The New England States Committee on Electricity (NESCOE) pressed transmission owners Thursday to increase the transparency of their asset condition projects and incorporate them into ISO-NE’s planning process.

In a presentation to the Planning Advisory Committee (PAC), NESCOE also called for more information on spending plans and assumptions used in estimating project costs. NESCOE also suggested the RTO create guidelines around right-sizing transmission projects and integrating asset condition project planning into the RTO’s regional planning process.

Thursday’s discussion came in response to NESCOE’s Feb. 8 memo to the New England Transmission Owners (NETOs), which called for maximizing the use of the region’s transmission, saying that “modernizing planning processes and protecting system reliability will be fundamental in the transition to the clean energy future.”

Asset condition projects are undertaken by transmission owners to maintain transmission infrastructure that is aged or damaged. While ISO-NE directs the regional transmission planning process for transmission reliability projects, asset condition projects are not included in this process and are therefore subject to less scrutiny from other stakeholders.

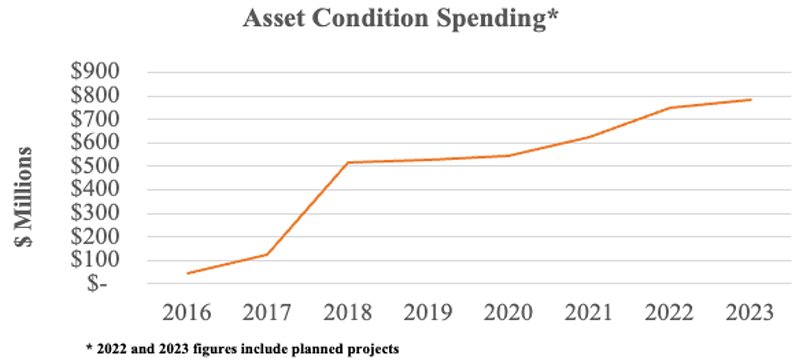

NESCOE has previously highlighted how costs associated with asset condition projects have been trending upward in recent years, with over $3 billion in projects currently proposed, planned or under construction. Asset condition project costs are eventually passed on to ratepayers.

“The process by which asset condition projects are developed by NETOs, reviewed by ISO-NE, states and the public, approved for rate recovery, and considered in overall transmission system needs and planning is antiquated and ultimately, inadequate,” NESCOE wrote in its February request to reassess the planning process. “It is the right time to implement planning process improvements to protect consumers from excessive costs and to maximize the use of all transmission assets by moving Asset Condition Projects from the current siloed, notice-based method into meaningful and holistic transmission system planning.”

In a memo sent to participants prior to the PAC meeting on behalf of consumer advocate members of NEPOOL, Synapse Energy Economics argued that the current process risks putting unnecessary burdens on ratepayers.

Asset condition spending since 2016 | NESCOE

“Asset condition spending now constitutes the majority of new regional transmission investments and is projected to continue increasing,” Synapse wrote. “Ratepayers ultimately bear the costs for asset condition projects, but unlike other investments that have cost reviews built into approval processes, there is little to no meaningful check on the prudency of asset condition spending.”

NESCOE wrote in its February memo that modernizing planning procedures is also important in anticipation of increased reliance on clean energy technologies in the energy transition.

“The question of whether and to what extent to ‘right-size’ transmission to account for broader potential needs will arise more often in the future as the region considers transmission expansion to account for clean energy resources and state decarbonization requirements,” NESCOE wrote.

In its March 2 response to NESCOE’s memo, the New England Transmission Owners expressed their support for a review of the planning process while emphasizing their commitment to reliability and transparency. “Specifically, we agree that there is an opportunity to better integrate asset condition planning with longer-term planning for transmission to meet future system needs,” they wrote.

At the PAC meeting, NESCOE asked for feedback from stakeholders to be submitted to pacmatters@iso-ne.com by June 2.

Asset Condition Projects

Also at the PAC meeting, National Grid and Eversource outlined their plans to spend a total of $492.4 million on infrastructure updates and repairs, while New Hampshire Transmission detailed a projected $14 million cost increase for its Browns River capacitor bank station.

New Hampshire Transmission, a subsidiary of NextEra Energy, said that the cost estimate for the capacitor bank station it is building near the Seabrook nuclear plant in Southern New Hampshire has more than doubled, increasing from $8.9 million to $22.9 million. The company said that most of the projected increase — $10.9 million — is because of additions to the scope of the project, with an additional $3.1 million increase resulting from rising costs, including changes in commodity prices.

National Grid projects that the relocation of its substation in Adams, Mass., will cost $133.5 million, with an expected in-service date of early 2030. The current substation is located in a wetland area along Hoosic River and is frequently subject to flooding events. The proposed new location is at a higher elevation next to a mobile home neighborhood in North Adams.

Eversource expects to spend a cumulative $358.9 million on a series of transmission infrastructure rebuilds and replacements in New Hampshire. In Northern New Hampshire, the company would replace wood structures with new steel structures and install optical ground wire on 115-kV lines B112, Q195 and U199, with respective in-service dates of late 2024, late 2026 and mid-year 2026. The company would also replace wood structures with steel structures and replace 49 circuit miles of shield wire with optical ground wire on 115-kV and 345-kV lines in Southeastern New Hampshire, with in-service dates ranging from late 2023 to early 2024.

Most regions of the North American grid remain at elevated risk of supply shortfalls this summer, NERC said in its 2023 Summer Reliability Assessment released Wednesday, with an organization official warning the media that “the system is close to its edge.”

In presenting the assessment, John Moura, director of reliability assessment and performance analysis, and other NERC staff stressed the impact on reliability of changing weather patterns, combined with the transition to renewable energy sources that has left some areas relying on weather-dependent technologies like wind and solar power. In a video released alongside the report, NERC said that “generator retirements continue to increase the risks associated with extreme summer temperatures.”

“With the grid transformation in full force, the retirement of conventional generation remains highly concerning,” Moura said. “That’s something that we’d really like to focus on in the coming years as we … respond to environmental rules [and] enable a cleaner grid, but also maintain reliability every step of the way.”

Weather Driving Demand

NERC publishes the assessment each year to identify potential regional reliability issues and topics of concern, covering the June to September timeframe. This year MISO, Ontario and New England, SPP, ERCOT, SERC’s Central subregion — comprising all of Tennessee and portions of Georgia, Alabama, Mississippi, Missouri and Kentucky — and the U.S. Western Interconnection all “face risks of electricity supply shortfalls during periods of more extreme summer conditions,” the assessment said.

According to the National Weather Service, above-normal temperatures are likely across most of the continental U.S. and Alaska, while most of Canada is expected to see normal or below-normal temperatures.

The assessment marks an improvement in one regard from last summer because MISO is no longer assessed at high risk, which indicates the potential for insufficient operating reserves in normal peak conditions. NERC said the reduced risk level is because of higher firm import commitments coupled with lower forecasted demand for the region, though its resources are also projected to be lower than last year. MISO’s anticipated reserve margin has increased to 23% this year, from the 21% predicted for summer 2022.

Resources are also expected to be lower this year in New England and Ontario, though still adequate for normal peak demand, confirming the regional entity’s own summer assessment released earlier this month. (See NPCC Warns of Tight Summer Margins in Ontario.) NERC warned that “generation and transmission outages will be increasingly difficult to accommodate” in Ontario for the foreseeable future because of generator retirements, especially among the province’s nuclear fleet.

NERC also expressed concern that utilities would be “unable to reschedule certain outages” during summer, as the Northeast Power Coordinating Council suggested in its assessment. The ERO said that Ontario might need to rely on as much as 2,000 MW of non-firm supply from other areas, along with “additional operating actions,” though NPCC said the province would likely need “only limited use” of its operating procedures during the summer.

SERC-Central has seen its forecasted peak demand rise by more than 950 MW since 2022, with no accompanying growth in anticipated resources. However, while the subregion’s prospective reserve margin is significantly lower than last year as a result, entities reported to NERC that they expect to “address unexpected short-term issues by leveraging diverse generation portfolios and spot purchases from the power markets when necessary.”

IBR Issues Continue in Texas

Mark Olson, NERC | NERC

For Texas, the report’s authors noted that the growth of inverter-based resources (IBRs) in the region continues to create concerns around “system stability and strength,” along with rising curtailments of energy production because of transmission constraints, frequently at solar sites. The ERO has issued multiple warnings about the reliability of IBRs in recent years after events like the Odessa disturbances in 2021 and 2022, when the Texas Interconnection lost multiple gigawatts of solar PV and synchronous generation. (See NERC Repeats IBR Warnings After Second Odessa Event.)

Mark Olson, NERC’s manager of reliability assessments, also observed that the region’s growing use of solar generation carries additional risks because of the mismatch between solar PV sites’ most productive time in the early afternoon and the period of greatest demand later in the day. Without dispatchable generation, utilities may find themselves operating closer to the edge than the numbers would indicate at first glance.

In WECC’s U.S. footprint, NERC warned that while resources in the interconnection are sufficient to support normal peak demand, a wide-area heat event could create problems for multiple subregions that normally rely on regional transfers to meet peak demand when solar production falls off. In addition, the assessment noted the risk of wildfires to the transmission network, which can limit the transfer capacity and lead to localized load shedding.

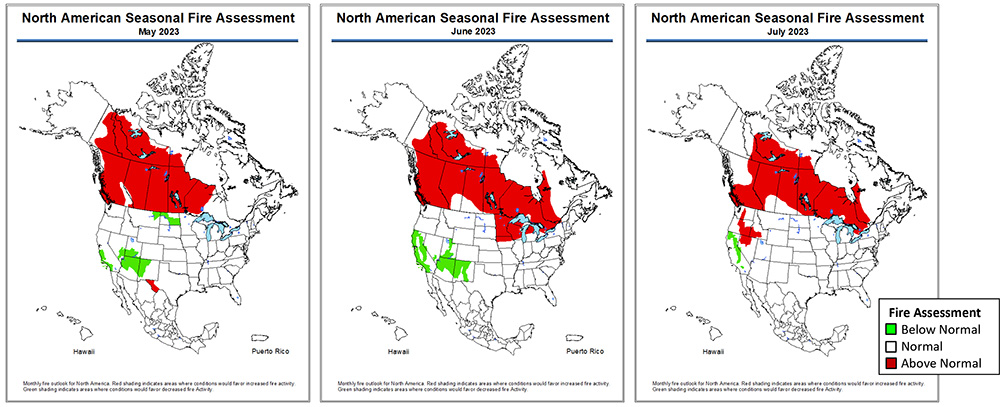

North American seasonal fire assessment for May through July 2023. | NERC

Olson also noted that while California’s hydroelectric system has experienced some relief from snowmelt refilling reservoirs, it is too early to tell whether this supply will continue to aid the region in late summer.

“Higher temperatures now can lead to a lot of melt early on, [but] much of the summer risks in the West tend to be later in the season when hydro is normally starting to be lower. So it’s harder to project how the current rainfall and snowpack may play out later into the season,” Olson said.

Supply Chain, Spare Parts Issues

Other potential reliability issues noted in the report include low inventories of replacement parts, such as distribution transformers, that could delay restoration of power following hurricanes and severe storms. Additional supply chain issues, along with labor shortages, could cause challenges for maintenance, summer preparedness and new resource additions.

The assessment also noted that EPA’s Good Neighbor Plan, which will require significant reductions of emissions at power plants and industrial facilities in 23 states, will likely limit the operation of coal-fired generators that are currently used for dispatchable generation. (See EPA Good Neighbor Plan Expected to Accelerate Coal Plant Retirements.) NERC recommended that entities familiarize themselves with the plan’s electric reliability provisions and be prepared to “act to preserve generation resources … to support periods of high demand.”

Industry groups seized on the assessment’s warnings about coal retirements as ammunition in their arguments against both the Good Neighbor Plan and EPA’s more recent proposals for carbon dioxide emission standards at power plants. (See Regan: New EPA Standards Designed to not Jeopardize Grid Reliability.) America’s Power, which represents coal-fired generators, said in a statement that retiring coal plants “will needlessly expose consumers to potential power outages,” while Jim Matheson, CEO of the National Rural Electric Cooperative Association, said that “America’s ability to keep the lights on has been jeopardized” by growing demand and restrictions on supply.

“American families and businesses expect the lights to stay on at a cost they can afford. But that’s no longer a guarantee,” Matheson said. “Nine states saw rolling blackouts last December as the demand for electricity exceeded available supply. … Absent a major shift in state and federal energy policy, this is the reality we will face for years to come.”

The results of MISO’s inaugural seasonal capacity auctions, released late Wednesday, showed sufficient supply for the 2023/24 planning year, with prices ranging from $2/MW-day in winter, to $10/MW-day in summer and spring, and $15/MW-day in fall.

The RTO’s first set of concurrently conducted seasonal capacity auctions is a far cry from last year’s annual auction, which cleared all of MISO Midwest at the nearly $240/MW-day cost of new entry (CONE), signifying a critical need to build resources. (See MISO’s 2022/23 Capacity Auction Lays Bare Shortfalls in Midwest.)

This year, all zones were shown to have enough capacity on their own. Even MISO’s external resources zones followed suit. However, Zone 9 in Louisiana and southeast Texas experienced price separation to meet its requirements and cleared at $59.21/MW-day in fall and $18.88/MW-day in winter, the only departure from the otherwise uniform clearing prices.

The RTO said the mostly flat prices were a function of adequate supply this year. It entered the auctions with a 133-GW summer planning reserve margin requirement systemwide. The Midwest region was able to turn its previous deficit around through a combination of “lower demand, new generation, delayed retirements, additional imports and higher accreditation.”

While wind, gas and solar units in the Midwest were able to increase their accredited capacity values by nearly 2 GW, the region’s coal resources lost 924 MW in accredited capacity owing to MISO’s new availability-based accreditation process that assigns thermal units value based on past performance and anticipated availability during predefined risky periods. (See FERC OKs MISO Seasonal Auction, Accreditation.)

2023-24 Planning Resource Auction clearing prices by zone and season | MISO

The grid operator said members offered capacity in the Midwest that exceeded the summer planning reserve margin by 4,760 MW, compared to the 1.2-GW deficit uncovered in last year’s auction.

On the other hand, MISO South offerings declined this year. Though the subregion still beat its summer requirement by 1,723 MW, it was not as robust as last year’s 2.8-GW surplus. MISO said the South’s natural gas, nuclear and other generating units lost a little more than 1 GW in accredited capacity through the new accreditation process.

MISO’s Independent Market Monitor has reviewed and certified the auction results, finding no exercise of market power.

The RTO said the adequate supply this year is not indicative of “continued risks posed by the portfolio transition.” It said its move to seasonal requirements reduced the summer planning reserve margin. It also said its lower load forecast this year might become an anomaly, so members cannot postpone their planned generation retirements indefinitely. Projects continue to show a “continued decline in accredited capacity even as installed capacity increases,” MISO said.

Since last year, MISO Midwest has retired almost 1.2 GW worth of coal, while MISO South has retired about the same amount from its natural gas fleet.

The grid operator said it continues to need “urgent reforms” to its resource adequacy and market design to ensure reliability.

Entergy’s operating companies have challenged MISO’s seasonal capacity market at the D.C. Circuit Court of Appeals (22-1335). They are asking the court to review FERC acceptance of MISO’s availability-based capacity accreditation for thermal resources, the timeline to move to the seasonal market and the 120-day advance notice requirement for planned outages, among other elements of the commission’s order.

NV Energy will keep looking for resources to replace its coal-fired North Valmy Generating Station, scheduled for retirement in 2025, after Nevada regulators shot down the utility’s plan for a $466 million battery storage system.

The Public Utilities Commission of Nevada (PUCN) voted 3-0 last week to reject the project. The battery storage system was part of NV Energy’s fourth amendment to its 2021 integrated resource plan (IRP). The commission approved the amendment in part, but denied some components.

NV Energy had planned to replace capacity lost from the North Valmy coal plant closure with the Hot Pot and Iron Point solar-plus-storage projects. The 522-MW North Valmy plant, in Northern Nevada, is NV Energy’s only remaining coal-fired power plant.

Hot Pot and Iron Point together would provide 600 MW of solar paired with 480 MW of battery storage. In January 2022, PUCN approved NV Energy’s plan to buy Hot Pot and Iron Point from developer Primergy Solar.

But in its proposed IRP amendment, NV Energy said that due to supply-chain issues, Hot Pot and Iron Point are “no longer expected to move forward as previously approved.”

The 200-MW Valmy battery system was intended as a substitute for Iron Point and Hot Pot. NV Energy acknowledged the four-hour battery system wouldn’t be a total answer to the North Valmy coal plant closure, but said more resources could become available in Northern Nevada in the future.

But the commission wasn’t ready to give up on Hot Pot and Iron Point, saying NV Energy had “provided limited evidence” about the projects’ status.

“The commission finds it premature and unreasonable to approve the $466 million Valmy BESS investment as a cost-effective replacement for the Valmy coal plant without all the necessary facts,” the order stated.

The commission directed NV Energy to come up with a “complete solution” for the Valmy retirement in the next amendment to the 2021 IRP, or in its 2024 IRP, whichever comes first. The utility said it would file a fifth IRP amendment over the summer.

PUCN also asked for a thorough analysis of financial impacts of each potential solution for the Valmy closure.

And the commission wants details on “federal and state limitations on continued operations of the Valmy coal plant and associated costs.”

Another issue, the commission said, is whether NV Energy or its customers are entitled to damages resulting from delays in the Hot Pot and Iron Point projects.

Postponed Retirements

In another part of the fourth amendment to its 2021 IRP, NV Energy proposed a 400-MW gas-fired peaker plant in Southern Nevada, which PUCN approved in March. (See Nev. Regulators OK Controversial Gas-fired Peaker.)

NV Energy also asked to postpone retirements of several gas-fired plants by five or 10 years. The commission approved the extensions and, in some cases, postponed the retirements even further. That includes the Silverhawk and Higgins generating stations, for which NV Energy had proposed a 2044 retirement date. Instead, PUCN set a 2049 retirement date, in recognition of the state’s 2050 target for economywide net-zero greenhouse gas emissions.

“At a time when planning to meet the energy needs of customers is more complex, the commission believes that all cost-effective options which also allow NV Energy to meet state environmental requirements should be modeled and considered,” the commission’s order said.

The commission also approved NV Energy’s addition of a 120 MW portfolio of geothermal resources.

NV Energy said the IRP amendment was intended to reduce Nevada’s dependence on the open energy market, improve reliability and advance the state’s clean energy goals.

FERC on Thursday approved CAISO’s second attempt at complying with Order 2222, which requires RTOs and ISOs to foster participation of distributed energy resource aggregations (DERAs) in organized markets.

Thursday’s ruling found that CAISO fully addressed the directives the commission laid out last June in its order on the ISO’s first compliance filing (ER21-2455). In that order, FERC said the ISO — as the first RTO/ISO to implement a DERA model — had already complied with “the vast majority” of Order 2222 mandates, but the commission determined its proposal came up short in a number of areas. (See CAISO Order 2222 Filing Needs Some Work, FERC Says.)

Chief among the commission’s concerns last June was CAISO’s partial compliance with Order 2222 provisions around the role of distribution utilities in DERA market participation.

Order 2222 requires RTO/ISO markets to accept bids from a DERA if the aggregation includes resources that are customers of utilities that distributed more than 4 million MWh in the previous fiscal year. But it prohibits grid operators from accepting bids from an aggregation that includes resources that are customers of smaller utilities without the approval of the relevant electric retail regulatory authority.

Thursday’s ruling found that the ISO’s revised proposal had complied with FERC’s directives to:

specify the criteria utilities must use to determine whether each DER is capable of participating in an aggregation;

develop a process in which utilities will determine that a specific DER’s participation in an aggregation “will not pose significant risks to the reliable and safe operation of the distribution system;” and

share with utilities any “necessary information” and data collected about the individual DERs participating in an aggregation.

The commission further found that CAISO’s revised proposal met a requirement that the ISO share with a DER provider any information about a DER that a utility provides to CAISO as part of the utility review process. In approving CAISO’s related tariff revision, the commission also ruled that Pacific Gas and Electric’s protest that the rule could conflict with non-disclosure obligations between the ISO and utilities represented an “untimely request for rehearing” of FERC Order 2222-A, since PG&E “did not seek rehearing or clarification of the commission’s determination during the rehearing period of that order.” But the commission added that it acknowledged PG&E’s concern about “the appropriate protection of confidential information,” saying Order 2222-A does not preclude the use of NDAs.

“We believe that in a case where a utility distribution company declines to provide information because of confidentiality concerns, one avenue CAISO could use to facilitate participation of distributed energy resources is to encourage the distributed energy resource provider to sign a non-disclosure agreement in order to obtain the information needed to participate in the CAISO market via an aggregation,” the commission wrote.

The commission also found that CAISO’s revised proposal satisfied Order 2222’s requirement to revise its tariff to include a dispute resolution provision as part of the utility review process. Responding to a concern by PG&E, the commission clarified that the DERA dispute resolution process is not intended to supersede the existing process outlined in the ISO wholesale distribution tariff for resolving disputes related to interconnection issues — including the interconnection of DERs.

Lastly, the commission approved CAISO’s request to set the effective date for the DERA rules to no later than Nov. 1, 2024.

“As CAISO explains, ‘software enhancements required for this compliance will be highly complex, incorporating both energy injection and load curtailment into a single model that allows aggregations over a wider footprint than the majority of ISOs and RTOs have proposed,’” the commission wrote.

The author of a California bill that could eventually turn CAISO into an RTO said he will hold it in the legislative committee that he chairs while he tries to overcome opposition from labor unions, ratepayer advocates and his fellow lawmakers.

State Assemblymember Chris Holden (D), chair of the Assembly Appropriations Committee, said at the start of a committee hearing Tuesday that he still intends to move forward with AB 538.

“Interactions with my colleagues and stakeholders throughout the West persuade me that there is strong and widespread interest in working together on the details of governance and operations of a Western regional transmission organization,” Holden said. “I’m putting AB 538 on hold for now to allow that to happen. I’m hopeful of rapid progress, opening the way for legislative action at the earliest possible date.”

The move was not a surprise. In a hearing of the Assembly Utilities and Energy Committee in April, committee members allowed the bill to move forward only on the condition that Holden hold the bill in the Appropriations Committee while he addresses concerns with several key provisions. (See Committee Gives CAISO RTO Bill a Cool Reception.)

The bill would allow CAISO to develop a plan for independent governance, free from legislative oversight and with board members who are not appointed by California’s governor. (See Lawmaker Introduces Bill to Turn CAISO into RTO.)

CAISO is a public benefit corporation created by the legislature in 1998. The governor appoints the ISO’s Board of Governors, and the State Senate confirms them.

Having independent governance is essential for CAISO to become an RTO because other states will not join one dominated by California. But Golden State lawmakers have refused to cede control.

Holden’s prior efforts to expand CAISO governance to include other states in 2017/18, which were supported by former Gov. Jerry Brown, failed because of opposition from fellow Democrats in the legislature.

Until this week, Gov. Gavin Newsom has been silent on Holden’s latest effort, but he issued a statement after Tuesday’s announcement indicating support.

“I’d like to thank Assemblymember Holden for his leadership in the discussions around a Western regional transmission organization,” Newsom said. “I Iook forward to our continued work with the legislature, California stakeholders and our partners in other states to advance this important effort on enhanced regional collaboration that will benefit all the West.”

Circumstances have changed since Holden’s prior effort to expand CAISO governance. Notably, SPP is planning to establish a Western version of its Eastern Interconnection RTO, called RTO West, and is planning Markets+, a program with a day-ahead market.

Proponents of Holden’s bill have warned lawmakers that Western entities will abandon CAISO’s successful interstate Western Energy Imbalance Market and join SPP unless the ISO can offer an RTO with independent governance.

Jan Smutny-Jones, CEO of the Independent Energy Producers Association, told energy committee members in April that SPP “will be a different RTO than the one that would be built by [CAISO]” and asked whether they wanted a Western RTO to be run from California or Arkansas, where SPP is based.

Opponents of the measure say expanding CAISO to other states will siphon clean-energy construction jobs to states such as Arizona and Nevada, where it is cheaper to build and operate generation and storage resources.

They also contend that California lawmakers should not relinquish control of CAISO.

“The creation of a multistate RTO divests the legislature from having any ongoing role, and, in fact, you’re being asked to make yourselves and state agencies and the governor completely irrelevant,” Matthew Freedman, staff attorney for ratepayer advocacy group The Utility Reform Network, said in April’s hearing.

FERC on Thursday approved NERC’s proposed plan for registering owners and operators of inverter-based resources (IBRs) (RD22-4).

While the commission declined to incorporate any of industry stakeholders’ suggested changes to the plan, it reminded them there is still considerable work left to shape the final registration framework and encouraged them to raise their concerns during the ERO’s stakeholder process.

NERC’s registration proposal originated from a FERC order in November requiring the ERO to develop a work plan for identifying and registering owners and operators of IBRs that are connected to the grid and “in the aggregate have a material impact” on reliable operation but are not currently required to register with NERC. (See FERC Addresses IBRs in Multiple Orders.)

The commission was motivated by concerns over the ongoing transition from conventional generation resources to IBRs like wind and solar facilities. Specifically, current rules defining which resources qualify as part of the Bulk Electric System — and thus must register with NERC, follow its reliability standards and respond to its alerts — do not apply to many smaller IBRs.

NERC submitted its registration strategy in February, proposing a three-stage process: revise its Rules of Procedure (ROP) to create a new registered entity function, generator owner-IBR (GO-IBR), within 12 months of FERC’s approval of the plan; identify candidates for GO-IBR registration with 24 months of approval; and register GO-IBRs within 36 months of approval.

The GO-IBR category would include IBRs that have an aggregate nameplate capacity of 20 to 75 MVA interconnected at a voltage of at least 100 kV, or an aggregate nameplate capacity of at least 20 MVA interconnected at less than 100 kV. IBRs connected to the local distribution system would not be included; neither would IBRs that are distributed energy resources. NERC said it would also consider developing reliability standards to apply to GO-IBRs.

The ERO’s original submission neglected to mention registration of generator operators; at FERC’s prodding, NERC said in March that it intended GO-IBR to refer to both owners and operators of IBRs, but it acknowledged that this practice would differ from its use of separate terms for existing registered generators and could create confusion. NERC pledged to consider “other potential designations” when revising the ROP.

Stakeholders were generally supportive of NERC’s proposal, but some asked the commission to modify the ERO’s plans. For example, the American Clean Power Association (ACP) and the Solar Energy Industries Association (SEIA) objected to the idea of only registering IBRs with an aggregate material impact on reliability, suggesting that this measure could result in the registration of IBRs that “use equipment and settings that ensure that they ride through grid disturbances and avoid reliability concerns that were observed in past events.”

Solar energy developer Pine Gate Renewables urged the commission to ensure that NERC’s work plan does not place IBRs at a competitive disadvantage compared to conventional generation, noting that the commission has previously ordered that reliability standards not create undue advantages for one competitor over another. Pine Gate, along with SEIA and ACP, also argued that older IBRs may be unable to meet the standards’ performance requirements and asked for a registration exemption for IBRs with older equipment that cannot be easily updated.

In response to these objections, FERC determined that issuing specific restrictions on NERC’s ROP or standards development processes would be outside its authority. Instead, it urged stakeholders to participate in the normal feedback process to influence the ERO’s actions.

During FERC’s monthly open meeting Thursday, acting Chair Willie Phillips said reliability is “job No. 1 for the commission” and described the IBR order as an important step in dealing with the “projected addition over the next decade of an unprecedented proportion” of IBRs.

Commissioner Allison Clements said she looks forward to “engaging” with the ERO as work continues on the registration framework.

“I hope that NERC’s substantive filing on its registration approach, which is still to come, ensures an effective registration framework but does not compromise IBRs’ ability to provide the reliability services they are capable of providing, including … reactive power, black start and fast frequency response,” Clements said.

President Joe Biden on Tuesday made good on his pledge to veto a proposed resolution that would have rolled back a two-year moratorium on solar tariffs imposed on cells and panels produced in Cambodia, Malaysia, Thailand and Vietnam.

Passed with bipartisan support in the House of Representatives and the Senate, the bill, H.J. Res. 39, “disapproved” the moratorium and declared it “shall have no force or effect.”

The House passed the resolution on April 28, by a vote of 221-202, with 12 Democrats joining the GOP majority and eight Republicans opposing the measure.

Nine Democratic senators supported the measure in the Senate, where it passed on a 56-41 vote on May 3. The Democrats voting for the resolution were senators Joe Manchin, (W.Va.), Sherrod Brown (Ohio), Ron Wyden (Ore.), Bob Casey (Pa.), Jon Tester (Mont.), Debbie Stabenow (Mich.), Gary Peters (Mich.), John Fetterman (Pa.) and Tammy Baldwin (Wis.).

Because neither house is likely to muster the two-thirds majority needed to override the veto, the House and Senate votes and the resolution itself were mostly political posturing, giving Democrats and Republicans cover to appear tough on China and the solar industry’s ongoing reliance on overseas suppliers. About 80% of solar panels used in the U.S. come from the four Asian countries in question, according to the Commerce Department.

In his veto message to the House, Biden characterized the moratorium, which the Commerce Department issued in June 2022, as a “24-month bridge” to allow the buildout of a domestic solar supply chain that will break the industry’s dependence on Southeast Asian countries and China.

Since the passage of the Inflation Reduction Act, Biden said, “private companies have announced commitments to build enough solar panel manufacturing capacity to power nearly six million homes.

“America is now on track to increase domestic solar panel manufacturing capacity eight-fold by the end of my first term. But that production will not come online overnight,” he said. “The Department of Commerce’s rule supports American businesses and workers in the solar industry and helps provide sufficient, clean and reliable electricity to American families, while continuing to hold our trading partners accountable.”

The veto message also repeated Biden’s commitment that he will not extend the moratorium when it expires in June 2024.

The president ordered the waiver on tariffs on solar panels and cells imported from Cambodia, Malaysia, Thailand and Vietnam last year, after the Commerce Department announced an investigation into whether panels and cells from those countries contain components from China that would be subject to tariffs. (See Biden Waives Tariffs on Key Solar Imports for 2 Years.)

Reactions

Industry trade groups and individual installers were quick to back the president’s action.

“President Biden’s veto has helped preserve our nation’s clean energy progress and prevented a bill from becoming law that would have eliminated 30,000 American jobs, including 4,000 solar manufacturing jobs,” said Abigail Ross Hopper, CEO of the Solar Energy Industries Association (SEIA). “This action is a reaffirmation of the administration’s commitment to business certainty in the clean energy sector and a signal to companies to continue creating jobs, building domestic manufacturing capacity and investing in American communities.”

Gregory Wetstone, CEO of the American Council on Renewable Energy, agreed. “President Biden’s veto today is a welcome step to avoid a disastrous impact on the U.S. economy and ensure continuing progress toward the clean energy transition and our climate goals,” he said. “The [resolution] passed by Congress would have changed the rules renewable developers and manufacturers rely upon, resulting in many dozens of canceled solar projects, tens of thousands of lost jobs, and a dangerous increase in carbon emissions.”

George Hershman, CEO of SOLV Energy, a utility-scale solar contractor, said the veto would “provide clarity to domestic solar manufacturers and allow the industry to move forward on important projects that boost solar deployment.”

On the other side, Rep. Dan Kildee (D-Mich.), one of the Democrats who voted for the resolution in the House, expressed disappointment with the veto and called for an override vote.

“Failing to stand up to those who engage in unfair trade practices hurts American workers and manufacturers,” Kildee said in a statement Tuesday. “Our workers and businesses will never be able to compete globally unless we hold those who violate U.S. trade laws accountable. The Biden administration found, in its own investigation, that Chinese companies are violating the law. Yet the president’s position, and today’s veto, fails to hold China accountable and hurts American workers.”

Robbie Diamond, CEO of SAFE, a group focused on reducing U.S. dependence on foreign oil, appeared to favor a tariff rollback, as reported in The New York Times.

“We must back up the message of wanting to build a U.S. supply chain with action — even if it is difficult and complicates some deployments,” Diamond said. “If we’re going to talk the talk, we must walk the walk.”

The Supply Chain Buildout

Prior to the passage of the Infrastructure Investment and Jobs Act and Inflation Reduction Act, tariffs on Chinese solar panels and cells were not particularly effective in kickstarting a domestic supply chain. Even after former President Donald Trump approved the tariffs on Chinese solar panels and cells in 2018, the solar industry continued its dependence on Southeast Asian and Chinese manufacturers.

But the announcement of the Commerce Department investigation the following month threw the industry into an uproar, with more than 300 projects delayed or canceled, according to SEIA. Biden’s moratorium, and the IIJA’s and IRA’s tax credits, finally provided the impetus for companies to start investing in new facilities in the U.S.

The American Clean Power Association recently reported that more than $150 billion in domestic utility-scale clean energy investments have been announced in the last eight months. “This amount is equivalent to five years’ worth of American clean energy investments, surpassing total investment into U.S. clean power projects commissioned between 2017 and 2021,” ACP said.

Even so, there’s no guarantee that an adequate domestic supply chain will be up and running by June 2024, when the moratorium runs out.

The Commerce Department issued a preliminary finding in the investigation in December, stating that “certain Chinese solar panel manufacturers were indeed attempting to bypass the [tariffs] via transport through these investigated Southeast Asian partners.” A final decision has been pushed back from May to August.

Two recent reports quantify the rapid growth of the U.S. offshore wind sector, while a third flags technical and reliability challenges posed by the ever-larger scale of turbines being installed.

There are just seven turbines spinning in U.S. waters, but thousands more are being planned. The American Clean Power Association’s (ACP) May 2023 Offshore Wind Market Report puts the U.S. development pipeline at nearly 51,400 MW, while the Business Network for Offshore Wind’s (BNOW) first-quarter report puts the combined goals of oceanfront states at 83,900 MW.

A comparison shows the growth of offshore wind equipment through the years. | GCube Insurance

Meanwhile, GCube Insurance in its second-quarter report this month warned that the latest-model high-capacity wind turbines favored by many developers are showing an unprecedented number of component failures, mechanical breakdowns and serial defects.

And the National Offshore Wind Research and Development Consortium in an April update of its road map points out a shortage of operational experience and data that could guide development of the large turbines planned for U.S. waters.

The potential consequences of this concurrent push for size and speed are that standardized, modular construction and the resulting economies of scale become hard to achieve and that quality control suffers.

This has been flagged many times by stakeholders, analysts and manufacturers. But taken together, the spate of recent reports provides a new look at the issue with fresh data.

Big Plans

The U.S. is very late to the offshore wind sector.

Thirty-two years after the first offshore wind farm went online in Denmark with a 5-MW capacity rating, worldwide installed capacity is 63,200 MW, with just 42 MW of it in U.S. waters. But the country is trying to make up for lost time to reduce greenhouse gas emissions and limit harm to the environment. President Joe Biden has set a national goal of 30 GW of offshore wind capacity installed by 2030 and 15 GW of floating offshore wind by 2035.

Major logistical hurdles stand in the way of the first goal: Domestic infrastructure and capacity to fabricate and install 2,000 fixed-bottom wind turbines are virtually nonexistent, and today’s grid cannot carry all those electrons.

But U.S. developers and regulators can at least draw on the body of knowledge gained from the 63 GW of fixed-bottom wind power in foreign waters. There is no such operational history with floating wind.

ACP’s report notes there are now 32 offshore wind leases in active development nationwide, with 18 projects in early development and 18 in advanced development. They total 51,377 MW of nameplate capacity, 938 MW of which is now under construction.

Most of this is on the East Coast: New York and New Jersey lead the nation with 4,362 MW and 3,758 MW in their pipelines, respectively.

In its report, BNOW notes that numerous infrastructure upgrades and manufacturing expansions are being undertaken to help make all the megawatts envisioned a reality. It also notes that the federal government this year moved to streamline the yearslong review process for development.

So far, the only records of decision issued by the U.S. Bureau of Ocean Energy Management have been for the two projects totaling 938 MW now under construction: Vineyard Wind 1 and South Fork Wind off the New York/New England coast, which are both expected to come online this year.

Big Turbines

In this environment, and with costs spiraling, developers and manufacturers are trying to squeeze as many watts as possible out of each turbine to maximize return on investment.

One notable example: Avangrid in September said it was pushing the completion dates of its Park City Wind and Commonwealth Wind projects back one year to 2027 and 2028, respectively, in hopes that next-generation 17- to 20-MW turbines would be available in time. It said the cutting-edge turbines it would be installing in Vineyard Wind 1 in 2023 can produce only 13 MW.

Some observers warn that this continual upscaling creates the risk that nothing ever really moves beyond the prototype stage; designs would be continuously being tweaked, upgraded and replaced.

GCube in its report said the largest turbines in production five years ago were rated at 8 MW.

The Siemens Gamesa SG 14-222 DD offshore wind turbine has a capacity of up to 15 MW. | Siemens Gamesa

Fresh off December certification of its Haliade-X turbine for 14.7-MW operation, a GE executive told investors in March the company is preparing a variant that will produce 17 to 18 MW.

The GCube report — titled “Vertical Limit: When is Bigger not Better in Offshore Wind’s Race to Scale?” — asserts that while this relentless upsizing has sharply reduced the cost of wind power and sharply increased the amount of power produced, there are negative consequences:

manufacturers competing for market share sign contracts for next-generation equipment years before it goes into production, sometimes without fully understanding the necessary processes and pricing;

with ever-evolving technology, every project can have its own unique learning curve;

turbines are becoming obsolete only a few years into a projected 25- to 30-year lifespan, and replacement parts are sometimes unavailable;

maintenance and repairs are incrementally more difficult, costly and time consuming as machines get larger;

support infrastructure has trouble keeping up — only three vessels in the world can install the newest 15-MW turbines; they cost up to $2 million a day to charter; and they are booked for years to come; and

insurance claims are escalating, but insurers, eager to burnish their environmental, social and corporate governance credentials (ESG), continue to enter the offshore wind market.

GCube, which insures 100 GW of renewable energy projects in 40 countries, analyzed a decade of proprietary data and determined that offshore wind claims increased significantly in frequency and severity over the decade from 2012 to 2021, with turbine component failures increasing sharply after 2017.

It also found that as a proportion of total claims, larger turbines are generating more claims during construction than their smaller, older cousins did. Then, once installed, turbines larger than 8 MW are sustaining component failures much sooner than smaller units.

In a May 2 announcement, GCube CEO Fraser McLachlan presented the study and its data as a cautionary tale.

“The push to rapidly develop more powerful machines is piling pressure on manufacturers, the supply chain and the insurance market,” he said. “Scaling up is an essential part of driving forward the energy transition, but it is now creating growing financial risks that pose a fundamental threat to the sector. We advise manufacturers to focus on improving the quality and reliability of a reduced number of products to put themselves back on a sustainable path of development.

“At the same time, developers must support manufacturers by sharing the risk of larger machines more equitably and open their lending books to supply chain companies.”

Recurring Message

The GCube report’s warning of too much, too fast is a message expressed in different ways for different reasons by both opponents and proponents of offshore wind.

In an email to NetZero Insider, BNOW wrote of the climate and economic benefits of this rapid technological evolution but also flagged some concerns.

“The scale and speed of the technological advancement, however, is challenging for the supply chain to keep pace, let alone expand to meet rising demand,” the organization wrote. “Standardization and optimization are keys to creating more supply chain capacity, ensuring deployment goals are met and even further driving down costs, but those benefits must be weighed against fostering innovation in this still evolving industry.”

The National Renewable Energy Lab told NetZero Insider there would be greater value in industrializing at the current scale than in upscaling beyond 15 MW. NREL in its January offshore wind supply chain road map said it expected some modularity to evolve in design and construction of turbine nacelles. But it also saw the potential upscaling of nacelles from 600 tons to nearly 1,000 tons.

The R&D Consortium in Version 4.0 of its road map last month said operations and maintenance costs constitute more than 30% of the cost of offshore wind, and it is imperative to control those costs at the design stage.

However, it noted, there are few test facilities that can accommodate components on the 15-MW scale and no record of operations data from which to draw insight, as 15-MW turbines are so new.

“The offshore wind industry has been focused on turbine megawatt upscaling, but optimization of the current generation of 15-MW turbines for performance and load reduction has been compromised as a result,” the report noted. “The consortium does not envision direct support of new turbine development. Rather, acceleration of turbine optimization solutions in harmony with the needed industrialization and standardization of the supply chain would better serve U.S. development.”

It is likely, the consortium added, that maintenance systems and protocols for 15-MW turbines will be developed and proved in U.S. waters.

Quality Control

One after another in the past year, the major turbine manufacturers have acknowledged sharply escalating quality-control problems and warranty claims in their wind power products. To judge by their statements to investors and analysts, they have already embraced some of the points in the GCube report.

The GE Haliade-X 14.7MW-220 offshore wind turbine prototype is shown in Rotterdam, Netherlands. | General Electric

In an October 2022 earnings call, GE CEO H. Lawrence Culp Jr. spoke of the warranty costs that were a drag on the financials of GE Renewables and blamed some of that on rapid product development over the preceding five years.

“Such rapid innovation strains manufacturing and the broader supply chain,” he said. “It takes time to stabilize production and quality on these new products, which in turn pressures fleet availability. We need to industrialize faster to counteract these dynamics, and we are.

“We’re drastically simplifying and standardizing too many variants into what we call workhorse products, so we and our suppliers can implement more repeatable manufacturing processes. This enhances product quality and reduces cost. In our existing fleet, we’re deploying corrective measures, enhancements and monitor-and-repair programs.”

Vestas reported in February that lost production factor — the measure of energy production not captured by the 56,400 wind turbines under its service — has been rising steadily for several years, surpassing 3% by the end of 2022. Warranty costs equaled 6.3% of Vestas’ 2022 revenue.

“Lost production factor continues at high level as a consequence of the extraordinary repair and upgrade level,” it said in a quarterly report May 10, but the numbers were better: Warranty costs equaled only 4% of first-quarter revenue, compared with 7.8% in the first quarter of 2022.

“Optimizing the complete value chain calls for increased focus on improving our existing platforms,” Vestas said in its annual report. “We believe strongly in this approach, because introducing new platforms too fast obstructs supply chain industrialization. As turbine components become larger and more efficient, they also create logistical challenges to the expansion of wind power around the world. For this reason, we are paving the way for scale through modularization and optimizing how our products are designed and produced.”

And in a quarterly report to investors in February, Siemens Gamesa wrote, “Service performance during Q1 [2023] was severely affected by the outcome of the periodic monitoring and technical failure assessment of the installed fleet, which revealed a negative trend in the failure rate of certain components. As a result, the estimated cost of fleet maintenance and warranty provisions is higher than initially estimated.”

CAISO’s summer forecast looks better than last year’s thanks to the addition of thousands of megawatts of new resources and California’s record snowpack, which is expected to increase hydroelectric generation by 72% compared with drought conditions a year ago.

In its annual Summer Loads and Resources Assessment, published Tuesday, the ISO says it has made “sound progress towards meeting the conventional ‘one day every 10 years’ loss-of-load expectation planning target.”

“Under current high hydro conditions, the resource fleet scheduled to be online by June 1, 2023, exceeds the one-in-10 planning target with a margin of approximately 200 MW … [and with] the resource fleet scheduled to be online by Sept. 1, 2023, exceeds the one-in-10 planning target with a margin of approximately 2,300 MW,” the assessment says.

That compares with a 1,700-MW shortfall in meeting the planning target last year, CAISO management says in a slide presentation on the assessment.

“These results do not take into account more extreme events such as those demonstrated in the last several years, e.g., extreme drought, wildfires and the continued potential for widespread regional heating events and other disruptions that continue to pose a high risk of outages to the ISO grid,” it says.

California experienced energy emergencies caused by extreme heat and wildfires in the past three summers, when the state and much of the West endured worsening drought and decreased hydropower.

The ISO was forced to call for rolling outages in August 2020 during a Western heat wave that dried up imports. It declared an energy emergency in July 2021 when an out-of-control wildfire in Southern Oregon nearly shut down a major transmission pathway between California and the Pacific Northwest.

And it came within minutes of ordering blackouts during a record-setting heat wave in September 2022, when demand outpaced supply. (See CAISO Reports on Summer Heat Wave Performance.)

Since last summer, CAISO has been connecting thousands of megawatts of new battery and solar resources.

By June 1, the ISO expects to have connected 2,500 MW of solar and 2,300 MW of batteries since Sept. 1, 2022. By September of this year, it expects to add another 1,300 MW of solar and 2,000 MW of batteries, bringing the totals to 3,800 MW of solar and 4,300 MW of batteries and (8,100 MW total) added since September 2022, CAISO says in its slide presentation.

In addition, a series of atmospheric rivers this winter filled the state’s hydroelectric reservoirs and pushed the snow water content to approximately 240% of average on April 1, a key date for California’s measurement of snowpack in the Sierra Nevada. The snow melted slowly in April thanks to cloud cover and below-normal temperatures, the state Department of Water Resources said. (May, however, has been hotter than normal, including in the Sierra.)

“The year-to-date snow water content totals are significantly above average, which should result in above-average hydro energy generation in 2023,” the ISO’s summer assessment says.

The assessment does not include a projection of the amount of hydropower that could be generated, but it notes that the state has large and small hydroelectric facilities with more than 7,900 MW of installed capacity.

In the unusually wet winter of 2016/17, large and small hydro generated more than 43,000 GWh of hydroelectric power, compared with about 14,500 GWh in the drought of 2021, a 66% decrease, California Energy Commission records show.

On May 10, the U.S. Energy Information Administration forecast a 72% increase in hydropower generation in California this year compared to 2022.

“One source of uncertainty in our forecast is the possibility of warmer spring temperatures, which would melt the Sierra Nevada snowpack earlier than expected,” the EIA said. “In this case some of the melting snow may bypass power generating turbines for flood control purposes.

“Less snowpack also means less water available to supply hydropower plants during summer months, when electricity generation has historically been at its highest.”

CAISO management plan to present their findings to the Board of Governors at its meeting Thursday.

Asset condition spending since 2016 | NESCOE

Asset condition spending since 2016 | NESCOE