NYISO on Feb. 13 defended its proposal to set a 10-kW minimum requirement for distributed energy resources to participate in an aggregation in response to a deficiency letter from FERC, which asked it to justify the figure (ER23-2040).

The ISO argues the rule would prevent staff from being overwhelmed by initial program participation requests. Renewable energy advocates have protested, arguing the rule would discriminate against smaller aggregations. (See Clean Energy Groups Protest NYISO DER Proposal.)

NYISO explained the 10-kW threshold “is based on its two decades of experience administering” the existing special-case resource (SCR) and emergency demand response programs (EDRP), which it views to be the “participation models closet in kind to the DER and aggregation model.”

The ISO said it settled on the 10-kW requirement because it believes that, like the SCR program and EDRP, managing DER aggregations would include “a significant amount of manual work” and want staff to become accustomed to it.

It also reasoned the rule would impact mostly residential facilities employing demand-reduction technologies, such as energy storage resources or smart home products, and the 172,434 rooftop solar installations in New York with capacities under 10 kW.

These smaller resources, NYISO claimed, are minor contributors to the ISO’s markets and might not even opt to participate in the DER aggregation model, favoring other programs meant for small facilities, such as the SCR.

“The question is whether the delayed implementation and costs associated with building the infrastructure to enable sub-10-kW resource participation in the DER and aggregation participation model is justifiable in light of their expected contribution to the Bulk Electric System,” it said.

This is the second time NYISO has responded to a deficiency notice to its DER participation model proposed in June; much of its response reiterated arguments it made the first time, in October. FERC had requested more details about how the ISO settled on the 10-kW figure.

The ISO argued that any further delays, such as FERC rejecting its proposal, would mean it would need to “undertake a significant multiyear process to develop new market rules” addressing the commission’s concerns and potentially “delay the transition of over 400 MW” of demand-side resources capable of participating in the DER aggregation model.

NYISO said it “is ready to implement the model immediately upon commission acceptance of the tariff revisions proposed,” adding that “seven entities” already “submitted aggregator registration materials” and three have completed their registration.

The ISO urged FERC to act on the proposed revisions by April 15, as it is prepared to roll out its DER aggregation participation model April 16.

After a year in which unusually mild weather depressed electric use, Southern Co. is forecasting 5 to 7% annual earnings growth thanks to a robust economy in Georgia.

The company faced “unprecedented headwinds” in 2023 but achieved numerous milestones during “an exceptional year,” CEO Chris Womack said in announcing the company’s fourth-quarter and full-year earnings Feb. 15.

Among the accomplishments Womack highlighted in his presentation was the long-delayed completion of Unit 3 at the Vogtle nuclear power plant near Waynesboro, Ga., which entered commercial operation on July 31 more than seven years late and $17 billion over budget.

The CEO pointed out that Southern subsidiary Georgia Power reached an agreement with the state’s Public Service Commission last August to resolve all remaining prudency issues at Unit 3 and Unit 4. Under the agreement, the recovery of capital construction costs from ratepayers for both units is capped at $7.6 billion, leaving the remaining costs — estimated at around $2.6 billion — to be paid by Georgia Power. The PSC approved the agreement in December.

Womack said Southern is making “meaningful progress” toward completion on Unit 4, with initial criticality achieved Feb. 14, marking the start of the nuclear chain reaction inside the reactor. The company expects the final unit to be in service by April.

Along with the progress on Vogtle, Womack mentioned the completion of Unit 8 at Alabama Power’s Plant Barry, a 727-MW combined cycle unit that began operating Nov. 1, and the acquisition of two solar projects that will provide 350 MW when finished.

The company’s operating revenue for the three months ending in December came to $6 billion, compared to $7 billion for the same period in 2022. Net income for the period — excluding losses on plants under construction, losses on capital investments and tax impacts — stood at $700 million, compared to $285 million for the same period the year before.

Operating revenue for the full year was $25.3 billion, down from $29.3 billion in 2022; however, net income for the full year — excluding the same elements — was $4 billion, up from $3.9 billion the previous year.

Southern reported adjusted earnings per share of 64 cents for the quarter, up from 26 cents for the same period in 2022, with adjusted earnings per share for the whole year rising from $3.60 to $3.65, which CFO Dan Tucker noted was “at the very top of our 2023 guidance range.” He cited “higher utility revenues and lower nonfuel O&M [operations and maintenance] costs and income taxes.”

Tucker said the company’s electric revenue was reduced because 2023 was “the mildest year in our history for our electric service territories.” Electric retail sales, adjusted for weather, were down 0.4% from 2022, with reduced residential and industrial usage (down 0.5% and 1.9% respectively) balanced by strong commercial sales growth of 1.3%.

The decline in industrial sales was primarily due to “continued slowing in [the] housing and construction-related sectors, as well as lower sales to chemical companies due to outages and long-planned plant closures,” Tucker said. However, he pointed out that the population in Southern’s electric territories grew by 0.8% between July 2022 and July 2023, with Georgia adding more than 26,500 new jobs last year. In 2022, the state added 45,600 jobs, more than 15,000 of them from auto factories being built by Hyundai and EV truck maker Rivian.

Based on these trends, Southern is setting an adjusted earnings per share guidance range for 2024 of $3.95 to $4.05, with long-term adjusted EPS growth rate of 5-7%, Tucker said. These figures assume Vogtle Unit 4 is completed on schedule.

Despite the challenges, Womack said Southern’s electric and gas businesses “continued to excel at the fundamentals and started this year strong,” noting that the company operated reliably during January’s winter storm even as “electricity demands reached all-time winter peaks.”

NYISO’s Operating Committee on Feb. 15 voted to approve the results from the Expedited Deliverability Study (EDS) 2023-01 report that included 16 projects, two of which were found to be undeliverable.

The 14 projects found to be deliverable have until Feb. 22 to accept or reject their deliverable megawatts as determined by the EDS report. Developers that fail to notify NYISO about their decision will be deemed nonacceptances.

“Should every developer accept their deliverable megawatts, then EDS 2023-01 will be deemed complete,” said NYISO Manager of Facility Studies Wenjin Yan.

The EDS process fast-tracks projects seeking capacity resource interconnection service (CRIS) rights by assessing whether the project is deliverable as proposed, without the need for system deliverability upgrades. (See “Class Year & Expedited Deliverability Study Update,” NYISO to Ask FERC for Order 2023 Compliance Extension.)

The two projects deemed not fully deliverable, Q1039 Morris Solar (20 MW) and Q1212 Roosevelt Solar (19.9 MW), now must decide whether to await the next EDS cycle or join the upcoming transitional cluster study as a CRIS-only request to identify what upgrades are required to become deliverable. Projects looking to participate in the cluster study, however, must complete a small generator facility study.

NYISO will report to the developers about each other’s decisions, sharing whether projects chose to not proceed. Should one or more developers provide a nonacceptance notice after the initial decision period, then the ISO will issue updated study results for the EDS projects remaining that reflect the impact of any projects withdrawn.

The study is expected to be completed Feb. 22, but if a non-acceptance is issued, a revised EDS report will be issued March 7.

NYC PPTN

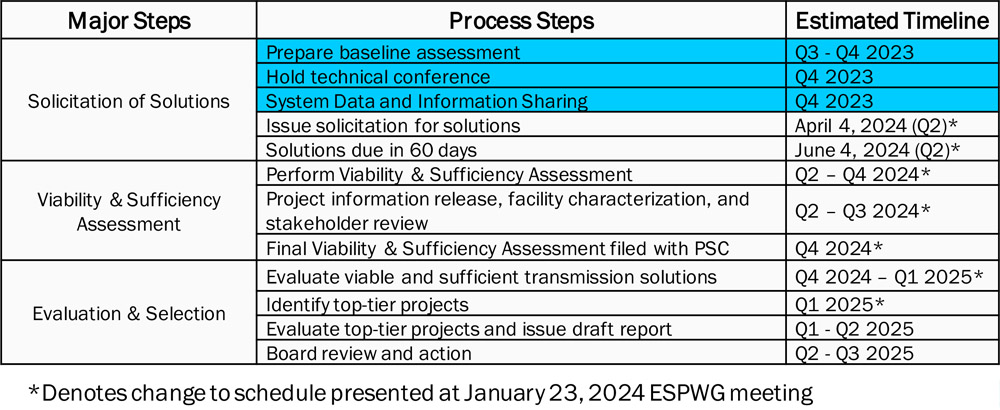

NYISO told the committee the New York City Public Policy Transmission Needs (PPTN) solicitation window will open April 4.

Developers’ proposed solutions are due by June 4, with NYISO committing to provide technical documents to developers prior to issuing the solicitation.

NYC PPTN schedule with solicitation window opening April 4 | NYISO

The New York Public Service Commission initiated the PPTN in June 2023, with the aim to both facilitate the delivery of 6,000 MW of offshore wind power generated off the Long Island coast to New York City and help meet the state’s Climate Leadership and Community Protection Act mandate to develop at least 9,000 MW of OSW by 2035 (22-E-0633).

Doreen Saia, an attorney with Greenberg Traurig, asked if NYISO was aware of the two Feb. 14 filings from the state’s Department of Public Service, which requested the ISO clarify how recent contract terminations from two OSW projects, Beacon Wind and Empire Wind 2, would be reflected in the PPTN and shared questions the department has received from stakeholders concerned about the terminations. (See Empire Wind 2 Cancels OSW Agreement with New York.)

Saia also wanted to know if the cancellations would result in NYISO adjusting the PPTN’s base case, power flow cases, modeling results, timeline or technical guidance documents.

Supriya Tawde, manager of transmission integration at NYISO, responded that the ISO will be “sharing updates to the power flow cases” next week and then reviewing “our procedures to make a determination if any other changes need to be made” based on these developments.

January Operations

Aaron Markham, NYISO vice president of operations, shared the January operations report with the OC, saying, “the above-average temperatures we’ve been experiencing came to an end” and resulted in a winter season peak load of 22,754 MW, which was roughly 94% of the baseline forecast for winter.

The cold snap led to increased natural gas prices, which in turn drove up wholesale energy market prices and contributed to slightly higher local reliability costs.

External ICAP Rights

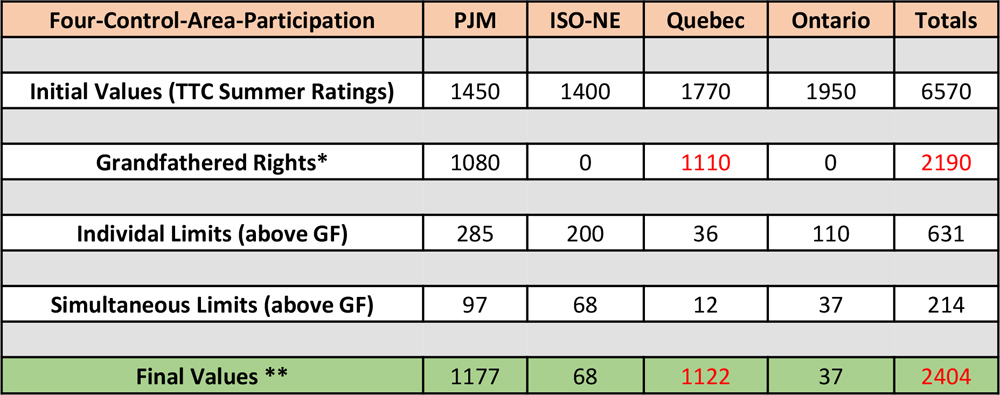

NYISO’s Business Issues Committee on Feb. 14 voted to approve revisions to the Installed Capacity Manual that update the maximum amount of import capacity allowed from neighboring control areas for the 2024/25 capability year.

The ISO can import 214 MW above grandfathered rights from its neighboring control areas this coming capability year, with 97 MW available from PJM, 68 MW from ISO-NE, 37 MW from Ontario and 12 MW from Quebec.

2024/25 import rights for NYISO’s neighboring control areas | NYISO

The revised figures represent a 10-MW decrease from the 2023/24 capability year, with PJM’s and Quebec’s limits increasing by 39 MW and 1 MW, respectively, and Ontario’s and ISO-NE’s decreasing by 43 MW and 7 MW, respectively.

Including existing transmission capacity for native load, and other grandfathered rights, the ISO’s biggest import sources are PJM (1,177 MW) and Quebec (1,122 MW).

The summer capability period auction will be held no later than 30 days prior to the start of the period on May 1.

The West-Wide Governance Pathways Initiative is advancing on its $570,000 funding target.

And its members also are wading deeper into one of the key subjects it was conceived to address: how to work around CAISO’s state-run governance model to create the framework for an independent Western RTO that pointedly includes the ISO and builds on its Extended Day-Ahead Market (EDAM).

Members of the initiative’s Launch Committee addressed both topics during a virtual monthly update Feb. 16.

“We are making really good progress [and] want to acknowledge and thank all of those entities who have pledged funding or committed funding in one way to support the launch framework,” committee Co-chair Kathleen Staks, executive director of Western Freedom, said during the update.

The Pathways Initiative has reached around “$300,000-ish” in pledges and is “still in fundraising mode,” Staks said.

“So, if you have not yet been hit up, or you have not asked, consider yourselves solicited for funding,” she told meeting participants.

Staks also noted the Pathways Initiative had hired Seattle-based energy consulting company Utilicast to provide project management and meeting coordination, relieving the Regulatory Assistance Project of some of its initial responsibilities as a facilitator of the effort.

Utilicast’s Sarah Davis and independent consultant Jessica Singh will become the Pathways Initiative’s key points of contact for stakeholders, as noted on the group’s landing page on the Western Interstate Energy Board website, Staks said.

‘Stepwise’ Governance Approach

Pathways Initiative stakeholders have signaled “general support” for a “stepwise” approach to addressing the issue of CAISO’s state-run governance, Northwest & Intermountain Power Producers Coalition Executive Director Spencer Gray said during the call.

Gray is co-chair of the Launch Committee’s Priority Functions and Scope Working Group, which is driving the legal analysis around ISO governance.

Under the stepwise approach, the committee would take the first step of exploring how far “a more autonomous [CAISO] governance option could be pushed” under existing California law. (See Western RTO Initiative Outlines Governance Options.)

“We’re still working with [legal] counsel to figure out where that boundary is, where it seems obvious that state law precludes a more autonomous option, or the litigation risk of a more autonomous option becomes unreasonably high,” Gray said.

The next step would seek to determine what legislation would be needed to provide the ISO with more autonomy.

“The overall feedback on a stepwise approach is it would be helpful to push the ball further, without having the assumption that legislation would pass in California, and then also envision what is a durable governance structure that could be put into place with some continuity from what we would scope from step one,” Gray said.

Gray said his group also is examining the processes used by different RTOs in the U.S. to identify potential models for the Western effort.

Research has focused specifically on governance structures that allow for dual filings with FERC under Section 205 of the Federal Power Act. He said the “strongest precedent” for that model is in New England, where ISO-NE and the NEPOOL stakeholder group operate under a “jump ball” provision that gives both organizations equal rights to file competing ISO-NE tariff provisions with FERC when the two organizations fail to agree on rule changes.

“A fruitful area for us to explore: How did that get designed in the beginning in New England, and what should we think about ways to structure dual-filing opportunities in this context that would be consistent with what FERC’s found in New England?” Gray said.

Gray pointed out that the objective of having a dual-filing option to resolve disputes is to avoid triggering it and instead compel both parties to reach a compromise ahead of a FERC filing.

Gray’s group is additionally working to address the issue of identifying when Pathways Initiative backers would seek to trigger any governance changes outlined in the first part of the stepwise process.

Gray said the group is trying to avoid making changes to the joint authority structure shared between CAISO’s Board of Governors and the WEIM’s Governing Body “without any indication that there’s actually a critical mass of entities interested in EDAM.”

The Launch Committee’s incremental approach to building a governance framework is rooted in the fact that Western transmission owners are not yet clamoring for deeper cooperation than a day-ahead market, Gray said.

“There are some utilities who have publicly expressed interest in doing so; there are a couple state mandates in the West about utilities joining RTOs of some form,” he said. “But the reality we’re facing is a really heterogeneous interest and public expression of interest in steps beyond EDAM, and that fundamentally affects the design of the ladder steps of what we’re imagining.”

Gray said his group plans to offer “public-facing” legal analysis by the end of March, followed by a substantive report back to stakeholders by mid-April, in time to report findings at the spring joint meeting of the Committee on Regional Electric Power Cooperation and Western Interconnection Regional Advisory Body to be held in Denver April 24-26.

ERCOT stakeholders last week agreed with staff’s position to continue tabling a rule change that would address reliability concerns with inverter-based resources (IBRs) while both sides work on settlement discussions in an attempt to compromise.

The Technical Advisory Committee had agreed to move up its February meeting by a week to send a timely endorsement to ERCOT’s Board of Directors before the latter’s Feb. 27 meeting.

That the rescheduled meeting fell on Valentine’s Day was not lost on its participants. A bowl of “metaphorical” candy, printed with acronyms specific to the discussion, was set out for members.

TAC celebrated Valentine’s Day with special candy. | Caitlin Smith via X

“My only question is, [who] do I send the bill to for the bouquet of flowers I had to buy my wife for being here today?” Engie North America’s Bob Helton jokingly asked.

Eric Goff, speaking for the joint commentators negotiating with ERCOT staff, said those he represented were not opposed to keeping the nodal operating guide revision request (NOGRR245) on the table.

“We believe that we’re getting through productive dialogue with ERCOT,” he said. “There are some outstanding issues that will take some time to resolve, but I’m feeling cautiously hopeful … that we will be able to give something for the March TAC [meeting].”

ERCOT’s Stephen Solis agreed and apologized for not meeting the timeline.

“We’re not quite there yet,” he said. “We cleared up some misunderstanding, I think, and there are some core issues that we’re still working on where we stand apart and trying to find perhaps more creative ways of addressing that.”

The grid operator says the prevalence of IBRs on ERCOT’s system has increased the likelihood of potential instability issues, such as the recent Odessa disturbances. They say the issues are only going to increase along with the continued growth of solar and wind resources. (See NERC Repeats IBR Warnings After Second Odessa Event.)

ERCOT says the NOGRR would improve the clarity and specificity of IBRs’ voltage ride-through requirements. The measure would align the grid operator’s rules with NERC reliability guidelines and the most relevant parts of the Institute of Electrical and Electronics Engineers standard for IBRs interconnecting with the grid. (See ERCOT Technical Advisory Committee Briefs: Jan. 24, 2024.)

Vistra’s Katie Rich is serving as an independent arbiter during the settlement discussions, which Goff said could take either of two directions.

“One, we have a common agreement on language, which would be great. The other is ERCOT would file comments, we would file responsive comments, and Katie would tell us the difference between the two,” he said. “We’ll see which one we get to.”

TAC will meet twice before the board’s April 23 meeting.

NPRR1186 Goes to Board

TAC did not take up a protocol change (NPRR1186) regulating energy storage resources (ESRs) that was remanded back to ERCOT last month by the Public Utility Commission. (See Texas PUC Sends ESR Change back to ERCOT.)

The grid operator’s staff said that as the PUC’s directive ”seems straightforward,” they recommended the Board of Directors adopt the commission’s recommendations “without formally requesting additional input from the [TAC] or other stakeholder bodies.”

“The board’s authority to decide this question without soliciting stakeholder feedback is consistent with the governing statute,” staff said, noting stakeholders always can submit a comment on the NPRR for the board’s consideration.

The rule change sets a one-hour state of charge (SOC) for ESRs participating in two ancillary services (ERCOT contingency reserve service and non-spinning reserve). It also includes penalties of up to $25,000 per violation.

The PUC’s remand included “suggested modifications” to remove the SOC compliance requirements and other minor clarifications.

ERCOT also is asking the board to provide direction on NPRR1209, a directive from the directors, as NPRR1186 ran into trouble and has been tabled. The change would consider an SOC insufficiency by any ESR carrying an ancillary service resource responsibility to be a “failed quantity” that would result in a clawback of AS revenues.

Both measures are seen as stopgaps until ERCOT deploys real-time co-optimization, targeted for the latter half of 2026.

The ISO had 3.3 GW of ESRs on its system in June. It expects to have 9.5 GW of ESRs energized by October.

TAC: More Info on Budget

Staff’s two-slide presentation on the budgeted system administration fee’s forecasted adequacy for 2025 — “currently forecast to be adequate” and requiring no changes — led to a request from TAC for more background.

“It wouldn’t hurt to have maybe a few slides that actually show us the actual budget itself and kind of where we’re trending and what we’re spending the money on,” Reliant Energy Retail Services’ Bill Barnes said. “Some background: ‘Well, why is it adequate?’”

At TAC’s request during the 2016-2017 budget process, ERCOT provides stakeholders advance notice of any future administrative fee rate increases. The board in December approved the fee and the ISO’s budget for 2024-25 after the PUC trimmed both; the admin fee was cut from 71 cents/MWh to 63 cents/MWh, up from the previous 55.5 cents/MWh. (See “Revised Budget Passes,” ERCOT Board of Directors Briefs: Dec. 19, 2023.)

Controller Richard Schaal promised “a couple” of extra slides to provide more information.

8 Revisions on Combined Ballot

TAC’s unanimously approved combined ballot of voting items endorsed Rich as chair of the Reliability and Operations Subcommittee. Rich stepped aside temporarily in January after a job change.

The combo ballot also included four NPRRs, a NOGRR and a load planning guide revision request (LPGRR), and two changes to the settlement metering operating guide (SMOGRRs) that, if approved by the board, would:

NPRR1193: Change the ERCOT-polled settlement (EPS) design-proposal form’s referenced location when it moves from the other binding document (OBD) list into the SMOG.

NPRR1199: Revise the protocols to add definitions related to the Lone Star Infrastructure Protection Act (LIPA), a 2021 law that prohibits Texas businesses and governments from contracting with entities owned or controlled by individuals from China, Russia, North Korea or Iran if the contracting relates to “critical infrastructure.” The measure also adds language reflecting ERCOT’s statutory authorization to immediately suspend or terminate a market participant’s registration or access if the ISO has a reasonable suspicion that the entity meets any of the LIPA’s criteria, among other revisions.

NPRR1210: Change the frequency of the next-start resource and the load-carrying tests from every five years to every four calendar years.

NPRR1213: Amend requirements for distribution generation resources (DGRs) and distribution energy storage resources (DESRs) seeking qualification to provide ERCOT Contingency Reserve Service (ECRS). The NPRR also modifies requirements for ancillary service self-arrangement and ancillary service trades for DGRs and DESRs that provide non-spinning reserve on circuits subject to load shed.

LPGRR074: Align specific term language in the profile decision tree “definitions” worksheet with profile segment language that was added to the “segment assignment” worksheet with the Public Utility Commission’s 2022 approval of LPGRR069.

NOGRR261: Incorporate the OBD “Procedure for Calculating Responsive Reserve (RRS) Limits for Individual Resources” into the nodal operating guide.

SMOGRR027: Move the EPS metering design proposal from the OBD list into the SMOG, standardizing the approval process, and amend the design proposal form to require more information identifying any and all distribution service providers that have the right to serve a project.

SMOGRR030: Move the EPS metering facility temporary exemption request application form from the OBD list into the SMOG to standardize the approval process.

FERC on Feb. 16 approved Vistra Energy’s deal to buy Energy Harbor, which it wants largely for its four nuclear plants and retail business, for $3 billion plus paying off $430 million of debt (EC23-74). The commission required divestment of two of Vistra’s fossil plants in PJM.

Vistra plans to launch a new subsidiary combining its clean energy generation and retail business called “Vistra Vision” of which 15% will be owned by Energy Harbor shareholders, while spinning off its natural gas and coal units into a separate subsidiary called “Vistra Tradition.”

Energy Harbor is the competitive generation and retail business spun off from FirstEnergy several years ago. It owns three nuclear plants: Beaver Valley Power Station at 1,969 MW, the Davis-Besse Plant at 962 MW and the Perry Nuclear Power Plant at 1,302 MW.

Energy Harbor also owns some fossil plants, and Vistra already owns generation in PJM. The merging firms argued their impact on competition should be measured against the whole RTO, while PJM’s Independent Market Monitor, the U.S. Department of Justice’s Antitrust Division and the Ohio Consumers Counsel all argued FERC needed to consider smaller submarkets.

Both Energy Harbor and Vistra own generation in the American Transmission System Inc. (ATSI) zone, so Vistra agreed to sell off its 369-MW Richland natural gas peaking plant and its 16-MW Stryker oil plant to end concerns over an excess of power in that submarket of PJM.

The sale of those plants “obviates the need” for FERC to determine any submarkets relevant to the transaction so it focused on its impact on PJM as a whole, the order said.

“After the proposed transaction closes and after completing the divestiture of Richland-Stryker, the Davis-Besse and Perry generating units, currently owned by Energy Harbor, will comprise the only units owned by Vistra in the ATSI transmission zone,” FERC said. “Furthermore, as discussed below, Vistra must sell Richland-Stryker to a buyer that will not fail the horizontal competitive analysis screens, including the delivered price test, for the PJM market or any relevant submarket, post-transaction.”

FERC was not convinced the deal would impact any other submarkets, saying they failed to show any consistent price separation caused by transmission constraints that would indicate a submarket under commission precedent. The commission found the deal would not impact the whole of PJM either, and declined to adopt behavioral requirements suggested by the Monitor.

“The PJM IMM relies on perceived existing limitations in PJM’s market power mitigation as the basis for proposing additional behavioral mitigation,” the order said. “These arguments are directed at the effectiveness of the PJM markets and mitigation measures as a general matter.”

FERC declined to deal with such general issues in this merger case, saying it is not the appropriate venue for that.

The IMM also used a different analysis than what FERC employs in merger reviews to argue the combined firm would have market power in PJM, especially in local markets. DOJ’s Antitrust Division also wanted FERC to use a “supply curve” analysis to review the deal.

“The commission’s regulations do not require a supply curve analysis, and applicants have provided a horizontal market power analysis, including three delivered price tests, consistent with our requirements,” FERC said. “Moreover, the divestiture commitment appears to alleviate DOJ Antitrust Division’s specific concern about the proposed transaction given that the divestiture of Richland-Stryker eliminates Vistra’s ‘ability’ to engage in strategic withholding using that facility.”

The OCC and the Northeast Ohio Energy Council argued FERC should examine the deal’s impact on Ohio’s retail energy market as it will combine two of its largest firms. While FERC lacks explicit authority over the retail power market, the Ohio PUC is unable to review the merger and its impacts on the market, the two said.

The federal regulator’s policy is to review the impact on retail competition whenever a state regulator asks it to. Because the PUC made no such request, FERC declined to examine the deal’s retail market impacts.

The Ohio Energy Advocate, which was set up to represent the interest of the state’s energy consumers at FERC and before other federal regulators, did file a request to review the impact on retail markets, but the commission said it does not count as a state regulator.

State regulators in SPP’s Markets+ footprint have approved tariff language designed to address a “gap” in the accuracy of information to be shared with the Market Monitor under FERC’s duty-of-candor requirements.

Weeks of discussion between regulators, SPP’s Market Monitoring Unit, and SPP and western utility legal staff resulted in the Markets+ State Commission’s endorsement of a paragraph during its regular monthly conference call Feb. 16.

Nebraska abstained from the vote.

The proposed tariff language would require market participants to “exercise due diligence and good utility practice” in providing material information when responding to the MMU’s written request for data and information. The MMU would provide a “reasonable amount of time” for utilities to deliver the requested information, depending on the amount of information.

If the market participant determines there is an error in its response, it would have to “promptly” notify the MMU and work to correct the mistake.

Questioned as to why the language is necessary, Keith Collins, vice president of market monitoring at SPP, said the MMU has encountered several instances within the RTO’s current footprint of entities either ignoring the monitor’s request or submitting incorrect action.

“This does happen, unfortunately,” he said, noting the MMU based several hypothetical examples shared during deliberations over the language on those circumstances.

“We feel that this particular language will solve that gap that we’ve identified with those examples,” Collins added.

“Given what we’ve seen in the West, I just think there’s some real scar tissue about market manipulation,” said MSC Chair Eric Blank, who also chairs the Colorado Public Utilities Commission. “This is just common-sense protection that it seems the lawyers for SPP and for the market participants have agreed to.”

Western commissioners brought the issue up during the Markets+ Participant Executive Committee meeting in January, requesting a clear definition of the participant obligation gap. (See “MMU, MSC to Collaborate,” SPP Markets+ Participants Executive Committee Briefs: Jan. 23-24, 2024.)

A 2022 FERC Notice of Proposed Rulemaking related to “duty of candor” would require all entities communicating with the commission or other organizations — e.g., the MMU — about FERC matters to provide “accurate and factual information” (RM22-20). (See FERC NOPRs Would Require ‘Candor,’ Improved Accounting for Renewables.)

The language will be brought forward for stakeholder approval during MPEC’s virtual meeting Feb. 20.

Consolidated Edison last week reported its plan to invest nearly $20 billion over the next four years in transmission infrastructure as part of its Reliable Clean City initiative and to mitigate climate vulnerabilities.

The New York-based utility, which serves parts of New Jersey via Orange & Rockland (O&R) Utilities, made significant strides in the past year with the Clean City project, completing several sections and receiving state authorization for further upgrades to the six-mile-long Queens-based underground transmission line. It also was approved to start its $810 million Brooklyn-based interconnection hub for offshore wind power. (See $1.2B Con Edison Clean Energy Upgrade Approved.)

“Clean energy is the future of our industry, and we are making strategic investments to build a grid capable of carrying that clean energy and protecting our infrastructure from climate change while maintaining our world-class reliability,” said ConEd CEO Tim Cawley in a statement.

ConEd’s subsidiaries, Consolidated Edison Co. of New York (CECONY) and O&R, submitted plans to the state’s Public Service Commission (PSC) to invest $1.3 billion over five years to prepare for climate change (22-E-0222). They also proposed investments of about $2.82 billion in heat pump programs (18-M-0084) and obtained approval to increase their electric vehicle implementation budgets to nearly $450 million (18-E-0138).

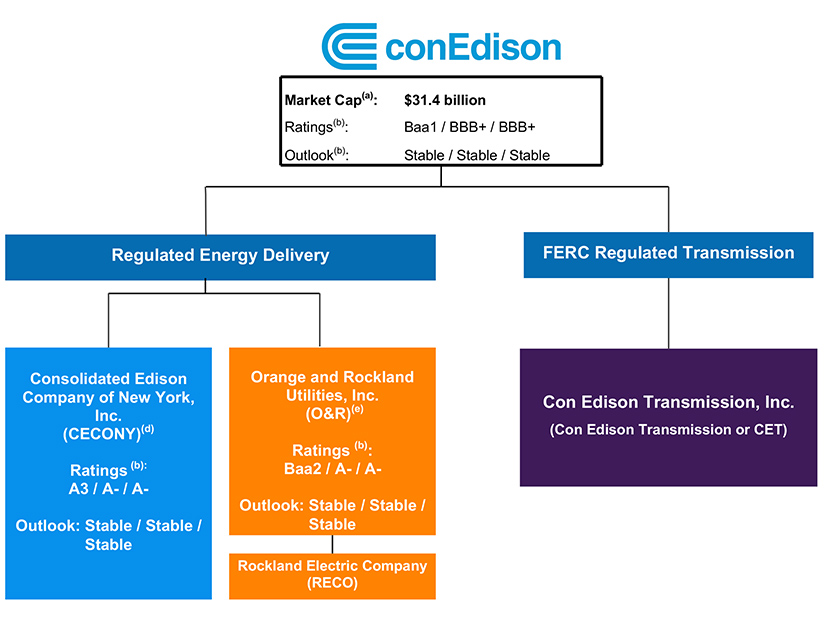

Con Edison’s corporate structure and ratings | Con Edison

The subsidiaries submitted utility thermal energy network pilot proposals totaling $289 million but await PSC approval (22-M-0429).

ConEd plans to fund these investments by issuing $3.25 billion of long-term debt in 2024 and an additional $1 billion in 2025, with $6 billion more in long-term debt expected through 2026 and 2028 at CECONY and O&R.

“Con Edison closed the year with no long-term debt at the parent company, due to the strategic sale of our former subsidiary, the Clean Energy Businesses,” said ConEd CFO Robert Hoglund.

ConEd sold off CEB, consisting of 3,300 MW of renewable energy projects, to RWE Renewables America in 2022 for $6.8 billion and continues to realize financial benefits. In its 10-K filing, the utility reported a nearly 41% increase in annual net income, which rose to just under $2.52 billion ($7.25/share) in 2023 from $1.66 billion ($4.68) in 2022. (See Con Ed Yearly Earnings Continue to Rise.)

Adjusting for the CEB sale, and other financial hypotheticals, ConEd’s annual earnings saw a more modest 9.6% increase, rising to $1.76 billion ($5.07/share) in 2023 from $1.62 billion ($4.57/share) in 2022.

ConEd forecasts its 2024 adjusted earnings per share to be between $5.20 and $5.40 and expects an average annual increase in peak demand for electricity and gas over the next five years to be 2.7% and 1%, respectively. It also anticipates a 6.4% annual rate base growth through 2028.

FERC on Feb. 15 allowed We Energies a MISO tariff waiver, making it simpler for the utility to trade gas for coal at its Oak Creek campus in Wisconsin.

The commission granted We Energies a one-time waiver of MISO’s generator interconnection procedure requirements so it can link up a new gas-fired generator at a different voltage to replace its Oak Creek coal plant under a replacement generating facility request (ER24-646).

We Energies plans to retire two of its 60-year-old Oak Creek coal units in May and the remaining two units by December 2025. It intends to replace the capacity with a $1.4 billion, 1.1-GW natural gas power plant and LNG storage facility to be completed in 2028.

Oak Creek is connected to ATC’s 230-kV transmission facilities. ATC plans to transition its system surrounding Oak Creek to 345-kV and 138-kV only and eliminate its 230-kV facilities by 2027, hence the new gas plant requiring an interconnection at a different voltage than the existing coal plant. We Energies said it had to request the waiver due to factors outside of its control.

ATC supported We Energies’ waiver request and said it would be the most cost-effective and efficient means of dealing with the issue. We Energies said if it wasn’t granted the waiver, it would have been forced to either install facilities to interconnect with ATC’s current 230-kV facilities and then replace them soon after with 138-kV- or 345-kV-compatible facilities, or “submit a new interconnection request for a project that would otherwise qualify for MISO’s generating facility replacement process due to no fault of its own.”

Oak Creek’s generator interconnection agreement struck in 2000 did not specify a voltage level for the coal plant’s interconnection service.

FERC said We Energies acted in good faith and that the waiver addresses a concrete problem with no detrimental consequences.

We Energies executives have said the Oak Creek gas plant would serve as a backup power source when renewable energy output dwindles. Nonprofit Clean Wisconsin has argued any new natural gas additions go against We Energies’ goal of achieving an 80% reduction in carbon emissions from 2005 levels by 2030 and 100% carbon-neutral energy by 2050.

Below is a summary of the agenda items scheduled to be brought to a vote at the PJM Markets and Reliability Committee meeting Feb. 22. Each item is listed by agenda number, description and projected time of discussion, followed by a summary of the issue and links to prior coverage in RTO Insider.

RTO Insider will be covering the discussions and votes. See next week’s newsletter for a full report.

Markets and Reliability Committee

Consent Agenda (9:05-9:10)

B. Endorse proposed revisions to Manual 3A: Energy Management System (EMS) Model Updates and Quality Assurance with the goal of aligning to NERC’s Bulk Electric System (BES) definition. (See “Other Committee Business,” PJM OC Briefs: Feb. 8, 2024.)

C. Endorse conforming revisions to Manual 11: Energy and Ancillary Services Market Operations to implement the real-time temporary exception process FERC approved in EL21-78. (See “Real-time Temporary Exceptions Manual Revisions Proposed,” PJM MIC Briefs: Jan. 10, 2024.)

D. Endorse proposed revisions to Manual 38: Operations Planning resulting from its periodic review. (See “Other Committee Business,” PJM OC Briefs: Feb. 8, 2024.)

E. Endorse proposed revisions to Manual 40: Training and Certification Requirements resulting from its periodic review.