak to grow significantly faster, with a projected increase of about 33% over the next decade.

In 2033, ISO-NE expects the region’s summer peak to reach 27,052 MW and the winter peak to reach 26,768 MW. The RTO expects winter peaks will surpass summer peaks in the mid-2030s because of heating electrification.

The New England power system reached its peak load in 2023 on Sept. 7, topping out at just over 24,000 MW.

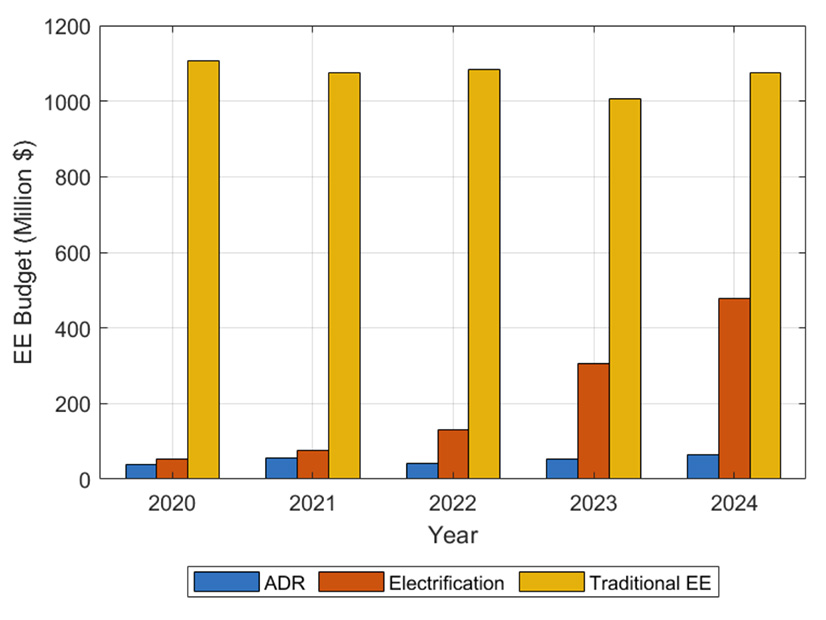

Energy use in New England has declined since the early 2000s, largely because of energy efficiency programs and behind-the-meter solar. However, ISO-NE projects the amount of energy efficiency participating in its capacity market to decline in the coming years as states shift their focus toward building electrification and heating retrofits.

New England states’ energy efficiency budget allocations | ISO-NE

In a recent presentation, ISO-NE noted that state energy efficiency budgets “have remained consistent, while production costs have increased.” In contrast, states have dramatically increased funding for electrification programs over the past four years and have slightly increased funding for active demand response.

ISO-NE projects energy efficiency resources that expire and exit the market will outpace energy efficiency resource additions by 2029.

“Since [Forward Capacity Auction] 14, the amount of expiring EE measures has been surpassing the pace of new EE cost-of-service agreements entering the market,” ISO-NE spokesperson Mary Cate Colapietro noted.

And 2024 marks the fourth consecutive year in which the RTO’s energy efficiency forecast has declined.

While ISO-NE indicates it expects BTM solar capacity to continue to grow at about 1,000 MW per year over the next decade, it projects solar will reduce the region’s peak load by just over 200 MW by 2033. (See NEPOOL Participants Committee Briefs: May 3, 2024.)

Colapietro noted that increasing amounts of BTM solar “will shift the timing of peaks to later in the day when the panels produce less power.”

ISO-NE projects BTM solar will reduce total energy demand by about 10,000 GWh in 2033 — down 6.6% compared to gross energy demand — compared to about a 4,000-GWh reduction in 2023.

The RTO said it plans to re-evaluate its methodology for forecasting energy efficiency and demand-reduction efforts in light of the states’ shift away from traditional energy efficiency measures.

“The current method of using projections of EE counterfactuals to develop an accurate net energy and demand forecast has proven challenging and may introduce more uncertainty to the forecast than forecasting net of EE load directly,” ISO-NE noted.

Siemens Energy has begun a multiyear restructuring of its wind power business, which temporarily has halted sales of certain onshore turbine models due to quality-control problems.

Siemens Gamesa CEO Jochen Eickholt will step down effective July 31 and the company will focus its onshore efforts on attractive markets with stable regulatory frameworks, primarily in Europe and the United States. Siemens Gamesa hopes to end its losses by 2026 and then return to profitable growth.

The announcements came May 8, as Siemens Energy reported its second-quarter earnings. Eickholt’s impending departure is “by mutual agreement.”

Siemens Energy CEO Christian Bruch thanked Eickholt for laying the foundation for the reorganization and planned rebound and emphasized the quality-control problems that flared up did not begin while Eickholt was CEO.

Siemens Gamesa orders in the second quarter of fiscal 2024 were down 76% from the same quarter a year earlier but revenue was down only 5%, with higher offshore revenue more than offset by lower onshore revenue.

The company expects substantially better revenue in the second half of fiscal 2024, especially because of its efforts to ramp up its offshore production capacity. Multiple internal organizational changes are underway, as well.

Siemens Gamesa temporarily has stopped selling its 4.X and 5.X onshore turbines as it deals with the defects that have been observed.

Bruch addressed this early in his conference call with financial analysts.

“Obviously, we will need time to work through the quality matters,” he said.

“We will develop new onshore business based on, first of all, selected regions, and second, based on revised 4.X and 5.X platforms but with a heavily reduced number of variants. This is what Jochen and the team [have] been also driving over the past couple of months already — simplify the product structure in our company.”

Bruch said the target date for restarting turbine sales in Europe is the end of fiscal 2024 for the 4.X and fiscal 2025 for the 5.X, with relaunch in the United States later.

“Please keep in mind the volumes will not come back immediately,” he said. “We still have a big plan to work through. And we also have still the quality matters but we are confident that we are able to rebuild a strong market position over the coming years but it’s really a long-term trajectory.”

Siemens Energy stock closed 12.8% higher in trading on May 8.

Members of key Western Resource Adequacy Program (WRAP) stakeholder groups have expressed support for a recent move by participants to delay the program’s “binding” penalty phase by one year, to summer 2027.

Those stakeholders shared their views during a May 8 meeting of the WRAP’s Program Review Committee (PRC), a sector representative group “charged with receiving, considering and proposing design changes” to the RA program operated by the Western Power Pool (WPP).

They were reacting to an April 22 letter by the WRAP’s Resource Adequacy Participants Committee (RAPC) seeking the delay and outlining a number of concerns in meeting RA obligations in summer 2026, including supply chain delays, rapid regional peak load growth and extreme weather events that could affect participants’ ability to procure enough capacity to meet resource adequacy requirements. (See WRAP Participants Seek 1-Year Delay to ‘Binding’ Operations.)

Members of WPP’s voluntary program face a May 31 deadline to commit to binding operations by summer 2026, which would subject participants to penalties for capacity deficiencies.

PRC member Ray Johnson, deputy general manager with Tacoma Power, reiterated the concerns set out in the letter.

“The intent is to close the gap on some capacity deficits, but supply chains are causing delay,” Johnson said. “It’s very difficult in this current environment to procure or build all the capacity that’s required in the time frame that we’re currently operating under. And so, the modifications will enable a little bit more of a ramp into the program and then enable the program to be fully binding, I think, in early 2029.”

Asked to clarify Johnson’s 2029 reference, Tacoma Power told RTO Insider in an email that Johnson was referring to the first year beyond the program’s phase-in transition period set out in the WRAP tariff, which ends in 2028.

“They are still working toward a critical mass of participants electing binding operations for summer 2027, which falls in the existing transition period window,” a utility spokesperson said.

Rebecca Sexton, director of reliability programs at WPP, said the one-year delay is “not technically a loss.”

“This current undertaking here to select summer 2027 is well within the current tariff, so we don’t really see it as a delay,” Sexton said. “It does mean kind of a paradigm shift of what we think about binding. I think the terms that are being preliminarily discussed for the transition would hopefully encourage folks, even if they can’t meet the expectations of the WRAP program, to still be a binding participant.”

Non-utility Perspectives

Non-utility stakeholders agreed that they don’t want the program to enter the ‘binding’ phase until it includes a critical number of participants.

“I fully appreciate that this program is going to be more successful if we get this critical mass and everybody is in it together, and to incent that, I see why we proposed kind of ramping in,” said Ben Fitch-Fleischmann, director of markets and transmission at Interwest Energy Alliance.

Sommer Moser, an attorney representing Alliance of Western Energy Consumers (AWEC), shared a similar view but said it did not reflect a formal position from AWEC.

“Taking the time to get things right to make sure that we are eliminating inefficiencies and being thoughtful about implementation tends to lead to a program that is more cost effective and [has] greater benefits for participation,” Moser said. “I was a little concerned at the delay but ultimately think that getting it right is most important.”

Serving new demand from medium- and heavy-duty vehicle (MHDV) electrification will require some grid upgrades, but it could lower utility rates, Advanced Energy United said in a paper published May 6.

Impacts at the substation and feeder level will vary by where fleets of electric MHDVs might charge and how much headroom exists on the distribution system. That will require careful estimation and planning as fleets electrify, the report says.

“Greater MHDV electrification will result in greater electricity sales, increasing utility revenues,” the report says. “As long as the increased utility revenue from [electric vehicle] charging exceeds increases in utility system costs, transportation electrification will benefit all electric utility ratepayers by putting downward pressure on rates.”

That might not mean lower rates overall because other factors could drive them up, Richard Khoe, program supervisor at the California Public Utilities Commission’s Public Advocates Office, said on a webinar held by United on May 7.

His office did a similar study for California, which estimated a total of $26 billion to upgrade the distribution grid for the electrification of light-duty vehicles, MHDVs and homes, compared to a $50 billion estimate from a different report conducted for the PUC.

“We also found that the downward pressure on rates might not be achieved if any of the following things were to occur,” Khoe said. “For example, if EVs mostly charged in the evenings near peak hours, that would drive peak load up … and that would lead to higher upgrade costs.”

Using electric rates to subsidize charging excessively — or the study’s upgrade cost estimates being too low — could lead to higher rates, he added.

“We found that on a systemwide basis, peak loads probably are only going to increase by about 1 to 2% … by 2035,” said United report co-author Sarah Shenstone-Harris, of Synapse Energy Economics. “So not all that much. But at the feeder and substation level, the impact is much more varied.”

The main issue with MHDV electrification is that vehicles are likely to be clustered at specific sites, such as a warehouse district with panel trucks, or a bus depot, Shenstone-Harris said on the webinar. Some of those areas might have enough headroom to accommodate charging, but others will require upgrades.

“Generally, studies have found that loads of 1 to 5 MW will require a new feeder, or an upgrade, and loads of 5 to 10 MW will require a new substation or a substation upgrade,” Shenstone-Harris said. “But again, it really depends on the specifics. And as you can imagine, cost ranges also vary a lot depending on the specifics of the project, as well as lead time.”

United’s report offers four recommendations for states to get it right:

require utilities to share data about capacity of the distribution grid;

improve utility planning and regulatory processes to address barriers to electrification;

implement programs to manage peak loads and minimize costs; and

target certain areas for grid investment and/or MHDV adoption.

“A state or utility that doesn’t adopt these kinds of recommendations [is] surely going to be confronted with painful challenges down the road,” the New York Department of Public Service’s Zeryai Hagos said. “And this is because the four recommendations will work in unison to avoid long delays in interconnection — delays that could last for several years.”

A study in New York found that MHDV make-ready programs, which cover the upgrade costs of electrification, have a neutral to beneficial impact on rates through 2045, the report says. Benefits grew when charging was shifted to off-peak hours.

MHDVs can also serve as batteries in vehicle-to-grid services, contributing to grid stability and supporting the integration of renewable energy sources. Possessing larger batteries than standard cars, MHDVs can charge with more renewable energy when it is producing a surplus and can offer bigger discharges when the grid is stressed.

EVs cost more upfront than standard models, but they benefit from major fuel and maintenance savings over their lifetime. An electric delivery truck can save 34% compared to a diesel model over its lifetime, while an electric bus could save 24%.

“Electric vehicles have fewer moving parts and simpler drivetrains compared to internal combustion engines, leading to substantially lower maintenance needs,” the report says. “Plus, with EVs’ regenerative braking technology, certain pieces of braking equipment need to be replaced less frequently.”

AURORA, Colo. — FERC Commissioner Mark Christie, who still refers to himself as a state regulator after 17 years on the Virginia State Corporation Commission, offered words of praise and encouragement for SPP’s state regulators in his first appearance before the RTO and its Regional State Committee.

“I’ve always been very admiring of this RSC structure,” Christie told the RTO’s regulators and stakeholders during the RSC’s May 6 meeting. “I’m pleased to be here watching the action of this committee I’ve heard about for 20 years now that I’ve been so envious of.

“Your job is incredibly important. I’m obviously very adamant about the state role of RTOs. Someone once told me, ‘You’re like a state regulator on loan to FERC,’ so I’ll take that,” he added. “But I’m adamant about the state’s role because I’m adamant about protecting consumers. Everything that as a state regulator we do, and you all on the front lines, should be about putting consumers first.”

As most of the state commissioners that constitute the RSC listened attentively, Christie described resource adequacy as the key element of grid reliability, one of two major issues facing state regulators.

“Resource adequacy means what generation resources will get built, which ones get retired,” he said. “You — I should say, we — at the state level are on the frontlines because you’re the ones who are approving the construction of new generating resources. You’re the ones who are overseeing retirements. That’s why your role is actually the most important in the whole regulatory universe.”

Christie said the second major issue facing state regulators is consumer confidence because they’re “on the front line of rising power prices.”

“They’re going up, and they’re going up at a higher rate than it was 10 years ago,” he said. “When you approve a rate increase, and I know this from 17 years of having been a state regulator, it’s going to go right into people’s monthly bills. That’s one thing about being a state regulator is that you hear about it. You live among the people who you’re impacting, and that’s why state regulators are so important. I trust you all to know what is best for your state.”

The feeling was mutual. RSC President John Tuma of Minnesota thanked Christie for attending, saying: “We still welcome you as a full state commissioner, ever though you carry that other title.”

RSC Celebrates 20 Years

The RSC’s agenda, which included the quarterly stakeholder briefing, was scheduled for four hours. It went three-plus. Credit Tuma, who ran a tight ship that shaved off more than an hour of discussion. “Today may be a new land speed record,” cracked John Cupparo, SPP’s board chair.

The early finish allowed attendees to begin their commemoration of the RSC’s 20th anniversary 45 minutes early.

“I can’t believe it’s been 20 years for the RSC,” CEO Barbara Sugg said. “There’s lots for us to celebrate.”

“As someone who spent a good chunk of their career in the non-RTO West and experienced regional issues and trying to pull together participation from the regulatory community and others, this is a very challenging effort,” Sugg said. “That continues today. From that experience, the RSC group that we have is a special and powerful thing.”

The Advanced Power Alliance’s Steve Gaw was the only one of the RSC’s original six founding members present for the event. A Missouri regulator at the time and also involved in standing up the Organization of MISO States, Gaw said both groups first had to determine how much legal authority they had.

Former FERC Chair Pat Wood’s standard market design, released after the 2003 Northeast blackout, helped set some guardrails for future RSC members. It took about 18 months for the group to agree on the committee’s bylaws and its responsibilities.

“The key to the success of these groups has been about … collaboration and about building bridges and being dedicated [to] trying to find a way to work together to come up with things that would produce a positive result,” Gaw said. “If the commissioners had gone with an attitude of saying, ‘I have to have my state’s interest and it’s … the only thing that I’m in here for,’ nothing would have ever moved forward.”

SPP credits the committee with developing and implementing funding mechanisms that have helped build more than $12 billion of transmission lines since 2006; producing policies governing cost allocation for upgrades facilitating the integration of more than 33 GW of wind energy in the region; and for its role in helping refine resource adequacy methodologies.

“When the RSC was formed, critics questioned whether representatives of such a diverse group of states could reach consensus on anything,” SPP general counsel Paul Suskie, the RSC’s staff secretary, said in a news release. “For more than two decades, the group has navigated complex challenges, fostered innovation in our industry and contributed to the resilience of an electric grid that serves millions of customers across the central United States.”

REAL Team Work Approved

Despite the shortened meeting, the RSC still approved several revision requests, including two brought forward by its Resource and Energy Adequacy Leadership (REAL) Team. Both passed unanimously, as did all seven of the committee’s voting items.

The tariff changes, RR605 and RR616, were approved by the Markets and Operating Policy Committee in April. They are the result of RSC directives last October to clarify resources must be available if they’re going to be accounted for in the resource adequacy construct and in some load-responsible entities’ accreditation.

RR605 would define an authorized outage and criteria, add requirements for resources’ availability during both the summer and winter seasons (unless on an authorized outage), and help load-responsible entities and generation owners better understand when to submit resource adequacy capacity in providing workbooks to meet their obligation. RR616 would ensure any outage not approved by the SPP balancing authority and not an outside management control event is accounted for in performance-based accreditation.

The RSC also endorsed the REAL Team’s price-formation policy to dispatch resources based on the true obligation and price of the system using the obligation without the impact of the load shed and emergency energy assistance. The policy protects resources that hold day-ahead positions.

South Dakota’s Kristie Fiegen, who chairs the REAL Team, said it is close to approving a winter planning resource margin and a fuel assurance policy. Both should be coming to stakeholders, regulators and staff during their July and August meetings. (See SPP, Members Close in on Fuel Policy, Base PRM.)

“We’ve had a lot of policies, but [the winter PRM] is the most time-consuming,” Fiegen said.

The REAL Team has spent six months on the PRM tariff revision, but it’s had its side effects.

“I feel like we’ve become a family this past year,” she said.

“Chair Fiegen has done a wonderful job leading these family discussions of the REAL Team,” COO Lanny Nickell said. “We haven’t yet evolved into a food fight, so that’s a good thing.”

JTIQ NTCs Possible This Year

Casey Cathey, SPP’s new engineering vice president, told the RSC that staff hopes the Board of Directors will issue construction permits by year’s end for the five projects in the Joint Transmission Interconnection Queue.

SPP and MISO staffs and potential transmission owners are pursuing a direct billing approach that would require SPP to modify a revision request (RR620), which would implement RSC-approved cost-allocation policies for JTIQ projects. MOPC delayed taking action on RR620 during its April meeting.

“We need to ensure we have the revision request locked up,” Cathey said, noting staff determined its current approach would be the most efficient way to administer the JTIQ settlement process.

SPP and MISO have agreed to assign 90% of the JTIQ portfolio’s $1.06 billion in costs for its five projects to generation. Load will cover the remaining 10%. (See MISO, SPP Propose 90-10 Cost Split for JTIQ Projects.)

RSC Welcomes Missouri’s Hahn

The committee welcomed Missouri’s Kayla Hahn, who chairs the state’s Public Service Commission, as its 47th member over the past 20 years and honored the service of recent RSC members Will McAdams (Texas) and Scott Rupp (Missouri).

Two potential future members also were present for the meeting: Mary Throne, chair of the Wyoming PSC, attended in person, while Utah Commissioner John Harvey listened in virtually.

“We look forward to your participation in the RSC and Wyoming’s participation in the RSC as part of the RTO West expansion into the Rocky Mountain area,” Sugg told Throne.

Wyoming is one of four states that, with Colorado, will make up much of SPP’s RTO footprint in the Western Interconnection. Arizona and Utah will increase the grid operator’s footprint to 17 states.