FERC on Feb. 16 approved a MISO transmission connection agreement for the $7 billion, 5-GW Grain Belt Express HVDC transmission line despite protests from developer Invenergy over a three-year construction lag contained in the contract (ER24-715).

FERC disagreed with Invenergy Transmission that it should order MISO to insert a limited operation provision into the Grain Belt transmission connection agreement to allow it to begin partial operations in 2027. The commission said the agreement aligns with MISO’s current interconnection rules for merchant HVDC generation and approved it unexecuted.

Invenergy argued the transmission connection agreement for Grain Belt is unfair because it doesn’t include an option for a limited operation of the line while Ameren Missouri completes network upgrades necessary for the merchant HVDC line. Invenergy said it began negotiations on the transmission connection agreement with a 2027 in-service date and MISO notified it in September that it must use a Dec. 1, 2030, in-service date.

The transmission developer argued that other generators that gain injection rights on the MISO system are eligible for limited operations until they can be fully accommodated.

However, FERC said Grain Belt’s agreement “appropriately reflects” the state of MISO rules and noted the agreement could be modified with a limited operation provision if a new rule is agreed on through the RTO’s stakeholder process.

FERC said while it has allowed nonconforming interconnection agreements, they either must be necessary for reliability, raise a fresh legal issue or be required by “other unique factors.”

“Grain Belt does not allege specific reliability concerns, novel legal issues, or other unique factors sufficient to show that the provision is necessary. Rather, Grain Belt states that, absent the nonconforming provision, there will be broad ‘adverse impacts on [Grain Belt] and on the customers that would otherwise benefit from the reliability, economic and public policy benefits that the GBX Line will provide,’” FERC wrote, adding that Invenergy’s arguments “merely highlight” the potential benefits — not essentials — that limited operation could provide.

Grain Belt is the first merchant HVDC customer to proceed through MISO’s interconnection queue, and Invenergy has said the status of the line means it and MISO inevitably will discover hiccups in the merchant HVDC interconnection queue rules and bring them forward for solutions in the stakeholder process.

Invenergy said MISO told its employees it could initiate stakeholder discussions on adding limited operation options to merchant HVDC interconnections in the future but that the RTO didn’t commit to a timeline for introducing the issue in its stakeholder committees.

“Under MISO’s timetable, by the time it starts stakeholder proceedings in a few years, develops a tariff proposal, and files it with and obtains commission approval, Grain Belt’s desired 2027 in-service date will have come and gone and MISO’s promise to look into this will not be a delay, but will amount to a denial of service,” Invenergy argued.

The company said the RTO should have offered the same accommodations it would have for other interconnection customers, including limited operations provisions. It pointed out that both generation and merchant HVDC will transfer energy from their projects onto the grid and should be treated comparably under Order 2003.

MISO responded that FERC’s Order 2003 was meant for generating facilities interconnection to the grid and doesn’t extend to merchant HVDC projects. It said Grain Belt was attempting to justify “nonconforming revisions with nonexisting policies.”

Invenergy said that MISO’s rejection of a limited operations arrangement is wrong “given the urgent need for transmission in the U.S. and the harm to Grain Belt and MISO loads.”

The transmission developer also claimed that “some amount of connection service and associated injection rights,” varying from 158 MW to 1,491 MW, could be supplied prior to the completion of Ameren’s system upgrades.

Ameren Missouri maintained that it wouldn’t have given Grain Belt an impression of how much below the requested injection rights it could flow over its system because it’s up to MISO, not a transmission owner, to make that call. MISO said a possible amount of interim injection rights is irrelevant because Grain Belt didn’t meet FERC’s standard of addressing reliability concerns of unique operational issues.

An uninhabited island on Maine’s central coast is the preferred site for a port to support the offshore wind farms state leaders hope will be built nearby.

Sears Island had emerged as the likely choice during a lengthy deliberation that included Eastport and Portland.

Gov. Janet Mills (D) announced Feb. 20 that it had in fact been chosen.

Consideration of Sears Island had been controversial all along, as it is a wooded nature preserve. After the decision was announced, island advocates confirmed the fight against development is far from over.

This has become a familiar role for them. Over the past few decades, they have fought proposals including a nuclear reactor, LNG terminal, coal-burning power plant and oil refinery. None ever reached construction.

The nearby region is not heavily industrialized, nor is it virgin wilderness. Tankers dock at a mainland oil terminal just a few hundred yards from northwest Sears Island.

And as Mills noted in her announcement, 330 acres of the 941-acre state-owned island are reserved for port development. Approximately 100 acres of that would be needed for fabrication, staging, assembly, maintenance and installation.

Nearby Mack Point, on the mainland, was evaluated along with Sears Island in a process that stretched more than two years. But Mack Point would have required dredging, adding to the cost of a project already expected to run in the $500 million range.

There are many more steps before the state can break ground on an offshore wind port, including independent state and federal reviews of the permit applications the Maine Department of Transportation plans to submit this year.

In consideration of the state’s large fishing industry, Mills in 2021 signed legislation banning new offshore wind construction in state waters. This puts the 3 GW of offshore energy generation capacity state leaders envision in federal waters too deep for fixed-bottom turbines. (See BOEM Designates Draft Wind Energy Area in Gulf of Maine.)

Floating turbines still are in research and development, including in Maine, where the state university has an ambitious program the state hopes to parlay into a lucrative new sector for its economy.

A good deepwater port would be a key part of Maine assuming a national or regional leadership status in floating wind.

Friends of Sears Island indicates it is not opposed to the drive for offshore wind or for a port. But Mack Point seems like a better site to them.

In a Facebook post Feb. 20 after Mills’ announcement, the organization said: “We are disappointed beyond words, of course, but there are many steps necessary before the port is built. The federal, state and local permitting process is onerous, and multiple challenges can be anticipated.”

Others applauded Mills’ decision, including labor and environmental groups eager for the anticipated economic and environmental benefits of offshore wind development.

Maine completed its Offshore Wind Roadmap a year ago. (See Maine Finalizes Offshore Wind Roadmap.) The state currently is awaiting federal approval to lease a site in the Gulf of Maine where it can tether 10 to 12 floating turbines as a test project.

State leaders hope placing the nation’s first floating research array off Maine’s coast will further boost the small state’s profile as the floating wind expands in the United States.

AUSTIN, Texas — Infocast offered attendees to its annual ERCOT Market Summit on Feb. 13-15 an “unparalleled deep dive” into impending changes still facing the Texas market and how they affect it.

Policymakers joined together with utility, renewable and trading executives to explore ERCOT’s future and examine the effects on resource adequacy, power prices and how to best meet the shifting needs of commercial, industrial and retail customers.

Coming as it did during the three-year anniversary of the 2021 winter storm that shut down thermal plants and natural gas facilities, leading to more than 20 GW of load shed and dayslong outages that devasted the state, speakers did not need much prodding to be reminded of what happened back then.

State Sen. Charles Schwertner (R), a leading voice on market design issues as chair of the powerful Senate Business and Commerce Committee that oversees electric market policies, said the Legislature’s work is not yet done.

“We have a responsibility to continuously assess the durability of the grid and potential deficiencies — the continual demands of our growing state — and update our policies to ensure our system adapts to ever changing conditions,” he said.

Schwertner cited recent comments from Texas Gov. Greg Abbott (R) that the state will need to grow its power supply by 15% a year to keep up with rising demand from industry and residential consumers.

“That’s a big number, 15%, and one that was not even considered a year ago,” he said. “Legislators must keep this in mind next session [in 2025] and be prepared to continue our work on powering Texas. We can confidently meet the projected demands of the state when we take an all-the-above approach to building our power portfolio.”

Much of the focus will be on resource adequacy and ERCOT’s potential movement away from market solutions to capacity shortfalls. A panel debating market design principles was asked whether the current design is sending the proper signals or whether investors remain concerned about regulatory uncertainty.

“Yes, all of the above,” responded Emily Jolly, associate general counsel for the Lower Colorado River Authority. “Fundamentally, I think there is a dispute about whether we do have a resource adequacy problem in ERCOT … and looking at the indicators of the viability of the forward market today and the amount of volatility that we’re seeing. But from our perspective, no question it’s a resource adequacy concern driven by market fundamentals that do not incentivize the types and quantities of generation that are needed to support the growth in Texas.”

“I completely agree with everything you just said,” R Street Institute’s Beth Garza told Jolly. “I think it’s relatively indisputable that the market is really not sending the price signals for resource adequacy.”

Garza, who was ERCOT’s market monitor until 2020, said the inaccurate price signals are the reason lawmakers created — and voters approved — the $10 billion Texas Energy Fund to incent more dispatchable generation, primarily gas-fired, and that state regulators and ERCOT are working on a performance credit mechanism (PCM) to restructure the current energy-only market. (See 2023 Elections Bring Billions for Texas Gas, Dem Wins in Virginia, NJ.)

“The question for us today is whether those steps are enough, whether the Texas Energy Fund is actually going to incentivize the kind of dispatchable generation that Texas needs,” Garza said, “whether the performance credit mechanism is going to incentivize the kind of reliability that ERCOT needs, and whether it’s going to provide the necessary funding for generators to conduct the kind of maintenances that are required to be able to provide energy during weather emergencies.”

E3’s Olson Defends PCM

Arne Olson, a senior partner at Energy and Environmental Economics (E3), found himself defending the firm’s PCM proposal from his fellow panelists.

The PCM is a market tool that would retroactively award incentive payments to dispatchable generation that meets performance criteria during the tightest grid periods. ERCOT and the Independent Market Monitor plan to produce a cost-benefit analysis on the PCM before next year’s legislative session. The mechanism had an early price tag of $500 million, but legislation last year set a $1 billion cap.

The cap “could limit its ability to perform the intended function, which is to stabilize revenues, particularly during a calm year. … That’s when you see the highest payments,” Olson said. “If the payments are lower than what it was, then the revenues are stabilized less. You have less market entry, and you have less reliability.”

“We all want reliability; we all want to improve sending the signals to resources; but we also want to balance the reliability benefit with the costs,” Shell Energy’s Resmi Surendran said. “The guardrail was put in based on a lot of debate and discussion … to say that annual net cost of PCM should not be more than $1 billion minus any of the benefits that are added to grid solutions.”

“One of the concerns I’ve had about some of the PCM is the interplay with the energy-only market. We don’t want to have 60% of the revenues coming out of PCM and 40% coming out of energy and ancillary services. That’s not a sustainable market,” Engie North America’s Bob Helton said. “So, as we design this, we’ve got to ensure that the PCM is the icing on the cake, and it is leveling out those revenues over a longer period of time and you save on investment. The rest gives you the flexibility and what types of generation you need.”

Helton said another of his concerns is dependent on the penalties for nonperformance during critical scarcity hours.

“You could create a situation where you overbuild the system and increase the cost of that just due to administrative penalties and not just because of some reliability issues,” he said.

Olson reminded the panel that the PCM’s primary purpose is revenue stability.

“It’s meant to address the boom-bust cycle, so when there’s a couple of blowout years, we’ll measure investments,” he said. If the “system is overbuilt and nothing happens for 10 years — the margins are low — then people start to exit the market. … It’s a residual market. It’s going to be based on the net cost of capacity, not zero cost, and so if someone has a blowout year, the PCM payments are going to be low. When it’s a calm year, that’s when the PCM payments will be higher.

“That’s how it increases revenue stability year over year with dispatchable generators and as a result of increased revenue stability. Carrying the cost of financing those resources should go down,” he added.

Noting other markets will continue to have boom-bust cycles, Jupiter Power’s Caitlin Smith said, “You can’t have one market that is completely stable and the inputs and outputs are boom-bust. I think that’s just the nature of markets.”

“We’re all looking at the same thing, and that’s, how do you operate and incent investment in a zero-marginal cost world?” Helton said. “It’s not going to be just the PCM. The PCM is a bridge to help us get there. We’ve got a lot of sausage-making, and we don’t know how good this is going to be.”

AC Link to National Grid Unlikely

News broke during the summit’s second day that U.S. Reps. Greg Casar (D-Texas) and Alexandria Ocasio-Cortez (D-N.Y.) had filed the Connect the Grid Act, mandating interconnections between ERCOT and its neighboring grids.

The legislation would direct ERCOT to build between 2.6 and 4.3 GW of capacity with MISO, SPP and the Western Interconnection. It would also give FERC oversight over pricing and transmission planning in ERCOT, a concept long considered anathema by Texas lawmakers and the market’s participants.

“I think it’s been discussed many times that we don’t want good connections because we don’t want FERC coming and telling us how to manage things,” Schwertner said during his opening keynote. “I don’t think we could have passed [legislation] in Texas these last three years, ensuring as robust response to those weather events, if we had Mother Federal Government telling us what to do. So, no, I don’t think it’s going to happen. I don’t really know how much of a reliability improvement it would be, quite frankly.”

A day later, Schwertner was more direct: “Not going to happen!” he posted on X.

Texas does have several smaller DC ties with SPP and MISO. Pattern Energy’s Southern Spirit, a 400-mile, 345-kV DC link into the SERC Reliability region, gained regulatory approval in 2022 after seven years of review. Because no ERCOT electrons will be mingled with other grids, the project will not bring Texas under FERC jurisdiction. (See “SCT Proceeding Closed,” Texas Public Utility Commission Briefs: Sept. 29, 2022.)

“AC ties are never going to happen. Too hard, too expensive,” Garza said. “DC, on the other hand, we’re missing out on.”

“I think it’s an incredibly unlikely idea that will never come to fruition, if for no other reason than creating that level of AC inter-tie to [other regions] invites far more FERC oversight than ERCOT wants,” Jolly said.

Panelist: ‘Bigger, Faster, More Tx’

Matt Pawlowski, vice president of development for NextEra Energy Transmission, had a quick response when asked how ERCOT can plan to ensure it has enough transmission to support oil and gas growth in the Permian Basin.

“Bigger, faster; make more transmission available. I mean, that’s the answer, right?” he said. “You’ve got to plan for it. It’s going to take seven or eight years to build transmission. This is an issue in every single region around the country. Plan for the build because the generation is coming; the transition is coming. You’ve got to get faster on planning; you’ve got to issue [notifications to construct] faster to build that transmission.”

Pawlowski’s mindset is driven in part by his experience lobbying politicians on Capitol Hill. He related an experience with three senior U.S. senators who were unable to distinguish between electric transmission and transmission systems in vehicles.

“Most of the time, I used to get laughed out of the room. People say, ‘Oh, he’s talking about that stuff. It’s really hard. It’s really expensive. We don’t need it anymore; everything’s fine,’” he said. “Now, all the questions that I hear is, ‘Can you do it faster, better, bigger?’

“I think it speaks to all the changes that are going on,” Pawlowski added. “There’s a lot of policy changes, a lot of things that we need to do, but you know, transmission is really at the forefront of what we’re hearing from our customers, from our regulators, from policymakers, from everybody all around. So, it’s an exciting time to be in the transmission space.”

ISO-NE’s proposal to comply with FERC’s Order 2023 failed to meet the voting threshold to receive support from the NEPOOL Transmission Committee on Feb. 15. A series of stakeholder amendments to the proposal also failed to exceed the threshold.

Order 2023 is set to upend how the RTO handles the interconnection of new generators, but the upcoming April 3 compliance deadline has put a strict timeline on the development of the proposal and the stakeholder engagement process.

Intended to speed up interconnection timelines, the order requires RTOs to group interconnection requests together in “first-ready, first-served” cluster studies, while sharing upgrade costs among projects within the cluster. ISO-NE currently uses a “serial first-come, first-served study process,” which evaluates requests oneata time.

Prior to the vote, ISO-NE outlined its compliance proposal, which it has been discussing with stakeholders at the TC since August.

“ISO-NE is proposing to adopt the large majority of the requirements of Order No. 2023 to address queue backlogs, improve certainty, and prevent undue discrimination of new technologies through its incorporation of improved processes, deadlines and penalties,” said Al McBride of ISO-NE.

McBride highlighted several key changes to the region’s interconnection procedures. Along with the adoption of cluster studies, the new rules will include provisions intended to weed out speculative interconnection requests, including new withdrawal penalties and increased financial and site control requirements.

The compliance proposal also will change how ISO-NE models storage resources in the interconnection process. Instead of studying the impacts of storage resources charging at peak load levels, the RTO will study battery charging at a “shoulder” load level.

As proposed, each cluster process will take more than two years to be completed, with subsequent clusters initiated 582 days after the start of the previous cluster.

Throughout the stakeholder process, companies and organizations have brought over 25 amendments to the TC. This list was narrowed to six amendments by the time the committee voted Feb. 15. The proposals included amendments by RENEW Northeast, Advanced Energy United, New Leaf and Glenvale Solar.

In two amendments, RENEW proposed to separate the study costs for capacity and energy-only requests and give resources the option to request capacity interconnection only if the service would not require additional system upgrades.

Under this proposal, “a project that is viable as energy-only and is unable to pay for capacity upgrades still can attempt to get a capacity interconnection to the extent no upgrades are needed.”

ISO-NE responded that the costs from capacity and energy-only interconnection requests cannot feasibly be separated. The proposal received 57% support from the TC, failing to reach the 66.67% threshold.

In Alignment

To further the order’s intent to reduce interconnection backlogs and wait times, Advanced Energy United (AEU) proposed creating an “Interconnection Reforms Working Group” along with a reporting requirement related to interconnection timelines.

“ISO’s proposed timelines significantly exceed the requirements of FERC’s Order,” AEU’s Alex Lawton said. “Ongoing discussion of further reforms is needed to identify opportunities to streamline the process and bring it in line with FERC’s expectations and the region’s pressing need to bring resources online more efficiently.”

Advanced Energy United also proposed a joint amendment with RENEW to add an opportunity for interconnection customers to decrease the size of a project prior to a restudy if it does not affect the cost and timing of another project. The proposal also received 57% support.

Glenvale Solar proposed an amendment aimed at reducing the costs of commercial readiness deposits, which pose a “barrier to accessing transmission for viable projects,” said Aidan Foley of Glenvale. The proposal garnered 39% of support from the TC.

New Leaf proposed that ISO-NE continue work on interconnection studies that are projected to be completed between the current cutoff date for study work and the start of the first cluster study, with goals of speeding the timelines for these projects and reducing the number of projects in the initial cluster.

Alex Chaplin of New Leaf noted this would apply to nine clean energy projects with a combined 1,485 MW of nameplate capacity. This proposal received 66.6% support from the TC, falling just short of the 66.67% threshold.

Chaplin told RTO Insider that New Leaf supports all the proposed amendments, and particularly emphasized the importance of Advanced Energy United’s proposal to create an interconnection working group.

“We think the region needs to commit to ongoing evaluation and continuous improvement of our interconnection process,” Chaplin said, adding that the working group “would help facilitate the ongoing improvement of the interconnection process that we believe is required to meet the region’s clean energy goals in an efficient manner.”

ISO-NE’s unamended compliance proposal also failed to pass the TC’s voting threshold with 56% of the committee in support.

An ISO-NE spokesperson told RTO Insider that its compliance proposal “aligns with FERC Order 2023, and we do not anticipate any expansion of our compliance,” but noted the RTO still is assessing the amendments and has not made a final decision.

The Participants Committee will vote on the compliance proposal in March, and stakeholders also can put forward any amendments. NEPOOL votes are recommendations to ISO-NE, and the RTO does not need to adopt any amendments in filings to FERC.

HOUSTON — Leaders from the gas and electric industries warned NERC on Feb. 14 that there are no easy answers to the challenges posed by the growing interdependence of their sectors.

Speaking at the ERO’s quarterly technical session in Houston, Todd Snitchler, CEO of the Electric Power Supply Association, acknowledged that the winter storms of February 2021 and December 2022 — also called Uri and Elliott, respectively — represented “two strikes” against the industries.

NERC and FERC’s joint report following the 2022 storm called the effects of cold weather on the gas and electric systems — gas production declined by more than 50% at some facilities, and generation failures led to more than 90 GW of unplanned outages — an “unacceptably familiar pattern.”

Leaders at both organizations have endorsed the idea of a gas reliability organization similar to the ERO, echoing a suggestion from the chairs of the North American Energy Standards Board’s Gas-Electric Harmonization Forum. (See NAESB Forum Chairs Push for Gas Reliability Organization.)

Snitchler was joined on stage by Interstate Natural Gas Association of America CEO Amy Andryszak, Natural Gas Supply Association CEO Dena Wiggins and NERC Chief Engineer Mark Lauby. He said that even before the FERC-NERC report was completed, he was already talking with Andryszak and Wiggins about how they could prevent the kind of supply issues, with gas needed for both home heating and electric generation, that led to so many outages during both winter storms.

“I reached out to Amy and Dena and said, look, we all agree [on] and recognize the importance of natural gas for the power sector; we’re all part and parcel of the system. And it would do us all a lot better if we tried to collaborate on what some workable solutions would be instead of pointing fingers,” Snitchler said.

“There’s no silver bullet that’s going to solve all the issues before us,” he continued. “In fact, I’m not even convinced there’s silver buckshot, because the situations are unique to regions, they’re unique to pipelines, they’re unique to resources, and they’re unique to each of our sectors and what we do. But I think what we tried to convey is that there are incremental changes that can be made, that will be very helpful when … you layer them on top of one another.”

Andryszak spoke more pointedly against the idea of a natural gas equivalent to the ERO, observing that the gas industry is “already heavily regulated by FERC and” the Pipeline and Hazardous Materials Safety Administration. She questioned whether a separate organization would really make much difference in overcoming the challenges cited in FERC and NERC’s report.

“FERC already has within their authority the right to ask more information of the pipeline industry as it relates to winterization, so we don’t think that there needs to be a new regulator to deal with that aspect, in addition to what we already voluntarily do,” Andryszak said. “But we think there’s more of a role that FERC could probably play there if they chose to do so.”

Wiggins pointed out that creating a gas reliability organization also poses practical challenges because the legislative environment today is different from how it was in 1967, when the Electric Power Reliability Act was passed, creating NERC, or even in 2005, when the Energy Policy Act created the ERO.

“Even if we believe that a mandatory GRO is the best thing since sliced bread, it takes legislation,” Wiggins said. “And as everyone knows who’s watching Congress these days, that is going to be, in this Congress or the next, a really tough [time] … which I think should further incentivize all of us … to work together and come up with solutions that we all can work with.”

Looking back, it concludes the first-ever flow of electricity from a utility-scale project to the U.S. mainland, while a landmark moment, was one of the few bright spots in 2023.

The U.S. market began the year with 17.6 GW of slated offshore wind capacity, but developers terminated contracts for 51% of that amount and sought financial support for another 24% amid soaring coasts and supply chain constraints.

This had a chilling effect on the nascent domestic supply chain and industrial infrastructure that must develop if the U.S. offshore wind industry is to grow to maturity, benefiting the U.S. economy and environment at a sustainable cost to ratepayers and taxpayers.

The delays, price hikes and other fallout continue as states and developers try to regain the momentum of the early 2020s.

Officials have been putting a resolute face on the situation or sidestepping questions about their aspirational timelines, but Oceantic was blunt in its report:President Biden’s goal of 30 GW of offshore wind installed by 2030 is now out of reach, it said.

Oceantic remains optimistic about the industry’s prospects, however, and sees its recovery already beginning.

As she announced release of the report to Oceantic’s 600-plus members, CEO Liz Burdock said:

“Global economic challenges hindered our progress in 2023, bringing uncertainty to this new and growing market. However, with each step back, we’ve seen the industry press forward and are seeing a transformation in market fundamentals. New power contracts that are resistant to broader economic pressures are being executed and states like New York, New Jersey and Massachusetts remain dedicated to offshore wind development and investing in a domestic supply chain. In 2024, we are seeing the market rebound with interest rates and inflation falling along with new supply chain capacity.”

The fundamental strengths of the U.S. market remain unchanged, the report says. It’s the details that have been scrambled.

Signs For Concern, Optimism

To strain a metaphor, the U.S. offshore wind industry has a chicken-and-egg problem — but with chickens that cost hundreds of millions of dollars apiece and eggs that take years to hatch.

To generate economies of scale and lasting momentum, the industry needs certainty that someone will build its components and provide the machinery to install them. To commit to that, manufacturers need certainty that a given project will be built, or at least financed.

There were failures on both sides of the equation in 2023: Multiple offshore wind projects were put on indefinite pause and multiple supply chain bottlenecks appeared.

Completion delays on a new installation vessel were a big part of Ørsted’s decision to end Ocean Wind I and II, the first and so far only outright cancellation in the present era of U.S. offshore wind development.

Oceantic’s report highlights multiple failures in the past year and multiple signs of optimism for the years ahead, including:

Federally permitted projects jumped from 0.93 to 8.3 GW in 2023 and could reach 14 GW by the end of 2024.

States are pressing to replace canceled contracts and could reach 20 to 25 GW under contract by the start of 2025, which would be a rebound from the 17.6-GW peak before cancellations started.

Domestic manufacturing has begun, including underwater export cable and the first-ever U.S.-built offshore substation.

The first-ever wind energy auction in the Gulf of Mexico was a flop in 2023, generating limited interest and minimal revenue. Three or more auctions could be held in 2024.

Multistate collaboration has begun even as individual states inevitably compete with others for limited resources. Three regional clusters — Connecticut-Massachusetts-Rhode Island, New Jersey-New York and Maryland-North Carolina-Virginia — are working together in some capacity.

Some investors may choose to remain on the sidelines to await the results of the 2024 elections, which could have a significant impact on federal support for offshore wind development. Others might see an inviting market.

The manufacturing and shipbuilding sectors are seeing multiple positive signals in 2024, including falling interest rates, stabilizing prices, issuance of tax credit guidance and multiple large state offshore wind solicitations being underway.

Installation timelines have been significantly delayed; market analysts project only 14 to 16 GW of installation by 2030.

Inflationary pressures are unlikely to ease any time soon but may not get worse in 2024.

Compensation is rising: The awarded strike price in the 2023 solicitation was 28% higher on average than the 2021 awards in New York and 40% higher in New Jersey.

The U.S. Department of Energy issued its Atlantic Offshore Wind Transmission Action Plan in 2023, addressing one of the most pressing needs for the entire endeavor: Getting those new megawatts to market.

In late 2023, South Fork Wind became the first utility-scale offshore wind farm to send power to the U.S. grid. Vineyard Wind soon followed. South Fork expects to wrap construction next month. Vineyard is larger and will take longer. Installation work is set to begin this year on Revolution Wind and Coastal Virginia Offshore Wind.

Washington legislators are proposing to give the state’s utilities $150 million to be rebated back to residents to help them defray costs associated with the state’s cap-and-invest program.

The proposals come after Washington last year grappled with some of the highest gasoline prices in the country, which cap-and-invest opponents attributed to the rollout of the program early last year. (See Cap-and-invest to Loom Large in Wash. Legislative Session.)

Democratic legislative leaders in both chambers unveiled similar $150 million clean energy credit programs Feb. 19 in two supplemental 2023-2025 budget proposals that must be reconciled before the current legislative session ends March 7.

If the funding is approved, the money will go to utilities, which have increased rates partly due to expenses stemming from the cap-and-invest program, then credited back to utility customers.

In the Senate, Ways and Means Committee Chair June Robinson (D) and Sen. Joe Nguyen (D) said lawmakers will have to hash out details related to the size of individual credits and the income thresholds for eligibility to receive them. Robinson speculated the credits would likely be distributed to residents in the fall.

Lawmakers in the House have proposed a one-time $200 credit to eligible households in September.

The credit programs have been proposed ahead of a looming referendum to be held in November on whether to repeal the cap-and-invest program.

In December, Gov. Jay Inslee (D) asked the Legislature to establish a rebate program for lower- and middle-income residents to counteract the higher-than-expected gasoline prices being linked to cap-and-invest. Inslee called for a one-time $200 credit applied to the utility bills of roughly 750,000 low- and moderate-income households. Rep. April Connors (R) introduced a bill similar to the governor’s request, but it never received a committee hearing.

‘Really Suspicious’

At a Feb. 20 press briefing, Washington GOP leaders criticized the timing of the proposed rebate, characterizing it as an election ploy by the Democrats. The Republicans contended the rebate will occur prior to the election with no legislative guarantees of future rebates if voters repeal the cap-and-invest program in November.

“Let’s be candid on how much $200 will help … It’s not much … It’s a little like electioneering,” said Senate Minority Leader John Braun (R).

House Minority Leader Drew Stokesbary (R) echoed that view, saying the timing of rebate “is really suspicious.”

“I wonder how Representative Stokesbary will pay for [the rebates] if we revoke the Climate Commitment Act,” House Majority Leader Joe Fitzgibbon (D) said at a later briefing by Democrats.

Democratic leaders also responded to Republican criticism of Sen. Marko Liias (D), chair of the Senate Transportation Committee, who said repealing the cap-and-invest program will hurt the state’s transportation budget. GOP leaders countered that the transportation budget is independent of the cap-and-invest program.

But Senate Majority Leader Andy Billig (D) noted the cap-and-invest program pays for transportation expenses such as free transit for residents under 18 and some of the conversions of the state’s diesel ferries to hybrid electric vessels, programs the Democrats do not want to revoke.

If the cap-and-invest revenue is eliminated, the limited transportation budget will have to pay for transit and some ferry finances currently supported by the Climate Commitment Act, Billig said.

“We will have to reprioritize everything in transportation,” he said.

Liias noted that cap-and-invest money is paying for roughly one-third of the supplemental transportation budget that the Legislature is currently assembling.

Washington raised about $1.8 billion in its 2023 cap-and invest auctions, money the Legislature is allocating toward clean energy development and programs that mitigate the impacts of climate change, particularly in disadvantaged communities. The Inslee administration is predicting the auctions will raise another $941 million in the first six months of 2024.

The Edison Electric Institute’s senior executives briefed Wall Street on Feb. 20 on the state of the utility industry and some of the policies it supports.

The briefing was the first for EEI CEO Dan Brouillette, who joked that many in the audience were expecting former CEO Tom Kuhn, who retired at the end of 2023. Brouillette came to EEI from Sempra Energy after serving as energy secretary under President Donald Trump. As a staffer in Congress, he helped write the Energy Policy Act of 2005.

“This is an exciting industry,” Brouillette said. “And there’s never been a more exciting time to be a part of it. What is happening today, I think, is truly transformational. We talk a lot about the energy transition; we talk about the changing generation sources. There’s even more to it than that.”

EEI members make up 5% of the economy, which Brouillette called the “first 5%” because they contribute to all the other sectors. The utility sector is seeing growth for the first time in years, he said, with residential customers using electricity more and more for heating and transport, and new demand from commercial and industrial customers as data centers expand because of artificial intelligence, battery manufacturing, microchip factories and reindustrialization.

“There are challenges ahead for the next several years,” said Philip Moeller, EEI executive vice president of regulatory affairs. “But it’s a pretty good challenge to have, when you’re looking at the kind of growth that a lot of our member companies are looking at.”

New England, the Midwest and the West have been facing resource adequacy issues in recent years, but with the rapid growth in demand recently, most of the country needs to build more infrastructure to keep pace, he added.

Member utilities have gotten creative in how they approach regulators on how to meet the new demand, bringing in large new customers like data centers to explain what is driving the need, EEI Chief Strategy Officer Brian Wolff said.

“They are starting to get the rhythm of taking those customers in with them to be able to explain what the need is,” Wolff said. “Because as you know, regulators are first and foremost about customer affordability. So, they’ve really got to be able to make the case for that, and there’s nothing better than hearing from somebody else in the community about how important that is.”

EEI is expecting several final rules from federal agencies, especially EPA, to come out this spring, well before the end of President Joe Biden’s term, as they want to avoid the possibility of the next Congress overturning them through the Congressional Review Act, General Counsel Emily Sanford Fisher said. The rules include an update to the Mercury and Air Toxics Standard, which the industry has already exceeded, she said, along with the effluent limit guidelines on water pollution and another rule on coal combustion residuals.

But the big item coming out of EPA is its new rule on carbon emissions from power plants under Clean Air Act Section 111(d). Fisher said EPA successfully implementing the carbon rules affordably and reliably will require it to be flexible in when plants retire, with the transition to clean energy moving faster some years than others depending on the grid’s reliability needs.

That would ensure “that we don’t need to make big control investments in units that will either accelerate their retirement in ways that are unhelpful from a reliability perspective or encourage folks to run those like into the 2040s to recover their investments,” Fisher said. “There’s a happy medium there, and I hope we can land that plane.”

Fisher expects the final rule to use either carbon capture and storage or clean hydrogen as the requirement for clean power plants, both of which offer the industry-needed 24/7 clean energy production.

“We need that 24/7 clean to balance the grid and to address reliability, and the fact that those technologies aren’t available at cost and scale right now is actually one of the contributors to our concerns about resource adequacy,” Fisher said. “If we had more of those technologies available to us, I think some of those concerns would be lessened.”

The industry has wanted to see new permitting laws to help make it easier to build out the infrastructure subsidized by the Inflation Reduction Act and Infrastructure Investment and Jobs Act, but Wolff said not to expect anything until at least a lame duck session after the November elections.

“If we’re not really moving to agree to fund the war in Ukraine, you can imagine how the rest of the oxygen has left the Congress with regards to getting something actually done,” Wolff said. “And at the end of the day, whether you’re a Republican in the House or a Republican in the Senate, you don’t want Joe Biden to be signing one more piece of legislation into law.”

While many Republicans have called for the repeal of the IRA and IIJA, Brouillette said he doubted either would go away entirely if the GOP wins in November. Money from both is flowing to red states, where it often is easier to get a permit to build infrastructure.

“So of course, the money is going to continue to flow to places like that,” Brouillette said. “What that means, obviously, is that there’ll be support for those programs in Congress going forward.”

Some of the programs the law funds, like hydrogen, have been important to the industry and others for years, so they are unlikely to be swept away in a Republican electoral wave. Likely changes could come if Republicans are in charge of the appropriations process for some of the long-term programs under the laws that will need to have future funding approved.

“If Republicans take both the House and the Senate and the White House, you’ll see some changes,” Brouillette said. “But I would dare say that those changes will be largely at the margins, not at the heart of what was passed in the IRA.”

An RMI study into the applicability of grid-enhancing technologies (GETs) on the PJM grid found they could save consumers hundreds of millions of dollars a year and speed renewable development when used as an alternative to reconductoring and rebuilding lines.

“With growing demand for electricity to power our lives and an influx of clean energy projects under development, the U.S. grid needs to expand, fast. Grid-enhancing technologies can be deployed in a matter of months and offer a multifaceted solution — they unlock greater efficiency on the grid, keep electricity rates down and enhance reliability throughout the energy transition,” Katie Siegner, RMI electric sector expert, said in an announcement of the study. The study was funded by Amazon and included analysis by Quanta Technology.

The study, released Feb. 15, looked at how dynamic line ratings (DLRs), topology optimization (TO) and advanced power flow controls (PFCs) could be used in the analysis PJM conducts to determine network upgrades required for generation interconnection requests. It modeled the feasibility of using the technologies for projects in the PJM interconnection queue and compared costs to reconductor or rebuild lines to GET alternatives.

Some of the greatest cost-saving potential came from PFCs, which modulate the reactance on a line to redirect power from congested lines to those with available capacity. The study identified 69 transmission overloads that could be addressed by flow controllers, with the potential to reduce interconnection costs for associated projects by $523 million over reconductoring or rebuilding lines. PFCs are limited to circumstances where there would be multiple paths for power to flow and are best suited for transmission under 550 kV.

The study found DLRs were applicable to 49 overloads and could reduce costs by $504.5 million by increasing line ratings under favorable conditions. The technology uses sensors and existing data about installed infrastructure to change line ratings based on how factors such as wind speed, air temperatures and conductor sag can affect the amount of power a line can handle before overheating. Although overall summer line capacity could be increased by 17% over current static ratings, the study acknowledges dynamic ratings vary with the weather and therefore are more suited to making energy deliverable than bringing new capacity online.

Topology optimization could reduce the cost to alleviate 72 overloads by $273 million by using software to determine alternate grid configurations that reroute power around constraints, such as opening or closing breakers automatically.

The report states GETs can significantly reduce the amount of time to make the necessary grid adjustments to bring new generation online, addressing concerns PJM has raised about the balance of deactivations and new resource entry, as well as reducing energy costs by speeding development of low-cost renewables. It estimates ratepayers could save $1.1 billion in annual production costs by 2033 against a $0.1 billion installation cost for GETs.

“These findings make a compelling case for more widespread deployment of GETs in PJM, where today there are only a handful of pilots and proposed projects. PJM and its stakeholders have an opportunity to spur broader uptake of these technologies by leveraging the growing proof points, modeling tools and changing regulatory landscape that are driving GETs adoption,” the study said.

It calls for PJM and utilities to train staff in GET deployment and for regulators to draft new guidance and oversight for their usage, arguing adoption in the U.S. is behind Europe due to a lack of understanding and few incentives to seek cheaper transmission options. Generation developers also can benefit from evaluating GETs as an alternative to PJM’s recommended network upgrades for their projects.

There have been some inroads for DLR usage in PJM, in which a pilot program to install the technology on PPL’s Juniata-Cumberland line resulted in line capacity increasing 18% under normal conditions and 10% under emergency conditions, Joseph Lookup, PJM’s director of asset management, told RTO Insider last year. (See Grid-enhancing Technologies Poised for Growth with Federal Funds.)

Speaking in the announcement of the study, Alexina Jackson, AES vice president of strategic development, said it presents an opportunity for greater understanding of how new technologies can benefit the grid.

“There are numerous market-ready technologies that can optimize our electrical grid and accelerate the future our customers need. Realizing how to model the functionality and quantify the benefits of these technologies is a barrier to the implementation of grid-enhancing technologies,” she said.

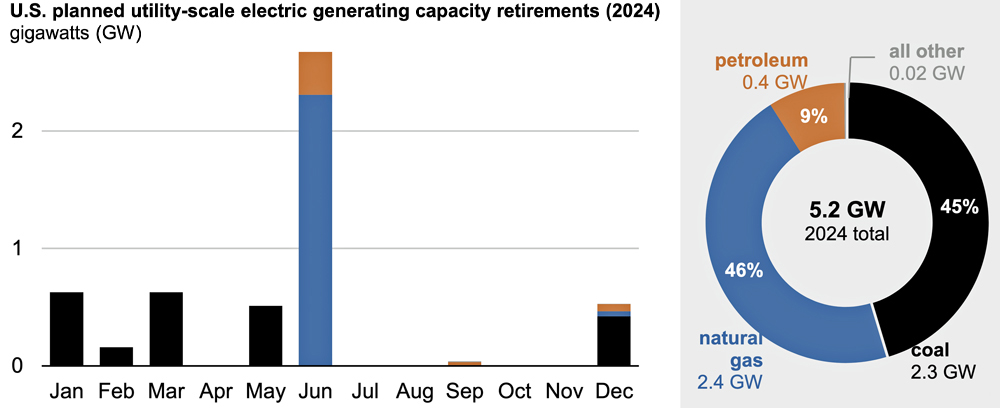

The U.S. Energy Information Administration reports that fossil fuel generation retirements will slow in 2024 and that solar and storage will dominate capacity additions.

The two forecasts represent a pause and an acceleration, respectively, of recent trends.

EIA said Feb. 20 that operators plan to retire 5.2 GW of capacity this year, most of it coal- or natural gas-burning plants. Coal retirements alone totaled 22.3 GW in the past two years and are expected to total 10.9 GW in 2025.

EIA said Feb. 15 that developers and power plant owners plan to add 62.8 GW of new utility-scale capacity in 2024. Almost all scheduled additions are emissions-free power sources, including a record 36.4 GW of solar. That would nearly double the 2023 total of 18.4 of new solar, which itself was a record.

The 5.2 GW scheduled for retirement in 2024 would be the least since 2008 and would be down 62% from 2023, when 13.5 GW was retired. Forecast for retirement in 2024 are plants totaling 2.4 GW of natural gas, 2.3 GW of coal, 450 MW of petroleum and 20 MW of other power sources.

The largest gas retirement will be the last six units (1,413 MW) at the Mystic Generating Station outside Boston, one of the nation’s oldest power plants. The other large gas retirement scheduled is TVA’s Johnsonville station (754 MW).

The largest coal retirements will be Seminole Electric Cooperative’s Unit 1 in Florida and Homer City Generating Station’s Unit 1 in Pennsylvania, both 626 MW.

Almost all of the petroleum-fired capacity retirement will be at TVA’s Allen plant, which has 20 old combustion turbine units totaling 427 MW.

Construction

EIA forecasts heavy growth in renewable energy development in 2024 — particularly in photovoltaics, which is outstripping other generating resources as supply chain challenges and trade restrictions ease.

The planned additions break down to 36.4 GW of solar, 14.3 GW of battery storage, 8.2 GW of wind, 2.5 GW of natural gas and 1.1 GW of nuclear, plus about 200 MW from other sources.

Slightly more than half the nation’s 2024 utility-scale solar construction is planned in three states: Texas (35%), California (10%) and Florida (6%). Elsewhere, the nation’s largest single solar project — the Gemini facility in Nevada, with 690 MW of solar capacity and 380 MW of battery storage — will start to come online this year.

Battery construction also could set a record: 14.3 GW of grid-scale storage capacity added in 2024 would nearly double the installed capacity nationwide, which stood at 15.5 GW at the start of this year. The heaviest battery development is expected to be in the states with the heaviest solar development: Texas (6.4 GW) and California (5.2 GW).

Wind energy is the outlier in the report. Wind capacity addition has slowed after record construction of 14 GW-plus in both 2020 and 2021. The big news in U.S. wind energy in 2024 is likely to be the Vineyard Wind (800 MW) and South Fork Wind (130 MW) projects, the nation’s first utility-scale offshore wind farms. Both are nearing completion off the Northeast coast.

The 2.5 GW of natural gas additions planned in 2024 is the lowest total in a quarter-century. Also notable: 79% of the gas capacity added in 2024 will be simple-cycle turbines, which can start up and ramp up or down relatively quickly to support the grid at times of fluctuating demand or faltering supply from wind and solar generation. This will be the first year since 2001 the slower but more efficient combined-cycle turbine technology did not account for most capacity additions.

EIA forecasts a relatively small amount of fossil fuel generation retirements in 2024. | EIA

Finally, start-up of the fourth reactor at the Vogtle nuclear plant in Georgia, originally scheduled for 2023, now is slated for 2024.