Federal regulators have completed their environmental analysis of plans for Empire Wind, finding potentially significant impact on the fishing industry and endorsing some changes to the 2.1-GW offshore wind farm proposal.

Publication of the EIS typically is one of the final steps in the review process. It’s the third EIS that BOEM has published in the past four months for a major offshore wind project; the previous two were followed five to six weeks later by records of decision approving construction and operation of Ocean Wind 1 and then Revolution Wind.

Empire Wind is a joint venture of Equinor and BP that would stand as close as 12 nautical miles south of New York and 17 nautical miles east of New Jersey. New York State has contracted with it to deliver 816 MW and 1,260 MW in Phase 1 and Phase 2, respectively.

Impact Statement

The details differ, but the final EIS announced Monday for Empire Wind reaches conclusions similar to EIS reviews prepared recently for other projects. They offer an often-wide range of possible outcomes for the criteria examined.

Empire Wind is expected to have minor to moderate beneficial effects on air quality and economics, for example.

It’s expected to have minor to moderate adverse effects on environmental justice communities and vessel navigation.

The effects on birds could be adverse or beneficial, or both.

The EIS also looks at the results of not building Empire Wind — the effects of climate change continuing unchecked as fossil fuels are burned to generate the electricity the offshore wind turbines otherwise would produce. In this no-action scenario, the adverse impacts on birds or people or fish often are projected to be of a similar magnitude even as the specific details are different.

But one thing is consistent in every EIS: the impact on the Northeast fishing industry.

BOEM forecasts Empire Wind will have a minor to major adverse effect on fishing, depending on the type of vessel and the species it’s harvesting.

Combined with the other 19 offshore wind farms that potentially could stand between Cape Cod and Cape May, the cumulative impact on commercial and for-hire recreational fishing is expected to be major.

For Empire Wind’s lease area OCS-A 0512, the greatest commercial impact is expected to be on the scallop fishery. Most of the area produced more than $4,000 worth of sea scallops per square kilometer per year from 2008 to 2018, and the harvest in a large swath exceeded $8,000 mean annual value.

Other major adverse impacts from Empire Wind are projected on the view from shore, search and rescue operations, and scientific surveys. Adverse effects on the critically endangered North Atlantic right whale could range from negligible to major.

Changes

Empire Wind 1 was proposed to have up to 57 turbines and Empire Wind 2 as many as 90. Their rotors would reach as high as 951 feet above sea level. They would be served by two offshore substations and up to 260 miles of inter-array cables. Up to 67 miles of export cable would run to landfall points in Brooklyn and farther east on Long Island.

However, after the draft environmental impact statement was published, Empire and BOEM conducted further analysis of glauconite soils in the lease area. Monopile foundations are so difficult to drive into glauconite that Empire concluded 40 of its potential turbine sites might not be viable. This cut the maximum number of turbines to 138.

Meanwhile, BOEM endorsed four changes to the routing and construction technique of the export and onshore cables.

BOEM has gathered these changes into a “preferred alternative”; it is the option the agency is leaning toward as it moves to its final Record of Decision.

Headwinds

Empire Wind is in line to be the fifth utility-scale offshore wind farm green-lighted in U.S. waters. The first two, Vineyard Wind and South Fork Wind, are under construction.

But Ocean, Revolution and Empire all have significant cost and supply challenges to overcome before they can start construction, as do other developers in the new U.S. offshore wind sector.

Equinor and BP have told New York they may not be able to proceed with Empire without substantially more money than was agreed upon.

Ørsted is seeking more money for Ocean and Revolution before it makes a final investment decision and has pushed the completion date for Ocean back a year.

Developers of two of Massachusetts’ three contracted offshore wind facilities are paying $100 million in penalties to back out of their power purchase agreements in hopes of bidding back into the Bay State’s latest solicitation at higher costs.

Earlier this summer, Orsted’s proposal for Revolution Wind 2 was rejected as too expensive in Rhode Island. And New York has invited bidders in its latest offshore solicitation to resubmit bids with lower price tags.

DFW AIRPORT, Texas — Keeping the lights on has long been a simple proposition for grid operators. Look at historical demand, add in growth expectations and ensure you have enough generation available to meet that demand.

No more. With older thermal plants retiring or breaking down and being replaced by a flood of more variable renewable resources, grid operators need a more comprehensive focus to ensure they have enough capacity and reserves to keep the system in balance.

SPP last week invited federal and state regulators, academics, market participants and other stakeholders to its inaugural Resource Adequacy Summit. There, they discussed the events that have led the industry to this juncture and the actions necessary to improve the grid’s reliability in the face of enormous change.

“This is the first opportunity we’ve really had to kind of open up a stakeholder, customer and just simply interested party dialogue on a very important topic,” SPP COO Lanny Nickell said in kicking off the Thursday summit.

FERC Commissioner Mark Christie likened the current state to that of the Great Depression, when President Franklin D. Roosevelt said the country was facing a rendezvous with destiny.

“We’re at a very critical time … reliability means, ‘Are the lights going to stay on?’ That’s what it means to the general public,” Christie said. “Are the lights going to stay on? We’re really at a point where that’s coming into serious question. Are the lights going to stay on?

“Right now, when it comes to the reliability of our grid, the United States is facing a rendezvous with reality. Reality is just around the corner. You may think you can avoid it for a while, but reality will track you down. And reality is tracking us down when it comes to the reliability of our grid,” he added.

Testifying before the Senate’s Energy and Natural Resources Committee in May, Christie told lawmakers the grid is facing “potentially catastrophic consequences.” He said he was not trying to be melodramatic. (See Senators Praise Phillips, FERC’s Output at Oversight Hearing.)

“We were not trying to get a sound bite out there into the media. I used the term ‘catastrophic’ because when we have multiple-day outages … that’s catastrophic by any definition. People die if it’s a cold-weather outage, and so that is catastrophic.”

The core reason, Christie said, is not necessarily the vast amount of wind and solar generation that is being added to the grid. It’s the subtraction of coal, gas and other dispatchable thermal resources at a pace that is unsustainable, he said.

“The first rule of holes is if you’re in one, stop digging,” he said. “If the fundamental problem we’re facing is we’re shutting down dispatchable resources far too prematurely, then the answer is to stop shutting down dispatchable resources far too prematurely.”

Christie brought receipts with him. He said PJM forecasts the loss of 40 GW of mostly dispatchable capacity by 2030. He said MISO expects to be 9 GW short by 2028. He noted an earlier presentation from Nickell saying SPP has installed 24 GW of wind and solar in recent years but has lost 8 GW of dispatchable resources.

“And by the way, that is before the EPA came out with the power plant rule, which is going to make that number even worse, as every RTO knows,” Christie said. “The numbers don’t add up. You lose 8 gigs of dispatchable and you pick up 24 gigs of wind and solar, [you think] you’re fine right now. You’re not fine, because as we all know, a megawatt of nameplate wind and solar is not equal to a megawatt of nameplate coal or gas. It’s just reality.”

“There’s really no reason why we should be retiring perfectly good resources in this country,” said Zachary Ming, a director with San Francisco-based consulting firm Energy and Environmental Economics (the folks behind ERCOT’s market redesign).

“We should be focusing on building as many new resources, primarily renewables and storage, and keeping the firm dispatchable resources online that we have. That is both going to maximize affordability, and it’s going to maximize environmental benefits as well,” Ming said. “You reduce emissions by building renewable resources that come first in the dispatch order and will dispatch ahead of dispatchable resources. All building renewables will do is allow us to use the dispatchable resources less, but renewables have limited contributions to reliability. So, it doesn’t mean we can retire the resources. It just means that we can use them less. They will have less emissions, and they will have environmental benefits, and they’ll still stay there for reliability.”

“We’re facing reality very, very simply. I think everybody knows that,” Christie said. “The question is, is there going to be the political will to make a turn in policy and recognize that we’re not going to get to where everybody wants to get, which is a lower-carbon grid, without reality being part of the equation, because reality will track you down. We’re headed to some bad outcomes and none of us want to be around when those outcomes hit, because that’s when the finger-pointing starts.”

Sitting next to Christie, NERC CEO Jim Robb said the industry’s ability to conduct resource planning with a “highly variable intermittent generating system” will define the industry’s next 10 to 15 years.

“That’s the challenge that’s in front of us, and it’s not our grandfathers’ resource adequacy problem,” he said, noting NERC would like to hold an event similar to SPP’s. “I think we have to recognize that we take constructs that we all grew up with and we’ve been trying to modify them to adapt to a system that’s just fundamentally very, very different than what we grew up with. Whatever [resource adequacy] construct you look at is a very important number, but it’s no longer close to being a sufficient number for planning and operating the system.”

Robb pointed out that the traditional resource adequacy constructs are based on meeting demand during peak hours with enough of a margin to account for the “random independent equipment failures.”

“That doesn’t work anymore,” he said, pointing to what he called “common conditional failures” of the emerging generation fleet that is flush with renewables.

“A wind drought, solar drought, cloud cover, unexpected cloud cover, extreme cold weather affects the ability of large amounts of generation to operate, so this whole notion of kind of random failure being the driver of how much generation we need isn’t sufficient,” Robb said.

Policymakers need to “come to grips” with three questions, he said: how frequently they can tolerate loss-of-load events, how long an event are they willing to tolerate and how much are they willing to pay to prevent them.

“We know we can’t afford a 100% reliable system,” he said. “We’re going to have to make important tradeoffs between reliability and those three parameters [frequency, duration and scale] and how much we will be paid to avoid that. Resilience and reliability is not free.”

Robb said he’s encouraged by recent research into what customers are willing to pay to avoid multiday outages. He said those numbers are “much, much higher” than what he’s seen in the past.

“We’ve taken away the obligation to serve, and in these market areas, we rely on commercial constructs to try to recreate that,” he said. “It’s an imperfect substitute, but we have to figure out how to get the market rules to reward reliability with investments that aren’t going to be naturally paid for during the 98% of the normal periods.”

SPP is taking those steps with several recent changes. It increased its planning reserve margin from 12% to 15% last year and made several tariff changes for load-responsible entities’ deficiency payments and a payment structure based on a sufficiency valuation cure.

Buddy Hasten, CEO of Arkansas Electric Cooperative Corp., one of SPP’s LREs, called for fairness in meeting reliability commitments.

“We’re propping up reliability, but we get paid nothing for it,” he said. “When the wind blows hard enough or the sun shines bright enough, we have to pay the market to just keep our resources online to prop up the market to be there for reliability. So when [prices] go negative, I’m paying to keep that resource online.

“We like to play games. You create the rules of the game, and everyone plays it, and it’s all about who can get the lowest cost because we’ve turned electricity into a commodity instead of an essential service,” Hasten added. “At some point, there has to be a financial metric rule, some payments, something somewhere to pay for that reliability. Otherwise, everyone’s going to keep playing the game and just chasing the cheapest electron.”

A nuclear submariner for 20 years, Hasten said he’s very aware of the importance of resource adequacy.

“If you don’t have enough resources, you go to the bottom of the ocean,” he said. “Resource adequacy is life or death. I’d hate to be the person that go to those folks’ home and says, ‘Hey, I’m sorry, you froze to death.’ … 2021 was the first time we sent linemen out and white bucket trucks to go open breakers and put people on the dark. That’s called progress, I guess.”

Several speakers pointed out the role natural gas played during that winter storm. Gas plants without firm fuel contracts — and some with firm contracts — were unable to get those supplies as heating homes took precedent. Other thermal generators simply weren’t prepared for the extreme winter conditions.

Aubrey Johnson, MISO’s vice president of system planning and competitive transmission, said aging plants in the RTO’s fleet also played a role in the 2021 and 2022 winter storms.

“It’s actually a fleet that’s not responsive when you actually need it,” said Johnson, who has a background in power plants. “Working with Southern Co., we used to have real competition about how you showed up during peak season and how well your plants performed. When I look at some of the performance numbers today, I’m kind of shocked. You would spend a lot of time in the principal’s office with those kinds of performance numbers.

“The No. 1 way to ensure resource adequacy is ensuring you have adequate resources,” he added.

Given a chance to provide suggestions to the audience during a lightning Q&A round, Johnson’s message was simple.

Apple put its considerable heft behind a California bill that will, if passed, increase the emissions reporting requirements for more than 5,000 large companies that do business in the state.

In a move lauded by the bill’s author, Apple, the $2.8 trillion behemoth, came out in support of The Climate Corporate Data Accountability Act (SB 253). The bill was approved Monday in the state Assembly and now goes to the state Senate.

The proposed legislation would require corporations with total annual revenue greater than $1 billion that do business in California to report the prior year’s Scope 1 and Scope 2 emissions by a date yet to be determined in 2026 and Scope 3 in 2027, with annual reports thereafter. Scope 1, 2 and 3 emissions are used globally to define the different types of greenhouse gas emissions of companies:

Scope 1 emissions are direct greenhouse gases emitted by a company, for example from running boilers, burning fuel in a manufacturing process or powering non-electric vehicles;

Scope 2 emissions are indirect emissions from electricity, steam, heating or cooling purchased by the company for uses ranging from lighting to charging electric vehicles;

Scope 3 emissions are indirect and related to a company’s supply chain, both its inputs through to the end use and eventual disposal of the goods. These emissions may include goods and services a company buys, employees’ commuting and work travel, emissions from transporting and distributing a product to consumers and final use and disposal of the product. This is not only the largest category of emissions but also the hardest to measure.

State Sen. Scott Weiner (D–San Francisco) on Friday posted a message on X (formerly Twitter) about Apple’s move: “Huge new endorsement — @Apple — of our groundbreaking climate bill to require large corporations to disclose their carbon footprint (SB 253). Thank you, Apple, for making clear that this is doable & a critically important piece of climate action.”

The endorsement of the bill came in a letter to Weiner which stated, in part:

“We’re strongly supportive of climate disclosures to improve transparency and drive progress in the fight against climate change, and we’re grateful for your leadership to drive comprehensive emissions disclosure.”

Apple’s support comes more than two weeks after a group of companies including Microsoft, Adobe, IKEA USA and Atlassian issued a joint statement in support of SB 253 that said “California is on track to be the fourth-largest economy in the world and this bill would set a global standard for emissions disclosure. SB 253 would level the playing field by ensuring that all major public and private companies disclose their full emissions inventory, creating a pathway for collective reduction strategies.”

By requiring Scope 3 emissions reporting, SB 253 exceeds the proposed Securities and Exchange Commission (SEC) rule, which largely lets companies out of reporting them unless they already have a stated target for reducing them or if they are material, that is, if a “reasonable investor” would be “substantially likely” to consider them important when making an investment or voting decision.

This is not Weiner’s first attempt at passing the bill: SB 253 failed to pass by one vote in 2022, but has been amended to delay Scope 3 emissions reporting by a year, aligning the bill with the International Sustainability Standards Board’s IFRS S2 Climate-related Disclosures standard issued in June 2023.

Corporate Support is Far from Unanimous

In August, a policy advocate specializing in energy issues at the California Chamber of Commerce, Brady Van Engelen, critiqued the bill, calling for legislators “to reject an onerous emissions tracking and paperwork requirement that will increase costs on California businesses.”

Much of CalChamber’s concern centers on the use of secondary data or industry averages for calculating Scope 3 emissions.

“Secondary data is inherently flawed and unreliable, nor does it paint an accurate picture. This flawed method of calculating Scope 3 emissions means that virtually every reporting entity could be subject to a violation,” Van Engelen said in his August 23 post.

CalChamber, along with many other companies and associations including the Western States Petroleum Association, the California Retailers Association and the California Manufacturers and Technology Association, issued a joint statement opposing the bill, which stated in part: “At this juncture, Scope 3 emissions reporting is more of an art than it is a science. Due to the likelihood of double counting, assessing Scope 3 emissions data with any degree of accuracy is not yet possible.”

The letter from Apple directly addressed the challenge of Scope 3 emissions reporting, highlighting its own efforts: “We acknowledge that there is inherent uncertainty in modeling carbon emissions, primarily due to data limitations. Scope 3 emissions, in particular, involve making educated assumptions and complex modeling. We believe, however, that our reports attest to the feasibility of reasonably modeling, measuring and reporting on all three scopes of emissions, including scope 3 emissions, which represent the overwhelming majority of most companies’ carbon footprint and are therefore critical to include.”

The bill is not the only proposed climate-related legislation being considered in California. Senate Bill 261, the Climate-Related Financial Risk Act (SB 261), would require companies with greater than $500 million in revenue to report on “material risk of harm to immediate and long-term financial outcomes due to physical and transition risks,” by the beginning of 2026 and biennially thereafter. Assembly Bill 1305, the Voluntary Carbon Market Disclosures Act (AB 1305), requires much more detailed disclosures on the websites of companies marketing or selling voluntary carbon offsets within the state.

Installed small-scale solar capacity increased by an estimated 6.4 GW in 2022 — a record amount, even amid supply chain constraints and rising costs.

The Energy Information Administration highlighted the data Monday and said small-scale solar nationwide totaled 39.5 GW by the end of 2022 — about a third of U.S. installed solar capacity.

EIA defines small-scale or distributed solar as systems with up to 1 MW nameplate capacity. But most small-scale solar is much smaller than 1 MW — rooftop residential installations account for most small-scale capacity.

When EIA began its annual estimates of the subsector in 2014, it placed the installed capacity at just 7.3 GW. Since then, falling solar panel costs, government incentives, policy changes and rising retail electric costs have helped accelerate the buildout.

California, with its abundant sunshine and statutory requirement that new residential buildings be equipped with solar panels, accounted for 36% of installed capacity nationwide, by far the most of any state.

But Hawaii, which has historically relied on expensive imported fuel to power its electric generation, has by far the greatest market penetration: 541 watts of installed solar capacity per capita. California is second, at 364 watts.

Other top states for installed small-scale solar capacity include New York, New Jersey and Massachusetts. None of the three have optimal amounts of sunshine, but all have strong and long-standing policies that encourage installation.

New York is No. 2 in the nation, at 2.6 GW, and New Jersey is third, at 2.4 GW.

Sun Belt states Texas (2.2 GW) and Arizona (2.1 GW) are catching up, however, and have surpassed Massachusetts (2.0 GW).

Sunny Florida is close behind, at 1.9 GW. Every other state is estimated to have 1 GW or less of small-scale solar generation installed on homes, businesses and industrial sites.

MISO said it will seek approval from its board of directors for 578 transmission projects totaling $9.4 billion in December.

The RTO’s 2023 Transmission Expansion Plan (MTEP 23) makes for MISO’s largest-ever annual planning cycle and includes a substitution for two MISO South reliability projects. That’s according to MISO’s final round of subregional planning meetings for the year Sept. 5-8.

MISO South transmission owners plan to build 76 new projects at $4.3 billion, most of them to meet their own reliability planning criteria or NERC’s reliability standards. The dramatic jump in proposed spending led some stakeholders this year to allege Entergy was circumventing more comprehensive and cost-shared regional projects. (See Initial MTEP 23 Ignites Familiar Arguments over MISO South’s Reliability Spending.)

By comparison, MTEP 22 yielded a total $4.3 billion investment package. MISO’s first long-range transmission plan (LRTP) portfolio approved last year — considered separate from the annual MTEP planning — produced a $10 billion investment.

MISO this year tested alternative designs for 11 proposed projects that represented 40% of MTEP 23 spending. Planning staff previously said multiple MISO South reliability projects, particularly substation work, might benefit from substitute projects. (See MISO Weighs MTEP 23 Alternatives to South Reliability Projects.)

Now, MISO said it’s pursuing an alternative for the first phase of the three-part, nearly $2 billion Amite South line and substation work in Entergy Louisiana’s southern territory. MISO said its selected alternative, the 500-kV Commodore-Waterford-Churchill loop project, will tie the area’s 230- and 500-kV systems together at three points instead of two and better equip the system for future load growth in both the Amite South and Downstream of Gypsy load pockets in Louisiana. The extended 500-kV line will negate the need for another MTEP 23 project proposed by Entergy Louisiana, the 27-mile, 230-kV Downstream of Gypsy reliability project.

The project alternative is pricier than the original two projects combined, at $1.7 billion instead of the originally proposed $1.4 billion for Amite South Phase 1 and the $164 million for the Downstream of Gypsy project. The project involves building a new 500/230-kV substation; stringing a new 60-mile, 230-kV line and a new 85-mile, 500-kV line; upgrading an existing substation; and upgrading an existing nearby 230-kV line to 500 kV.

“So, we chose one project alternative to replace two proposed projects,” Manager of MISO South Expansion Planning Trevor Armstrong said during a Sept. 6 South Subregional Planning Meeting. “The alternative is more expensive, but it provided more load-serving opportunity for growth.”

Entergy expects 2 GW of new load across the Amite South load pocket soon.

MISO also said the larger project will improve system resilience when extreme events strike and will address coming generation retirements in Amite South by allowing the option to cut multiple sources into existing stations.

The project still will have a 100% local allocation to load. MISO South’s first regionally cost-shared, market efficiency project remains elusive.

Southern Renewable Energy Association’s Andy Kowalczyk asked if Entergy pitched the idea for the substitution.

Armstrong said the design was on Entergy’s list of alternative project suggestions, but it resembled a project idea MISO independently devised. He said the alternative ultimately was developed in conjunction with Entergy.

“This was the only one we felt needed to be selected in place of the original projects,” Armstrong said.

Kowalczyk asked whether MISO planners will develop load growth projections for its planning modeling. MISO was forced to perform a separate sensitivity outside of its usual modeling to test for alternatives because it doesn’t account for forward-looking load additions and generation retirements in modeling.

“I think they’re credible inputs that need to be considered. I think it’ll be a bit of a shock every year to have projects this size, and you have to perform a separate sensitivity,” Kowalczyk said. “Maybe we’re not accounting for future needs in the most cost-efficient way.”

MISO planners said they don’t have definite plans to include load growth estimates in planning modeling.

Armstrong said the majority of the South region’s MTEP 23 projects will be placed into service within the next three years.

Armstrong added that MISO still is working to develop possible alternatives to the third phase of Entergy Louisiana’s Amite South reliability project. He said MISO likely will delay project approval into 2024; MISO planners said they didn’t know whether the project will be included as a late addition to MTEP 23 or be deferred into the 2024 planning cycle.

However, MISO left standing the controversial $1.1 billion, 150-mile 500-kV line and substation project Entergy proposed for Southeast Texas. Planners said they couldn’t find a better alternative in terms of economics or reliability to the baseline reliability project consisting of a 150-mile, 500-kV line, 500-kV substation and 500-230-138-kV substation.

Entergy said the Southeast Texas project will help meet its local planning criteria, reduce dependence on aging and increasingly unavailable resources, and be useful when restoring the grid from extremes wrought by winter storms and hurricanes.

During the Planning Advisory Committee last week, MISO Director of Cost Allocation Jeremiah Doner said load growth and reliability issues are driving the need for more transmission investment.

Because of the size of this year’s MTEP, MISO will add another meeting of the System Planning Committee of the Board of Directors in mid-October to give MISO board members more time to understand the package’s contents.

Sustainable FERC Project’s Natalie McIntire asked MISO to revisit its definition of “other” projects because most of the spending is classed under the category this year. MISO’s other project category includes reliability projects based on TOs’ self-imposed criteria separate from NERC standards, projects needed for load growth and projects to address the age and condition of existing facilities. Other projects have become the lion’s share of MTEP spending since the 2018 cycle.

MISO is accepting stakeholder suggestions and considering what additional planning studies it may undertake as part of MTEP 24. However, planning staff warned that MISO is limited next year in what it can accomplish because it’s performing extensive analysis under its ongoing LRTP.

MISO will hold stakeholder workshops on the nascent, second LRTP portfolio again Dec. 1 and at the end of January.

MISO: Expedited Review Process Needs Revamp

Lastly, MISO said the MTEP 23 planning cycle has made it clear it should rethink its expedited project review process for projects that can’t wait until the usual December MTEP approval to begin construction. MISO said it fielded more than 30 expedited project review requests — double the number it received in 2022 — predominantly because of new load interconnections.

Armstrong said some expedited requests were “simple, while others have become quite complex.” He said MISO planning staff is struggling to complete on-time studies on the out-of-cycle requests. MISO likely will need to overhaul its expedited processing to make the ever-increasing analyses manageable, he said.

“We have seen some ones that cause harm to the system and require some back and forth. At this volume, it’s not sustainable,” Senior Manager of Expansion Planning Amanda Schiro added during a Sept. 8 East Subregional Planning Meeting.

Schiro told stakeholders MISO staff is discussing internally how to best modify its process and said stakeholders should expect a proposal in coming months.

The U.S. Southeast may have grabbed a major share of private investment in electric vehicle and battery manufacturing, but it is well behind the rest of the country in EVs actually on the road, according to a new report from the Southern Alliance for Clean Energy (SACE).

Based on announcements through the first half of the year, the region ― which includes Alabama, Florida, Georgia, Mississippi, the Carolinas and Tennessee ― accounts for 40% of all new investments in EV-related manufacturing and 35% of the jobs those projects will create, according to the report, compiled by Atlas Public Policy.

Yet, light-duty EV sales in the Southeast lie well below the national average, which is now inching up toward 10% of all new vehicle sales. Figures for the Southeast range from EVs accounting for 7% of new car sales in Florida and Georgia, down to about 2.5% in Alabama.

But that seemingly upside-down market could turn out to be a plus for transportation electrification in the region in the long term, said Stan Cross, SACE’s electric transportation program director.

“There are some states and some regions that are electrifying transportation motivated by and driven by policy: clean energy policy; climate policy,” Cross said during a launch webinar for the report on Thursday. In the Southeast, “it’s really an economic development mechanism that’s driving the market,” which could produce a slower but more deeply rooted transition, he said.

“If we start to see more charging stations, more EVs owned, more equitable accessibility across the region because those products are being made here and because those companies that are moving here are beginning to amass political sway, then that could potentially be a much more durable transition over time,” Cross said.

The Southeast could also be a strong market for the U.S. and foreign automakers seeking to challenge Tesla’s tight hold on 50% of new vehicle sales, he said. The automakers locating or expanding their manufacturing plants in the region “are a lot of those legacy automakers. It’s Honda; it’s Volkswagen; it’s Volvo, GM [and] Ford,” Cross said. “As those carmakers really step up their EV game, there’s a lot of additional opportunity [for sales] here in the Southeast … because those are the brands that consumers already trust, already have an affinity for.”

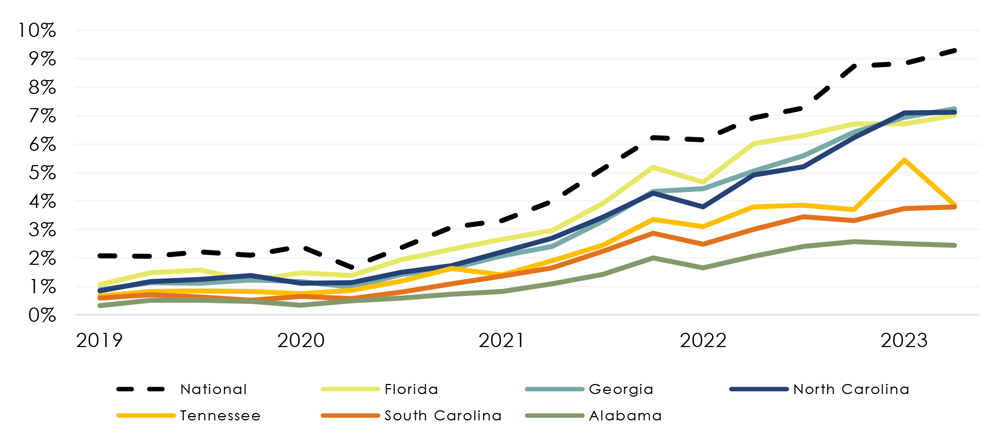

EV market shares in the Southeast lag behind the national average. | Atlas Public Policy/SACE

Ripe for EV Adoption

Another reason the region could be ripe for EV adoption is that relatively little fossil fuel production or refining is located there, Cross said.

“The Southeast doesn’t have any skin in the oil game,” he said. “As a result, when consumers go to the gas pump to fill up their cars … only about 23 cents of every dollar spent at the pump stays in the Southeast.”

With EVs, however, “about 71 cents of every dollar spent on locally generated electricity stays in the Southeast,” Cross said. SACE estimates that if all cars, trucks and other vehicles across the Southeast were electrified, “the region would get a $60 billion boost to the economy annually.”

While behind national figures, EV sales in the region are growing, from a cumulative total of 312,316 in the second quarter of 2022 to 469,602 this year, a 50.4% increase year over year, the report says.

Other topline figures in the report reflect the push-pull of policy and economic development in the Southeast’s EV market. Georgia leads the region in investments and jobs announced. Rivian is putting up $5 billion for a plant that could turn out 400,000 EVs per year and create up to 7,500 jobs. Hyundai is working on two EV battery plants in the state, one with LG Energy Solutions and one with SK On, with a total investment of $8.3 billion, creating up to 6,500 jobs.

But job creation is uneven across the region ― and still speculative, based on the estimates companies have announced. SACE is tracking announcements for 65,242 EV manufacturing jobs in the Southeast. Georgia leads with 27,817 potential jobs announced versus a scant 314 in Florida.

Three-quarters of all public funding for transportation electrification in the Southeast is going toward school bus and public transit electrification, with just under a quarter going toward charger deployment. The Southeast averages $3.84 per capita in public spending on vehicle electrification, well below the national average of $13.81.

A Slow Energy Transition

Transportation electrification in the Southeast is following a similar pattern as the region’s adoption of renewable energy has been bottom-line and market driven and, to a great extent, utility controlled. Southern investor-owned utilities held off on committing to clean energy until the cost per kilowatt-hour for solar or wind was competitive with or below the cost of fossil fuels and could be included in their rate base.

IOUs have also been a major force in slowing the development of residential rooftop markets in some states in the Southeast. For example, the North Carolina Utilities Commission recently approved a proposal from Duke Energy to establish a minimum monthly bill for residential rooftop solar owners and slash compensation to solar customers for the excess power they put on the grid.

For the EV market, IOUs are “crucial enablers of transportation electrification by being the primary supplier of energy, managing the electrical grid and investing in all or parts of electrical infrastructure that serves EV charging,” the report says.

But here, again, the Southeast lags behind the rest of the nation. Through June 2023, IOUs across the U.S. received regulatory approvals for $5.8 billion in transportation electrification investments, with approvals pending for another $1.5 billion, the SACE report says.

Approved investments in the Southeast came in at $394 million, or 7% of the national total. Only $6 million of that figure was approved for programs targeting deployment of EV chargers in low-income or other underserved communities, well below the national average.

Investments approved in individual states also varied widely. Florida IOUs are at the top of the list, putting $278.2 million into EV infrastructure, and South Carolina is at the bottom, with $8.8 million.

Florida also leads the region in charging ports deployed, with 1,843 DC fast chargers and 6,080 Level 2 chargers.

To date, most Southeast states have used money from the 2016 Volkswagen settlement ― paid after the automaker admitted to cheating on figures for vehicle emissions ― as a source of public funding for EV chargers, the report says. But SACE sees a major opportunity for EV charger deployment in the $680 million in federal funds that the region is slated to receive from the National Electric Vehicle Infrastructure (NEVI) program, established by the Infrastructure Investment and Jobs Act.

The NEVI funds are initially targeted at putting DCFCs every 50 miles on interstate and major state highways.

The Policy Landscape

EV market growth faces other obstacles in the Southeast in the form of state policies that make it harder and more expensive for consumers to buy and own EVs.

Additional registration fees for EVs ― intended to compensate states for lost gasoline taxes used to maintain highways ― are now in effect in 32 states, according to a recent analysis in Money. But Georgia and Alabama have the second and third highest in the nation, $211 and $203, respectively, behind Washington state, which charges $225.

The regional average for such fees in the Southeast is $161 versus a national average of $126, according to SACE.

Cross sees the problem not as one caused by EVs, but rather by a gas tax system that itself is breaking down as all vehicles become more fuel efficient. “Many states are looking at how to transition from a gas tax to a tax on vehicle miles traveled as a way to deal with this issue, which is only going to get worse, regardless of whether electric vehicles are purchased or not,” he said in a separate interview with NetZero Insider.

The Southeast has a mixed record on laws that limit or prohibit the direct sales and servicing of EVs, another critical issue for EV market growth across the country. At issue is the sales model used by Tesla and other new EV manufacturers, selling directly to consumers, versus the legacy model of auto sales through dealerships, which is codified in law.

Florida, Mississippi and Tennessee allow direct sales; Alabama and South Carolina do not, while Georgia and North Carolina limit direct sales to one automaker, Tesla.

As with gas taxes, Cross sees attempts to limit direct sales as a counterproductive response to fundamental changes in the market ― in this case, the evolving business models and trends in consumer choice and buying habits. Direct sales are not a threat to the longstanding relations between automakers and dealerships, he said.

“Nobody’s arguing that [legacy dealerships] should not be respected,” he said. But for EV companies “to stand up nationwide dealerships is ridiculous. It’s not financially feasible, and it’s not what consumers want. … I mean, it’s difficult to find any other commodity that we purchase the same way we purchased [it] 50 years ago.”

The Virginia State Corporation Commission on Friday approved Appalachian Power Co.’s 2023 Renewable Energy Portfolio Standard development plan.

The plan has the American Electric Power subsidiary entering into six new power purchase agreements for 184 MW of solar, renegotiating another solar PPA worth 20 MW, and approves its purchase of the Grover Hill wind farm in Ohio at 146.2 MW.

The commission rejected Appalachian’s request for cost recovery associated with a legacy wind project built more than a decade ago, finding it did not lead to positive value for customers.

The SCC approved a revenue requirement for the renewable purchases, required under the Virginia Clean Economy Act (VCEA), of $16.37 million for the rate year of October 2023 through September 2024.

“The commission … is guided in these matters by the statutes and the record,” the SCC’s order said. “The commission has continued to exercise its delegated discretion in a manner that faithfully implements the VCEA’s carbon-reduction requirements, while best protecting consumers who expect and deserve reliable and affordable service.”

Appalachian’s territory is in the southwest of the state, while most of the rest is served by Dominion Energy. Its larger neighbor weighed in on the proceeding in favor of removing the load of customers who sign up voluntarily for 100% renewable energy to cover their demand, an idea the AEP subsidiary agreed with.

SCC’s senior hearing examiner asked for different treatment of such customers, which instead would count their renewable credits toward Appalachian’s RPS compliance.

The SCC itself was unable to decide on the issue, which would both cover customers taking service under the two utilities’ renewable tariffs and large “shopping” customers who get 100% renewable energy.

SCC directed the two utilities to make either a joint filing, or file separately, in a new docket addressing those issues and presenting specific proposals. The filing would need to include a proposed mechanism for netting the benefits of such renewable energy credits.

Appalachian wanted to recover some of the costs of its power purchase agreement with the Beechwood 100-MW wind farm in West Virginia, which it entered back in 2010, despite the SCC previously rejecting a similar request.

The Beech Ridge PPA would have inflated the cost of the total RPS package by $4.5 million on the year. The utility tried to get the deal approved under what was at the time a voluntary renewable portfolio standard, the state attorney general said in a filing from last month. It was rejected as too costly by regulators.

The company argued new wind projects have been more difficult to build lately, and the project does produce renewable energy, which is a requirement under Virginia law., However, nothing in the statute requires the purchase of renewable energy that would be a net negative for consumers, said the attorney general’s office.

“The record reflects in this case, among other things, the Beech Ridge PPA fails to produce a positive NPV under any of the analyses presented in this case,” the commission said in explaining its rejection of that request.

A southeast Washington economic development organization plans to set up a nonprofit subsidiary to help develop clean energy businesses in a region with deep ties to nuclear power.

Details of the plan by the Tri-City Development Council (TRIDEC) still must be worked out, according to the Karl Dye, the group’s CEO.

Washington’s Tri-Cities area consists of the cities of Richland, Pasco and Kennewick, located near the Hanford Nuclear Reservation and Energy Northwest’s Columbia Generating Station nuclear reactor. Richland also is home to the Pacific Northwest National Laboratory. All these have made the area a major science and engineering center.

The nonprofit TRIDEC announced recently it will create a nonprofit subsidiary called the Energy Forward Alliance to push the development of clean energy technologies. TRIDEC has not yet developed a timetable for getting the venture fully functional or determining its specific goals, Dye told NetZero Insider.

“The goal is to find the right leader and have that leader be part of the planning process,” Dye said. TRIDEC hopes to hire a leader and set up a board of directors this year, he said.

The effort is separate from a U.S. Department of Energy initiative to attract clean energy companies to establish a presence in unused parts of southern Hanford adjacent to Richland. That effort will be discussed with potentially interested businesses Sept. 22 in Richland.

Starting in 2024, consumers buying an electric vehicle that qualifies for a $7,500 tax credit under the Inflation Reduction Act (IRA) will be able to transfer that credit directly to the dealer selling them the EV.

“This will effectively lower the vehicle purchase price by providing customers with an upside-down payment on their vehicle at the point of sale that equals the value of the credit instead of having to wait to claim that credit on their tax return next year,” said Lily Batchelder, assistant secretary for tax policy at the U.S. Department of the Treasury.

Speaking during a Thursday press call, Batchelder said the Internal Revenue Service will launch an online portal in January that will allow dealers “to submit clean vehicle sales information to the IRS and promptly receive payments for the transfer credits.”

Batchelder and Deputy Secretary of the Treasury Wally Adeyemo were on the call to preview what the Treasury Department is calling Phase 2 of its implementation of the IRA’s clean energy tax credits and the specific guidance that the agency will release this fall.

During the past year, since passage of the IRA, Treasury’s focus was “on the core elements needed to accelerate the significant economic and climate benefits of the law,” Adeyemo said. In addition, “Treasury prioritized guidance on all the bonus provisions to ensure companies and other entities planning projects were able to pencil out new projects and secure financing across a wide range of technologies,” he said.

The focus in Phase 2 will be “boosting America’s manufacturing to create good-paying jobs and strengthening our security, to remove choke points that will hurt our ability to lower costs and meet our economic and climate goals,” he said.

Taking a victory lap for the billions in private investment the law has unleashed, Adeyemo noted that “companies have announced more than 200 new projects, totaling more than $110 billion in investment in building America’s clean energy economy.”

A Treasury Department analysis released last month found that “investments [in] electric vehicles and batteries are concentrated in communities with lower wages, lower college graduation rates and lower employment rates. The law is working as intended,” he said.

Clarity on Content

But the past year also has been a bumpy one for Treasury and the IRS as they rolled out successive guidelines for the IRA’s many tax credits. The law’s domestic content provisions — for EVs and other clean energy equipment — have been an ongoing flashpoint.

Sen. Joe Manchin (D-W.Va.), a key architect of the IRA, has been a constant critic, arguing that Treasury has not followed the letter of the law on domestic content, which was intended to boost the domestic supply chain for EVs and EV batteries, but instead has benefited foreign automakers. (See IRA’s EV Tax Credits Spark Senate Debate.)

The solar industry also has said qualifying solar panels for the domestic content credits has been more complicated than expected. “Without full clarity on qualifications and processes, developers, manufacturers and financiers are often left in limbo,” said Michelle Davis, head of global solar for industry analyst Wood Mackenzie, in a third-quarter market report released Thursday,

“As a result, the full benefits of the IRA, in the form of more development of solar projects that meet various policy objectives, won’t manifest until developers, asset owners and financiers have enough regulatory clarity to make confident investments,” Davis said.

Batchelder acknowledged more work is ahead on the domestic content provisions, as part of the agency’s work on all the clean energy tax credits expanded or created by the IRA.

Treasury’s priorities for guidance to be released in the coming months include:

The Section 45X advanced manufacturing tax credits aimed at incentivizing production of clean energy equipment, from solar panels and wind turbine blades to inverters and batteries, to be issued by the end of the year.

New energy efficient home credits, which will incentivize home builders to use the most up-to-date efficiency standards in their new construction.

Tax credits for clean hydrogen and sustainable aviation fuel, with initial guidance coming again by the end of the year.

The Bottom Line

A key question ahead for Treasury and the Biden administration is just how much the IRA tax credits will cost. Although originally estimated at $370 billion, a recent update from the Congressional Budget Office added about $180 billion to the law’s bottom line, according to a New York Timesreport.

Batchelder noted Treasury set aside at least $1.6 billion for 48C tax credits for clean energy projects in “energy communities” with closed coal plants but, so far, the Department of Energy has received concept papers from potential applicants seeking a total of $11 billion in tax credits.

Responding to a reporter’s question, a Treasury official said while the IRA was a historic investment in clean energy, China continues to invest about five times as much into its energy system, and the entrepreneurs and businesses getting money from the IRA are putting their dollars into the U.S. economy.

Supplies of coal and natural gas are likely to be less of a concern for the North American electric grid this winter, according to a member of the team developing NERC’s 2023-2024 Winter Reliability Assessment (WRA).

Stephen Coterillo, NERC | NERC

Speaking at the ERO’s Preparation for Severe Cold Weather webinar on Thursday, Stephen Coterillo, an engineer with NERC’s Reliability Assessment department, previewed findings from this year’s WRA. The team has been working on the report since July.

NERC’s WRAs cover the months of December through February and typically are based on demand and generation availability forecasts provided by regional entities, utilities and other stakeholders. This year’s assessment also will include information gathered as part of the ERO’s first-ever Level 3 alert, which was issued this year after NERC’s Board of Directors approved it at its meeting in May. (See “ERO to Issue First Level 3 Alert May 15,” NERC Board of Trustees/MRC Briefs: May 10-11, 2023.)

Coterillo cautioned the team has not finished processing the data, but he told webinar attendees he could share some preliminary findings. These include the rising stockpiles of coal, which are “trending toward an adequate level,” and natural gas storage levels, which are above the five-year average for this point in the year. According to data from the Energy Information Administration, natural gas underground storage in the lower 48 states was more than 3,000 Bcf, higher than any year since 2017 except for 2019.

“This is definitely a welcome change from prior years, where supply chain issues, coupled with global supply concerns, caused lower inventory levels of stored coal and natural gas headed into the winter season,” Coterillo said.

However, while the fuel levels are a welcome sign for the ERO overall, Coterillo also highlighted several areas of concern that will be featured in the upcoming report. First, several assessment areas — including Manitoba, SPP and British Columbia — reported their anticipated reserve margins have fallen from the previous year’s assessment.

In the case of British Columbia, the reduced reserve margin risks dropping below the area’s reference margin level, which, as in many assessment areas, is higher than last year’s. Coterillo attributed the declining reserve margins in SPP and other areas to increases in peak demand and generator retirements.

Coterillo also singled out MISO, which is projecting a significantly higher reference margin compared to last year, for comment. Noting the RTO has “recently re-evaluated the reference margin for cold weather operations,” Coterillo said MISO “opted for a higher [reference] margin to cover this impact for winters going forward.”

Finally, the team previewed its extreme condition risk analysis for the upcoming winter. The risk analysis is based on data provided by each assessment area, including their anticipated resources for the winter and projected maintenance outages and forced outages. The analysis then factors in a potential extreme low-generation scenario, as well as projected peak demand under both normal and extreme conditions, to identify any areas where resources may not be sufficient at some point during the season.

NERC plans to publish this year’s WRA in the middle of November.