Utility-scale solar construction reached record levels across the United States in 2023 and its cost continued to decline, the Berkeley Lab announced in this year’s edition of its annual report on the sector.

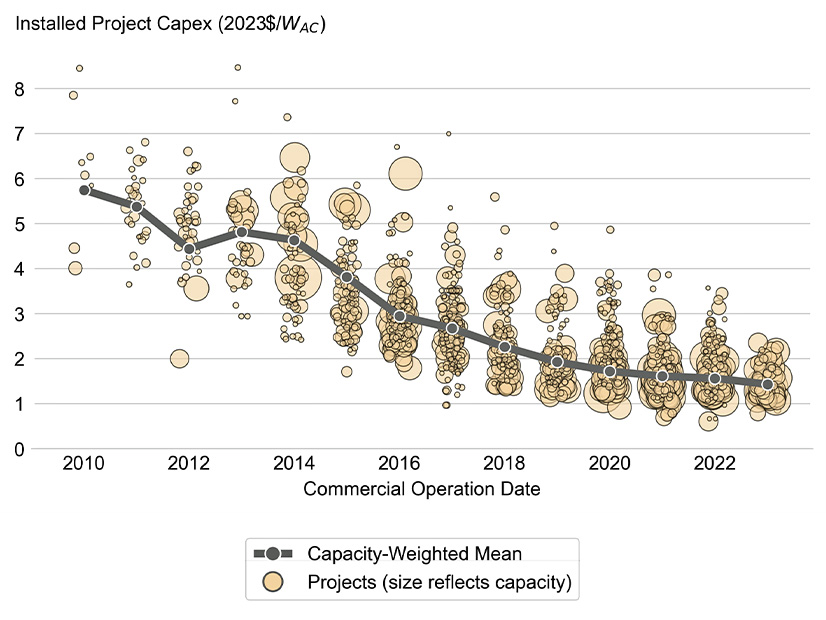

A total of 18.5 GWAC of large-scale solar was brought online last year, bringing total installed capacity to 80.2 GWAC in 47 states, the report says, while capacity-weighted average installed costs decreased 8% to $1.43 per watt AC.

The levelized cost of electricity from these utility-scale photovoltaic systems rose slightly to $46/MWh, not counting tax credits, but decreased slightly to $31/MWh once the federal incentives were factored in.

For the first time ever, more than half of new grid capacity nationwide was solar — 17% distributed and 35% utility-scale.

The report predicts that 2024 will be another record year, with more than 35 GW of utility-scale solar and distributed commercial or residential solar installed.

A whopping 1.09 TW of utility-scale solar is stacked up in the nation’s interconnection queues, but historically, only 10% of requests ever advance to construction, the Lawrence Berkeley National Laboratory noted as it announced the new report Oct. 15.

Capital costs of building utility-scale solar generation have steadily decreased over the past decade, as measured by cost per output. | Lawrence Berkeley National Laboratory

The 2023 report and its executive summary drill down on the state of the utility-scale solar sector. Among the details, data points and conclusions:

Average energy and capacity value nationwide was $45/MWh; average market value ranged from $27 MWh in CAISO, where solar has the largest market share, to $67/MWh in ERCOT, where summer heat waves and record electricity demand were seen during peak solar production hours.

Only 4% of utility-scale PV capacity added in 2023 was installed on a fixed-tilt mount; the rest used single-axis tracking. Fixed-tilt is relegated mainly to challenging sites and least sunny regions of the Northeast; tracking mounts add 20 cents per watt to the cost on average but can boost capacity significantly in sunny regions.

Projects larger than 50 MW cost 13% less per megawatt on average than their counterparts rated at 5 MW to 50 MW.

Plant output still declines with age, but more recent projects are showing a slower decline than earlier projects did at the same points in their lifespans.

Projects in the regions with the lowest solar insolation have the highest levelized cost of electricity — ISO-NE and NYISO were $76 and $78/MWh, respectively — while the sun-rich ERCOT, CAISO and non-ISO West ranged from $37 to $42. (Project costs and size contributed to this disparity.)

Solar power purchase agreements have largely closed the gap with onshore wind PPAs — both were much more expensive 15 years ago, but solar PPA prices have declined more sharply than wind. Lower natural gas prices, meanwhile, have given existing combined-cycle gas-fired generators a near-term cost advantage over solar.

Concentrating solar thermal power has been lagging, with no U.S. installations since 2015. The newest of the existing installations have underperformed expectations.

With the recent completion of the first phase of the New Jersey Wind Port, the state’s offshore wind sector looks to take a key role in the East Coast turbine industry despite the closure of the state’s two most advanced projects, speakers said at the state’s annual OSW conference.

A year after Ørsted stunned state officials and abandoned the state’s first two offshore wind projects, New Jersey has adapted to changing circumstances and developers are better prepared to weather the still difficult environment, speakers said at the Time for Turbines conference Oct. 11 in Atlantic City.

Atlantic Shores Offshore Wind, now the most advanced project in the portfolio approved by the New Jersey Board of Public Utilities (BPU), is moving ahead with its previously approved project, Atlantic Shores South 1, and a second one, Atlantic Shores South 2, Joris Veldhoven, the developer’s CEO, told attendees.

The Bureau of Ocean Energy Management (BOEM) on Oct. 1 approved the two projects’ construction and operations plan. And the company is close to awarding the last contracts and subcontracts for the first project, he said.

Veldhoven, in what emerged as a central theme among conference speakers, cited developers’ need to secure a strong supply chain pipeline, and the state’s ability to provide it, as key factors in their ability to move projects to completion, and for the sector to advance.

“In the current market, it is so critical that we locate these packages,” Veldhoven said. “Having that maturity, having the certainty that the supply chain is for you, is absolutely critical.”

In some respects, the state’s OSW sector is better able to get projects done than in the past, because developers such as Atlantic Shores are “more aware of the supply chain risk,” he said.

Likewise, regulators have recognized — and adapted to — the financial pressures that developers can face, among them the rise in interest rates, he said.

“What regulators have done over the last few years, and kudos to them, here in New Jersey and other states, there’s now a bit more of these inflation adjustment mechanisms that take into account various factors, and they started to even take into account cost of money,” he said. “Is that perfect? No, it’s not. But it shares some of the risk.”

‘Miracle’ Port Advance

Tim Sullivan, CEO of the New Jersey Economic Development Authority, which oversees port construction and funds much of the state’s OSW initiatives, said completion of the first phase of the wind port shows the state is a serious player in the East Coast wind sector.

The fact the first phase of the project came in “on time and under budget,” he said, is “close to a damn miracle.”

Other state competitive strengths include a “steady diet” of new project procurements, a “real commitment” from Gov. Phil Murphy (D) and — in the EEW monopile factory in Paulsboro — the only manufacturing facility that’s active in the U.S. for offshore wind components.

“Despite having fallen behind on the generation side a bit, we’re going to catch up,” Sullivan said. “We are still in the best position long term, and we are investing for the long term. … This is not a one-, two-, three-, four-, five-year ambition. This is a 50-year ambition. A century-long ambition.”

Murphy has set a goal for the state to have 11 GW of OSW capacity by 2040. Atlantic Shores is one of three companies awaiting the BPU’s decision in the state’s fourth offshore wind solicitation, which is expected by the end of 2024. The state is preparing to launch a fifth solicitation in early 2025. (See 3 OSW Proposals Submitted to NJ.)

The BPU approved Ørsted’s Ocean Wind 1 in the first solicitation in 2019 and the developer’s Ocean Wind 2 in the second solicitation in 2021, in which the 1,510-MW first part of Atlantic Shores also was approved. The BPU backed two projects — the 1,342 MW Attentive Energy Two and Leading Light Wind, with two phases of 1,200 MW each — in the third phase and is expected to announce the designated projects in the fourth solicitation by the end of 2024.

That fourth solicitation allowed developers awarded contracts in the first or second procurement — of which Atlantic Shores is the only remaining project — to submit a rebid that would enable them to adjust for rising costs. Atlantic Shores took that opportunity and also submitted the second half of the project, Atlantic Shores South 2.

The other applicants awaiting the BPU’s decision are Attentive Energy, with a second project, and Community Offshore Wind, for a 1,300-MW project.

Supply Chain Building

Yet the sector still is challenging, as shown by the difficulty Leading Light Wind has experienced in finding an economically viable turbine. On Sept. 25, the BPU approved a request by developer Invenergy to delay the project by three months because none of the three turbine manufacturers initially selected by the developer — GE Vernova, Siemens Gamesa Renewable Energy or Vestas — are able to supply suitable new turbines.

Abby Watson, president of The Groundwire Group | Christian Fiore

Some projects are moving to mitigate risk and create key elements of their own supply chain, conference speakers noted.

Attentive Energy, which hopes to begin construction in two to three years and complete the project by 2031, is vying for space in the wind port, said Karen Imas, the company’s senior external affairs manager. If Attentive’s bid is successful, the company plans to execute project marshaling and work with a manufacturer to build a factory there, she said.

Attentive also has committed $58.85 million into the third phase of EEW’s Paulsboro factory building monopiles, part of the foundations of offshore turbines, Imas said in an interview with NetZero Insider after her panel.

The arrival of Attentive and other developers in a second OSW wave may make them better placed to handle future challenges, she said.

“We are able to maybe anticipate a little bit more supply chain, timelines, projections,” she said. “We bid in with a certain price that we think is realistic today, and you know, maybe that sets us up with a little more stability than those awarded two, three years ago.”

Mitigating Risk

Imas pointed to the developer’s recent partnership with the New Jersey Manufacturing Extension on a policy paper published in October analyzing the readiness of the state’s manufacturing sector to adapt to the needs of the offshore wind sector. The extension interviewed 18 manufacturers about their capacity and interest in shifting gears.

The study found the companies can “pivot and provide some of the materials, the widgets, the products that would be needed for the larger Tier One, Tier Two manufacturers,” she said. Yet the study also found that 66% of the companies interviewed would require “targeted funding for process or technology upgrades” to take part in the sector.

“They need some technical assistance,” she said. “They may need increased staffing. They may need some special certifications and trainings. And that pivot will take some work. So we as a developer are taking note of this survey and what’s been reported, because we want to work hand in hand with these companies and really help arm them with the tools they need to participate.”

Those kinds of supply chain challenges are enhanced by the steady advance of a wave of OSW projects from different states all moving head and seeking the same resources, said Abby Watson, president of The Groundwire Group, a consultancy that focuses on sustainable energy.

“We have a lot of projects now that are all looking at building within a fairly short period of a couple of years,” Watson said, speaking on a panel entitled “Navigating Choppy Financial Waters.” “And that is an incredibly challenging commercial environment in which to build a successful business case for a manufacturing facility that’s going to be viable in the long term.

“I think we’re seeing that in some of the ways that different states are kind of redesigning some of their procurements to emphasize viability” and looking for ways to “de-risk that project.”

NYISO on Oct. 16 presented its updated modeling for combined-cycle gas turbines that employ duct firing to produce additional electricity and advanced a motion to recommend that the Management Committee revise the tariff in accordance with the model.

Stakeholders were unhappy that NYISO did not factor multiple “ramp rates” into its model, which they fear could result in improperly applied penalties for over- or under-generating in response to dispatch. NYISO had included multiple ramp rates in its original considerations but dropped them during model development.

“Generators should not have to waste a lot of time and expense fighting an improperly applied penalty that results from … NYISO not recognizing the ramp rate that a generator has already given the ISO,” said stakeholder representative Mark Younger of Hudson Energy Economics.

“Let me be clear upfront: I have no assurances that resources that are dispatched in their duct from a less-than-feasible ramp rate reflection will not be subject to penalties,” said Shaun Johnson, director of market design for NYISO. “I will point out that there are some wrappers around those penalties that make it less likely.”

“I totally agree it’s less likely,” Younger said. “The problem I’m having is that it’s totally inappropriate if it ever happens.”

When the motion was raised, the New York Power Authority seconded but encouraged NYISO to figure out a way to satisfy the concerns. Younger voted in opposition, noting that the dropped multiple ramp rates was effectively “moving the goalposts” to say the project had been completed, when it hadn’t.

East Coast Power and two other stakeholders abstained from the vote. The overall motion passed with a “vote by exception.”

Background

NYISO has been working since 2022 to improve modeling it uses to better accommodate combined-cycle gas turbine generators equipped with duct firing. Current models don’t account for the additional power generated by plants that use the technology.

Combined-cycle gas turbines burn gas to spin combustion turbines. Exhaust gas is directed to a heat recovery steam generator to pressurize steam and generate power in a steam turbine. Plants with duct burners may burn additional fuel to heat the exhaust gas, which can help maintain the generation of the heat recovery steam generator.

In 2020, according to the U.S. Energy Information Administration, about 75% of the U.S. combined cycle plant capacity used duct burners. In New York, about 79% of the power generated from natural gas plants came from plants with duct burners.

Johnson said the tariff revisions represented an incremental improvement in the way NYISO models ramp rates for duct firing combined-cycle plants.

“It doesn’t address all scenarios, and we need to keep working on that,” Johnson said. “I understand your frustration that not all scenarios were fixed, but this is an improvement, and we want to proceed forward with the incremental improvement where we continue to work on future improvements.”

Clarification: A previous version of this article mentioned JERA Americas as abstaining from the vote. Marie Pieniazek, director of regulatory affairs for JERA Americas, said she was voting for East Coast Power, which is a NYISO market participant. JERA Americas is not a NYISO market participant.

CARMEL, Ind. — MISO maintains that a member request to create a multiday gas purchase requirement for use during extreme cold is unnecessary but offered financial assurances for resources whose commitments are canceled.

MISO’s Jason Howard said instead of a multiday fuel purchase requirement for market participants, MISO wants to develop two new financial guarantees to resources committed days in advance of upcoming grid situations.

The first would be a canceled startup cost provision, where a resource would be guaranteed a portion of startup costs depending on when MISO cancels within the startup window. The second would be an “as-committed/as-dispatched” lesser of settlements rule, which would move multiday commitments into the day-ahead solution of an effective operating day and allow generators to earn make-whole payments based on the lesser of a real-time or day-ahead offer cost.

“We feel these are ideal to provide more security and assurance to resources,” Howard said at an Oct. 10 Market Subcommittee meeting. He said the rules are simpler than instituting a multiday market and that they help members feel more comfortable when they must contract for gas.

“When you compare this solution to doing the necessary software changes in our settlements system, that’s a huge cost benefit,” Howard said.

Howard also said the rules’ wording will establish assurances that extend beyond gas units.

MidAmerican Energy Co. — which serves natural gas customers in Iowa, Illinois, Nebraska and South Dakota — had argued that owners of natural gas units “undertake significant risk in purchasing or not purchasing natural gas when natural gas supplies are very tight” and are faced with either capacity loss or financial loss. MidAmerican said on rare occasions, there isn’t any natural gas available to buy after next-day trading in some portions of MISO. (See MISO’s MSC to Debate Multiday Gas Requirements.)

While some stakeholders have said the time is right for such a requirement, others said they worried about over-procurement of gas and whether the requirement would lead to pricing spikes at hubs.

Howard has said MISO already runs a multiday reliability assessment and commitment engine — the RTO’s Forward Reliability Assessment Commitment process — every day to position generation owners for upcoming obligations.

MidAmerican representative Dennis Kimm said he was happy with MISO’s compromise. He asked if the guarantees could be in place for upcoming cold weather.

“It might be a tough sell for this winter,” Howard said, referencing the settlements and tariff changes the rules will require.

Kairos Power and Google have reached a first-of-its-kind power purchase agreement involving several units of the small modular reactor Kairos is developing.

The two companies announced Oct. 14 that Kairos would deploy the first of its small molten-salt reactors for Google’s benefit by 2030 and a fleet totaling 500 MW by 2035.

Google said the power purchase agreements are part of its larger effort to develop and commercialize advanced clean electricity technologies to run its offices and energy-intensive data centers.

Kairos said the deal will support the iterative process through which it is pursuing its first commercial deployments, with each reactor contributing learnings that will optimize subsequent plants.

This year, California-based Kairos began construction of a low-power demonstration version of its reactor design at Oak Ridge, Tenn.

It is the first non-light-water reactor permitted for construction in the United States in more than half a century. The U.S. Department of Energy will invest up to $303 million to support construction and commissioning of the reactor, which is expected to be operational by 2027.

Many companies have committed to renewable energy or signed purchase agreements for new generation. One of the largest such consumers is Google, which has signed more than 100 agreements totaling over 14 GW since 2010.

A few companies have begun negotiating supply agreements with operators of existing nuclear plants, eager for the reliable flow of zero-emissions electricity they can supply.

The Google-Kairos deal is on a different level, pinned on a developing technology long on promise but short on operational experience.

Advanced nuclear technology is gaining increasingly broad support as a potential solution to the dual need to produce electricity with less environmental impact. Small modular reactors (SMRs) add the tantalizing prospect of faster, more nimble, less expensive deployment.

SMRs potentially could be collocated with a large power user as a behind-the-meter power source and avoid the costs and delays that accompany grid interconnection.

However, SMRs still must complete their development cycles and emerge in a form that is affordable and commercially scalable, and will pass muster with regulators, investors and host communities.

The Google-Kairos announcement did not specify a price tag or location for the reactors.

Large-scale nuclear power has become extremely expensive to build in the United States, in part because so few reactors have been built in the past three decades.

If each project is a “first-of-a-kind,” or first-in-a decade, it is hard to develop the economies of scale and institutional knowledge that would be expected to benefit an “nth-of-a-kind” project.

The Department of Energy addressed the differences between FOAK and NOAK in the September update of its “Pathways to Commercial Liftoff: Advanced Nuclear” report. There are more than 50 unique designs among the 94 operating commercial reactors in the United States, almost all of which came online before 1990.

The report indicates SMRs are likely to cost more per MW to build than large reactors and have smaller overall price tags.

It flags the potential to achieve what Kairos is attempting to accomplish with its iterative development approach and vertical integration: “An SMR could complete FOAK construction and implement cost-saving learnings on the second-of-a-kind reactor.”

In a news release, Kairos CEO Mike Laufer said the agreement will help propel the company he co-founded in 2016:

“Our partnership with Google will enable Kairos Power to quickly advance down the learning curve as we drive toward cost and schedule certainty for our commercial product. By coming alongside in the development phase, Google is more than just a customer. They are a partner who deeply understands our innovative approach and the potential it can deliver.”

In its announcement, Google said its power procurement from multiple reactors will help Kairos bring costs down and speed up development and is part of a broader effort Google is making with other advanced energy technologies.

Kairos is designing a low-pressure, high-temperature reactor that will operate with molten fluoride salt heated to 650 degrees Celsius. Its KP-X demonstrator will be a single unit rated at 50 MWE, and the KP-FHR commercial version will be dual units rated at 75 MWE each.

They are sized to ease manufacturing and construction of components.

The Union of Concerned Scientists released a paper Oct. 15 arguing the electric industry should focus on expanding renewable energy aided with storage rather than keeping natural gas plants running with hydrogen, biomethane or carbon capture and storage (CCS).

“Beyond the Smokestack: Assessing the Impacts of Approaches to Cutting Gas Plant Pollution” noted that gas plants are the largest source of carbon dioxide emissions produced by the electric industry.

“Every path to addressing our nation’s climate commitments and public health priorities calls for a cleaned-up power sector — and that makes reducing CO2 and other harmful emissions from gas plants an urgent priority,” the scientists group said in its paper.

CO2 emissions from power plants are just one way gas plants exacerbate climate change, according to the report, which notes that natural gas itself – methane – is a more potent greenhouse gas, trapping 28 times more heat over 100 years than carbon.

Co-firing hydrogen can cut smokestack emissions, but how the hydrogen is produced has major impacts on the emissions created and can lead to higher emissions than just burning methane, the report said. And because hydrogen is less energy dense than methane, three times as much of it must be burned to produce the same amount of electricity.

“Hydrogen production is energy intensive, making its production method a major factor in determining the overall change in carbon emissions from using hydrogen in gas plants,” the paper said. “Virtually all hydrogen used in the United States today — overwhelmingly for petroleum refining and in the chemicals industry — is produced via steam methane reforming (SMR), the main byproduct of which is CO2.”

That so-called gray hydrogen is not what the industry, or DOE hubs, are trying to promote. They’re pushing so-called blue or green hydrogen, which can be produced via CCS or from water using electrolyzers — though they must be run with zero-carbon power to achieve a carbon-free “green” hydrogen. Even green hydrogen comes with built-in inefficiencies compared to just using renewable electricity directly, according to the report.

“Producing hydrogen by using solar or wind energy to power an electrolyzer with a typical efficiency of 75% and then using that hydrogen in a gas power plant with an efficiency of 45% would result in only one-third as much electricity as that originally supplied by the renewable sources,” the report said. “That is, it would take three times as many wind turbines or solar panels to supply the same amount of electricity via hydrogen blending as from wind or solar directly.”

Hydrogen can be stored but is less efficient than technologies that store electricity outright. It could make sense if other options to capture and store electricity do not work, or in a system that has enough excess renewable electricity to make hydrogen, according to the report, which concluded that direct use of renewable power has a much bigger impact on cutting emissions.

Another option for cleaner gas plants is to keep burning the fuel with a CCS system, an approach the paper claims does not address upstream emissions of methane and introduces other challenges.

“Any CO2 leaking from the pipelines, or the storage would undo the carbon capture effort, at least in part,” the paper said. “Over time, CO2 can slowly leak into the atmosphere if storage reservoirs are not carefully monitored; abandoned oil and gas wells intersecting with CO2 storage sites also increase the risk of leakage.”

CCS technology requires energy to work, and it can take away between 10 to 20% of the electricity produced at the plant, according to the paper, which concluded would exacerbate upstream emissions. The third option cited by the paper is “biomethane” or “renewable natural gas.” It is produced from the anaerobic breakdown of organic matter such as manure, sewage or landfill waste. Smokestack emissions when it is burned are the same, but it avoids emissions in production of the fuel.

The assumption that CO2 produced at the smokestack has a lower climate impact than just venting methane from a farm or dump “is not reasonable in a net-zero framework, where every source of pollution counts; with the United States committed to achieving a net-zero economy by 2050, there is no credibility to a baseline assumption of unmitigated methane venting,” the paper said. “Instead, if biomethane can be captured for use, at minimum, the appropriate baseline climate comparison is flaring, such as is now required at certain regulated landfills.”

It would make more sense, according to the report, to compare biomethane to the best alternative for the climate, which would be to avoid those initial methane emissions through climate-smart farming techniques or avoiding organic waste in landfills.

The West-Wide Governance Pathways Initiative has revised its “regional organization” stakeholder process proposal to expand the size of a key stakeholder committee and boost representation for some groups.

The revision also provides more detail about the makeup and functioning of the Stakeholder Representatives Committee (SRC), among other changes.

“The Launch Committee’s recommendations regarding sectors and sector representatives are intended to promote the goals of the SRC and recognize the uniquely diverse stakeholder community that has a vested interest in the RO,” the committee wrote in the revised proposal. “It is also intended to ensure robust dialogue and guard against changes to the market that would decrease efficiency, result in any market manipulation practices and negatively impact benefits to customers.”

The revised plan would increase the number of seats on the RO’s proposed SRC from 16 to 19. More specifically, it bumps up the number of SRC representatives from the Extended Day-Ahead Market (EDAM) Entities sector (from one to two), the Western Energy Imbalance Market (WEIM) Entities sector (from two to three) and the sector representing non-investor-owned utilities serving load from the EDAM or WEIM (three to four).

The Launch Committee said it proposed to increase the number of seats for the WEIM Entities sector to reflect the size of the WEIM, which has 20 participants.

“The three SRC representatives are intended to provide the flexibility to ensure that both public power and IOUs have representation, as well as enable geographically diverse representation from the Northwest, [the] Desert Southwest and California,” the committee wrote.

The committee’s proposal to increase the number of non-IOU seats on the SRC was intended “to ensure the unique voices of public power, municipal utilities, cooperatives and community choice aggregations are represented. However, if an entity participates collectively through an EDAM entity (e.g. BANC members), they cannot also participate in a different sector as individual entities (i.e., generators or [municipal utilities]).”

The revised proposal also clarifies definitions of the nine SRC sectors set out in the original proposal.

For example, it draws from CAISO’s tariff to clarify the definition of an EDAM entity as being a balancing authority “that represents one or more EDAM Transmission Service Providers and that enters into an EDAM Entity Agreement with the CAISO to enable the operation of the Day-Ahead and Real-Time Markets in its Balancing Authority Area.”

Similarly, a WEIM entity is described as a BA “that represents one or more WEIM Transmission Service Providers and that enters into an WEIM Entity Agreement.”

According to the proposal, EDAM and WEIM entities can be investor-owned utilities, federal power marketing agencies or publicly owned utilities.

The revised plan also removes the reservation of SRC seats for independent power producers (IPPs) and marketers in the sector shared among IPPs, marketers and independent transmission developers — which continues to hold three seats.

Other Changes

The revised proposal additionally recommends creating the roles of an SRC chair and vice-chair to “serve as the primary point of contact with the RO staff and provide administrative leadership for organizing the SRC” but “not have any decision making or enhanced authority.” The stakeholders filling each role must be from different sectors.

The positions would rotate yearly and be selected by the SRC, with each sector casting a single vote.

The proposal also calls for limiting SRC membership to “market participants” (those with a direct stake in the EDAM or WEIM) but recommends creating another stakeholder category of “other load-serving non-market participants” who would sit outside the SRC. That arrangement would allow “people or organizations who do not participate in the WEIM or EDAM and therefore do not fit within one of the designated sectors” to register with the RO to offer a nonbinding vote on issues before the SRC.

“The votes will not count toward an SRC recommendation [to the RO board] or remand threshold but will be shared with the RO staff and Board for information only. This group of individuals or organizations may participate in the stakeholder process and submit comments that will be included in the package of information that goes to the RO staff and/or board when appropriate,” the proposal said.

The Launch Committee also calls for a reevaluation of the SRC sectors and structure at two points in the future: during implementation of the RO and two years later.

“Reevaluation could include both consolidation of sectors and reorganization of sectors to reflect necessary changes based on meeting the goals. It should also consider whether it successfully prevents sector shopping and astro-turfing, and whether it creates the right balance across sectors for achieving the market goals,” the proposal said.

The revised proposal also recommends removing a provision in the original plan that would trigger an “automatic remand” of an RO initiative back to the stakeholder process if voting on the proposal shows “significant opposition” among stakeholders. That’s defined as a lack of support from a simple majority of sectors or one-third of SRC sectors registering at least 70% of their members voting in opposition.

“We recommend removing the automatic remand but still using the ‘significant opposition’ thresholds to trigger additional discussion at the SRC about whether remanding back to the stakeholders would be beneficial to the process and the initiative,” the Launch Committee wrote.

The committee is seeking comments on the sector proposal until Oct. 25.

ARLINGTON, Va. ― Order 1920 was a “big lift” for FERC, recalled Liz Salerno, who was lead adviser to former FERC Chair Richard Glick when work on the transmission planning order started in 2021.

“You know, this rule went from an [advanced notice of proposed rulemaking], which was just hundreds of pages of hundreds of questions, open-ended questions, of FERC trying to figure this out, to a detailed proposed rule to a final rule in three years,” said Salerno, who now is a principal with industry consultants GQS New Energy Strategies. “That is lightning speed for a regulatory body.”

FERC’s rule on long-term transmission planning was, predictably, a recurring theme at the American Council on Renewable Energy’s (ACORE) Grid Forum on Oct. 10. But while calling the order a big step forward, Salerno and other speakers urged broad and ongoing industry engagement, stressing that compliance and implementation of 1920 likely would take even longer and prove more challenging for the commission, grid operators, utilities and developers.

Industry stakeholders have estimated it may take five to 10 years for the order to have any major effects on transmission planning in the U.S.

Order 1920 is “not a ‘set it and forget it’ type of thing,” Salerno said. “It doesn’t dictate outcomes. It is a framework; it is rules of the road.”

Much work remains, she told the forum. “There are still folks who don’t want transmission to be built,” she said. “They like the status quo. They’re going to be there … voicing their opinion, and so you need to be there, making sure this thing gets implemented.”

Approved in May with a 2-1 vote, Order 1920 requires RTOs and ISOs to undertake long-term transmission planning ― with a 20-year time frame ― taking into account anticipated load growth, state laws and generation retirements, while also looking at seven core benefits of new transmission, such as cost savings and fewer outages. The long-term plans must be updated every five years. (See FERC Issues Transmission Rule Without ROFR Changes, Christie’s Vote.)

The order also calls for grid operators to open a six-month process to allow states to develop new cost allocation methodologies or adopt one or more “ex ante,” or default, methods for cost allocation filed prior to any selection of projects.

The order has triggered dozens of requests for rehearings, which FERC is considering. Eleven legal challenges have been filed across the country but recently were consolidated to the 4th Circuit U.S. Court of Appeals in Richmond. (See FERC Order 1920 Sees Wide-ranging Rehearing Requests) .

Since 1920 was approved, former Commissioner Allison Clements has left FERC, and three new commissioners have come on board, including David Rosner, who also weighed in on the order during an onstage conversation with ACORE CEO Ray Long. Rosner said he will look for ways to “turn down the temperature ― the political temperature that some people think this rule is taking ― in ways that are directionally consistent with what the rule is trying to do, which I firmly believe … is [that] we’ve got to find ways to build needed transmission.”

Drawing on his experience as an energy industry analyst at FERC and as an adviser to the Senate Energy and Natural Resources Committee, Rosner described himself as “an energy nerd.”

“Like I live in the dockets,” he said. “And what that means is, I still read the orders. I read the comments. That helps us to get to good decisions.”

Industry comments are “foundational” in the commission’s decision making, Rosner said.

While providing no details on FERC’s pending decision on a 1920 rehearing, Rosner was “hopeful that there are a number of things in that record that we can do that achieve those goals, and I am also hopeful that we can work with all five commissioners and ideally get a 5-0 [vote].”

Successful implementation, he said, would ensure “that all resources on the grid can provide all the services that they’re technically capable of driving.”

Considering GETs

But Abdul Ardate, director of transmission and interconnection for developer EDP Renewables, said 1920 may not provide the kind of certainty that is a top priority for his company and others in the industry.

The requirement for long-term plans to be re-evaluated every five years “is a double-edged sword because some [projects] could potentially get stuck in re-evaluations every five years, [so] that nothing can get built,” Ardate said.

He pointed to projects EDP has seen utilities or RTOs repeatedly re-evaluate and redesign at escalating costs, with one project going from $3 million to $8.5 million to more than $60 million, with nothing yet built. The cost to customers for the resulting grid congestion and “generation that cannot deliver its energy is just tremendous,” he said.

Ardate was also skeptical of 1920’s provisions calling on RTOs to “consider” grid-enhancing technologies ― such as dynamic line ratings or advanced conductors ― that can increase capacity on existing lines to provide short-term upgrades while longer-term transmission projects are planned.

“I don’t think the language is strong enough to require them to include grid-enhancing technology, not just consider, because I think that’s too loose a definition,” he said. “I don’t think this is going to push the needle on anything short-term in terms of implementing any grid-enhancing technologies.”

Karin Herzfeld, senior transmission counsel to FERC Chairman Willie Phillips, countered that 1920 does “include a requirement for the transmission provider to justify its decision and to be transparent about that decision. So, I do think that component will provide some incentive or give stakeholders some confidence that they have actually reviewed and considered to see whether a grid-enhancing technology might be appropriate.”

The catch here is the amount of discretion the rule gives operators to decide what projects or technologies may be appropriate for their systems and to reopen consideration of individual projects every five years, Salerno said. “There is no requirement in this rule to select anything; that is up to the discretion of the transmission provider.

“That cuts both ways,” she said. “That means there’s no guarantee for any of us that transmission is going to get built … which again goes back to why you have to engage and make sure that this is a good process, and there is a likelihood of selection.”

“We can do all the planning; we can look at all the benefits, all the requirements, but then ultimately it’s up to the states to decide which project is going to get selected or built, or how it’s going to be cost-allocated as well,” Ardate said. “We have to get active on the state level, the public utility commission level, the Department of Energy, even on the FERC level to make sure that we get our voices heard.”

Win a Little, Lose a Little

Cost allocation has long been a major challenge ― if not an outright deal killer ― for some interregional transmission, and both Herzfeld and Salerno emphasized the importance of 1920’s requirement that states hold a six-month engagement period to determine whether they will use a grid operator’s default methodology or come up with one of their own.

They can also opt for a state agreement approach, “by which they can punt a project that gets selected to a future cost allocation,” Herzfeld said. “They can punt it to their future selves to decide cost allocation voluntarily.”

Salerno said the default methodology ensures that once a project has been selected as part of a long-term plan, “there’s a cost allocation method waiting for them. There is no additional work to be done.

“This is going to make sure we don’t have a world where great projects get planned and get through the selection process because they have great benefits and then they go nowhere because no one can agree on cost allocation,” she said.

On the other end, the six-month engagement period could help circumvent permitting challenges, she said. “Giving some control back to the states to let them decide how [a project] gets paid for is critical to bringing them to the table and getting them comfortable and happy with the project, so maybe [it] smooths out the process on the back end with permitting.”

Herzfeld agreed the ex-ante provision will “just absolutely make sure that transmission will be built” and prevent a project from stalling should a single state hold out on cost allocation.

“Everyone always wins a little and loses a little” in cost negotiations, she said. But “when there’s nothing to kick in as a default, everyone wants to win a lot and lose nothing.”

Thinking Outside the Box

Rosner’s appearance at the ACORE forum was his second on Oct. 10, following an early morning on-stage conversation with Jason Grumet, CEO of the American Clean Power Association, at an ACP event. (See FERC’s Rosner Talks Priorities at American Clean Power Association.)

Repeating some of the key points from his ACP appearance, Rosner said job one for FERC is managing the U.S. energy transition, which “means a lot of different things. It [means] where we have markets, be smart. Let’s make sure those markets are sending the right signals to get the investments, the technologies or the attributes that the system needs to be reliable.”

Interconnection is another top concern for Rosner, who pointed to FERC’s Order 2023 on interconnection, passed in 2023, and, like 1920, “will take many more years to get compliance with it and get it working,” he said.

At the same time, Rosner said, “I am very open to thinking outside the box about what other things can speed that up,” such as the use of artificial intelligence to cut the time needed for interconnection studies.

“Anything we can do to move those studies faster is going to help us get through those queues faster, and if it’s something we don’t have to write a regulation on … I’m like all in on that. So, I want to learn more.”

ERCOT and the Public Utility Commission of Texas have knocked down recent media reports that a proposed HVDC transmission link between Texas and its Louisiana and Mississippi neighbors will bring the state’s grid under FERC jurisdiction.

Speaking to the ISO’s Board of Directors Oct. 10, ERCOT CEO Pablo Vegas said news coverage of the U.S. Department of Energy’s plan to invest up to $1.5 billion in four transmission projects, including Pattern Energy’s Southern Spirit Transmission 525-kV link eastward, “made it sound like there had been some substantive change in the policy around interconnecting the ERCOT grid to other grids in the United States.” (See DOE Funding 4 Large Tx Projects, Releases National Tx Planning Study.)

“That’s not the case. That is not what has occurred with this recent announcement, nor with the underlying drivers for this project,” Vegas told directors.

Texas has long resisted federal oversight of the ERCOT grid by not mixing its electrons with those of the Eastern and Western Interconnections. It does have four DC ties with neighboring grids, two with SPP and two with the Mexican system, totaling about 1,220 MW of capacity.

One of the links to Mexico is through a variable frequency transformer with a control system that operates like a generator, but it is not a synchronous tie, Vegas said.

Several news stories following the DOE announcement implied that ERCOT soon would be connected to the Eastern Interconnection for the first time. A headline from the EV news site Electrek, “Hell froze over in Texas – the state will connect to the US grid for the first time via a fed grant,” drew most of the attention.

PUC Chair Thomas Gleeson said inquiries from a politician or two prompted him to issue a statement Oct. 4, the day after the DOE announcement.

“While the Southern Spirit Transmission line would cross multiple state lines, the Texas grid will remain independent from the national grid and would not be subject to any federal oversight,” he said.

Gleeson, like Vegas, noted ERCOT already has the four DC ties with its neighbors. “They do not have any impact on the independence of the Texas grid,” he said.

Southern Spirit, a merchant transmission line more than a decade in the making, would provide a 320-mile, HVDC link from Texas capable of carrying 3 GW of power either way. While it was originally designed to move renewable energy to the Southeast, some reports have framed the project as saving Texas should there ever be a repeat of the 2021 winter storm that almost brought down the ERCOT grid.

DC ties approved under Sections 210 and 211 of the Federal Power Act do not pose a risk to ERCOT’s independence, Vegas said. FERC says the Texas grid is not jurisdictional because it is not synchronously connected to the other two interconnections and thus its power sales are not considered interstate commerce and not subject to oversight.

Vegas said the 19 switchable units that can provide about 4 GW of power to either ERCOT or the Eastern Interconnection are “an incredible asset to us,” offering them as an alternative to DC ties.

“DC ties could [solve the reliability problem], but I think they need to be fairly evaluated from all of these factors to really understand what is the best investment for the ERCOT consumers when it comes to investing in reliability and the economic potential of more infrastructure,” he said.

FERC approved the Southern Spirit project, previously named Southern Cross, in 2014. The Texas PUC followed suit in 2017, approving Garland Power & Light’s application for a permit to build a 38-mile, 345-kV line connecting ERCOT to a Pattern Energy DC converter station in the Eastern Interconnection.

The PUC also established 14 tasks, or directives, for ERCOT to complete in accommodating Southern Spirit. The commission closed the project in 2022, saying it agreed with the ISO’s solutions.

The project got a major boost in August when the Louisiana Public Service Commission approved it, 3-2. However, that also opened an appeals window from landowners and lawmakers who have opposed the project. Mississippi regulators have not yet signed off on the project.

If Southern Spirit is fully approved, Pattern Energy says it would begin construction in 2026 and enter commercial operation in 2029. The company plans to invest $2.6 billion in Southern Spirit, which is eligible for up to $360 million in DOE financing support.

Another set of proposed changes to NERC’s Rules of Procedure is before FERC, after the ERO filed them with the commission Oct. 14 (RR25-1).

The revisions are directed at Appendix 4E of the ROP, which governs the procedures for hearings by the ERO’s Compliance and Certification Committee, appeal hearings, and mediation. NERC has been developing these changes for the past two years, after the CCC first approved revising Appendix 4E at a meeting in April 2022. The ERO’s Board of Trustees approved the revisions at its open meeting in August.

According to the CCC’s charter, “the CCC serves as a hearing body in matters when NERC … directly monitors [power grid] owners, operators and users for compliance with reliability standards.” The committee also serves as a mediator for “disagreements and disputes between NERC and the regional entities concerning NERC performance audits of [REs’] compliance programs,” as directed by NERC’s Board of Trustees, and hears appeals from REs challenging NERC noncompliance findings and related penalties.

Regarding the last point, NERC’s proposed revisions would remove references to REs challenging noncompliance findings, on the basis that there are no longer any REs “complying with NERC reliability standards.” This reflects the elimination of the ERO’s “Regional Reliability Organization” function for registered entities, along with the Reliability Coordinator function that some REs possessed, a spokesperson told ERO Insider.

They also would insert a footnote clarifying that hearings involving the CCC “are likely to be extremely limited” because there are no standards applicable to REs, and that NERC probably never will have to directly monitor compliance by registered entities itself due to lack of an RE in their area.

The next category of revisions relates to the CCC’s procedures for hearing appeals of certification matters. NERC said these changes are intended to maintain consistency with the previous category and other hearing procedures in the ROP, and to update language that has remained unchanged since this passage originally was approved in 2010.

Finally, NERC proposed updating the section of Appendix 4E relating to the CCC’s mediation procedures to “clarify which CCC members are eligible to serve as mediators.” The revisions specify that only committee members who “are disinterested parties,” have not worked in the territory of the RE involved in the dispute and have no other conflicts can serve. In addition, potential mediators would be required to attend a training course.

NERC has been active in revising its ROP in recent years, with FERC approving multiple changes in the past 12 months. First, the commission accepted a set of revisions last November intended to streamline the ERO’s standard development process and allow a faster response to emerging issues by granting NERC’s board the authority to direct the development of a new or revised standard when the board feels it is necessary to maintain grid reliability, bypassing the normal stakeholder comment process. (See FERC Approves NERC Standards Process Changes.)

Additional changes followed in June, with FERC accepting NERC’s proposed revisions that would allow the ERO to register owners and operators of inverter-based resources. The commission also dropped its proposal to require NERC to submit performance assessments every three years, rather than every five years as currently required. (See FERC Accepts NERC ROP Changes, Drops Assessment Proposal.)