Changes meant to bolster CAISO’s day-ahead market and a planned day-ahead extension of its Western Energy Imbalance Market won approval from the ISO’s Board of the Governors and the market’s Governing Body on Wednesday.

The new day-ahead market enhancements will introduce an imbalance reserve product meant to deal with increasing uncertainty in the net-load forecast between day-ahead and real-time markets, driven largely by the proliferation of weather-dependent solar and wind generation in the West.

“This proposal is intended to give the ISO better tools to be able to handle the growing challenges involved in managing the electrical grid, specifically around growing uncertainty and variability,” Becky Robinson, CAISO’s principal economist, said at the board and Governing Body’s joint meeting Wednesday.

“It is the latest in a series of steps to devise market products and tools to procure and incentivize flexibility, which is increasingly needed and more valuable because of the increasing quantities of weather-dependent renewable generation,” Robinson said. “This is a trend [facing] ISOs and RTOs across the country, and it is an important incremental step on top of our existing flexible-ramp product in the real-time market.”

The imbalance reserve product is designed to procure flexible reserves to cover supply-and-demand differences between the day-ahead forecast and real-time conditions.

For the WEIM’s proposed extended day-ahead market (EDAM), the imbalance reserve product is “essential … as it best ensures EDAM entities, including the ISO, can benefit from the footprint-wide diversity in the day-ahead market’s optimization,” CAISO’s revised final proposal states.

The interstate WEIM, currently a real-time-only market, includes 79% of load in the Western Interconnection. CAISO is hoping many real-time participants also sign up for EDAM.

Robinson said the imbalance reserve product is especially important for the EDAM because it will ensure there are sufficient offers into the real-time market to “address system needs that may well turn out to exceed day-ahead energy awards.”

It will increase reliability and economic benefits for EDAM participants and increase confidence in the market, she said.

The enhancements are also meant to improve the residual unit commitment process, CAISO said.

To address uncertainty between day-ahead forecasts and real-time supply, “market operators have historically taken manual actions outside of the market framework to procure additional capacity in the day-ahead time frame,” the proposal states. “Specifically, grid operators increase the demand forecast used in the day-ahead market’s residual unit commitment process.”

That can distort price signals and mask the value of more flexible resources, Robinson said.

Introducing imbalance reserves in the day-ahead time frame will “greatly decrease the need for grid operator adjustments to the demand forecast used in the residual unit commitment process, creating a more efficient and effective market outcome,” the proposal states.

The enhancements were developed in a stakeholder process that began in 2019 and involved 17 stakeholder meetings and four straw proposals. CAISO had expected to bring the proposal to the CAISO and WEIM boards in February but extended the stakeholder process to May to discuss alternative approaches.

One result was the decision to continue refining the effort with recommendations from a working group of stakeholders as more is learned about its real-world effects.

Commenters were consistent in their message that this is a new product, still in development, and with a number of unknowns, said Jan Schori, vice chair of the CAISO board.

“The bottom-line message I came away with is this that we do need to get on with this; get the software in development; get going on the design and start testing it,” Schori said before Wednesday’s unanimous vote, adding, “I think we’re at a point where it is logical to make that decision today.” But she asked CAISO management to regularly update the two boards on the project’s progress.

CAISO CEO Elliot Mainzer responded, “You have my absolute commitment on that.”

MISO executives on Friday told stakeholders that the capacity market still needs fixing, warning that the surplus gained from last week’s auction is fleeting without long-term changes.

Todd Ramey, senior vice president of MISO markets and digital strategy, said that given the current vertical demand curve and enough capacity to go around for this year at least, the auction “predictably produced relatively low prices.” (See related story, 1st MISO Seasonal Auctions Yield Adequate Supply, Low Prices.)

“Anytime we have adequate capacity, prices tend to go lower,” Senior Director of Resource Adequacy Durgesh Manjure said.

Manjure said the dearth of capacity and expensive clearing prices in MISO Midwest last year appears to have influenced offer behavior this year. The results simply buy the grid operator more time to work out improvements to its resource adequacy construct, including applying a downward-sloping demand curve in the auction, he said.

“This year’s outcome is just that: an outcome for this year. The long-term risk, driven by the resource transition, continues,” Manjure warned. “A lot of these changes in capacity appear to be temporary.”

Some stakeholders said the auction outcomes seemed diametrically opposed to NERC’s recently released 2023 Summer Reliability Assessment, which said MISO, among other regions, faces supply shortfall risks during upcoming hot weather. (See related story, NERC Warns of Summer Reliability Risks Across North America.)

“We understand it’s a big difference from last year,” MISO Executive Director of Resource Planning Scott Wright told stakeholders. But he added that even though “there’s good reliability value” to capacity beyond requirements, MISO’s current auction setup is not equipped to put a value on it.

The auction was the first under MISO’s new seasonal construct. Energy consultant Kavita Maini said she was “intrigued” that the highest prices were for the fall.

Manjure said MISO cannot “speculate or pinpoint” what exactly drives market participants to submit higher offers in a particular season, though it can surmise that maintenance outages were a factor.

Bill Booth, consultant to the Mississippi Public Service Commission, said he is interested in learning how accredited capacity values of thermal resource classes changed year over year, given MISO’s new accreditation process. He said the information would be especially helpful in figuring out why Zone 9 had to clear higher-cost generation to meet its supply requirements.

MISO staff promised a breakdown of capacity accreditation changes by fuel type for the summer. They said it would take more time to calculate those differences.

Far from MISO’s view of the auction results not being an indication of what’s to come, Toba Pearlman, senior attorney for the Natural Resources Defense Council, said the clearing prices show that the RTO can maintain reliability while incorporating lower-cost wind, solar, energy storage and demand response to the grid.

“MISO’s auction sent an important signal last year, and the region’s utilities and energy resource providers took steps to meet capacity needs,” she said in an emailed statement. “As new generation is built and other plants retire, NRDC looks forward to working with MISO and other stakeholders to ensure a reliable system. Solutions should increase available capacity, lower costs and enable more clean energy to come online.”

Pearlman said MISO should continue to concentrate on “bedrock” transmission solutions necessary to support capacity expansion.

But the presenters also emphasized that tight margins in most of the continent could lead to problems with reliability in the event of hotter-than-expected weather conditions.

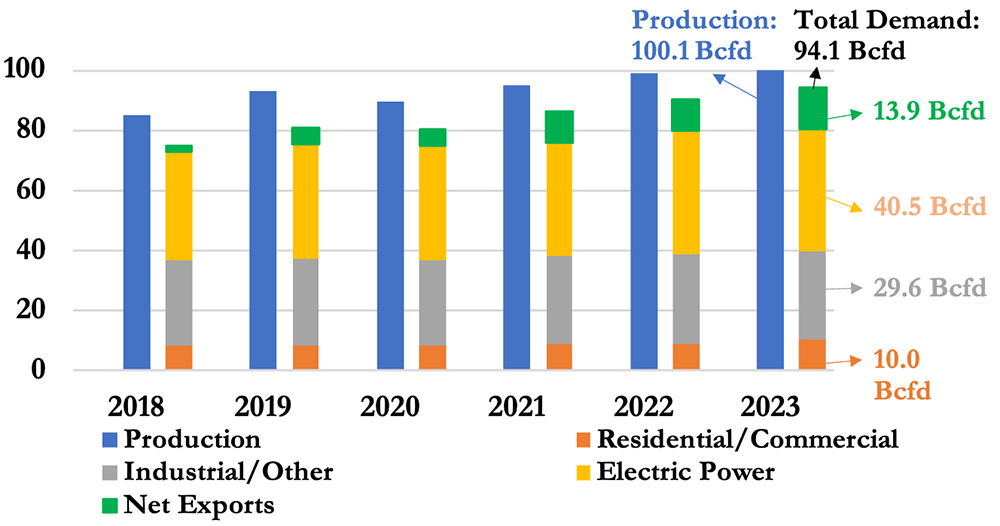

Presenting the assessment, James Burchill of FERC’s Office of Energy Policy and Innovation (OEPI) said that staff expect natural gas prices to be lower than last summer based on “record high natural gas production levels along with above-average natural gas storage inventories.” Gas production is expected to reach a record high of 100.1 Bcfd, up from last year’s forecast of 96.9 Bcfd, while demand is set to rise to 94.1 Bcfd from the 89.8 Bcfd predicted last year, 14% above the previous five-year average.

U.S. natural gas demand and production | EIA

The electric power sector is expected to be the biggest domestic user of gas with 40.5 Bcfd, followed by the industrial sector at 29.6 Bcfd and residential/commercial at 10 Bcfd. These figures are largely in line with last year’s forecast. The increase primarily comes from net exports, including LNG and pipeline net exports, which are expected to average 13.9 Bcfd this summer, up 36.9% from summer 2022.

Despite burgeoning demand, FERC staff said that natural gas futures for June-September are significantly down at most trading hubs from their pre-summer levels last year, reflecting what OEPI’s Micah Gowen called “forecasts of greater availability of supply than last summer with a reduced need to inject natural gas into storage given above-average storage inventories.” Storage inventories ended the 2022-2023 withdrawal season at 1,830 Bcf, 32% higher than the start of the 2022 injection season and 22% above the five-year average.

One exception to this trend is California; the U.S. Energy Information Administration recorded natural gas storage levels at 74 Bcf by the end of the winter season in the Pacific region. The FERC report said a late summer heat wave last year reduced inventories, with the fall build unable to recover them to the same level. As a result of the low storage, California may experience “a tighter supply-demand balance and higher prices this summer as more supply will need to be routed into storage … than in a usual summer.”

Fears Continue over Electric Reliability

The FERC report came the day after NERC released its Summer Reliability Assessment, warning that most of the North American grid, including ERCOT, MISO, Ontario, New England, SPP, and parts of SERC and WECC, faces risk of supply shortfalls during “periods of more extreme summer conditions.” (See related story, NERC Warns of Summer Reliability Risks Across North America.) The National Weather Service has predicted that above-normal temperatures are likely across most of the continental U.S. and Alaska, while most of Canada is expected to see normal or below-normal temperatures.

NERC Manager of Reliability Assessments Mark Olson joined Thursday’s meeting to discuss the ERO’s assessment and its place in FERC’s summer forecast. He explained that the replacement of conventional generation with renewable energy resources has left some areas heavily reliant on weather-dependent resources such as wind and solar.

The ERO believes these generators are capable of meeting the needs of the grid in normal circumstances, but weather disturbances — particularly a drop in wind production — could cause multiple regions to turn to energy imports. If these issues affect multiple regions, utilities may not have neighbors to whom they can turn to ease the burden.

While acting FERC Chair Willie Phillips and Commissioner Allison Clements focused on the positive sides of the report — with Clements noting the renewal of California’s hydroelectric reservoirs — Commissioner Mark Christie reminded his colleagues that FERC and NERC assessments also show that concern is warranted. (See related story, Hydro, New Resources Boost CAISO’s Summer Outlook.)

“I take [the NERC report] as, ‘We hope we can get through the summer,’” Christie said. “We have a good chance: We have increased hydro in the West because the drought conditions have diminished. But the long-term trends, I don’t think [are] good news. … We hope we get all good news this summer. I hope so, and maybe we’ll get through the summer. But the long-term trends are still threatening, [and] we’ve got some major, major threats facing the reliability of the grid.”

Electricity prices in organized markets are set by a single clearing price at a given location and a given time. This is the same price-setting mechanism for all commodities, as well as for publicly traded financial instruments like stocks.

How We Got Here

The wisdom of this mechanism has been explained many times. The most cogent explanation is a two-page summary by Maryland professor Peter Cramton, and an accompanying longer piece by Texas professor Ross Baldick, which in turn cites seminal works by Alfred Kahn, Steven Stoft, Sue Tierney and other worthies.[1] If you care about rational market design, please look at these.

Let me quote from Cramton: “The single clearing-price auction is important because of its simplicity and effectiveness at answering the most basic questions: who should get the goods, who should produce the goods, and at what prices. Based on each market participant’s expressed preference, the single clearing-price auction awards the goods to all consumers who value the goods more than the cost (the clearing price) and the goods are produced by all suppliers who have a cost less than their payment (the clearing price). In this way, the clearing-price auction maximizes gains from trade: consumption comes from demand with the highest values and production comes from supply with the lowest cost. This is perhaps the most celebrated result in economics.”

Latest Revisionism

FERC Commissioner Mark Christie challenges the single clearing price mechanism in an Energy Law Journal article.[2] He observes that every resource is paid the highest price that is paid to the last resource needed to meet demand. Which is of course true.

But the flip side is also true: Consumers pay the lowest price that will secure sufficient resources to meet their collective demand. Should consumers, instead of paying a single clearing price, pay what the electricity is worth to them? So instead of paying, say, $50/MWh, should they pay their “value of lost load” of, say, $5,000/MWh? 100 times what they pay now?

Because consumer demand for electricity is inelastic, the “consumer surplus” (essentially net consumer benefit) under a single clearing price is a zillion times the “producer surplus” (essentially net producer benefit).[3] Christie would further diminish the relatively small producer surplus and add to the already immense consumer surplus. Without explaining why.[4]

Renewable Marginal Costs

Commissioner Christie says renewables’ very low (or negative) marginal costs do not flow through to consumers, which he suggests fixing by paying renewable projects what they bid: “pay-as-bid.” But of course renewable developers wouldn’t build such projects if they were to receive prices based on their marginal costs instead of single clearing prices. The return on and of capital when a producer receives its marginal cost is zero point zero.

And as Alfred Kahn pointed out 20 years ago: “The critical assumption is, of course, that after the market rules are changed, generators will bid just as they had before. The one absolute certainty, however, is that they will not.”[5]

Myriad Other Deficiencies in Pay-as-bid

Not to mention myriad other deficiencies in pay-as-bid. As Baldick observed: “From a practical perspective, there is no empirical or experimental evidence that pay-as-bid would reduce prices significantly compared to single clearing price. … the theoretical, experimental and empirical evidence does not support a change to pay-as-bid. There are also a number of very serious drawbacks to pay-as-bid, including: inefficient dispatch; difficulty of participation for small, competitive asset owners; the reduced ability of demand response to mitigate market power; and difficulties for market monitoring.”

A comprehensive dissection of pay-as-bid is here, concluding among other things that prices for consumers would likely be higher under pay-as-bid.[6]

Reliability Challenge from Subsidized Renewable Resources

Christie says renewable subsidies suppressing energy prices challenge reliability in organized markets. Yes. But that is precisely why we need capacity markets — now more than ever — so sufficient dispatchable resources (or functional equivalent) are procured to meet peak demand.

Christie disparages renewable subsidies. He seems to think it’s OK to somehow offset these subsidies by changing energy market design to restore “true markets in which competitors operate on a level playing field.” Making it FERC’s job to override Congress?

Capacity Market Granularity

Speaking of capacity markets, Christie says they are not as granular as energy markets, with price differences “at best zonal.” Actually, in PJM, locational deliverability areas (LDAs) can be and are sub-zonal as warranted.[7] But more important, the reasoning for LDAs was provided in excruciating detail in PJM testimony some 18 years ago,[8] and approved by FERC for PJM following similar approvals for ISO-NE and NYISO.[9] Nothing has changed to undermine that reasoning.

Who’s Speculating with Whose Money?

Christie says RTOs with capacity markets are speculating on future supply and demand just like vertically integrated utilities are speculating.

This is not correct. Competing resource providers in RTOs “speculate” on future revenue streams with investor money. Vertically integrated monopoly utilities don’t compete and don’t “speculate” — they get guaranteed (and excessive) returns with captive consumers’ money, as I’ve discussed before.[10]

Poster child: Southern Co.’s Vogtle Units 3 and 4 — $16 billion over budget and seven years late.[11]

This is just like the contrast between competition and monopoly in transmission facilities, if I might bang that drum again.[12]

As that utility CEO famously said in 1995, “This is the only industry I’ve ever seen where you can increase your profits by redecorating your office.”[13]

And as Pat Wood has said since 1996, “Even on my best day [as a regulator] I can’t substitute for what the market and competition can do.”[14]

Real-time and Day-ahead Energy Markets

Christie draws a distinction between real-time energy markets and day-ahead energy markets. Most RTOs have both.

What’s relevant here is that Christie attaches some significance to his claim that the real-time energy markets “enable the buying and selling of a physical product, the electrical power itself,” in supposed contrast to the day-ahead markets, which he says enable trading in “a financial product, a contract setting a price of power to be delivered the next day.”

I’m not sure what the point of this is, but I would repeat from past columns that electricity is not a physical product — even the electrons don’t move.[15] And both real time and day ahead markets clear in dollars, so they’re both “financial” in that sense. Finally, “real time” is somewhat of a misnomer. In PJM, for example, the real-time market is cleared based on offers that can’t be changed fewer than 65 minutes before the operating hour.[16] Is there some fundamental difference between an hour-ahead market and a day-ahead market? No.

Standard Market Design

Before I wrap up, please let me address Christie’s dismissal of what he calls the “misbegotten” Standard Market Design, which he says “crashed and burned.”[17] As I explained seven years ago, there were 10 core elements of Standard Market Design, and all 10 got implemented in the RTOs.[18] The vision of Pat Wood, Nora Brownell, Bill Massey and Linda Breathitt ultimately prevailed, helping save consumers tens of billions in avoided nuclear costs alone.[19] Kudos to them.

It’s Tough Enough

We have a collective challenge in the industry of making a difficult and expensive energy transition with incredible challenges. If we have to revisit core principles like the single clearing price mechanism, we’ll never get out of the starting gate.

Columnist Steve Huntoon, principal of Energy Counsel LLP, and a former president of the Energy Bar Association, has been practicing energy law for more than 30 years.

[7] In PJM sub-zonal LDAs are DPL South, PS North and ATSI-Cleveland. Criteria for creation of new LDAs are set forth in PJM Manual 18, section 2.3.3, and PJM Manual 14B, Attachment C, section C.2.1.2.

FERC last week rejected rehearing requests from MISO and stakeholders over the grid operator’s minimum capacity obligation. In affirming a previous decision, the commission again blocked MISO from requiring load-serving entities to demonstrate that they have obtained at least 50% of the capacity required to meet their peak load before capacity auctions (ER22-496-002).

The agency last August denied MISO’s request to install the minimum capacity obligation (MCO), explaining that the RTO did not show the rule would address resource adequacy concerns or that it would incent members to construct new generation. The commission said the rule would likely only shift “a portion of the supply and demand for capacity from the auction into the bilateral market in a given year.” (See FERC OKs MISO Seasonal Auction, Accreditation and Regulators, LSEs Ask FERC to Reconsider MISO’s Seasonal Capacity Accreditation.)

MISO and Entergy and Cleco filed for a rehearing, the latter two challenging the commission’s view that the rule would lead to market power concerns. Entergy’s Arkansas, Louisiana, Mississippi, New Orleans and Texas operating companies have also asked the D.C. Circuit Court of Appeals to override FERC’s rejection. (See Entergy Seeks Review of FERC’s Block on MISO Capacity Obligation.)

The commission stuck to its original decision, saying MISO did not meet its burden of proof and that its proposal ran the risk of “negative impacts on bilateral market dynamics.” It said that the proposal ran the risk of concentrating market power in MISO South, where buyers would likely have limited recourse to purchase capacity in the auction.

FERC said an MCO would “undermine the important disciplining effect the auction has on the bilateral capacity market.”

“This disciplining effect becomes all the more important as reserve margins throughout MISO tighten. Shifts in market dynamics, such as concentration of market share, may exacerbate these concerns,” the commission said. “Particularly given the tightening of reserve margins in MISO as a whole and a capacity shortfall in [MISO Midwest] in the 2022/23 auction, under the MCO as proposed, entities in MISO South might struggle to identify and transact with capacity sellers in bilateral markets to meet half of their reserve requirements and would not be able to rely on the full disciplining effect of the auction to mitigate possible exercises of market power in bilateral capacity markets.”

Commissioner James Danly dissented, as he had previously, saying FERC mishandled the decision by not further examining potential market-power issues. He said he was disappointed that his “colleagues did not pursue a paper hearing in this proceeding.”

“More information is needed regarding the possible exercise of market power. After considering the arguments on rehearing, I am even more firmly convinced that we should have sought further development of the record,” Danly said. “In this case, the commission failed to sufficiently explore the market power issues raised by the litigants both initially and on rehearing. My questions on this subject remain unanswered, and I am not convinced that the commission’s determinations on rehearing are supported by the record.”

Commissioner Mark Christie wrote a separate concurrence to again stress that potential market power consequences were his only sticking point with the proposed MCO.

“There is nothing inherently wrong with an MCO in the MISO capacity market — which, we should remember, is voluntary — and if MISO can resolve such concerns, the outcome of a future filing should not be predetermined by our order herein,” he said. “Indeed, I appreciate the concerns expressed by MISO and other parties in this proceeding that an overreliance by load-serving entities on MISO’s capacity auction may jeopardize the reliability of the MISO system.”

Pattern Energy’s SunZia transmission project, a 550-mile line from New Mexico to Arizona, has received route approval from the federal Bureau of Land Management, and construction is expected to start this summer, the company announced last week.

The BLM decision completes the National Environmental Policy Act (NEPA) process and was the last major approval needed for the project. The 525-kV transmission line is expected to be operating in 2026.

The SunZia line will carry energy from Pattern Energy’s 3,500-MW SunZia Wind project in central New Mexico to south-central Arizona. From there, the wind energy will serve customers in Arizona and California. The idea is to supply wind energy to those states during the early evening, when demand is high but solar resources have dropped off.

Pattern Energy announced last week that power purchase agreements have been signed with two California buyers of SunZia wind energy: Shell Energy North America LP and the Regents of the University of California.

A Pattern Energy spokesman said the existing grid would be used to deliver the wind power from Arizona to California.

“In addition, we will fund some upgrades to the grid to facilitate these deliveries,” the spokesman said.

Pattern Energy acquired the project from SouthWestern Power Group last year. Pattern Energy said SunZia Wind and Transmission combined will be the largest clean energy infrastructure project in U.S. history.

Also this month, Pattern Energy announced it had chosen contractors for engineering, procurement and construction of the SunZia Transmission and Wind projects.

Quanta Services (NYSE:PWR) will work on the transmission line.

In addition, Blattner, which Quanta acquired in 2021, will work on the SunZia Wind project and an associated switchyard. The project will include the installation of more than 900 turbines, 10 substations, operations and maintenance facilities, and more than 100 miles of wind-generation transmission lines.

Hitachi Energy will provide HVDC converter stations and digital control platforms for the transmission project.

Construction of the wind project is expected to begin this year with a 2026 target date to start operations.

UC’s First Wind Contract

For the University of California system, the newly announced SunZia agreement is its first wind energy contract, and its largest renewable energy commitment so far, according to a release. The university signed its first utility-scale contracts for solar eight years ago.

The 85 MW of SunZia wind energy will be used by every UC campus and medical center. It will help the UC Clean Power Program meet the requirements of California’s renewable portfolio standard. The UC Clean Power Program operates under California’s Direct Access Program, in which customers buy electricity from a competitive provider instead of a regulated electric utility.

“The SunZia project expands the systemwide collaboration needed to support each of our campuses as they complete their plans to transition away from fossil fuels,” said David Phillips, associate vice president of capital programs, energy and sustainability.

The university system has more than 50 MW of on-campus green electricity projects. It also buys 60 MW of power from Five Points Solar PV Park and 20 MW from Giffen Solar Park, both in California. An additional 45 MW is expected from a solar facility coming online in 2025.

The CAISO Board of Governors on Thursday approved a $7.3 billion transmission plan that breaks with the ISO’s traditional planning process in an effort to bring needed resources online faster while dealing with an interconnection queue that has grown too large and unworkable.

“The plan reflects a more proactive and strategic approach in studying and recommending new transmission infrastructure needed to reliably and efficiently meet California’s clean energy objectives over the next decade and beyond,” Neil Millar, CAISO’s vice president of infrastructure and operations planning, told the board.

The new approach aligns with a memorandum of understanding that the leaders of CAISO, the California Public Utilities Commission and the California Energy Commission signed in December to establish closer links between their planning processes, Millar said. (See CAISO CEO Lauds Transmission Planning Agreement.)

In California’s divided energy planning process, the CEC forecasts demand, the CPUC orders utilities to procure resources and CAISO handles transmission planning and interconnecting new resources to its grid.

“The MOU tightens the linkages between resource and transmission planning activities, interconnection processes and resource procurement,” Millar wrote in a briefing paper to the board.

Under the reworked process, CAISO is taking a new “zonal” approach to transmission planning that targets regions of the state where resources can be developed and interconnected to transmission most effectively, such as the southern Central Valley, where more large-scale solar arrays with battery storage are proposed.

“As set out in the MOU, expectations are that the CPUC will continue to provide resource planning information to the ISO as it did for this transmission planning cycle,” Millar wrote. “The ISO will develop a final transmission plan, initiate the transmission projects and communicate to the electricity industry specific geographic zones that are being targeted for transmission projects along with the capacity being made available in those zones.

“The CPUC will in turn provide clear direction to load-serving entities to focus their energy procurement in those key transmission zones, in alignment with the transmission plan. To bring this more coordinated approach full circle, the ISO will also give priority to interconnection requests located within those same zones in its generation interconnection process.”

Adding 7,000 MW a Year

The goal is to expedite the interconnection of new resources needed for the state’s transition to 100% clean energy while maintaining reliability.

“The need for additional generation of electricity over the next 10 years has escalated rapidly in California as it continues transitioning to the carbon-free electrical grid required by the state’s clean-energy policies,” Millar wrote. “This in turn has been driving a dramatically accelerated pace for new transmission development in current and future planning cycles — as much as 7,000 MW/year over the next decade.”

The 2022/23 transmission plan adopted Thursday calls for 45 projects totaling $7.3 billion that California needs over the next decade. They include 24 reliability projects “driven by load growth and evolving grid conditions as the generation fleet transitions to increased renewable generation” and 21 policy-driven projects totaling $5.53 billion to “meet the renewable generation requirements established in the CPUC-developed renewable generation portfolios,” he wrote.

The plan is based on the CPUC’s projections that the state needs to add at least 40 GW of new resources over the next 10 years in a base-case scenario and 70 GW by 2032 in a “sensitivity” scenario “reflecting the potential for increased electrification occurring in other sectors of the economy, most notably in transportation and the building industry,” the transmission plan says.

“The network upgrades are recommended in this plan to make all of the base amounts available and, in Southern California, to also make most of the sensitivity amounts available as well,” it says.

The final tally of projects differs from an April 3 draft because a 500-kV line project, estimated at $2 billion, “has been held back pending additional analysis of stakeholder input and may be considered as an extension to this planning cycle or the next planning cycle.” (SeeCAISO Retools Transmission Plan for Reliability, Renewables.)

In a letter to the board, the Northern California Power Agency, which invests in resources for 16 member cities and public entities, expressed concern over the plan’s projected costs.

“With $7.3 billion in estimated new investment, the Revised Draft 2022-2023 Transmission Plan will be the most expensive plan in CAISO’s history,” the agency wrote. “CAISO estimates the high voltage transmission access charge will increase from under $15/MWh today to over $22/MWh in a decade.”

“That estimate does not include the possibility of cost overruns (an inevitability), transmission investments made outside CAISO’s planning process (historically the bulk of transmission investment), or the impact to the low-voltage transmission access charge (which substantially exceeds high-voltage in certain TAC areas); thus, the true impact to California electric consumers will be much greater than the CAISO estimates alone,” NCPA wrote.

In Thursday’s meeting, Millar said CAISO takes the high costs seriously, and that the transmission plan is designed to meet the state’s needs in the most cost-effective way.

Some projects in the 2022/23 plan address needs outlined in the 70-GW sensitivity portfolio, which the CPUC expects to be the base case next year, he said.

“We need to get a head start on these major projects,” Millar said.

Next year’s transmission plan will address more sensitivity-case projects as well as transmission for offshore wind development and will also be expensive, he said.

But the two annual plans should address the “bulk of the major corridor requirements” for years, he said.

“This is not going to be year-over-year at this level of expenditure,” Millar said.

Interconnection Process Enhancements

The board on Thursday also approved the first phase of its interconnection process enhancements to help deal with an overwhelming number of generator interconnection requests.

CAISO received 359 interconnection requests totaling more than 105 GW during its Cluster 14 window in April 2021, quadruple the number from prior years, with 205 projects totaling 65.5 GW proceeding into phase 2 of the interconnection study process.

This year it received 541 requests totaling 354 GW for its Cluster 15 window.

Running cluster studies on such an immense volume of requests makes little sense, CAISO CEO Elliot Mainzer has said.

In March, the ISO launched a stakeholder initiative to revamp its interconnection process and fast-tracked it for approval by the Board of Governors.

The new initiative has two tracks. In the first track, CAISO proposed postponing its processing of Cluster 15 requests until the Cluster 14 studies are finished next year.

The board approved that track Thursday.

Track 2 of the initiative is meant to prioritize projects that would use available transmission capacity and are located in zones where the ISO’s transmission planning process identifies the need for additional capacity based on state resource planning.

The ISO is planning to hold stakeholder meetings on Track 2 this year and to seek board approval in December.

ST. LOUIS — MISO participants weighed in on the grid operator’s recent moves to fortify resource adequacy during this week’s Organization of MISO States’ annual Resource Adequacy Summit.

The May 15-16 summit played out as the results from the RTO’s first seasonal capacity auction were pending. The auction was delayed a month after a FERC show-cause order to calculate an accurate capacity ratio. (See MISO Unveils New Seasonal Auction Timeline, Ratio.)

“This isn’t your grandfather’s resource adequacy problem,” NERC CEO Jim Robb told attendees. He said the convergence of increasing electric demand, intermittent generation and baseload generation retirements, and intensifying weather events are complicating reliability planning.

“We all have to figure out what the right balance is between reliability, environment and affordability,” Robb said.

He said NERC is noticing a “disorderly retirement” of thermal generation where lost reliability value is outstripping new resources’ contributions. He added that firming capacity from long-duration storage, small nuclear reactors and hydrogen is a long way off.

However, he said, four-hour storage is currently making a “big, big difference” during weather events, contrasting CAISO outages between 2020 and 2022 heatwaves. Robb said fewer outages could be chalked up in part to increased storage capacity; developers added more than 2.5 GW of battery power capacity in 2022, about double the installed battery power capacity in 2021.

Robb said using a measure of capacity on a peak day to ensure resource adequacy is “not sufficient anymore.” He said MISO stakeholders must ask themselves the length of outages customers are willing to endure and how much they’re willing to pay to avoid them. He said markets should use pricing constructs that mimic where customers draw those lines.

“There’s no such thing as a worst-case scenario. There’s always worser,” he warned.

Ameren Missouri’s Andrew Meyer said counter to some perceptions, his utility carefully weighs its fossil fleet’s retirement decisions. The utility plans to keep its coal-fired Labadie Energy Center’s units and the Callaway Nuclear Generating Station online through the early 2040s.

“Some of that coal needs to remain online so we can reliably deliver a whole lot of renewables, which is what our customers prefer,” Meyer said. “We are thinking twice before we retire coal, but we do have a timeline. These are aging plants.”

Meyer said Ameren is preparing to file an integrated resource plan this fall. He said much has changed since it filed its last plan in 2020, including carbon capture and hydrogen conversion, reliability backstops in a faster clean energy transition, a consideration of seasonal generation availability and accounting for supply chain obstacles.

Constellation Energy’s Bill Berg agreed that RTOs are entering a new era of resource adequacy challenges and must roll out improved risk modeling.

“We’re learning about it. I’m not sure we’re learning about it fast enough,” Berg said of evolving risk. He said when it comes to accreditation, only about 30 hours matter throughout the year.

“The real question in my mind is, ‘Are you going to be reasonably available’” during those hours, he said.

Todd Ramey, senior vice president of markets and digital strategy, said MISO’s push for availability-based accreditations across all resource classes is critical, given that an ever-growing share of the fleet is becoming dependent on weather.

“This is a complex process that we were allowed to not worry about when we could assume that individual resources’ accreditation levels were static throughout the season,” he said.

Ramey pointed to the 170 GW of renewables and energy storage requests that hit MISO’s interconnection queue last year. He said decarbonization is driving more renewable energy, with the “delta” between installed capacity and accredited capacity continuing to widen.

“All arrows, all vectors are pointing to the trend continuing,” he said.

Just a few years ago, Ramey said, his team was expecting 215 GW of installed capacity by 2042. Today, staff anticipates they will have 466 GW of resources by 2042.

“Things are changing, and they’re changing faster than we thought they would a few years ago,” he said. Ramey said MISO will likely need dynamic operating reserves and load integration in its markets to keep up the pace.

He joked that MISO’s vertical demand curve in its capacity auctions worked exactly as intended: It “produce[s] inefficiently low or inefficiently high prices, if that’s your design objective as an economist.”

Adopting a downward-sloping demand curve is imperative, Ramey said, because it will eliminate some near-zero capacity pricing and keep some resources from retiring. He said allowing inefficiently low-capacity prices results in a bias that ignores real reliability risks. Retaining even a “handful of gigawatts” is crucial when MISO is on a razor’s edge to meet reserve margin requirements, Ramey said.

“I think one of the reasons we’re in the situation we are today is because the markets don’t value capacity,” Michigan Public Service Commission Chair Dan Scripps said. He said MISO should enact administrative requirements or change auction price signals to correct “essentially free” capacity prices and that Michigan agrees with the sloped demand curve.

“If the problem has been caused by the signals the market has been sending, then correcting the signals the market has been sending is probably the first step,” Scripps said.

“The market has to send a signal of the true value of the capacity,” North Dakota Commissioner Julie Fedorchak said. “One thing we’ve been really good at is retiring excess capacity, so, mission accomplished. Success. Let’s move on to other things.”

MISO Independent Market Monitor David Patton said “perpetually” clearing prices close to zero is “killing” vertically integrated utilities and forcing them to subsidize other parties who buy their excess capacity in the auctions.

Patton said he’s not worried that introducing a downward sloping demand curve will lead to surpluses. Also, he advocated for a marginal accreditation methodology that captures the diminished returns of increased output from renewable energy.

“If we accredit resources right, we’re going to find that we’re pretty tight,” he said. “I don’t see that we have any option other than to accredit capacity on the margins. It’s the only way to facilitate accurate planning. … This market cannot work without accreditation.”

Stakeholders recently pushed back on MISO’s plan to use a marginal accreditation based on units’ performance during predefined tight operating conditions. The grid operator proposed the new methodology for all resources less than a year after winning FERC approval to use an availability-based accreditation for thermal generation. A marginal approach across all resource classes will eventually have MISO assigning solar generation near-zero capacity credits by 2031. (See MISO Accreditation Impasse Persists at Workshop.)

Arne Olson, senior partner at consulting firm Energy and Environmental Economics, said that if capacity market’s primary purpose is “to provide the right incentives for economically efficient resource entry and exit,” then it must use marginal accreditation based on effective load carrying capability (ELCC).

“There, I said it,” he joked. “But it’s true.”

He said marginal ELCC accreditation is the only method that recognizes the complementary interactions between solar and battery storage, solar and wind, and renewable energy and hydropower.

“No resource is perfect,” Olson said. “We need to hold all resources to the same standard.”

He said loss-of-load probability modeling remains “the foundation for understanding resource adequacy needs.” However, he recommended the RTO adapt its weather data to account for climate change.

Zak Joundi, MISO’s executive director of market and grid strategy, touched the third rail of resource adequacy and accreditation during his presentation.

“I was told there are two things you can’t talk about at the Thanksgiving table: religion, politics, and I believe we should add resource adequacy. Completely polarizing, especially if you’re talking about accreditation,” he said, drawing laughs from his audience.

Joundi said though the RTO has a lot to tackle, its current RA efforts appear to be in the right direction.

He said MISO has to quicken the pace and pointed out that its transmission planning futures have transformed dramatically in the few years since their last refresh.

“There are a lot more problems coming at us faster than we have solutions,” Joundi said.

Eric Vandenberg, deputy director of FERC’s Office of Energy Policy and Innovation, said two commissioners believe much of the country is “barreling toward” a resource adequacy crisis.

“I think across the board there is a fair amount of concern,” he said, noting it’s not because any grid operator is doing anything wrong, but that the resource transition is gathering steam.

Vandenberg said the MISO region is staring down the country’s largest share of coal retirements. “I don’t think these are intractable problems. I think we can work together to solve them,” he said.

Entergy Louisiana’s Laura Beauchamp said the utility wants to bring more resources online and reliably balance the new renewables.

She said Louisiana is experiencing “once-in-a-generation” industrial load growth and Entergy doesn’t want to impede the new generation international developers are clamoring for. However, she said, Louisiana’s future load obligations are worrying.

“Our concern is planning for resource adequacy,” she said. “We don’t want to be the one to tell Louisiana it can’t grow.”

OMS Executive Director Marcus Hawkins said MISO’s progression to a voluntary auction with a vertical demand curve, including failed attempts to introduce mandatory participation, a minimum price offer rule, a sloped demand curve and a forward market for retail choice states, are examples of MISO “supporting state oversight of resource adequacy.”

He said MISO’s recent shift to a four-season capacity market with an availability-based capacity accreditation and a proposal to use a sloped demand curve still seeks to respect state jurisdiction while meeting a new operating environment.

“We have this new role where more is being considered for resources adequacy both at the state level and at the RTO level,” Hawkins said. Resource adequacy activities are becoming “increasingly connected” between the states and MISO, he said.

Referring to the accreditation debate, MISO’s vice president of system planning, Aubrey Johnson said “nothing works without transmission connecting it.”

“Transmission is the conduit to deliver generation to the load,” he said.

Xcel Energy’s Drew Siebenaler said MISO’s long-range transmission planning effort is a “cornerstone” of Xcel’s future generation plans.

National Renewable Energy Laboratory researcher Jess Kuna said she’s happy that transmission expansion has entered the conversation as a way to build resource adequacy.

“We often think about resource adequacy, and we think about building generation, and then transmission comes in after the fact,” Kuna said. She said RTOs should coordinate capacity planning alongside transmission expansion.

“Since Sept. 4, 1882, when the Pearl Street Station opened, generation has been changing,” Johnson said. “Now, it’s changing at a rate faster than anything that has ever happened in the history of the electric system.”

Johnson also said while an auction demand curve change might keep aging resources online, an accreditation incentive also is necessary to keep aging units properly maintained and available when needed. He said “you haven’t accomplished anything” if resources are saved from retirement but are neglected to the point where they might as well be retired.

MISO delivered an incomplete summer readiness report Thursday to allow staff to digest the results of the RTO’s first seasonal capacity auctions.

J.T. Smith, MISO executive director of market operations, said the monthlong delay in the Planning Resource Auction left the RTO without the capacity data it gleans from the results and unable to prepare its seasonal resource assessment.

“It’s generally an attraction to this meeting,” he told stakeholders during a teleconference Thursday.

MISO posted the results late Wednesday, showing sufficient capacity across all seasons in all zones, which diminish the chances that the RTO anticipates emergency operating procedures this summer. (See related story, 1st MISO Seasonal Auctions Yield Adequate Supply, Low Prices.)

Smith said MISO will present its usual summer assessment at the Reliability Subcommittee’s meeting Tuesday.

He said that though the assessment might show a chance of an emergency declaration, “emergencies in MISO aren’t necessarily emergencies.” Smith said the RTO usually has about 12 GW of load-modifying resources that clear in the capacity auctions but aren’t available unless the grid operator calls for emergency procedures.

“I want to emphasize that emergency declarations in MISO don’t mean we’re on the cusp of load shedding,” Smith said.

But he also said MISO had been expecting more solar generation additions to the system than what ultimately will begin operations in time for summer. About 41 GW worth of resources with signed generator interconnection agreements are prevented from commercial operations because components are tied up in supply chain issues, Smith said.

Lacking capacity data, MISO staff nonetheless presented all other summer system outlooks during the call, predicting a decent chance for June heat, a rainy summer for the Midwest and low chances for a hurricane in the Gulf of Mexico.

Staff also said they are predicting a second summer in a row where the hottest days are clustered early in the season. Last summer, the MISO footprint saw nine days in June and July when the systemwide temperature exceeded 90 degrees Fahrenheit. MISO said the hottest — and riskiest — days last year were “frontloaded” in June.

MISO meteorologist Adam Simkowski said that with an El Niño climate pattern developing as predicted, the RTO is anticipating a “near- to slightly below-normal hurricane season in the Atlantic Basin.”

Fellow meteorologist Brett Edwards said that while there was a dry pattern across much of the footprint last year, above-normal precipitation is expected this year across MISO Midwest.

Smith said it’s useful to assess even uneventful summers like last year because equal preparation goes into system events and non-events alike.

“Luckily, 2022 was generally a calm summer,” Smith said, adding that hurricane activity in the South was low, and MISO was able to successfully navigate the June heat wave.

“We came close, but we didn’t quite get to that level,” MISO Senior Adviser Mike Mattox said of the lack of maximum generation emergency declarations last summer. June 21 marked the hottest day systemwide in more than a decade, he said.

MISO risk manager Congcong Wang said the RTO has rolled out an operations risk assessment process this year to better manage “increasing uncertainty and variability” occurring on the system. Wang said MISO will assess summer risks from weeks to hours ahead using analytics and meteorological data.

Finally, MISO planner Dalton Daughtrey said an RTO analysis showed that all major transmission constraints already have mitigations in place for this summer. Daughtrey said MISO will monitor future transmission outages that may be necessary as construction ramps up on its first long-range transmission plan portfolio. Most of the $10 billion portfolio used existing rights of way for the new line work.

ALBANY, N.Y. — Facing the possibility that it will not be able to generate enough electricity with renewable technologies such as wind and solar, New York is considering adding more controversial forms of power generation to its climate protection strategy.

The state’s Public Service Commission on Thursday began a review process that could lead to a greater role for hydrogen, bioenergy, nuclear power, carbon capture and other technologies viewed with suspicion or outright hostility by the environmental advocates who have pushed for climate legislation (15-E-0302)

.

The PSC ordered staff to identify technologies that might work for New York, started a two-month public comment period, and directed that at least one technical conference on the subject be held within the next four months.

New York codified one of the most ambitious decarbonization schedules in the nation in 2019, with the landmark Climate Leadership and Community Protection Act (CLCPA). It sets a goal of 70% renewable energy by 2030 and a 100% zero-emission grid by 2040.

Enough projects are now in the pipeline to reach 66% renewable, but many are unlikely to ever reach the construction stage. And those that are built will not produce power when the sun does not shine or the wind does not blow.

The CLCPA scoping plan completed in December 2022 relies on other technologies maturing to a scale and price that will make the 2040 goal attainable.

But the PSC order notes that several studies indicate current renewable resources may not be able to reliably replace fossil fuels — that existing technology is incapable of meeting the growing needs of the grid.

The order also notes that neither state Public Service Law nor the CLCPA define “zero-emissions” technologies.

‘Magical’ and ‘Scary’

Thursday’s order incorporates some aspects of a petition submitted to the PSC in August 2021 by a power industry trade association and two labor organizations: the Independent Power Producers of New York, the New York State Building & Construction Trades Council and the New York State AFL-CIO.

The 12-page petition urged the PSC to consider zero-emitting technologies that are not renewable, and to define zero-emissions energy systems as those that do not lead to a net increase in greenhouse gas emissions.

Comments included a 32-page rebuttal by the Sierra Club and 24 allied groups, shooting down the petition detail by detail.

More recently, NYISO has warned of narrowing reliability margins as fossil fuel plants are retired and replaced by renewable energy generated by intermittent resources. NYISO calculates the New York grid would need 27 to 45 GW of dispatchable emissions-free resources under the CLCPA scenario.

That is potentially more than the entire currently installed generation capacity in New York state — 37 GW — and there is no technology identified to fulfill that need.

IPPNY President Gavin Donohue, who helped draw up the scoping plan and voted against its adoption, has railed against what he calls the reliance on magic in the planning process — the belief that something will come along in time to affordably fill the gap.

He told NetZero Insider on Thursday that the PSC order does not solve this problem, but he is glad to see aspects of the 2021 petition incorporated in it.

“I see it as incremental progress,” Donohue said. “Nonetheless, it’s better than nothing. I’m appreciative that after two years people are taking this issue seriously.”

Whatever technology the PSC decides on, he said, it needs to be tested, proved, abundant, affordable and be available soon, as things take a very long time to build in New York.

“How we get to zero by 2040 is really magical, and at this point scary, because the technology doesn’t exist.”

The vote by the PSC was unanimous.

“The Commission’s action reaffirms efforts to ensure New York has the needed clean-energy resources to replace existing fossil fuel-fired power plants,” PSC Chair Rory Christian said in a news release. “I am proud that New York continues to lead by advancing important clean energy initiatives, such as the one commenced today.”

Two commissioners who frequently object to the process by which the regulatory agency is overseeing the energy transition — and to the costs it is authorizing — weighed in on the theme of wishful thinking.

“The order, maybe for the first time, clearly, expressly identifies that we are realizing the challenges of getting to where we need to be [and] the false narrative around that,” Commissioner Diane Burman said.

There is a need to get under the hood, she said — not to halt the transition, but to be good stewards of regulated industries and their ratepayers’ dollars.

Commissioner John Howard said much of the CLCPA is based on hopes, dreams and good intentions. “This process that’s outlined is much more reality-based. This is the entity that needs to be the reality-based decision maker. It doesn’t seem to be emerging from other state agencies and authorities. It’s our job to say what can work and what can’t work.”