Independent entities cannot review and challenge tank congestion charges and revenue credits in the annual true-up process for the cost-of-service agreement between ISO-NE and the Mystic Generating Station, FERC ruled Friday (ER18-1639).

The commission also ruled against a request by a group of municipally owned utilities for additional audit disclosures related to the agreement, saying that ISO-NE’s existing audit procedures and disclosures are adequate.

The ruling responded to both the municipal utilities’ request for additional information and a request for rehearing by Constellation Mystic Power, which argued against FERC’s determination that “interested parties” can review and challenge the true-up. That “could be read to allow interested parties to obtain information that is commercially sensitive, and that poses a security risk,” the company said.

In contrast, the utilities argued that the significant costs of the agreement — which they estimated to be more than $400 million over the first 10 months — necessitated the disclosure of additional information to allow interested parties to challenge the credits and charges. (See Public Power Groups Seek Information on Mystic Agreement.)

Credits account for revenues that Mystic earns from sources other than the agreement, while tank congestion charges refer to any costs associated with the increased need for uneconomic self-scheduling or short-term vaporization LNG.

FERC sided with Constellation, reversing its previous determination and also agreeing that shared revenue from third-party natural gas vapor sales should not be included in the true-up process. The commission said these contested issues are inconsistent with the Mystic agreement’s true up process because “none of them are projected in advance, but rather they are each settled and audited on a monthly basis.”

The commission also denied the municipal utilities’ request for additional audit information, which is “not supported by the Mystic agreement and unnecessary, given the attention that ISO-NE, its auditors and the Market Monitor give these items on a regular basis.” The request “goes beyond the terms of the Mystic agreement, which vests ISO-NE with audit rights and requires ISO-NE to maintain the confidentiality of audit-related information.”

“Allowing all interested parties to review Mystic’s revenues and revenue credit could require disclosure of proprietary information about Mystic’s actual fuel costs,” FERC wrote. “We recognize the potential competitive harm to Mystic, Constellation LNG and the market that could ensue from the disclosure of unmasked, offer-specific, commercially sensitive information to third parties.”

FERC wrote that it is “sympathetic” to the concerns about the high costs of the Mystic agreement, but “there is no record evidence that the Mystic agreement formula rate is being improperly executed.”

“The existing cost review and audit processes, which are facilitated by ISO-NE, its auditors and the Internal Market Monitor … are sufficient to ensure that Mystic adheres to its filed rate,” FERC added.

FERC also accepted a proposal ISO-NE had filed as an intermediate solution, which stopped short of the broad disclosures requested by the public power groups but allows for releasing redacted audit reports, providing summaries of its discussions with Constellation about fuel supply decisions, and making a member of Levitan & Associates’ tank congestion audit team available for questions at several points throughout the agreement.

“We are pleased that the commission has recognized the significant information the ISO has made available regarding the ongoing auditing of Constellation’s fuel supply decision,” an ISO-NE spokesperson told RTO Insider via email. “We will continue to work with Constellation and our stakeholders on ways to provide additional information while protecting confidentiality.”

Hit by one storm after another, Vermont’s largest electric utility is proposing to install battery systems in certain customers’ homes as a resilience measure.

The plan is one piece of Green Mountain Power’s 2030 Zero Outages Initiative, which it calls a first-in-the-nation combination of hardening power lines, creating community microgrids and placing distributed storage assets strategically across its service area — then crunching external data to find the best strategy against power outages on each of 300 circuits.

GMP has been promoting in-home storage units for eight years, and its residential customers now have 5,000 battery units in their homes. The customer waitlist stood at 1,200 when the Vermont Public Utility Commission in August lifted the enrollment cap on two GMP programs to promote in-home storage.

Under one program, GMP leases Tesla Powerwall batteries to customers for 10 years at a discount; under the other, GMP provides an up to $10,500 incentive to ratepayers who buy a system on their own.

In a petition to the PUC Monday, GMP proposes to spend $280 million to increase storm resilience (Case No. 23-3501-PET). Some $250 million would be used to harden 8 to 10% of GMP’s 10,000 miles of overhead lines — either by moving them underground or by protecting them with spacer cables or other devices.

The other $30 million would place battery units in some homes in what GMP calls Zone 4 — areas served by single-phase “last-mile” power lines in rural areas. Some parts of the mountainous state have sufficiently few customers per mile that moving power lines underground or even just hardening them would be less economical than installing batteries.

The utility would cover the cost of the batteries so individual homeowners who couldn’t afford the upfront cost of a battery wouldn’t be left behind.

Ratepayers would pick up the tab, although GMP plans to pursue federal funding.

Other pieces of the puzzle include trailer-mounted energy storage, demand-response-enabled EV chargers and electric school buses with V2G capability.

GMP said the unique aspect of the 2030 Zero Outages Initiative is that it takes all these pieces and overlays them with federal community vulnerability data, topography and other metrics to calculate the best resiliency strategy for each circuit.

Utilities and grid operators nationwide are wrestling with the long-term implications of the clean energy transition and the immediate impact of extreme weather blamed on climate change.

In Vermont, the storms have been coming fast and furious. GMP has spent $115 million on repairs from major storms in the past decade, $45 million of it in just the past year. The three storms with the highest number of outages in GMP history have all hit in the past 12 months.

That is unsustainable, GMP said. It needs to accelerate resiliency efforts so future storms cause less damage and fewer outages.

GMP President Mari McClure said in a news release Tuesday: “We all see the severe impacts from storms, we know the impact outages have on your lives, and the status quo is no longer enough. We are motivated to do all we can to combat climate change and create a Vermont that is sustainable and affordable, but we must move faster. Together with our customers, regulators, our communities and that Vermont spirit that manages to innovate despite all odds, we have all we need to revolutionize the energy system and ensure a stronger, more affordable Vermont.”

If the PUC approves, the $280 million would be spent over the next two years. GMP said it expects the improvements to start yielding savings on storm recovery costs by 2026 and will submit a request for an expanded second phase of improvements to be made through 2030.

In a promising sign, the first 50 miles of power lines relocated underground came through the recent series of major storms undamaged and trees that fell on new spacer cables caused no outages.

GMP serves more than 270,000 homes and businesses in Vermont. It is by far the largest electric utility in the state, and the only one owned by investors.

A spokesperson told NetZero Insider Tuesday that GMP is confident it can secure enough storage units, even amid surging demand for batteries. It already has been working with suppliers.

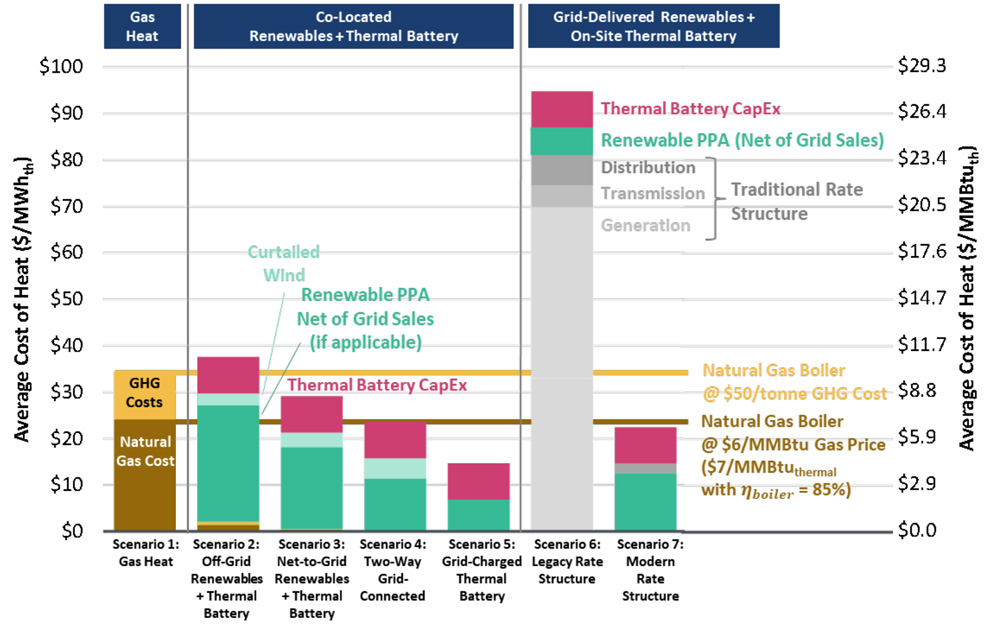

Thermal energy storage (TES) powered by renewables could be a flexible, cost-effective way to decarbonize heavy industry in the United States, if such projects could access wholesale power prices and rate structures based on cost causation, says a new report from the Renewable Thermal Collaborative and Center for Climate and Energy Solutions.

The technology essentially is a two-fer, capable of providing the high-temperature heat needed for a range of so-called “hard-to-abate” industrial processes, as well as vital grid-support services to ensure power system reliability, according to the report, authored by industry consultants The Brattle Group. Like other storage technologies, it also can be used as a hedge against volatile fossil fuel prices, acting as a sponge to absorb excess renewable power during times of high production and low costs, and discharging during periods of peak demand.

“If widely deployed to their maximum potential, renewable-powered thermal batteries could displace the entirety of the emissions associated with industrial heating demand, amounting to 779 million metric tonnes (MMT, also equivalent to 1 Megatonne) of carbon dioxide equivalent (CO2e) emissions per year in the United States, or approximately 12% of total economy-wide GHG emissions.” the report says.

Globally, renewable TES could slash industrial CO2 emissions by 6,000 MMT per year, or 14.5% of all energy-related emissions, the report says.

A first step for scaling the technology is simply getting it on the radars of critical stakeholders, from potential industrial users to utilities and state and federal regulators, the report says. For example, policymakers and regulators should classify renewable TES as a “qualified technology solution that can be considered equally alongside other alternatives in” state and federal studies examining economy‐wide and grid decarbonization pathways, the report says.

Similarly, the report calls on grid operators to recognize the attributes of renewable TES as a technology that can ramp within minutes or even seconds and operate as either a dispatchable or flexible resource.

Speaking during a recent webinar on the report, Phillip Stephenson, vice president of business development for startup Electrified Thermal Solutions, praised the study for “finally laying out what I think is a great secret we want people to know. … We actually just need to change the rules a bit to match costs and benefits to make this work.

“We are not asking for dumping subsidies on us to unleash a lot of decarbonization and [show] how real these benefits are and how widespread the benefits can be in terms of the grid, which means really [for] the energy transition and society,” he said.

‘The Right Thing to Do’

Thermal energy storage is based on the same basic technology as a toaster or electric stove. Electric power is run through a “resistive material” ― for example, some form of carbon or graphite that impedes power flow, creating heat that can be stored.

The technology has long been used in space and water heating applications, especially in district heating or combined heat and power systems, to capture waste heat for heating and cooling. Such systems often store heat in vats or other large containers of water.

But the high temperatures needed for heavy industry — such as glass, paper and chemical production — typically have required the combustion of fossil fuels. Many companies in these sectors anticipate decarbonizing their factories either by switching from fossil fuels to green hydrogen or cutting their fossil fuel emissions with carbon capture and storage. (See Summit Showcases New Technologies to Accelerate Industrial Decarb.)

Instead, startup companies like Electrified Thermal and Antora Energy have developed technologies that can turn renewable power into high-temperature heat that is stored in special bricks or carbon blocks and released as needed. At present, these and other renewable thermal storage companies can provide heat of up to 750 degrees Celsius, or 1,382 degrees Fahrenheit, high enough to cover 75% of all industrial heat demand, the report says.

Antora, a startup with funding from Bill Gates’ Breakthrough Energy Ventures, recently announced a pilot project in California where the company’s system produced heat at 1,800 degrees Celsius, or more than 3,200 degrees Fahrenheit, high enough to cover almost any industrial process.

Greg Wellman, technology manager of decarbonization for Eastman Chemical Company, talked about the commercial benefits of renewable TES for his firm, a Fortune 500 company producing a range of “specialty materials,” such as bird-friendly glass for building facades.

Spun out of Eastman Kodak in the 1990s, the company is looking at thermal storage because it fits well with its existing natural gas-based infrastructure, and the new systems are modular, meaning they can be sized to try out on a single process or to produce industrial heat for a whole factory, he said.

Another reason Eastman is looking closely at the technology is its potential for price parity with natural gas in the near future, Wellman said. “[When] you think about what’s the long-term trajectory of natural gas pricing, what’s the long-term trajectory of electron pricing … there’s going to be a compelling case to make these changes [to renewable TES], not just because it’s the right thing to do but also because it’s a financially right thing to do,” he said.

The Brattle report notes that for companies like Eastman, renewable TES could allow fuel switching, that is, keeping fossil fuel infrastructure, and natural gas, as backup generation to respond to price fluctuations or emergency events.

Stephenson said the technology also could be an attractive option for utilities anticipating new, higher peaks in energy demand as industrial customers seek to electrify their plants and processes. With renewable TES, industries could electrify “without having those peak demand impacts,” he said.

For utilities, the benefits include improved “economics on their entire system by being able to take all that new heat load coming from the customers … but tuck it under their existing peak by using only off-peak energy,” he said.

Depending on project configuration and rate structure, renewable thermal energy storage can be cost-competitive with natural gas. | RTC

Good for All Customers

Beyond raising industry awareness of renewable TES, scaling the technology will depend on getting it to price parity with natural gas, which, in turn, may depend on a range of factors, such as the configuration of individual systems, rate structures and access to wholesale power prices.

Price parity could vary across system configurations, the report shows, specifically whether the renewable power is located off- or on-grid, whether the system can export power to provide grid-support services or whether the renewable power is coming from the grid itself.

At present, the report says, the most cost-competitive configurations for renewable TES are for projects that “self‐supply or directly contract with a renewable power supplier in an off‐grid or partially grid‐connected status.”

But project configuration often is determined by the specifics of a customer’s site, said Nick Soncrant, Antora’s head of business development.

“If a customer is space-constrained, colocated, new-build renewables will be pretty tough to implement,” Soncrant said. “If a customer is in a renewable-dense region … where the price of power is competitive with natural gas, we can look to work with utilities either under their existing tariff or partner with them to develop a new wholesale market tariff.”

Such new “modern” rate structures are vital for renewable TES to successfully compete with natural gas, the report says. Traditional rate structures, which include generation, transmission and distribution fees, presume “the customer can’t change when they use power,” said Kathleen Spees, a Brattle Group principal and lead author of the report.

For renewable TES to pencil out, Spees said, will require “very principled ratemaking structures of cost causation. … You only apply costs that are really relevant and caused by this sort of customer, which are low because you can really optimize when you would withdraw any power from the grid with a thermal battery,” she said.

“The good news about these modern rate structures, of course, is that they are good for all customers,” Spees said. “They’re good to incentivize all customers to behave in ways that actually reduce costs to the power grid. There is just much more potential and capability to shape whether and when any consumptions patterns take place.”

The report points to two electric cooperatives, the Vermont Electric Cooperative and the Victory Electric Cooperative in Kansas, that have adopted new rate structures based on cost causation. The Victory co-op, for example, has a rate for industrial customers that, the report says, is “aligned with wholesale power prices, consumption during system coincident peak demand and other (smaller) cost components, including local delivery charges.”

841 and 2222

Whether renewable TES projects will be able to access wholesale prices raises another key question: Is the technology covered under either FERCOrder 841 or Order 2222, regulations that require, respectively, that energy storage and distributed energy resources be able to participate in wholesale power markets.

To date, Spees said, “that question has not been specifically asked or answered” and would require one or more affirmative rulings from FERC.

The fact that renewable TES can provide multiple value streams, both storing and discharging power, adds another layer of complexity to the issue, said Jordan Kearns, vice president of project development for Antora Energy.

“We … and other folks in the space have systems that can produce electricity back from these thermal batteries, and it’s kind of hard to argue that’s not a battery that would be covered under 841 or 2222,” Kearns said in an interview with NetZero Insider. “But then how do you treat the heat [that] goes off of it? Are you going to be punished for capturing and … putting that waste heat to good use?”

The report offers several recommendations for grid operators and FERC to ensure renewable TES can participate on a level basis in energy, capacity and ancillary markets, including:

Having the same size requirements for standalone batteries and renewable TES, with a minimum of 100 MW.

Establishing “distinct participation models” for different renewable TES configurations, such as standalone thermal batteries with controllable demand, colocated renewable electricity and thermal battery systems that can be scheduled to charge or discharge power, and TES systems that receive renewable power from the grid.

Allowing thermal batteries to access wholesale energy prices based on the same locational marginal price available to generation resources and electric batteries.

NYISOannounced on Tuesday that the state broke its hourly wind generation record Sunday, generating 1,939 MW from 28 wind power facilities.

The ISO said that meant wind energy met 12.9% of New York state’s electricity demand between 3 and 4 p.m. that day. The previous record of 1,897 MW was set Feb. 17, 2022, during the 1 a.m. hour.

“Wind generation is an important part of the diverse energy mix that helps maintain system reliability for consumers across the state,” NYISO CEO Rich Dewey said in a statement. “While there’s much more work to be done to decarbonize our system, this new record demonstrates wind energy’s increasing contribution to the state’s climate goals.”

“New York’s clean energy transition is ensuring more homes and businesses across the state are powered by renewable energy sources like land-based wind — a shift that is especially important during times of peak demand,” said Doreen Harris, CEO of the New York State Energy Research and Development Authority.

The milestone comes as offshore wind developers exit the power purchase agreements off New England and seek to renegotiate them amid high inflation and supply chain constraints. (See Park City Wind to Cancel PPAs, Exit OSW Pipeline.)

None of New York’s four OSW projects under development have made that move yet, but their developers have said they may be forced to do so if the Public Service Commission does not grant NYSERDA’s request to adjust the reference price for offshore wind renewable certificate contracts to account for inflation. The PSC is set to rule on the matter Thursday (15-E-0302/18-E-0071).

“Unforeseeable economic forces — including unprecedented global supply chain bottlenecks, high inflation [and] rising interest rates, along with permitting and grid delays — have eroded the financial viability of” Empire Wind and Beacon Wind, their developers told the PSC in comments filed Friday, “to the point where contract restructuring is required to permit those capital-intensive projects to move forward. Notwithstanding these severe market shocks, however, the projects remain the most cost-effective means of fulfilling the [state’s] renewable energy mandates.”

In the same docket Friday, the PSC granted a one-year extension for NYSERDA to create an implementation plan for Tier 4 of its renewable resource procurement program. (See NYSERDA Can’t Meet Deadline to Design New REC Plan.)

SACRAMENTO — Nine of the world’s largest manufacturers and suppliers of building heating and cooling equipment have signed an agreement to support California’s goal of having 6 million electric heat pumps installed by 2030.

The deal was announced at a two-day Summit on Building Electrification co-hosted by the California Energy Commission and the Electric Power Research Institute (EPRI), held at the California Natural Resources headquarters in Sacramento.

The broad public-private partnership is being convened in a move CEC member Andrew McAllister said will be “critical in aligning policy and reality.”

The goals of the program, McAllister said, are to:

create the manufacturing capacity to help achieve the state’s goal of installing 6 million heat pumps by 2030;

ensure heat pumps are good citizens of the electric grid by enhancing efficiency and incorporating load flexibility;

collaborate with the CEC to develop a public-private partnership to facilitate policy and market support to bring heat pumps into the mainstream.

“The pledge builds on policies and programs already underway at the Energy Commission, the [California] Air Resources Board, the [California] Public Utilities Commission and the Governor’s Office of Business and Economic Development, GO-Biz. The activities are supported by the California Climate Commitment and federal Inflation Reduction Act, which combined will provide $1.3 billion for efforts to reduce emissions from buildings,” McAllister said.

A body will be convened that includes the nine manufacturers plus other companies in the supply chain, public interest groups, utilities, labor groups and state agencies. McAllister said the partners in the group could “collaborate on initiatives focused on, but not limited to, consumer awareness, contractor training, product availability, performance, efficiency, load flexibility, refrigerant management, data, equity and financing.”

“We can’t do it alone. It takes strengths of partnerships like this to achieve the kind of massive market transformation required to reach our goals,” he said.

The manufacturers are AO Smith, Carrier, Daikin, Johnson Controls, Lennox, LG Electronics, Mitsubishi Electric Trane HVAC US, Rheem Manufacturing and Trane Technologies.

Driving consumer acceptance is a key part of the program, he said. “This new commitment will ensure that grid-friendly heat pumps are widely available and can help consumers understand why they’re a better choice for both comfort and for the climate. The partnership will promote a comprehensive consumer awareness campaign to educate consumers on the benefits of electrification and work on ways to ease the purchasing process.”

The group will periodically report on progress toward meeting the goal of having 6 million heat pumps installed in buildings across California by 2030.

FERC responded to ISO-NE’s request for rehearing on its Order 2222 compliance Friday, agreeing to delay the required timing of implementation while providing a clarification about the responsibility and role of distributed energy resource (DER) aggregators and utilities in providing ISO-NE with metering information and data (ER22-983-002).

Order 2222 directed RTOs and ISOs to remove barriers for aggregations of DERs to participate in wholesale markets. ISO-NE filed its initial compliance in February 2022, and FERC partly accepted and rejected it in March 2023. (See FERC Gives ISO-NE Homework on Order 2222.) ISO-NE requested a rehearing at the end of March.

A significant portion of FERC’s order Friday focused on its requirement that DER aggregators be responsible for reporting the necessary metering information to their respective RTO or ISO. In ISO-NE’s compliance filing, the organization proposed to task the host utility — which refers to either a transmission owner or a distribution utility — with this responsibility.

“Shifting the meter reporting role for [DER aggregations] to the DER aggregator would treat DERAs differently from all other resources participating in New England Markets and place them at a disadvantage relative to all other resources,” ISO-NE wrote in its March request for rehearing.

ISO-NE also interpreted FERC’s order in March to require the exclusion of host utilities from the flow of metering information from the DER aggregator to the RTO. ISO-NE argued that because host utilities typically are in charge of metering, giving the responsibility to the DER aggregator while excluding the utility from the process would be difficult to implement and would require new infrastructure and tariff changes.

In its response to the rehearing request, FERC maintained that the DER aggregator is responsible for providing metering information to ISO NE.

The commission said it disagreed with the “underlying interpretation upon which ISO-NE bases its rehearing request” and said Order 2222 “does not preclude metering data coming from or flowing through the host utility.”

“Metering data may come from or flow through distribution utilities if ISO-NE coordinates with distribution utilities and relevant electric retail regulatory authorities to establish protocols for sharing such metering data and explains how such protocols minimize costs and other burdens and address concerns raised with respect to privacy and cybersecurity,” the commission wrote.

FERC said this clarification would preclude the need for the significant metering changes and burdens highlighted by ISO-NE in its rehearing request.

Also in Friday’s order, FERC sustained part of the March order directing ISO-NE to explain or alter its measurement requirements for some classes of behind-the-meter DERs.

Time Change

In ISO-NE’s initial compliance filing in 2022, the RTO wrote that it would need a response from FERC no later than Nov. 1, 2022, to include distributed energy capacity resources (DECRs) in Forward Capacity Auction (FCA) 18, which is scheduled for 2024 affecting the 2027/28 capacity commitment period. Since FERC did not make a determination until March 2023, ISO-NE argued in its rehearing request that it should not be required to include DECRs in FCA 18.

FERC accepted this request Friday, noting ISO-NE has proposed a new effective date that would require DECRs to be included in FCA 19.

Commissioner Christie’s Dissent

Commissioner Mark Christie dissented with Friday’s order, as he did with the commission’s order in March regarding ISO-NE’s compliance filing.

“Today’s order represents yet another example demonstrating that Order No. 2222 has created nothing short of an incomprehensible quagmire bearing a substantial price tag that will inevitably add to the rising power costs already faced by consumers,” Christie wrote.

He expressed his concern that the order does not adequately address ISO-NE’s concerns and will require “yet another return to the drawing board for ISO-NE and its market participants.”

Christie added that the order “uses the ‘clarification’ as a sword to dispense with the rehearing request, but also as a shield from providing substantive explanation on how this ‘clarification’ addresses each of ISO-NE’s problems and concerns.”

California needs both building-focused and material-focused approaches to driving down the embodied carbon in new construction if it is to reach the state’s net zero goals, according to a new study.

Policies such as state and local building codes requiring low-carbon materials need to be adopted along with strategies such as reusing existing buildings and minimizing new construction, the Embodied Carbon Reduction Roadmap report, authored by Arup, a sustainable development consultancy, for the Natural Resources Defense Council (NRDC) found.

The study quantified the reduction potential of strategies for new residential and commercial construction in California and the state’s ability to meet its 2045 net zero goal under Executive Order B-55-18, or its more aggressive 2035 net zero goal under AB 2446. The study focused on California “due to its capacity, leverage and track record for lowering barriers and risks for others in the nation and around the world.”

A building’s embodied carbon is the emissions related to materials extracted, processed and transported to the site as well as generated by the construction process and its end of life. It does not include emissions related to operating the building, which are about three times the embodied energy over a building’s lifetime, according to a study on reducing embodied carbon emissions in the building construction sector released last week. (See New Buildings May be the Next Climate Solution.)

The NRDC report grouped embodied carbon reduction strategies for buildings by those that optimize reductions at the project level, in the building systems or at the materials procurement level. “A building-focused approach uses whole building life-cycle assessment to evaluate performance. A material-focused approach uses environmental product declarations to evaluate performance.”

The study found that in the near term, optimizing the project provided the greatest opportunity to reduce the embodied carbon of buildings, while in the long term, optimizing the building materials procured made the biggest impact. However, if new, lower-carbon materials are brought to market more quickly, then optimizing procurement will make the biggest impact in the near term as well.

The highest impact strategy to cut buildings’ embodied carbon is to use low-carbon concrete, though no single strategy will enable the state to reach its net zero goals. Minimizing new construction, reusing buildings and buying low-carbon steel and insulation are the next most effective strategies to reduce new construction’s Global Warming Potential (GWP).

As far as policies go, those that encourage clean procurement have a larger impact than building codes, though both are substantially bigger levers than zoning, climate commitments, training and education or waste and circularity policies.

Local Policies Vital

The report called for more policies to encourage design and construction practices that lower whole-building emissions.

“While many emerging policies address material-level carbon performance, it is recommended that more focus goes into policies that encourage project- and building-scale reductions. This study has shown the gap and opportunity of policies focused on planning and design of whole buildings. Advancing building-focused policy approaches at the same time as materials-focused approaches would accelerate the buildings sector towards a zero-carbon future.” the report said.

It’s not just state-level policies that are important; city and county policies can be critical to driving building improvements and can play a role in raising the bar. In 2019, Marin County was the first local jurisdiction in California to adopt embodied carbon requirements in its base building code amendments, and since then, other jurisdictions have adopted code amendments and “stretch codes” that go even further, such as requiring all-electric new construction. California has approved building changes to include mandatory embodied carbon requirements in the state’s green building code, CALGreen, which should go into effect in 2024.

“Policies impacting building embodied carbon are vast and applied ranging from the hyper-local level to the state level. Some policy types more directly prescribe embodied carbon performance, while other policy types have indirect impacts to embodied carbon. The broad range of policies presents both a challenge and opportunity, in that multiple levers can be explored to enact change.”

Policies requiring the use of lower-carbon materials impact both public and private developments, and while they influence a building’s design, often it is the contractor who is responsible for procuring materials that conform with the policy, the report noted.

VALLEY FORGE, Pa. — The PJM Market Implementation Committee endorsed two proposals intended to include multi-schedule modeling in the market clearing engine (MCE) without causing performance impact because of the large number of additional offers the engine would have to consider. (See “Discussion Continues on Multi-schedule Clearing in The Market Clearing Engine,” PJM MIC Briefs: Sept 6, 2023.)

PJM’s proposal, which would create a formula to select the offer expected to produce the lowest total dispatch cost and forward only that offer to the MCE, received the greatest amount of support and will be considered the main motion before the Markets and Reliability Committee. A joint PJM and GT Power Group proposal was also endorsed by the committee and would select resources’ cost-based offers when they fail the three-pivotal-supplier (TPS) market power test and their parameter-limited offers during emergency conditions.

The problem statement that PJM brought forward in December 2022 states that each resource schedule entered into the MCE is modeled as a logical resource. When paired with the number of configurations that combined cycle and storage resources can enter schedules for, the introduction of multi-schedule modeling would cause an exponential increase in the number of logical resources the engine would have to process, potentially leading to untenable increases in computational times. All five proposals aimed to reduce the number of schedules that are submitted to the MCE prior to the optimization process.

Three proposals from the Independent Market Monitor, including one jointly sponsored with GT Power, failed to receive majority support. During first reads in September, Deputy Monitor Catherine Tyler told the MIC that the proposal’s goal was to solve the performance issues that multi-schedule modeling is expected to pose while also improving market power mitigation. She also argued that the PJM proposal could be dispatched on schedules that don’t match the most cost-effective fuel and that it would allow generators with market power to raise energy prices by using high markups and to extract uplift using inflexible parameters.

The first Monitor proposal would combine the lowest offer points and most flexible parameters from resources’ price- and cost-based offers under certain scenarios; impose offer capping and parameter limits to all resources that fail the TPS test; and apply parameter limits to capacity resources during emergencies. The Monitor’s second package would do the same as above but would use the status quo rules for resources with multiple cost-based offers.

The joint Monitor and GT Power proposal would commit resources that fail the TPS test and have multiple offers to operate based on the fuel that the generation owner expects to use in each hour of the day. Tyler said that any generators not submitting the most efficient offer may be considered to be engaging in market manipulation.

Creation of Fifth CONE Area Endorsed

Stakeholders endorsed a joint proposal from PJM, the Monitor and E-Cubed Policy Associates to create a fifth cost of new entry (CONE) area for the Commonwealth Edison region.

The proposal is intended to allow the CONE for the ComEd region to reflect the expected shortened lifespan of the reference resource, a combined cycle unit, under the Illinois Climate and Equitable Jobs Act. (See “Fifth CONE Area Under Consideration,” PJM MRC/MC Briefs: Sept. 20, 2023.)

PJM’s Gary Helm stated that the new CONE value for ComEd will be $201,714/MW-year, compared to $197,800/MW-year in CONE area 3, from which the existing area would be broken out of under the proposal. All other variables, such as labor costs, will remain the same, but they may be revised under the next Quadrennial Review.

E-Cubed had previously sponsored a proposal to create an automated process for adding new CONE areas when local or state factors affect key parameters of the reference resource, such as asset lifespan, or when they may imply a different reference resource than the one PJM has designated.

Capacity Obligations for Forecasted Large Load Adjustments

Stakeholders approved an issue charge brought by Dominion Energy and American Electric Power to consider changes to how capacity obligations are allocated following a large change in the load in one or a small number of load-serving entities.

Josh Burkholder of AEP said that the capacity obligation accounting for such a change in load is allocated across all entities within the zone, regardless of whether they are under fixed resource requirement (FRR) or Reliability Pricing Model (RPM) rules.

Unlike standard changes in load, the problem statement argues that large load customers, such as data centers, tend to be geographically concentrated in one region that can be tied to one or a handful of LSEs. It states that the issue is isolated to forecasted loads, as once they come online, their actual consumption is accounted for in the capacity obligation assigned to the LSE.

The issue charge was revised following a first read at last month’s MIC to revise the focus from being on large load additions to adjustments, to reflect that forecast reductions in load can have a similar effect. The scope was also clarified to include the assignment of obligations between RPM and FRR markets as well as individual LSEs. The stakeholder process was also changed to the full consensus-based issue resolution (CBIR) process, instead of the abbreviated CBIR Lite pathway, and the estimated timeline was revised to four months with the goal of having changes that can be implemented in the 2025/26 Base Residual Auction (BRA) if feasible.

Burkholder said the issue charge would not change the settlements process but instead focus on how capacity obligations for identifiable forecast large loads are allocated. Settlements are in-scope only to avoid any unintended consequences.

Calpine’s David “Scarp” Scarpignato made the case that the issue extends beyond load changes in regions served by RPM entities resulting in changes to the capacity obligation for FRR resources, saying that a significant change in load within an LSE whose footprint lies in multiple transmission zones can result in that impact bleeding across zones.

PJM Reviews Board of Managers CIFP Letter

PJM Vice President of Market Design and Economics Adam Keech said the RTO is on track to make a FERC filing by the Oct. 13 deadline the Board of Managers set in a letter announcing a slate of capacity market changes resulting from the Critical Issue Fast Path (CIFP) process it initiated in February. (See PJM Board Releases Outline of Capacity Market Changes.)

To meet the aim of having changes that can be implemented for the 2025/26 BRA, Keech said FERC approval would be required by early February to leave time for pre-auction activities and for market participants to prepare. Portions of the changes being proposed involve processes that begin toward the start of the pre-auction activities, meaning an order is needed before work can substantively begin.

Keech said two approaches that PJM could take when drafting the filing would be to either ask the commission to delay the auction until an order is released, or to state that the RTO will begin with pre-auction activities under the current rules unless directed to do otherwise. Any delay to the 2025/26 auction would likely mean changes to the timeline for subsequent auctions as well because of how tightly packed together they are.

PJM is also discussing whether it is best to proceed with a single filing encompassing all of the proposed changes, or to break it into two filings, grouping together changes that staff believe would have to be made as a package. Keech said he believes that changes to performance assessment intervals would have to be linked with the market seller offer cap because there’s a connection between the two with the eligibility to receive Capacity Performance bonus payments.

PJM Senior Counsel Chen Lu said staff considered waiving the RTO’s right to preclude the commission from conditioning approval of a Federal Power Act Section 205 filing under NRG Power Marketing v. FERC, but they determined that not all of the components of the proposed changes are severable.

Keech said the board is currently deliberating the direction and best forum to hold further discussions of issues that are not expected to be resolved through the filing, such as a seasonal capacity market.

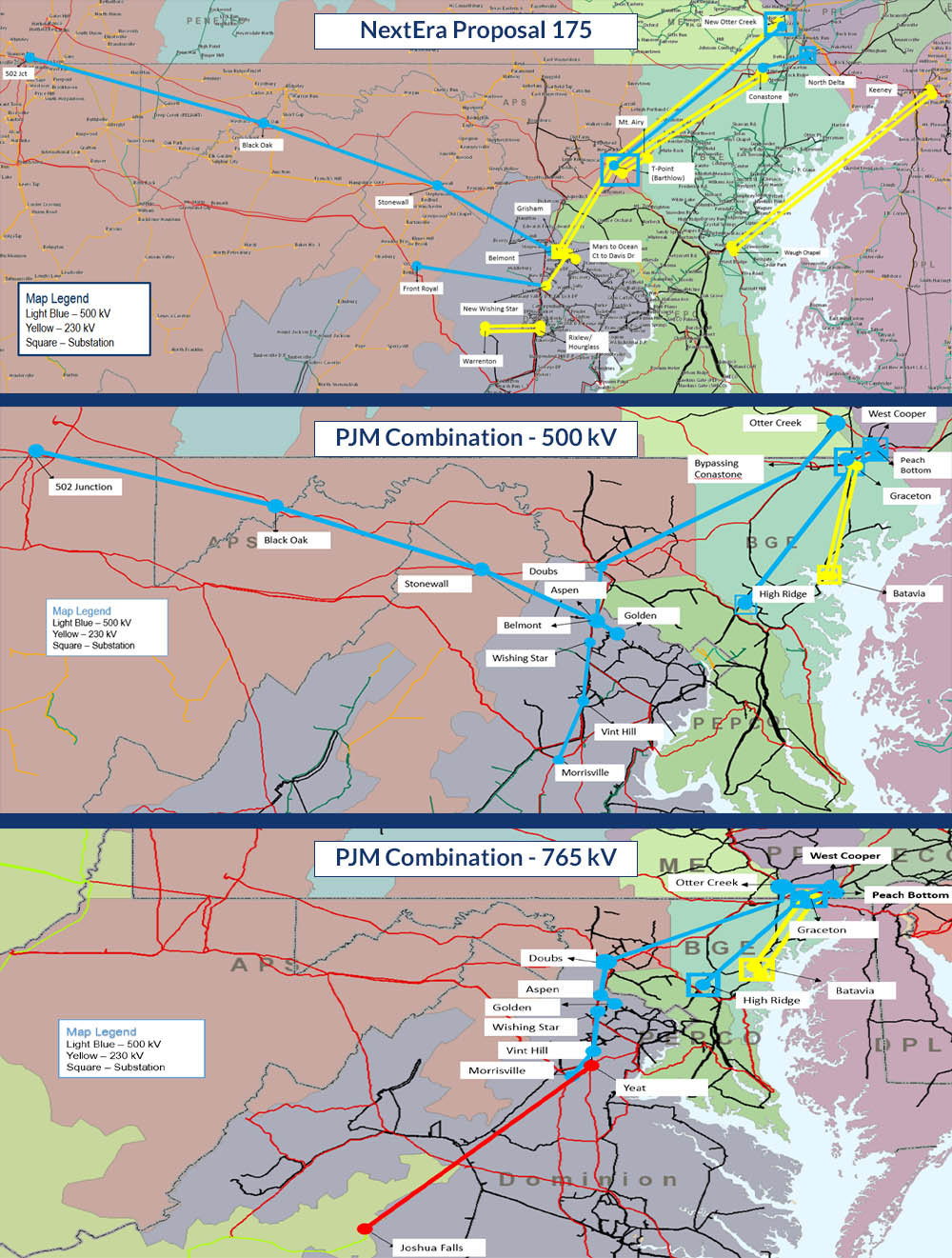

PJM last week presented a shortlist of three scenarios of transmission upgrades to address needs identified in the 2022 Regional Transmission Expansion Plan (RTEP) Window 3. (See “Update on RTEP Windows,” PJM PC/TEAC Briefs: Aug. 8, 2023.)

“There is a lot of interest in this particular planning window. … This is a major expansion of our transmission system,” PJM Senior Vice President of State Policy and Member Services Asim Haque said during an Oct. 3 meeting of the Transmission Expansion Advisory Committee (TEAC). “We’re facing some serious changes to the electric grid in this area based on increase in the electric demand and retirements of fossil fuel generators.”

All three scenarios would expand the 500-kV grid, and potentially construct the first 765-kV line in the Dominion region, to meet growing data center load and generation retirements such as the 1,295-MW Brandon Shores plant. PJM Executive Director of System Planning Dave Souder said more information about the potential of a reliability-must-run contract being reached with Talen Energy should be available around the end of the year. (See “Brandon Shores Deactivation to Require $786M in Grid Upgrades,” PJM PC/TEAC Briefs: June 6, 2023.)

PJM received 72 proposals from 10 entities, portions of which were combined to form two scenarios. Only NextEra’s proposal #175 was selected as a shortlisted scenario without PJM modification. PJM’s Sami Abdulsalam said the RTO plans to bring one of the shortlisted scenarios to stakeholders for a first read Oct. 31 and to the board for approval in December.

PJM shortlisted a NextEra and two aggregated proposals to meet transmission needs identified in its 2022 Regional Transmission Expansion Plan (RTEP) Window 3. | PJM

The 765-kV line proposed in one of the two aggregate PJM scenarios would begin at the Joshua Falls substation and run north to the data center alley in Loudoun County, Va.

One of the PJM plans would construct a 765-kV line between the Joshua Falls and Yeat substations, bringing power into Loudoun County from the south. Additional transmission capability would also be constructed to the northeast, tapping into the 500-kV grid at Peach Bottom.

PJM’s other scenario focuses on expanding the 500-kV grid by building new lines from northern Virginia out to Peach Bottom to the northeast and the 502 Junction substation to the northwest.

Both scenarios include additional 500- and 230-kV lines that would be built in the BGE zone to meet some of the expected need created by the Brandon Shores retirement.

The NextEra scenario would follow a similar 500-kV pathway between the 502 Junction and the data center alley, as well as several 500- and 230-kV lines to the northeast routing through a proposed Barthlow substation and continuing to the Conastone and New Otter Creek facilities.

Two 230-kV lines would be constructed between the Keeney substation on the Delmarva Peninsula, across the Chesapeake Bay and connecting to the Waugh Chapel substation in the BGE area.

Abdulsalam said each of the scenarios comes with positives and negatives. The NextEra scenario would avoid modifications to the Doubs substation, which has become the terminus for an increasing number of lines, while the Barthlow substation would have nearly a dozen lines tying into it. The scenario would also require significant acquisition of new rights of way and the component running a line under the Chesapeake could pose voltage concerns in BGE, as well as environmental and permitting concerns.

The 500-kV scenario offers the advantage of avoiding disruption to the Conastone substation and having strong cost containment for the component constructing a line between Doubs and Otter Creek. The 765-kV plan would relax flows in the north with the addition of the higher voltage transmission proposed in the south and would add to the backbone capability in Dominion. Siting, permitting and procuring equipment for a 765-kV line comes with higher risk, but Abdulsalam said the 500-kV components of the scenario could provide short-term relief while the 765-kV is built.

Abdulsalam said the proposals contain commonalities that demonstrate a general understanding that additional transmission capability will be needed to move energy from the east to the west, augmented by transmission either from the south or northwest.

PJM’s Nebiat Tesfa said planning staff used a combination of NextEra, Exelon, FirstEnergy and Dominion proposals as a starting point to construct its aggregate proposals, in some cases working with proposing entities to break out individual components to combine with portions of other proposals. Analysis of combining several LS Power, Transource and NextEra proposals found a larger number of violations in the 2028 case.

Of the 72 proposals, 50 involve greenfield development of new lines, while the remainder are upgrades or construction within existing rights of way.

PJM’s characterization of the impacts and risks that greenfield proposals carry was disputed by several residents who live in the communities some of the projects would pass through. They argued that expanding rights of way to construct lines paralleling existing infrastructure would have a larger impact than is represented in PJM’s analysis and that the extent of the amount of greenfield was underplayed.

The window contains models for both 2027 and 2028, with the primary differences being that the latter includes more deactivations, including Brandon Shores, and adjustments to how resource dispatch is reflected in the analysis. Both the Brandon Shores retirement and the changes to block dispatching came after PJM had released the 2027 case, but before the following year had been finalized. (See “Load Forecast for Northern Virginia Data Centers Continues to Climb,” PJM PC/TEAC Briefs: Jan. 10, 2023.)

Exelon’s Alex Stern encouraged PJM to reach out to both the relevant incumbent transmission owners and state commissions regarding any non-incumbent proposals that include underbuilding on existing lines, particularly if it could cause states to lose jurisdiction. Incumbent TOs are also likely to have more detailed insight into anticipated needs in their region and may have a use for the underbuilding capability they were planning to use in the future.

After an initial assessment of the potential of each of the 72 proposals, PJM created an initial shortlist for more detailed analysis of their cost estimate, cost containment, scheduling, constructability, brownfield and outage coordination risks. The risk assessment also considered permitting, potential environmental issues and public opposition to past projects.

BOSTON — With construction underway for the country’s first large offshore wind projects, government, nonprofit and industry representatives from across the U.S. came here to discuss the industry’s progress and prospects for the American Clean Power Association’s Offshore WINDPOWER conference.

The slogan for the conference (“STEEL IN THE WATER. PEOPLE AT WORK.”) — which was featured prominently on the merchandise, the pre-conference trailer video, and screens and posters throughout the convention center — invoked this major first step forward for the industry.

There was great uncertainty about when the next wave of steel will hit the water on the East Coast and the people these projects will employ will get to work. The developers for Massachusetts’ Commonwealth Wind and SouthCoast Wind projects backed out of their power purchase agreements in recent months: Avangrid reached an agreement at the start of this month to exit the PPAs for its Park City Wind project in Connecticut; Rhode Island’s electric distribution company rejected the only bid from its last solicitation; and four New York projects under active development are in limbo as they seek better terms for their contracts.

While developers can rebid projects that have canceled their PPAs at future auctions, the question remains whether they can find a price that states and utilities deem acceptable to pass on to ratepayers. But speakers at the conference argued that it was only a matter of when, not if.

At a panel featuring state legislators from Massachusetts and California, Massachusetts Rep. Jeff Roy (D-Franklin), co-chair of the Joint Telecommunications, Utilities and Energy Committee, urged developers to send in strong bids for the state’s solicitation and boasted about “the most robust wind in the entire contiguous United States right here off the coast of Massachusetts.”

At the same time, Roy said, the state will be faced with difficult questions around “how much are we willing to spend” when the project bids are due at the end of January.

Supply Chain, Interest Rates and Inflation

“It’s easy to focus on the doom and gloom of the moment right now,” Sam Huntington, director of climate and sustainability at S&P Global, said at a panel on global economics and offshore wind. “There’s still a lot of room for optimism. … There’s just a tremendous commitment to this.”

The industry has been hit with “a perfect storm of supply chain snarls,” Huntington said.

Walt Musial, a principal engineer at the National Renewable Energy Laboratory, said cost pressures from high interest rates and expensive commodities like steel should subside in the coming years. However, “there’s still going to be this issue around supply chain deficits and the inability of suppliers to meet demands.”

As countries and developers across the world all look to scale up offshore wind at the same time, the panelists expressed worry that delays could push the next round of projects back into the 2030s.

In the long term, Musial said he remains confident about the industry, calling it a “cornerstone” of New England’s future electricity supply.

“With climate change as a background, we have to do this,” he said.

Søren Lassen, head of offshore wind research for Wood Mackenzie, called the supply chain issues the industry’s “greatest challenge.” He said the combined issues of supply chain constraints, high interest rates and inflation hit the nation’s industry right as it was trying to make the jump from a small, subsidized industry to the commercial scale.

Lassen said these setbacks could put national and statewide clean energy commitments in jeopardy: An August report by his firm found governments across the world (excluding China) would need to invest about $100 billion in the supply chain by 2026 to meet their 2030 offshore wind goals. (See Report Quantifies OSW Supply Chain Constraints.)

“We don’t think that’s feasible, to be frank,” Lassen said.

Supply chain constraints could also be the limiting factor for the size of offshore wind turbines, which have increased rapidly in recent years. While Huntington said that larger turbines could be the key to lower costs in the long term, Musial cautioned that further increases in blade sizes will only put additional stress on the existing supply chains.

Musial said that industry should “double down” on 15-MW turbines to flatten the learning curve and bring costs down.

For context, Vineyard Wind 1 is being constructed with 13-MW turbines, while Vestas has been testing its 15-MW prototype this year, and General Electric is developing an 18-MW prototype.

“Any attempt to go larger than [15 MW] will just delay progress,” Musial said.

On a panel about installation vessels, Graham Tyson of Crowley Wind Services said that the increase in turbine size is an obstacle to investing in new vessels.

Tyson said investors need “a good eight to 10 years of life out of each turbine class” to justify investment in a new vessel, and either overbuilding or underbuilding the size of the ship poses significant risks.

“You want to know that there’s work for it,” Tyson said.

Speakers throughout the conference called for more federal support for states and developers to help overcome the industry’s recent struggles.

“States cannot do this alone,” said Catherine Klinger Kutcher, director of the New Jersey Governor’s Office of Climate Action and the Green Economy, adding that the state remains committed to offshore wind.

In mid-September, the governors of Connecticut, Maryland, Massachusetts, New Jersey, New York and Rhode Island signed a joint letter asking President Joe Biden for additional federal help for the industry. (See Northeast Governors Ask Feds to Assist OSW Industry.)

“Without federal action, offshore wind deployment in the U.S. is at serious risk of stalling because states’ ratepayers may be unable to absorb these significant new costs alone,” the governors wrote, citing the cost pressures of inflation, lingering supply chain disruptions and Russia’s invasion of Ukraine.

The governors asked Biden for updated guidance on the available clean energy tax credits, a new revenue sharing program for offshore wind leases and a streamlined clean energy permitting process.

In her keynote speech to the conference, Massachusetts Gov. Maura Healey (D) emphasized the importance of federal support, calling for additional resources while applauding the steps that the Biden administration has already taken.

“We can only control so much as states,” Healey said. “We need all parts of the federal administration to work with us to understand that this is our moment.”

Others expressed concern about the effects a new president — presumably Donald Trump, whose name was often implied but infrequently mentioned by speakers — could have on the industry and clean energy efforts more broadly.

Stakeholders should make the best possible use of the Inflation Reduction Act, said Damian Bednarz, managing director of Attentive Energy. “We cannot take any of this for granted,” he said.

SouthCoast CEO Francis Slingsby said stakeholders must specifically push to expedite clean energy permitting processes under the current administration and “make hay while the sun shines.”