The U.S. energy storage market scored a record-breaking third quarter, putting 2,354 MW and 7,322 MWh of new residential, commercial and utility-scale projects online, according to the Energy Storage Monitor/Q4 2023 report from industry analysts Wood Mackenzie (WoodMac) and industry advocates American Clean Power Association (ACP).

But the sector faces “multiple headwinds … resulting in a volatile near-term pipeline and difficulty in bringing projects to mechanical completion,” the report says, downgrading its predictions for total capacity by 2027 from about 66 GW to 63 GW, a 5% drop.

With WoodMac pegging U.S. market size at present at 8.3 GW and 24.7 GWh, even reaching the reduced target could require substantial growth.

Frank Macchiarola, ACP’s chief policy officer, hailed the numbers as clear evidence that “energy storage is increasingly a leading technology of choice for enhancing reliability and American energy security.”

“It will be essential to our future energy mix,” he said.

A 2022 analysis from the National Renewable Energy Laboratory estimated that, depending on the energy mix, the U.S. might need between 129 GW and 368 GW of storage to reach President Joe Biden’s goal of a 100% clean electric power system by 2035.

The WoodMac-ACP report highlights a number of key figures and trends on the current state of the market and the challenges ahead:

Grid- or utility-scale storage continues to be a primary driver of market growth, jumping from 1,261 MW in the third quarter of 2022 to 2,158 MW for the same quarter this year, a 71% increase.

Community, commercial and industrial (CCI) and residential storage both posted modest year-over-year increases: 3% and 4% respectively. CCI capacity stands at 30.3 MW, while residential is at 166.7 MW. California leads the residential market, with 78.4 MW installed in Q3 alone.

Despite the record-breaking Q3, storage market growth is hobbled by project delays, with 82% of projects originally scheduled to come online from July through September now pushed back. But these delays could result in ongoing growth in 2024, the report says.

The grid-scale pipeline is particularly volatile, with 86 GW of projects announced and 453 GW sitting in transmission interconnection queues, a 36% increase over Q3 2022.

But prices continue to fall for grid-scale lithium-ion battery storage systems, with WoodMac noting that “as of November 2023, [the] lithium carbonate spot price reached its lowest level since 2021.” However, while system prices are down, other “balance of plant” costs and labor costs are on the rise, the report said.

While not specifically mentioned, the impact of the energy storage tax credits and other incentives in the Inflation Reduction Act are incorporated into the report’s analysis, according to Vanessa Witte, senior research analyst for energy storage at Wood Mackenzie.

Thus, the increase in project labor costs is due partly to a tight market for skilled labor, but also “administrative fee increases due to fulfilling the prevailing wage and apprenticeship requirements” that are part of the IRA’s tax incentives, the report says.

Waiting for Long Duration

As with solar and wind, the headwinds for storage are all too familiar: supply chains, permitting and interconnection. But Witte sees more nuanced and transitory issues at play.

“A near-term headwind is the increased cost of capital, which also increases the [due] diligence for these projects,” she said in an email to NetZero Insider. “As interest rates and inflation come down next year, this will likely calm down as well. For supply, as opposed to last year, where the supply issue was centered on the availability and price of cells, it is now centered on substation equipment, such as transformers, circuitry, switchgear[s], etc.”

Macchiarola sees the industry playing a strong role in the energy transition and in building out domestic supply chains. But he said, “streamlined permitting and evolving market rules” will be needed to “further accelerate the deployment of storage resources.”

Another critical trend to monitor is that growth in capacity may not be matched by growth in storage duration. Across all sectors, the average duration is just over three hours.

The capacity of a storage project is measured in megawatts or gigawatts: the energy it produces, in megawatt- or gigawatt-hours. Duration is a measure of how long a project can produce energy at its capacity. Thus, a 2-MW, 6-MWh project would have a three-hour duration.

As renewables increase on the grid ― and fossil fuel plants are retired ― longer-duration storage will be needed to provide a range of grid support and backup services.

“Duration is growing, generally speaking, but not over four hours,” Witte said. “There are no market signals to incentivize four-plus hours. … There are a handful of states that have average duration at or over four hours, but not many, [and] these systems are typically solar plus storage.”

“Paired systems fit better with a four-hour (or slightly longer) duration for the firming ability of the paired system versus standalone that just plays into the wholesale market,” she said. “Batteries are not typically getting revenue from ancillary services and capacity markets.”

A still-emerging market, long-duration storage is not yet on WoodMac’s radar, Witte said.

“Long duration is growing. We expect to see more traction next year in terms of pilot projects and increased manufacturing,” she said. “But again, there are no market signals for four-plus hours, so the only [companies] actually utilizing longer than four-hour are utilities, for the reliability aspect, and again, these are few and far between.

“One- to four-hour dominates and will still dominate in the next 10 years for sure.”

Increased electrification and reliance on solar and wind resources will make electricity supply and demand more weather-dependent, resulting in more variable winter peak loads on the New England grid, Benjamin Wilson of ISO-NE told the RTO’s Planning Advisory Committee (PAC) on Dec. 12.

Analyzing the results of the Economic Planning for the Clean Energy Transition (EPCET) pilot study, ISO-NE anticipates the range between maximum and minimum peak load weather years will reach 14 GW by 2045, a significant increase compared to the 4-GW range expected for 2025.

This gap could require a large subset of dispatchable resources that run only in high-end cases, Wilson told the PAC.

“The region may end up paying for a pool of resources which are only needed once every few years,” Wilson said. “Uncertainty surrounding how often dispatchable resources will actually be needed may lead to a need for higher capacity payments.”

Wilson noted that even with the continued penetration of wind and solar, dispatchable generators still will need to cover about 90% of the expected peak load, underlying the importance of ensuring adequate revenue sources for dispatchable resources.

The EPCET study also compared two future policy scenarios focused on resource compensation. One scenario focused on the continued use of power purchase agreements (PPAs) similar to state procurements. The second scenario included PPAs along with a reliability adder (RA) charge to fossil resources that would be allocated to non-emitting dispatchable resources.

The scenarios included a carbon constraint of about 6 million tons by 2045. For context, the New England power system was responsible for about 30 million tons of carbon emissions in 2021.

In both scenarios, ISO-NE found the cost of PPAs will increase significantly between 2035 and 2045, with new intermittent resources lowering the capacity factor of existing intermittent resources. Both scenarios also projected declining revenues for existing solar and wind resources through 2045, as these resources are “increasingly underbid by new resources with higher priced PPAs,” Wilson said.

In the PPA-only scenario, nuclear profits also declined significantly by 2045, coinciding with the decline in energy prices. In contrast, profits remained relatively stable with the introduction of the RA.

The RA likely would result in lower capacity market prices compared to the PPA-only scenario by increasing the revenue available to clean dispatchable resources in the energy market, Wilson said.

“The PPA plus RA scenario generally does a better job of securing resource revenue adequacy,” Wilson said. “Providing greater revenues to baseload resources may reduce the likelihood of retirement.”

Wilson added that demand response resources may play a role in reducing demands but could be limited in their ability to ease extended winter peaks.

“Significant development of demand response resources could help alleviate the uncertainty surrounding multiple weather years. However, it may prove difficult to curtail some load (such as heating, cooling or transportation) during periods of extreme weather,” Wilson said.

Nuclear generator net profits in PPA and PPA+ revenue adder scenarios | ISO-NE

Instead of categorizing transmission lines’ original in-service year, the database will list the in-service year of each line’s oldest component to account for line rebuilds. For transformers, the database will list both the in-service year and the manufacturing year.

Trotta said cost projections would not be included in the database. He said including accurate cost metrics would require a significant amount of work and noted that cost projections were included in a pair of recent presentations.

He said the NETOs plan to update the database annually, and that the transmission owners will “evaluate the feasibility of adding additional information to the database,” including asset health scores and data on other pool transmission facilities, such as circuit breakers and control houses.

The first iteration of the database, along with related stakeholder comments, will be published in January, Trotta said.

Project Presentations

Eversource presented to the PAC a project to replace deteriorating wood structures on two 115-kV lines in New Hampshire with a total projected cost of $15.7 million. The expected in-service dates for the replacements are mid-2024.

In accordance with the new asset condition presentation guidelines, Eversource is soliciting stakeholder feedback due Jan. 11.

AUSTIN, Texas — ERCOT staff and Potomac Economics, the firm that serves as the grid operator’s Independent Market Monitor, set aside their differences this week and promised to work together to improve the ISO’s procurement and deployment of ancillary services.

Potomac Economics President David Patton said the IMM’s staff has had “encouraging” discussions with ERCOT over changes to its ancillary service methodology. The ISO’s staff has also agreed to revisit its use of ERCOT contingency reserve service (ECRS), its first new ancillary service in 20 years, which was deployed in June.

“I felt like the board and ERCOT were pretty receptive to the message,” Patton said after the ISO’s Board of Directors meeting Dec. 19. “I feel like there was an acknowledgement by ERCOT that this is an issue worth studying and potentially making some changes to address it. Ultimately, my goal was to try to address this as quickly as we can so that these costs don’t accumulate.”

The IMM has said ERCOT’s use of ECRS has created artificial supply shortages that produced “massive” inefficient market costs totaling about $12.5 billion this year through Nov. 27. (See “Members Support 2024’s Ancillary Services Methodology, Despite Costs,” ERCOT Technical Advisory Committee Briefs: Dec. 4, 2023.)

ECRS is economically dispatched within 10 minutes of deployment, using capacity resources that can be sustained at a specified level for two consecutive hours to supplement ERCOT’s conservative operations posture, in which it sets aside ample reserves to address sudden energy drops.

Patton said that because ERCOT doesn’t co-optimize energy and ancillary services in real time like other grid operators, the ECRS megawatts are quarantined from the real-time market. He said the problem comes when ERCOT bought more 10-minute reserves this year than it did in 2022 in quantities that “dwarfed” those of other RTOs and ISOs, most of which are smaller than the Texas grid.

“We went to a whole other level in terms of buying 10-minute reserves,” Patton told the board’s Reliability and Markets (R&M) Committee. “At that same time that we’re buying those very high quantities, we quarantine them off from the real-time market so that it exposes the market dispatch to believing that it’s short when it’s not actually short.”

There were few questions for Patton during his presentation to the R&M and none in the board meeting that followed. The directors did approve ERCOT’s ancillary services methodology for 2024, including the commitment to reevaluate ECRS and meet with stakeholders by May.

Dan Woodfin, ERCOT vice president of system operations, said the high prices generally come when ERCOT is short of capacity.

“It’s those days when we were really tight on capacity and we had to release ECRS just to have enough to have it available to serve energy. If we can release it earlier on those days, then that may help with the efficiency of the pricing outcomes,” he said. “We’ve agreed we’re going to look at that. You got to be careful with that because there are people that are out there making investment decisions that are looking for regulatory certainty. I think this is one of those places that it’ll be really good to talk through that with the stakeholders to figure out what’s the right balance there.”

Texas Public Utility Commissioner Lori Cobos said the PUC has received a petition from retail providers to pass on ECRS costs in fixed-rate contracts and that legislation passed this year requires the commission to revisit ancillary services and their structure.

“There’s a recognition amongst the commission that, ultimately, the PUC needs to be involved in approving the ancillary service methodology [for 2025],” she said. “The reevaluation that happens in April needs to be a true reevaluation, given all of these costs. ERCOT, PUC staff, IMM staff need to get together and look at some near-term perspectives and long-term perspectives and how the ancillary service methodology can be more thoroughly and diligently vetted.”

In recent months, IMM’s then-Director Carrie Bivens raised the board’s hackles and received vigorous pushback for saying ECRS “likely” increased the real-time market energy costs by at least $8 billion. (See ERCOT Board, IMM Debate Ancillary Service Costs.)

After Bivens resigned from the IMM in November, the Monitor took another look at the ECRS analysis. Simulating energy cost increases from higher online reserve procurements, the Monitor found prices in August were more than double what an efficient price would have been. Taking those prices and evaluating the total number of megawatts in the real-time market, that pricing phase had a value of $12.5 billion.

“I think this is where the misunderstandings have come,” Patton said. “Some people believe that $12.5 billion is almost irrelevant and some people believe that $12.5 billion is sort of the market. It’s neither one of those. The most important price in this market is [the energy] price. This price is the one price that has to be right because this price drives everything else.”

When Patton first shared his presentation with the Technical Advisory Committee early in December, ERCOT called the numbers “absolutely false” in a document posted to its website.

“Electric consumers DID NOT pay $8 [billion] to $12 billion more for electricity in 2023 than they would have if ECRS were not purchased,” the grid operator said. “These types of hyperbolic declarations may be great for grabbing headlines or driving a particular narrative, but they do a grave disservice to Texans because they simply aren’t true.”

In his presentation Dec. 19, Patton said ERCOT’s response was “very disappointing.” He noted the IMM has always reported the numbers as wholesale market costs and that consumers are “partially protected” from those costs by suppliers’ hedges and contracts.

“Eventually, those hedges expire and then the future price that’s going to be paid and new bilateral contracts are all going to be based on expectations of what the spot price is going to be” in the future, Patton said. He said forward prices for next July and August have risen 67% with ECRS’ deployment.

“That suggests that as some of those hedges expire and they get re-signed, they’re going to be re-signed at a much, much higher cost,” Patton said. “Right now, the expectation is we’re going to have high and volatile prices next summer and the summer after that.”

Cobos to Rejoin Board

Cobos will rejoin the ERCOT board as a nonvoting, ex officio member for 2024. She was a member of the pre-Winter Storm Uri board through her position as the Office of Public Utility Counsel’s CEO and public counsel.

A recent rule change gives the PUC two nonvoting seats on the board. Interim PUC Chair Kathleen Jackson also is a board member.

Revised Budget Passes

The board approved the ERCOT budget and system administration fee for 2024/25 after both were recently trimmed by the PUC. The commission cut both original proposals, slicing a little over $31 million from the original biennial budget request and reducing the administration fee from 71 cents/MWh to 63 cents/MWh, a 13.5% increase over the current admin fee of 55.5 cents/MWh. (See Texas PUC OKs Smaller Budget, Admin Fee Increases for ERCOT.)

The grid operator’s original budget request of $424.03 million and $426.99 million for 2024 and 2025, respectively, was reduced to $405.7 million and $414.3 million.

The commission reduced the admin fee to be in place for two years, rather than four, because of future uncertainty. It also directed ERCOT to meet certain performance measures and file quarterly progress reports on the development of a reliability standard, dispatchable reliability reserve service and the performance credit mechanism, and the real-time co-optimization plus batteries project. The first report is due Sept. 1.

Bill Flores, chair of the Finance and Audit Committee, cautioned the board that ERCOT could revisit the admin fee for 2025 late next year. He said the budget relies on more interest income than any previous budget.

“Assumed interest income is not guaranteed, so while we’re comfortable that we have a locked-in budget and interest amount for 2024, 2025 is still at risk,” Flores said. “Each 1% change in interest rates … is equivalent to a $20 million budget impact. If you had a 4% drop in interest rates back to close to zero, where we were in late 2020, then your interest income would show a reduction of somewhere between $80 [million and] $100 million, and each 1% drop affects the system admin fee by several cents.

“The new rate is 63 cents, which I think is a good outcome for ratepayers in Texas, but there is a risk to what can happen to that rate as soon as 2025, 2026 and 2027.”

The board also confirmed the Technical Advisory Committee’s membership for next year, as selected by its members. TAC will elect its chair and vice chair during its Jan. 24 meeting. South Texas Electric Cooperative’s Clif Lange is leaving the committee after four years as chair.

The directors approved a nodal protocol revision request (NPRR1172) that passed despite opposition from the generator segment during the October TAC meeting. The NPRR, brought forward by consumer groups, removes the mitigated offer cap multipliers and creates a 100% claw-back for reliability unit commitments.

The change is intended to encourage generation resources to self-commit.

The board also approved five other NPRRs and single changes to the nodal operating guide (NOGRR), planning guide (PGRR) and retail market guide (RMGRR):

NPRR1181: Requires qualified scheduling entities representing coal or lignite resources to submit to ERCOT a seasonal declaration of coal and lignite inventory levels and to notify the ISO when the inventories drop below target and critical-level protocols.

NPRR1192: Incorporates the other binding document, “Requirements for Aggregate Load Resource Participation in the ERCOT Markets,” into the protocols.

NPRR1196: Corrects and updates equations used to determine ancillary service (AS) failed quantity calculations for load resources other than controllable load resources (NCLRs) developed under NPRR1149. Changes include calculation updates to account for AS allowances and restrictions that NCLRs can and cannot carry simultaneously with ERCOT contingency reserve service’s (ECRS) implementation; specifying the snapshot components to be used for the “telemetered AS for the NCLRs as calculated” variable; and adding a nonzero check for the “telemetered ECRS responsibility for the resource as calculated” variable.

NPRR1201: Reduces exposure from resettlements and default uplift invoices for historical operating days by limiting resettlement timelines due to errors that are discovered, and a market notice is provided to the market within one year after the operating day. This limit does not apply to alternative dispute resolution resettlements, a procedure for return of settlement funds or a board-directed resettlement addressing unusual circumstances.

NPRR1204: Implements the state-of-charge (SOC) concepts necessary for awareness, accounting and monitoring energy storage resources’ SOC within the RTC+B project.

NOGRR257: Resolves a conflict in emergency response service event-reporting timelines between the operating guide and protocols by striking the guide’s 90-day event-reporting requirement.

PGRR110: Removes a paragraph from the planning guide to accommodate the release of steady-state planning models in node-breaker format pursuant to a system change request.

RMGRR176: lays out the processes Lubbock Power & Light must use when it begins offering customers their choice of electric providers March 4.

FERC on Dec. 19 approved an exit fee for Tri-State Generation & Transmission Association members, rejecting the cooperative’s preferred method in favor of a modified version that its own trial staff came up with during a hearing process (ER21-2818).

Tri-State is a generation and transmission cooperative that provides wholesale power and transmission service to 45 members in Colorado, Nebraska, New Mexico and Wyoming. Its members have to buy almost all their power from it, with the exception of 5% of their needs that is carved out for self-supply and community solar.

The fact that members have to get most of their supply from Tri-State while the industry is shifting to more distributed and intermittent resources has driven some of its members to leave, said Guzman Energy Chief Commercial Officer Robin Lunt. Guzman is now providing wholesale services to two of Tri-State’s former members: Delta-Montrose Electric Association in Colorado and Kit Carson Electric Cooperative in New Mexico.

“I think that there was a combination of wanting more local control over generation mix and then the ability to build things in their community,” Lunt said in an interview. “And then [the] increasing prices and price volatility that was coming from Tri-State; so co-ops were looking at alternative paths.”

The case goes back to 2021 when FERC issued a show-cause order requiring Tri-State to demonstrate its tariff was just and reasonable without clear procedures for its members to withdraw by making a contract termination payment (CTP). (See FERC Accepts Tri-State’s Exit Fee Calculation.)

Tri-State filed a proposal for a CTP based on the higher of a lost revenues approach (LRA) or a debt covenant obligations (DCO) approach. A FERC administrative law judge came to an initial decision in September 2022, rejecting Tri-State’s method and others crafted by its members in favor of the trial staff’s proposal to base the exit fee on a “Balance Sheet Approach” (BSA).

The commission said that Tri-State had a chance to prove that its preferred LRA method with a floor based on the DCO was just and reasonable, even though the earlier hearing order signaled some concerns. However, Tri-State failed to adequately respond to those concerns, FERC said.

Tri-State argued the CTP was meant to hold remaining members harmless from early contract terminations by paying them for lost revenue under any terminated deals.

“We decline to provide an overarching, industry-wide rule for what a generally applicable tariff-based CTP must address,” FERC said. “The purpose of a CTP may vary depending on circumstances.”

FERC noted the D.C. Circuit Court of Appeals has said an exit charge “protects members of a cooperative against rate increases caused by the exit of a member, while also increasing membership commitment and stability” and covers the costs that a cooperative incurs “to provide full requirements service to the member.”

When it comes to Tri-State, FERC previously stated that the exit fee is meant to compensate the association “for the costs that it has incurred or has an obligation to incur in the future to satisfy its service obligations” under its departing member’s contract.

“Tri-State invested in generation and transmission facilities, and entered into [power purchase agreements], in order to serve the generation and transmission needs of its members,” FERC said. “If a member withdraws, it is reasonable for Tri-State to recover the share of the debt and other obligations it incurred on that member’s behalf, in order to protect against cost shifts to other members.”

The exit fee should cover the debt and other obligations undertaken by Tri-State for the withdrawing member, but remaining members should not be held harmless for lost revenues that they would have received over the full term of the contract, FERC said. Paying for lost revenues would go beyond compensating Tri-State for actual costs and obligations it incurred to serve departing members.

Tri-State also argued that allowing members to leave early would undermine its cooperative business model, but FERC said that neither the wholesale contracts nor its bylaws entitle the association to benefits of scale.

An LRA could be valid for an exit fee, but FERC had issues specifically with what Tri-State proposed, finding that the association failed to show that revenues equal its costs over the short term. The LRA would also allow Tri-State to recover decades of revenues not yet earned from a department member — based on decades of projected costs that the association will never actually incur plus a margin.

Because the DCO was linked to the LRA, the latter’s unreasonableness was enough for FERC to reject the former on its own. But FERC also would have rejected the DCO on the merits, it said, because it fails to consider key credits and adjustments, and it would recover transmission debt from withdrawing members who continue to take transmission service from Tri-State.

Members could also time their withdrawals to whenever Tri-State has low debt, or the association could manage its debt in a way that discourages withdrawals, FERC said.

FERC wound up deciding that the BSA — which was first proposed by United Power, a departing member, and then modified by its trial staff before being tweaked by the commission — was the best way to go. FERC has never used the approach for utilities pulling out of similar deals, but it has also never precluded using it.

“We believe that the situation here is not analogous to a withdrawal from long-term requirements contracts, because it involves additional complications, such as: accounting for a withdrawing member’s ownership interest in Tri-State; the possibility of a withdrawing member continuing to take transmission service from Tri-State; and a specific set of obligations under the [wholesale electric service contracts] and bylaws, among other factors,” the commission said.

FERC found that the BSA is unlikely to lead to higher rates for remaining members, noting that its ALJ said the DCO would have kept rates stable in the near term and the BSA is likely to lead to higher exit fees than that method.

Tri-State said Dec. 19 that it was reviewing the order, which includes actually analyzing the CTP methodology adopted and calculating the payments withdrawing utilities must pay. The association has to make a compliance filing within 30 days.

United Power is withdrawing effective May 1, and its DCO was calculated at $736.4 million, Tri-State said. Northwest Rural Public Power District is also withdrawing in May, while Mountain Parks Electric has submitted a notice to withdraw by Feb. 1, 2025.

Tri-State does own the transmission grid that serves some of its members, but others, including its members in Wyoming, are on others’ transmission lines, so that could bring up issues that need to be clarified on rehearing, said Guzman’s Lunt. Some PPAs that Tri-State has could also be sold and then credited to departing members, which could also come up on rehearing.

While those issues could change the final amount, FERC’s order yesterday will give United Power and Northwest Rural more certainty about what they have to pay on their exit in May, with true-ups to follow, she said.

The issues in Tri-State are part of the same trend that is driving increased interest from corporate customers in their energy supply and even mass-market customers’ adoption of distributed solar and plug-in vehicles, Lunt said. Instead of building a large, central coal plant and building/procuring the transmission needed to get that supply to customers, now members want more control.

“There are efficient and cost-effective ways to have reliable power that’s more customer-focused rather than the big, coal-plant-focused,” Lunt said.

FERC on Dec. 19 reiterated its rejection of SPP’s proposal to allocate “byway” transmission projects case by case, urging the RTO to vet the proposal through a stakeholder process (ER22-1846-004).

The commission’s order addressing arguments raised on rehearing defended its July 13 order, which rejected SPP’s proposed methodology. It said a rehearing request filed Aug. 14 by Sunflower Electric Power, Basin Electric Power Cooperative, Midwest Energy and Kansas Electric Power Cooperative had been denied “by operation of law” when the commission failed to act within 30 days.

Since 2010, SPP has allocated transmission facilities based on the highway/byway method, with highway facilities (300 kV or above) assigned 100% on a regional, postage-stamp basis and byway facilities (between 100 and 300 kV) split, with 33% assigned regionally and 67% assigned to the pricing zone in which the facilities are located. Facilities at or below 100 kV are allocated 100% to the host zone.

Some stakeholders said that allocation method was unjust as applied in “generation-rich” pricing zones, where generation that is not affiliated with load in the zone significantly exceeds the amount of load in the zone — an issue of increasing importance because of the influx of wind generation on the SPP system.

In 2022, SPP proposed allowing parties to petition the RTO’s Board of Directors to reallocate byways as highways if they satisfy three criteria:

Capacity: The total nameplate capacity of generating resources that are physically connected in the zone where the byway facility is located (and that are not affiliated with load in that zone) exceeds 100% of the prior calendar year’s average 12-coincident peak resident load.

Flow: Energy flow on each byway facility that is attributed to generating resources physically connected in the zone where the byway is located and that are not affiliated with load in that zone exceeds 70% of the sum of flows on the byway facility attributed to generating resources affiliated with the load in the zone and generation physically connected in the zone and not affiliated with load there.

Benefit: The byway facility provides benefits to load outside the pricing zone where the facility is located (e.g., adjusted production cost savings or savings through the Integrated Marketplace).

The commission initially approved the changes, saying it would help ensure the costs of byway facilities are allocated in a manner at least roughly commensurate with estimated benefits. It ordered the RTO to modify the language to specify that the board’s decision on such requests would be based solely on whether the three criteria were satisfied.

The decision was 3-2, with then-Chair Richard Glick and fellow Democrats Allison Clements and Willie Phillips in the majority, and Republicans James Danly and Mark Christie dissenting.

But after Glick’s term expired and Phillips was appointed chair, the commission reversed course in July in response to rehearing requests by utilities including Southwestern Electric Power Co., Oklahoma Gas & Electric and municipal utilities in Springfield and Kansas City, Mo. This time, Phillips and Clements joined Danly and Christie.

FERC ruled that even with the modifications it required, the tariff changes would grant the SPP board too much discretion because it could deny a requested reallocation even when RTO staff had determined the criteria were met, or approve a reallocation in which the criteria were not met.

The commission said it may reverse its prior position as long as it explains itself and that it does not need to establish that its newer position is superior to the previous one. The commission said allegations that SPP’s existing cost allocation method is unjust and unreasonable “are misplaced in a proceeding addressing a filing made under [Federal Power Act] Section 205. The proper vehicle for challenging existing tariff provisions as unjust and unreasonable is a complaint under FPA Section 206.”

In a joint concurrence with the order, Phillips and Clements said they were “sympathetic to … concerns that the commission’s decisions in this docket have caused parties to spend considerable resources over several years, without a solution to the deeper cost allocation challenges that prompted SPP’s filings in this proceeding.”

The commissioners said that while those seeking rehearing of the July ruling “raised compelling points that revisions to the highway/byway cost allocation approach may be appropriate under these circumstances, in our view the best path forward to address this issue would be an open, collaborative process between the relevant parties and stakeholders. Such open dialogue would allow for fulsome exploration of any legal or administrative barriers to potential cost allocation approaches, without some of the rigidity of a contested proceeding.”

The rehearing process, they said, “is not the ideal venue for the collaborative discussions that we envision would lead to durable policy solutions.”

New York officials have released the framework for a state cap-and-invest program and recommendations for allocating funds from the associated Consumer Climate Action Account (CCAA) to state residents.

The preproposal outline and a Climate Affordability Study released by the New York State Research and Development Authority (NYSERDA) and the Department of Environmental Conservation (DEC) on Dec. 20 suggest a broad and layered “waterfall” approach to distributing CCAA funds. The method would primarily use a refundable tax credit that then cascades down to those unable to access the funds through more targeted methods, such as through existing welfare programs.

The state has been evaluating a cap-and-invest proposal for more than a year. The program would auction emission allowances to obligated sources, such as large-scale emissions producers, and nonobligated entities, such as agricultural or forestry industries. Proceeds from those auctions would feed the CCAA, which in turn would fund climate projects, particularly in disadvantaged communities (DACs). (See NYISO to Comment on State’s Cap-and-invest Plan.)

NYSERDA and DEC reviewed 29 policy precedents and assessed the eligibility of 14 benefit programs, concluding that an ideal cap-and-invest program would minimize the exclusion of eligible individuals due to administrative or systemic barriers.

The outline details the key regulatory and compliance aspects of the cap-and-invest program, including the mandatory greenhouse gas reporting program rule, cap-and-invest rule and auction rule. The document currently contains placeholder values for aspects such as price levels for emission allowance price triggers or ceilings, but the actual values will be released in January.

The study focuses on the effective and equitable distribution of money collected in the CCAA from the cap-and-invest program.

The agencies recommend that CCAA fund distribution prioritize low-income individuals, those facing high energy costs and non-tax filing households, proposing a progressive, means-tested benefits program to expand accessibility. The report also recommends exploring direct payments, utility bill assistance or transit vouchers to reach non-tax filing individuals or households.

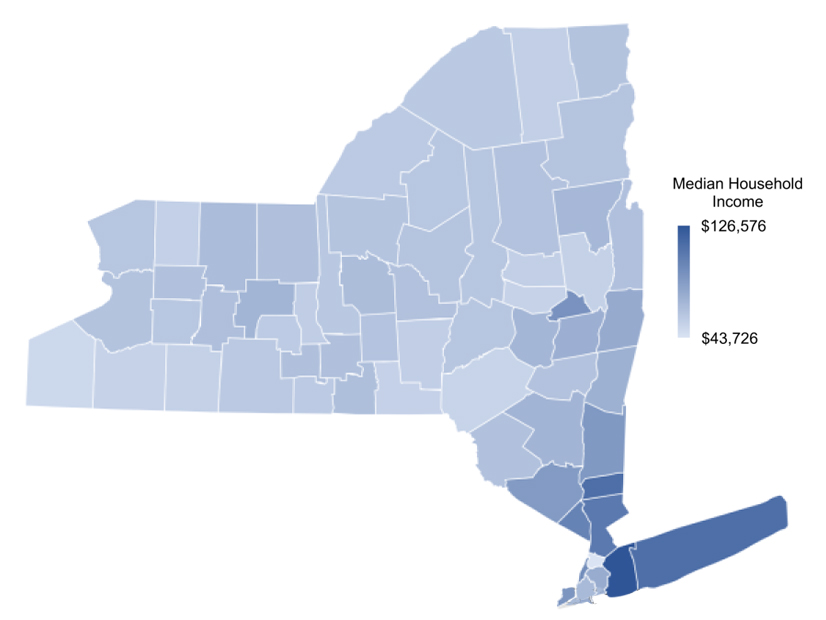

Median household income by county across New York | NYSERDA

‘Cornerstone’

New York currently lacks any programs with a waterfall approach, but the study draws comparisons to federal programs like Supplemental Security Income for disabled individuals or those over 65 and government health insurance programs that use personal income to determine eligibility for state-sponsored health tax credits.

The study says, “a waterfall approach would likewise utilize multiple programs to reach a larger set of households and would likewise restrict the ability of households to receive cumulative benefits from multiple programs.”

The proposed waterfall approach aims to prioritize and channel funds to DACs, ensuring support for climate-related expenses and energy costs for the most impacted populations.

However, the agencies acknowledge that no single distribution approach or regulation can achieve all the goals of the cap-and-invest program. They therefore recommend assessing the feasibility of the waterfall approach while also considering other methods to ensure all eligible New Yorkers benefit from the CCAA funds.

NYSERDA and DEC will continue accepting stakeholder comments on their cap-and-invest proposals. The agencies plan to issue a draft regulatory package and start the formal regulatory process after hosting three public meetings in January.

Anne Reynolds, executive director of the Alliance for Clean Energy New York (ACE), said in a statement that “the cap-and-invest policy is a cornerstone of New York’s Climate Scoping Plan — not just because it would create the cap on carbon pollution that declines over time, but because it would generate funds to help pay for implementation of the rest of the plan.”

She added that the DEC should “include the electricity sector, as ACE argued in comments submitted this past August.”

Kate Courtin, senior manager at the Environmental Defense Fund, said in a statement that “an ambitious program with a high-integrity cap on emissions will play a critical role in getting New York on track to meet its climate targets and delivering a safer, healthier future for New Yorkers.”

FERC on Dec. 19 opened an inquiry into whether it should continue to grant blanket authorizations for holding companies — particularly large investment management companies — to purchase public electric utility securities (AD24-6).

Under Federal Power Act Section 203, companies must seek FERC approval for purchases of utility securities that are worth more than $10 million. Under Order 669, issued in response to the Energy Policy Act of 2005, the commission grants companies three-year blanket authorization to do so — rather than require them to return for each such purchase — subject to certain conditions, including that it cannot use that ownership to direct utilities’ management.

FERC said at the time its goal was to ensure the rules did “not impede day-to-day business transactions or stifle timely investment in transmission and generation infrastructure.”

In a Notice of Inquiry issued at its monthly open meeting, FERC is seeking comment on “whether, and if so how, the commission should revise that policy given the significant changes in the financial services sector in recent years and their investments in and effects on wholesale electric power markets.”

The notice asks commenters to respond to 17 questions, with five devoted to large investment companies. “The three largest index fund investment companies currently vote over 20% of the stock in the largest U.S. public companies, a number that may soon rise to 40%,” the commission noted. “Some have argued that the size of these investment companies creates issues related to competition and gives the investment companies unique leverage over the utilities whose voting securities they control.”

“It simply is no longer a credible assertion that investment managers, like BlackRock, State Street Corp. and The Vanguard Group Inc., are always or should be assumed to be merely passive investors,” Commissioner Mark Christie said in a concurrence to the NOI. “These investment managers are often the three biggest investors in publicly traded companies across the U.S. economy, including the utility industry, and wield significant financial power by virtue of their investments.”

Christie and his colleagues indicated last year they were wary of granting blanket authorizations for the so-called “Big Three” investment companies he cited. Though they approved BlackRock’s reauthorization, he and Commissioner Allison Clements called on the commission to reconsider its regulations (EC16-77-002). (See BlackRock Decision Unearths FERC Wariness of Investor Influence on Utilities.) Consumer advocacy group Public Citizen protested, arguing it was impossible for BlackRock to remain passive, given its size.

Christie and fellow Republican Commissioner James Danly cited competition concerns, while a group of Republican state attorneys general challenged Vanguard’s petition on the grounds the investment manager was seeking to pressure utilities to adopt environmental, social and governance (ESG) investing policies.

“I think it’s important to note that we’ve had a pretty broad call from a lot of stakeholders — from members of Congress; from state attorneys general,” FERC Chair Willie Phillips told reporters at a press conference after the commission’s meeting. “What I agree with is that it’s time to revisit our authority regarding these financial institutions, and how we address their blanket authority.”

Initial comments are due within 90 days of the NOI’s publication in the Federal Register, with reply comments due 30 days after that.

Along with questions regarding the size of companies seeking blanket authorizations, the commission also asks whether the current conditions and restrictions it imposes are enough to ensure the companies lack control over the utilities, and whether there should be additional ones. “It has been argued that by holding voting securities in a large number of public utilities, investment companies are able to influence utility behavior in ways that are not captured by the commission’s current analysis of control,” FERC said.

“The subject that I think would be most helpful to the commission is for people to file comments regarding what types of control should get the commission’s scrutiny,” Danly said during the meeting. “There’s good reason to believe that, in fact, this control question has not been perfectly adhered to, or at least not adhered to in the way that the commission would have thought of when we originally implemented this program.”

“Let us be clear — ‘ESG’ investor activity is simply a symptom of a larger, more pernicious threat that has always existed in the utility industry: improper investor influence and control over public utilities,” Christie wrote. “Large investors can and do force utilities to make decisions that are contrary to their public service obligations to their retail customers.”

In an article published in the Energy Law Journal in November, authors Hugh Hilliard and Caileen Gamache found that FERC has denied blanket authorization only three times. “In each case, FERC denied approval because the applicants ‘failed to demonstrate that the proposed transaction will not have an adverse effect on rates,’” they wrote.

But to Hilliard and Gamache — retired senior counsel with O’Melveny & Myers, and a partner in the Projects Group of Norton Rose Fulbright, respectively — “this means the vast majority of proposed transactions are consistent with the public interest.”

“It would save a lot of time and resources if the rules more effectively resulted in applications for transactions that actually have potential to raise public interest concerns. This will facilitate ‘greater industry investment and market liquidity,’ which FERC has agreed ‘are important goals,’” they wrote, citing a supplemental policy statement to Order 669 the commission issued in 2007.

The authors also argued that this policy statement, intended to clarify the order, “has been insufficient for determining whether each of the veto and consent rights … in many equity investment documents are consistent with a finding that the investment is passive.”

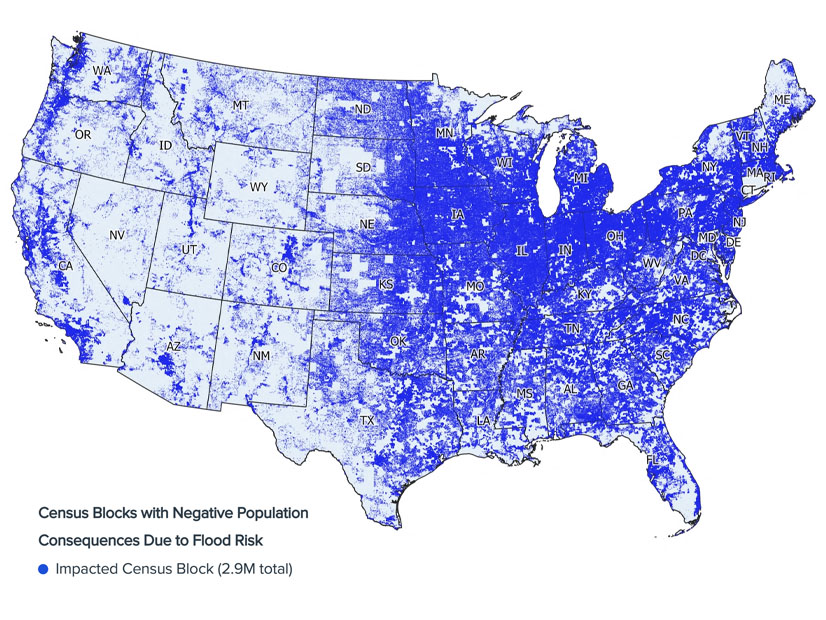

More than 110 million Americans live in places where flood risk is impacting housing choices, and millions have already left or chosen not to move to communities that climate research nonprofit First Street Foundation calls risky-growth and “climate abandonment” areas.

Together, those areas are home to one-third of the population and 42% of all housing stock in the contiguous U.S., and additional areas are expected to reach a tipping point and see similar impacts over the next few decades.

In a Dec. 19 webinar, the authors of the foundation’s Climate Abandonment Areas report published in Nature Communications said the areas experienced a loss of 3.2 million people between 2000 and 2020 that was directly attributable to flood risk. Risky-growth areas, on the other hand, still grew, but at a lower rate than if there were no flood risk.

“More than 34% of the population in the contiguous U.S. live in [census] blocks which have already seen an impact from flood risk on population growth or decline,” said lead author of the study, Evelyn Shu, a senior research analyst at First Street Foundation. “This doesn’t mean that all of these populations declined because of flood risk or even that they will necessarily decline in the future, but a big proportion of the U.S. population is in blocks which may have seen slower growth than they would have otherwise.”

“No matter where you are across the country, models are showing that areas that have high flood risk within a community are not growing as fast or are declining versus places that don’t have that flood risk,” Jeremy Porter, head of climate implications at First Street Foundation, said. The models control for amenities such as schools and medical care, socioeconomic characteristics such as age and income, and economic opportunities such as job availability.

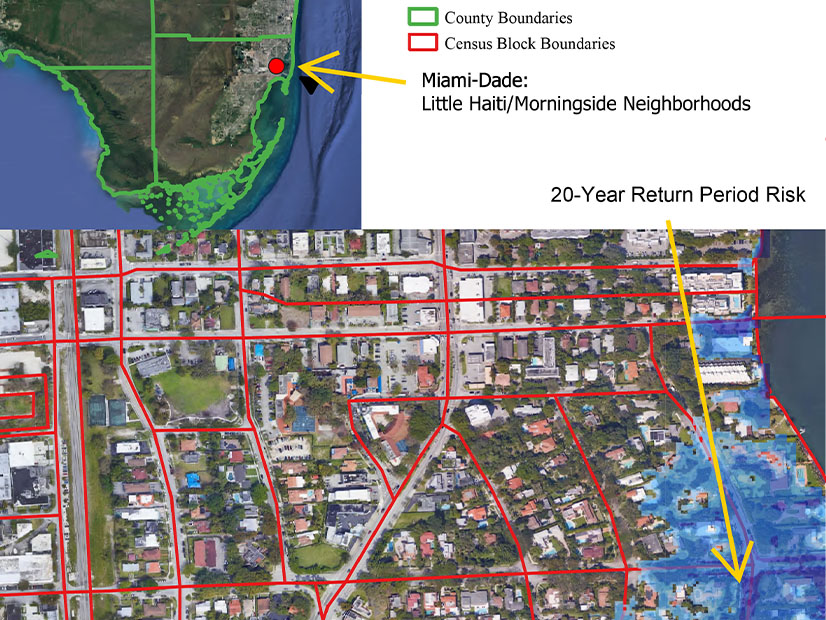

The study mapped high-resolution flood data against granular population changes. Population data was compared for the 11 million census blocks in the contiguous U.S., each with around 80 to 120 people — that is, areas as small as a building in a dense city or a block in a suburban neighborhood.

“We use high-resolution data on historic and current flood exposure, which includes data from the First Street Foundation flood model, and the proportion of properties that are inundated in a given block across the 5-, 20-, 100- and 500-year return periods,” Shu said.

Climate risk is a house-by-house issue, not a state-by-state issue. | First Street Foundation

Climate Disasters and Population Mobility

First Street Foundation tracks events resulting in at least $1 billion in damage, including wildfires, droughts, floods, hurricanes and winter storms, and while all states are affected, there are notable concentrations.

“Of the $2.65 trillion in billion-dollar damages that we’ve seen since 1980, over half of it is accounted for by four U.S. states: California, Texas and Florida plus Louisiana. We can see this sort of hyper-concentration of damages and exposure in these areas,” Porter said.

The study focused on flood risk; however, all climate-related risk factors are likely to impact migration within the U.S. The cross-state migration trend that has been going on for decades is dominated by moves “from the Rust Belt to the Sun Belt,” Porter said. “But we’re also seeing information that people are starting to take climate into account.”

While there is interstate migration, they are vastly outweighed by moves within a state or county, and those local moves are where climate risk is layered with personal experience, Porter said.

“You’re starting to take into account things like local knowledge and information about the community that you don’t have when you move across state lines. If I moved in my neighborhood, I know what streets flooded during a heavy rainfall, I know what areas to avoid during coastal flooding,” he said.

34.5% of the population live in census blocks that have already been impacted. | First Street Foundation

Water’s Siren Song

People have a love-hate relationship with water: They are drawn to areas with beaches, rivers and lakes, but there comes a point where the increased flood risk drowns out their siren call. “We tend to see the densest areas, both within cities and across the country, close to water,” Porter said. “As you get more and more properties at risk of flooding within a community, we’re seeing this increase in population until you hit a certain tipping point and then we’re seeing a level-off or even decline.”

While climate abandonment areas had net population declines, risky-growth areas “grew by about 17.4 million people from 2000 to 2020, relatively significant growth for those 2.1 million blocks, but the model showed that they would have grown to about 21.5 million people if it wasn’t for the flood risk,” Porter said. Those areas were so attractive based on amenities, job opportunities and other factors that they outweighed the flood risk for many, but not all, people choosing a community to live in.

People leaving climate abandonment areas often move locally, leading to what some have called climate gentrification. A disproportionate amount of climate abandonment areas are in growing metropolitan areas such as San Antonio, El Paso, Fort Worth and Houston in Texas, and Tucson and Phoenix in Arizona.

“People don’t want to live in those flood-risky neighborhoods, even if they would still want to live in the same area,” Shu said. For example, someone who still wants to live in Miami-Dade County, which has a lot of flood risks, is likely to consider neighborhood differences and make trade-offs, resulting in a migration from the lower-lying areas to higher elevations.

Flood risk isn’t the only thing leading to population loss in climate abandonment areas. Of the 9 million in total population loss in those areas from 2000 to 2020, about 3.2 million could be attributed to flood risk while the other 5.8 million were related to other socioeconomic characteristics of a community, such as lack of opportunity in rural areas. Those areas tend to spiral downwards, with declining housing prices and a loss of local businesses eroding the city tax base and cutting services.

FERC rejected SPP’s proposal to modify its market power test for the Western Energy Imbalance Service, faulting a provision granting the Market Monitoring Unit discretion in applying the rules (ER23-2183).

SPP proposed tariff changes to address a finding in the MMU’s August 2020 WEIS Market Power Study, which identified a high level of structural market power in the WEIS market.

SPP said its residual supply index (RSI) — the ratio of capacity not owned by a market participant to total market demand — failed to consider the total capacity from affiliated market participants together. That created an opportunity for an entity to split its fleet of resources into multiple market participant registrations to avoid failing the test, the MMU said.

FERC’s Dec. 19 order approved new tariff language specifying that the RTO would consider together “all on-line resource capacity from any affiliate of the market participant.”

But the commission rejected a second change that would have allowed the MMU to exclude from the RSI calculations capacity associated with an affiliate if the monitor was convinced the participant maintained “safeguards and corporate controls to prevent coordinated or collusive market activity,” such as maintaining electronic permissions and access controls and physically segregating the personnel who make daily bid/offer or strategic market decisions.

FERC said the second change would undermine the first and thus was not just and reasonable.

“Accordingly, we reject the entire proposal as filed, but we note that SPP may resubmit a proposal that addresses the concerns described above,” the commission said.

FERC approved a settlement between PJM and 81 parties to reduce the $1.8 billion in non-performance charges assigned to generators that did not meet their capacity obligations during the December 2022 winter storm (ER23-2975, EL23-53).

The commission’s Dec. 19 order lowers the penalties to approximately $1.25 billion, a nearly 32% reduction, and resolves the bulk of the 15 complaints generators filed over the charges. In a separate order, the commission rejected a complaint from Energy Harbor disputing how PJM factored a maintenance outage into its calculation of the W.H. Sammis coal generator performance shortfall.

“PJM appreciates the cooperation of its members who participated in the FERC-supervised settlement proceedings and reached this consensus-based resolution, allowing the PJM stakeholder community to focus on improvements and solutions going forward,” PJM General Counsel Christopher O’Hara said in an Inside Lines post regarding the commission’s order.

The agreement caps off months of settlement judge procedures the commission initiated June 5 resulting in the agreement reached in September. All of the complainants supported the agreement, with the exception of the Old Dominion Electric Cooperative (ODEC), which joined as a non-opposing party. (See Settlement over PJM Elliott Penalties Receives Broad Support.)

Because the collection process for the penalties already is well underway, reduction of the penalties will involve recipients of overperformance bonus payments returning a portion of their allocations. Under the capacity performance structure, underperformance penalties are paid out to generators that exceeded their expected performance during emergency conditions.

During the Dec. 20 Markets and Reliability Committee meeting, PJM Executive Vice President of Market Services Stu Bresler said staff are drafting an FAQ detailing how the settlement will be implemented, the effects it will have overall and how companies can calculate the change to their penalties and overperformance bonuses.

PJM and supporters of the settlement argued it would reduce market disruption that could result from penalties of that magnitude and protracted litigation about their legitimacy.

Chief Keystone Power and Chief Conemaugh Power raised the only objections to the settlement, but were overruled by the commission, which found the companies had lost their chance to be party to the agreement by waiting until after it had been filed with FERC to seek intervenor status and file a protest.

“Allowing entities to intervene in the new docket generated by the filing of a settlement, when such entities did not participate in the underlying dockets and settlement discussions, would run contrary to cases where the commission has disallowed parties to intervene for the first time after the parties have agreed to a settlement,” the order says.

The settlement left two issues raised by Energy Harbor and the East Kentucky Power Cooperative (EKPC) open for the commission to decide: how to calculate the penalties the Sammis facility is responsible for, and an argument the cooperative made that the capacity performance penalty structure and annual stop loss are unjust and unreasonable without a connection to generators’ capacity market revenues.

In its complaint, Energy Harbor argued that PJM had effectively disregarded a 300-MW maintenance outage the Sammis facility was on at the time of Winter Storm Elliott by subtracting the outage from the resource’s installed capacity (ICAP) value. The company said that was the wrong figure to look at, since it includes both committed capacity and uncommitted capacity the resource is not obligated to make available during emergency procedures. Instead, it made the case that PJM should have netted it against the performance shortfall it experienced — the difference between its expected and actual output used to derive the penalties.

PJM stated that excused outages, such as for maintenance, can reduce only a capacity resource’s performance shortfall and associated penalties if it is the sole reason the generator did not meet its obligation. In this case, PJM said forced outages Sammis experienced Dec. 23 and 24 accounted for the full shortfall.

“Even taking into account the maintenance outage of 300 MW, Energy Harbor should have been able to meet its expected performance. It failed to do so, because of the forced outages of Units 5 and 7. Hence, the maintenance outage was not the sole cause of Energy Harbor’s inability to meet its expected performance as the tariff requires,” the commission’s order says.

The EKPC complaint argued that basing the penalty rate and annual stop loss on the net cost of new entry (CONE), rather than the Base Residual Auction (BRA) clearing price, results in the potential for penalties being higher than the revenues a resource can earn in the market. The commission has yet to issue an order on that filing.

In a filing at the conclusion of the critical issue fast path (CIFP) process, PJM proposed to revise the calculation of the annual stop-loss limit to be based on the BRA clearing price and retain the penalty rate derived from net CONE. (See “PJM Steams Ahead with CIFP Filing Timeline After FERC Deficiency Notices,” PJM MIC Briefs: Dec. 6, 2023.)