A working group focused on gas resource participation in CAISO-run markets held its second meeting this week, with stakeholders saying they don’t receive enough advance information to make good decisions on gas procurement.

CAISO is hosting the gas resource management (GRM) working group to explore challenges that stakeholders face while participating in the Western Energy Imbalance Market and potentially the extended day-ahead market, which is under development.

The working group process will result in an “action plan” that CAISO will use in potentially crafting future initiatives.

During Tuesday’s workshop and in written comments, stakeholders discussed the challenges of gas procurement.

Salt River Project (SRP) pointed to what it called a “mismatch between when gas is traded, when gas is scheduled, and when power awards are made by the organized market.”

“It is critical to know the quantity of gas required to meet load/market awards so that the correct amount can be scheduled,” SRP said in written comments.

SRP said reliability risks may be created, such as in situations when intraday gas isn’t available to buy.

Alan Meck, a business and economics advisor at San Diego Gas & Electric, described the problem as “lack of foresight.”

“You have to figure out … am I going to go ahead and buy the gas and then potentially be stuck holding the bag?” Meck said during Tuesday’s meeting. “Or am I going to not [buy the gas] and potentially get an energy schedule going into real time and then have to pay the real-time price?”

Stakeholders including SDG&E and PacifiCorp said their limited ability to store gas adds to the problem. And recent increases in variable energy resource capacity have made forecasts more uncertain when it comes to gas procurement.

Timeline Alignment

The working group is expected to revisit a topic CAISO has explored: a potential alignment of electric and gas market timelines.

CAISO said its previous analysis of such an alignment found it wouldn’t be in the interest of market participants. In particular, the switch would require business process changes, and earlier timelines might increase forecast inaccuracy.

The ISO has asked working group members to weigh in on whether those issues still are a concern.

On other topics, the Northern California Power Agency proposed a discussion of how hydrogen could be incorporated into the markets.

“Any effort or interest now in incorporating how hydrogen fits into gas resource management will only provide compounding benefits in the future,” NCPA said in written comments.

Salt River Project wants to see more discussion of multi-stage generators, which are units with multiple operating configurations.

“SRP would like to emphasize the importance of multi-stage generators (MSGs) and that enhancements in their management have the potential to significantly impact efficiency and reliability,” SRP said in written comments.

Existing Tools

Vistra Corp. noted that CAISO previously discussed gas resource management issues in a 2016 paper called “Commitment Cost and Default Energy Bid Enhancements” (CCDEBE). The CAISO board then approved a CCDEBE proposal in 2018.

“Vistra strongly encourages the CAISO to examine its existing tools and procedures’ effectiveness and to implement the remaining elements of CCDEBE as soon as possible,” Vistra Corp. said in written comments. “After which, a discussion on whether new tools and procedures are needed can be held.”

Mark Richardson of CAISO, who facilitated Tuesday’s session, said CAISO will examine what previously was approved — but hasn’t been implemented yet — before the next working group meeting.

In addition to Tuesday’s session, the GRM working group met on July 27. After each meeting, CAISO plans to release a discussion paper that summarizes the working group’s conversation.

The next working group meeting is scheduled for Sept. 18.

The Department of Energy on Thursday issued three reports on wind-generated electricity, projecting strong but not uniform growth for the nation’s onshore, offshore and distributed wind power sectors.

Wind was second only to solar in new generating capacity installed in the U.S. in 2022, DOE said in a news release, attracting $12 billion in capital investment and employing more than 125,000 Americans.

The flurry of policy changes made and financial incentives offered during the first two years of the Biden administration have significantly boosted near-term forecasts for future deployment of environmentally friendly wind power, DOE added.

This trend serves another purpose beyond climate protection — economic stimulus. DOE noted at least 11 announcements of opening or expansion of U.S. manufacturing facilities to serve the onshore wind industry.

The reports also touched on significant challenges facing the industry, primarily due to high costs, short supplies and constrained transmission.

The problems are such that the first generation of offshore wind development could be stunted for the next few years, the authors write.

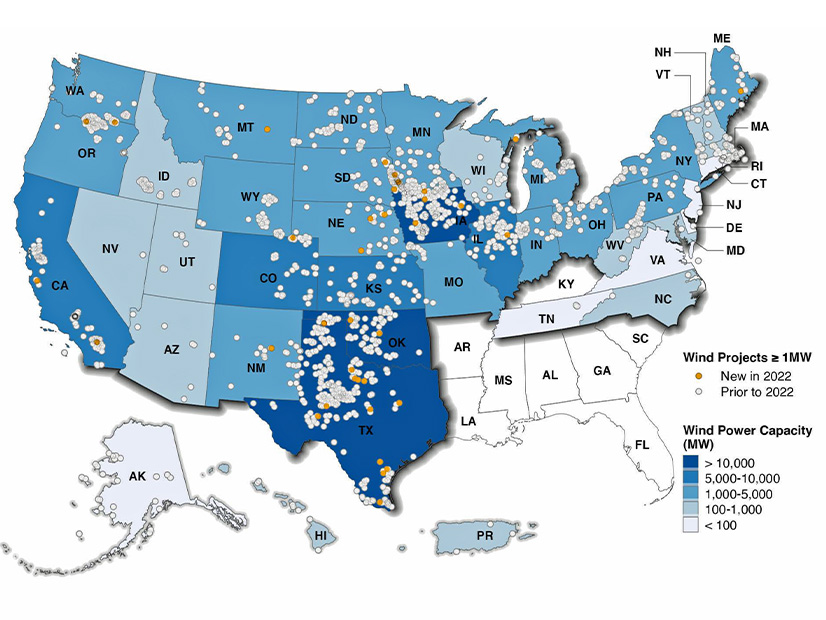

It found that 8,511 MW of new utility-scale onshore wind generation capacity was added nationwide in 2022.

That was the smallest increase since 2018, due to a confluence of factors that included inflation, supply-chain constraints, rising interest rates, interconnection delays, siting challenges and — until passage of the Inflation Reduction Act last August — a reduction in the value of the Production Tax Credit.

Other key takeaways from the report include:

The U.S. is second only to China in wind power generation, but wind provides only 10% of the electricity generated in the U.S., far less than wind power leader Denmark (57%).

Iowa is the state wind power leader, deriving 60% of its power from wind.

New utility-scale turbines were installed in 14 states in 2022, with Texas accounting for nearly half the capacity, at 4,028 MW.

For the first time, corporations and other nonutility buyers bought more wind-generated electricity than utilities did in 2022; direct retail purchase of wind power accounted for at least 44% of the new capacity added last year.

The average nameplate capacity of newly installed onshore turbines was 3.2 MW in 2022, up 7% from 2021; the average hub height was 98.1 meters above ground, a 4% increase.

Wind power as a percentage of system load ranged from 37.9% in SPP to 3.1% in NYISO.

Offshore

The 2023 edition of the Offshore Wind Market Report was prepared by DOE’s National Renewable Energy Laboratory.

It found that the U.S. offshore wind pipeline reached 52,687 MW in 2022, up 15% over 2021. This breaks down to 40 projects in some stage of development totaling 47,606 MW, and 5,039 MW of potential capacity in planning stages. (The two U.S. projects already in operation have a combined 42 MW capacity.)

Other key takeaways from the report include:

The U.S. offshore wind industry invested $2.7 billion in ports, vessels, the supply chain and transmission capacity.

Offshore wind lease areas continued to grow in number and variety, as a late 2022 auction offered the first Pacific Coast leases and the first that will require floating wind turbine technology.

The policy and statutory goals of 13 states have reached 112,286 MW of nameplate capacity.

Many U.S. offshore wind projects are facing headwinds from supply chain constraints, inflation and interest rate hikes, particularly those with an expected commercial operation date in 2025 or 2026; project costs increased 11% to 30% in 2022.

Key indicators in the U.S. offshore wind energy market point toward sustained market growth, but macroeconomic hurdles could significantly stunt that growth for the first generation of commercial projects; incentives provided by the IRA may provide some relief.

It tallied 1,755 distributed wind turbines added in 13 states in 2022. Those 1,755 turbines had a combined capacity of 29.5 MW and required a total investment of $84 million.

Other key takeaways from the report include:

Cumulative distributed wind capacity has reached 1,104 MW from more than 90,000 turbines in all 50 states, the District of Columbia, Guam, Puerto Rico and the U.S. Virgin Islands.

California, Iowa and Nebraska had the most capacity additions last year, due in part to projects that entail large-scale turbines — those greater than 1 MW in size.

A visualization of new and existing wind power projects larger than 1 MW across the United States. | DOE

Minnesota led the nation again in smaller-scale capacity additions — turbines rated at 100 kW or less — due primarily to the continued push there to sell small-scale wind power to agricultural markets.

None of the distributed wind projects reported in 2022 used midsize turbines — those rated at 101 kW to 1 MW.

Iowa by a wide margin has the greatest installed distributed capacity, at 222 MW; runners up are Minnesota (128 MW) and California (83 MW).

Agriculture is the most common use for distributed wind installed in 2022, accounting for 33% of projects; residential and commercial were second, tied at 26%.

Only 10% of distributed wind projects completed in 2022 were interconnected to the grid; the great majority were intended to provide energy for on-site use.

CHARLESTOWN, Mass. — In a massive warehouse surrounded by a sprawling parking lot at the edge of the Mystic River, a small team of engineers is hard at work testing the wind turbine blades that could power a major portion of the state’s electricity needs over the coming decades.

The Wind Technology Testing Center (WTTC) is the only commercial-scale facility in the country capable of testing the long-term durability of large wind blades. These have included the 350-foot-long blades for the Vineyard 1 project off the state’s coast, an 806-megawatt wind farm expected to come online in the fall.

The center is overseen and supported by the Massachusetts Clean Energy Center but has only seven full-time employees at the facility. The small group of engineers perform a wide range of tasks from data analysis to suspending the several-hundred-foot-long blades in midair across the length of the floor.

The WTTC opened in 2011, originally testing onshore blades about half the size of those tested for the Vineyard 1 project. The size of the blades has increased rapidly in recent years.

“The last four years have been extremely busy for us,” WTTC Executive Director Rahul Yarala told RTO Insider. Yarala noted that along with the steady demand for blade testing, “longer blades take longer to design, build and test.”

Located just past the Tobin Bridge upstream from Boston Harbor, the location allows the WTTC to receive blades via cargo ship, as many of the blades are too large to arrive by truck.

Inside the facility, three blades are attached to the wall and suspended midair, where they’re manipulated to simulate the wear a blade will experience over its lifespan, from everyday use to severe impacts from extreme storms. At the end of a blade’s testing process, the engineers sometimes will bend the blade past the point of collapse to test the outer limits of its durability.

As the only large-scale blade testing facility in the country, Yarala sees the WTTC as playing an essential role in enabling the domestic offshore wind supply chain sought by the Biden administration.

“It is very important for the U.S. offshore market and domestic supply chain to have the necessary infrastructure to provide blade testing capabilities both for new product development and reliability of the turbines being deployed,” Yarala said. “It takes a lot of coordination and cost to transport a long offshore wind blade and hence it is a great benefit to have this testing capabilities in U.S. as the domestic supply chain is being developed.”

As blade models have gotten longer and heavier, the largest offshore wind blades no longer fit in the WTTC facility, requiring the tips of the blades to be cut. To keep up with the increasing blade sizes, the WTTC hopes to obtain funding to expand the testing space.

“The industry partners are demanding it,” Yarala said. “We might fall back if we don’t expand and have the capacity to test longer blades and higher loads.”

While the center initially was funded largely using federal money, its day-to-day operations are entirely self-sufficient based on the fees it charges clients for blade testing. The state already has allocated $10 million of federal funding from the American Rescue Plan Act (ARPA) for the design and early construction of the WTTC expansion, but the center has not yet procured full funding for the expansion.

“We are continuously exploring different potential funding sources, including all relevant federal funding opportunities, and also working with the state officials who are supportive of the WTTC expansion,” Yarala said.

In 2022, Republican then-Gov. Charlie Baker proposed using $70 million in ARPA funds to pay for the expansion, but ultimately failed to secure the funding. Democratic Gov. Maura Healey’s administration also supports expanding the facility.

“The Healey-Driscoll administration is committed to the expansion of MassCEC’s Wind Technology Testing Center,” a spokesperson for the Executive Office of Energy and Environmental Affairs told RTO Insider. “We are considering every option to fund this much-needed expansion that will advance Massachusetts’ clean energy industry.”

The governor’s March supplemental budget proposal included $35 million to be transferred to the Clean Energy Investment Fund, which could have been used to support the WTTC expansion.

The expansion proposal appears to have some support in the state legislature, which has passed bills promoting offshore wind development over the past two legislative sessions. So far this session, a range of often-competing interests including utilities, environmental organizations and labor have supported bills increasing the state’s offshore wind procurement goals. (See Utilities, Generators and Wind Developers Spend Big on Lobbying in Mass.)

The center is one of the few places in the region where individuals can get a close-up look at the massive blades that have the potential to power the state’s clean energy transition, and the center holds frequent tours for a variety of groups interested in offshore wind technology.

“We’ve seen rapid changes in the technology and size of the turbines and blades, at such magnitude that nobody could have anticipated 10 years ago,” said state Rep. Jeffrey N. Roy (D), House chair of the Joint Committee on Telecommunications, Utilities and Energy, who supports expanding the facility. “We are trying to make Massachusetts a leader in offshore wind in the nation, and the testing services that this facility provides are a critical component of that.”

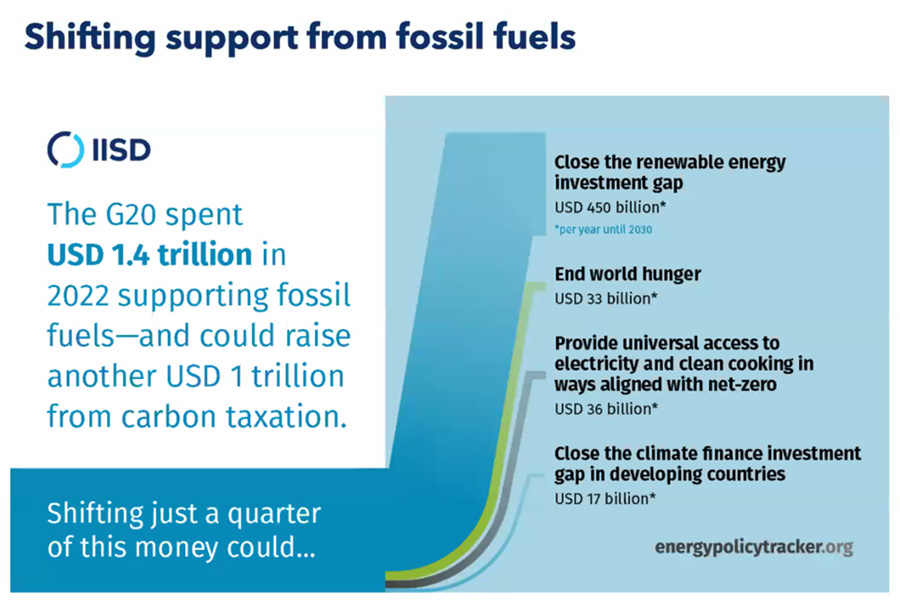

The industrialized nations of the G20 piled up a record $1.4 trillion in subsidies for fossil fuels in 2022, driven in large part by consumer subsidies to soften the impact of the energy crisis triggered by Russia’s war in Ukraine, according to a new report from the International Institute for Sustainable Development (IISD).

Such subsidies come in the form of price supports or caps on gas prices, as well as tax cuts or other government actions to lower heating or gasoline costs, Tara Laan, a senior associate at IISD and lead author of the report, said during a Wednesday webinar.

“It’s understandable that during a crisis, governments need to intervene to assist their citizens,” she said. “But what we know is that fossil fuel subsidies are an extremely inefficient way to assist the poor and to provide sort of social welfare, and this is simply because those who use the most fuel often harness the most benefits.

“Why should the amount of help you get from the government be directly proportional to the amount of fossil fuels you use? What we recommend countries do is remove these subsidies and use the savings to provide targeted welfare to those who need it.”

Other key findings of the report include:

Government-owned or -controlled companies invested $322 billion in investments in fossil fuel infrastructure in 2022, “and it’s only going to increase,” Laan said. “We know that national oil companies are doubling down [on investments] because of the massive profits they made in 2022.”

G20 governments made commitments to provide $265 billion in subsidies for renewable energy between June 2020 and June 2023. That comes out to about $88 billion per year, or less than one-tenth of the 2022 fossil fuel subsidies, and Laan said, “This is commitments, not annual spending.”

If all the G20 nations implemented a tax on carbon dioxide — proposed at $75/ton for high-income countries and $25/ton for lower-income countries — the tax could raise $1 trillion per year, “a vast amount of money that could be used for other purposes,” Laan said.

A carbon tax provides governments a way to make businesses pay for the hard-to-value “externalities” of fossil fuel consumption, such as climate change, other air pollution and traffic congestion, said Nate Vernon, an economist with the International Monetary Fund.

Such “corrective taxation” can result in “these externalities only occurring when the benefit to consumers exceeds the full cost of consumption, which improves the allocation of resources across the economy, raises revenues and results in the economically efficient level of externalities,” Vernon said.

Combining a carbon tax with a phaseout of fossil fuel subsidies could add up to $2.4 trillion per year to be diverted to a range of social welfare and clean energy initiatives, the report said.

Just 25% of that total could provide $33 billion per year to end world hunger, $36 billion to provide universal access to electricity and clean cooking technologies, $17 billion for clean energy investments in developing countries and $450 billion to boost renewable energy generation, the report says.

Renewable Energy Investment Gaps

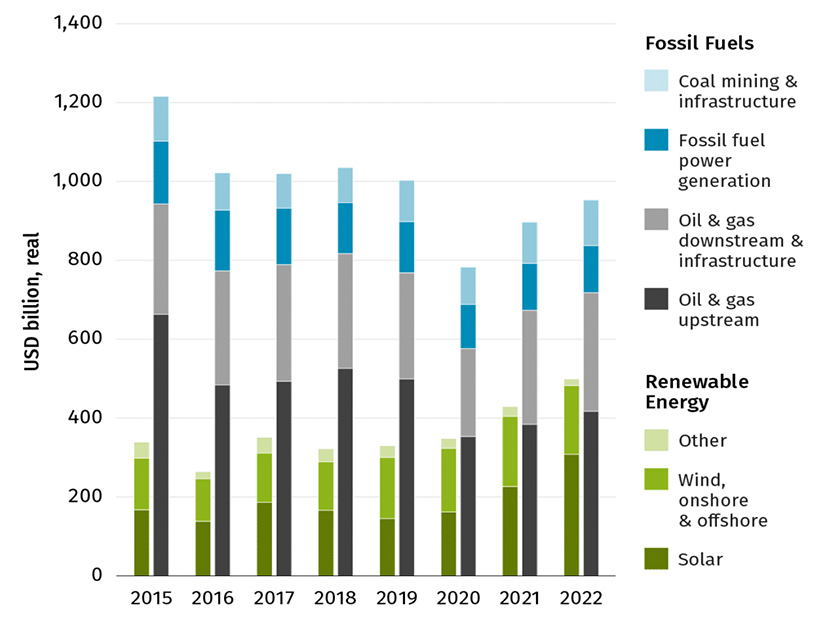

Investment trends in renewable energy also raise concerns on a global level, said Diala Hawila, program officer at the International Renewable Energy Agency. Private and public investment in renewables worldwide hit half a trillion dollars in 2022, versus $440 billion in fossil fuel investments in the G20 alone, she said.

| IISD

But, Hawila said, “If we look again, at the global investments in renewables, we see more and more concentration not only in developed countries, but also in developed technologies. So, solar PV, onshore and offshore wind are almost accounting for 97% of investments. Overall, we are relying more on private investments to drive the energy transition, but private investments only go to countries with reliable markets.”

Progress on the energy transition is primarily in the power sector “because those are the mature technologies, and only in developed markets,” she said. “So, we are leaving a large chunk of the globe outside the energy transition.”

Per capita figures reveal the enormous gap between clean energy investments in the northern and southern hemispheres, Hawila said. In 2015, per capita investments in renewables in North America were 23 times higher than per capita investments in sub-Saharan Africa, she said. As of 2021, the North American figure had risen to 57 times greater than sub-Saharan Africa.

Annual investment in fossil fuels and renewable energy (public and private), 2015-2022 | IISD

Further, Hawila said, the figures on renewable energy investment focus solely on assets and do not include “the government support that goes into creating enabling environments … for example, investing in infrastructure like grids and investing in R&D.” More than triple the current level of renewable energy investments will be needed.

“A lot of the money that is now going into subsidizing fossil fuels or into the fossil fuel industry will be needed to be channeled into [those] enabling environments,” she said.

Commitment vs. Action

The release of the IISD report appears to be strategically timed in advance of the G20 Summit in India on Sept. 9-10.

Representing the world’s largest economies, the G20, or Group of 20, was formed in 1999 to provide an international forum for economic cooperation. While sessions initially were attended by finance ministers, the recession of 2008-09 resulted in the forum being “upgraded” to high-level meetings of heads of state and government.

The group’s efforts to phase out subsidies for fossil fuels began in 2009, when members made a commitment to phase out “inefficient” subsidies, but without setting a deadline. In 2016, the smaller G7 — including Canada, France, Germany, Italy, Japan, the United Kingdom, the U.S. and the European Union — set a 2025 deadline for the subsidy phaseout, with progress reports due in 2023.

Unfortunately, these and other international commitments on climate change have rarely led to substantive action, Laan said.

“Reform has to be made domestically,” she said. “It has to be about regulations and policies put in place by leaders in their home countries to actually implement these decisions, and that’s exactly what we’re lacking at the moment on fossil fuels.”

Exact figures on fossil fuel subsidies in the U.S. are elusive. A recent article from Reuters provided a range of $10 billion to $50 billion per year, while Sen. Sheldon Whitehouse (D-R.I.) cited a figure of $20 billion per year at a Senate Budget Committee hearing in May.

At the same time, fossil fuel giants like BP, Shell and Exxon are walking back previous commitments to cut emissions and invest in renewables, as they rake in record profits, according to an article in Grist. BP, for example, has downgraded a commitment to cut emissions 35% by 2030 to 20 to 30%.

President Joe Biden’s proposed 2024 budget included measures to scrap fossil fuel subsidies, which almost certainly will not be included in any final deal in September. On the upside, the passage of the Inflation Reduction Act in 2022 has put the U.S. way ahead of all other G20 countries on investments in renewables.

Canada Delivers

In July, Canada became the first G7 nation to issue federal guidelines for a phaseout of fossil fuel subsidies, with specific definitions of what kinds of subsidies would and would not be considered “inefficient.” To earn an exemption from the phaseout, subsidies must meet one of six criteria, such as reducing greenhouse gas emissions, supporting clean or renewable energy or providing essential energy services to remote, off-grid communities.

Subsidies also will be allowed for the development of emission-abating technologies such as carbon capture and storage.

The guidelines are backed up with “a fairly exhaustive set of definitions … to eliminate the risk of these exemption criteria being used [to allow] for support outside the spirit and intent of the framework,” said Matthew Watkinson, director of regulatory analysis at Canada’s Department of Environment and Climate Change.

However, Watkinson said, the guidelines are designed to provide for an evolution in the understanding of net zero, which “is fraught with a lot of uncertainty. When you’re putting something out there now, it’s difficult to close the door completely on technologies that are still largely unknown or where there are still question marks.”

The guidelines also include “a clear statement of intent to periodically review and ensure that we are maintaining alignment with technologies as they emerge and government priorities as they emerge,” he said.

Whether Canada will serve as a spur for other G20 nations remains to be seen. Laan would like the G20 to go further, either removing the world “inefficient” from the phaseout language or more narrowly limiting exemptions to only allow for “energy subsidies for the poor,” she said.

Another big step would be for the group to set a deadline as the G7 has, she said.

The September G20 summit in India is being watched closely as any climate action or lack of it certainly will affect the already mixed expectations for the United Nations Climate Change Conference (COP28) to be held in early December in the United Arab Emirates, a major oil producer.

Along with efforts to phase out fossil fuel subsidies, the G20 also may make decisions “on new areas of concern like supply chains, like essential critical minerals,” said Aarti Khosla, director of Climate Trends, a consulting firm in India. “Trying to just simply understand how much G20 countries that are talking about climate change are also supporting on the other hand the production and consumption of fossil fuels … is something that is going to give us a clearer idea of how climate action is being understood across the world.”

NERC’s Standards Committee agreed to authorize the shortening of public comment periods for two high-priority standards development projects at its monthly conference call Wednesday.

At issue were Projects 2021-07 (Extreme cold weather grid operations, preparedness and coordination) and 2023-03 (Internal network security monitoring). The former was begun in response to the February 2021 winter storms that led to the largest controlled firm load shed event in U.S. history, the latter after FERC ordered NERC to modify the Critical Infrastructure Protection standards to require entities to implement internal network security monitoring (INSM) at crucial cyber systems. (See FERC Orders Internal Cyber Monitoring in Response to SolarWinds Hack.)

Normally the ERO’s standards development process requires an initial formal comment and ballot period of 45 days for proposed standards, with the same time allotted for additional formal comments and 10 days for the final ballot. However, NERC’s Standards Processes Manual allows the ERO to shorten these periods when needed to meet deadlines imposed by regulatory bodies or NERC’s Board of Trustees.

Both affected projects are the subject of FERC deadlines. The commission ordered NERC to file the INSM standard by July 9, 2024, and to file revisions to EOP-012-2 (Extreme cold weather preparedness and operations) by February 2024. In addition, the board set a deadline of Sept. 30, 2023, for submitting EOP-011-4 and TOP-002-5, both part of Project 2021-07.

Project 2023-03 has not reached the stage of having a standard ready for comment. In fact, the proposal submitted by NERC staff on Wednesday was to accept the project’s standard authorization request, meaning any comment and ballot periods are relatively far in the future. By comparison, Project 2021-07 is much further along: EOP-011-4 and TOP-002-5 both are part of the second phase of the project, which began after FERC approved its first two standards this year. (See FERC Orders New Reliability Standards in Response to Uri.)

NERC Manager of Standards Development Jamie Calderon, speaking of the INSM standard, explained the request to shorten the comment period was a necessary expedient to meet what she called a “very tight deadline” set by FERC. Likewise, Latrice Harkness, NERC’s director of standards development, said the standard development team (SDT) working on 2021-07 “has been working diligently to make sure that they are successful in meeting the board deadline this year.”

While the proposal to accept the SAR and reduce the comment period for 2023-03 — from 45 days to “as few as 30” for the first period to “as few as 20” for additional periods and “as few as five” for the final — passed with no discussion, Steve Rueckert of WECC lobbied to change the motion for 2021-07. Rueckert argued that the motion submitted by NERC staff, which would shorten the 45-day comment period to “as little as 25 days,” might not give the SDT enough time to respond to comments and moved to authorize a further reduction to 20 days.

Members passed the changed motion, despite three votes in opposition from William Chambliss of the Virginia State Corporation Commission, Kent Feliks of American Electric Power and Terri Pyle of Oklahoma Gas and Electric. A NERC spokesperson told ERO Insider the 20-day comment period for EOP-011-4 and TOP-002-5 would begin Aug. 24.

Additional standards actions approved at Wednesday’s meeting included posting proposed standard FAC-008-6 (found on page 47 of the agenda) for an initial 45-day formal comment and ballot period. The committee also agreed on a set of minor grammatical corrections to TOP-003-6 (Transmission operator and balancing authority data and information specification and collection), which NERC’s board approved at last week’s meeting in Ottawa.

New Leadership Coming in 2024

Standards Committee Chair Amy Casuscelli of Xcel Energy | NERC

The Standards Committee will hold its next meeting in person at NERC’s Washington, D.C., office Sept. 20. Chair Amy Casuscelli of Xcel Energy reminded attendees the September meeting will include discussions of next year’s meeting schedule and asked for input on potential schedule conflicts.

Also on the agenda for next month are elections to replace the committee’s leadership, including Casuscelli, who confirmed at Wednesday’s meeting that she plans to retire from the committee after its December meeting. Casuscelli, who has headed the committee for the past four years — following two years as vice chair — jokingly suggested that members “dust off and polish up” their resumés ahead of the election.

CAISO asked FERC on Tuesday to approve its tariff revisions implementing an extended day-ahead market (EDAM), as well as revisions to its existing day-ahead market that also would apply to the new regional market (ER23-2686).

The EDAM has been in discussion for several years. The proposal would make the ISO’s day-ahead market available to participants in the Western Energy Imbalance Market (WEIM).

The proposed revisions, called the Day-Ahead Market Enhancements, are meant to better align day-ahead market outcomes with real-time conditions, which has proven more difficult because of the growth in intermittent resources and more common extreme temperatures as a result of climate change.

“Filing the EDAM tariff with FERC is an important milestone for the CAISO and our partners across the West,” CAISO CEO Elliot Mainzer said in a statement Wednesday. “EDAM and the day-ahead market enhancements will build on the success of the Western Energy Imbalance Market and go even further in lowering costs and improving reliability for electricity customers throughout the region. I am grateful for the strong engagement and participation from the diverse group of stakeholders who worked tirelessly to help shape and refine these tariff provisions.”

CAISO estimates the EDAM will save between $100 million and $1 billion annually, which comes on top of benefits already produced by the WEIM. (See West Could Save $1.2 Billion a Year in CAISO EDAM.)

The EDAM represents the most significant market enhancement for CAISO and the West since the WEIM was established in 2014, the ISO told FERC. The proposal will enhance reliability, cut costs to ratepayers, optimize generation dispatch across a broader footprint and help participants and states achieve clean energy policies.

The proposed Enhancements would establish two new products: imbalance reserves and reliability capacity. Both products are aimed at cutting the “load imbalances” between day-ahead market outcomes and the real-time market.

“Two sets of forecasts drive the net load forecast: the gross forecast of load and the production forecast from wind and solar resources,” the filing said. “Unless these forecasts for the day-ahead market perfectly match the forecasts for the real-time market, an imbalance is unavoidable.”

Net load imbalances are to be expected, but they have grown in recent years as increasing intermittent resources and extreme weather make grid conditions the next day more difficult to predict.

CAISO relies on its out-of-market residual unit commitment (RUC) process to adjust the load forecast and thus avoid being short of the online capacity and ramp capability needed to maintain reliability.

Under the Enhancements, the ISO would procure imbalance reserves up and down to meet the range of expected imbalances between the day-ahead and real-time net load forecasts. It also would procure reliability capacity up in the same way it procures RUC capacity for the same reason currently, and procure reliability capacity down to address scenarios in which the day-ahead market awards too much energy relative to the forecast.

Imbalance reserves would be flexible reserve products to cover uncertainty in the net load forecast and real-time ramping needs not covered by hourly day-ahead market schedules. Any resources-procured imbalance reserves would have to submit economic bids in the real-time market for its awarded capacity range.

Reliability capacity would meet the positive or negative differences between cleared physical supply in the integrated forward market and the load forecast. It is similar to the RUC process, but it also could deal with situations when actual demand exceeds the forecast, while RUC does only the opposite.

“With the bidirectional reliability capacity product, the CAISO will replace the existing unidirectional RUC capacity product it procures today with the reliability capacity up product as well as the ability to procure decremental capacity with the reliability capacity down product,” the ISO said in its filing.

Suppliers for both products would provide bids for both up and down products. Each bid would have a single price/quantity pair, with imbalance reserves having a $55/MWh cap and reliability capacity bids at $250/MWh.

EDAM Tariff

The EDAM offers a voluntary regional day-ahead market by using the ISO’s current day-two market with targeted adjustments that recognize the unique challenges and needs of the WEIM balancing authorities that might participate and other market participants. The new marker would include the Day-Ahead Market Enhancements.

“For the balancing authorities that join, the extended day-ahead market will settle all loads and resources in the day-ahead timeframe and all imbalances between day-ahead positions and the real-time market,” CAISO said. “The extended day-ahead market will optimize the transmission and resources offered into the market to identify the most efficient resource commitments and energy transfers to meet forecasted demand across the footprint.”

Like WEIM, entities participating in the EDAM would have to show they meet readiness criteria to ensure the ISO and participants are prepared for the operation of the day-ahead market in each balancing area. The proposal also has transitional measures to insulate participants from adverse impacts when the market goes live.

The new market would provide legacy transmission contracts and transmission ownership rights in an EDAM balancing area with a scheduling priority and settlement process consistent with existing mechanisms in the ISO’s tariff while making the flow capability available to the entire market.

Another similarity with WEIM is that every balancing authority in the EDAM would have to go through a process ensuring it has enough resources to meet demand, with those that pass being pooled together for the regional real-time market, and those that fail getting a chance to cure that in the integrated forward market.

The EDAM also would take into account the fact that some of the states covered have greenhouse gas regulations, but others do not, by requiring bidders outside of them wishing to sell into such states to include an adder for emissions costs.

The process for joining the EDAM would be based on that for WEIM, with implementation agreements, onboarding cost recovery mechanisms and onboarding processes before participation begins.

CAISO told FERC it could reject the EDAM and still approve the Enhancements, but the latter are needed to approve the EDAM. The new market needs the changes to manage the increasing system variability and uncertainty around the West, but the Enhancements would benefit CAISO’s own markets enough to warrant their approval alone, the ISO argued.

The ISO asked FERC for an order by Dec. 21 and asked for an extension of the due date for comments to 30 days after its filing, with replies to be due 20 days after that.

VALLEY FORGE, Pa. — None of the 20 proposals PJM and stakeholders drafted through the Critical Issue Fast Path (CIFP) to rework the capacity market garnered sector-weighted support from the Members Committee on Wednesday.

The vote caps off five months of stakeholder meetings, culminating in the proposals being presented to the PJM Board of Managers on Wednesday before the MC vote. With the stakeholders’ portion of the CIFP process complete, the board now will decide if it will direct PJM to make a FERC filing to revise the capacity market and what form that may take. In its letter initiating the process, the board targeted Oct. 1 for making a filing.

Board Chair Mark Takahashi said they will work through the proposals and perspectives they heard Wednesday and how stakeholders voted when considering next steps over the coming weeks. He said the board may reach out to CIFP package sponsors for more information about what they proposed.

“I do think we’re trying to get something as far as we can in the next few weeks,” he said.

Though none of the packages received the committee’s support, PJM CEO Manu Asthana said he saw pockets of support that could aid the board in its deliberations. PJM posted the sector-weighted voting results on its website. The detailed voting report likely will come later in the week.

“We’re going to have to spend several working sessions working item by item … and this input is going to be invaluable,” he said.

A proposal focused on limiting the October filing to revising the Capacity Performance (CP) nonperformance penalty rate generators pay should their units not meet their obligations during an emergency, as well as the stop-loss limit capping the amount they can pay in penalties over a year. Instead of being based on the net cost of new entry, the proposal would have based the penalties on the Base Residual Auction (BRA) clearing price for that delivery year. The Independent Market Monitor; Daymark Energy Advisors and East Kentucky Power Cooperative; and American Municipal Power (AMP) and J-Power all submitted identical proposals making those changes, which were voted on as one. (See “Several Stakeholders Propose Variants of PJM Proposals,” PJM Stakeholders Finalize CIFP Proposals Ahead of Vote.)

Speaking after the vote, Paul Sotkiewicz, representing J-Power USA, urged the board to take into consideration that changing the CP structure to de-risk the market using the BRA price as the basis for penalties and stop-loss did receive majority support (2.8 out of 5), although it failed to meet the sector-weighted threshold. It was the only proposal to receive a majority of support. He noted that the MC previously endorsed changing the penalty rate and stop-loss to be based on the auction clearing price in May. (See FERC Approves PJM Change to Emergency Triggers.)

“I would encourage you to think clearly that you’re getting a second signal from the membership on that,” he said.

PJM’s annual capacity market proposal was the second-highest vote getter with 41% support. It includes the risk modeling, winterization requirements, hourly bilateral capacity obligation exchanges and other components of the seasonal proposal the RTO has made throughout the CIFP process, but retains the annual capacity auction structure. The seasonal model received 24.7% support. (See “PJM Adds Annual Auction Design Proposal,” PJM Stakeholders Finalize CIFP Proposals Ahead of Vote.)

Two proposals from AMP and J-Power received the third- and fourth-highest support, 39.4% and 37.9%. They would create a transitional phase with the changes to the penalties, as well as revising the balancing ratio to include net exports and applying the same penalties to FRR resources that generators participating in PJM’s Reliability Pricing Model face. The option of using physical penalty commitments also would be eliminated for FRR entities. (See “Stakeholder Hourly Capacity Proposals,” PJM Stakeholders Finalize CIFP Proposals Ahead of Vote.)

The proposal for the second phase would revise use of a variant of the Monitor’s proposed hourly capacity model, changed to have a two-year procurement horizon with two Incremental Auctions and no exceptions to the requirement that capacity resources offer into the energy market.

The Monitor’s Sustainable Capacity Market followed in fourth place with 37.4% sector-weighted support and would have paid capacity for each hour they are able to offer their capacity into the energy markets. (See “Monitor Proposes Hourly Model with Annual Pricing,” PJM Stakeholders Finalize CIFP Proposals Ahead of Vote.)

[Editor’s Note: An earlier version of this article incorrectly stated that AMP’s and J-Power’s proposals came in second and third in voting.]

Pennsylvania has announced an investment of federal funds totaling $33.8 million to install 54 electric vehicle charging projects as the state seeks to put more EVs on state roads.

It’s the first award from $171.5 million in federal money allocated to the state under the National Electric Vehicle Infrastructure (NEVI) program. The award will put 216 charging ports on or close to more than a dozen highways across the state, including Route 80, Route 84 and Route 95.

Twenty-two of the projects will be in or near disadvantaged communities, and construction of the first projects, all of which include four charging ports, is expected to begin by the end of 2023.

“This funding will allow us to deploy electric vehicle charging stations across our Commonwealth, from cities to suburbs to rural areas, promoting energy security, creating jobs and reducing our carbon footprint,” U.S. Sen. Bob Casey (D) said in a release from the state Department of Transportation (DOT).

Richard Price, executive director of the Pittsburgh Region Clean Cities Coalition, a federally funded advocacy group, said once the 54 projects are implemented, “a lot of the range anxiety” will go away.

Most EV owners now must charge their vehicle at home or work using a Level 2 charger, rather than a Direct Current Fast Charger, he said. It takes several hours to charge a vehicle with a Level 2 charger, compared to less than an hour with a fast charger.

“Now this allows somebody with a battery electric vehicle that can take the DC fast charge to travel long distances and be able to know that they can go outside their local area and be able to charge or refuel — all along all these corridors,” Price said.

The state has 3,668 publicly available EV charging ports at 1,481 sites, about one-quarter of which are direct current fast chargers. Most of the rest are Level 2 chargers, according to DOE figures. It’s unclear how many non-public chargers are in the state. The state’s EV Mobility Plan, released in July 2022, set a goal for the state to add 2,000 new EV charging ports at 800 sites by 2028.

Increasing Charger Accessibility

The focus on charger installation is part of the state’s effort to reduce greenhouse gas emissions by 80% below 2005 levels by 2050. The state’s two largest sources of greenhouse gas emissions are electricity transmission and industrial facilities, which account for 34% and 30%, according to the state’s Electric Vehicle Roadmap. Transportation, which is third with 20% of greenhouse gas emissions, is the focus of a variety of state programs designed to motivate residents to adopt EVs.

Pennsylvania, with 47,400 EVs on the road in 2022, about double the 2021 figure, was ranked the 13th state in the nation by the number of EVs, according to the U.S. Department of Energy.

A year ago, the DEP increased the incentive available for EV buyers from $750 to $2,000-$3,000, depending on household income.

The annual “transportation electrification” scorecard compiled by the American Council for an Energy-Efficient Economy (ACEEE) ranked Pennsylvania 16th, with a strong assessment for its incentive programs and middling grades for its grid optimization efforts. The scorecard gave Pennsylvania low grades for its planning and goals, efficiency of its transportation system and the outcome of the state’s policies and whether they were influencing putting more EVs on the road.

Fuel Corridors

NEVI funds support the planning, design, construction, operation and maintenance of charging sites. Under NEVI, states are required to identify alternative fuel corridors (AFCs), major state and interstate highways where EV charging stations would be located every 50 miles. The Biden administration eventually will award $5 billion in NEVI funds, with money for all states. The administration in July released a report stating the first year of the program showed it’s working as planned. (See Federal Plans to Electrify Highway Corridors Advancing.)

Goals set out in the NEVI plan for Pennsylvania, which has 1,800 miles of AFCs, include making sure direct current fast chargers are located within a mile of a highway intersection, and to “build redundancy” to ensure sufficient chargers where demand is high. The plan also seeks to ensure 95% of Pennsylvanians live within 15 miles of a public EV charging station and for 50% of municipalities to have at least two Level 2 plugs open to the public 24/7 by 2027.

The plan requires developers to put up at least 20% of the investment, according to the Pennsylvania DOT.

The first round of NEVI money focused on “building out the AFC network,” the DOT release said. When that task is accomplished, NEVI will “fund right-sized EV chargers for Pennsylvania’s community charging,” the department said.

Price said he expects the next round of funds to be spent on putting chargers every 25 miles, instead of every 50 miles, and in creating “redundancy,” so there are enough chargers at each site, so drivers don’t have to wait long to get connected.

The state, which received 271 applications for first-round funding, selected the winning projects based on ones that:

Provided a variety of amenities and services to improve customer experience (such as varied payment options);

Offered local economic development and workforce opportunities; and

Featured locations that are “welcoming, safe, and accessible for all.”

The chosen projects will put chargers at various convenience stores such as Wawa, Sheetz, KwikFill and Al’s Quick Stop, and at truck stops and travel plazas. Twelve of the awards are for Tesla charging stations.

The offshore wind sector will need a $100 billion supply chain investment to meet the 2030 targets that policymakers have set, a new analysis finds.

Wood Mackenzie’s report issued this month, “Cross Currents: Charting a Sustainable Course for Offshore Wind,” explores the disconnect between the desire to build offshore wind and the ability to manufacture the components. It compares a baseline increase in generation capacity of up to 30 GW per year with policymakers’ goals of up to 77 GW per year. To accomplish this, much more money must be plowed into the supply chain: $27 billion by 2026, and more than $100 billion by 2030, the report finds.

This bumps up against investor hesitation because of low margins and uncertainty of project timing in the offshore wind sector, the authors say.

Suggested solutions include extending the planning process beyond 2030, building better supplier-develop partnerships and capping turbine size to pause manufacturers’ race to build ever-larger machinery.

The report finds this “arms race” is particularly damaging, shortening the timeframe to recover investments and recoup research-and-development costs, increasing the cost of installation and repairs and rendering expensive equipment and facilities obsolete if they can handle a 12-MW turbine but not its 15-MW successor or the 18-MW prototype under development.

It also notes that 24 GW of projects scheduled to come online in 2025-2027 have secured a subsidy or power purchase agreement but have not made a final investment decision. Multiple projects are delayed worldwide as they seek to renegotiate offtake contracts to reflect their rising costs.

Delays, Constraints

Chris Seiple, vice chair of power and renewables at Wood Mackenzie and co-author of the report, said governments’ commitment to offshore wind is clear but the supply chain will be an impediment to achieving their targets.

“Nearly 80 GW of annual installations to meet all government targets is not realistic,” Seiple said in a news release. “Even achieving our forecasted 30 GW in additions will prove unrealistic if there isn’t immediate investment in the supply chain.”

Another factor, Seiple said, was an oversupply that followed a supply chain buildout a decade ago, depressing profitability.

“Burned once, current suppliers are cautious in their investment plans, and the lack of profitability is hampering their ability to fund manufacturing capacity expansion — ultimately stalling innovation in the sector.”

Given the decade-plus time needed to realize a return on investment, there is hesitation by manufacturers to supercharge a buildout that peaks in 2030 and then subsides. To counter this, the authors suggest not setting the 2030 goal too high and creating a clear post-2030 road map.

The report excludes one major player in the offshore sector — China — because it relies largely on a domestic supply chain and because that supply chain largely has not extended abroad. But that could change as Chinese companies look to expand their markets, the authors note.

2026 Estimates

The report’s estimated need for $27 billion in investments by 2026 is closely focused — not on a full supply chain buildout, just what is required for installation, foundations, towers, blades and nacelles. None of this can come from the onshore wind supply chain, they noted, because of the size differential.

Installation of equipment offshore is the largest gap, the report finds, because half of the fleet of ships is too small to handle the next generation of supersize turbines. More than 20 new vessels are needed, at an estimated cost of $13 billion.

Foundations — massive steel tubes driven into the seabed — are needed in greater number and larger size. But scaling up manufacturing capacity is more challenging than with other components because of their sheer bulk, and because of the customization needed for individual sites.

The towers that stand on the foundations are getting larger and more complicated as the turbines that sit on top of them grow more powerful, rendering some factories obsolete. Many plans have been announced to expand them or build new ones, but only a third have reached a final investment decision.

Nacelles are the bright spot in the report, deemed the least likely to become a supply chain bottleneck because of the firm commitment manufacturers have made to expanding production capacity. The sticking point might be coordinating expansion of the suppliers of all the components of a typical nacelle.

Blade manufacturing requires ongoing investment because of demand growth and retooling to produce longer blades. Manufacturers are sustaining losses or limited profit as a result and have committed to only a fraction of the $4 billion investment needed in new factories, which typically have a three- to five-year lead time.

The authors also note that the supply chain has become highly concentrated in the past decade — to the point that the top three manufacturers of foundations, towers, blades and nacelles account for 67%, 70%, 93% and 96% of their markets, respectively. This allows them greater influence on pricing and timing in their industries.

SPP set a new record for summer peak demand Monday, the first of several that could come this week with a heat dome settled over the Great Plains.

The grid operator, which serves a 14-state footprint in the middle of the country, registered a peak demand of 56.18 GW at 4:27 p.m. (CT). That broke the previous mark of 53.24 GW set last summer by nearly 6%.

The record came as SPP was operating under a conservative operations advisory, declared because of the extreme heat, high load forecast and low wind forecast. The RTO issued another conservative operations advisory Tuesday. It also remained under previously declared resource and weather advisories; both have been extended until 8 p.m. Friday.

None of the advisories require public conservation and have been issued to raise awareness of potential reliability threats.

“It’s possible we may set another record,” SPP spokesperson Meghan Sever said in an email. “Stay tuned.”

Demand within the footprint hit 54.63 GW Tuesday afternoon, according to GridStatus.

About 143 million people in the country’s heartland were under heat alerts Tuesday. The National Weather Service is expecting high-temperature records to fall throughout the week, as the oppressive heat continues into next week.

Sitting almost squarely under the heat dome, parts of Kansas are under an excessive heat warning through Friday. Lawrence saw a heat index of 134 degrees Fahrenheit Sunday and Topeka broke an unofficial record at 127. Other cities in the region have seen, and will continue to see, heat indices approaching 120 degrees.

Sever says SPP expects to have enough generating capacity to meet the demand and its assessments don’t raise reliability concerns. The RTO’s summer reliability assessment indicated a 99.5% probability the system will have sufficient capacity to meet demand.

C.J. Brown, SPP’s director of system operations, said during a recent stakeholder meeting that the alerts and advisories are becoming regular.

“That’s been really challenging. Thankfully, we’ve had good renewable resource penetrations [on peak days],” he said. “We’ve teetered on [energy emergency alert 1] where it’s been really close, and a small contingency might have put us there, but we were able to make it through. That’s what I’m really calling the new normal.”

Tropical Storm Offers Relief to Texas

Tropical Storm Harold gave Texas a bit of a reprieve with rain in the south and cloud cover elsewhere. Average hourly demand failed to reach 80 GW for only the second time since July 29.

Austin had a 45-day streak of 100-plus temperatures broken when the thermometer only reached 99 degrees. However, Dallas extended its streak of 100-plus days to 41 Tuesday after having set an all-time high of 109 last week.

The cooler weather will be short-lived. ERCOT is projecting demand to once again approach record levels through Thursday.

The ISO did set another weekend peak demand mark Sunday at 85.12 GW, not far from the system’s all-time high of 85.44 GW. The ISO was forced to call for voluntary conservation when a large thermal unit went offline.