Previewing NERC’s Summer Reliability Assessment at the ERO’s quarterly technical session May 8, Director of Reliability Assessment and Performance Analysis John Moura warned that the organization expects significant challenges to grid reliability during periods of extreme heat.

NERC publishes the assessment annually to identify potential regional reliability issues and topics of concern in the June-to-September time frame. According to the timeline Moura presented at the technical session, the report has been submitted to CEO Jim Robb for approval and will be sent to the Board of Trustees later this week. The organization plans to publish the assessment May 15.

Hot conditions are likely across the U.S. and Canada this summer, Moura said; the National Weather Service predicts a greater than 50% chance that New England and most of the Southwest will experience above-normal temperatures, and at least a 1-in-3 chance in the rest of the U.S. Canada also forecasts a high probability of above-normal temperatures across all provinces.

The report also noted the risk of drought across large areas of North America, with abnormally dry conditions predicted in the Northwest U.S. and eastern Canada, and moderate to extreme drought in the Southwest and western Canada. Drought conditions could lead to higher wildfire risk, along with reduced hydropower output.

Moura emphasized the ERO expects all regions to “have an adequate electricity supply for normal peak conditions,” just as it did when it issued last summer’s assessment. (See NERC Warns of Summer Reliability Risks Across North America.) This comes despite 12 of the 20 assessment areas projecting a higher peak demand than in past summers; Alberta and British Columbia lead the pack with predicted increases of 8.9% and 7.4%, respectively, while Quebec’s expected growth is the lowest at 0.3%.

Reserve margins in many areas also are expected to be higher than last year thanks to the addition of new resources and demand response. For example, the Western Interconnection is adding solar and battery capacity; Ontario authorities have rescheduled maintenance activities to make more nuclear generation available; SERC Central has added natural gas and solar generators; and multiple areas have lined up firm imports.

But while normal conditions are not a major concern, Moura said extreme scenarios are a different story. Long periods of widespread high temperatures raising demand across multiple regions could limit the ability of individual assessment areas to import power, because neighbors likely will have similar demands. The ERO also foresees difficulty for areas with high levels of wind, solar or hydropower to meet their needs when those resources run low.

Moura said the published assessment will provide several recommendations for industry, including that reliability coordinators, balancing authorities and transmission owners in areas with elevated risk review their operating plans and protocols for supply shortfalls. He also said NERC will ask owners of solar generation resources to implement the recommendations in the Level 2 alert for inverter-based resources the ERO issued last year.

ISO-NE predicts New England’s peak load will increase by about 10%, and electricity consumption by 17%, by 2033, according to its 2024 Capacity, Energy, Loads and Transmission (CELT) report, released May 1.

The increasing peak load forecast is driven by increasing transportation and building electrification, ISO-NE said. The estimate is a slight decrease from the peak load projections in the 2023 CELT report. (See ISO-NE Decreases Its 10-year Peak Load Forecast.)

While the New England grid currently peaks in the summer, ISO-NE projects the winter peak to grow significantly faster, with a projected increase of about 33% over the next decade.

In 2033, ISO-NE expects the region’s summer peak to reach 27,052 MW and the winter peak to reach 26,768 MW. The RTO expects winter peaks will surpass summer peaks in the mid-2030s because of heating electrification.

The New England power system reached its peak load in 2023 on Sept. 7, topping out at just over 24,000 MW.

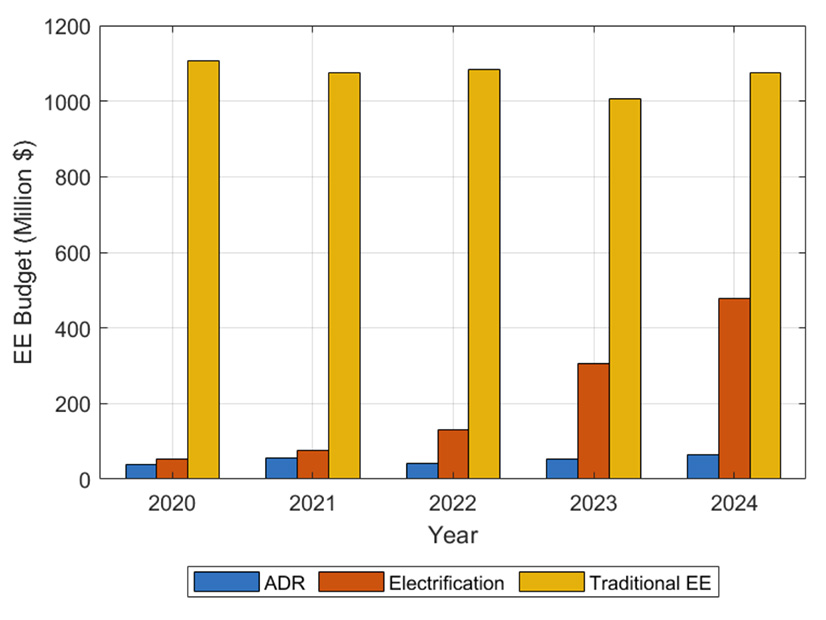

Energy use in New England has declined since the early 2000s, largely because of energy efficiency programs and behind-the-meter solar. However, ISO-NE projects the amount of energy efficiency participating in its capacity market to decline in the coming years as states shift their focus toward building electrification and heating retrofits.

New England states’ energy efficiency budget allocations | ISO-NE

In a recent presentation, ISO-NE noted that state energy efficiency budgets “have remained consistent, while production costs have increased.” In contrast, states have dramatically increased funding for electrification programs over the past four years and have slightly increased funding for active demand response.

ISO-NE projects energy efficiency resources that expire and exit the market will outpace energy efficiency resource additions by 2029.

“Since [Forward Capacity Auction] 14, the amount of expiring EE measures has been surpassing the pace of new EE cost-of-service agreements entering the market,” ISO-NE spokesperson Mary Cate Colapietro noted.

And 2024 marks the fourth consecutive year in which the RTO’s energy efficiency forecast has declined.

While ISO-NE indicates it expects BTM solar capacity to continue to grow at about 1,000 MW per year over the next decade, it projects solar will reduce the region’s peak load by just over 200 MW by 2033. (See NEPOOL Participants Committee Briefs: May 3, 2024.)

Colapietro noted that increasing amounts of BTM solar “will shift the timing of peaks to later in the day when the panels produce less power.”

ISO-NE projects BTM solar will reduce total energy demand by about 10,000 GWh in 2033 — down 6.6% compared to gross energy demand — compared to about a 4,000-GWh reduction in 2023.

The RTO said it plans to re-evaluate its methodology for forecasting energy efficiency and demand-reduction efforts in light of the states’ shift away from traditional energy efficiency measures.

“The current method of using projections of EE counterfactuals to develop an accurate net energy and demand forecast has proven challenging and may introduce more uncertainty to the forecast than forecasting net of EE load directly,” ISO-NE noted.

Siemens Energy has begun a multiyear restructuring of its wind power business, which temporarily has halted sales of certain onshore turbine models due to quality-control problems.

Siemens Gamesa CEO Jochen Eickholt will step down effective July 31 and the company will focus its onshore efforts on attractive markets with stable regulatory frameworks, primarily in Europe and the United States. Siemens Gamesa hopes to end its losses by 2026 and then return to profitable growth.

The announcements came May 8, as Siemens Energy reported its second-quarter earnings. Eickholt’s impending departure is “by mutual agreement.”

Siemens Energy CEO Christian Bruch thanked Eickholt for laying the foundation for the reorganization and planned rebound and emphasized the quality-control problems that flared up did not begin while Eickholt was CEO.

Siemens Gamesa orders in the second quarter of fiscal 2024 were down 76% from the same quarter a year earlier but revenue was down only 5%, with higher offshore revenue more than offset by lower onshore revenue.

The company expects substantially better revenue in the second half of fiscal 2024, especially because of its efforts to ramp up its offshore production capacity. Multiple internal organizational changes are underway, as well.

Siemens Gamesa temporarily has stopped selling its 4.X and 5.X onshore turbines as it deals with the defects that have been observed.

Bruch addressed this early in his conference call with financial analysts.

“Obviously, we will need time to work through the quality matters,” he said.

“We will develop new onshore business based on, first of all, selected regions, and second, based on revised 4.X and 5.X platforms but with a heavily reduced number of variants. This is what Jochen and the team [have] been also driving over the past couple of months already — simplify the product structure in our company.”

Bruch said the target date for restarting turbine sales in Europe is the end of fiscal 2024 for the 4.X and fiscal 2025 for the 5.X, with relaunch in the United States later.

“Please keep in mind the volumes will not come back immediately,” he said. “We still have a big plan to work through. And we also have still the quality matters but we are confident that we are able to rebuild a strong market position over the coming years but it’s really a long-term trajectory.”

Siemens Energy stock closed 12.8% higher in trading on May 8.

Members of key Western Resource Adequacy Program (WRAP) stakeholder groups have expressed support for a recent move by participants to delay the program’s “binding” penalty phase by one year, to summer 2027.

Those stakeholders shared their views during a May 8 meeting of the WRAP’s Program Review Committee (PRC), a sector representative group “charged with receiving, considering and proposing design changes” to the RA program operated by the Western Power Pool (WPP).

They were reacting to an April 22 letter by the WRAP’s Resource Adequacy Participants Committee (RAPC) seeking the delay and outlining a number of concerns in meeting RA obligations in summer 2026, including supply chain delays, rapid regional peak load growth and extreme weather events that could affect participants’ ability to procure enough capacity to meet resource adequacy requirements. (See WRAP Participants Seek 1-Year Delay to ‘Binding’ Operations.)

Members of WPP’s voluntary program face a May 31 deadline to commit to binding operations by summer 2026, which would subject participants to penalties for capacity deficiencies.

PRC member Ray Johnson, deputy general manager with Tacoma Power, reiterated the concerns set out in the letter.

“The intent is to close the gap on some capacity deficits, but supply chains are causing delay,” Johnson said. “It’s very difficult in this current environment to procure or build all the capacity that’s required in the time frame that we’re currently operating under. And so, the modifications will enable a little bit more of a ramp into the program and then enable the program to be fully binding, I think, in early 2029.”

Asked to clarify Johnson’s 2029 reference, Tacoma Power told RTO Insider in an email that Johnson was referring to the first year beyond the program’s phase-in transition period set out in the WRAP tariff, which ends in 2028.

“They are still working toward a critical mass of participants electing binding operations for summer 2027, which falls in the existing transition period window,” a utility spokesperson said.

Rebecca Sexton, director of reliability programs at WPP, said the one-year delay is “not technically a loss.”

“This current undertaking here to select summer 2027 is well within the current tariff, so we don’t really see it as a delay,” Sexton said. “It does mean kind of a paradigm shift of what we think about binding. I think the terms that are being preliminarily discussed for the transition would hopefully encourage folks, even if they can’t meet the expectations of the WRAP program, to still be a binding participant.”

Non-utility Perspectives

Non-utility stakeholders agreed that they don’t want the program to enter the ‘binding’ phase until it includes a critical number of participants.

“I fully appreciate that this program is going to be more successful if we get this critical mass and everybody is in it together, and to incent that, I see why we proposed kind of ramping in,” said Ben Fitch-Fleischmann, director of markets and transmission at Interwest Energy Alliance.

Sommer Moser, an attorney representing Alliance of Western Energy Consumers (AWEC), shared a similar view but said it did not reflect a formal position from AWEC.

“Taking the time to get things right to make sure that we are eliminating inefficiencies and being thoughtful about implementation tends to lead to a program that is more cost effective and [has] greater benefits for participation,” Moser said. “I was a little concerned at the delay but ultimately think that getting it right is most important.”

Serving new demand from medium- and heavy-duty vehicle (MHDV) electrification will require some grid upgrades, but it could lower utility rates, Advanced Energy United said in a paper published May 6.

Impacts at the substation and feeder level will vary by where fleets of electric MHDVs might charge and how much headroom exists on the distribution system. That will require careful estimation and planning as fleets electrify, the report says.

“Greater MHDV electrification will result in greater electricity sales, increasing utility revenues,” the report says. “As long as the increased utility revenue from [electric vehicle] charging exceeds increases in utility system costs, transportation electrification will benefit all electric utility ratepayers by putting downward pressure on rates.”

That might not mean lower rates overall because other factors could drive them up, Richard Khoe, program supervisor at the California Public Utilities Commission’s Public Advocates Office, said on a webinar held by United on May 7.

His office did a similar study for California, which estimated a total of $26 billion to upgrade the distribution grid for the electrification of light-duty vehicles, MHDVs and homes, compared to a $50 billion estimate from a different report conducted for the PUC.

“We also found that the downward pressure on rates might not be achieved if any of the following things were to occur,” Khoe said. “For example, if EVs mostly charged in the evenings near peak hours, that would drive peak load up … and that would lead to higher upgrade costs.”

Using electric rates to subsidize charging excessively — or the study’s upgrade cost estimates being too low — could lead to higher rates, he added.

“We found that on a systemwide basis, peak loads probably are only going to increase by about 1 to 2% … by 2035,” said United report co-author Sarah Shenstone-Harris, of Synapse Energy Economics. “So not all that much. But at the feeder and substation level, the impact is much more varied.”

The main issue with MHDV electrification is that vehicles are likely to be clustered at specific sites, such as a warehouse district with panel trucks, or a bus depot, Shenstone-Harris said on the webinar. Some of those areas might have enough headroom to accommodate charging, but others will require upgrades.

“Generally, studies have found that loads of 1 to 5 MW will require a new feeder, or an upgrade, and loads of 5 to 10 MW will require a new substation or a substation upgrade,” Shenstone-Harris said. “But again, it really depends on the specifics. And as you can imagine, cost ranges also vary a lot depending on the specifics of the project, as well as lead time.”

United’s report offers four recommendations for states to get it right:

require utilities to share data about capacity of the distribution grid;

improve utility planning and regulatory processes to address barriers to electrification;

implement programs to manage peak loads and minimize costs; and

target certain areas for grid investment and/or MHDV adoption.

“A state or utility that doesn’t adopt these kinds of recommendations [is] surely going to be confronted with painful challenges down the road,” the New York Department of Public Service’s Zeryai Hagos said. “And this is because the four recommendations will work in unison to avoid long delays in interconnection — delays that could last for several years.”

A study in New York found that MHDV make-ready programs, which cover the upgrade costs of electrification, have a neutral to beneficial impact on rates through 2045, the report says. Benefits grew when charging was shifted to off-peak hours.

MHDVs can also serve as batteries in vehicle-to-grid services, contributing to grid stability and supporting the integration of renewable energy sources. Possessing larger batteries than standard cars, MHDVs can charge with more renewable energy when it is producing a surplus and can offer bigger discharges when the grid is stressed.

EVs cost more upfront than standard models, but they benefit from major fuel and maintenance savings over their lifetime. An electric delivery truck can save 34% compared to a diesel model over its lifetime, while an electric bus could save 24%.

“Electric vehicles have fewer moving parts and simpler drivetrains compared to internal combustion engines, leading to substantially lower maintenance needs,” the report says. “Plus, with EVs’ regenerative braking technology, certain pieces of braking equipment need to be replaced less frequently.”

AURORA, Colo. — FERC Commissioner Mark Christie, who still refers to himself as a state regulator after 17 years on the Virginia State Corporation Commission, offered words of praise and encouragement for SPP’s state regulators in his first appearance before the RTO and its Regional State Committee.

“I’ve always been very admiring of this RSC structure,” Christie told the RTO’s regulators and stakeholders during the RSC’s May 6 meeting. “I’m pleased to be here watching the action of this committee I’ve heard about for 20 years now that I’ve been so envious of.

“Your job is incredibly important. I’m obviously very adamant about the state role of RTOs. Someone once told me, ‘You’re like a state regulator on loan to FERC,’ so I’ll take that,” he added. “But I’m adamant about the state’s role because I’m adamant about protecting consumers. Everything that as a state regulator we do, and you all on the front lines, should be about putting consumers first.”

As most of the state commissioners that constitute the RSC listened attentively, Christie described resource adequacy as the key element of grid reliability, one of two major issues facing state regulators.

“Resource adequacy means what generation resources will get built, which ones get retired,” he said. “You — I should say, we — at the state level are on the frontlines because you’re the ones who are approving the construction of new generating resources. You’re the ones who are overseeing retirements. That’s why your role is actually the most important in the whole regulatory universe.”

Christie said the second major issue facing state regulators is consumer confidence because they’re “on the front line of rising power prices.”

“They’re going up, and they’re going up at a higher rate than it was 10 years ago,” he said. “When you approve a rate increase, and I know this from 17 years of having been a state regulator, it’s going to go right into people’s monthly bills. That’s one thing about being a state regulator is that you hear about it. You live among the people who you’re impacting, and that’s why state regulators are so important. I trust you all to know what is best for your state.”

The feeling was mutual. RSC President John Tuma of Minnesota thanked Christie for attending, saying: “We still welcome you as a full state commissioner, ever though you carry that other title.”

RSC Celebrates 20 Years

The RSC’s agenda, which included the quarterly stakeholder briefing, was scheduled for four hours. It went three-plus. Credit Tuma, who ran a tight ship that shaved off more than an hour of discussion. “Today may be a new land speed record,” cracked John Cupparo, SPP’s board chair.

The early finish allowed attendees to begin their commemoration of the RSC’s 20th anniversary 45 minutes early.

“I can’t believe it’s been 20 years for the RSC,” CEO Barbara Sugg said. “There’s lots for us to celebrate.”

“As someone who spent a good chunk of their career in the non-RTO West and experienced regional issues and trying to pull together participation from the regulatory community and others, this is a very challenging effort,” Sugg said. “That continues today. From that experience, the RSC group that we have is a special and powerful thing.”

The Advanced Power Alliance’s Steve Gaw was the only one of the RSC’s original six founding members present for the event. A Missouri regulator at the time and also involved in standing up the Organization of MISO States, Gaw said both groups first had to determine how much legal authority they had.

Former FERC Chair Pat Wood’s standard market design, released after the 2003 Northeast blackout, helped set some guardrails for future RSC members. It took about 18 months for the group to agree on the committee’s bylaws and its responsibilities.

“The key to the success of these groups has been about … collaboration and about building bridges and being dedicated [to] trying to find a way to work together to come up with things that would produce a positive result,” Gaw said. “If the commissioners had gone with an attitude of saying, ‘I have to have my state’s interest and it’s … the only thing that I’m in here for,’ nothing would have ever moved forward.”

SPP credits the committee with developing and implementing funding mechanisms that have helped build more than $12 billion of transmission lines since 2006; producing policies governing cost allocation for upgrades facilitating the integration of more than 33 GW of wind energy in the region; and for its role in helping refine resource adequacy methodologies.

“When the RSC was formed, critics questioned whether representatives of such a diverse group of states could reach consensus on anything,” SPP general counsel Paul Suskie, the RSC’s staff secretary, said in a news release. “For more than two decades, the group has navigated complex challenges, fostered innovation in our industry and contributed to the resilience of an electric grid that serves millions of customers across the central United States.”

REAL Team Work Approved

Despite the shortened meeting, the RSC still approved several revision requests, including two brought forward by its Resource and Energy Adequacy Leadership (REAL) Team. Both passed unanimously, as did all seven of the committee’s voting items.

The tariff changes, RR605 and RR616, were approved by the Markets and Operating Policy Committee in April. They are the result of RSC directives last October to clarify resources must be available if they’re going to be accounted for in the resource adequacy construct and in some load-responsible entities’ accreditation.

RR605 would define an authorized outage and criteria, add requirements for resources’ availability during both the summer and winter seasons (unless on an authorized outage), and help load-responsible entities and generation owners better understand when to submit resource adequacy capacity in providing workbooks to meet their obligation. RR616 would ensure any outage not approved by the SPP balancing authority and not an outside management control event is accounted for in performance-based accreditation.

The RSC also endorsed the REAL Team’s price-formation policy to dispatch resources based on the true obligation and price of the system using the obligation without the impact of the load shed and emergency energy assistance. The policy protects resources that hold day-ahead positions.

South Dakota’s Kristie Fiegen, who chairs the REAL Team, said it is close to approving a winter planning resource margin and a fuel assurance policy. Both should be coming to stakeholders, regulators and staff during their July and August meetings. (See SPP, Members Close in on Fuel Policy, Base PRM.)

“We’ve had a lot of policies, but [the winter PRM] is the most time-consuming,” Fiegen said.

The REAL Team has spent six months on the PRM tariff revision, but it’s had its side effects.

“I feel like we’ve become a family this past year,” she said.

“Chair Fiegen has done a wonderful job leading these family discussions of the REAL Team,” COO Lanny Nickell said. “We haven’t yet evolved into a food fight, so that’s a good thing.”

JTIQ NTCs Possible This Year

Casey Cathey, SPP’s new engineering vice president, told the RSC that staff hopes the Board of Directors will issue construction permits by year’s end for the five projects in the Joint Transmission Interconnection Queue.

SPP and MISO staffs and potential transmission owners are pursuing a direct billing approach that would require SPP to modify a revision request (RR620), which would implement RSC-approved cost-allocation policies for JTIQ projects. MOPC delayed taking action on RR620 during its April meeting.

“We need to ensure we have the revision request locked up,” Cathey said, noting staff determined its current approach would be the most efficient way to administer the JTIQ settlement process.

SPP and MISO have agreed to assign 90% of the JTIQ portfolio’s $1.06 billion in costs for its five projects to generation. Load will cover the remaining 10%. (See MISO, SPP Propose 90-10 Cost Split for JTIQ Projects.)

RSC Welcomes Missouri’s Hahn

The committee welcomed Missouri’s Kayla Hahn, who chairs the state’s Public Service Commission, as its 47th member over the past 20 years and honored the service of recent RSC members Will McAdams (Texas) and Scott Rupp (Missouri).

Two potential future members also were present for the meeting: Mary Throne, chair of the Wyoming PSC, attended in person, while Utah Commissioner John Harvey listened in virtually.

“We look forward to your participation in the RSC and Wyoming’s participation in the RSC as part of the RTO West expansion into the Rocky Mountain area,” Sugg told Throne.

Wyoming is one of four states that, with Colorado, will make up much of SPP’s RTO footprint in the Western Interconnection. Arizona and Utah will increase the grid operator’s footprint to 17 states.

Both houses of the Vermont Legislature have approved a bill updating the state’s Renewable Energy Standard to move it toward 100% renewable electricity by 2030.

It would require most retail electricity providers to make renewable energy at least 63% of their annual load by the end of 2024 and 100% by the end of 2029. Municipal retail electricity providers and a provider serving a single customer at 115 kV have until the end of 2034.

Scott offered his opinion of the measure right in the headline of a Feb. 27 news release, referring to it as the “Potential Billion Dollar Rate Hike Bill.”

He said: “There is clearly a more affordable and equitable alternative to H.289. We can and should do better.”

Scott said the Public Service Department conducted an 18-month public engagement process to produce a proposed bill providing better progress toward the state’s mandated emissions reduction targets than H.289.

Legislators did not consider the department’s work as they drew up H.289, which carries a potential 10-year price tag of $1 billion, he said.

Both houses of the General Assembly passed the measure with more than the two-thirds majority needed to override a veto.

Environmental and clean-energy advocates hailed passage of H.289 and said it would slow climate change, a priority objective for many Vermonters.

The Vermont Natural Resources Council thanked legislators who pushed back against the “fake narrative that a renewable energy future is too expensive.” It said H.289 would double the power produced within the borders of Vermont, which is 48th in the nation for percentage of power generated in-state.

The Sierra Club’s Vermont Chapter and Renewable Energy Vermont said the measure would double the amount of renewables Vermont utilities must build in-state to 20% of the electricity they deliver; add efficiency and lifecycle greenhouse gas metrics that limit the eligibility of new biomass plants to meet the new standards; prevent classification as a source of new renewable power any lands newly flooded in the future by Hydro Quebec; and phase out off-site or “virtual” net metering, a program to increase access to community solar.

In a news release, Lauren Hierl, executive director of Vermont Conservation Voters, said: “After the recent flooding and other climate disasters facing Vermont communities, it’s encouraging that Vermont is on the cusp of adopting one of the most ambitious renewable energy standards in the country. This bill is an important step in Vermont’s efforts to cut climate pollution and leave a better Vermont for future generations.”

The U.S. Department of Energy is looking to boost interregional transmission with its announcement May 8 of 10 proposed National Interest Electric Transmission Corridors (NIETCs), where projects could be eligible for a share of $2 billion in federal loans and special permitting under FERC’s backstop permitting authority.

DOE defines a NIETC as a geographic area where “it is determined that consumers are harmed, now or in the future, by a lack of transmission in the area and the development of new transmission would advance important national interests for that region, such as increased reliability and reduced consumer costs.”

But beyond those findings, the department looked at factors such as reliability, resilience, congestion, consumer costs and future generation demand growth, “which is a very important issue right now,” the official said. “And for some of these also, we’re looking at what ultimately unlocks clean energy and allows for clean energy resources to interconnect to the grid.”

Energy Secretary Jennifer Granholm said the preliminary list includes areas that are high priority for more transmission buildout. “This program is going to help us build out transmission capacity quickly and efficiently for the people who need it most without compromising on the quality of environmental reviews or community outreach.”

The list includes corridors as narrow as 0.3 miles across and as wide as 345 miles east to west, for example:

the New York-New Jersey corridor, 4 miles wide and 12 miles long, providing an interregional connection between PJM and NYISO, as well as interconnection points for offshore wind projects;

the Plains Southwest corridor, running 345 miles east to west and 220 miles north to south, covering portions of Kansas, New Mexico, Oklahoma and Texas; and

the Mountain-Northwest corridor, 0.3 miles wide and 515 miles long, running from Oregon to Nevada.

Some corridors also stretch over multiple parallel or adjacent sections, such as the Mid-Atlantic corridor, covering parts of Maryland, Pennsylvania, Virginia and West Virginia with parallel lines 2 miles across and up to 180 miles long.

These and the other corridors on the list all have one or more potential transmission projects under development, which a NIETC designation could help accelerate, according to the DOE announcement.

Other considerations include co-location with an existing highway or transmission right-of-way, and the potential to get more renewable energy online and increase transmission capacity between the Eastern and Western interconnections. The longest potential NIETC, the Midwest-Plains corridor, runs 780 miles, beginning in Kansas, crossing Missouri and Illinois and ending in Indiana.

The proposed corridors on the list could be reconfigured through further public and industry input, DOE officials said. But projects located within any NIETC corridor are eligible for federal loans drawn from a $2 billion fund set up by the Inflation Reduction Act.

NIETC projects also could be eligible for permitting through FERC’s backstop authority, established in the Infrastructure Investment and Jobs Act, allowing the commission to permit projects in a corridor if state regulators don’t have permitting authority or have delayed project approvals.

FERC has yet to decide if and how it might use the backstop permitting option, but the issue is on the commission’s agenda for May 13, when it is expected to vote on its long-awaited transmission planning and cost allocation rule.

The senior DOE official stressed that the NIETC designation process is separate from any FERC decision on its backstop permitting authority but said the backstop authority can only be used for a project in a NIETC.

‘A Few Backyards’

The NIETC announcement was the latest in a string of initiatives DOE has rolled out in recent weeks expanding transmission capacity across the country and streamlining the permitting process. On April 25, DOE launched its Coordinated Interagency Authorizations and Permits (CITAP) program, which is intended to cut environmental permitting time for transmission projects to two years.

Even more strategically, the release of the preliminary NIETC list comes less than a week before FERC is scheduled to vote on its long-awaited transmission planning rule, which administration officials again stressed is separate from the NIETC program, which may not be directly affected by the decision.

“We’re looking forward to a rule that will … give people certainty and stronger tools to make sure these projects get built,” John Podesta, White House senior adviser on international climate policy, said at the May 7 briefing. “[FERC] will at the end of the day render their judgment about how far to go in that regard, but I think it’s another important step to ensure we have the ability to cut through the red tape.”

The need for an acceleration of transmission planning and permitting remains pressing. About 2.6 GW of projects, mostly solar, wind and energy storage, are sitting in RTO and ISO interconnection queues across the country, according to Lawrence Berkeley National Laboratory’s 2024 Queued Up report.

To meet President Joe Biden’s 100% clean power goals by 2035, “we need to more than double our current transmission capacity,” Podesta said. “The truth is, if we can’t build critical clean energy projects through a few backyards, then no one will have a backyard.”

The May 8 announcement marks the beginning of the second of four phases of NIETC designation as outlined in the guidelines DOE issued in December. In the first phase, which ran from mid-December to early February, DOE gathered input from stakeholders.

The release of the preliminary list kicks off a 45-day comment period, which will run through June 24. Phases 3 and 4 will include a due diligence process and environmental reviews under the National Environmental Policy Act, which could take up to two years.

DOE has yet to state how many NIETCs may be on the final list or when it will be released.

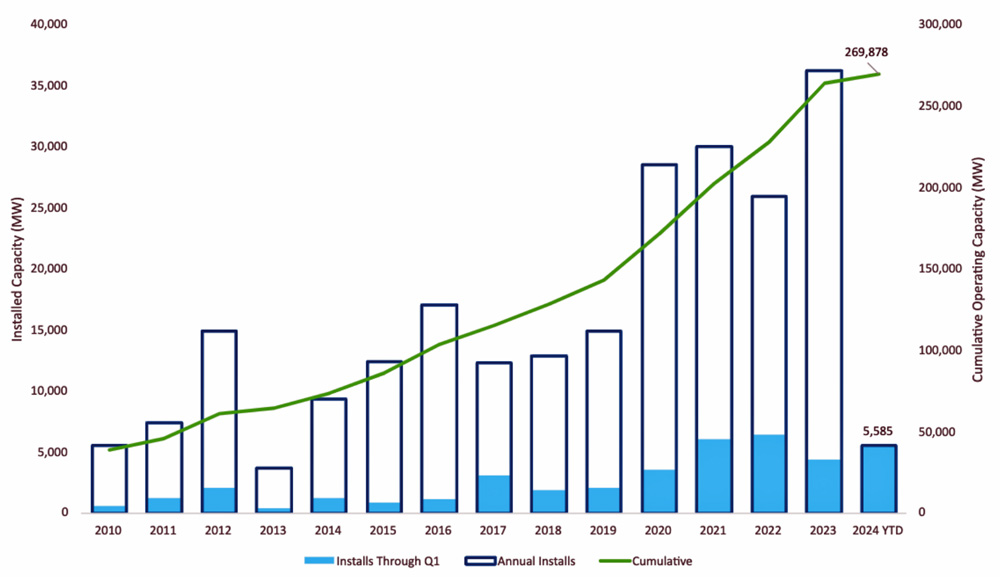

Nearly 5.6 GW of new solar, wind and storage capacity was added in the U.S. in the first quarter of 2024, the American Clean Power Association reported.

The clean energy trade group said May 7 that capacity additions in the first quarter of 2024 were 28% higher than in the same period in 2023, putting utility-scale solar power installations over the 100-GW mark for the first time. It took 18 years to reach 50 GW of installed utility-scale solar but only four years to jump from 50 to 100, noted John Hensley, ACP’s vice president of markets and policy analysis.

“Given current trends and expectations, [we expect] that the next doubling will come in a relatively short time,” he said at a news conference.

At the close of the first quarter, installed clean power capacity stood at 269.88 GW nationwide, ACP said. The pipeline of projects under construction or in advanced development nationwide reached 174 GW, up 2% from the fourth quarter of 2023 and 23% from the first quarter of 2023.

Offtake mechanisms for clean energy projects under development | ACP

“So 2023 was already a great year, but we’re already off to an even better year here in 2024,” Hensley said. “Just to give you some sense, those 5.6 GW of projects that came online this year are about enough to power a million American homes.”

The projects ACP considers “in the pipeline” are either under construction or far along in the preconstruction process, he said. There are supply chain challenges, trade and tariff issues, and crowded interconnection queues, but “I will say that for the first time in quite a while, as we’ve looked at project delays, we’re starting to see that number slow pretty significantly,” Hensley said. “I mean, we were generally adding 10 [GW to] 15 GW of delays a quarter. We had 7 GW of delays in Q1 2024.”

As of the first quarter, ACP counts 151 GW of onshore wind, 101 GW of solar and 18 GW of storage operational nationwide.

In response to a reporter’s question, Hensley said the political situation in the U.S. introduces some uncertainty, but the industry is in a sound position: Customer demand for clean energy is increasing, technology costs are easing, and the economic benefits are spread across red and blue states.

“It may be kind of strange to concede that 80-plus percent of our projects are actually taking place in more conservative parts of the country,” Hensley added.

So much of what is being built is solar, which has a lower capacity factor than wind or fossil fuel-burning generation and needs more of a backstop. Wind was first to market, about a decade ahead of large-scale solar, Hensley noted, and there has been some balancing of wind-dominant generation portfolios. ACP expects to see developer interest in wind start to rebound in 2025 and beyond.

First-quarter additions and cumulative growth of U.S. clean energy capacity | ACP

“And again, let’s not forget about storage, we built close to 8 GW last year, another 8 to 10 this year,” Hensley added. “It’s starting to proliferate, and in more markets than just California and Texas. … We’re not quite there yet on that balanced mix, but I think that’s the direction that we see things go.”

By the Numbers

Datapoints from the report include:

4,557 MW of utility-scale solar came online in the first quarter of 2024; onshore wind and storage totaled about 450 MW each.

132 MW came online from South Fork Wind, the first major infusion of offshore wind in the nation.

NextEra Energy was the leading clean-power developer in the first quarter; its 1,829 MW of solar, 449 MW of onshore wind and 50 MW of battery storage made up 41% of the national total.

The nationwide development pipeline reached 94,462 MW of utility-scale solar in the first quarter, up from 81,509 a year earlier; 25,321 MW of onshore wind, up from 20,176; and 31,627 MW of batteries, up from 19,621.

66,959 MW of clean power capacity is now operational in Texas, the most of any state; California is second, at 35,002 MW, and Iowa is third, at 13,486.

1,964 MW of clean power came online in the first quarter in Texas, the most of any state; Florida was second, at 1,789 MW, and California was third, at 293 MW.

Texas led the U.S. in capacity under active construction in the first quarter, with 18,950 MW; New York led in capacity in advanced development stages, at 13,850 MW, though 4,000 MW of offshore wind fell out of its pipeline early in the second quarter.

Developers reported a cumulative 62 GW of clean power projects as “delayed” in the first quarter and expect a little less than half of that — 29.8 GW — to become operational by the end of this year.

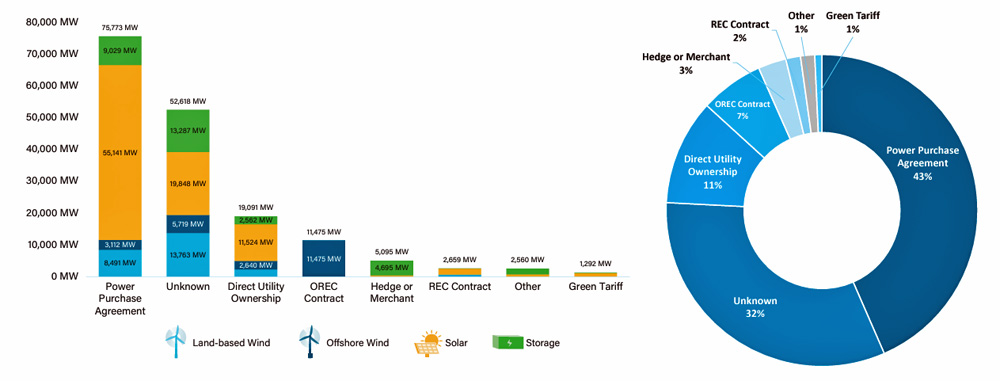

7,773 MW of power purchase agreements were announced in the first quarter, 52% more than in the same quarter of 2023. Utilities were responsible for most of the increase, but corporate PPAs increased as well: Microsoft alone announced 1.4 GW of new PPAs, and Meta, Amazon and UnitedHealth Group also reached sizable PPAs.

Ameren executives have reassured shareholders that Missouri’s capacity shortfall beginning this summer is no cause for panic.

Speaking May 3 on a first-quarter earnings call, CFO Michael Moehn said he doesn’t expect Missouri ratepayers to see “material” bill impacts from MISO’s capacity auction. The utility also doesn’t expect to encounter “any issues with providing reliable electric service throughout the year for our customers,” he said.

MISO’s recent capacity auction returned insufficient capacity for the upcoming fall and spring 2025 in Missouri’s Zone 5, where capacity prices hit the $719.81/MW-day limit on par with building new generation.

Moehn said the cost of new entry prices in MISO Zone 5 are a function of “higher load requirements, changes to the accredited capacity of generation available and reduced import capability.”

He said auction results indicate that Ameren Missouri needs to redouble efforts to “execute the generation plans” laid out in its integrated resource planning. The pairing of new, large loads with new renewable generation means that significant transmission expansion is more necessary than ever to maintain reliability, he said.

“We stand ready to work with stakeholders in our region to address the capacity needs,” Moehn said. He added that the Ameren Illinois and Ameren Missouri service territories are on track to experience mounting load growth, with new projects proposed from the automotive, aerospace manufacturing, data center and agricultural industries.

Ameren’s retiring Rush Island Energy Center — which played a role in the Zone 5 capacity shortfall — also factored into the utility’s earnings picture for the first quarter.

Ameren announced first-quarter earnings of $261 million ($0.98/share) compared to $264 million ($1/share) a year ago. CEO Marty Lyons said unseasonably warm conditions in February and March reduced profits, as did expenses related to mitigation relief stemming from Rush Island’s unresolved air pollution case.

“Despite the year-to-date weather headwinds and the Rush Island charge, our team is taking steps to contain spending, and we remain on track to deliver within our 2024 earnings guidance range of $4.52 per share to $4.72 per share,” Lyons said.

For the rest of 2024, Ameren will implement hiring restrictions, reduce its contractor and consultant workforce and cut back on discretionary spending, Moehn said.

Coal Woes

The company recently filed a plan with the U.S. District Court of Eastern Missouri to remediate 14 years of unlawful air pollution from Rush Island. The $20 million plan involves a surrender of the plant’s sulfur dioxide allowances under EPA’s cap-and-trade program, distributing air filters to disadvantaged households downwind of the pollution and an offer to purchase 20 electric school buses and 40 charging stations for the St. Louis area.

Ameren expects evidentiary hearings on the matter this summer and the court’s decision by the end of the year.

“When you look at the components of the two programs, they are very similar in terms of electric school buses, air filtration program, charging infrastructure. … It really is seemingly not a matter of the program mix, but sort of the extent of them and the cost of them. So, we can’t predict what mitigation the court would ultimately order,” Lyons said.

He added that any penalty will be “nonrecurring and onetime and won’t be something that affects ongoing operations or earnings.”

The district court last year ordered Rush Island to shut down no later than Oct. 15. Ameren opted to close the plant rather than spend several million dollars to install a flue gas desulfurization system to scrub excess emissions. The Justice Department and Ameren have been at an impasse for two years over how to remediate Rush Island’s longstanding environmental harms beyond the plant’s early retirement.

Lyons said Ameren is progressing on its request with the Missouri Public Service Commission to securitize the remaining balance of Rush Island, noting that PSC staff in March recommended the company be allowed to securitize $497 million instead of an original request for $519 million. The PSC is expected to issue a ruling in late June.

Lyons cautioned that another Ameren Missouri coal plant, the Labadie Energy Center, faces an uncertain future. While units at the plant aren’t slated to retire until 2036 and 2042, they are vulnerable to EPA’s new rule stipulating that coal plants either close by 2039 or use carbon capture or other technologies to capture 90% of their emissions by 2032. (See EPA Power Plant Rules Squeeze Coal Plants; Existing Gas Plants Exempt.)

Lyons said EPA “expects generators to rely heavily on carbon capture and storage technologies, which are not ready for full-scale economy-wide deployment.” He added that the rule’s application to new gas-fired units with greater than 40% capacity factors will likely complicate Ameren’s plan to add a gas-fired combined cycle plant sometime in the early 2030s to maintain reliability. Litigation by stakeholders is likely, Lyons said.

“While we are still assessing the impact of the rules on our integrated resource plan, these new rules are making it more challenging and costly to maintain existing dispatchable generation or build new dispatchable generation. These challenges come at a time when supply and demand is tight, and the industry has seen significant potential load growth. … These rules, if not modified, would require significant investments beyond what’s in our current 10-year pipeline to meet compliance obligations and maintain a reliable system,” Lyons said.

Transmission Awards

Finally, Lyons called attention to MISO selecting Ameren to build three competitively bid projects from its first, $10 billion long-range transmission portfolio. (See MISO Chooses Ameren for 3rd Long-range Tx Project.) He said the awards provide evidence of the company’s “record of being able to deliver cost-effective, high-value projects to our communities.”

“Ultimately, Ameren was assigned or awarded approximately 25% of total Tranche 1 portfolio projects addressing the MISO Midwest region and 100% of the projects in our service territory,” Lyons said.

Lyons said he expects construction on the projects to “substantially begin in 2026.” He noted also that Ameren representatives have been collaborating with MISO planners in “ultimately approving the most appropriate path forward” on the approximately $20 billion in long-range transmission projects proposed in the RTO’s second portfolio.