More than 11,000 MW of battery storage resources are now deployed across CAISO’s grid — with much more on the way.

But how much are California’s batteries really displacing gas-fired generation?

Answering that question isn’t easy, according to CAISO staff and other electric industry experts, who say that while batteries are having a notable impact, several factors — including weather conditions and the behavior of storage resources — complicate the narrative that they are displacing gas on the grid.

“You can confidently say that batteries are displacing the need for natural gas energy production, but — and this is a large ‘but’ — batteries are not displacing the need for natural gas capacity just yet,” Carrie Bentley, CEO and co-founder of Gridwell Consulting, told RTO Insider.

Battery buildout has coincided with the need for additional capacity to ensure reliability, especially as 2024 saw another record-breaking year for high temperatures. Reliability modeling indicates that most, if not all, of the gas fleet is still needed, as well as all the current and planned batteries for the next decade, Bentley added.

“This is not as bleak for the environment as it sounds because batteries are displacing the gas fleet energy production and therefore lowering natural gas emissions,” Bentley said.

No ‘One-for-one Displacement’

Energy storage capacity on the CAISO grid grew from under 500 MW in the summer of 2020 to 11,200 MW as of June 2024, representing a “significant” pace of deployment, Sergio Dueñas Melendez, the ISO’s battery storage sector manager, said in an interview with RTO Insider.

CAISO’s Western Energy Imbalance Market includes an additional 3,500 MW of battery capacity, according to a June 2024 report from the ISO’s Department of Market Monitoring.

While Dueñas Melendez noted that the ISO does not currently have a metric to determine whether batteries have displaced the need for gas on California’s grid, the addition of energy storage has had an obvious impact.

“Now that we have way more batteries, we definitely are seeing that batteries are charging in periods of high solar radiation and discharging as the sun starts to set into the afternoon peak and the peak hours,” Dueñas Melendez said. “Earlier this year, the ISO broke a record of peak battery discharge, with over 7,000 MW in a given five-minute interval of battery discharge.”

Pointing to data from the DMM showing the change in hourly generation by fuel type between 2022 and 2023, “you can see how gas, on average, especially in certain hours, has reduced its output, and batteries have increased their output,” CAISO COO Mark Rothleder told RTO Insider.

But the behavior of batteries complicates making an exact calculation of the level of displacement.

“You will not see a one-for-one displacement because a four-hour battery is not going to perfectly displace a dispatchable gas resource over the day,” Rothleder said. “The capability of the batteries over four hours versus being able to ramp day-over-day and intraday of the gas fleet doesn’t allow you, at this point, to fully replace the gas fleet with batteries. But there is certainly energy displacement.”

Guillermo Bautista Alderete, CAISO’s director of market analysis and forecasting, added that a one-to-one replacement of gas with storage supply cannot be assumed because of the dozens of storage and gas resources with varying costs and locations. He also noted that, given the level of storage in the system, those resources can also be displacing of other types of supply, not just gas — the exact value of which is also unclear.

“Since the market determines the optimal dispatch of all resources based on their bid costs and attributes, it can’t precisely track in isolation the specific volumes of gas supply displaced by storage resources compared to other supply types,” Bautista Alderete said in an email. “Changes in the level of gas supply dispatched at any given time depend on various factors, including the relative bid costs of different technologies, demand levels, hydro conditions, renewable production, resource availability, gas prices, seasonal conditions, transmission congestion and broader supply/demand conditions in the WEIM that influence the level of transfers.”

Weather Impacts

The degree to which batteries displace gas can also depend on prevailing weather conditions.

A May 2024 blog post from energy data provider Grid Status contended that battery storage was the “standout performer” in CAISO last spring, saying that “batteries are displacing natural gas when solar generation is ramping up and down each day in CAISO.”

But the report only cited data from April, which does not show the full picture, according to Bentley.

“April is not indicative of the annual trend, because what’s happening in April is you have very low demand, but it’s starting to get sunny,” she said. “This is basically the perfect time for batteries.”

California successively broke records for summer heat in 2023 and 2024, which drove high — although not record —peak loads. While natural gas usage remained high, it decreased as batteries grew, even as peak demand increased.

According to CAISO data, the ISO’s 2023 peak demand occurred on Aug. 16 at 44,534 MW. In the early evening hours, as solar ramped down, natural gas peaked at 26,490 MW, with batteries dispatching at 927 MW. As the evening progressed, batteries ramped up, peaking at nearly 3,000 MW, while natural gas ramped down to just over 25,000 MW.

The 2024 peak of 48,353 MW occurred on Sept. 5. As solar ramped down in the early evening hours, both gas and batteries ramped up well into the night. Despite the increased net demand and record-breaking heat compared with the prior year, the natural gas peak topped out at just over 23,000 MW, while battery output rose to over 6,000 MW — reflecting a seasonal pattern that resulted in an “uneventful” summer despite periods of extreme heat, according to CAISO. (See Batteries, Energy Transfers Support ‘Uneventful’ Summer in West.)

When considering different periods and associated trends, all system conditions must be considered, Bautista Alderete added.

“The supply mix will inherently be lower across various technologies to meet the demand on a spring day with a peak of 30,000 MW, compared to a much higher supply mix needed to meet the demand on a summer day with a peak of 50,000 MW,” Bautista Alderete said. “Naturally, a higher level of supply is required to meet peak demand during the summer.”

The growth of battery energy storage in tandem with the decrease of natural gas is expected to continue. The California Energy Commission projected the need for 52,000 MW of battery energy storage by 2045, a goal that CAISO’s Dueñas Melendez said the state is on track to meet.

“We have more in the queue than that,” Dueñas Melendez said. “The real challenge — across the different agencies, for developers and for the ISO — is to be able to manage that influx in an orderly way to get to that goal.”

CAISO, California and other parts of the Western Interconnection are moving into 2025 with a heavy load of priorities: implementing a day-ahead market, developing the transmission and other infrastructure needed to meet ambitious climate goals, and moving forward with new and continuing initiatives to address some of the ISO’s biggest challenges.

But the ISO is no stranger to ambitious workloads.

“We’ve been in a heavy lift for several years, and we’ve already been anticipating this, and so we’ve been preparing,” CAISO COO Mark Rothleder said in an interview with RTO Insider.

Key among CAISO’s priorities: continuing the steadfast work required to implement the Extended Day-Ahead Market (EDAM) in time for the 2026 launch date.

“2025 is going to be a major, major focus on implementation of EDAM,” CAISO CEO Elliot Mainzer said at a Dec. 18 joint meeting of the ISO Board of Governors and Western Energy Markets Governing Body.

PacifiCorp’s “go-live” date is scheduled for the spring of 2026, and PGE’s is slated for that fall.

“We’re going to be doing a lot of work this year to keep both of those entities on track for implementation,” Mainzer said. “I’m very confident that we’re going to continue making progress there.”

But this won’t come without challenges. PacifiCorp, the first Western entity to begin taking steps to join EDAM, already faces scrutiny over its implementation process.

During the Dec. 18 meeting, Carrie Bentley, a consultant representing the Western Power Trading Forum (WPTF), told the ISO board and Governing Body of WPTF’s intent to file a FERC protest in January over PacifiCorp’s proposed tariff changes to implement EDAM.

“WPTF has significant concerns with this filing, specifically that PacifiCorp proposes to allocate virtually all congestion revenues it receives from … CAISO to measured demand,” Bentley said in the Dec. 18 meeting. “At the most basic level, PacifiCorp’s filing goes against a foundational aspect of the EDAM market design — that fundamentally, EDAM is a day-ahead market overlaid on OATT transmission rights, and it’s not a full ISO or RTO that includes congestion management instruments.”

PacifiCorp’s filing, Bentley added, “hands opponents of EDAM a valuable weapon to undermine it, which is completely unwarranted,” and was not part of the EDAM design agreement.

Mainzer validated Bentley’s concerns.

“We are very aware of the nature of your concerns,” Mainzer said. “I think we share your optimism and hopefulness that this matter can be resolved in a mutually acceptable manner, and we will continue to work with PacifiCorp and others to support what they need to bring it to a satisfactory resolution.”

‘In Good Shape’

In 2025, reliability will be — and always is — “job number one,” Mainzer said, emphasizing that the ISO already has begun planning for winter.

CAISO’s forecast team expects above-normal temperatures across California and in the Desert Southwest (DSW) from December through February, with the highest likelihood of above normal temperatures in the southern region. In contrast, there’s a greater potential for below-normal temperatures in the Pacific Northwest.

Northern California saw above-normal rainfall through early December, Mainzer noted, which then “dissipated a bit” as the month progressed. Between December and February, there is a projected risk of below-normal precipitation for the Desert Southwest and a higher likelihood of above-normal precipitation in the Pacific Northwest.

Current reservoir conditions across California and the West are at about half-capacity, so the expected precipitation in the Northwest could help the region recover some of its hydro storage, with the Desert Southwest expected to remain at greater risk of low water conditions, Dede Subakti, the ISO’s vice president of system operations, wrote in a Dec. 20 posting on the ISO’s Energy Matters blog.

“We’re going to be keeping a close eye on the forecast, temperature and precipitation,” Mainzer said. “Fortunately, given this outlook, our operations team is reporting that all major transmission paths are expected to be fully available to support transfers across the region, allowing market participants in balancing areas to move energy across the system as needed.”

Resource adequacy is “looking good,” Mainzer added, showing sufficient supply to meet firm demand through the winter.

CAISO has intensified its winter readiness planning, with more time and resources being spent on forecasting, coordination and preparation around cold weather events, Subatki wrote in his post.

“The ISO is prepared and has been working hard to make sure all the customers and market entities we serve in California and the broader West are ready for winter,” Subakti wrote. “Mother Nature often has her own plans and weather predictions are never 100 percent accurate, regardless of what season we’re in. But with all of the work and preparation, we are going into the winter of 2024-2025 in good shape.”

New and Continued Initiatives

CAISO is moving into 2025 with 10 active stakeholder initiatives, and several include sub-working groups dealing with some aspect of EDAM implementation.

In the Greenhouse Gas Coordination Working Group, ISO staff and stakeholders are in the process of developing a process for accounting for GHG emissions in EDAM for states that don’t price carbon but have other policies to reduce emissions. (See Western Market Developers Compare Approaches to GHGs.) The ISO is expected to develop a policy in the first quarter of 2025 and make a decision in the second.

In the Price Formation Enhancements Initiative, staff and stakeholders are, among other things, considering whether to include fast-start pricing in the EDAM design. (See CAISO Considering Fast-start Pricing for Extended Day-Ahead Market.) A straw proposal for this initiative is expected in Q2, with policy development in Q3.

Other efforts, such as the Storage Design and Modeling Initiative, are new, but piggybacking on the work of prior working groups. This effort will continue to tackle an array of challenges related to the market participation of storage resources, including further addressing bid cost recovery issues and developing a default energy bid formula specifically for batteries. (See CAISO Launches New Initiative for Storage Resource Design.)

‘We’ve Got to Push Through’

Rothleder reflected on the past four years, highlighting that since 2020, when the ISO faced challenges meeting demand, the state has stepped up to increase the amount of capacity being brought on, and that pace of development has increased.

Going into 2025, the pace must be sustained, Rothleder emphasized, to maintain reliability and meet the state’s climate goals.

“Taking your foot off the gas pedal is not going to be helpful at this point,” Rothleder said. “We’ve got to push through, continue the development, continue the transmission and continue the collaboration across the region because the lack of not doing so will be both costly and create more operational challenges for not coordinating and collaborating across the greater West.”

Protests and endorsements have turned up in response to MISO’s second attempt with FERC to annually cap project submittals to its interconnection queue based on a megawatt value.

MISO filed its intentions with FERC in late November to impose a yearly cap of 50% of the non-coincident peak per study region in its interconnection queue (ER25-507). RTO staff have said repeatedly that a cap would make their interconnection studies manageable. MISO first filed for a cap in late 2023 but was rebuffed by FERC. (See MISO Queue MW Cap to be Filed Sans Regulator Exemption for RA Generation Projects.)

Multiple stakeholders weighed in with FERC over the revamped proposal, with some claiming the cap would introduce a discriminatory process that would inject more uncertainty into the queue.

“Rather than help MISO manage its rapidly growing queue, this proposal would add uncertainty and create a rush of projects seeking to be included in the next available capped queue cycle,” the American Clean Power Association, Advanced Energy United, the Solar Energy Industries Association, the Southern Renewable Energy Association and Clean Grid Alliance said in a joint protest. The groups said MISO’s cap filing didn’t contain any elements that would speed up queue processing, like offering more schedule certainty or providing network upgrade cost estimates earlier.

“Instead of addressing these underlying issues, MISO has simply opted to prioritize shrinking the queue size over boosting queue throughput without any evidence that smaller clusters will be processed faster than larger clusters,” they argued, adding that it’s a “false assumption” to assume that a more modest queue equals a more accurate and faster queue.

Shell Energy and its subsidiaries said the cap “misses the mark” because just a few interconnection customers are responsible for the overwhelming number of requests in recent years.

“Given this fact, it is unjust, unreasonable and unduly discriminatory to impose sweeping restrictions on the majority of interconnection customers not contributing to the problem,” Shell argued. The company suggested MISO craft queue caps by corporate family, which would have the same effect on queue size without punishing all developers “for the behavior of a few.”

On the other hand, the Organization of MISO States called the cap a “necessary mechanism — at least in the near-term — to ensure MISO can efficiently manage” an oversaturated interconnection queue.

OMS pointed out that the 171 GW of interconnection requests MISO received in 2022 and the 124 GW that followed in 2023 aren’t sustainable and aren’t conducive to realistic study results.

“The sheer size of MISO’s interconnection queue has resulted in unreliable, outdated and inaccurate network upgrades identified early in the study process. It is simply infeasible to study clusters of resources that when combined exceed MISO’s all-time peak load,” OMS wrote.

However, the Mississippi Public Service Commission and Louisiana Public Service Commission objected to MISO’s cap plans because MISO didn’t include a cap exemption for projects that further states’ resource adequacy targets. MISO’s first, failed attempt to instate a queue cap featured an exemption for regulators’ pet generation projects. The grid operator since has morphed the promise of a cap exemption for critical projects into the creation an exclusive express lane for projects that preserve resource adequacy. (See MISO Outlines Plan on Fast-track Queue for Resource Adequacy.)

But the two state commissions said exclusion of the exemption this time around “usurps the exclusive authority of state retail regulators and their jurisdictional utilities to plan for adequate generation resources needed to provide resource adequacy within the jurisdictional footprint.”

Mississippi and Louisiana regulators said FERC should reject the cap or direct MISO to reintegrate the exemption into its plan. They said without a cap, MISO’s queue could limit or purge dispatchable resources like natural gas and nuclear units that will keep resource adequacy from degrading.

Despite the MISO South states’ opposition, Entergy and Cleco lent support to the cap. The two said MISO’s interconnection models are too bogged down to produce accurate study results for interconnection customers.

Duke Energy likewise supported the cap and said many of the recent rounds of submittals likely are “speculative projects with high withdrawal rates.”

Alliant Energy didn’t outright oppose the cap but said it harbored concerns that “serious risk” would remain on load-serving entities’ ability to interconnect projects in a timely manner. It asked FERC to hold off on a final decision on the cap until it also could weigh MISO’s upcoming expedited queue lane for resource adequacy projects. MISO plans to file the proposal for fast-track queue processing with FERC sometime in the first quarter of 2025.

MISO chimed in to remind stakeholders that the prior regulator exemption was part of a “previously rejected process that is not currently before the commission and not relevant for any purpose here.” MISO said it was being unfairly forced to defend its current filing based on the rejected one.

The RTO also said references to and making the cap contingent on its upcoming filing to fashion an RA expedited queue process are misplaced because the “budding” plan remains under development in the stakeholder process.

“MISO should neither be required to defend proposals previously rejected by the Commission in other dockets, nor should it be required to expand upon a … process that is still in development between MISO and stakeholders,” MISO said.

MISO said the cap proposal at its core merely asks FERC to “simplify a math problem — MISO’s study process — by limiting the number of variables — interconnection requests — it must solve for in each queue cycle.”

New England transmission owners no longer can require interconnection customers to pay operations and maintenance (O&M) costs for required system upgrades, FERC ruled Dec. 19 (EL23-16-00). The ruling could help reduce costs associated with interconnection in the region, potentially shifting some O&M expenses into transmission rates.

The decision responds to a 2022 complaint by trade organization RENEW Northeast, which was supported by major clean energy associations including the New England Power Generators Association and Advanced Energy United.

RENEW argued that the O&M requirement “can be a substantial burden on interconnection customers and can cause an unfair shifting of O&M costs from transmission customers to interconnection customers,” discouraging new development.

The association noted that New England is the only region in the country that requires interconnection customers to pay the O&M costs associated with interconnection upgrades.

“Because the O&M costs can be assessed for the 20- to 30-year duration of the [large generator interconnection agreement], the interconnection customer could pay O&M costs that exceed the capital costs of the network upgrades themselves,” RENEW wrote.

ISO-NE declined to take a position on the merits of RENEW’s complaint, writing that it has no financial interest in the matter. It asked to be dismissed as a party to the proceeding, arguing that the disputed parts of the RTO’s Open Access Transmission Tariff “are within the exclusive right” of the region’s transmission owners.

FERC denied the RTO’s request, writing that “retaining ISO-NE as a party to this proceeding will ensure that all parties required to make tariff changes pursuant to this order are parties to this proceeding.”

Meanwhile, the New England Participating Transmission Owners (PTOs), the New England States Committee on Electricity (NESCOE), the Massachusetts Attorney General’s Office and a group of consumer-owned utilities argued that RENEW did not meet the burden of proof to show that the O&M requirement is unjust.

“RENEW seeks to replace long-settled rules that put development risks and costs on interconnection customers with a one-sided bargain that shifts 100% of those costs to consumers,” NESCOE wrote.

The transmission owners argued that “the current allocation of interconnection costs … is the result of a grand compromise of many interrelated rights and obligations among generation owners, transmission owners, public power and end-use customers that was determined to be just and reasonable by the commission and should not be casually tossed aside by modification of a single component.”

FERC sided with RENEW, directing ISO-NE and the region’s transmission owners to submit a compliance filing within 60 days “removing from the tariff any language that provides for the assignment of network upgrade O&M costs to interconnection customers.”

FERC noted that Order 2003 allows transmission providers to assign “but for” costs — which FERC defines as costs that would not exist without the interconnecting project — to interconnection customers. However, FERC determined the O&M requirements are not covered by this provision.

“RENEW has provided substantial evidence that the network upgrade O&M costs that are being assigned to interconnection customers … do not reflect the actual but for network upgrade O&M costs that each interconnection customer’s interconnection request causes to be incurred,” FERC wrote.

FERC also accepted RENEW’s request to require the transmission owners to widen the definition of an “interested party” within the transmission formula rate protocols. RENEW and similar trade groups are not included in the existing definition of an interested party.

FERC wrote that the current definition “limits interested parties to a specific enumerated group and does not provide for sufficiently broad participation.”

RENEW applauded FERC’s order, writing in a statement that the ruling “will eliminate the risks and uncertainties for interconnecting power generators that increase costs to consumers for energy and potentially delay the transition to a cleaner energy grid.”

Joe LaRusso, manager of the Clean Grid Program at the Acadia Center, wrote on social media that “FERC has broomed away a significant obstacle to interconnection that was unique to New England.”

A representative of ISO-NE said the RTO is assessing the order to determine its next steps.

Pennsylvania Gov. Josh Shapiro on Dec. 30 filed a complaint with FERC on behalf of the state asking the commission to revise how the maximum clearing price in PJM’s capacity auction is determined, arguing that the current design could result in consumers overpaying by as much as $20 billion (EL25-46).

The state seeks to lower the price cap to 1.5 times the net cost of new entry (CONE) on the grounds that the status quo approach of using the greater of gross CONE or 1.75 times net CONE could result in high prices without any corresponding reliability benefit. It argued that 1.5 times net CONE is the theoretical price point to ensure that the reference capacity resource can remain in business on top of any energy and ancillary service (EAS) revenues, and that any price above that would be excessive.

It asked that the change be effective for the 2026/27 Base Residual Auction (BRA) and the following two auctions while stakeholders consider the market design more holistically through the Quadrennial Review process, which has been expedited by a year and is in the initial phases of the PJM stakeholder process with the Market Implementation Committee.

“The public interest simply cannot tolerate up to $20.4 billion in unreasonably high rates dictated by a steep demand curve that was designed for an entirely different environment,” Pennsylvania said. “To prevent an unjustly high auction price and to reflect current market conditions, PJM should be directed to return the price cap to 1.5 times net CONE until a new demand curve is established by the ongoing sixth Quadrennial Review.”

Under normal circumstances, the state said, a higher clearing price could create a stronger incentive for development of new resources. But PJM’s backlogged interconnection queue prevents the construction of any projects not already in line. Paired with several delays to the auction schedule that have compressed the three-year advance timeline to 11 months, it said that any developers seeking to respond to a high price signal would not be able to do so until the delivery year has passed.

“It is difficult to escape the conclusion that PJM’s capacity market is currently failing,” Pennsylvania said. “This is not one isolated failure: Respected analysts have ranked PJM’s interconnection queue process the worst in the nation. PJM has also habitually failed to run its capacity auctions on time — earning the distinction of being the only grid operator in the nation with a forward auction design that is effectively being held as a prompt auction.”

In a statement responding to the complaint, PJM said there is an imbalance between supply and demand creating an increasing risk of capacity shortages, in part because of state and federal policies that are causing generators to prematurely deactivate. It said it has proposed rule changes to FERC that would reduce the price cap and allow new generation to come online quicker.

The RTO has also implemented changes to its interconnection process to study projects faster, allowing about 50 GW to come out of the queue and move on to the next steps of development, it said. Many have run into roadblocks that PJM said are outside of its control, such as permitting, financing and supply chain challenges.

“We remain open to additional solutions to this generational challenge, as long as they support keeping the lights on. Service interruptions, brownouts and blackouts cannot be an option,” PJM said. “We have had productive engagement with the Shapiro administration and all of our states to date, and we appreciate their active engagement and advocacy. It will take all of us working together to help create the conditions for increased investment in new generation that is needed for long-term price stability as well as grid reliability for customers.”

Pennsylvania acknowledged the proposed revisions to aspects of the capacity market and how new resources can progress through the interconnection process, but it said the prospect that the 2026/27 auction will clear at an unreasonably high cap remains, and construction timelines make it unlikely that new resources could be online in time to add supply.

“Even PJM’s proposed ‘fast track’ Reliability Resource Initiative (RRI) — which Pennsylvania generally supports — is not projected to allow new resources to come online before the 2029/2030 delivery year [ER25-712]. These obstacles mean most new projects are unable to even get in line to join the PJM grid for the foreseeable future, and none can realistically expect to be delivering power within 11 months,” the state said, referencing the RTO’s proposal to allow 50 resources to be added to the Transition Cycle 2 queue based on their expected in-service date and deliverable capacity.

The state also argued that PJM’s proposal to undo a change to make the reference resource a combined cycle unit and revert back to a combustion turbine would resolve the concerns that led it to increasing the net CONE multiplier in the 2022 Quadrennial Review prices (ER25-682). Because CCs tend to rely on the energy market for a larger share of their revenues, there was a concern that high prices in that market could suppress capacity clearing prices even when new resources are expected to be needed. The 2026/27 BRA would be the first to use a CC as the reference resource, but PJM requested that FERC allow it to continue using a CT unit when it determined that net CONE would fall to zero in some zones.

A net CONE of zero would result in a substantially steeper variable resource requirement (VRR) curve that could swing capacity prices with relatively small changes in the amount of capacity offers, in addition to knock-on effects for other market constructs that use net CONE as an input. (See FERC Approves PJM Quadrennial Review.)

Pennsylvania said there is no theoretical basis for including gross CONE when defining the price cap, and it was added in the 2011 Quadrennial Review to address possible inaccuracies in the EAS offset, which it says have been resolved by the shift to forward-looking estimates of energy prices rather than historical data.

Even with the higher capacity prices that using gross CONE could lead to, Kris Aksomitis, director of commercial power development and strategy for consultancy Power Advisory, said in an affidavit that resources capable of coming online quickly are unlikely to be further incentivized to do so. Owners of mothballed assets would likely be wary of continued market volatility, and there is no evidence that demand response requires “scarcity-level pricing” to increase participation, he said. Projects already in the queue are also unlikely to receive interconnection service agreements in time to offer into the market.

“Setting the price cap at gross CONE is likely to increase capacity prices for the 2026/2027 BRA by as much as 50% relative to prices under a lower price cap, with no reasonable expectation of an incremental market response sufficient to justify the cost,” Aksomitis said. “This represents an unjustified wealth transfer, as the incremental capacity and reliability benefit are shown to be minimal and come at cost orders of magnitude greater than any reasonable estimate of the” value of lost load.

Pennsylvania acknowledged that load growth will push demand and prices higher, a process it said is already happening as designed with a surge in clearing prices in the 2025/26 auction to $269.92/MW-day, up from $28.92/MW-day in the prior auction. (See PJM Capacity Prices Spike 10-fold in 2025/26 Auction.)

“Indeed, record load growth is making it plainly evident that new capacity is needed in the marketplace, and the capacity market is responding as designed with a strong build signal,” it said. “Under these conditions, net CONE is functioning as intended and recently produced an all-time high RTO-wide capacity price in response to increasing supply-demand imbalance in July 2024.”

The Maryland Public Service Commission on Dec. 31 received an application from PSEG Renewable Transmission for the company’s Maryland Piedmont Reliability Project, a 67-mile, 500-kV transmission line that could be vital to power reliability in the state but has already sparked opposition.

The proposed line would run from a connection with a Baltimore Gas and Electric transmission line in northern Baltimore County, through Carroll County and end at a substation in Frederick County, near the state’s border with Pennsylvania. With a 150-foot-wide right of way, the project would cover approximately 1,221 acres, according to details in the application.

The 500-kV line would be built on “303 H-frame structures, consisting of two vertical tubular poles with an average height of 145 feet (varying from 85 to 195 feet) and an anticipated foundation diameter of 6 to 14 feet,” the application says. The distance between the pylons would vary from 800 to 1,400 feet, with an average of 1,200 feet.

PJM has warned the state repeatedly that new transmission is needed to meet growing demand from data centers and avoid potential power loss as existing fossil fuel plants are closed.

But Joanne Frederick, board president of Stop MPRP, a grassroots, nonpartisan group opposing the project, isn’t buying that argument.

“They have maintained all along that this was the only solution that would work, and we don’t believe them,” Frederick said in a Jan. 2 interview with RTO Insider. “This project, as proposed, is catastrophic to farmlands. It’s catastrophic to property values. It’s catastrophic to farming businesses. It’s catastrophic to several agri-tourism businesses. … We plan to argue against this project; against each of those broad negative impacts it would bring.”

Frederick is one of several individuals and groups that have raised concerns about the project, from individual farmers to Gov. Wes Moore (D), who has questioned how the new transmission line would benefit the state and its residents.

Opponents argue that MPRP was designed to bring power from Pennsylvania to data centers in Northern Virginia, but Maryland residents could end up paying a major part of the project’s $424 million price tag.

PSEG has laid out a schedule for MPRP that includes PSC approval of a certificate of public convenience and necessity by the end of 2025, with construction beginning in 2026 and the project going online in 2027.

The PSC soon will announce the date for a pre-hearing conference to set an administrative schedule and consider petitions from individuals and groups seeking to intervene in the case, according to Communications Director Tori Leonard. The commission also will schedule public hearings on the project in Baltimore, Carroll and Frederick counties, she said.

“PJM has determined that the bulk 500-kV electric transmission system serving large parts of Maryland is forecasted to experience serious reliability violations including thermal overloads and voltage collapse violations (blackout) in 2027,” PSEG said in its application. “If these serious reliability violations are not addressed, it could compromise overall system reliability in the PJM region, including for Maryland customers, and could lead to widespread and extreme conditions, including system collapse and blackouts.”

Maryland imports about 40% of its power from the regional grid, and PJM has said the threats to reliability are so severe that upgrades to increase capacity on existing lines, by installing advanced conductors or other grid-enhancing technologies, would not be sufficient, the company said.

PSEG also has said its proposed route was chosen out of 10 alternatives because it “impacted fewer conservation easements, had fewer residences and community facilities in close proximity to the right of way, and it was shorter and had fewer hard turns, which reduces cost and complexity.”

The route also avoids Civil War battlefields and state parks, PSEG said in the application.

Responding to community requests that the line be run along existing rights of ways, PSEG said doing so “would require removing over 90 residential homes and community buildings.” However, the proposed route would require easements on private land.

According to PSEG’s website for the project, the company has started reaching out to landowners on the proposed route to talk with them about the project and answer questions. The company will seek temporary right-of-entry agreements “to conduct surveys and other studies needed to assess the suitability of the property for the MPRP and to gather information needed for the CPCN evaluation.”

PSEG counters concerns about who will pay for MPRP by noting that as a PJM project, the cost will be allocated to customers across the RTO’s service territory, which includes 13 states and D.C. It also estimates $306 million in project benefits for Maryland, including “direct, indirect and induced positive economic impacts over an assumed 30 years of operations” and 1,709 full-time jobs during construction.

Possible Legislation

The company first released a map of its 10 alternative routes in July 2024, followed by the announcement of the preferred route in October. PSEG held three public meetings, one in each of the affected counties, in November.

Project opponents argue the rollout schedule did not leave enough time for individuals and communities to study the proposed route and provide informed feedback.

PSEG’s public meetings were a step in the right direction but not sufficient, said Kim Coble, executive director of the Maryland League of Conservation Voters.

“There needs to be more conversations,” Coble said in a Jan. 2 interview with RTO Insider. “You can fill a room with a bunch of people and a PowerPoint [presentation], and that does not equate into meaningful engagement of the communities that are impacted. There’re conversations; there’s listening; there’s [asking], ‘What are your concerns, and how can we help address them?’”

In a Nov. 22 statement, Gov. Moore laid out his own “grave concerns about how the study area for this project was determined, the lack of community involvement in the planning process and the lack of effective communication about the impacts of this project.”

Maryland lawmakers plan to introduce legislation that could slow the approval process for PSEG and the MPRP.

Del. Jesse Pippy (R), minority whip in the House of Delegates, is working on a bill that could require PSEG to provide more documentation of the alternative routes the company considered.

PSEG “kept their cards very close to their chest,” Pippy told WBAL. “So, what we want to ensure is that when the Maryland Public Service Commission is making decisions, they are requiring these applicants to consider alternative routes.”

Senate Minority Leader Justin Ready (R) may propose a bill to ensure that farmers displaced by the project receive a 350% premium for any of their land taken by eminent domain, according to WBAL.

Stop MPRP’s Frederick also wants further study of alternatives to the project, such as combining system upgrades with grid-enhancing technologies and a new natural gas plant.

“What’s the [difference] between … the negative environmental impact of a new, clean natural gas power plant versus the negative environmental impact of wiping out 473 acres of old-growth forest, of doing that kind of environmental damage to wetlands, woodlands across Maryland?” she said. “We owe it to ourselves to understand the facts; to clearly articulate the choices we should be making and not just ignore them.”

The U.S. offshore wind industry will find out soon where election rhetoric turns into action or turns into hollow words.

Donald Trump’s pledges and threats on the campaign trail suggest he will attempt many transformational changes. But few targets have been identified so clearly and firmly as when Trump said he would end offshore wind on Day 1 of his second term as president.

It was a classic campaign rally message: bold and decisive but devoid of details, delivered to a friendly crowd on a beach in New Jersey, an epicenter of offshore wind opposition.

But given Trump’s longstanding antipathy toward offshore wind, it may have been more than a soundbite.

The industry has attracted tens of billions of dollars in investment and put thousands of Americans to work as it attempts to build a new U.S. power sector.

That would seem to check a lot of Trump’s favorite boxes, many advocates note — if it did not entail thousands of giant wind turbines along the nation’s coastlines.

Path of Most Resistance

Analysts, advocates and industry members speaking to RTO Insider or to public and private audiences in late 2024 see a variety of ways President Trump could thwart offshore wind development.

There is the executive order — bold and decisive but subject to court challenge.

Indirect measures would be harder to fight and could net similar results:

Refusing to defend specific projects against litigation.

Slow-walking permit reviews.

Not holding auctions.

Moving to reduce or eliminate tax credits.

Limiting the funding and staffing for regulatory agencies.

Jacking up tariffs on the expensive (and still almost entirely foreign) components of offshore wind farms.

Creating a level of uncertainty that scares off the investors needed to build factories, ships, ports, workforce and other parts of an industrial ecosystem.

Given Trump’s deliberately unpredictable leadership style, it is hard to guess what he will do. Even the more predictable presidents have been known to say one thing and then do another.

An all-of-the-above energy portfolio with both fossil and renewable energy is backed by many Republicans, including former North Dakota Gov. Doug Burgum, whom Trump has chosen to head the Department of the Interior, lead agency on offshore wind regulation.

During Burgum’s eight-year tenure, North Dakota doubled its installed onshore wind generation capacity to more than 4 GW.

Offshore wind advocates have their hopes. But analysts and observers whose comments were reviewed for this report expect U.S. offshore wind development to be at least somewhat stunted during Trump 2.0 — not a full-on implosion but probably well short of the robust growth of the Biden years.

Headwinds

In a mid-December update to clients, ClearView Energy Partners said it sees two scenarios for Trump to deal with offshore wind: Retaliate against one of Biden’s prized initiatives by actively moving to thwart it, or merely refocus resources elsewhere, letting it sputter along without support.

One can envision reasons for both scenarios, ClearView wrote, but Trump’s past attacks on renewables are not necessarily the best indicator: “Campaigning is one thing, and governing is another. Trump has demonstrated a mercurial willingness to reverse or modify his prior stated positions.”

Killing permitted offshore wind projects on principle also would run counter to Trump’s goal of energy dominance and be counterproductive in a time of growing concerns about resource adequacy, Clearview wrote.

Three South Fork Wind turbines are shown off the New York coast in early 2024. | South Fork Wind

Wood Mackenzie said the impact of the Trump administration’s decisions could vary considerably. Restricting permitting and leases would not have much effect on the 10-year outlook, it said, given that nearly 25 GW of projects are far along in the permitting process or have completed it. Limiting finances, on the other hand, would have a greater effect.

“If the administration chooses to not issue guidance on the domestic content bonus credit for offshore wind, or pares back the 45X advanced manufacturing tax credit, investments in a domestic supply chain could be significantly delayed,” Wood Mackenzie analyst Stephen Maldonado said in mid-November. “While Wood Mackenzie’s base case outlook expects 27 GW of cumulative installed capacity by 2033, the compound effects of these constraints could lead to a 30% decrease over the same time frame.”

In a subsequent update in mid-December, Wood Mackenzie said change already was underway, with some early stage U.S. projects mothballed or paused. It said: “The segment’s longer lead times may limit the immediate impact on 2025 budgets, but offshore wind is set to slide down the investment priority list for many diversified renewables developers next year.”

During an American Offshore Wind Academy webcast in mid-December, Boston Consulting Group Managing Director Jeremy Merz said Trump could pull many levers, ranging from financial disincentives to executive orders to a permitting slowdown.

He expects a mid-range approach with mid-range effects on the industry. Individual projects would sustain greater or lesser impacts depending on where they are in their timeline — those that are fully permitted with offtake agreements and a clear path to construction are at much less risk than those that merely have secured a lease and are in early planning.

“I don’t believe it will actually lead to death of offshore wind in the U.S. I think that’s a very, very unrealistic scenario,” Merz said.

But he added: “Given the increased uncertainty that we have at the moment, investors, developers will probably shift some of their capital to offshore wind outside of the U.S., or to other energy sources in the U.S.”

Yvan Gelbart, lead analyst at Spinergie, wrote in mid-November that Trump’s potential actions all could create short-term headwinds for the industry — even a 10% increase in capital costs due to tariffs would render many projects unviable.

He noted, however, that the election cycle brought no significant changes to the leadership of the states that are helping to drive offshore wind development.

Gelbart wrote: “State-level support and approved project pipelines will help mitigate some of the federal-level challenges. While progress may slow, it’s unlikely to come to a complete halt. … The coming years will be trying, but with careful navigation, the industry may weather this storm.”

For a different perspective, look at GE Vernova, a giant among power equipment manufacturers.

It has not taken an offshore wind turbine order in more than three years. Its decision to halt development of an 18-MW model was blamed for the collapse of an entire offshore wind solicitation totaling more than 4 GW in New York in early 2024.

But it has expanded its gas turbine manufacturing capacity.

Consider two paths to 9 GW of generation capacity: In 2019, New York set a 9 GW offshore wind goal and gave itself 16 years to reach it. Shortly after Trump was reelected in 2024, GE Vernova needed just 30 days to book reservations for 9 GW of new gas-fired turbines.

CEO Scott Strazik said during an investor update in mid-December that the company will not chase bad offshore wind deals. Two days later in an interview with Bloomberg News, he doubled down: “The reality is, the economics of this industry don’t make sense.”

GE Vernova will need to start from scratch to assess the finances of offshore turbines, Strazik told Bloomberg, with pricing more analogous to nuclear power than to onshore wind or solar.

Strazik’s comments touch on a larger problem: Whatever effect Trump may have on U.S. offshore wind in 2025, the industry was not swimming along smoothly in 2023 and 2024. It sustained significant setbacks in both years, even as it logged significant progress.

History May Not Repeat

It is probably unwise to predict how offshore wind will fare during Trump 2.0 based on what happened during Trump 1.0. First, the U.S. industry of the mid-2020s is far advanced from the late-2010s industry. More important, President Trump is “mercurial.”

But consider a December 2018 Department of the Interior news release on a Massachusetts wind lease auction titled: “BIDDING BONANZA! Trump Administration Smashes Record for Offshore Wind Auction with $405 Million in Winning Bids.”

Then-Interior Secretary Ryan Zinke goes on to say: “To anyone who doubted that our ambitious vision for energy dominance would not include renewables, today we put that rumor to rest. With bold leadership, faster, streamlined environmental reviews, and a lot of hard work with our states and fishermen, we’ve given the wind industry the confidence to think and bid big.”

Walter Cruickshank, then-acting director of the Bureau of Ocean Energy Management, added: “This auction will further the Administration’s comprehensive effort to secure the nation’s energy future.”

The first monopile for Equinox’s Empire Wind 1 project off the coast of New York is completed Nov. 28 at Sif’s facilities in the Netherlands. | Sif Group

So the Trump administration presented at least the appearance of an all-of-the-above approach to energy development.

One also could count the number of announcements Interior has made about offshore wind. There have been 215 under Biden as of late December 2024; 131 during the last five years that Barack Obama was president; and just 43 during Trump’s four years in office.

Or one could ask James Bennett, who was BOEM’s manager of renewable energy programs during the Trump administration and parts of the Obama and Biden administrations.

During an early-November webcast staged by the American Offshore Wind Academy, Bennett suggested the effusive news release about the Massachusetts auction was disingenuous.

“By then, some of the policies had taken hold, and there were some slowdowns, if you will, in the latter part of the Trump administration, which, of course, changed quite a bit with the incoming Biden administration. And it’s been going very, very aggressively since then.”

Bennett also reminded viewers that offshore wind was little more than a paper industry in the United States in 2016. It is now a multibillion-dollar endeavor — and those are much harder to shut down with the flick of a switch.

Pushing Forward

The day after Trump won reelection, Oceantic Network reminded him of the economic value of offshore wind, and of his earlier role in building it.

Several weeks later, Senior Vice President Stephanie Francoeur told NetZero Insider that this remains the strategy. Wind farms totaling 4 GW of capacity are under construction in U.S. waters, dozens more gigawatts of capacity are moving closer to construction, $41 billion in investments have created thousands of jobs and the supply chain spans 40 states.

All this began during the first Trump administration, she added.

“This new administration is signaling a seriousness with expanding domestic energy production, and we really believe that offshore wind energy is going to be a critical part of that future energy mix,” Francoeur said.

Nick Guariglia, outreach manager for the New York Offshore Wind Alliance, said rolling with changes in administration is an indispensable part of offshore wind development — no project can get done in four years.

New York’s South Fork Wind started development under Obama, continued during Trump and became the first completed utility-scale wind farm in U.S. waters during the last year of the Biden presidency.

“There were always going to be changes in Washington,” Guariglia said flatly.

His membership is neither optimistic nor pessimistic about Trump’s return. The industry is fine-tuning its message to emphasize priorities it shares with Trump and continuing with its business, he said.

“We have produced jobs. We’ve spurred economic development. We are literally creating new tax revenues for local municipalities.”

Kelt Wilska, offshore wind director at the Environmental League of Massachusetts, said he was excited to see Massachusetts Gov. Maura Healey redouble her state’s commitment to offshore wind.

He said states can counter federal headwinds facing the offshore wind industry by offering their own support through aggressive procurements and through supply chain development, both of which the Bay State has done.

It sends an important message of confidence to the industry and to other states, Wilska said.

“This is a national industry,” he said. “It’s taking off everywhere. I give examples of New England, because that’s where I work, but this truly is a regional and also a national industry that is vulnerable.”

That speaks to a key part of the strategy for the offshore wind industry and the larger renewables industry as it attempts to move forward through the Trump years.

The Inflation Reduction Act passed with not a single Republican vote, yet its economic benefits are flowing to Republican-controlled areas.

At the two-year anniversary of the signing of the IRA, the energy and environment advocacy group E2 tallied 334 major announced clean energy/clean vehicle projects. Of these, 278 offered estimates of job creation (total: 109,278) and/or private capital investment ($126 billion).

E2 calculated that 60% of the 334 announcements were in Republican congressional districts, and that they represented 68% of the new jobs and 85% of the investments.

Clean energy advocates hope enough legislators in the slim Republican majorities in both houses of Congress will want to protect those gains that they can temper Trump’s harshest moves.

U.S. Rep. Salud Carbajal (D-Calif.), co-chair of the Congressional Offshore Wind Caucus, said via email that attempts at persuasion already have begun:

“The bipartisan Offshore Wind Caucus has been committed to educating members of Congress about the economic benefits of this burgeoning industry and working across the aisle to support the renewable energy job creation happening in communities across America. I’m confident that it will continue doing that work in the next Congress and will look to engage with the incoming administration to help them see the support this homegrown American energy source has throughout the country.”

Dominion Energy, which is building the nation’s largest offshore wind project to date, expects to finish on time and on budget regardless of partisan politics. It has important advantages over other developers: It is a regulated utility with itself as the offtaker, and it locked in cost certainty on the project before macroeconomic factors began to shake the offshore wind industry.

Spokesperson Jeremy Slayton said via email: “Virginia’s clean energy transition and our ‘all of the above’ strategy, including Coastal Virginia Offshore Wind, have been underway for several years under multiple state and federal administrations and with bipartisan support from policymakers at every level.

“Bipartisan leaders agree it has been an economic boom for Virginia, creating thousands of jobs and stimulating billions in economic growth, while providing consumers with reliable and affordable energy. Leaders from both parties also agree on the importance of American energy dominance, maintaining our technological superiority and creating good-paying jobs for Americans.”

A first-of-its-kind power purchase agreement will send more than 10 million MWh of power to federal buildings and help Constellation Energy increase the output from its nuclear fleet.

Constellation and the U.S. General Services Administration announced the contract Jan. 2. The 10-year deal is valued at $840 million and is accompanied by a $172 million contract for Constellation to provide energy savings and conservation upgrades at five GSA facilities in the D.C. region.

In its news release, GSA framed the announcement with the multipronged benefits of boosting U.S. nuclear generation capacity, protecting taxpayers from price hikes and helping 14 government entities transition to 100% carbon-free electricity by 2030.

Constellation operates the largest U.S. reactor fleet. The contract will help it meet the costs of extending licenses for its existing nuclear plants and installing upgrades that will increase their output by a combined 135 MW. It covers 80 federal facilities in five states within PJM territory and will begin in April.

GSA called the contract historic and said it was modeled on long-term corporate carbon-free procurements.

Not all of the power supplied under the deal will be carbon-free. Neither side specified the anticipated percentage, but GSA said that over the next decade, it would purchase 2.4 million MWh of Constellation’s newly expanded nuclear output, as well as the associated energy attribute certificates.

For Constellation, the agreement is another step toward the market certainty it needs to invest in nuclear power. For example, the company announced its 2024 request to renew the license for its Dresden nuclear facility with the caveat that it needed “adequate market or policy support.”

Corporate predecessor Exelon had planned to retire Dresden and another Illinois facility early, then kept them open when the state implemented policy changes in 2021. Constellation is now planning to restart a reactor at the former Three Mile Island facility to supply electricity to Microsoft data centers.

In Constellation’s news release Jan. 2, CEO Joseph Dominguez spoke of the value proposition his company’s “clean energy centers” present.

“For many decades, Constellation’s nuclear fleet has provided carbon-free, reliable, American-made energy to millions of families and institutions,” he said. “Frustratingly, however, nuclear energy was excluded from many corporate and government sustainable energy procurements. Not anymore. This agreement is another powerful example of how things have changed.”

He said the GSA agreement, like the previous agreements with Microsoft and other entities, “will allow Constellation to relicense and extend the lives of these critical assets.”

The energy will be supplied to the Architect of the Capitol, the GSA, the Social Security Administration, the Army Corps of Engineers, the Department of Veterans’ Affairs, the Department of Transportation, the U.S. Mint, the U.S. Railroad Retirement Board, the National Archives and Records Administration, the Federal Bureau of Prisons, the Federal Reserve System, the National Park Service, the National Oceanic and Atmospheric Administration, and the Washington Metropolitan Area Transit Authority in locations the agencies own or operate in Illinois, Maryland, New Jersey, Pennsylvania and Ohio.

The energy savings performance contract awarded to Constellation includes lighting, weatherization, HVAC and building control upgrades to increase energy efficiency, decrease emissions and lower energy costs.

Work will start shortly and continue for 42 months. The centerpiece is the conversion of four D.C.-area buildings from steam to electric boilers and heat pumps. Constellation also will provide preventive maintenance services and train GSA personnel.

NERC has urged power grid operators to take action to “ensure the highest levels of reliability” ahead of a wave of extreme winter weather predicted to blanket much of North America in the first weeks of January.

“The reliability of the North American electric grid is the key priority for NERC — we know 400 million North Americans are counting on an uninterrupted supply of electricity to support our way of life,” NERC said.

NERC noted in its release the issue of a hazards outlook by the National Weather Service forecasting “extremely low temperatures, damaging winds, snow and freezing rain” across the U.S. East Coast, Southeast and Midwest that could lead to “a series of successive events that could create challenges for those reliant on inventoried fuels.” The ERO said it’s particularly concerned about the supply of natural gas, which is used for electric generation and home heating.

NWS’s most recent outlook, covering the week of Jan. 10-16, is consistent with these warnings, forecasting a combination of low pressure in the eastern U.S. and high pressure in the West and Greenland that likely create a “deep trough” to “funnel Arctic air into the Lower 48 east of the Rockies.” The outlook said there is a greater than 60% chance of “much below-normal temperatures” for much of the Southeastern U.S. on Jan. 9-11, meaning daily minimum temperatures that are less than the 15th percentile and near or below freezing.

Even Florida faces the potential of a hard freeze, NWS said. Low pressure conditions also could lead to “widespread breezy conditions and very low wind chills,” with at least a 20% chance of wind speeds passing the 85th percentile over the Northern and Central Plains Jan. 10-14.

Heavy snow also is possible across the central and eastern Continental U.S. in the middle of the covered week, and even in the Southeast — along with other precipitation types — due to moisture from the Gulf of Mexico. NWS noted that earlier outlooks predicted moderate risks of heavy snow between Jan. 9 and 15, but this has been changed to a slight risk. The change is due partly to lower predicted snowfall totals, but also because models indicate “some of the anticipated heavy snow” shifting into the preceding week.

In a video statement, NERC CEO Jim Robb said the coming cold weather could represent a “major” challenge to grid reliability and reiterated the ERO’s call for action from the industry.

“While forecasts are forecasts and undoubtedly contain error, these systems do seem to have the potential to bring a prolonged period of very cold weather — as cold as single digit temperatures in the U.S. South,” Robb said. “As a result, I’m asking everyone in the electricity supply chain … to take all appropriate actions to ensure that we can maintain an uninterrupted supply of electricity to customers. … The actions you take now may very well help us avoid the consequences of events such as we saw in Texas in 2021 and the Mid-Atlantic in 2022.”

Winter weather has been a growing source of concern for NERC and the rest of the ERO, with the organization warning in this year’s Winter Reliability Assessment that all or part of multiple regions face elevated risk of energy shortfalls from extreme winter conditions. NERC said rising demand and retirements of thermal generation capacity contribute to slimmer reserve margins across the continent. (See NERC Sees ‘Reasons for Optimism’ as Winter Approaches.)

MISO will waste no time in 2025 trying to blunt the threat of a shortage that could arrive in the summer months by encouraging new generation and enacting more resource adequacy measures.

MISO leadership spent 2024 reiterating that the grid operator is on a collision course with a supply deficit unless members get more projects built, it supercharges transmission planning and it can persuade members to stave off generation retirements.

During MISO’s Board Week Dec. 10-12, MISO executives said they would pursue large-scale load shedding drills among the membership, indicating the RTO anticipates blackouts.

However, MISO CEO John Bear said he feels that MISO has accomplished more in terms of resource adequacy in the past “three years versus the last 10.”

“I do feel like we’re at a little bit of inflection point though,” Bear said at a Dec. 12 MISO Board of Directors meeting. He said though MISO is cleared to roll out a sloped demand curve in its seasonal-based capacity auctions this spring, a new capacity accreditation by 2028 and has attained board permission for its newest long-range transmission plan, it still faces a resource gap as soon as summer.

“Now we need members to revise their plans and really roll up their sleeves. … We’ve got to get resources added to the system,” Bear said. He added that even before the surge in data center growth projection, MISO and the Organization of MISO States’ (OMS) resource adequacy survey indicated reserve margin deficits could occur within months.

In September, MISO Independent Market Monitor David Patton agreed MISO is implementing resource adequacy improvements at a “remarkable” clip — a good thing for the sake of future reliability.

“The seasonal capacity auctions and reliability-based demand curve are being implemented in a third of the time it takes other RTOs,” Patton said.

“Pressures on resource adequacy from fleet transition and projected large spot load additions continue and will increase unless MISO and members take mitigating action,” Durgesh Manjure added during MISO’s mid-September Board Week.

“We are losing megawatts faster than we can replace them,” he emphasized.

Manjure also said the generator interconnection queue isn’t the source of guaranteed resource additions that it used to be. He said approximately 57 GW of new resources have attained interconnection agreements but remain unfinished largely due to straggling supply chains. Manjure said projects could face anywhere from three to seven years of delay before megawatts materialize on the system after signing their interconnection agreements.

The true conversion rate of the interconnection queue “is becoming more and more nebulous,” Manjure said. “It’s becoming harder to predict what’s going to come online.”

However, he said there’s “no dearth” of projects in the queue. Staff often point out that MISO’s 312-GW interconnection queue alone is more than twice the RTO’s peak load.

MISO in late 2024 concluded its members need to add projects at an “unprecedented” 17 GW/year clip to achieve resource adequacy while decarbonizing the grid. That’s triple the rate members have added per year over the past few years. (See MISO Assessment Calls for 17 GW in New Resources Annually.)

The Need for Queue Speed

To get more new generators churning out energy sooner, MISO is fashioning an express lane in its interconnection queue for projects that bolster resource adequacy. The idea — which is set for more workshopping with stakeholders in the coming months — would have select generation developers entering a fast lane devoted to projects with authorization from their state authorities. MISO would perform individual, rather than batch, studies on the projects and funnel them to interconnection agreements quicker. (See MISO Tells Board RA Fast Lane in Interconnection Queue is a Must.)

MISO’s emphasis on needing more generation expeditiously appears incompatible with its call in late 2024 to officially skip acceptance of a 2024 cycle of queue projects for study. But the RTO insists it has good reason to take a step back — it’s working with a tech startup to create a more automated queue that turns out studies faster. (See MISO to Skip 2024 Queue Cycle While it Automates Study Process with Tech Startup.)

If MISO gets its way, it will process smaller queues this year and into the foreseeable future. The grid operator has filed with FERC to impose a 50% peak demand cap on the project submittals it will accept into its interconnection queue annually. The 2025 cycle of queue projects is tentatively scheduled to kick off in the third quarter, since MISO intends to have the cap in place before it formally accepts a new cycle. MISO has said smaller queue classes will make interconnection studies workable and realistic.

Sloped Curves to Net More Capacity

MISO’s springtime capacity auctions for the 2025/26 planning year will be the first to feature a sloped demand curve. The grid operator hopes to use the curves as a safety net to have more capacity on hand than strictly necessary to meet planning reserve margin requirements. FERC allowed MISO to use them in place of the vertical demand curve it had been using since 2011. (See FERC Approves Sloped Demand Curve in MISO Capacity Market.)

Amid talk of heightened operating risks, MISO filed to increase its current $3,500/MWh value of lost load to $10,000/MWh. The plan is pending before FERC.

MISO, OMS to Outline Possible New Resource Adequacy Standard

Further, MISO has promised to work with state regulators in 2025 to come up with a potential new direction on its resource adequacy standard.

MISO has said it might draw on a combination of measurements gaining attention across the industry, including:

Its existing loss of load expectation to capture frequency of events.

Expected unserved energy to capture the size of events.

Loss of load hours to capture event duration.

Value at Risk or Conditional Value at Risk to measure the magnitude of the aftermath of worst-case events.

MISO Director of Strategic Initiatives and Assessments Jordan Bakke told attendees at a November Resource Adequacy Subcommittee that “more investigation is needed” to figure out how risk will play out as its system evolves. MISO has suggested its current loss of load expectation criterion could in the future lead to “materially higher risk” by underestimating system vulnerability.

Bakke said MISO’s one-day-in-10-years loss of load resource adequacy standard “has a number of limitations.” But he also said MISO believes it has some time on its side because the new risks the industry is trying to steel itself against will arise from a “highly evolved” system that is a few years down the road. Bakke pointed out that MISO’s Regional Resource Assessment shows that within 20 years, risk will swing from summer to winter, with emergency events expected to grow in size and be longer lived.

OMS is standing up a devoted resource adequacy committee to work with MISO. Bakke said the RTO will collaborate with OMS throughout 2025 to develop a recommendation on preferred changes to resource adequacy criteria at the end of the year.

Bakke added “it’s too soon to know” when MISO might be able to employ new criteria. He said it’s MISO’s goal to “illuminate the topic” by providing risk assessments while OMS holds deciding power.

Executive Director of Market and Grid Strategy Zak Joundi has said “we were fortunate in the past” to operate the system reliably simply by preparing for summer peak load.

“That’s no longer the case,” he told attendees at the March MISO Board Week.

Futures to Become Bolder

The grid operator will take a break from long-range transmission planning over 2025 to refurbish its three 20-year futures scenarios, which form the foundation of MISO’s long-term transmission planning. (See MISO Pauses Long-range Tx Planning in 2025 to go Back to the Futures.) The RTO has promised to come back in 2026 with another portfolio of long-range transmission projects for its Midwest region.

Bear said the changing world means it’s time for MISO to revisit its 20-year transmission planning futures and contemplate more load growth, more electrification and a resource transition in overdrive.

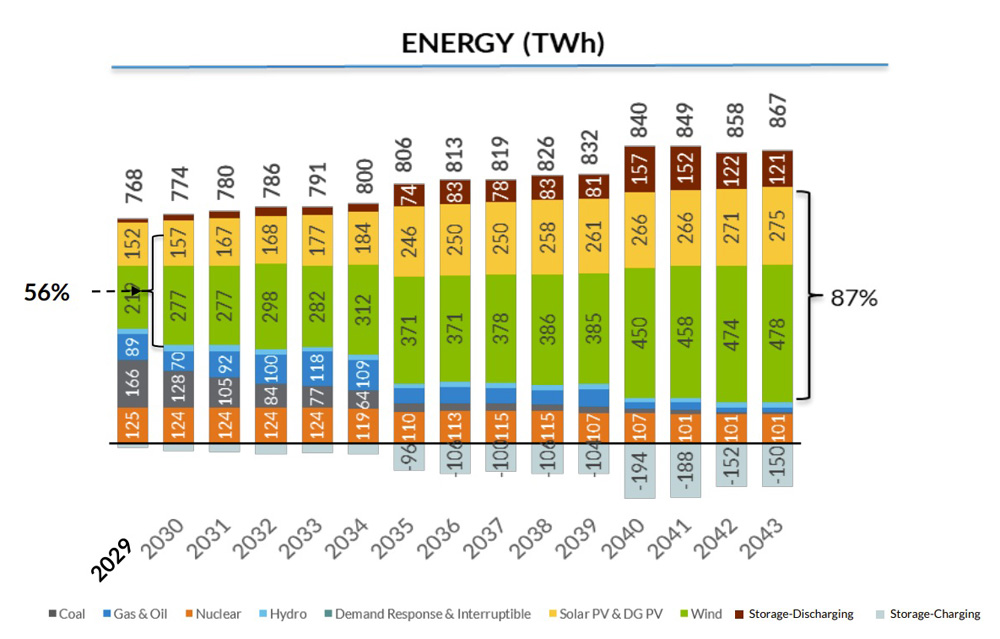

MISO’s projected resource portfolio from its 2024 Regional Resource Assessment. The RTO predicts a 56% share of renewables in 2030 and an 87% share by 2043. | MISO

Meanwhile, regulatory work will begin on MISO’s second, nearly $22 billion LRTP portfolio, approved in December. MISO staff have vowed to appear before state commissions to vouch for the transmission’s importance in its members’ resource planning. (See MISO Board Endorses $21.8B Long-range Transmission Plan.)

Director of Cost Allocation and Competitive Transmission Jeremiah Doner called the second LRTP portfolio a “step forward for the system in the 765-kV transmission,” pointing out that swaths of MISO Midwest lack a 765-kV backbone.

Load Growth Looms

Bear said while MISO has accomplished more resource adequacy initiatives than ever before through the stakeholder process in 2024, he joked that the “bad news” is MISO and stakeholders must consider several more in the coming months.

“My concern is that all the things we’re seeing, our neighbors our seeing. Our reserve margins are getting tighter, and we’re seeing load growth … not seen since the ‘60s and ‘70s,” Bear said during the September board meeting.

“When you start adding load additions the size of small cities, you really have to step back,” he said.

“MISO folks need to stay ahead of the curve,” Board Chair Todd Raba agreed at the time.

MISO executives expect load to grow by about 60% by 2040. That will be paired with an anticipated 87% renewable energy output from the RTO’s fleet. By 2030, the RTO expects more than 50% renewable energy output.

MISO expects a 10%-14% increase in load over the next few years, fueled primarily by the rise of data centers.

“There’s not a state in our footprint that doesn’t want to see that economic development,” MISO’s Bob Kuzman said at Infocast’s inaugural Midcontinent Clean Energy conference in late August.

However, Kuzman warned that data centers need dispatchable, at-the-ready resources. He warned that the replacement generation coming online needs to have the same reliability attributes that departing thermal generators were able to furnish.

“These large AI and data centers need power 24/7/365. … They are not interruptible,” he said.