Below is a summary of the agenda items scheduled to be brought to a vote at the PJM Markets and Reliability Committee and Members Committee meetings Wednesday. Each item is listed by agenda number, description and projected time of discussion, followed by a summary of the issue and links to prior coverage in RTO Insider.

RTO Insider will be covering the discussions and votes. See next week’s newsletter for a full report.

Markets and Reliability Committee

Consent Agenda (9:05-9:10)

The MRC will be asked to endorse:

D. proposed revisions to Manual 3: Transmission Operations resulting from its periodic review. The proposed language updates references in the document and aims to add clarity.

E. proposed revisions to Manual 11: Energy and Ancillary Services Market Operations related to real-time values through its periodic review. The changes are largely typographical.

G. proposed conforming revisions to Manual 11, Manual 27: Open Access Transmission Tariff Accounting and Manual 28: Operating Agreement Accounting Market Operations related to the hybrid resources phase 1 package approved by the MC on Feb. 23. (See “MIC Endorses Proposal on Hybrid Resources,” PJM MIC Briefs: Nov. 2, 2022.)

H. proposed revisions to Manual 15: Cost Development Guidelines related to the heat input guidelines and the Independent Market Monitor’s opportunity cost calculator. The changes to the heat input guidelines include documenting the current methods for units to develop their heat input curves, while the opportunity cost calculator changes include a description of a two-hour look-ahead window for the commitment and de-commitment of generators in the calculator.

1. Synchronized Reserve Requirement for Reliability (9:10-9:50)

A. PJM’s Donnie Bielak and Phil D’Antonio will present proposed revisions to Manual 11 section 4.3 and Manual 13: Emergency Operations section 2.2 to correspond with the increase to the synchronized reserve requirement announced at the May 11 Operating Committee meeting. The revisions seek to clarify when PJM can increase the reserve requirements. (See “PJM Doubles Synchronized Reserve Requirement,” PJM OC Briefs: May 11, 2023.)

B. Monitoring Analytics President Joe Bowring will give a presentation on the Monitor’s perspective on the increase.

Members Committee

Consent Agenda (1:05-1:10)

The MC will be asked to endorse:

B. proposed tariff and Operating Agreement revisions addressing renewable dispatch. The proposal was endorsed by the MRC at its April 26 meeting and is intended to provide dispatchers with more data to aid in anticipating the output of renewables. (See “Renewable Dispatch,” PJM MRC Briefs: April 26, 2023.)

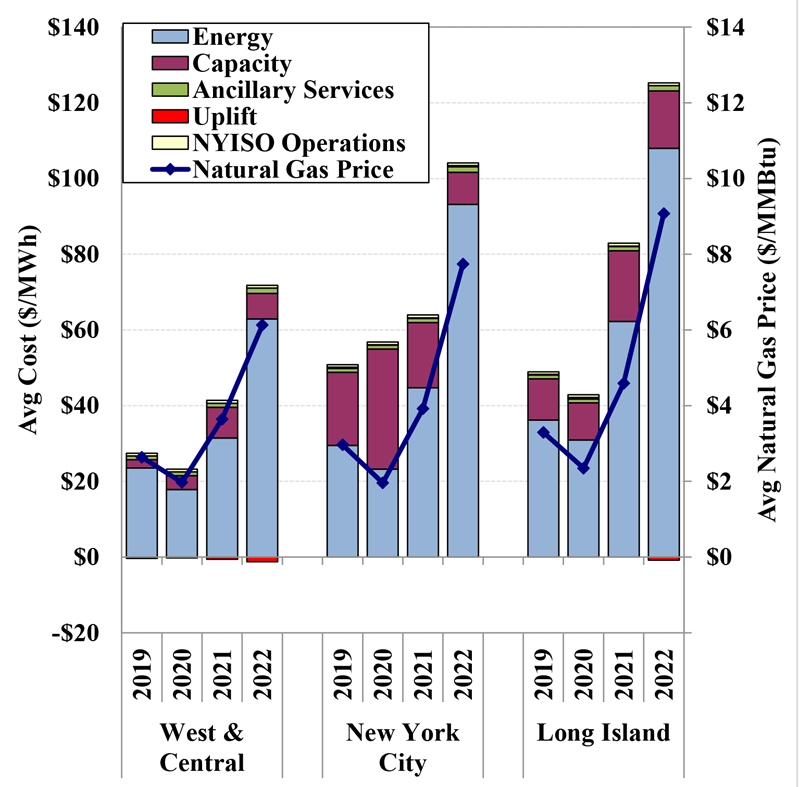

NYISO needs to improve shortage pricing and create smaller capacity zones, the ISO’s market monitoring unit (MMU) said in its 2022 State of the Market report.

MMU Potomac Economics, which presented its findings at Thursday’s Installed Capacity/Market Issues Working Group (ICAP/MIWG) meeting, reported that the ISO remained competitive in 2022 but said changes are needed to ensure market efficiency as renewable penetration increases.

Average all-in price by New York region | Potomac Economics

The report includes five high-priority recommendations, three of which — modeling local reserve requirements in New York City load pockets, dynamically adjusting operating reserve requirements, and improving capacity modeling and accreditation (Recommendations #2017-1, 2015-16 and 2021-4) — are already being pursued.

Also on the high-priority list are a recommendation from 2017 to modify operating reserve demand curves to improve shortage pricing (#2017-2) and one new recommendation: to create more “granular” locations in the capacity market (#2022-4).

The MMU found that NYISO’s shortage pricing has fallen well below that of neighbors PJM and ISO-NE. “When there is an imbalance between the market incentives provided in two adjacent regions, it can lead market participants to schedule interchange from the area with weaker incentives to the area with stronger incentives even when the area with weaker incentives is in a less reliable state,” the MMU said.

Four Capacity Zones Not Enough

The MMU said the ISO’s current four capacity zones (New York City, Long Island, Lower Hudson Valley and Rest-of-State) are too large to provide efficient locational price signals to incent new flexible generation and encourage the retirement of less valuable resources.

The state’s four zones do not account for transmission limits within the zones, meaning resources at some locations are over- or under-compensated relative to their reliability value, the MMU said.

It recommended the ISO create and “dynamically update” an increased number of capacity zones reflecting the known transmission constraints, saying the change also would address “concerns that the current deliverability framework is an inefficient barrier to investment in new resources.”

It said the ISO should not use its existing capacity zone creation process, which it called “flawed and ineffective.”

Potomac said the ISO’s method for determining local capacity requirements (LCRs) results in inefficient prices across zones and excessive price volatility.

Instead, it said the ISO should consider basing locational pricing on marginal reliability values instead of the current zonal demand curves. “This could result in sizeable reliability and economic benefits over the long term and simplify the administration of the capacity market,” it said.

In the 2023/24 capability year, the MMU said, large resources and “Special Case” demand response resources in New York City will receive as much as $52 million in excess capacity revenue.

Some fossil fuel and nuclear generators also were overpaid because the ISO included in their installed capacity 1,200 MW that was “functionally unavailable” on the hottest days last summer, Potomac said. “This includes resources with emergency capacity that is virtually never committed in practice, resources with ambient water and air humidity dependencies that are not captured in the [dependable net maximum capability] testing process, and cogeneration units that face limitations associated with their steam host demand.”

The MMU reiterated a recommendation from its 2021 report that the ISO improve its resource adequacy model (#2021-4) and added a new proposal: that it compensate capacity suppliers based on their contribution to transmission security when LCRs are set by transmission security needs (#2022-1).

Deliverability Testing

Potomac also highlighted what it called a misalignment of the ISO’s deliverability framework, which it said “unreasonably inhibits new investment.”

It noted that the recently completed Class Year 2021 study initially allocated $1.5 billion in system deliverability upgrade costs to 4 GW of new projects seeking to sell capacity — costs that equaled between 50% and 293% of the net cost of new entry of a new peaking plant. “Unsurprisingly, three-quarters of the affected projects refused to pay these costs and either withdrew from the Class Year or accepted a reduced quantity of [capacity resource interconnection service] rights,” Potomac said.

Current ISO rules use a deterministic test “that often does not represent a realistic or likely dispatch of the system during conditions when reliability is threatened,” Potomac said. “This problem is exacerbated by performing the test in relatively large capacity zones with many potential intrazonal constraints.”

In the short term, the MMU said, the ISO should identify “a comprehensive set of granular locations” that would effectively shrink the size of the capacity zone in which new interconnecting resources would have to be deliverable. The change also would allow reduced clearing prices in export-constrained areas, it said.

Seasonal Capacity Market

The MMU also recommended the ISO move to a seasonal capacity market, with requirements and demand curves that consider the reliability needs of each season separately (#2022-2). Although the capacity market is divided into six-month summer and winter capability periods, the installed reserve margin and LCRs are determined annually, so ICAP requirements are the same in all months. “As a result, seasonal prices are determined by the amount of ICAP available in each season, which bears little relation to resource adequacy risk,” Potomac said.

Transmission Planning

The MMU also offered a new recommendation on transmission planning, saying current rules allow inefficient projects to crowd out competing market-based investments — including transmission and nontransmission resources — that could achieve the same policy goals at lower cost.

Potomac acknowledged the ISO’s recent addition of capacity expansion modeling tools. But it said additional changes are needed to respond to the increased uncertainty from the growth of policy-sponsored resources.

It recommended the ISO update its planning study methodology to reflect the market incentives of renewable and storage resources; consider changes to the resource mix resulting from the inclusion of economic and public policy projects; and estimate transmission project benefits based on their market value to the ISO (#2022-3).

The MMU’s report was discussed with stakeholders for the first time at the ICAP/MIWG meeting, where the focus was on energy and ancillary services. Potomac will present the report to the Management Committee meeting and discuss capacity market issues at the next ICAP/MIWG meeting, June 6.

Other Recommendations

Potomac’s Pallas LeeVanSchaick, who presented the findings at the May 25 meeting, said the efficiency of the energy and ancillary services markets will become increasingly important as NYISO increasingly shifts from fuel-secure generation to intermittent renewables.

The report cited inefficiencies for reserve providers, which are not being compensated for their congestion relief; duct-firing combed cycle units, which are not being properly dispatched; and phase angle regulators, which are inappropriately being used to satisfy bilateral contract flows.

In addition to the high priority recommendations, LeeVanSchaick also highlighted five other proposals during Thursday’s meeting.

2015-9: Eliminate transaction fees for coordinated transaction scheduling at the PJM-NYISO border.

2016-1: Consider rules for efficient pricing and settlement when operating reserve providers provide congestion relief.

2020-1: Consider enhancements to the scheduling of duct-firing capacity in the real-time market that more appropriately reflect its operational characteristics.

2021-2: Model full locational reserve requirements for Long Island.

2022-3: Improve transmission planning assumptions and metrics to better identify and fund economically efficient transmission projects.

Market Highlights

Potomac reported that average natural gas prices roughly doubled from last year in eastern New York and rose 70% in the western part of the state due to increased LNG exports and cold weather.

The high gas prices drove energy prices, with average energy prices in Western New York rising to 109% over 2021 and Eastern New York rising as much as 126%. Gas prices, cold weather and transmission congestion pushed all-in energy prices to the highest levels observed in more than a decade, ranging from $58/MWh in the North Zone to nearly $127/MWh in Long Island.

More severe transmission congestion in the Central-East interface because of lengthy outages during construction of the AC Public Policy Transmission Projects contributed to the East-West price separation.

Capacity costs fell, primarily because of changes in the installed reserve margin for the system and LCR requirements for New York zones.

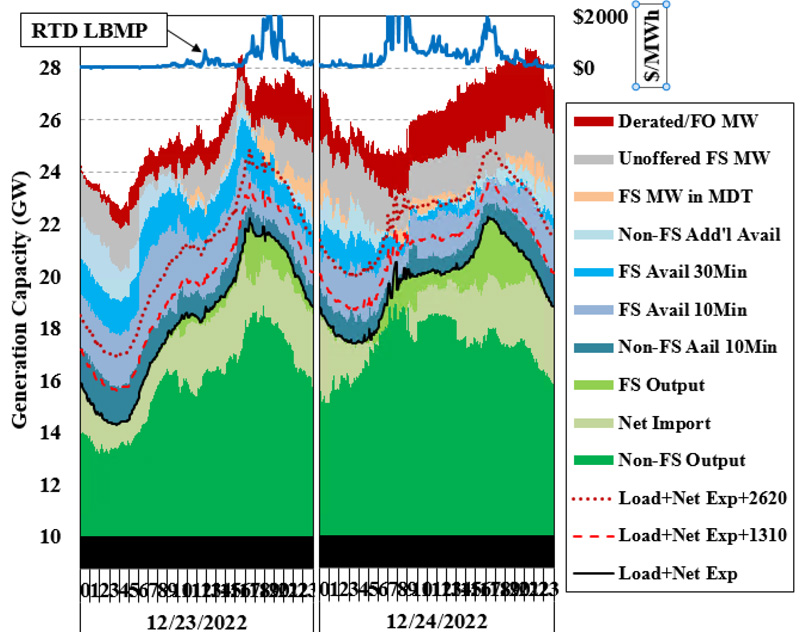

Winter Storm Elliott

Another highlight from Potomac’s annual report was the analysis of Winter Storm Elliott’s impact on the New York grid, which showed NYISO’s market operations relied heavily on the scheduling of internal peaking units to meet high demands and that large quantities of generating capacity was unavailable because of fuel limits or outages.

Resource supply availability and utilization during Winter Storm Elliott | Potomac Economics

Winter Storm Elliott hit the Northeast from Dec. 23 to Dec. 27, 2022, and blizzard conditions through the 24th caused New York energy prices to spike to more than $4,000/MWh.

LeeVanSchaick said the storm “was the first significant test for some market processes that have come into place over the past 10 years that deal with shortage conditions.”

“This was the first time we’ve seen long-duration reserve shortages since PJM and ISO-NE put [Pay-for-Performance] rules in place,” he added. PFP rules incentivize generators for being available during tight supply conditions.

On Dec. 23 and 24, NYISO experienced eight hours of reserve shortages, locational-based marginal prices of more than $2,000/MWh, roughly 4 GW of import curtailment and around 2.3 GW of unavailable fossil fuel capacity because of outages or derates.

Because the amount of forced outages and derated capacity was higher than anticipated, Potomac said NYISO needs to better monitor generator performance during extreme weather, given that current resource adequacy models may be underforecasting load during these cold conditions and inefficiently dispatching generators to provide reliability.

The report also noted that about 80% of unoffered capacity during the blizzard was from energy storage and other duration-limited resources. The MMU said NYISO needs to investigate ways to make sure that during cold conditions, these resources can recharge after being called upon and be available for extended periods of time.

Potomac said the ISO’s real-time commitment scheduling was being undermined, citing the number of import curtailments and unforeseen reductions in supply availability, because of either high gas prices or inefficient market signals.

The MMU noted that several fast-start units were either being shut down or not started up when they might have otherwise, which meant 470 MW of these units was unavailable and an additional 1,350 MW of 30-minute fast-start capacity was sitting offline. This resulted in imports from neighbors like PJM to be curtailed because of unnecessarily high prices in New York.

Based on these findings, Potomac made several recommendations to improve NYISO’s capabilities during future winter storms.

The MMU recommended setting prices consistent with the reliability risks during a reserve shortage event, enhancing capacity accreditation models for nonfirm fuel generators or duration-limited resources, and scheduling additional reserves before blizzard conditions to decrease the NYISO’s reliance on imports.

WASHINGTON – The United States Energy Association saw a change of leadership and heard from speakers on the transition to clean energy at its Annual Membership Meeting and Public Policy Forum last week.

Acting USEA Executive Director Sheila Hollis, of Duane Morris, has run the organization since longtime Executive Director Barry Worthington died in 2020. She announced her term was coming to an end and that she would be replaced by former U.S. Deputy Energy Secretary Mark Menezes.

NARUC’s White Speaks on the Role of the States

“We have an international programs department, and Sheila has heard me say this many, many times,” said Greg White, executive director of the National Association of Regulatory Utility Commissioners. “I consider us to be a partner with USEA. USEA does training for the utilities around the world. And we go into those exact same countries, and we train the regulators.”

NARUC has worked in more than 50 countries in its history and is currently helping 30 with their regulatory systems, he said. White’s first overseas trip was to the country of Georgia, where he helped fix its creaky, post-Soviet grid.

“Everybody in the country was carrying a flashlight with them because in the Soviet-era buildings, the elevators usually didn’t work,” White said. “And so, people had to walk up many flights of stairs in the dark to get to their apartments.”

Now the Georgian grid is reliable 24/7, and the days of always needing a flashlight are over, he said. That is what drives regulators here and abroad — bringing light to the world, he said. The challenge now is to make the grid’s transition happen without major issues.

“We’re trying to get cleaner energy that is sustainable, reliable, resilient and affordable,” White said. “And we need to balance all those interests.”

Most of the progress that has been made on clean energy in recent years is because of state and local policies, but now much of the conversation in D.C. on permitting reform would strip those states of at least some of their authority to site transmission lines.

“We’ve got some proposals in Congress right now that, quite frankly, would eviscerate the role of the states and permitting new infrastructure, especially as it pertains to the much needed electric transmission infrastructure,” White said. “We believe that that would be a mistake because the states have considerably more success at siting infrastructure than the federal government.”

NARUC’s engagement with FERC has been more fruitful, with White highlighting the Joint Federal-State Task Force on Electric Transmission as helping to reach common policies needed to make the energy transition work.

The ‘Materials Transition’

Another aspect of the clean energy transition that was not addressed much by major legislation last Congress is materials, said Michelle Foss, fellow at Rice University’s Baker Institute for Public Policy.

“I’m going to take a modicum of credit for the phrase ‘materials transition,’” Foss said. “The idea that the energy transition is a materials transition is because I pushed to get minerals on the agenda of an international meeting last year. And we were successful in that, and now I’m finding this phrasing is rolling around.”

The conference was in Tokyo, and the Japanese government has been pushing the issue to the forefront. Foss said the G7 nations are now actively pursuing the issue.

“My own view on this is that you put materials first,” Foss said. “But we didn’t do that. We rolled out an enormous spending program, sending people off in all manner of directions trying to do things that they can’t do, because we don’t have the material supply chains to support them. And that … is energy policy in the United States.”

Foss is an alumna of the Colorado School of Mines. When she was there in the 1980s, the domestic mining industry was dying, and now it has essentially given up all of its capacity, she said. Labor and compliance with environmental laws, which brought benefits, have made the business generally too expensive here, so it moved overseas.

“China constitutes 44%, in our math, of total tonnage of nonfuel minerals in the world today, everything from metals to non-metals, to construction materials — they are it,” she said. “This is not their fault; it’s ours. We gave up our capacity, and China took a market share.”

The U.S. is going to need secure supply chains of many minerals as it transitions to a clean economy, replacing equipment and infrastructure as they wear out, said Foss.

While much of the focus in the energy industry involves a shift away from carbon, Foss said that the element was going to be important forever because it is also used to make superior and cheaper materials that can replace metals.

“If I can displace metals with that, then I’m simply doing what humans have been doing for decades now, which is displacing metals with plastic, but a better form of it; a more advanced form of it,” Foss said.

SPP staff told stakeholders Friday they will work with MISO staff to draft a white paper on rate pancaking and unreserved use, two issues that bedevil utilities along the RTOs’ seam.

Clint Savoy, SPP’s manager of interregional strategy and engagement, told participants during the RTOs’ spring update on common seams initiatives that the focus will be rate pancaking. He said while the two issues are separate and distinct, rate pancaking “is more of an issue that occurs.”

The RTOs’ staff will work with stakeholders and solicit their input in developing solutions, Savoy said. SPP will also use Seams Advisory Group as a sounding board in determining the paper’s final draft. Later work will involve analyzing the proposals to determine their impact.

MISO’s Marc Keyser, director of seams coordination, membership services and customer coordination, said his staff will be slow to join the effort, given their work with the grid operator’s long-term transmission planning.

“We may have difficulty doing some of the analysis we want to do with the white paper, but we’re looking forward to working with SPP,” he said.

A working group composed of state regulators from the grid operators’ footprints was the most recent stakeholder group to look at rate pancaking, which occurs when power is scheduled across more than one transmission provider’s borders and each provider assesses full or partial charges for use of the facilities. That leads to duplicate transmission fees between the various providers.

Arkansas Electric Cooperative Corp. (AECC) said during a presentation to the group that it has incurred about $100 million in incremental costs over the past 10 years because of pancaked rates. AECC is connected to four transmission systems within the two RTOs.

Unreserved use charges can be assessed when an RTO transmission customer does not reserve adequate service to cover its load obligation. These charges are higher than the cost of reserving transmission and can have a ratcheting effect that transmission customers see as punitive.

The RTOs are currently involved in a dozen seams initiative between themselves and with stakeholders, both at the state and federal level. Their staffs will hold another update on seams initiatives in November.

FERC last week denied a solar farm developer’s tariff waiver request and a complaint against SPP over the RTO’s interconnection studies for the planned facility (EL22-89).

The commission issued an order May 23 finding that Cage Ranch, a 900 MW project in West Texas, had not met its burden to show that SPP violated its tariff or conducted its studies in an unjust and unreasonable manner. It said the solar facility did not demonstrate the study models underlying the cluster study were defective.

Cage Ranch said in an amended complaint that the study in question should not have been used to determine interconnection costs for the solar farm and other customers in the study group because SPP failed to resolve alleged nonconvergence issues. But FERC pointed out that the grid operator assigned Cage Ranch network upgrade costs using a modeling approach it applies to all interconnection customers.

The Cage Ranch developers last year challenged SPP’s use of what it called a “defective” study model that assigned interconnection costs and calculated its security obligations within its study cluster. It asked FERC to direct the grid operator to resolve the study model’s defects, allow interconnection customers to post security after the defects are resolved, and require SPP to restore the customers’ queue positions in the study cluster.

Cage Ranch also requested a tariff waiver to extend a decision point deadline until FERC resolved the complaint and SPP issued an updated and corrected study. The commission denied the request, finding Cage Ranch did not satisfy the criteria for such requests (the applicant acts in good faith, the waiver is of limited scope, it addresses a concrete problem, and it does not have undesirable consequences).

OPPD Show-cause Order Ended

The commission also accepted SPP’s tariff changes revising Omaha Public Power District’s (OPPD) protocols, effective January 2024, and terminated a show-cause proceeding under Section 206 of the Federal Power Act (ER23-72).

FERC issued the show-cause order last July after determining that OPPD’s protocols under the tariff appeared to be unjust and unreasonable. The commission directed SPP to either show cause as to why the protocols remained just and reasonable or explain the changes that could be made to remedy the identified problems should FERC find the protocols unjust and unreasonable.

In an order issued May 22, the commission found SPP’s proposed revisions to be just and reasonable and consistent with precedent established in 2015 by MISO protocols orders. FERC said the revisions resolved unclear wording and three technical errors identified by two protests late last year.

The commission said the revisions remedy the show-cause order’s identified concerns and terminated the proceeding.

As amended, the revisions require OPPD to respond to information or document requests within seven business days, giving parties additional time to review and raise informal challenges.

Eversource (NYSE:ES) last week began its anticipated departure from the offshore wind sector, announcing it would sell its interest in an uncontracted New England lease area to its development partner, Ørsted.

Eversource also said it would soon announce sale of its share of three other offshore projects that are farther along in the development process: South Fork Wind, Revolution Wind and Sunrise Wind. Ørsted holds a 50% stake in those projects as well.

The two companies — New England’s largest utility and the world’s largest offshore wind developer — teamed up six years ago to pursue a share of the clean energy production planned off the shores of New York and New England.

Their 132 MW South Fork Wind project south of Rhode Island is expected to start producing electricity this year. It will earn the distinction of being the first utility-scale offshore wind farm in the U.S. unless nearby Vineyard Wind 1 crosses the finish line first. Both started construction last year, but Vineyard is much larger than South Fork, at 800 MW.

Details

Eversource indicated last year that it was looking for an exit from the offshore wind business. CEO Joe Nolan told financial analysts this month that negotiations were nearing completion.

The company will fully exit the development space, but it expects to have a role in transmission of the offshore power generated by Ørsted, he said.

Eversource said Thursday it will sell its 50% stake to Ørsted for $625 million in cash, some of which Eversource will use to provide tax equity for the South Fork Wind project through a new tax equity ownership interest. Eversource will recover that investment through tax credits received around the time of the wind farm’s commercial operations date.

As part of the deal, Ørsted will gain full ownership of partnerships with Quonset Point, the Port of Providence and the Port of Davisville, all in Rhode Island, and the New London State Pier in Connecticut; ownership of the operations and maintenance hub in East Setauket, N.Y.; and the charter agreement for the offshore wind service operations vessel being built in Louisiana.

Eversource said Thursday it expects to announce sale of its share of Revolution, South Fork and Sunrise by the end of June.

Based on the prices being negotiated and on the value of its aggregate investment to date in offshore wind development, Eversource expects the transactions to result in a second-quarter after-tax impairment charge of $220 million to $280 million.

It said it would use net proceeds from the transactions for debt reduction.

The sale to Ørsted is subject to approval by The Committee on Foreign Investment in the United States.

The transaction announced Thursday entails Lease Area OCS-A 0500, known as Bay State Wind. The 187,000-acre tract of federal waters south of the Massachusetts islands of Martha’s Vineyard has a potential capacity of up to 4 GW of wind power.

Ørsted and Eversource as Bay State Wind LLC have submitted proposals for projects they called Sunrise Wind 2 and Revolution Wind 2 in the most recent offshore wind solicitations by New York and Rhode Island, respectively.

No contracts have been awarded yet in either solicitation.

Ørsted said it would continue as the sole bidder on both.

LOWER ALLOWAYS CREEK, N.J. — On a wind-swept tract in the shadow of three nuclear plants, New Jersey’s massive $1 billion play to jump start a new energy industry based on harnessing wind power is proceeding apace on the banks of the Delaware River.

Construction of the New Jersey Wind Port, a 200-acre marshaling, manufacturing and logistics hub for the offshore wind sector, is on schedule and on track for completion of the first phase in April. Phase one will be capable of simultaneously handling multiple turbine towers more than 400 feet long, state officials say.

That phase, with a $550 million price tag funded with state money, will be followed by a second phase, expected to begin construction in early- to mid-2024, with an additional expense of about $550 million. The target completion date is 2027 or 2028.

State officials say they are building the nation’s first custom-designed port able to handle the growing offshore wind (OSW) sector and capable of handling several projects at once, including those inside New Jersey and along the East Coast. And on a recent afternoon, as a state official led a tour of the site for RTO Insider, there were few signs that the state’s massive commitment to wind energy has been sapped by the controversy over a spate of whale deaths in the region or recent opposition to turbines that will stretch more than 900 feet into the air.

“We’re at 60% completion; we’re on or ahead of schedule,” said Jonathan Kennedy, vice president, infrastructure, of the New Jersey Economic Development Authority (EDA), which is funding the port and has overseen its development since Gov. Phil Murphy first announced the plan in June 2020.

“That’s a pretty rapid mobilization and progression from planning to construction,” Kennedy said. “If you came back here April 1, ‘24, you should be looking at a complete port, fully operational, that’s licensed by the Coast Guard.

“The driver here is that we have a non-negotiable need to get this port complete on time,” he said.

Emerging Need

That driver is the 1,100-MW Ocean Wind 1, the state’s first offshore wind project, which was approved in 2019 and is scheduled to begin construction next year. The state Board of Public Utilities (BPU) has since approved two more projects, the 1,148-MW Ocean Wind II and 1,510-MW Atlantic Shores, in the state’s second solicitation in 2021. (See NJ Awards Two Offshore Wind Projects.)

A third solicitation launched by the BPU on March 6 could approve projects totaling 4 GW, and perhaps more, as the state reaches for a goal of 11 GW of OSW capacity by 2040. (See NJ Opens Third OSW Solicitation Seeking 4 GW+.)

The EDA has steadily crafted a sweeping plan to create a support infrastructure around the offshore projects that includes a flagship research hub, small business nurturing programs to provide a groundswell of qualified contractors, and a Wind Institute for Innovation and Training.

At its May meeting, for example, the board approved five grants totaling $3.7 million for programs to train OSW workers and $500,000 for a marketing and communications budget for the wind port, including a new website. The board also backed $6 million in expenditures for construction and test piling done in the land parcel for the second phase of the port.

“New Jersey has a choice of whether we want to lead, follow or be left behind by the clean energy revolution, particularly offshore wind,” Tim Sullivan, EDA’s CEO, told an assembly budget committee hearing on May 17. “And that is an opportunity that if we don’t capitalize on it, I promise you, governors and legislators and other states will. And it’ll be gone, and we will have missed this generational opportunity.”

Hard Hats and Piling

The half-built port, on a recent afternoon, was a hive of activity. A cluster of a dozen half-sunken gray piles soared 30 feet into the air in one section, awaiting attention from a massive yellow crane to pound them down to ground level, ready to support the port marshaling platform. Nearer the water’s edge, workers in black and blue hard hats and bright yellow vests readied rows of steel rebar that would eventually be swathed in concrete to become the berth at the water’s edge.

A few hundred yards away, in the undeveloped section that will become phase two, workers drained water out of sand dredged from the river through a giant sucking pipe.

The first phase of the port, on about 125 acres, will consist of two berths, a 35-acre marshaling yard and two parcels totaling 55 acres for manufacturing. The first phase of the construction will require 1,850 piles, each 110- to 120-feet long and weighing 100,000 pounds. About half of the piles are in place.

They will support a wharf able to handle 6,200 pounds per square foot, enough to take the weight of two or more turbine towers as they are assembled and readied for shipment out to the wind farm in an upright position.

The second phase will add two berths, a 35-acre marshaling yard and 70 acres of additional manufacturing space.

As construction advances, workers are dredging a nearly one-mile channel to a depth of 45 feet to take vessels from the port to the river’s main navigation route. Although that work has stopped at present, so as not to disturb sturgeon in the river, dredging will resume July 1 for the final push to get the port ready.

Scheduled Marshaling

The need for a custom port lies in the specifics of OSW project creation, the EDA says: Turbines are far larger and heavier than most cargo; a regular port berth typically cannot take the weight or size. And the best way to install turbines is to do most of the construction onshore and ship them to the wind farm upright, which requires a route that has no height restrictions, specifically bridges, on the relevant waterway.

Both Denmark-based Ørsted, which is developing the two Ocean Wind projects, and Atlantic Shores, a joint venture between EDF Renewables North America and Shell New Energies US, have signed letters of intent with the BPU to conduct marshaling for their respective ventures at the port.

When the second phase is finished, the port will be able to handle the marshaling for more than one project at once, but the timing of Ocean Wind I and Atlantic Shores, which were approved two years apart, is such that they are not expected to need marshaling space at the same time, Kennedy said.

“Typically, it takes two to three years to marshal for a project of 1 to 1.5GW,” Kennedy said. “The way this port is designed to work is obviously the marshaling parcels will keep getting flipped. Your new projects will come in, and they’ll take two- to three-year leases.”

The EDA determined that having the capacity to handle more than one project at a time was important, in part, to strengthen the state’s offshore wind sector by “ensuring that no one developer locked up the port,” preserving competition, Kennedy said.

“We want all bidders on the BPU solicitations to have marshaling port capacity available in New Jersey, should they be successful in that solicitation,” he said.

The third phase solicitation document makes clear the port’s importance to the state’s OSW ambitions.

“Consistent with New Jersey’s commitment to position the state as a regional offshore wind hub, the BPU strongly encourages use of the New Jersey Wind Port for project marshaling and for locating Tier 1 manufacturing facilities, where feasible,” the document says.

So far, Siemens Gamesa Renewable Energy (OTCMKTS: GCTAY), Vestas-American Wind Technology (OTCMKTS: VWDRY), Beacon Wind and GE Renewables — all prominent offshore wind players — have expressed interest in the past, but it is unclear whether that interest will move ahead. (See NJ Wind Port Draws Offshore Heavy Hitters.)

Kennedy says the EDA is bullish on the question of whether the massive investment is worth it.

“We think there’s going to be continued demand for marshaling, you know, out 20-, 30-plus years,” he said. “We feel like the pipeline of projects that will need marshaling capacity extends well into 2040, 2050 and beyond.”

Turbine Size Increasing

The need for space is fueled, in part, by the rapid increase in turbine size as technology evolves. While turbines deployed in Europe 25 years ago had a capacity of about 2MW, Ocean Wind 1 will use a 14 MW GE Haliade turbine with 360-foot-long blades and total height of 920 feet. Atlantic Shores will use a 15 MW turbine made by Vestas Wind Systems, with 380-foot-long blades.

“Turbines are getting bigger, more efficient, (with) increased output,” Kennedy said, adding that increased efficiency is good for ratepayers but adds to the burden on ports handling them.

“The weight-bearing capacity of the wharf, the dredge depth, the backlands, strength and acreage — all of those things don’t exist, typically, in a port,” he said. “So that’s why we’re building a port.”

The state picked the site from multiple options, narrowing their choices to the Delaware River site and a 50-acre site that formerly housed an oil-fired power plant in South Amboy, opposite Staten Island at the mouth of the New York harbor. The Delaware River site, on a tract that also includes three nuclear power plants operated by PSE&G, had several benefits, including the fact that it was a greenfield site, and so required little remediation, Kennedy said.

Another benefit is the lack of height-limiting bridges on the 60-mile trip between the port and the sea. Any height limitations from a bridge would require the turbines to be moved in a horizontal position by barge and elevated at the final destination, a more complicated, expensive and time-consuming process, he said.

In addition, the large space available at the New Jersey Wind Port, 220 acres, means turbines can be manufactured and assembled on-site.

“You’re effectively wheeling the components out of the factory doors, straight onto the marshaling parcel,” Kennedy said. “And that, again, is good news for ratepayers, because it means you can manufacture and install these components cheaper than if you had to, say, you know, manufacture them elsewhere.

“Time is money with offshore wind, in terms of vessel costs, and other factors,” he said. “You need a large acreage, because you need to get as many components in and lay them down as possible, so that they’re ready to be assembled and shipped back out. You don’t want to be waiting for pieces to arrive, because the installation vessel is so expensive.”

Growing Competition

Whether all that is enough to make the port attractive beyond state borders remains to be seen. Kennedy and others at the EDA said the state has a first-mover advantage and a prime location.

“Basically, we have fortuitously located geographically in the middle of the (East Coast) wind belt,” which now stretches from Maine to South Carolina, Kennedy said.

Yet, competing marshaling and manufacturing facilities are also emerging along the coast. Wind ports of some scale are planned for New Bedford, Mass., New London, Conn., and in New York, at the South Brooklyn Marine Terminal, from where turbines will have to head out to sea lying flat on a barge to pass under the 230-foot-high Verrazano Narrows Bridge.

The Port of Virginia in August allocated $223 million to the construction of a 72-acre port, with a staging area and 1,500-foot berth. And in Maryland, Ørsted and US Wind are investing in OSW port and manufacturing facilities at the Tradepoint Atlantic that Maryland Gov. Wes Moore announced in April “is on track to become the offshore wind capital of America.”

Kennedy, however, cited a 2022 study that suggested the region will need whatever port and marshaling facilities are developed.

The study, by two University of Delaware researchers, concluded that the need for marshaling facilities is a “key bottleneck” in the push to meet state and federal offshore wind policies. The researchers calculated that state and federal offshore wind commitments would create projects with a collective capacity of 40 GW by 2040, stimulating “more demand for marshaling area than is currently available or planned.”

“The shortage of marshaling area supply has incorrectly been attributed to lack of suitable U.S. locations,” the report said. “Instead, we attribute it to developers having built ports to support early, smaller projects … rather than developing ports for long-term, large-scale, and economically efficient use.”

As the 88th Texas Legislature barrels towards its sine die Memorial Day, lawmakers are apparently trying to ensure gas-fired generators are protected from outside market forces and punish renewable resources by placing nearly insurmountable hurdles in front of them.

SB6, which would create a “Texas energy insurance program” by funding 10 GW of gas generation for use during emergency conditions, has been buried in the House of Representatives since mid-April. However, legislators have moved other legislation that threatens one of the world’s largest renewable energy segments. (See Texas Senate Lays out Changes to ERCOT Market.)

On Wednesday night, the Senate added amendments to the Public Utility Commission’s sunset bill (HB1500) that target the renewable energy sector.

The Senate’s Business and Commerce Committee had already added language this week that would require generators interconnected to ERCOT after Dec. 1, 2026, to be able to produce power for at least 15 hours when called upon. Another edit would allocate ancillary services’ and reliability services’ costs to all resources in proportion to their unreliability contributions.

To that, senators added nearly two dozen more amendments, including a firming requirement directed at renewables. One amendment included SB1287, which would raise interconnection costs for renewables by using a postage stamp method that includes the resource’s “reliability impact” to the grid. Another (SB624) would increase the paperwork necessary for renewable developers to secure permits for their facilities.

Conservative Texans for Energy Innovation called SB624 an “industry killer” in a statement, saying it would “impose an unprecedented permitting process on clean energy projects.”

“What a mess of a bill HB1500 has become,” tweeted Stoic Energy’s Doug Lewin, who advocates for energy efficiency and demand response. “It’s a Frankenstein’s monster at this point.”

The Senate unanimously approved the amended bill.

The chamber had already revised and approved HB5 earlier Wednesday. The tax abatement legislation excludes renewable resources, which had been a part of the previous program, from obtaining school property tax breaks for their new facilities but does include fossil-fuel-fired power plants. Renewable resources are already facing a loss of the state’s renewable portfolio standards.

Another bill (SB2627) would create a state-funded, low-interest loan program offering billions of dollars to companies that want to construct gas-fueled power plants; bonuses would be paid if the plants are completed and connected to the ERCOT grid by 2029. It has been amended in the House but must be reconciled in the Senate. Gov. Greg Abbott is said to be “intrigued” by the bill, which would require a constitutional amendment.

Energy consultant Alison Silverstein, a former staffer with the PUC and FERC, noted the magnitude of “thermal plant giveaways” have been reduced, with several bills dead or modified in the House.

“Broadly, however, thermal generators will be the biggest winners from this session,” she told RTO Insider. “Texas energy consumers are likely the biggest losers from this session. If the anti-renewables measures survive, that will raise electricity costs statewide.”

PCM and DRRS

Those costs could also increase with several measures related to the PUC’s proposed performance credit mechanism (PCM), designed to incent new thermal generation and keep existing dispatchable resources online. The PCM would allow generators to sell performance credits in exchange for promising to be available during tight operating conditions. Load-responsible entities would be required to buy the credits, with those costs likely passed on to businesses and residential customers. (See Texas PUC Submits Reliability Plan to Legislature.)

The House on Monday approved SB7, limiting the PCM’s cost to $1 billion a year, net of savings in the energy and ancillary services markets. The Senate’s approved version capped the credits’ costs at $500 million.

The Senate version also excluded energy storage from selling credits, though ERCOT has told the PUC it considers batteries to be dispatchable. The House version doesn’t. The differences will have to be either accepted or reconciled when it goes back to the Senate.

SB7 also includes a proposed dispatchable reliability reserve service (DRRS), a day-ahead reserve product to be deployed when ERCOT uncertainty associated with intermittent resources and load increases. An Austin-based research firm has estimated DRRS will increase market costs by about $4 billion annually.

The new reserve service can also be found in HB1500’s amendments. Both bills would mandate DRRS be implemented by the end of 2024.

“The PCM is a costly, unnecessary tool that will allow the PUC to guarantee profits for generators on the back of Texas customers. This is a regulated approach, but without the customer protections and spending oversight that go hand-in-hand with regulation,” Texas Association of Manufacturers CEO Tony Bennett said in a statement. “This unproven model has the potential to add billions to the market, and without a firm cost cap, it threatens to significantly increase prices on all consumers without meaningfully improving reliability. Future job growth, company location and investment decisions depend upon the Legislature charting the right course before the legislative session ends.”

Bennett was speaking for several other consumer groups who agree that without a cap, the PCM program will hurt their bottom lines. Most of the state’s power generators, including NRG Energy, Calpine and Vistra, support the commission’s version of the PCM and a higher limit.

“This bill will increase costs to our constituents, and it will not increase reliability,” Rep. Chris Turner (D) said during the House State Affairs Committee’s discussion. “That’s the truth. It’ll cost our state, the businesses in our state and our constituents; most importantly, it will cost them money without increasing reliability. And that’s the worst of both worlds.”

Already, several observers have pointed to clean energy investments that are being made in neighboring states and worry that Texas could be left behind. Enel North America announced Monday it will build a $1 billion solar panel manufacturing plant in Oklahoma. To the east, Louisiana has gone all in on developing carbon storage sites, offshore wind farms and clean hydrogen facilities.

“Access to clean, affordable power is an economic development tool,” Advanced Power Alliance CEO Jeffrey Clark said. “Availability makes states more attractive for investment. Emerging industries like carbon capture, synthetic fuels, hydrogen and LNG exports are going to rely on clean power to cut costs.”

Not much time is left: Bills that go to conference committee to reconcile differences must be approved by Sunday in both chambers.

“It’s all up in the air. More to come, but not sure when,” Clark said, summing up the work that lies ahead.

The Legislature’s frantic closing days were highlighted by Attorney General Ken Paxton’s demand that House Speaker Dade Phelan resign from his position after video emerged of him slurring his words during a late-night session. Within hours, the House announced its ethics panel has been investigating a $3.3 million settlement Paxton reached with four former employees who accused him of corruption; the investigators detailed their findings Wednesday during a public committee hearing.

On Thursday, the committee recommended that Paxton be impeached. The House could vote on the recommendation as soon as tomorrow.

Paxton has been under indictment since 2015 for securities fraud. The U.S. Justice Department is also conducting a corruption investigation into the embattled AG that began in 2020. Despite the allegations, Paxton has been re-elected twice since 2015.

New York this week announced two efforts to help boost hydrogen as a means of reaching its emission-reduction goals.

The New York Power Authority will allocate an additional 50 MW of low-cost hydropower to fuel cell manufacturer Plug Power to boost production of green hydrogen at a facility it is building in western New York.

Meanwhile the New York State Energy Research and Development Authority will administer a $10 million solicitation for clean hydrogen research, development and demonstration projects in hard-to-electrify sectors.

Both initiatives are part of the larger effort to slash emissions of greenhouse gases in New York. Hydrogen’s role in the drive to decarbonize is still being defined, as its potential as an economical and environmentally friendly fuel is still being developed.

Plug Power’s award was announced Thursday. The company is based just north of the state capital but has been expanding geographically in recent years as its market and sales have grown.

It began production earlier this year at a new factory south of the capital and is building a hydrogen generation facility near NYPA’s Niagara Power Project, which will supply the electricity announced Thursday. After starting construction of the western New York facility, the company expanded the plans, boosting the designed maximum output from 45 to 74 tons of liquid hydrogen per day.

NYPA sells inexpensive power to chosen businesses as a development tool; Plug receives 272 MW in total at its three existing in-state facilities. The state-owned utility’s board of trustees also authorized it to procure 62 MW of high-load-factor power for Plug on the energy market.

NYSERDA’s R&D solicitation announced Wednesday complements New York’s effort with six other states to form the Northeast Regional Clean Hydrogen Hub.

As its name implies, that is a broad regional effort. The solicitation is more closely focused on problematic New York applications.

“In partnership with the state’s leading innovators and problem-solvers, we are taking bold action to transition even the hardest-to-electrify sectors, helping secure a healthy and sustainable future for all New Yorkers,” Gov. Kathy Hochul said in a news release.

Proposals are sought in four areas:

hydrogen applications to decarbonize industrial process heat;

clean hydrogen production and integration with renewable energy such as solar and offshore wind;

mitigation of nitrogen oxides in hydrogen combustion; and

hydrogen storage technologies, including bulk storage and storage in limited footprint areas.

Applicants for state funding must be based in New York and must also be actively seeking federal funding for their projects. Any state award will be contingent upon the project also being approved for federal funding.

NYSERDA will host a webinar June 7 on the details and requirements. The application deadline is June 28.

STOWE, Vermont — New England must cut its natural gas use to meet the region’s decarbonization goals, panelists said at the New England Conference of Public Utilities Commissioners (NECPUC) 75th Symposium Tuesday. But there was no consensus on how fast the fuel should be phased out or whether its infrastructure should be repurposed.

The gas network is one of the largest sources of carbon pollution in the region. The Massachusetts Department of Environmental Protection estimates that natural gas accounts for nearly 40% of the state’s emissions from fuel combustion, an estimate that likely undercounts actual emissions by a significant margin because of unmonitored leaks from gas infrastructure.

Natural gas is used to heat about 51% of homes in the state and is also the largest source of electricity generation in New England, accounting for about 52% of the region’s generation.

“The natural gas infrastructure is viable and necessary,” said José Costa, the CEO of the Northeast Gas Association, which represents the region’s gas utilities. “We should push back on those that want to phase out the infrastructure.”

Costa said that he opposes efforts to ban gas hookups in new buildings, a movement that has been gaining steam in Massachusetts, which authorized 10 municipalities to implement gas bans for most new building construction during the state’s previous legislative session.

“You should have choice there,” Costa said.

Mackay Miller, a partner at consultant ERM and the former director of U.S. strategy at National Grid (NYSE:NGG), disagreed with Costa, saying that states with mandatory emissions reductions targets should ban new gas interconnections. “By 2030 approximately, there should be ratepayer protections in place; there should be exemptions for critical facilities and other potentially industrial commercial customers where there’s no comparable substitute service,” he said.

“Every country that is on track for net zero has taken this step already — the U.K., Netherlands — this would not be a huge deal.”

Costa acknowledged that natural gas use must decrease to meet decarbonization targets but argued that it could be replaced with alternative fuels such as renewable natural gas and hydrogen.

Priya Gandbhir, a senior attorney at the Conservation Law Foundation, pushed back on Costa’s characterization of those potential alternatives to natural gas, and said that decommissioning the bulk of the gas system makes the most sense for ratepayers and the environment.

“The evidence just isn’t there that these alternative fuels, hydrogen and biomethane, are up to snuff,” Gandbhir said. “In most circumstances, electrification is more efficient, more cost effective, safer, and more viable.”

Gandbhir said regulators should be “reviewing and prohibiting utility propaganda about the purported benefits of alternative fuels such as renewable natural gas and hydrogen.”

Mark LeBel, a senior associate at the Regulatory Assistance Project, said that accurately assessing emissions associated with the lifecycle of natural gas and alternative fuels will be an important step going forward.

“The leakage in the distribution system, in the transmission system, gas extraction — all that impacts the planet. So, I think at some point we’re going to have to wrestle with some of those questions that we’ve been putting off in some of our environmental regulations,” LeBel said. “When you burn the hydrogen, zero GHG emissions come from the point source. But the question is, where do you get the hydrogen from?”

Miller said that a focus on equity will be important in considering how to decarbonize the system while maintaining its safety, to ensure that cost burdens do not fall on low-income customers.

New England states that have pursued expedited pipeline replacement programs are facing a tension between the mounting costs of these programs and the risks that the infrastructure could become stranded assets as states move away from natural gas.

Miller said that regulators for states with newer, less leak-prone infrastructure “can probably accelerate depreciation or take some other fairly plain vanilla regulatory steps such that by the time you’re at relatively low demand, you’re still within the bounds of affordability.”

For states with older, deteriorating gas systems, he said that regulators are facing a larger task to maintain affordability.

“There you would likely need to be looking at ways to offer capital investment opportunities to utilities that are not going to build up rate base. You need to be looking at ways to bring in other sources of funding to handle the capital expenditure,” Miller said. “We’ve been hearing that there’s some interest at the Department of Energy in supporting some of these safety-related pipeline expenditures. That would provide an interesting opportunity for a bit of a safety release valve on ratepayer bill pressure.”