The NEPOOL Participants Committee on March 7 unanimously approved ISO-NE’s package of tariff revisions to comply with FERC Order 2023.

ISO-NE expects to submit the compliance filing April 1, two days before the deadline set by FERC in its efforts to unclog interconnection queues that have bogged down nationwide.

The vote follows months of deliberations that included a Feb. 15 NEPOOL Transmission Committee meeting at which an initial proposal, as well as six proposed amendments to it, failed to gain the two-thirds support needed for approval. (See ISO-NE Order 2023 Compliance Proposal Fails to Pass NEPOOL TC.)

ISO-NE incorporated several elements of the amendments into the final package, which was approved with only two abstentions.

The RTO summarized the post-Feb. 15 changes to the package in a March 1 memo to the committee:

An interconnection customer may specify in its interconnection request for capacity network resource (CNR) interconnection service that the requested service be downgraded to network resource interconnection service under certain conditions.

After the completion of a cluster study (not including the transitional cluster study), if the RTO determines that a cluster restudy is required (because of the withdrawal of other projects), the developer of a remaining project may request a specific one-time decrease in the size of the generating facility or elective transmission upgrade for the restudy.

For customers with assigned queue positions as of 30 calendar days after April 1, but for which system impact studies are projected to be completed between May 1 and June 30, the RTO will still tender transitional cluster study agreements. However, if the SIS is complete and accepted by the customer by July 1, the request will no longer proceed to the transitional cluster study. Instead, the customer will be tendered an interconnection agreement pursuant to the applicable provisions in the respective interconnection procedures.

Where a request successfully participates in the transitional CNR group study and then later obtains a capacity supply obligation in the Forward Capacity Market, the rules governing any termination of the CNR capability will be governed by the relevant FCM rules.

“Importantly, each of these additions can be incorporated without adding to the overall time frames or decreasing the efficiency of the new process,” ISO-NE said.

When FERC issued Order 2023 last July, the potential capacity of projects waiting in interconnection queues exceeded 2 TW, more than the amount of generation already online nationwide. It seeks to streamline the interconnection process for transmission providers, provide greater timing and cost certainty to interconnection customers and prevent discrimination against the wave of renewables being proposed nationwide. (See FERC Updates Interconnection Queue Process with Order 2023.)

Nevada regulators approved NV Energy’s plan to convert its last coal-fired power plant to natural gas, while also allowing the company to move forward with a $1.5 billion, 400-MW solar-plus-storage project.

Approval of the solar-plus-storage project, known as Sierra Solar, may allow the utility to reduce an open position that’s been described as one of the largest in the West. NV Energy is developing the project, which would be about 15 miles northeast of Fernley in northern Nevada.

But whether Sierra Solar will be built remains to be seen.

In an order approved March 1, the Public Utilities Commission of Nevada (PUCN) set conditions on Sierra Solar including payment of damages to ratepayers if the project is delayed or doesn’t perform as expected.

The order admonished NV Energy for arguing that it needed to move forward quickly with the project, then balking at conditions. It quoted NV Energy’s response when asked about a maximum project cost: “If the commission … feels like it has to have an upper limit on costs, we’ll assess if we think it’s reasonable and whether we can move forward with the project or not.”

“The commission is persuaded that there is a resource adequacy need necessitating consideration of the Sierra Solar project now and is troubled by the suggestion that this need may be ignored unless NV Energy gets the terms that it desires for the Sierra Solar project,” the commission wrote in its order.

In a news release after the commission’s vote, NV Energy said it “is diligently reviewing the conditions the commission placed upon the project.”

Planning Process Questioned

NV Energy proposed the Sierra Solar project through the fifth amendment to its 2021 Integrated Resource Plan. The amendment also proposed the conversion of the North Valmy Generating Station, NV Energy’s last coal-fired plant, to run on natural gas through 2049.

PUCN largely approved the amendment, despite objections of stakeholders who said the projects should go through a more comprehensive evaluation as part of the utility’s 2024 IRP that will be filed this year.

Instead, the utility has resorted to “crisis planning” through multiple amendments to the IRP, said Emily Walsh, clean energy policy adviser at Western Resource Advocates. Walsh noted that the cost of projects proposed in the fifth amendment far exceeded that of projects in the 2021 IRP.

“They’ve really been gaming the IRP process,” Walsh told RTO Insider.

In addition to approving Sierra Solar and the North Valmy conversion, the commission authorized a 2049 retirement date for two gas-fired units at the Tracy power plant, which had been scheduled for closure in 2031.

But the commission declined to approve an asset purchase agreement for future development of the 149-MW Crescent Valley solar-plus-storage project about 50 miles from the Valmy plant. Because the project is at an early stage, the utility can bring the proposal back as part of its 2024 IRP, the commission said.

Open Position

One of the drivers behind NV Energy’s proposals was to reduce its open position — resource needs that are met through short-term market purchases rather than by utility-owned resources or long-term contracts.

In a survey of 13 Western utilities, NV Energy’s projected open position in 2025 was 1,092 MW, second only to that of PacifiCorp’s 1,637 MW, according to testimony filed with PUCN on behalf of the utility. As a percentage of peak demand, NV Energy’s open position was 13%, ranking sixth out of the 13 utilities.

Proposals in NV Energy’s IRP amendment would reduce its open position to 820 MW in 2026, representing 10% of peak demand.

The commission’s order also addressed NV Energy’s participation in the Western Resource Adequacy Program, directing the utility to postpone its financially binding season from winter 2026/27 to winter 2027/28.

“NV Energy’s [forecast] open position for the summer of 2027, with or without commission approval for the requests in this docket, would subject NV Energy to substantial penalties that could be passed on to ratepayers,” the commission wrote.

Valmy Solution

In its 2021 IRP, NV Energy planned to replace capacity from the coal-fired North Valmy Generating Station with the Iron Point and Hot Pot solar-plus-storage projects. The utility plans to end coal combustion at Valmy by the end of 2025.

But supply chain issues derailed the solar projects, according to the utility, which then proposed a 200-MW battery storage project as a partial solution for the Valmy retirement. The commission rejected the proposal, asking NV Energy to come back with a complete solution for Valmy. (See NV Energy Rejected on Plan to Replace Coal Plant with Storage.)

In its March 1 order, the commission approved the plan to convert Valmy to natural gas but granted only $50 million of the $83 million NV Energy wanted for the project.

The $50 million is NV Energy’s actual costs for the project, the commission said, while the remaining $33 million is “just a placeholder amount associated with upgrades that may be needed at some point in the future.”

NV Energy plans to split the cost of the Valmy conversion with Idaho Power, which is 50% owner of the plant.

NV Energy acknowledged that it initially didn’t consider a gas conversion for Valmy. But a new transmission study found that an area called the Carlin Trend needs voltage support from a firm dispatchable resource.

The commission said the Carlin Trend constraint is “a real condition.” In addition, “without Valmy, there is a high probability Nevada would have experienced rolling blackouts three out of the last four years,” the commission stated in its order.

Once NV Energy’s Greenlink West transmission line is completed, the Valmy plant may be able to run less often, the commission noted.

ALBANY, N.Y. — The networked heating systems New York wants to test on a pilot scale hold promise for the environment and society but are taking time to design.

A March 6 conference brought together many of the people advocating for thermal energy networks (TENs), one of the tools the state is considering to reduce its carbon footprint.

Buildings account for a third of New York’s carbon dioxide emissions, and TENs hold the promise of reducing that by using less energy and using it more efficiently.

The Public Service Commission in 2022 ordered the seven largest investor-owned utilities to propose pilot projects that point the way for a permanent regulatory structure for utility TENs.

Eighteen months later, the order has accomplished its initial goal — yielding a greatly varied set of proposals that could broadly inform future efforts — but the proposals are still at the first of several stages of PSC review. (See NY Utility Thermal Energy Network Pilot Program Simmers.)

And the potential framework for what would be an entirely new class of utility in New York only recently has been released in draft form.

The title of the summit — “Scale Up! Decarbonizing NY’s Neighborhoods” — accurately conveyed its mood: The room was full of supporters.

The Building Decarbonization Coalition was one of the organizers, and its New York director, Lisa Dix, called the state’s first-in-the-nation utility TENs enabling legislation “one of the most important efforts to date to usher in the clean energy transition for buildings at scale in this state.”

Simple and Complicated

Some potential tools of the clean energy transition — long-term battery storage, small modular nuclear reactors, economical but clean hydrogen generation — would require technological or engineering leaps to be usable.

TENs are straightforward by comparison: Move heat from where it is unwanted to where it is needed within a group of buildings via fluid in pipes. Less energy is used, less is wasted.

A project might be more or less complicated, depending on whether it includes details such as geothermal bores and heat pumps, or if there is a motherlode of wasted heat nearby, such as a data center.

But the technology for accomplishing these tasks is known and mature. And as Jared Rodriguez of Emergent Urban Concepts pointed out, municipalities have decades of experience moving water from place to place through pipes. “It’s not rocket science.”

The more daunting tasks in New York are shaping up to be organizational:

getting enough property owners on board in a neighborhood.

siting the infrastructure.

deciding who pays for it.

building it strategically so natural gas infrastructure can be retired or at least not expanded.

transitioning gas workers to thermal jobs.

maintaining union representation.

ensuring economic and environmental benefits for disadvantaged communities.

creating a new class of state regulated utility.

making the entire process fit into the larger picture of the clean energy transition.

This is why the state is starting with pilot projects, and why development of those pilot projects is proceeding methodically.

Department of Public Service Chief of Staff Jessica Waldorf said: “It has taken us centuries to build the systems that we have in place, and we cannot make a wholesale shift of our energy systems and the way that customers choose to use them in an instant.

“Advancing projects like these at scale in existing communities as part of neighborhood-level decarbonization efforts is a new frontier, and one that will require partnership of many different stakeholders, like all of you in this room, to effectuate.”

She said, however, that progress to date makes her confident of progress to come:

“Make no mistake — the transition to cleaner sources of energy has been taking place for decades, where we have witnessed transitions away from dirtier sources of energy, like coal or oil in the power sector, to movements in our building sector to make our buildings significantly more energy efficient and in greatly reducing emissions for our transportation sector.”

Varied Perspectives

Jessica Azulay, executive director of the Alliance for a Green Economy, said TENs are just one tool in the clean energy transition.

Their value is that they help bring about a managed transition, in which everyone in a defined area can switch away from gas. The alternative path to building decarbonization is individual homeowners installing heat pumps, which is an unmanaged transition, and leaves the residents unable to afford heat pumps shouldering an increasing share of the cost of the gas infrastructure.

“Obviously this is not an either-or; our transition is going to be multifaceted, but I think we’re going to be much better off if we use thermal energy networks as a major tool in our toolbox,” Azulay said.

She noted the rate of heat pump adoption in New York would have to increase tenfold for the state to reach its building decarbonization milestones through heat pumps alone.

Indu, the director of energy at the nearby University at Albany, described the situation at her campus, which essentially is a small city with a population that sometimes exceeds 20,000 in a diverse collection of 100-plus buildings spread across 500 acres.

It’s an ideal place for TENs, and in fact there are two TENs in operation, but they are fossil powered and only about 70 to 80% efficient. A $30 million upgrade was included in the 2023-24 budget to change this, and better achieve the promise of TENs.

A new high-efficiency electric centrifugal and heat recovery chiller connected to a new geothermal well field, new hot water system and new piping will reduce campus gas use 15%.

“So, this idea of saying OK, seasonal thermal storage, moving it around, I don’t want to be burning gas or oil to create heat and I have this heat already,” Indu said. “All I have to do is store it and move it from one place to another. When you start thinking about it like that, [instead of] the 70 to 80% efficiency system, you’re talking 350 to 700% efficient systems.”

It’s a win-win-win for the campus, community and planet, she added, and the efficiency is such that the operating budget will not increase.

Vikas Anand, Danfoss vice president of climate solutions North America, keyed on the opportunities presented by efficiency. He cited the famous chart compiled by Lawrence Livermore National Laboratory showing more than half of U.S. energy consumption evaporating in the form of waste heat.

A graphic representation of the estimated quantities of energy wasted in the United States. | Lawrence Livermore National Laboratory

“So, the opportunity for us to manage waste heat is so immense, that we can meet our climate goals as a country, I will say, very easily,” Anand said.

The question was raised about how large commercial properties fit in these systems.

“Most residential consumers don’t voluntarily pay for green,” Trent Berry of Reshape Infrastructure Strategies said. “That is more prevalent in the commercial sector because they’re competing for tenants” that have net-zero goals. Other factors making TENs attractive to commercial building owners include energy standards for new buildings and local regulations requiring energy efficiency or decarbonization.

New York is the second-most unionized state, and officials include labor-friendly provisions in many of their initiatives. But where does the next generation of union members come from?

John Murphy of the New York State Pipe Trades Association said it’s important the transition be framed as a path to the future rather than the end of an era for certain trades. People need to see a future they can plan a career around.

“I think what’s most important is that when we have a certainty of work, we know that there’s a pipeline of work ahead. It allows building trades unions to recruit from the community, to be able to train the workforce — can’t happen without that work certainty,” Murphy said.

“I can tell you, even for the workers and the members in my industry, when they say, ‘Where is our transition,’ we need to show them this is the path, this is the future, and it’s nothing to be afraid of, you can work here.”

Eric Walker of WE ACT for Environmental Justice sought to focus on the many New Yorkers using energy they can’t afford, to the detriment of their health:

“How are we going to think about these … technocratic solutions as ways to meet basic needs for people who are often not even discussed in the conversation around what our energy and economic development agendas are in the state?

“I think of thermal networks really as one of many approaches to meeting a series of basic needs,” Walker said. “We have a really serious problem around energy affordability, and energy security across multiple types of buildings and demographics within the state. There are 3½ million [low- to moderate-income] households in the state that essentially qualify for some form of energy assistance.

“And that is that’s really kind of scary, with about $1.7 billion of utility arrears that remain outstanding. And that to me signals a real need to invest in the kinds of interventions at the system level that provide the energy trilemma … sustainability, security and affordability.”

Which leads once again to the question of who pays for it all.

Much of the expected benefit of decarbonization would be societal and much of it would play out unevenly over years or decades in the form of avoided costs.

The bill for the transition, by contrast, is concrete and inevitable. The only uncertainty is how much of it will fall directly on individual ratepayers and how much of it will be embedded in other things, such as taxes, fees and consumer costs.

Walker said however the bill is allocated, it is worth the cost.

“What we have is an environment where first cost is scaring people without any sort of contextualization for what the actual overall benefit is to every ratepayer in the system, every building owner in the system, to every community across the state,” he said. “If we do nothing, the costs only get bigger; if we do something, the net cost is much better than the first cost. It’s all about investment. … There’s no dollar that we spend at a societal level that doesn’t benefit us in some way.”

The Timeline

Dix said later that the utility TENs pilot program is progressing well — even quickly by the standards of the regulatory world — but a lot of questions about its details are unanswered and some of the questions haven’t even been asked.

Other details are moving targets, such as whether the state will remove the requirement that gas utilities connect new customers to gas lines for free if they are within 100 feet of the line. That’s on the table in budget negotiations.

Dix said she appreciates the two-pronged approach. The theory behind the utility TENs bill was to get pilots moving forward, she said, “because we needed to learn from them, because we really are creating new utility models, an integration of the electric and gas utilities, maybe water. We’re creating all kinds of new customer engagement plans; we’re creating different ownership mechanisms.” Once the projects get going, the regulatory process is “going to be a year or two to get those rules all final and ready to go.”

One thing that gives Dix hope is that the Utility Thermal Energy Network and Jobs Act, the impetus for the pilot projects and the forthcoming TENs regulatory structure, received near-unanimous legislative approval in 2022. Moreover, it wasn’t embedded in a budget package, the back-door route by which many contentious measures become law in New York state.

“This was a very long effort where we worked together to focus on the solutions that unite us rather than divide us,” she said.

The Public Service Commission set Case No. 22-M-0429 in motion in September 2022 with an order that the state’s seven largest investor-owned utilities propose one to five pilot TENs projects.

By September 2023, they had submitted 14 widely varied proposals with a price tag of up to $435 million.

At their meeting that month, the PSC judged those proposals good first efforts but insufficient in detail, and it issued an order providing guidance on how best to refine the proposals.

In February 2024, the Department of Public Service published its proposal for initial utility TENs rules and invited public comment. The latest technical conference — on potential performance metrics — is scheduled for March 19.

All indications are that FERC is working to complete its transmission planning and cost allocation rulemaking in the next few months, with public statements from commissioners saying it’s a priority and those familiar with the agency placing bets on which month’s open meeting a final rule will be announced (RM21-17).

With three nominees awaiting confirmation for the two open seats and that of Commissioner Allison Clements, whose term expires in June, sources said in recent interviews it might be best for FERC to act on the Notice of Proposed Rulemaking (NOPR) before its composition changes. (See Phillips: FERC to Issue Transmission Rule in ‘Very Near Future’.)

“I think Commissioner Clements very much wants to be part of this,” former FERC Chair Jon Wellinghoff said. “So, I’m sure she’s doing everything she can to work with staff and work with the other two commissioners, to move this forward as quickly as possible.”

The rulemaking could face a delay if it is not completed before the composition of the commission changes, said WIRES Executive Director Larry Gasteiger, a former FERC staffer.

“This is an extremely complicated rulemaking effort that the commission is doing,” Gasteiger said. “And just for [the new members] to get up to speed on it, in order to knowledgeably vote on it, is inevitably going to take a couple of months minimum. That will be added time on the timeline for getting the rule out.”

Another issue is uncertainty around November’s elections, with the House, Senate and White House up for grabs.

Republicans could use the Congressional Review Act (CRA) to overturn a rule that is filed late in the Biden administration, said former FERC Chair Neil Chatterjee, now a senior adviser at law firm Hogan Lovells. Rejecting a rule requires votes of disapproval by both the House and Senate but can be blocked by the president unless his veto is overridden.

“I don’t know if it’s constituted as a major rule, but I think the White House and FERC don’t want to take that risk,” Chatterjee said. “And I think that, certainly, there are steps the commission could take, if you had Republican majority control, that would try to change course on some of these rulemakings.”

The commission currently has two Democrats, Clements and Chair Willie Phillips, and one Republican, Mark Christie. The three candidates nominated by President Biden last month would give Democrats a 3-2 edge. But if Donald Trump retakes the White House, he could replace Phillips, whose term expires in 2026, with a Republican. (See Biden Names 3 Nominees to Give FERC 5 Members Again.)

Christina Hayes, executive director of Americans for a Clean Energy Grid, was a FERC staffer in 2011, the last time it made major changes to its transmission planning and cost allocation rules with Order 1000.

“There was something like 40 hours where the commissioners’ advisers were talking and negotiating, before they were able to issue Order 1000,” Hayes said. “That’s something like two months of negotiation among commissioners’ offices on the 11th floor. So, I imagine they’re probably well into that process at this point.”

The transmission rule came out of an advanced NOPR issued nearly three years ago, so the commissioners have been talking about the issues for some time, said Philip Moeller, executive vice president of regulatory affairs for the Edison Electric Institute.

“Each commissioner is going to have their own set of priorities,” said Moeller, who was on FERC when it passed Order 1000. “And those are probably going to be negotiated and probably have been negotiated to some extent for at least the last couple of years.”

To the extent that commissioners support the rule’s overall thrust — that the grid needs to expand to meet future needs —they will be working on compromises because the more consensus there is, the more robust the rule will be in the face of inevitable litigation, Moeller added.

Impact of Dissents

In 2011, Moeller dissented on Order 745 over its compensation method for demand response (DR). Litigation over the rule wound up at the Supreme Court, which ruled against appeals that claimed FERC had overstepped its jurisdiction. (See Supreme Court Upholds FERC Jurisdiction over DR.)

“It was kind of fun to have my dissent mentioned there during arguments,” Moeller said. “But I think ultimately the problem with that litigation, specific to 745, was that the main attack was on the jurisdiction. And that was really never an issue for me. For me, it was the level of compensation and how it was done. And unfortunately, the court focused solely on the jurisdiction and ruled that FERC had it.”

The more complex issue of compensation — Moeller would have preferred a somewhat smaller payment for DR in energy markets — was largely ignored by the courts because litigants focused on jurisdictional questions over how DR is treated in state-regulated retail markets and federally regulated wholesale markets.

Wellinghoff was the driving force behind Order 745 as chair of FERC at the time. While he did not convince Moeller, he did get a Republican vote from then-Commissioner Marc Spitzer.

“To the extent those dissents are well written, and those dissents have legitimate reasons for objecting to portions of the order, they act as fodder for the appellant,” Wellinghoff said. “Those are things that they use as arguments in court, so they can be compelling in that way.”

While partial dissents like Moeller’s on Order 745 are less of a threat to a rulemaking than a full dissent, Wellinghoff said judges will rule based on the legal arguments before them rather than counting votes of the commissioners.

Cost Allocation

Ultimately, the public will see the outcome of all the behind-the-scenes debates when FERC publishes a final rule. When asked what that should look like, Grid Strategies President Rob Gramlich (another former FERC staffer) pointed to a letter Senate Majority Leader Chuck Schumer (D-N.Y.) wrote to the commission last summer. Schumer said the commission should prescribe the benefits that transmission planners must consider to ensure cost-effective transmission is built and costs are properly allocated.

“Figuring out how they sort out cost allocation will be important — just to make sure that they stick to the beneficiary-pays approach, which is what the courts have said they need to do, and they don’t end up sticking too much of the costs on any one party or group,” Gramlich said. “And then making sure there’s a process to resolve disagreements.”

FERC likely will give states chances to come to an agreement on cost allocation before the commission considers stepping in, Gramlich said.

Asked about Clements’ thoughts on the NOPR, her office provided RTO Insider her response to Schumer. She said the commission aimed to develop a “comprehensive and durable approach” that leads to building the kind of infrastructure that has been underdeveloped in recent years.

“I agree that cost allocation rules should endeavor to involve states, while at the same time creating incentives for collaboration and against free ridership,” Clements wrote.

Figuring out how to balance competing policies — with some states seeking rapid progress toward net-zero emissions by midcentury and others wanting nothing to do with it — is a key issue commissioners are wrestling with, Moeller said.

“If you see what New Jersey is doing with their offshore wind [transmission], they’re willing to pay for it themselves,” Moeller said. “So, it’s certainly doable under the status quo.”

Chatterjee said the commission is likely to encourage states to take the lead in determining how public policy project costs are regionally allocated. “The fight will be over what is the dispute resolution mechanism,” he said.

That is where Christie might wind up issuing at least a partial dissent if Chair Phillips can’t bridge any divides among the three members, he added. It will be hard to get states like Chatterjee’s home of Kentucky that have little interest in the energy transition to agree on a transmission plan with states that actively support the transition, he said.

“I think for a state like Kentucky, the view would be we didn’t ask for these benefits, so we shouldn’t have to pay for them,” Chatterjee said. “And just because FERC is defining these benefits, that doesn’t mean that our ratepayers should bear the costs.”

Will a Federal ROFR be Reinstated?

Another point of contention as the transmission rule nears the finish line is what to do about competition. Both Moeller at EEI and Gasteiger at WIRES would like to see the federal right of first refusal (ROFR) at least partly reinstated; it’s one of EEI’s priorities.

WIRES recently released a report based on examples of 29 major projects around the country, arguing that collaboration is key to building out the transmission grid. The competition pushed by Order 1000 has served to discourage that collaboration, WIRES contends.

“If you’re competing against your neighbor for the ability or the right to build a project, it doesn’t create the same incentives to share information or to work with them on trying to get a project built,” Gasteiger said.

Wellinghoff, a champion of transmission competition in Order 1000, argued that pulling back on it now would reward bad behavior by incumbents.

Order 1000 required transmission providers to remove from their FERC tariffs ROFRs on projects selected in a regional transmission plan for cost allocation. It did not affect the right of incumbent transmission providers to upgrade their local facilities.

“There just needs to be, perhaps, more oversight,” Wellinghoff said. “There needs to be more consideration that perhaps even these smaller lines need to be competitive. I’m not sure that the exemption that we put in the original Order 1000 is appropriate. I believe that these lines can be bid competitively and developed and constructed competitively and we would come out better for it.”

CAISO’s Western Energy Imbalance Market (WEIM) played a crucial role in managing energy flows around the West to help support Northwest utilities during an extreme cold snap in January, according to a new report from the ISO describing its response to the winter weather storm.

The 80-page report released March 6 represents the latest volley in an ongoing skirmish among Western electricity sector stakeholders over exactly what occurred on the regional grid during the Jan. 12-16 deep freeze.

“The cold-weather event again demonstrated the benefits of the Western Energy Imbalance Market, an interstate electricity market that covers much of the West,” CAISO said in the report. “The market’s diversity of weather and generating resources allows Western regions to aid each other during winter and summer peak demand periods.”

The event plunged the Northwest into near-record cold and triggered five energy emergency alerts (EEAs), including one critical EEA 3, which requires a utility to prepare for rolling blackouts to protect its system.

It has provoked a debate in the Northwest over how vital CAISO and its WEIM were in supporting the region during the storm, or if other factors were more important. The dispute has become a stand-in for the contest between CAISO’s Extended Day-Ahead Market (EDAM) and SPP’s Markets+ and the related disagreement over whether the Bonneville Power Administration and other Northwest entities should join a single Western electricity market based on EDAM or continue to help SPP develop its alternative. (See NW Cold Snap Dispute Reflects Divisions over Western Markets.)

Analyses from the Western Power Pool, the Public Power Council (PPC) — which represents the Northwest’s publicly owned utilities — and others have downplayed CAISO’s role. They’ve pointed to interchange data showing that most of the generation that rescued the Northwest originated in the Rockies and Southwest regions — and not California. That was evidenced by the fact that CAISO itself was a net importer of energy during the five-day weather event. (See WPP: Cold Snap Showed ‘Tipping Point’ for Northwest Reliability.)

CAISO’s report hits back at that assertion — and other complaints about the ISO’s response — by explaining the mechanisms that directed the movement of electricity across the WEIM over the course of the cold snap.

The report says the WEIM “economically rebalanced supply across the West to meet increasing demand as real-time conditions evolved over the Martin Luther King Jr. Day weekend.”

“The market identified least-cost solutions within the wider WEIM footprint, transferring lower-cost electricity from the Southwest into California,” it says. “These transfers allowed exports scheduled in the day-ahead and hour-ahead markets to flow to the Northwest, replacing more expensive generation while managing congestion on key transmission lines.”

CAISO notes that its hourly exports in the day-ahead and real-time markets “increased significantly” during the event, exceeding 6,000 MW.

“CAISO became a net exporter over the Martin Luther King Jr. Day weekend for all hours of the day, excluding WEIM transfers,” the report says.

The ISO said WEIM transfers into the CAISO area were not the result of limited supply within CAISO but rather a function of the “economic displacement and opportunities optimized by the market and bounded by the transmission and transfers availability in the wider footprint.”

Congestion Response

Several factors were at play during the freeze, which the report notes. They included derates on the Pacific AC (PACI) and DC (PDCI) interties, generation outages and a fault in a fiber optic cable that caused Washington’s Jackson Prairie natural gas storage facility to briefly halt sendout Jan. 13, prompting pipeline operator Williams to declare a force majeure that cut deliveries to interruptible customers, including some power generators.

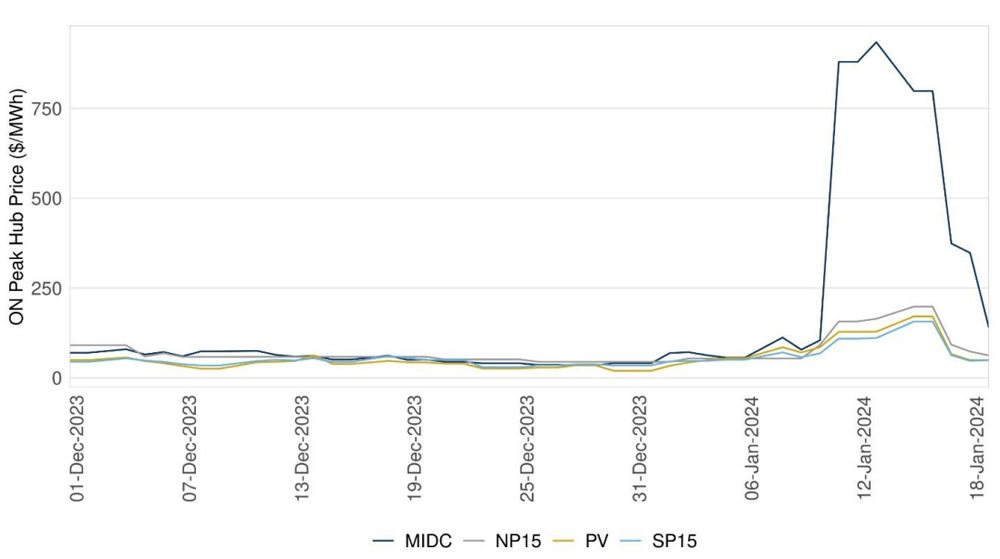

The ISO notes that day-ahead prices surged in the Northwest bilateral market, with Mid-Columbia peak prices hitting $934/MWh on Jan. 13 while off-peak spiked to $927/MWh. While prices rose at the West’s other major trading hubs (NP-15 and SP-15 in California and Palo Verde in Arizona), they never exceeded $250/MWh. The power price spikes in the Northwest in part resulted from the region’s high spot natural gas prices, but gas prices also were elevated in California.

Graph shows how significantly bilateral prices spiked at the Northwest’s Mid-Columbia trading hub during the winter weather event. | CAISO

As Fred Heutte, a senior policy associate with the Northwest Energy Coalition, explained in a recent interview with RTO Insider, the price differentials created a situation in which Northwest load-serving entities looked south for cheaper supply. The CAISO report shows the WEIM did the same.

“First, the WEIM market relied on the most economic supply available which was located in the Southwest; in turn, these import transfers displaced generation in California, which has been priced more expensively given higher gas prices,” the CAISO report said. “Second, there were transmission limitations to afford additional exports or WEIM exports transfers to the Pacific Northwest because Malin [PACI] capacity was already fully scheduled, and no exports could flow on NOB [PDCI].”

During some intervals, northbound segments of Path 15 in California also experienced congestion, limiting flows into Northern California and the Northwest.

The CAISO report additionally addresses a complaint by the PPC that congestion revenue rights (CRR) holders in the ISO’s market financially benefited from $125 million in congestion rents collected on interties into the Northwest during the freeze, while owners and capacity rights holders on the northern portions of those lines earned nothing.

“Before January, participants bought more than 900 MW of CRRs in anticipation of potential northbound congestion on California’s northern boundary,” the ISO’s report says. “None of these rights were held by external load-serving entities, such as Northwest utilities, although they could have obtained the CRRs through the CAISO’s CRR auction or the allocation process that provides CRRs for free to qualifying load-serving entities.”

The report additionally notes that CAISO is the only Western balancing authority in the West “that manages transmission congestion through electricity prices at specific locations in its day-ahead market.”

“Congestion in the Northwest can still result in higher prices, but those costs are not as visible to market participants as they are in the CAISO market,” the ISO said.

In the report, the ISO points out that EDAM “provides additional mechanisms for managing congestion on either side of balancing area borders for participating entities and provides transparency on the distribution of congestion revenues collected through nodal pricing. The EDAM will be able to help Pacific Northwest transmission operators better manage and allocate the costs of congestion on their systems.”

CAISO said it will discuss the report’s findings during a March 11 public meeting.

RTO Insider will provide additional coverage of the report after having more time to delve into its analysis.

A coalition of transmission, utility and consumer advocates on March 6 recommended that FERC incorporate cost management protocols into its final rule on transmission planning and cost allocation (RM21-17).

The group — which includes the Electricity Consumers Resource Council (ELCON), the Large Public Power Council (LPPC), Americans for a Clean Energy Grid (ACEG), the Clean Energy Buyers Association (CEBA) and the National Association of State Utility Consumer Advocates — hosted a webinar to endorse a proposal requiring that transmission providers incorporate cost-benefit reporting mechanisms throughout their projects’ lifecycles.

It urged FERC to mandate that providers periodically file cost allocation reports tracking anticipated project costs against initial projections. Under the proposal, if a provider’s publicly filed report reveals that a project’s costs have either exceeded a predefined threshold percentage of its original projected cost or fallen below an approved benefit-cost ratio, a process administered by an RTO or ISO would be initiated to reconsider the project’s cost allocation to prevent consumers from bearing undue financial burdens.

“Instilling greater transparency and cost discipline in transmission development protects consumers from undue costs and provides assurances that consumers will benefit throughout the life of the project,” ELCON CEO Karen Onaran said in a press release.

John Di Stasio, president of LPPC, said the proposed provisions would ensure that transmission projects approved through the regional planning processes undergo “a cost-benefit analysis not just at the outset, but [also] throughout the life of construction, because at the end of the day, consumers are the ones who bear the cost of new infrastructure, and we want to make sure there is oversight on their behalf.”

The group proposes that FERC’s final rule establish a reconsideration threshold at 25% or more above the projected cost allocation. This reconsideration process would allow project sponsors to justify their cost deviations and present mitigation plans, until construction.

“This rule would require planners to take a long-term look at the changing circumstances and plan for all economic or reliability benefits and adopt some sort of backstop or dispute resolution for cost allocation,” said Christina Hayes, executive director for ACEG.

“We’re no longer just talking about an energy transition, but we’re talking about a grid expansion,” said Bryn Baker, senior director of CEBA. “And this grid expansion means that we cannot just be talking about adding new generation, but we have to talk about moving the cheapest available electrons to where they’re needed.”

The commission issued a Notice of Proposed Rulemaking last year to change how transmission planning and cost allocation processes are conducted to help build out the grid in the long term. The docket has received a barrage of comments, reports and appeals from industry groups, politicians and transmission stakeholders urging that FERC’s final rule should allow for regional flexibility; not hinder ongoing innovation; consider factors related to competition, consumers and transparency; and be issued by year-end, among other recommendations. (See FERC Gets Dueling Competition Studies in Transmission NOPR Docket.)

“Striking a balance between advancing clean energy goals and protecting consumers from unforeseen costs is essential as FERC considers large-scale regional transmission planning,” Di Stasio said.

During the webinar a reporter asked how the group arrived at the 25% reconsideration threshold and if it could unreasonably slow down project approvals.

Di Stasio replied that the group has discussed with FERC how “these protocols could create a barrier” but added that “if it’s clear at the outset and there’s ongoing monitoring and recording, it still gives an opportunity for projects to continue” and “[the threshold] shouldn’t necessarily slow anything down and, in fact, gives us greater confidence in whatever gets approved.”

Hayes added that “this proposal makes sure that we’re very clear-eyed about the costs and benefits as we go through planning and makes sure that, should things go awry, there’s a check in that process.”

The 25% figure is “not necessarily a line drawn hard in the sand,” Baker concluded. “But the point of the entire exercise is to say if costs have increased that much, let’s just have a quick check.”

In its Long-Term Reliability Assessment released March 5, SERC Reliability said active collaboration with registered entities and other stakeholders still is needed to maintain reliability in the face of growing challenges over the next 10 years.

SERC’s LTRA covers the years 2023-2033; the regional entity described it as a “complement” to NERC’s LTRA, released last December, while also reflecting “updates within the SERC region since the release of the NERC report.” (See NERC: Growing Demand, Shifting Supply Mix Add to Reliability Risks.) The report’s conclusions were based on data gathered from SERC’s registered entities and independently verified by the RE.

NERC’s LTRA identified the SERC-Central subregion, which comprises Tennessee and parts of nine other states, as one of two high-risk areas along with MISO — meaning they are more likely to have insufficient supplies to meet demand at some point in the next decade. The SERC report confirms this assessment, noting that demand is projected to “increase faster than the transitioning resource mix grows.”

Data Centers Driving Load Growth

But SERC-Central is not the only subregion where growing demand is an issue.

The RE said load for its region is expected to rise at a compound annual growth rate of 1.2% over the next 10 years, significantly higher than the 0.6% CAGR in last year’s LTRA. (See SERC LTRA Notes Challenges from IBRs, DERs.)

As with last year, the highest growth is projected in SERC’s PJM subregion — comprising parts of North Carolina, Virginia and Kentucky — which the RE attributed to “growing data center load” driving demand to a CAGR of over 5%, more than double the 2.2% CAGR in last year’s report. Businesses’ interest in artificial intelligence and large language models, along with ongoing activity in the cryptocurrency space, are significant contributors to the rise in data center demand.

The LTRA also noted that while SERC is “traditionally … a summer-peaking region,” several subregions are projecting “similar peak demand for both summer and winter months” because of the adoption of electric heating systems over the next decade. Increased use of distributed energy resources like solar panels may help to reduce summer demand growth compared to winter because of increased sunlight in summer.

However, SERC warned that behind-the-meter DERs also complicate the task of load forecasting because grid operators lack visibility into these resources. Electric vehicle charging, home battery systems and state electrification programs also add complexity, the RE said.

Solar, Gas to Replace Coal

The projected load growth load will be happening while major shifts in the grid’s resource mix continue.

SERC said that more than 12% of the active coal generation fleet will retire by 2033, with future energy needs met by nuclear, natural gas and solar resources.

Overall internal capacity for the SERC region at the hour of peak demand is expected to grow from 309.6 GW in 2023 to 324.4 GW in 2033 for summer months, and from 323.1 GW to 327.2 GW for winter months. Solar resources are projected to grow the most for the summer, both in absolute and relative terms, with almost 9.8 GW added, a 67% increase. Solar’s winter share will grow by 1.8 GW, a 25% increase from 2023.

The second-largest projected absolute increase is in natural gas, for which summer capacity is predicted to rise by 9.3 GW, 6% higher than in 2023; winter capacity will rise by 4.3 GW, or 4%. This means gas will remain by far the largest resource in SERC’s footprint, accounting for over half of generation over the assessment period.

SERC observed that the variability of resources being added — including wind and battery systems as well as solar facilities — means that “system planning and operations must focus beyond the peak load hour.” For example, solar generation may be sufficient to meet peak load, but as available sunlight decreases, solar output may be insufficient later in the afternoon when electric demand for air conditioning still is high.

In addition, the possibility of extreme weather throughout the year creates unique vulnerabilities in the region. With natural gas accounting for such a high percentage of generation, utilities must be prepared for disruptions to the gas supply. Operators also will need to reduce the vulnerability of their systems to extreme temperatures.

SERC recommended stakeholders perform sensitivity studies to determine new technologies’ influence on the grid, with regulators and policymakers using “their full suite of tools to manage the pace of retirements and ensure that replacement infrastructure can be timely developed and placed in service.”

For its part, the RE promised to continue studying the impact of extreme weather events such as prolonged cold or hot temperatures, wetter winters and drier summers. It urged reliability coordinators and balancing authorities to focus on “communication and coordination activities” for an effective response to the developing risks to grid reliability.

The Western Area Power Administration’s Desert Southwest Region (DSW) pulled out of the second phase of developing SPP Markets+ after determining it would see few benefits from participating in either Markets+ or CAISO’s Extended Day-Ahead Market, the federal power agency told RTO Insider.

“For our Desert Southwest Region (DSW), the potential benefits of day-ahead market participation for either market are minimal; therefore, DSW has decided to not continue as a funding participant in the Markets+ development at this time,” WAPA said in an email March 5.

The agency said it will continue to monitor developments around both Markets+ and CAISO’s Extended Day-Ahead Market (EDAM).

“More information and a compelling business case would be necessary for the region to proceed with either day-ahead market option,” it said.

DSW operates the Western Area Lower Colorado (WALC) balancing authority in western Arizona and sells federal hydroelectric power and provides transmission service to nearly 70 cities, electric cooperatives, Native American tribes, government agencies and irrigation districts. One of its customers, Arizona Electric Power Cooperative (AEPCO), includes six distribution cooperatives and five public power entities that serve more than 420,000 residential, agriculture and corporate customers in Arizona, California, Nevada and New Mexico.

SPP Vice President of Markets Antoine Lucas informed the Interim Markets+ Independent Panel (IMIP) of DSW’s move March 1 shortly after the RTO received a letter from the agency stating its intent to withdraw from the effort and end its associated funding agreement. The announcement coincided with the IMIP’s approval of the Markets+ tariff, which is headed for a March 25 vote by SPP’s Board of Directors. (See MIP Sends Markets+ Tariff on to SPP Board.)

A WAPA spokesperson said agency officials involved with the matter declined RTO Insider’s request to release the letter. But a Jan. 31 internal slide presentation titled DSW Markets Update provided insight into the agency’s decision-making.

A section of the WAPA presentation appearing under the heading “AEPCO Update” reviews the results of the 2023 study that was commissioned by the Western Markets Exploratory Group (WMEG) and conducted by Environmental+Energy Economics (E3). The study examined potential costs and benefits associated with Western utility membership in Markets+ and EDAM under different scenarios reflecting various footprints in each market.

The 26-member WMEG had asked E3 to limit the scope of the study’s cost-benefit analysis to variable production costs and energy market prices, while not considering potential investment savings from lower capacity needs due to resource and load diversity, the ability to procure resources over a wider geographic area and coordinated regional transmission planning.

“Other market studies have shown those other benefit categories can create two to ten times the impact of production cost savings alone,” E3 cautioned at an Oct. 23 workshop hosted by the Bonneville Power Administration to present the results.

Results from the WMEG study indicated California would be the biggest financial beneficiary of a single day-ahead market covering the entire U.S. portion of the Western Interconnection, with most other entities in the West benefiting more from a two-market outcome. (See Study Shows Uneven Benefits for Calif., Rest of West in Single Market.)

The study showed that, under an “EDAM Bookend” scenario in which EDAM encompasses the West, California entities would save $80 million a year compared with business as usual, while most WMEG entities — including DSW/WALC (which excludes AEPCO) — would spend $20 million more.

Under a “Main Split” scenario, in which EDAM consists of California and PacifiCorp’s balancing authority areas, California would spend $247 million more, while the majority of WMEG entities would save $26 million. But DSW/WALC still would be a net loser in that scenario.

The “AEPCO Update” in the WAPA presentation outlines a handful of key takeaways regarding the WMEG study, offering the view that the study shows “modest” overall differences in production costs between the footprints and saying the “results vary significantly by entity.”

Another takeaway: that “one market is more efficient than two markets,” with two markets requiring additional transmission to be built between the Northwest and Southwest.

Perhaps the most significant conclusion is the view, raised by E3, that the WMEG study “did not consider benefits which can be significantly larger in impact than production cost savings,” including “coordinated generation and transmission planning and investment,” “resource procurement savings” and “reliability improvements during extreme weather or challenging operational conditions.”

The “AEPCO Update” also points out that DSW/WALC incurs losses in all but two WMEG scenarios. The first is the “Alternative Split 1,” in which the Northwest, Colorado and eastern Wyoming participate in Markets+ while the rest of the West joins EDAM. Under that scenario, the agency saves $8.3 million in 2026. “Alternative Split 2” is a variation on that scenario with even lower participation in Markets+. It saves DSW/WALC $4.8 million.

The presentation notes that the benefits in both scenarios result from increased wheeling revenue and net cost savings from California’s surplus solar.

The AEPCO portion of the presentation concludes with a slide labeled “Day-Ahead Market Strategy,” which states that the WMEG study results “are somewhat dated, but they reflect the limitations of DSW hydropower and realities of the current transmission footprint.” The slide also notes the cost and difficulties “of implementation/transition” related to joining a new market and “uncertainty” surrounding “which or whether either option becomes viable and/or more advantageous for DSW.”

“Conclusion is for DSW to wait for the foreseeable future,” the slide says.

EDAM Impact?

DSW’s decision to pull out of Markets+ comes amid an intensifying contest between Markets+ and CAISO’s Extended Day-Ahead Market (EDAM) ahead of the anticipated release of the Bonneville Power Administration’s market “leaning” in April. (See NW Cold Snap Dispute Reflects Divisions over Western Markets.)

DSW’s decision doesn’t exactly spell a victory for EDAM, but it does benefit CAISO by keeping DSW within the ISO’s Western Energy Imbalance Market, which the federal agency entered in 2023. Arizona utilities Arizona Public Service, Salt River Project and Tucson Electric Power all have been key participants in developing Markets+, and industry sources have told RTO Insider the Arizona group, along with the Bonneville Power Administration and Powerex in the Northwest, are leaning toward the SPP market.

It’s difficult to predict how DSW’s decision will affect other Southwest utilities’ choices. The agency operates about 3,100 miles of transmission lines, including the Parker-Davis Project, Intertie Project, Central Arizona Project and ED5-Palo Verde Hub Project — the last of which connects to one of the major electricity trading hubs in the Western U.S.

DSW’s WALC last year got $59.35 million in gross benefits from the WEIM over the three quarters it participated in the market, according to CAISO. Those benefits consist of “cost savings, increased integration of renewable energy, and improved operational efficiencies, including the reduction of the need for real-time flexible reserves,” the ISO says.

The Jan. 15 WAPA presentation shows DSW saved $8.6 million from April to October 2023 compared with the same period in 2022, against CAISO’s net benefits figure of $43.23 million for the first and second quarters of last year.

SPP spokesperson Meghan Sever said the RTO “understands each entity must decide whether participation in a market provides the most benefits for its customers.”

“While we respect any valuable Markets+ participant’s individual decision, SPP believes Markets+ is still a great option for a market that provides financial benefits and enhances electric reliability in the Western Interconnection,” Sever said. “We thank WAPA DSW for their participation in Phase 1 of Markets+ development and hope they will continue to be involved in the Markets+ stakeholder process.”

In its email to RTO Insider, WAPA said it “will remain engaged and assess potential opportunities for both day-ahead initiatives to ensure we are well positioned to continue providing the best service to our customers on a region-by-region basis.”

Targeted electrification could allow decommissioning of up to 10% of gas distribution mains, representing “a promising strategy but not a silver bullet to solve the long-term gas cost challenge,” researchers told the California Energy Commission.

At a Feb. 28 workshop, Energy and Environmental Economics (E3), nonprofit Ava Community Energy and Gridworks presented the results of CEC-funded research on whether pairing gas decommissioning with targeted building electrification — transitioning whole neighborhoods to electric rather than having a mix of services — could provide gas system savings while promoting equity and meeting community needs.

As building electrification advances, gas system costs will spread across fewer customers, leaving renters and low-income homeowners who cannot afford to electrify the most vulnerable, a “major equity concern,” E3 Associate Director Ari Gold-Parker said.

“We think this approach could be part of what we’re calling a ‘managed transition’ to reduce gas system spending and help to manage gas rates in the long term,” he said.

E3 and its partners said their research found 5-10% of gas distribution main miles could be decommissioned to save money over the next 20 years. To be eligible, lines must be “hydraulically feasible” — able to be removed without impacting gas system safety and reliability — such as mains at the end of radial systems. The team also targeted lines with the highest scores for operational risks — those most likely to need replacement within a decade.

“Even though this is a fairly small share of total main miles, these projects still reflect a very important opportunity to avoid a large share of the capital cost that would otherwise be incurred on the gas system during this time period,” Gold-Parker said.

The researchers concluded that combining targeted electrification with gas decommissioning can provide net benefits to the state, electric ratepayers and gas ratepayers. But they said there is a significant funding gap for the upfront costs of electrifying buildings, calling it the “missing money.”

In addition to high upfront costs, other challenges include customer preferences and current policies and regulatory rules, they said.

Identifying Sites

The first step of the research project was to develop a framework for finding potential sites for targeted electrification. From 11 candidate sites, the team proposed three pilot sites in Ava Community Energy’s service territory: East Oakland (an urban single-family, disadvantaged community with 70 gas meters); Oakland-Allendale (a mix of single-family, multifamily, and nonresidential buildings with 110 gas meters) and San Leandro (a suburban single-family disadvantaged community with 190 gas meters). The CEC grant did not include funding for implementation; the project team said in their June interim report that they plan to apply for funding to implement one or more pilot projects.

The team used Pacific Gas and Electric’s gas asset analysis tool to help them find areas that will likely need pipeline replacement. But the team said it needs a longer-term planning process to identify sites with enough lead time to implement electrification. Gas utilities identify these projects on the timeline of the general four-year rate case, but the researchers said a 10-year planning process was more appropriate.

Next, the team performed site-based benefit-cost analyses.

To address the “missing money” for the upfront costs of electrifying buildings, the team suggested repurposing savings to fund electrification, though that option could reduce long-term savings to gas ratepayers. “Even though this approach works on paper and might be valuable in the near-term, in the long term this approach would really undermine the potential for gas decommissioning projects to support the key equity objective of providing long-term cost reductions for gas ratepayers,” Gold-Parker said.

The greatest financial benefit will come from avoiding pipeline replacements. The study found that gas decommissioning will be the most cost-effective in less dense neighborhoods due to the cost of electrification. “While two gas decommissioning projects with the same length of gas mains will have the same gas pipeline savings, the costs of implementing a gas decommissioning project would be higher in a site with more dense development (i.e., with more customers to electrify),” the researchers said in theirbenefit-cost analysis.

Moving `at the Speed of Trust’

Ava Community Energy, which sells renewable energy in the East Bay, led efforts to engage its communities, including partnering with a community-based organization and the city of Oakland to host home energy resource fairs.

While the resource fairs provided educational opportunities for residents unfamiliar with electrification, Allison Lopez, senior analyst at Ava Community Energy, said attendance was very low.

“This could be for various reasons. Perhaps even the topic of electrification or home energy savings is a bit too foreign or novel to boost interest,” Lopez said. “While we think events like this have great potential, we found it very difficult to scale awareness about this project or gain feedback through this channel.”

Ava also partnered with Environmental Justice Solutions to assemble paid focus groups for residents in the proposed pilot sites. While attendance again was low, Lopez said they received good feedback.

Focus group participants expressed concern over the cost of electrification, increased electric bills and a lack of familiarity with electric equipment. Lopez said Ava is prioritizing affordability, working on improving communication and education, and building trust.

“We heard repeatedly that communities move at the speed of trust,” Lopez said. “It really takes a lot of time to build and maintain trust.”

For the plan to work, all pilot project site residents will need to consent to electrification, making implementation “extremely challenging,” Lopez said.

Recommendations

In addition to a longer-term capital project planning process and funding to address the upfront costs of electrification, the researchers called for better data and planning tools for site selection, and changes to utilities’ “obligation to serve.”

“In the current regulatory paradigm, utilities contend that 100% customer opt-in is required to decommission gas infrastructure. This requirement means large sites with many customers may prove difficult or impossible to implement gas decommissioning and even small sites may require substantial financial incentives to achieve 100% opt-in,” the researchers said. “Any gas system decommissioning projects pursued in the next few years will need to consider ways to work within the obligation to serve. In the longer term, California will need to evolve the obligation to serve to ensure it does not become a barrier to the state’s decarbonization goals.”

The researchers said the state and its utilities need a long-term plan for gas infrastructure aligned with the state’s climate goals. They noted the California Public Utilities Commission’s Long-Term Gas Planning proceeding “is entering a new phase focused on long-term planning for gas system decarbonization.”

“Clear plans and targets could provide key regulatory support for alternatives to gas pipeline replacement,” they said. “Long-term planning should consider the role of targeted electrification and gas decommissioning as part of a portfolio of measures to reduce gas system investments and mitigate long-term cost pressures.”

Next Steps

Ava is developing a deployment plan proposing a phased approach over a 10-year span beginning with community engagement.

“We recognize that this approach will take a lot of time and there will definitely be less certainty about whether customers will ultimately decide to remove gas service,” Lopez said. “But we believe this approach is in line with community feedback that we’ve received.”

The researchers noted their project considered two “important but distinct” equity goals: promoting electrification in disadvantaged communities and maximizing gas system cost savings.

“We believe the state may achieve better outcomes by developing and promoting different programs for these two goals,” they said.

Speakers at the ISO-NE Consumer Liaison Group (CLG) meeting March 6 stressed the importance of proactive efforts to unlock the potential of demand response and peak shifting, as electrification is projected to double New England’s peak loads in coming decades.

The CLG met in Portland for its first quarterly meeting of 2024 and featured discussions on the benefits of widescale load shifting, along with the barriers that prevent the realization of those benefits.

Andrew Landry, deputy public advocate for Maine, called demand response “an important tool that we need to take advantage of to the maximum extent.”

Landry cited ISO-NE’s projection of a 57-GW peak load in 2050, as well as the RTO’s finding that limiting this peak to 51 GW would save about $9 billion in avoided transmission upgrades.

“If we can find ways to reduce the demand, even with the amount of electrification that’s going on, it would reduce the need for transmission,” Landry said.

He highlighted FERC data showing demand response makes up a significantly lower percent of total installed capacity for ISO-NE compared to CAISO, MISO, NYISO and PJM.

Eric Johnson of ISO-NE echoed the importance of reducing demand but added that “there’s a lot of infrastructure challenges that need to be resolved.” He noted that the FERC data does not include the region’s significant energy efficiency gains. (Report: Many US Utilities not Delivering on Energy Efficiency.)

Jill Powers of CAISO presented to the CLG about load-shifting efforts in California, where demand response surpasses all other RTOs by percent of installed capacity. Powers said demand response programs have helped the state avoid rolling blackouts during grid stress events and emphasized the role of both in-market and out-of-market mechanisms to engage a wide range of customers.

“It’s not just at the wholesale level that we need to be collaborating” to unlock demand flexibility, Power said.

She outlined two out-of-market programs in California that incentivize demand reductions during peak hours: the Demand Side Grid Support Program and the Emergency Load Reduction Program. The programs are not administered by CAISO, but they do respond to real-time and day-ahead signals from CAISO.

“We believe that demand can provide responses similar to a flexible resource, helping to balance the grid,” she said.

The CLG also featured a panel of New England stakeholders, who focused on the role of ISO-NE in increasing demand response efforts within the region.

Doug Hurley, vice president of policy at Icetec Energy Services, stressed that peak demand reductions from one electricity customer on the grid provides benefits to all customers by reducing the clearing price, limiting emissions associated with peaker plants, and ultimately reducing the need for new transmission investments.

Hurley said the region needs to align state demand programs and retail rate design with optimal times to charge and discharge batteries — such as at night or midday when cheap solar power is available — to better balance load and reduce emissions.

He also called out ISO-NE’s compliance proposal for Order 2222 as a “missed opportunity” to increase the participation of flexible demand resources in its markets, saying the “compliance to date will not achieve any participation.” (See FERC Accepts ISO-NE Order 2222 Compliance Filing.)

Ian Burnes of Efficiency Maine Trust agreed with Hurley’s criticism of ISO-NE’s Order 2222 compliance and called on ISO-NE to help ease the barriers for small resources to participate as demand response resources.

“We have a lot of work to do here,” Burnes said. “It’s very, very difficult to aggregate lots of small assets and have them participate.”

Burnes added that significant investments in physical infrastructure to enable residential customers to receive and respond to incentives to shift their demand will be necessary.

“I do not want to trivialize that investment — it is going to be hard,” Burnes said. “I think that needs to be our focus.”