One of the two men charged with attacking electric substations in Washington state over the Christmas holiday has pleaded guilty to conspiracy to damage energy facilities, federal prosecutors said on Friday.

Matthew Greenwood of Puyallup, Wash., filed his guilty plea Friday with the U.S. District Court

for Western Washington, according to a statement. In the plea, Greenwood admitted to vandalizing four substations owned by Puget Sound Energy and Tacoma Power on Dec. 25. In addition, the plea said Greenwood and his co-defendant Jeremy Crahan, also of Puyallup, planned to cut down trees “to take out power lines,” although this plan was not acted on before the two were arrested.

Greenwood said he and Crahan sought to disrupt power in order to break into ATMs and local businesses to steal money, the same motive he mentioned to the officers who arrested him on Dec. 31. (See Feds Charge Two in Wash. Substation Sabotage.)

He also faced a charge of possessing unregistered firearms; a spokesperson for the Department of Justice confirmed that Friday’s guilty plea was only for the charges related to the substation damage. The plea agreement included a pledge from the U.S. Attorney’s Office for the Western District of Washington “not to prosecute [Greenwood] for any additional offenses known to it as of the time of this plea agreement” based on “the promises made by” Greenwood.

Crahan was also charged with conspiracy to destroy an energy facility. According to court records, he has not entered a plea. The conspiracy charges carry a maximum sentence of 20 years for both men, along with a fine of up to $250,000 and three years of supervised release, although the Justice Department said prosecutors will “recommend the low end of the [sentencing] guidelines range when Greenwood is sentenced.”

Greenwood was released on bail at the end of January to attend drug treatment.

Pair Damaged Multiple Facilities

According to the plea agreement, Crahan drove Greenwood to the substations and Greenwood performed the actual attacks. Their first target was the Hemlock substation in South Hill, where Greenwood cut through the perimeter fence around 2:30 a.m., manipulated a bank high side switch, and damaged additional equipment, causing an outage for about 8,000 customers.

Surveillance photos from Tacoma Power showing Greenwood at the Elk Plain substation. | Tacoma Power

The pair then drove to the Elk Plain substation about nine miles away in Spanaway, arriving around 5 a.m. Greenwood cut the padlocks on the exterior gate, manipulated the high side breakers, and damaged additional equipment. They arrived at the Graham substation about 30 minutes later, where Greenwood again manipulated a bank high side switch and damaged equipment. Together, the damage to the Elk Plain and Graham facilities caused at least 7,500 customers to lose power.

Finally, Crahan drove Greenwood to the Kapowsin Substation, also in Graham. Greenwood tampered with the facility’s bank high side switch and tried to pry open the linkage, causing sparks and flames. No outages were attributed to this attack in the plea agreement.

This was not the end of the men’s plans; they intended to continue causing outages by cutting down trees that would then fall on power lines. Although the men spent some time with a chainsaw looking for trees to cut over the next several days, the FBI tracked them down using cell phone records and surveillance photos before they could do so.

Greenwood’s arrest statement said that he and Crahan burglarized a local business and stole from its cash register during the outage, but this incident was not mentioned in the plea agreement.

The Washington sabotage was one of several physical security incidents late last year, most prominently the Dec. 3 gunfire attack on two Duke Energy (NYSE:DUK) substations in North Carolina, which left 45,000 customers without power for as long as four days. (See Duke Completes Power Restoration After NC Substation Attack.)

In response to the North Carolina attacks, FERC ordered NERC to review the effectiveness of its physical security reliability standards and determine whether improvements are needed. NERC released its report last month, identifying several possible areas of improvement and proposing a new standards development project to address the issues. (See NERC Says Changes Coming to Physical Security Standards.)

Vermont Gov. Phil Scott (R) plans to veto clean heat legislation for the second year in a row.

Scott said Friday that he agrees with the need to reduce greenhouse gas emissions, including in the heating sector, but the complex clean heat credit system approved by the state legislature is the wrong way to go about it.

The Affordable Heat Act (S.5), sponsored by Sen. Christopher Bray (D), would harm those who cannot afford to switch to cleaner forms of energy, Scott said, adding that Vermont should instead help its residents make the expensive transition, rather than financially punish them.

“Unfortunately, the Super Majority in the Legislature decided to take a completely different approach by giving an unelected commission, the Public Utility Commission, the power to design and adopt a system without guaranteeing the details and costs will be debated transparently through the normal legislative process, in full view of their constituents,” he said in a statement.

The General Assembly approved the measure last week with votes of 20-10 in the Senate and 98-46 in the House, both chambers falling short of unanimous support from their Democratic supermajorities.

A similar clean heat measure advanced through the legislature last year. Scott said then he would support that bill if its language explicitly required the policy details and projected costs of a credit system to come before the legislature and him for final approval.

Scott in his news release urged Vermonters to ask their representatives to sustain this veto as well.

The measure is presented as a means for Vermont to meet its greenhouse gas emission reduction goals by equitably reducing use of fossil fuels to heat buildings, which generates a third of the state’s emissions.

It orders the PUC to design a credit marketplace for the state’s regulated gas utility and heating fuel dealers that will help their customers pay to switch to emissions-free heating.

Scott has also expressed reservations about the cost of building electrification and the difficulty of doing it quickly. But his stated opposition to the plan is centered on its wording, which he and others read as contradictory and potentially enabling the PUC to design and enact what is essentially a carbon tax without legislative approval.

Scott criticized the legislators’ attempt add a “check back” provision to the bill that directs the PUC to report back to the legislature on its efforts to establish the Clean Heat Standard, with estimates of the impacts of the framework it draws up and any recommendations for legislative action.

“When I resisted the Legislature’s original approach to the bill, they inserted a ‘check back’ provision, saying it satisfied my concerns,” Scott said in a news release Friday. “It does not. Some claimed the bill is essentially a study. It is not. As recently as Thursday’s debate on the Senate floor, Senators from both parties have called the check back in the bill contradictory and confusing.”

Nuclear power in the U.S. is locked in a stalemate, according to a new report from the Department of Energy.

No matter how much renewable energy is deployed to decarbonize the grid, DOE is estimating that 500 to 750 GW of clean, firm power — including 200 GW of new nuclear — will be needed to reach net-zero emissions economy-wide by 2050.

“We’re going to need multiple reactor technologies to be successfully deployed at scale, from Generation 3 light water reactors to Generation 4 advanced reactors,” Kathryn Huff, who leads DOE’s Office of Nuclear Energy, told an online audience at Friday’s webinar on the recent Pathways to Commercial Liftoff: Advanced Nuclear report. Reactors of different sizes will also be needed, “from 1 MW, all the way up to gigawatt-plus reactors,” Huff said.

The report differentiates between Gen 3 and Gen 4 reactors based on the fuels they use and how they are cooled. Traditional, water-cooled Gen 3 reactors use low-enriched uranium, while Gen 4 reactors use high-assay, low-enriched uranium (HALEU) and alternative coolants such as molten salt.

“Each of these technologies has a different role to play in meeting our decarbonization goals,” Huff said. The first step to putting those 200 GW online will be “getting a committed order book of signed contracts for new reactors,” with five to 10 orders for each technology, ideally by 2025.

DOE is providing about $3.2 billion to help fund the construction of two new advanced, small modular reactors (SMRs), but the massive cost overruns and delays that have confounded Southern Co.’s Vogtle 3 and 4 reactors in Georgia have cast a long shadow over the industry, said Julie Kozeracki, a senior adviser at DOE’s Loan Program Office (LPO). (See Making the Case for Nuclear at NARUC.)

With Unit 3 just starting to produce power ― six years behind schedule and at more than twice its original $14 billion price tag ― “nuclear has a huge credibility problem to solve,” said Kozeracki, who helped author the report. “Everyone is staring at each other ― customers, suppliers, reactor designers. … Right now, every utility recognizes that they need new nuclear; they need clean, firm power. But they want to wait for someone else to go first, second, third, and order reactor No. 4 or reactor No. 5.

Launching DOE’s new report on building a strong domestic market for advanced nuclear were (clockwise from upper left) Jigar Shah, LPO; Kathryn Huff, Office of Nuclear Energy; Julie Kozeracki, LPO; David Crane, Office of Clean Energy Demonstrations, and Vanessa Chan, Office of Technology Transitions. | DOE

“But that’s not good enough,” she said. “Because if they all wait for the demo projects to be done, it’s going to be too late, and we’re going to miss the boat. … We need signed contracts, not press releases, not [memoranda of understanding] and not letters of intent, because you can’t finance a supply chain with MOUs.”

The report makes the case for nuclear as a carbon-free technology that checks a lot of boxes for grid reliability, energy security, economic development and equity, points underlined by speakers at Friday’s webinar.

“Between 2023 and 2050, about 200 electric GW of unabated coal assets are expected to retire,” Huff said. “Nuclear energy is uniquely positioned to replace those retiring assets with a similar electricity generation profile.”

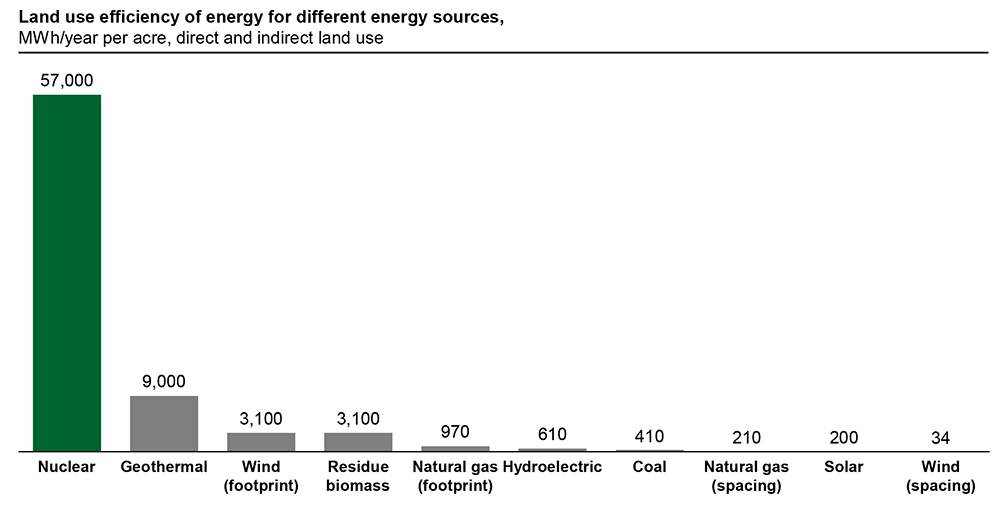

“Deploying clean, firm power sources like nuclear will enable the increased deployment of renewable power,” LPO Director Jigar Shah said. “In addition to providing clean power, nuclear also uses land efficiently [and] has lower transmission requirements; so, they can site themselves on existing coal plant sites … and can leverage existing transmission infrastructure as fossil assets are retired.”

A 2022 DOE study identified close to 400 existing or retired coal plants that could be suitable for advanced nuclear development.

Huff also stressed the economic benefits of coal-to-nuclear transitions for communities affected by the closure of coal or other fossil fuel plants. “Nuclear is one of the few generation sources that can preserve the volume of high-paying jobs from those retiring coal plants,” she said. “A lot of the same people who maintain turbines and steam boilers and electricity around the plant can be rehired, and some of them don’t even need to be retrained to be leveraged into a nuclear power plant.”

The report notes that nuclear plants create about three times the number of jobs per gigawatt compared to wind projects and pay 50% more than wind or solar. Benefits for disadvantaged communities in general are also part of the picture.

“Access to reliable and resilient clean energy resources is not equitably distributed across the U.S.,” the report says. “Increasing grid reliability and resilience for underserved, overburdened communities can support improved health outcomes, public safety, economic security and overall quality of life.”

‘Megaproject Issues’

But how does nuclear compare with the low levelized cost of wind and solar, or even natural gas? It’s a question often asked by nuclear skeptics.

Kozeracki says it doesn’t matter “because of the value it’s providing for a resilient, decarbonized grid. As a clean, firm resource, nuclear doesn’t need to compete with solar by itself or with natural gas by itself. It needs to compete with solar; with really long-duration energy storage, or natural gas with carbon capture,” technologies that have yet to be proven at scale, she said.

The bigger challenge ahead is getting the orders and then completing projects “reasonably” on time and on budget, a measure the report defines as plus or minus 20%.

The report tackles the cost and time overruns at Vogtle, which Kozeracki said “were not nuclear-specific boondoggles. … They are general megaproject issues that you see with any megaproject, from building bridges to Olympic stadiums.

“The design just wasn’t complete enough before construction began, which created a cycle of rework,” she said. “There wasn’t a detailed-enough integrated project schedule or fast-enough turnaround on” quality assurance.

Nuclear is by far the most land-efficient form of power generation. | DOE

Vogtle’s workforce of 9,000 at peak also created “diseconomies of scale,” the result of trying to manage “a city’s worth of people,” Kozeracki said.

One solution for bringing down costs is a “consortium approach,” said David Crane, director of the Office of Clean Energy Demonstrations, which is overseeing the advanced nuclear demo projects. As described in the report, the strategy would allow a group of companies, such as utilities, to “enter a cost-sharing agreement for the construction of multiple reactors, likely of the same design. This pooled demand would allow for sharing risk across multiple owners and could smooth the cost curve from the first reactor to the last.”

This approach also relies on a pipeline of five to 10 projects for different types of reactors, Crane said, so that “first of a kind” does not become “one of a kind.”

“If we could get an order book going for a new wave of nuclear reactors by 2025, then I think we’ll be on our way,” Crane said. “If we don’t start until [2035] … it’s virtually impossible. Given the lead time that’s associated with nuclear, we need to be moving now.”

Crane also said “Gen 3-plus” reactors ― light-water SMRs ― could be an important first step for the industry because of the “synergies” that SMRs have with advanced reactors. Kozeracki agreed, saying that light-water SMRs are a proven technology; the Navy has been using them to power nuclear submarines since the 1950s.

“SMRs may be a bit of a ‘gateway drug’ to get us back into the habit of building new nuclear in the U.S. at scale again,” she said.

Kozeracki pointed to the example of South Korea, which has built out a successful nuclear industry by “picking one design and sticking to it and building it over and over again,” she said. The country recently set a new goal for nuclear to generate more than a third of its power by 2036, up for about 27% today, and to sell 10 reactors on the international market by 2030, according to World Nuclear News.

Supply Chains

By comparison, the U.S. has 92 reactors with a capacity of about 95 GW, a fleet that generates 20% of the nation’s power and 50% of its carbon-free power. If new reactors start coming online by 2030, with a solid supply chain, the report says, the industry could reach a steady state of growth, about 13 GW per year through 2050.

But, as Crane said, even a five-year delay on deployments to 2035 could have serious impacts, requiring an annual growth rate of 20 GW per year, which could result in an overbuilt supply chain.

The challenge here is that the U.S. nuclear supply chain is adequate for keeping the existing fleet fueled but not primed for expansion or advanced technologies. For example, the U.S. has the capacity to mine and mill ― the first steps in processing nuclear fuel ― about 2,000 metric tons of uranium per year. Getting to 200 GW will require hitting 50,000 MT per year.

Other steps in the process are equally lagging, and the country has no commercial capacity at all to produce the HALEU needed for advanced reactors. Previously, the industry depended on a single processing facility in Russia for HALEU, but because of the country’s invasion of Ukraine, companies have had to quickly look for other sources.

The difference between the low-enriched uranium used in existing reactors and HALEU is each fuel’s level of the U-235 isotope needed to sustain a nuclear chain reaction. For low-enriched uranium it is around 5%, but for HALEU, it can be up to 20%.

TerraPower, the Bill Gates-funded company that is developing one of the DOE-funded advanced reactors, announced in December a two-year delay on project completion, from 2028 to 2030, because it has not been able to procure the HALEU it needed. The company’s Natrium project is to be located in Kemmerer, Wyo., near a coal-fired plant scheduled to close in 2025.

Patrick White, project manager for the nonprofit Nuclear Innovation Alliance, said the fuel supply chain for existing reactors is “robust,” but the industry would need clear demand signals before it will be ready to invest in expansion for new light-water SMRs.

“It’s a little bit of a chicken-and-egg problem,” White said in an interview with NetZero Insider. “Uranium enrichment companies and some of the other players in the supply chain [need] a clear line of sight on what their future commercial demand is going to be [so] they know that these major capital investments are worthwhile.”

He estimated that bringing new production online would take three to five years, a time frame that could support Crane and Kozeracki’s vision for an initial buildout of Gen 3+ SMRs.

For HALEU, the challenge is less the enrichment process itself, which is similar to low-enriched fuel, but making sure “your facility is designed and licensed to produce the higher enrichment,” along with some assurance of future demand, White said.

One possibility would be for the government — in this case, DOE — to be an initial off-taker of HALEU in order to guarantee production and sales to help bring companies into the market, he said.

Other recommendations in the “Liftoff” report include low-cost federal loans to suppliers to help them build capacity for future projects, as well as public-private collaboration to create a “HALEU bank,” a stockpile to meet the needs of the demonstration projects.

DOE is actively exploring other options as well. One example is the $200 million that the department provided to X-energy to build a HALEU facility to produce fuel for its XE-100 reactor, the second project in its advanced reactor program. The XE-100 uses a specialized kind of HALEU, which X-energy will produce at a facility in Tennessee. The scheduled online date is 2025.

The department also announced in November a $150 million cost-shared award to American Centrifuge Operating to install the necessary equipment at one of its plants in Ohio to produce HALEU.

Will Utilities Take the Plunge?

Storage of spent nuclear fuel is another major obstacle. According to the report, most reactors in operation are storing their spent fuel on site while the federal government tries to find interim and permanent storage locations. Previous efforts to build a spent fuel storage facility at Yucca Mountain in Nevada were abandoned after strong opposition from the state, as well as environmental and tribal groups.

According to the report, “New legislation would be required to build a federal consolidated interim storage facility or allow development of geologic repositories for permanent disposal at sites other than Yucca Mountain.” DOE is advocating for a new “consent-based siting process” to get local buy-in before attempting to build either interim or permanent storage.

DOE defines consent-based siting as “an approach to siting facilities that focuses on the needs and concerns of people and communities. Communities participate in the siting process by working carefully through a series of phases and steps with the department (as the implementing organization). Each step and phase helps a community determine whether and how hosting a facility to manage spent nuclear fuel is aligned to the community’s goals.”

White says the industry “has a clear understanding of how to keep [spent fuel] in a safe and stable state” for on-site storage at reactors currently in operation. After spent fuel has been cooled for a year or more in cooling pools, it is stored in “dry casks,” metal or concrete-encased containers.

Similar best practices should be used for newer SMRs and advanced reactors, White said.

But both interim and long-term waste storage remain open questions. “I don’t think this is something that’s technically impossible,” White said. “But I think a lot of it is making sure that we’re incorporating both the geology, the nuclear science and the social science, and [making] sure we come up with politically feasible ideas that aren’t necessarily overburdening or unfairly putting the responsibility for managing the waste on any single community.”

Like Huff and Crane, however, White stressed the importance of building a strong order book of five to 10 projects. “The challenge is we get stuck in this process of doing one-off reactors, and we don’t necessarily get the signal that we need to build out an effective supply chain,” he said.

Some utilities are planning for those first, second and third projects. In Washington state, PacifiCorp has partnered with TerraPower on the Natrium demonstration project and recently released an integrated resource plan that included two additional Natrium reactors.

The Tennessee Valley Authority is also moving forward with plans for a GE-Hitachi SMR at its Clinch River site near Oakridge. Speaking at the National Association of Regulatory Utility Commissioners’ Winter Policy Summit in February, CEO Jeff Lyash predicted TVA could build up to 20 nuclear plants by 2050.

“I have no interest in building one reactor,” Lyash said. “In order for us to be successful, TVA needs something on the order of 20 reactors over that period of time. So, if you can’t see your way to reaching nth-of-a-kind costs, supply chain, workforce, project execution for a portfolio of reactors, I don’t see the point in building one.”

WEC Energy Group’s (NYSE: WEC) first-quarter earnings dipped year-over-year after one of the mildest winters in its service territory in more than a century.

The utility reported net income of $507.5 million ($1.61/share) for the first quarter of 2023, a drop from the $565.9 million ($1.79/share) it brought in during last year’s first quarter.

WEC Executive Chair Gale Klappa said the weather was a “major factor” in the earnings results.

“We saw one of the mildest winters in the history of the Upper Midwest,” Klappa said during a conference call with financial analysts Monday. “For example, it was the second-warmest first quarter in Milwaukee since 1891. However, we’re confident in our plan for the remainder of the year.”

WEC serves nearly 4.7 million customers in Wisconsin, Illinois, Michigan and Minnesota.

Assuming normal weather for the rest of 2023, WEC will be able to achieve its annual earnings guidance of $4.58 to $4.62/share, Klappa said.

“We continue to focus on the fundamentals of our business: financial discipline, operating efficiency and customer satisfaction,” he said in a statement. “And we’re confident that we can deliver another year of strong results, in line with our original guidance for 2023.”

WEC’s consolidated revenues totaled $2.9 billion, down $20 million from the first quarter a year ago.

The utility said residential electricity use dropped by 5.8% compared to last year’s first quarter. Small industrial and commercial customer electricity consumption fell by 3.4%, and large commercial and industrial customer electricity use declined 3.9%.

Klappa said WEC continues to make progress on its $20.1-billion, five-year environmental, social and governance plan. He said it’s the largest five-year investment plan in the history of the company and should drive compound earnings growth of 6.5% to 7% annually from 2023 through 2027.

“As we look to the future, it’s clear that the mega-trend of decarbonization and the need for even greater reliability will drive investment plans that are long and strong,” he told analysts.

WEC CEO Scott Lauber said that since last December, the Wisconsin Public Service Commission has granted approval for two solar battery parks and WEC’s purchase of a portion of the solar and natural-gas output from Alliant Energy’s West Riverside Energy Center.

Lauber said work continues on Badger Hollow II Solar Farm and the Paris Solar Battery Park, in which WEC shares ownership interest with other utilities. He said the projects’ remaining solar panels are clearing customs in Chicago, and WEC hopes to place the solar parks into service late this year or early next year.

VALLEY FORGE, Pa. — Stakeholders last week continued to refine proposals to overhaul PJM’s capacity market through the second phase of the RTO’s Critical Issue Fast Path (CIFP) process.

The first stage two meeting on April 19 featured presentations from American Municipal Power (AMP), the Independent Market Monitor and a joint proposal from the East Kentucky Power Cooperative and Daymark Energy Advisors.

A second meeting on April 26 included presentations from MN8 Energy and the Capacity Coalition, a group of five generation companies collaborating to create a combined package. Vistra and Autumn Lane Energy were also scheduled to present on the that day but had to postpone until May 17 because of time constraints.

The proposals aim to address several issues highlighted by the PJM Board of Managers when it initiated the CIFP process in February, including evaluating whether the Capacity Performance (CP) construct is adequately incentivizing resources to meet their obligations and creating stronger winter or seasonal requirements for accreditation and fuel security standards.

The second phase of the process involves forming proposals, which will be finalized in the third stage and voted on by the Members Committee in August. PJM’s Dave Anders reiterated that there is not a hard line between the second and third phase, and proposals can continue to be created and modified at any point.

EKPC and Daymark Propose Two Types of Capacity

The proposal from EKPC and Daymark would create base and emergency capacity variants, with the latter being designed to address extreme weather conditions. Emergency capacity would also be required to have firm fuel or the technical equivalent to it, be available to commit within two hours’ notice and demonstrate the ability to financially withstand any non-performance penalties should it not operate.

“Should they fail to perform and thus not be paid as a consequence of that nonperformance and it could have a substantial impact, the next step should not be that they leave the market because that would be problematic,” Daymark’s Marc Montalvo said.

The base capacity would be focused on addressing systemic conditions and wouldn’t include winterization requirements above those already mandated by NERC. However, the PJM proposal would require all capacity resources to winterize to a higher standard or not receive any revenues for those months.

Adrien Ford of Old Dominion Electric Cooperative said multiple connections to gas pipelines may not be useful as a firm fuel qualification, given that in some locations a single pipeline connection can be more reliable than multiple pipelines in another location.

AMP Seeks Subannual Accreditation

AMP presented a proposal that would create sub-annual accreditation and replace capacity performance, which penalizes and rewards generators depending on whether they meet their obligations during emergencies. Under the concept, all capacity resources would be required to participate in sub-annual auctions, which would clear after the annual Base Residual Auctions (BRAs). Auctions would also be held closer to the delivery year, a shorter time frame than the current three-year advance schedule, reflecting market participants’ experience with auction delays leading to compressed timelines.

“The idea would be that we don’t do away with annual [accreditation] outright. … We firmly believe that the majority of the capacity that clears should be annual, but recognize that monthly or seasonal has value,” AMP’s Steve Lieberman said. The specifics of how granular sub-annual could go would depend on stakeholder feedback in the coming months, he said.

The proposal would replace CP with a regular testing requirement consisting of a penalty and reward structure based on testing performance. The incentives would be based on capacity market revenues and operate on a “pay as you go” basis.

Independent Market Monitor Adds Detail to Proposal

Monitor Joe Bowring provided additional detail on the proposal he unveiled during the first-phase CIFP meetings. The proposal would seek to identify the energy needs for each hour of a delivery year and provide capacity revenues that cover the avoidable costs for generators meeting that need. Capacity would be paid based on annual auction clearing, hourly supply and demand and an annual avoidable-cost rate (ACR).

The Monitor’s plan would base accreditation on a unit’s installed capacity (ICAP) multiplied by its modified availability factor (MAF), an attribute which aims to provide a methodology to capture the availability of all resource types by incorporating forced outage rates, maintenance outages and intermittent resource availability. Bowring said availability would be a stronger measure than PJM’s current effective load-carrying capability (ELCC) measure.

All resources holding capacity interconnection rights (CIRs) would be subject to a must-offer requirement for that capacity and weekly generator testing. Capacity resources would also be required to possess firm fuel or the technical equivalent. For intermittent resources, that would mean being obliged to perform at their full possible output when called upon. Winter Storm Elliott last December showed, however, that firm fuel is not a guarantee of the ability to perform when called upon.

Weekly testing may be considered an “extreme position” for many stakeholders, Bowring said, but he argued that regular testing throughout the year, not just during the summer, recognizes that resources need to be able to perform any time of year.

“If there had been adequate testing, we would not have had either the polar vortex or Winter Storm Elliott” challenges, he said.

Casey Roberts, with the Sierra Club, questioned whether the Monitor’s proposal would consider gas generators to be available if they did not nominate for fuel ahead of potential emergency conditions. Bowring responded the proposal doesn’t currently address that, but it is something all proposals will have to weigh.

Capacity Coalition Presents Short- and Long-term Proposals

Emma Nix of Leeward Renewable Energy and John Horstmann of AES presented a Capacity Coalition proposal that aims to introduce short-term changes to the capacity market through the CIFP process, while putting long-term changes on the table.

The short-term changes include retaining the status quo of exempting renewable resources from the capacity market must-offer requirement, developing transparent and coherent triggers for a Performance Assessment Intervals (PAI), increasing market seller’s flexibility in reflecting their risk in their market seller offer caps (MSOCs), and changing how thermal resources are accredited to reflect expectations of how they would operate through weather and historical performance.

The proposal says that, in the short term, the status quo must-offer exemptions for intermittent and limited-duration resources should remain in place given that capacity is an annual product that commits those resources around-the-clock at times they may not reasonably be expected to be provide capacity. Renewable and storage resources need the exemption so they can adjust their capacity offers based on their individual risk tolerance for Capacity Performance penalties should a PAI be called when the resource is not online, Nix said. Implementation of the seasonal proposal in the long-term would negate the need to maintain the must-offer exception in the short term.

The proposal would also only allow generators to be penalized when there has been advance notice of a PAI, when PJM is not exporting to non-firm load commitments in other regions and when the RTO does not have adequate system reserves. It would limit the bonuses derived from the penalties to only be payable to resources that participate in the capacity market. They are currently paid to any generator that performs above expectations.

PJM’s Becky Carroll said the RTO’s proposal to eliminate the pre-emergency demand response as a PAI trigger could effectively allow DR deployments to serve as advance notice for the potential for generators to be subject to penalties, though she added that there could be PAIs that don’t follow a pre-emergency DR call.

Horstmann said there’s an open question as to what obligations a capacity resource committed in PJM might have to serve load in other regions during an emergency. The coalition proposal seeks to define that as being an obligation to serve PJM’s load.

The proposal also calls for the creation of Capacity Performance quantified risk (CPQR) values for resource classes, to reduce the administrative burden in the unit-specific MSOC process while still allowing companies to reflect their risk across their portfolio.

The long-term side of the proposal calls for a transition from a single annual price to a seasonal capacity model consisting of 12 monthly intervals and four daily intervals by 2030.

The seasonal proposal would align accreditation and offers with how resources are capable of performing during specific times of day. Most important, the RPM auction would set the price for each interval allowing market forces to appropriately establish prices based on PJM system supply and demand needs to incentivize new capacity entry, particularly during times of system need. The coalition includes Leeward, AES, Pine Gate Renewables, Ørsted and Cypress Creek Renewables.

MN8 Energy Suggests ‘Pay as You Go’ Model

A proposal from MN8 Energy aims to build on PJM’s proposed accreditation and risk modeling — namely, capturing a larger breadth of factors affecting generator operation, such as temperature impacts and lead time — while proposing a “pay as you go” model for performance assessment, a seasonal capacity market and additional inputs to CPQR.

MN8’s presentation said PJM’s two-tiered PAI system risks including hours that are not relevant to maintaining reliability and could incentivize some resources in a discriminatory fashion. The PJM proposal would have a minimum of 30 assessment hours for each delivery year, with generators’ performance being assessed in the tightest hours if there are not 30 emergency hours in a delivery year.

The proposal would instead use a pay-as-you-go design for performance assessment where a performance factor would be determined for each generator at the end of a delivery year to calculate compensation. Those resources that underperform would collect a portion of revenues cleared in the BRA, while overperformers would receive all their cleared revenues plus a portion of uncollected revenues as a bonus.

Should the capacity market continue to carry a significant risk of penalties, the MN8 proposal suggests that CPQR should consider opportunity costs, expectations of penalties and bonuses, and the costs to manage risk.

The PJM Power Providers (P3) last week asked the 3rd U.S. Circuit Court of Appeals to overrule a FERC order allowing PJM to recalculate the reliability requirement parameter for Base Residual Auctions (BRAs) after bids have been submitted but before the auction closes.

The commission’s February order was centered on the 2024/25 auction, which would have seen capacity prices increase fourfold for the DPL South locational deliverability area. (See FERC OKs PJM Proposal to Revise Capacity Auction Rules.)

PJM attributed the increase to the reliability requirement calculation including resources that didn’t ultimately bid into the capacity auction. It explained that certain resources, such as disproportionately large generators or intermittent resources, can cause an increase in the reliability requirement to account for the imports needed when they are unavailable.

The RTO “ran an auction consistent with the rules; they didn’t like the outcomes of that auction, and they changed the rules,” P3 President Glen Thomas told RTO Insider.

He said that changing auction rules after companies have entered bids in part informed by those rules amounts to retroactive ratemaking and undermines confidence in the markets.

“If that’s going to be the new normal, that’s going to be something everyone participating in the PJM markets is going to have to consider,” he said.

P3 in its filing pointed to Commissioner James Danly’s dissent from FERC’s order in which he predicted it would be struck down by the courts for violating the filed-rate doctrine. He compared changing auction parameters after bids have been submitted to a game of blackjack in which the house changes the rules after the cards have been revealed.

“The house saves a bit of money on one hand, but no one ever plays blackjack at the Federal Energy Regulatory Casino again. That is this case. The only difference is that the capacity market is not a game but rather the mechanism by which we ensure sufficient generation resources are built and maintained to keep the lights on,” Danly wrote.

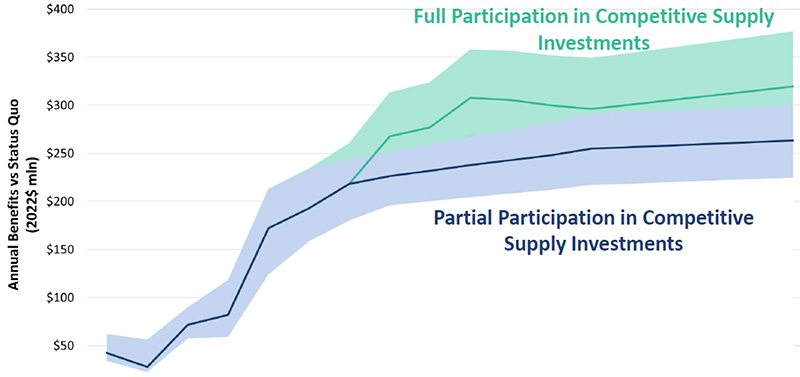

Participating in an RTO could provide South Carolina with benefits of up to $362 million per year, according to a report Brattle Group presented to a special joint legislative committee on Monday.

Brattle Group estimates South Carolina ratepayers can save $25 million to $120 million in the near term and $150 million to $370 million in the long-term if the state transitions to full or partial use of competitive generation supplies. | Brattle Group

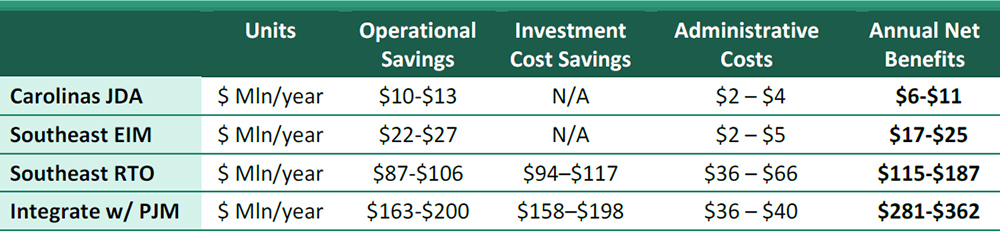

The report to the Electricity Market Reform Committee found that joining PJM would lead to the most benefits (up to $362 million per year), followed by South Carolina — and possibly some of its neighbors — forming a new organized market in the Southeast (up to $187 million). The report also covers a system like CAISO’s Western Energy Imbalance Market (as much as $25 million in net benefits) or setting up a joint dispatch agreement (JDA) between that state’s utilities that would save up to $11 million annually.

Duke’s two South Carolina utilities operate under a JDA, which could be expanded to include Dominion, Santee Cooper (a state-owned public utility) and others that serve the state.

South Carolina could also integrate with an existing RTO, but under a new governance model that would be similar to the Western EIM, with the addition of a day-ahead market and resource adequacy pooling.

Brattle said its savings projections were in line with other benefits studies around the country, which show 4 to 8% operational savings from RTO membership. When Louisiana joined MISO, it was able to cut its reserve margin from 18% to 12%, which is consistent with the savings projected in South Carolina.

Brattle Group estimated South Carolina customers can save up to $360 million per year if the state participates in a regional wholesale market. | Brattle Group

All the scenarios include operational benefits because they let power flow more freely over a wider region, but joining or creating an RTO comes with additional investment cost savings from coordinating resource adequacy over a broader region, which enables lower reserves for the state.

No Loss of Reliability

At Monday’s hearing, Brattle principal and report co-author John Tsoukalis said that the lower reserve margin would still provide the same level of reliability.

“Everybody in the market can achieve the same level of reliability with a slightly reduced reserve margin,” he added.

The main reason joining PJM leads to more benefits than setting up a new Southeast RTO is that South Carolina’s immediate neighbors have similar supplies, so trading power would not bring the state’s utilities as much income as linking up to the more expensive market serving the Mid-Atlantic and Midwest, Tsoukalis said.

Committee members at the hearing asked questions about Brattle’s conclusions, and legislators will use the report to inform their decision on any changes to the state’s regulatory structure. Committee co-chair Sen. Tom Davis (R) said at the hearing that the committee must make recommendations to the full legislature by January.

Setting up a joint JDA, an EIM or a new RTO are all lengthy processes that would include coordinating with entities outside of South Carolina’s control.

Joining PJM is the most expeditious path to full RTO membership, with PJM in the past having taken on new members in as little as 18 months.

“Under this model, South Carolina would operate within all existing RTO market and governance structures, including the option to retain its vertically integrated and state-jurisdictional utility structure,” Brattle said in the report.

Brattle found the biggest benefits came to South Carolina when it worked with its neighbors on its decision, advising the legislature to especially reach out to North Carolina. Dominion Energy North Carolina is in PJM already, but the rest of the state is not in any market.

South Carolina is also considering retail market reforms, but Tsoukalis said that moving on wholesale reforms first would make the most sense as they will inform potential changes to its retail regulations.

The committee posted a document of comments on the study, and while the state’s utilities largely focused on technical findings, AARP South Carolina opposes joining an RTO, saying it bases its views on “the realities of RTOs after 25 years in states that have them.”

“Our members in Texas and California have suffered from power interruptions and higher electricity prices caused by the complicated new RTO-induced structures where no one is clearly in charge of keeping the lights (and air conditioning and heating) on,” AARP said.

VALLEY FORGE, Pa. —

The PJM Markets and Reliability Committee on Wednesday endorsed a new renewable dispatch structure proposed by the RTO and the Independent Market Monitor.

The endorsement directs staff to return to the committee with revised tariff and manual changes incorporating the market changes. PJM’s Darrell Frogg said the structure would provide better data to allow dispatchers to anticipate the output of renewables and increase transparency on performance and forecast accuracy through regular reviews with stakeholders. (See “PJM, Monitor Present Renewable Dispatch Proposal,” PJM MRC/MC Briefs: March. 22, 2023.)

The construct would replace the use of curtailment flags sent to generators through the Inter-Control Center Communications Protocol (ICCP) with economic basepoints. Generators would be directed to follow those basepoints regardless of curtailments because of the potential for inadvertent curtailments.

Renewable resources would be required to offer into the day-ahead market unless they receive approval for an exception for a physical constraint from PJM and the Monitor. Their offers would be based on forecasts of both weather and equipment availability produced by either the market seller or PJM.

Generators would be required to update their critical parameters in real-time security-constrained economic dispatch (SCED) every five minutes and on an hourly basis for parameters in intermediate-term SCED cases.

The lost opportunity cost structure currently available for wind resources would be extended to solar, making them available for payments when they follow dispatch through SCED basepoints.

Paul Sotkiewicz, president of E-Cubed Policy Associates, said the proposal appears to leave a lot undefined at this point. Frogg agreed, but he added that those details will be filled in as tariff and manual language is developed.

Capacity Performance Penalties

Stakeholders discussed three proposals to change when generators can be assigned Capacity Performance (CP) penalties and how they are calculated. Proponents described the changes as an effort to put market changes in place while stakeholders consider longer-term proposals being drafted through the Critical Issue Fast Path (CIFP) process. (See PJM Presents More Detail on CIFP Proposal.)

All three would shift the charge rate from being based on the net cost of new entry to the Base Residual Auction (BRA) clearing price for that delivery year. If the alternative calculation was applied to the 2023/24 delivery year, it would result in a $394/MWh penalty, versus the status quo of $3,177/MWh.

The proposals differ in both the stop-loss limit (SLL) and the trigger for the performance assessment intervals (PAIs) that define when a generator can be assigned penalties or bonuses based on how they match up against their obligation.

LS Power and the Monitor are proposing a limit set at twice the BRA clearing price, while American Municipal Power used a lower SLL at 1.5 times the clearing price.

For the PAI trigger, LS Power and AMP suggested mirroring the provisions in PJM’s CIFP proposal, which would only allow PAIs when there is a real-time reserve shortage and declaration of emergency procedures more severe than pre-emergency demand response. Stakeholders said that DR should be utilized like any other capacity resource, and its dispatch shouldn’t subject other resources to penalties.

“It puts some discipline around when PAIs are called; it gives you some indication about when we’re getting close to when a PAI may be called,” LS Power’s Tom Hoatson said.

The Monitor’s proposal would predicate the implementation of a PAI on a shortage of primary reserves and a PJM declaration of a regional emergency.

LS Power’s Marji Philips said that FERC’s 2021 order on PJM’s market seller offer cap caused generation owners to lose the ability to adequately represent the risks they take on by participating in the capacity market. By reducing CP penalties, she said the proposal would de-risk the capacity market.

Vitol’s Jason Barker said the purpose of the penalties is to incent behavior, and reducing that wouldn’t lead generators to make the investments lessening the likelihood of events similar to the December 2022 winter storm.

“From our perspective there has to be a meaningful penalty,” he said.

PJM’s Adam Keech said the RTO is comfortable with the proposed changes to the PAI trigger, but it has concerns with reducing penalties without addressing the other side of the ledger: winterization and other mandates that would require capacity resources to improve their ability to perform. He said that the high penalties were a tradeoff to limited hard rules, and the proposals would significantly decrease penalties without introducing other ways of ensuring performance.

The LS Power proposal was introduced to the committee as a quick fix, meaning that the issue charge, problem statement and solution could be voted on during the same meeting. Noting the hourslong discussion it generated on Wednesday, some stakeholders questioned if it met the criteria of an issue that could be addressed with minimal stakeholder input.

Special meetings of the MRC and Members Committee have been scheduled for May 4 and 11, respectively, to further discuss the issue and potentially vote on endorsement.

Stakeholders Endorse Manual 11 Changes

Stakeholders endorsed revisions to Manual 11, which pertains to energy and ancillary services market operations, through the biennial cover-to-cover review of the document. Stakeholders deferred a vote on the changes during last month’s MRC meeting to allow more time to review amendments proposed in an effort to align the language with PJM’s other governing documents. (See “Other Stakeholder Discussions,” PJM MRC/MC Briefs: March. 22, 2023.)

The revisions presented at the second read on March 22 were revised to remove changes to the operating parameter definitions affecting the minimum run time for combined cycle units. The excised language is anticipated to return after being reviewed by the Governing Document Enhancement & Clarification Subcommittee.

Working Groups Begin Addressing Grid of the Future

KANSAS CITY, Mo. — SPP members and the RTO’s Board of Directors last week embraced an advisory group’s report on a future grid that is fast approaching, directing stakeholder groups to begin addressing the group’s recommendations.

The board on April 25 accepted the Future Grid Strategy Advisory Group’s (FGSAG) report that identified potential gaps between future state projections and current trajectories, and urged increased organizational awareness of the opportunities to shape the future grid.

The directors had charged the group in 2021 to explore how the grid will change over the next 10 to 15 years and to make recommendations that help SPP and its membership prepare for those changes. The report identifies trends and strategic pathways that could be disruptive and game changing and makes 32 recommendations to address them.

SPP says the grid’s future is “vitally important” to its stakeholders and that the FGSAG’s work sets the stage for their discussions and readies staff to meet its members’ needs. Of course, that work will have to be balanced with ongoing initiatives.

“We are often dealing with what’s right in front of us and trying to react to changes that are occurring. … Things can look very complicated when we’re trying to address them,” Advanced Power Alliance’s Steve Gaw, a member of the group, said during the board’s quarterly meeting. “If we only look down in front of our feet at what we are about to step on, we sometimes lose our way because we don’t look up. This is an attempt I think not to say that we should be constantly looking up and forgetting what’s right in front of us, but an attempt to balance what’s going on out ways in front of us so that we don’t lose our way with distraction of what’s the latest urgency.”

“I think one of the challenges is how do you balance all of this new work with the existing work,” Director John Cupparo said. “The work groups that are going to be tasked these assignments would come back with some timelines and work plans for how that work will fit in with all the existing [work] so that we can see the balancing of that and understand the tradeoffs.”

The FGSAG gathered assessments last year from surveys, industry experts and organizational expertise to compile a list of recommendations. The Strategic Planning Committee endorsed the work in January and requested the board to direct the appropriate organizational groups to begin considering each recommendation.

The group categorized the results into four areas: consumer trends, policy implications, resource impacts and transmission possibilities. Four sub-teams then drafted white papers that examined each topic’s concerns and defined preliminary recommendations. Because the sub-teams’ recommendations had some overlap and common themes, the full FGSAG reviewed and consolidated them into a final list, grouped into five categories:

energy adequacy/modeling/planning;

grid services/market design/operations;

transmission;

demand-side resources; and

innovation and collaboration.

The report sets out a three-phase plan to address its recommendations and provide progress reports back to the SPC:

educate primary working groups on the relevant recommendation and secondary and advisory working groups for input as needed;

draft initiatives that address the recommendations and develop tasks and outcomes to ensure their inclusion in SPP’s comprehensive roadmap; and

report quarterly on the initiatives’ progress and update the board on their implementation’s appropriateness, scope and pace.

The effort has been led by Mark Ahlstrom, NextEra Energy Resources’ vice president of renewable energy policy and board chair of Energy Systems Integration Group, a nonprofit engineering, resources and education association.

“Basically, what we’re planning to do is to take the recommendations that apply to each of the organizational groups out to them over the next six months or so, start the process of educating them, helping them understand it, get their feedback, and then engage other secondary and advisory groups,” Ahlstrom said. “It’s going to be an evolving set of things that we have to make sure we’re on top of and we get feedback and we evolve and improve as we go. I think you’re going to be seeing a lot of us as we continue to make sure that we keep ahead of the curve on what has to be done before we get to that 10- to 15-year time frame.”

The Inflation Reduction Act has added a complicating factor. The FGSAG said it attempted to document the legislation’s expected implications but that it will take more time and analysis to fully understand and address all its implications on generation, electrification, loads for green hydrogen production and economic development.

“What is already certain, though, is that the IRA’s impact on the SPP region will be dramatic,” the report said, pointing to tax credits for renewable, nuclear, green hydrogen production and energy storage.

“I can’t emphasize enough this is not going to be a one-and-done,” Ahlstrom said. “This is going to be an ongoing activity, but hopefully about a year from now, we would expect to see some sort of plan about how this will be taken up in methodical way by the various organizational groups and by staff.”

MMU Report: Energy Prices up

SPP’s Market Monitoring Unit gave the board and stakeholders a first peek at its annual report on the SPP market and its outcomes that reflect changing conditions.

According to the report, high natural gas prices resulted in increasing energy prices; the Panhandle Eastern hub’s average gas price of $5.83/MMBtu, up 69% from the year before, led to day-ahead and real-time prices of $48/MWh and $43/MWh, respectively, up 80% and 75% from 2021. Data from February 2021 was excluded to avoid skewing the metrics.

The SPP market also experienced continued higher renewable penetration and increased make-whole payments, congestion and revenue neutrality uplift. Keith Collins, the MMU’s vice president, said he wouldn’t be surprised if wind energy reaches a 40% share of SPP’s generation mix this year.

“SPP is in fact a wind system. At one time it was a coal system, but I think SPP is in fact a wind-dominated system,” he told stakeholders.

The MMU said the market’s challenges — increasing variability and supply uncertainty, out-of-market reliability actions, higher make-whole payments and more negative prices — are not necessarily new developments. It said addressing resource adequacy is “perhaps the most important lesson” from the severe winter storms of the last two years; the key issues include a lack of a seasonal resource adequacy requirement; fuel availability risks; correlated output and outages among similar resources; and an accreditation process that does not reflect actual resource performance.

“The SPP system was lucky to have significant imports from MISO, PJM and others. SPP cannot plan to count on these systems to help SPP in a future event as a wider regional cold snap could limit imports,” the report says.

“It’s important to know that the resources we have in the system can be counted on during these events,” Collins said. “We need incentives to ensure that that capacity is available. … We know we’re moving to winter [resource adequacy] requirements. I think we’ve seen evidence that having requirements in the shoulder periods as well is actually a growing importance.”

The MMU is adding four new recommendations for 2022:

consider limitations on virtual trading during emergency conditions;

address limitations with the ramp capability introduced last year;

improve situational awareness of transmission upgrades and the process to reassign projects; and

improve congestion-hedging mechanisms to make them more equitable.

The Monitor said it “has and will continue to engage in the SPP stakeholder processes to help promote improved resource adequacy in the SPP market.”

The final market report is expected to be released in May. The 267-page opus will likely meet with approval from Google’s Betsy Beck, who has a market monitoring background and professes to read market reports “back to back, cover to cover every year.”

“I love these State of the Market reports. There’s always so much great information in the report itself,” she said. “The MMU puts a tremendous amount of work and really good analysis, and you can get a sense of all the different pieces of the market — how things are working well together or not — from reading the report.”

Uri Helps SPP Response to Elliott

SPP staff told the board and members that lessons learned from the 2021 winter storm (also known as Winter Storm Uri), many of which are still being incorporated into daily processes, were “extremely helpful” in the grid operator’s response to the December winter storm (also known as Winter Storm Elliott) when accredited generation fell short of demand at times.

Still, staff identified 11 recommendations during a thorough review of its performance during Elliott that could help the RTO and its stakeholders be better prepared for extreme events in the future. The recommended changes are to internal processes, tools or functions and should not require additional resources or stakeholder prioritization to complete, staff said.

The board approved the latest recommendations as part of its consent agenda.

Mike Ross, senior vice president for external affairs and stakeholder relations, said almost two-thirds of recommendations from Uri are complete. He said the rest should be completed by 2025, depending on FERC and other approvals, and that staff have recommended staying the course on the Uri recommendations.

The new recommendations include improving situational awareness of neighboring conditions; adding extreme weather risks to SPP’s transmission planning process; and identifying options to better mitigate and manage congestion during extreme winter events. SPP did not have to shed load during Elliott as it did during Uri, but the balancing authority area came close, and Empire Electric District had to shed about 25 MW of load for 15 minutes. (See “December Storm Raises Same Issues,” SPP MOPC Briefs: Jan. 17-18, 2023.)

“While there was no load shed directed by SPP, we came closer than we would have liked,” Ross said.

The two storms have both presented significant challenges to maintain reliability, staff said. Coal outages and derates were actually worse during Elliott, Ross said, and drove home the point that two “historic” extreme weather events 20 months apart are a harbinger of what the future holds.

“I think we’re going to stop using the term, ‘100-year storm,’” SPP CEO Barbara Sugg said.

Sugg Drops the Mic

Sugg reflected on the year’s first months that included a tornado touching down within a half-mile of the RTO’s headquarters building in Little Rock, Ark., continued market expansion into the Western Interconnection and advancements in clearing the generator interconnection queue’s backlog.

In sharing the organization’s progress against its strategic plan, Sugg pointed to the traditional dinner that follows the Regional State Committee meeting the night before the board meeting as an example of SPP’s stakeholder-driven culture. The casual dinner brings together the board’s directors and the RTO’s staff, members, regulators and other stakeholders.

“It was loud; it was rowdy; and it was fun. It felt like old times, and it was great to see everybody having a good time,” she said. “Just that dinner alone is one of the things that makes SPP extremely unique, because you will not find that in another region. Building relationships … is the cornerstone of SPP and is really what makes SPP great.”

In closing her report to the board, Sugg reiterated a statement she has made before: “There is no place I would rather be than working collaboratively here with all of you and back at the office with all of our amazing staff to achieve our vision of leading our industry to a brighter future while delivering the best energy value. That’s my mic drop moment.”

2022 Annual Report Available

SPP has released its annual report for 2022 and for the third year in a row, it will be in a virtual format.

The report details the grid operator’s performance during the year. The RTO says it provided $3.787 billion in value to its members and expanded the services it is providing stakeholders in the Western Interconnection.

It also summarizes SPP’s response to Elliott, improvements to generation interconnection, development of a consolidated transmission planning process, and staff’s and members’ focus on the future grid.

New Members Committee Reps

The Members Committee welcomed three new representatives who will serve in an interim capacity until they are officially elected during the October membership meeting:

Stacey Burbure, legal counsel for American Electric Power, replacing AEP’s Peggy Simmons;

Al Tamimi, vice president of transmission planning and policy for Sunflower Electric Power, replacing retired Sunflower CEO Stuart Lowry; and

Christy Walsh, director of federal energy markets for Natural Resources Defense Council’s Sustainable FERC Project, replacing Invenergy’s Daniel Hall.

The meeting was also Tom Christensen’s last as an MC member. He is retiring from Basin Electric Power Cooperative in May as senior vice president of transmission, engineering and construction.

Consent Agenda Passes

Members and the board approved a consent agenda that contained one revision request:

RR530: identifies consistent criteria for when it is acceptable to implement a transmission reconfiguration, and outlines responsibilities for the reliability coordinator and transmission operator in developing mitigation plans to avoid system operating limit exceedances.

The consent agenda included several other items, including:

the Oversight Committee’s recommendation for the 2023 industry expert pool that will review and evaluate proposals for competitive transmission projects. The pool includes 15 holdovers from last year and two new members: independent consultant Frank Lembo, a former chief engineer with Consolidated Edison, and Mark Lawlor, a renewable developer with EDP Renewables and Clean Line Energy Partners.

a 26% increase for Basin Electric’s 60-mile, 230-kV sponsored upgrade project in North Dakota near the Canadian border. An additional 5 miles of transmission line bumped the project’s cost from $64.9 million to $81.4 million.

FERC on Friday approved Duke Energy’s (NYSE:DUK) settlement with two co-ops to reflect lower corporate tax rates from the Tax Cuts and Jobs Act of 2017 enacted under former president Donald Trump (ER23-1206).

FERC Order 864 required utilities to reflect the cut in the federal corporate income tax from 35% to 21% in their formula rates, specifically their accumulated deferred income tax (ADIT). ADIT is meant to account for the timing differences between filing taxes with the IRS and the method of computing them for regulatory and ratemaking processes.

The lower federal taxes meant that some of utilities’ ADIT collected from consumers was no longer due to the IRS. Order 864 was meant to ensure that ratepayers were made whole for those over-collections and that going forward utilities would have to reflect tax changes in their rates in a transparent manner.

Duke made its initial compliance filings for Duke Energy Carolinas, Duke Energy Progress and Duke Energy Florida in 2020, as required, but FERC sent it back for some additional clarifications. (See FERC Directs More Clarity in Order 864 Filings.)

The utility filed changes, but a limited protest came from two of its wholesale customers: North Carolina Electric Membership and Central Electric Power Cooperative.

The two customers said that Duke proposed changes that were not required by FERC’s initial order. Duke’s filing would have changed how it calculated “average rate assumption method” (ARAM) rates, using the “best available data” instead of calculating them in the fourth quarter of the previous year.

They argued that the changes were ambiguous and would let Duke base its calculation on a period other than the fourth quarter of the previous year, which could lead to a mismatch in how ARAM and ADIT rates are calculated. Neither the customers nor FERC had a chance to fully vet the proposal, they said.

Duke asked FERC to hold the proceeding in abeyance so it could negotiate with the co-ops and came to a deal with them before submitting the compliance filing approved Friday.

The firm is proposing revisions to each utility’s formula rate to clarify that the ARAM rate used for the amortization of excess deferred income tax from the tax cut will be the “ARAM rate based on the last filed final federal corporate income tax return, after all permitted federal extensions” as of the date of posting the annual update.

FERC found that Duke’s proposal complies with Order 864 and addresses the co-ops’ concerns, making their protest moot.

The commission accepted Duke’s proposal to return excessive ADIT to customers — or collect shortfalls from them — effective June 1, 2020. The commission said the utility had held customers harmless for the new tax rates in its 2018 and 2019 annual updates. FERC agreed that the June 2020 date would not adversely impact customers.

Surveillance photos from Tacoma Power showing Greenwood at the Elk Plain substation. | Tacoma Power

Surveillance photos from Tacoma Power showing Greenwood at the Elk Plain substation. | Tacoma Power