New standards intended to reduce air emissions from the crude oil and natural gas industries are scheduled to be published this week.

The EPA released the proposed rule in November 2021, supplemented it in December 2022 and announced the final rule in December 2023.

The prepared text was posted Feb. 23. It will become effective 60 days after publication in the Federal Register, which is scheduled March 8.

The standards cover new and existing facilities for production, processing, transport and storage of natural gas and crude petroleum. The sector is the largest U.S. industrial emitter of methane, a highly potent greenhouse gas blamed for one-third of the global warming resulting from human activity.

EPA in December framed the new standards as a sweeping series of changes that would apply to hundreds of thousands of sources nationwide and prevent 58 million tons of methane emissions from 2024 to 2038, delivering health and economic benefits worth billions of dollars in the process.

In the same time frame, EPA estimates reductions of 16 million tons of volatile organic compounds and 590,000 tons of various other toxic air pollutants that affect human health. It anticipates the prevention of the release of 400 billion cubic feet of fuel per year.

“Standards of Performance for New, Reconstructed and Modified Sources and Emissions Guidelines for Existing Sources: Oil and Natural Gas Sector Climate Review” (Document No. 2024-00366) takes several approaches to meeting these goals: It encourages use of advanced technology for detecting methane, encourages continued innovation, sets up a program to identify the “super emitters” blamed for about half of the methane emissions from the oil and gas sector, bars flaring at new oil wells, sets zero-emissions standards for process controllers and pumps outside Alaska, and gives existing emitters three years to submit compliance plans.

The 1,356-page unpublished version of the final rule lists four main components in its summary:

finalizing revisions to the new source performance standards regulating greenhouse gases and volatile organic compounds emissions for the crude oil and natural gas source category pursuant to the Clean Air Act.

finalizing emission guidelines for states to follow in developing, submitting and implementing state plans to establish performance standards to limit GHG emissions from existing sources in crude oil and natural gas sectors.

finalizing several related actions stemming from the joint resolution of Congress on June 30, 2021, that disapproved EPA’s final 2020 rule for these emissions standards.

finalizing a protocol under the general provisions for optical gas imaging.

EPA said it received nearly a million comments on the November 2021 proposal and December 2022 supplement, ranging from support for the measures to a desire that they be further strengthened, to practical and cost concerns, to technical suggestions.

After the rule was finalized in December 2023, it was hailed by groups such as the Environmental Defense Fund (“a major step forward in the fight against climate change”) and Clean Air Task Force (“worth the wait … worthy of celebration”).

Others were not so happy.

“The Biden administration has piled on another massive regulatory burden designed to encumber and even shut down American energy production,” said Sen. Kevin Cramer (R-N.D.), the nation’s No. 3 oil-producing state.

The American Exploration & Production Council said: “While we appreciate EPA’s commitment to bringing all stakeholders to the table and see some improvement within the rule, other provisions remain flawed and risk undercutting U.S. production in the near and long-term.”

MISO on March 4 suggested an approximately $20 billion portfolio for its second long-range transmission planning (LRTP) effort, calling for several 765-kV line segments.

The grid operator said its second LRTP draft portfolio for MISO Midwest “focuses on creating a 765-kV transmission ‘highway’ within the MISO region to maximize value based on land use, line distances, transfer levels and costs.” Together, MISO said the anticipated additions could range in cost from $17 billion to $23 billion.

Several of the suggested 765-kV lines are located near 345-kV line routes approved as part of MISO’s first, $10 billion LRTP portfolio, including routes through Iowa that have been cast into uncertainty by a recent court ruling finding the state’s right of first refusal law unconstitutional. (See MISO Asks Court for Injunction Reversal on Iowa LRTP Projects.)

The proposed 765-kV network snakes through Missouri, Iowa, Illinois, Wisconsin and Minnesota. Another suggested 765-kV segment cuts through Southern Michigan into Indiana. The second LRTP draft proposal also calls for several substations and more 345-kV lines in Minnesota, Wisconsin, Michigan, Iowa and Illinois.

As with its first LRTP portfolio, MISO said it sought to minimize new rights-of-way permitting with state regulators to help head off environmental concerns.

At the Gulf Coast Power Association’s MISO-SPP conference March 4, MISO CEO John Bear said the RTO hopes to finalize the second LRTP portfolio for approval by its board of directors at the end of the year.

MISO’s new line suggestions are premised on the RTO’s estimate that it will need 369 GW of new, mostly renewable resources by 2042 based on its members’ plans. MISO said the second LRTP portfolio is the next step to “developing a system needed to reliably and efficiently meet the load growth and resource evolution described in MISO’s members’ plans.”

“This portfolio focuses on creating a regional backbone to meet the long-term needs of our region,” MISO Vice President of System Planning Aubrey Johnson said in a press release. “Our transmission solutions — creating a sort of interstate highway system for electricity — enable the future resource plans of our states, utilities and members by addressing regional needs, while recognizing that local issues will continue to be addressed through our MTEP and generator interconnection queue processes.”

“The future grid must be able to integrate new load growth and respond to extreme weather, and a robust transmission system is required to ensure this occurs reliably and efficiently,” said Laura Rauch, executive director of transmission planning at MISO. “We know further transmission development can provide value and we will continue working with our stakeholders to refine this portfolio and ensure it is sufficiently robust.”

MISO said it will continue analyzing the benefits of anticipated portfolio over the coming months and take stakeholders’ suggestions for project alternatives through April 5.

MISO will hold its next LRTP workshop with stakeholders on March 15.

Bribery scandals and concerns over reliability and the pace of decarbonization have caused increasing scrutiny of utilities’ political activities.

Almost one-third of U.S. states have approved or are considering actions to bar investor-owned utilities from using customer funds to support political activities.

Michigan last month became the 11th state to consider legislation restricting utilities’ political spending, which already has been approved by four states, according to the Energy and Policy Institute, a watchdog group. In addition, the Louisiana Public Service Commission began a rulemaking last year to investigate utilities’ use of ratepayer money for trade association dues and political influence activities.

Floodlight, a nonprofit newsroom, reported recently that utility fraud and corruption in those states and Florida, Mississippi and South Carolina have cost ratepayers at least $6.6 billion. “Ratepayers have bankrolled nuclear plants that never got built, transmission systems that were over-engineered to beef up profits and aging coal facilities that couldn’t compete with cheaper ones powered by methane, which the industry calls natural gas,” it said.

Pay for Play?

Last week, a group of activists calling themselves the “Flip the Switch” coalition gathered outside the Washington, D.C., hotel where hundreds of state regulators, utility officials and other stakeholders gathered for the National Association of Regulatory Utility Commissioners’ (NARUC) Winter Policy Summit. The group protested what it called the “pay-for-play relationship between utility regulators and the fossil fuel industry” and called on NARUC to stop accepting sponsorship money from groups NARUC members regulate.

Natalie Mebane, chief program officer, for climate justice organization Zero Hour, speaks at protest outside the NARUC Winter Policy Meeting in Washington last week. | Zero Hour

The Winter Policy Summit’s sponsors included the American Gas Association, American Petroleum Institute and Edison Electric Institute, the organization representing investor-owned utilities. Groups supporting renewables, such as the American Clean Power Association, Advanced Energy United and the Solar Energy Industries Association, also were sponsors. (Disclosure: RTO Insider LLC also was a sponsor.)

Regina L. Davis, NARUC’s assistant executive director, rejected the protestors’ claim of a “pay-to-play” relationship.

“Because we work hard to convene meetings that foster collaborative discussions and dialogues on a range of issues, we will attract trade groups, whether or not they are sponsors,” she said. “As a fuel-agnostic association, our sponsors represent a range of energy sectors. At this meeting, more than 90% of our sponsors were not affiliated with the fossil fuel industry.”

“We would encourage anyone seriously interested in how our meetings are run to review the Winter meeting agenda instead of making broad generalizations that are not based in fact,” she added. “Our members and stakeholders hold diverse views related to the clean energy transition and are focused on how best to ensure safe, reliable, and affordable energy.”

She noted that attendees included consumer advocates and that NARUC provides free admission to the press, “who function as the eyes and ears of the public.”

In a statement last month, EEI defended its lobbying and its environmental record, saying U.S. power sector carbon emissions are as low as they were 40 years ago, while electricity use has climbed 73%.

“EEI’s member companies are among the most regulated companies in the country, and EEI engages on their behalf with federal and state legislators, regulators and other policymakers through lobbying, advocacy and regulatory proceedings, with the goal of providing customers with the affordable, reliable and resilient clean energy they need and expect,” it said.

In 2021, FERC opened a Notice of Inquiry over the recovery of trade association dues in utility rates, with commissioners questioning whether customers should pay for groups that seek policies that may be contrary to consumers’ interests (RM22-5). However, there has been no substantive action in the docket since comments were filed almost two years ago. (See FERC Questions Ratepayer Funding of Trade Association Dues.)

Michigan Legislation

At a press conference Feb. 22, several Michigan Democrats called for legislation to bar the state’s electric utilities from making political contributions to candidates, political parties and accounts tied to state politicians or social welfare groups.

HB 5521 prohibits an electric or natural gas utility regulated by the Michigan Public Service Commission from making donations or contributions to 501(c)(4) (political nonprofits) or 527 (political action committees) organizations. HB 5520 prohibits 501(c)(4) or 527 organizations affiliated with state regulated utilities from making donations or contributions to other 501(c)(4) or 527 groups.

The proposal is backed by a number of environmental and community activist groups but is opposed by DTE Energy and CMS Energy, Michigan’s largest utilities.

The proposal is aimed at forcing utilities to focus on improving their overall service “instead of increasing their profits,” said the sponsor, Rep. Dylan Wegela (D), referring to blackouts that have followed major storms.

Wegela, from the Detroit suburb of Garden City, was joined at the press conference by state Sen. Jeff Irwin (D) of Ann Arbor — a city that has an ongoing standoff with DTE over service and rates — as well as state Rep. Emily Dievendorf (D) of Lansing. Lansing and some of its suburbs are served by the city-owned Board of Water and Light and have had fewer blackout problems than either DTE or CMS. In December 2013, however, BWL customers suffered through a blackout that affected customers for as many as 10 days.

Katie Carey, a spokesperson for CMS, blasted the bills.

“We’re a Michigan company, and we’re all in on Michigan’s prosperity. We strive to conduct our business in a transparent way, including our participation in the legislative and political process. Contributions to elected officials can come from one of two places — either shareholder profits, or voluntary contributions made by our employees to the Employees for Better Government (EBG) PAC — and never customer dollars. The EBG PAC is nonprofit, nonpartisan and governed by an employee-run steering committee that is independent of the corporation’s officers and board. Participation in the PAC is voluntary and gives employees a voice in the political process, and all PAC contributions are publicly disclosed on the secretary of state’s website.”

DTE issued a statement, saying: “DTE’s political giving is transparent and within all campaign finance limits. Like most other organizations, DTE participated in the electoral process to advocate to propose safe, reliable, affordable and clean energy for the 3 million Michigan residents and businesses it serves every day.”

Both utilities have been tied to big money contributions in previous campaigns. In 2022, Michigan Energy First, a 501(c)(4) organization that got money from DTE, donated $1.1 million to the Michigan Democratic Party. In the same year, Citizens for Energizing Michigan’s Economy, a 501(c)(4) organization connected to CMS, donated $200,000 to the Michigan House Democrats.

Given that politicians from both parties have benefited from contributions from utility employees and community groups backed by the utilities, it’s unlikely either party will take a position in favor of Wegela’s bills. Bridge Michigan reported last year that 102 of 148 sitting Michigan lawmakers have received campaign funds from utility company PACs.

Bills Approved

Last year, Colorado, Connecticut and Maine enacted prohibitions on utilities’ recovery of lobbying, advertising or trade association costs, according to the Energy and Policy Institute, which seeks to “expose attacks on renewable energy and counter misinformation by fossil fuel and utility interests.” New Hampshire enacted similar legislation in 2019.

FERC denied a merger proposal in which Bridgepoint tried to buy a 19.9% stake in Energy Capital Partners, saying it did so without prejudice because the first firm failed to disclose its relationship with a third company — Blue Owl (EC24-2).

ECP is a private equity firm that owns interests in Calpine Corp., Terra-Gen Power Holdings, Convergent Energy and Power, and Pivot Energy, while Bridgepoint has a similar business model, but with more assets outside of FERC’s purview.

Blue Owl owned stock in both firms but told FERC only about its shares in Bridgepoint, saying part of the deal would involve executing an irrevocable deed under United Kingdom law to restrict its actual voting shares below 10%, which is the commission’s threshold that triggers affiliate regulations.

Public Citizen intervened in the FERC case to note that in requesting approval for the deal from U.K. regulators, the firms said that Blue Owl also owns 19.3% of ECP’s share. That information was never filed at FERC.

“We find that, based on the record in this proceeding, applicants have not shown the voting restriction is sufficient to eliminate a potential affiliation between Blue Owl and Bridgepoint and that applicants did not provide information as to the holdings of Blue Owl for the purposes of the commission’s competition analysis,” FERC said.

FERC staff would have normally reached out to the applicants and asked them to file information related to Blue Owl’s overlapping holdings, but the rejection (without prejudice) shows the commission is running out of patience when sophisticated players do not reveal required information, said Public Citizen’s Energy Program Director Tyson Slocum.

“FERC is a regulator that relies almost exclusively on self-reporting,” Slocum said. “They heavily rely on companies to just come to the table and put all of their cards on the table. And FERC apparently perceived that they didn’t do that here.”

Because the deal was rejected without prejudice, Bridgepoint said March 4 that it would shortly refile the application with the previously missing information and hoped to close the deal for nearly a fifth of ECP by the second quarter of this year.

“I think FERC is trying to navigate this space of dealing with increasingly complicated financial structures that are getting into the utility business,” Slocum said.

ECP is a dominant player in FERC-jurisdictional markets while Bridgepoint owns a great deal of energy infrastructure in Europe, so their combination would be huge. While the deal involves just $1 billion in cash, Slocum said the fact that two top executives at ECP are getting voting rights at Bridgepoint makes this “a merger of equals.”

Part of the reason for the NOI is the growth in “passive” investors like Vanguard and Blackrock that have put money behind multiple utilities but are not supposed to be active in their governance.

“Blackrock is a little unique in that it doesn’t just passively manage these funds on behalf of folks’ retirement accounts,” Slocum said. “They also have an actively managed fleet of private equity vehicles that go in and buy up majority stakes in infrastructure assets.”

The panel of independent directors overseeing SPP Markets+’s development in the Western Interconnection lent its approval to the market’s draft tariff March 1, the culmination of months of drafting and refinement.

The tariff still must be approved by SPP’s Board of Directors before it can be filed with FERC by the end of the month. The board will hold a webinar March 25 to review the tariff.

“Moments like this, sometimes they can be understated. This is really a momentous occasion,” Steve Wright, chair of the Interim Markets+ Independent Panel (IMIP), said during the virtual meeting March 1. “This is a huge project that has significant implications for how the West will operate over the coming years. It shows an incredible amount of dedication and commitment on the part of the various market participants to be able to move this forward and get to this point.”

To move forward, though, the IMIP agreed to temporarily pull language specific to Western Area Power Administration’s Desert Southwest Region (WAPA-DSW), which produces hydro power for customers in Arizona, southern California and southern Nevada.

Antoine Lucas, SPP’s vice president of markets, told the IMIP that staff received a letter from WAPA-DSW on the morning of March 1 that asserted the federal agency’s intention to terminate its Markets+ Phase 1 funding agreement.

“There are certain special provisions included in the Markets+ draft tariff that are only included in the tariff specifically for WAPA, given their status as a federal entity,” Lucas said. “The special provisions included in the tariff on behalf of WAPA-DSW are very much contained into very specific, discrete areas of the tariff. We do not think they will impact any other aspects of the tariff.”

Working in real time, staff and stakeholders agreed to set the language — found in Article 2, Section 6.4 — aside for the time being.

The section’s language will have to be deleted before the tariff is filed with FERC to ensure its approval, Lucas said. The Markets+ legal subgroup will review the WAPA language and provide a recommendation on its inclusion.

Lucas declined to give reasons for WAPA-DSW’s withdrawal from Markets+’s first phase of development and whether it eventually would join the market. He said his interpretation of the letter was that it is a “formal request” to terminate the agreement.

SPP attorney Chris Nolen said the Markets+ participation agreement anticipated a participant terminating their agreement and then joining the market after it goes live. It includes provisions that ensure participants who chose that route still would have to pay what would have been their share of Markets+’s costs.

“We’ve crafted that agreement so that we would avoid the potentiality that some parties might not want to take the risk of a substantial time pending at FERC,” Nolen said, noting the market’s $500,000 monthly run rate.

“The agreement was crafted where if someone leaves before Phase 2, not only do they have to pay their fair share when they come back in, they don’t get any credit for what they paid in Phase 1,” Nolen added. “That just goes to the market bucket to offset the cost of Markets+, so there was a disincentive built into the Phase 1 funding agreement.”

The IMIP easily approved several other pieces of tariff language, including greenhouse gas settlement and substantive and non-substantive items.

“We’re looking at a pretty good pathway to getting this filed by the end of March,” said The Energy Authority’s Laura Trolese, chair of the stakeholder-driven Markets+ Participant Executive Committee.

NYISO on Feb. 29 took the first steps to creating market rules enabling hydrogen to participate in its marketplace, after kicking off the market design concept for the clean energy resource.

The ISO’s current rules do not cover how an emissions-free generator co-located with a load resource like an electrolyzer, producing clean hydrogen using energy from a nearby solar or wind facility, could participate in New York. NYISO proposes investigating if it can enable this either by creating new, or modifying existing, participation models.

NYISO estimates its clean hydrogen market participation models will be deployed in 2027 but acknowledges hydrogen is a nascent technology and so any proposed enhancements must be adaptable to innovations.

Aaron Breidenbaugh, senior director of regulatory affairs at CPower Energy Management, sought clarification on whether the final proposals, though tailored to hydrogen, could apply to a range of future resources. CPower aggregates demand response and distributed energy resources, advocating for NYISO to always incorporate evolving technologies into its proposals. (See Providers See ‘Mixed Signals’ on Demand Response in NYISO.)

Harris Eisenhardt, a market design specialist with NYISO, responded that the ISO’s objective is to propose a final market concept that is “technology-agnostic” and “suitable for other use cases as well.”

New York has devoted less attention to developing hydrogen and other less prominent fossil fuel alternatives, like nuclear or bioenergy, because they can be controversial among climate activists. (See Take the Long View on Clean Energy, NY Legislators Urged.) Instead, the focus has been on yet-unknown technologies that NYISO collectively terms dispatchable emission-free resources (DEFRs). These DEFRs are not yet commercially available, prompting the state’s Public Service Commission to explore clean energy technologies, including hydrogen, bioenergy, nuclear power and carbon capture (15-E-0302). (See NY Drills Down on Statutory Meaning of ‘Zero Emissions’.)

New York has, however, seen some actions recently promoting hydrogen development. State senators have introduced a handful of bills this year to facilitate its deployment (S378A) (S8455); Gov. Kathy Hochul (D) announced several multimillion-dollar investments in hydrogen initiatives across the state last year (14-M-0094); and New York now leads a multistate regional clean hydrogen hub competing for federal funds. (See NY Moves to Boost Hydrogen Production and Development and Vermont Joins Northeast Clean Hydrogen Hub.)

NYISO plans to review its draft market design concepts with stakeholders in the second quarter of this year and expects to finalize the proposal by the end of the third quarter.

Capacity Accreditation

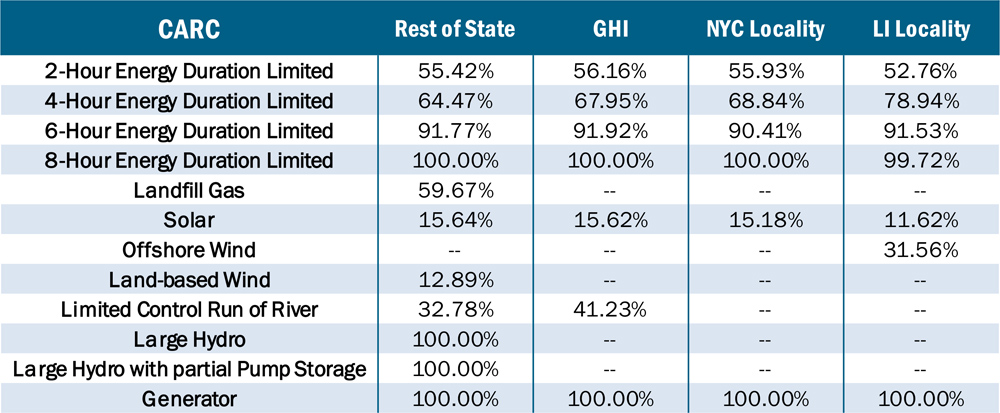

NYISO also informed the ICAP/MIWG that the final capacity accreditation factors (CAFs) and capacity accreditation resource classes (CARCs) for the 2024/25 capability year are published online.

CAFs calculate the marginal reliability contribution of “representative” generators for each CARC, a differentiation based on technology and operating characteristics. The CAFs reflect factors such as energy duration limitations and correlated unavailability due to weather or fuel supply limitations and were used alongside resource-specific derating factors to account for differences in a unit’s output from the modeled CARC profile.

Final capacity accreditation factors for 2024/25 capability year | NYISO

Last year, NYISO addressed issues in its capacity accreditation modeling, such as misrepresented marginal reliability contributions of some resources, leading to inaccurate CAF and CARC calculations. (See “Capacity Accreditation,” NYISO Finds No Need for New Capacity Zones and “Capacity Accreditation Modeling,” NYISO BIC Stakeholders OK Modeling, Market Design.)

ICAP suppliers who notice a discrepancy in their assigned values must notify NYISO by 5 p.m. March 18, when CAF assignments will be considered official.

NV Energy and several stakeholder groups have weighed in on how Nevada regulators should evaluate a request from the utility to join a day-ahead market or RTO.

Several of those who filed comments with the Public Utilities Commission of Nevada noted that PUCN faced a similar issue in 2014 — when NV Energy asked for approval to join CAISO’s Western Energy Imbalance Market (WEIM).

NV Energy made that request through an amendment to its energy supply plan. Some stakeholders said that process could also work well for considering a request to join a day-ahead market.

But joining an RTO raises new issues, stakeholders said, and PUCN should consider rulemaking to detail how such a request would be considered.

“NV Energy’s participation in the day-ahead market is analogous to its current participation in the WEIM in that NV Energy would not transfer operational control over any assets … and current state regulatory authority would be left unchanged,” Ben Fitch-Fleischmann of Interwest Energy Alliance, an association of utility-scale renewable energy developers, said in written comments.

“In contrast, joining an RTO may require a host of changes, including the development of joint transmission tariffs, consolidation of balancing area authority and operations, and changes to how transmission planning would be coordinated, and costs allocated,” Fitch-Fleischmann added.

PUCN will hold a workshop March 4 to discuss a process for reviewing an RTO or day-ahead market request.

Legislative Mandate

Senate Bill 448of the Nevada Legislature’s 2021 session directs NV Energy to join an RTO by 2030, unless PUCN waives the requirement or grants a delay. A waiver or delay is allowed if the utility can’t find “a viable and available” RTO to join or determines that joining an RTO wouldn’t be in the best interests of the utility and its customers.

PUCN opened a docket on the matter last year and, in January, ordered NV Energy to file comments by Feb. 16 answering several questions about how the commission should evaluate a request to join an RTO. Stakeholders had the opportunity to comment as well.

In NV Energy’s filing, Deputy General Counsel Timothy Clausen noted the utility’s promise in a 2013 proceeding to seek PUCN approval before participating in an RTO- or ISO-run market. But a procedure for seeking approval wasn’t detailed at that time.

In 2014, NV Energy asked for approval to participate in the WEIM through an amendment to the portfolio optimization procedures in its energy supply plan (ESP).

NV Energy said the ESP could also be used to request approval to participate in a day-ahead market or RTO. But certain aspects of joining an RTO or day-ahead market might need approval through the IRP process, the utility said. Those could include building or procuring resources or transmission to meet resource adequacy requirements.

Day-ahead Market Timeline

Some commenters worried that PUCN rulemaking to create a new approval process could delay NV Energy’s participation in a day-ahead market. CAISO’s Extended Day-Ahead Market (EDAM) and SPP’s Markets+ day-ahead offering are both expected to launch in 2026.

“Any delay in obtaining permanent regulations can impact the timeliness of NV Energy joining a day-ahead market. This delay would affect NV Energy’s customers who, in the interim, would miss out on benefits anticipated by joining a day-ahead market,” Justina Caviglia, an attorney representing Google, said in written comments. The company has data centers in Nevada.

But Advanced Energy United argued against using the IRP or ESP process for evaluating a request to join a day-ahead market or RTO.

“The regulations governing ESP/IRP [do] not currently contain requirements or standards for the evaluation of several relevant criteria, including market pricing policies, transparency and oversight, stakeholder and policymaker engagement and input, or respect for state policy mandates,” AEU director Brian Turner said in written comments.

And adding to the already complex subject matter of an IRP could be overwhelming for NV Energy, PUCN and stakeholders, AEU said.

If the commission starts rulemaking now, AEU said, regulations could be in place this summer or fall and NV Energy could apply for day-ahead market approval late this year or in early 2025.

WASHINGTON, D.C. — The power industry is facing an increasingly delicate balancing act as policies drive some generators to retirement, while major new loads are popping up and making planning for the future more difficult, presenters said during the National Association of Regulatory Utility Commissioners’ (NARUC) Winter Policy Summit.

Historically, PJM has seen its markets drive retirement decisions. Some 90% of the 66,000 MW that have retired in the past couple of decades have come offline when they requested, and most needed no upgrades to accommodate their absence from the grid, said PJM Director of State Policy Solutions Tim Burdis.

“I look out the next 10 years. In 2035 in the PJM footprint, we have 26 GW slated to come off of the system, just based on state and federal policy requirements,” Burdis said. “So that’s not factoring in anything related to the market signal, or the underlying reliability aspects.”

That’s going to lead to more of a division between generators coming off the system and its reliability needs, which means PJM and its members will need to do more to ensure reliability, he added.

“It’s also 26 GW of new load coming onto the system over that same time period in PJM’s latest load forecast,” Burdis said. “So that’s about 52,000 MW or so that are going to have to be accounted for of new supply on the system.”

While historically PJM has balanced the relatively few instances where a retirement leads to reliability issues by expanding the grid, that might not be enough going forward. Both the demand side and new generation being built at retired sites could help ensure the shift happens reliably, Burdis said.

The state of Oregon is facing many of the same issues on load, especially, which is making the PUC’s job of integrated resource planning more difficult, said Chair Megan Decker.

“I’m not going to waste our time with statistics, but suffice it to say that the Pacific Northwest in general and Oregon in particular are seeing significant interest from the data centers that are needed to power, among other things, the AI revolution and, even more exciting for our state’s economy, … high-tech manufacturing,” Decker said. “These can be hundreds or more megawatts at a time and collectively are pushing load growth projections for the region beyond anything we’ve seen or really imagined until very recently.”

Integrated resource plans (IRP) are not accustomed to the uncertainty around big new loads, with data center demand showing up more quickly than load traditionally has, and sometimes in the middle of an IRP process, making them hard to plan for.

“Because of the customer’s competitive sensitivities, they can’t be as transparently scrutinized,” Decker said.

Oregon is the rare state outside of an RTO with retail competition, and to the extent those new loads are served by competitors, Decker questioned how much retailers would contribute to the overall resource adequacy of the system.

One way of handling the situation would be to move away from IRPs and have the PUC look at procurement after the fact, but that would have negative implications for meeting state policies and affordability, she added.

Southern Renewable Energy Association Executive Director Simon Mahan is no stranger to IRPs, representing independent power producers interested in building clean energy around the Southeast. He has intervened on their behalf in many cases.

“The process is not necessarily geared towards ensuring that intervening parties like myself, like our organization, have all the information available,” Mahan said. “The information asymmetry is astronomically high as an intervening party.”

That makes it important for state regulators and their staff to prepare well ahead of time with data collection and ask the right questions, rather than waiting for the contested process to launch that starts a “sprint towards the finish line,” he added.

Typically, the processes might take a year, but utilities work on the filings starting well before that, which means they can be out of date by the time they are filed.

“They will vigorously defend the report, even though there may be news articles or press releases, even from their own corporate headquarters, saying: ‘oh, by the way, we plan to do XYZ,’ which is in total contradiction [to] what the Integrated Resource Plan actually says,” Mahan said.

Mahan quipped that the IRP reports are so full of redactions, including sometimes even publicly available data, that utilities must have a “side hustle in” markers.

The rapid changes make forecasting more difficult, and that means regulators and other intervenors are going to have to “trust but verify” what is being filed.

“How can we verify that what we’re being provided through the lens of the utility is what the customers need the best?” Mahan asked. “And one of the best ways is by letting people like me in the process, so that we can serve as another pair of eyes.”

While the industry and its regulators face hurdles to ensuring reliability on a transitioning grid, University of Chicago Law School assistant professor Joshua Macey said one common misconception of utility is not among them.

“To the extent that regulators are open to trying ambitious new options, there are no legal barriers. Our constraints are political, and they are economic,” Macey said.

The “regulatory compact” was overturned in 1934 by the Supreme Court in Nebbia v. New York, which gave Congress more power to regulate the economy. That overturned the old precedent on regulation, where utilities could be overseen because they had been granted a monopoly over the service territory.

“So, what’s notable about this is we have a set of industries that are the only industries where we have constitutional authority to regulate,” Macey said. “We then have a series of Supreme Court cases that say the question of proper regulation was a legislative determination. And yet we continue to hear arguments that the old model applies only in these industries.”

Cases since then (many dealing with the fallout from Three Mile Island and its impact on the nuclear industry) have made it clear that utilities are entitled to their existing assets, but the next set of assets are open to whatever regulatory determination is correct.

“I think we should be open to experimentation,” Macey said. “The fact that someone has done it in the past may or may not mean they’re in a position to do it most effectively in the future. But it certainly means utilities can take a loss. If they don’t reach their meet their contractual obligation, they can take a real loss.”

ERCOT CEO Pablo Vegas said last week that the “interesting dynamic” of solar energy helped the Texas grid operator meet record demand during its most recent winter storm.

“We continue to see strong solar performance being a very critical part of the resource mix,” he told ERCOT’s Board of Directors during its Feb. 27 bimonthly meeting. “We had very strong solar generation during the days of this winter event.”

ERCOT set a record for solar production at 14.84 GW during the storm’s peak Jan. 16, accounting for about 23% of system demand at the time. That mark has since been extended several times to just shy of 17.20 GW.

As of January, the grid operator had 22.26 GW of solar capacity. According to ERCOT data, another 13.15 GW of capacity is projected to be operational in 2025.

Wind production varied between 1.9 GW and 24.4 GW during the storm. Of course, demand was tightest during calm mornings before the sun rose. Vegas said “incredibly strong performance” from the thermal fleet, storage providing about 1.5% of total energy needs during the storm’s peak periods, and conservation calls helped make up for the missing renewables.

“We were right along the lines of what would be expected [for thermal outages] during that time of year and significantly improved over the performance we saw during Winter Storm Elliott,” Vegas said. “Batteries … are a growing resource on the grid that’s going to continue to be a growing component of the resource mix during those times of need.”

The grid operator set five new winter peaks during the storm, the record peak coming at 78.31 GW early Jan. 16. That was a 5.9% increase over the previous mark of 73.96 GW set during the December 2022 storm, itself a 27.7% increase over the prior record.

“So, a pretty significant increase over that period of time,” Vegas said.

He also applauded the collaboration and preparation across the industry for the grid’s performance during the storm.

“That was different than in prior storms,” Vegas said. “The planning and preparation was far more extensive and much earlier than we’ve experienced in prior storms.”

Ögelman to Retire from ERCOT

Vegas devoted part of his CEO’s report to the board in recognizing his “dear friend and colleague” Kenan Ögelman, who is retiring from ERCOT on March 30.

As vice president of commercial operations, Ögelman has overseen market operations, settlement and retail operations, and market design and development. He also led or supported several important initiatives, including various ancillary service products, Lubbock’s integration into the ERCOT market, real-time co-optimization, scarcity pricing reforms, and securitization of credit and financing after the deadly 2021 winter storm.

“Not only were the mechanics of the development and the elegance of the solutions attributable to Kenan’s leadership, but his ability to bring consensus together in these conversations was something that was really remarkable,” Vegas said. “Honestly, the most difficult thing about working with Kenan is pronouncing his name correctly, because there is nothing difficult about working with Kenan.”

For the record, Ögelman’s name is pronounced Keh-naan Oh-gell-mun.

Jupiter Power’s Caitlin Smith, who chairs the Technical Advisory Committee (TAC) where Ögelman represents ERCOT, offered her thoughts during her update to the board.

“I’ve known him, I think, my entire career in this industry,” she said. “He’s a great friend and mentor and I know that the stakeholders will miss him in this role.”

The board and stakeholders present gave Ögelman a round of applause.

He is the most senior executive to leave the ISO after Winter Storm Uri since then-CEO Bill Magness resigned.

Ögelman joined ERCOT in 2015 from CPS Energy, where he was director of energy market policy and chaired TAC from 2011 to 2013. Previously, he was a senior economist for the Texas Office of Public Utility Counsel, which represents residential electric consumers.

IMM Again Critiques ECRS

ERCOT’s Independent Market Monitor told the Reliability & Markets Committee that while the ISO managed the system reliably during the January storm and prices exceeded only $1,200/MWh, “excessively held” ERCOT contingency reserve service (ECRS) inflated prices during the event.

The IMM said prices cracked the $1,200 level even though reserves never fell below 5,000 MW during the storm and the operating reserve demand curve never exceeded $90/MWh.

“What we saw was large amounts of held ECRs likely drove some of that higher real-time pricing, particularly on Jan. 16,” Wen Zhang, the IMM’s deputy director, said, adding efficient prices could have lowered wholesale energy costs by about $90 million.

“This indicates that the concerns we raised about ECRS are still present,” she said.

The IMM has said ECRS, the newest ancillary product added in June, likely cost between $675 million and $750 million for 2023. It says the product created artificial supply shortages that produced “massive” inefficient market costs of about $12.5 billion last year.

The board agreed with the R&M committee’s and staff’s recommendations to approve a nodal protocol revision request (NPRR1186) regulating energy storage resources (ESRs) that was remanded by regulators back to the grid operator in January. (See “NPRR1186 Goes to Board,” ERCOT Technical Advisory Committee Briefs: Feb. 14, 2024.)

As directed by the Public Utility Commission, staff removed language that set penalties for batteries without sufficient state of charge to meet their obligations when deployed.

The directors also withdrew NPRR1209, which was designed to operate in tandem with NPRR1186’s compliance provisions.

Storage developers vigorously opposed NPRR1186 as it went through the stakeholder process last year. SOC requirements will be addressed by existing protocols and revisions still in the pipeline, staff said.

The directors confirmed Smith and Oncor’s Collin Martin as TAC’s chair and vice chair and approved Enerwise Global Technologies as an adjunct member. The ISO gives adjunct membership to entities that don’t meet the definitions or requirements to join as corporate or associate members.

The board also approved several other items that cleared the R&M committee Feb. 26 and previously were endorsed by TAC:

Texas-New Mexico Power’s Pecos County Transmission Improvement Project, a $114.8 million, 138-kV effort addressing reliability needs under maintenance outage conditions near Fort Stockton in the Far West weather zone.

The second phase of the Aggregate Distributed Energy Resources (ADERS) pilot project. ERCOT has cleared seven additional ADERS to go through the qualification and validation process of commercial operations, joining the two that already are participating in the wholesale market. (See “ADERs now up to 9,” ERCOT Technical Advisory Committee Briefs: Jan. 24, 2024.)

Its consent agenda included 11 nodal protocol revision requests (NPRRs), two changes to the settlement metering operating guide (SMOGRRs), a system change request (SCR) and single modifications to the load planning guide (LPGRR), nodal operating guide (NOGRR), planning guide (PGRR), retail management guide (RMGRR) previously endorsed by the Technical Advisory Committee that:

NPRR1170: define when a qualified scheduling entity (QSE) representing a resource that relies on natural gas as its primary fuel source should notify ERCOT about gas supply disruptions.

NPRR1179: ensure that QSEs representing resources with an executed and enforceable transportation contract procure fuel economically and file a settlement dispute to recover their actual fuel costs incurred when instructed to operate because of a reliability unit commitment (RUC). This change also would adjust the RUC guarantee to reflect the cost difference between the actual fuel consumed during the RUC-committed intervals and the fuel burn calculated based on verifiable cost parameters and would clarify that fuel costs also may include penalties for fuel delivery outside of RUC-committed intervals.

NPRR1193: change the ERCOT-polled settlement (EPS) design-proposal form’s referenced location when it moves from the other binding document (OBD) list into the SMOG.

NPRR1195: assign ERCOT-polled settlement metering facilities’ maintenance and repair responsibilities to the facilities’ owner if it is not a transmission and/or distribution service provider (TDSP).

NPRR1199: revise the protocols to add definitions related to the Lone Star Infrastructure Protection Act (LIPA), a 2021 law that prohibits Texas businesses and governments from contracting with entities owned or controlled by individuals from China, Russia, North Korea or Iran if the contracting relates to “critical infrastructure.” The measure also adds language reflecting ERCOT’s statutory authorization to immediately suspend or terminate a market participant’s registration or access if the ISO has a reasonable suspicion that the entity meets any of the LIPA’s criteria, among other revisions.

NPRR1206: clarify the QSEs required to have a hotline and a 24/7 control or operations center and reconcile the deadline by which QSEs representing resource entities that own or control resources must provide notice they are terminating their representation and the deadline that resource entities owning or controlling resources to change QSEs with a 45-day timeline.

NPRR1207: permit the incidental disclosure of protected information and ERCOT critical energy infrastructure information during a tour or overlook viewing of the ERCOT control room provided to eligible persons who have signed nondisclosure agreements and complied with screening and other requirements before accessing the control room.

NPRR1208: create a new daily ERCOT invoice report listing invoices issued for the current day and day prior at a counterparty level.

NPRR1210: change the frequency of the next-start resource and the load-carrying tests from every five years to every four calendar years.

NPRR1211: incorporate the OBD “Methodology for Setting Maximum Shadow Prices for Network and Power Balance Constraints” into the protocols.

NPRR1213: amend requirements for distribution generation resources (DGRs) and distribution energy storage resources (DESRs) seeking qualification to provide ECRS. The NPRR also modifies requirements for ancillary service self-arrangement and ancillary service trades for DGRs and DESRs that provide nonspinning reserve on circuits subject to load shed.

LPGRR074: align specific term language in the profile decision tree “definitions” worksheet with profile segment language that was added to the “segment assignment” worksheet with the Public Utility Commission’s 2022 approval of LPGRR069.

NOGRR261: incorporate the OBD “Procedure for Calculating Responsive Reserve Limits for Individual Resources” into the nodal operating guide.

PGRR109: require interconnecting entities associated with inverter-based resources to undergo a dynamic model review process before the commissioning date and mandate that resource entities owning or controlling operational IBRs undergo a review process before changing settings or equipment that could affect electrical performance and necessitate dynamic model updates.

RMGRR179: add a communication method so TDSPs can use Texas standard electronic transactions to inform retail electric providers of record which electric service identifiers are affected by a TDSP’s mobile generation or temporary emergency electric energy facility deployment.

SCR825: modify ERCOT’s current control room voice communication configurations to give QSEs and their subordinate QSEs greater flexibility when assigning agents, including allowing sub-QSEs to assign agents different from those used by the parent QSE.

SMOGRR027: Move the EPS metering design proposal from the OBD list into the SMOG, standardizing the approval process, and amend the design proposal form to require more information identifying all distribution service providers that have the right to serve a project.

SMOGRR030: Move the EPS metering facility temporary exemption request application form from the OBD list into the SMOG to standardize the approval process.

A dispute around the January cold snap that forced Northwest utilities to sharply increase electricity imports to meet surging demand has become a proxy for the broader contest between CAISO and SPP over their competing Western day-ahead markets.

The debate over exactly what played out on the Western grid during the Jan. 12-16 winter freeze comes amid growing tension in the Western electricity sector as stakeholders await word from the Bonneville Power Administration in April about whether it favors joining CAISO’s Extended Day-Ahead Market (EDAM) or SPP’s Markets+. It centers on whether CAISO and its Western Energy Imbalance Market (WEIM) played a key role in supporting the Northwest during the storm or other factors were more important.

The weather event that drove Northwest temperatures close to historic lows while pushing loads to nearly record highs coincided with a confluence of other developments that stressed the region’s grid. Those included: derates on the Pacific AC and DC interties; an 800-MW forced outage at Montana’s coal-fired Colstrip plant (until Jan. 13); and a fault that caused Washington’s Jackson Prairie natural gas storage facility to sharply reduce its sendout on Jan. 13, prompting pipeline operator Williams to declare a force majeure that cut deliveries to interruptible customers, including some power generators.

Those developments unfolded within the context of unusually low water levels in the region’s hydroelectric system, which has required BPA to operate the Columbia River system at minimum flows to ensure sufficient capacity behind the Grand Coulee Dam for spring fish operations.

A Feb. 8 assessment of the weather event by the Western Power Pool (WPP) showed how dire conditions became on the region’s grid. Reliability coordinator RC West placed four Northwest balancing authority areas into varying levels of energy emergency alerts (EEAs), including one EEA 3, a critical threat level that requires preparations for rolling blackouts to maintain system stability. (See WPP: Cold Snap Showed ‘Tipping Point’ for Northwest Reliability.)

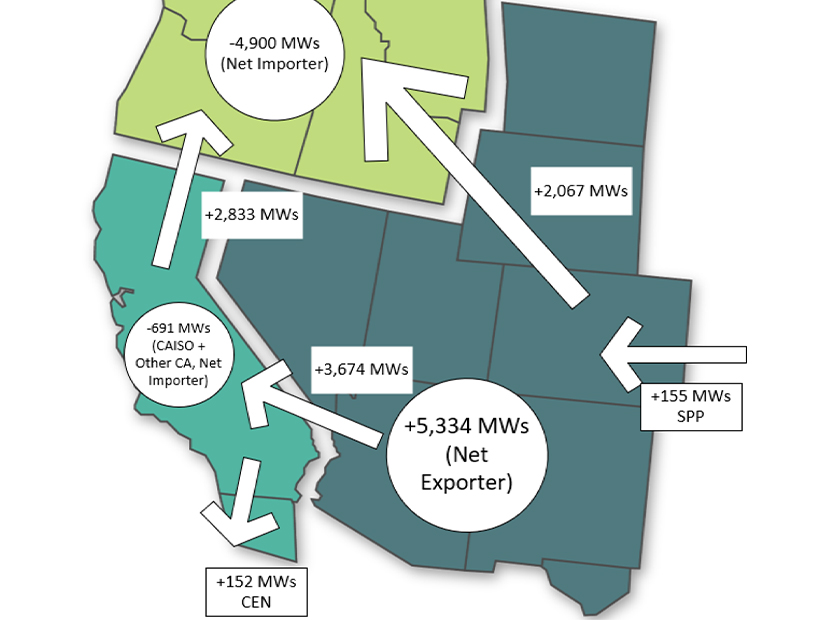

Relying on interchange data reported to the Energy Information Administration (EIA), WPP’s report showed the Northwest was a net importer of 4,900 MW of energy per hour during the five-day freeze.

And while the report showed that CAISO and other California BAs exported an average of 2,833 MW to the Northwest during the event, it also noted that the data indicated the California BAs themselves were net importers, suggesting most of the imports rescuing the Northwest originated from the Rockies and Desert Southwest — not California.

“The same interchange data shows the Desert Southwest/Rockies BAs were net exporters of approximately 5,334 MW on average,” WPP wrote. “Those exports from the Desert Southwest/Rockies region supported CAISO and other California BAs, as well as 2,833 MW of imports to the Northwest on the Pacific AC Intertie.”

Congestion Conflict

The Portland, Ore.-based Public Power Council (PPC) amplified that theme in a Feb. 23 letter to BPA Administrator John Hairston urging the agency to choose Markets+ when it issues its day-ahead market “leaning” in April. (See Northwest Public Power Group Endorses Markets+ over EDAM.)

The PPC told RTO Insider it conducted its own analysis “using data from a variety of sources including … EIA, CAISO OASIS and other publicly available sources.” It also reviewed data from WPP and Energy GPS.

Analysis by the Western Power Pool and Public Power Council indicates that most of the power supporting the Northwest during the cold snap originated in the Rockies and Southwest regions. | Western Power Pool

While the letter’s case against CAISO’s EDAM (and in favor of Markets+) focused largely on governance issues, the PPC highlighted the January cold snap, conveying concerns about how congestion revenue is allocated in the ISO’s WEIM.

“During the recent winter event in the Northwest, Northwest load imported resources largely coming from the Southwest and wheeling through CAISO,” the PPC wrote. It then spotlighted a complaint among some Northwest entities about how the ISO allocated transmission congestion fees generated during the event.

“CAISO’s congestion policies resulted in over $100M of congestion revenues being collected by the CAISO BAA, despite most of the generation serving the Northwest coming from outside California. The policy creating this result is explicitly maintained in the CAISO EDAM,” the PPC said.

CAISO responded to that contention in a Feb. 27 email to RTO Insider, saying the $100 million in congestion rent stemmed from the need for the ISO to hold back some energy flows to avoid damaging the Northwest grid because of the transmission outages in Oregon.

“Despite the assertions in the PPC letter, the ISO does not collect congestion rent for itself,” the ISO said. “It distributes it to holders of congestion revenue rights (CRRs). CRRs are mechanisms that guard against high congestion prices. They are available to a variety of market participants, including load-serving entities in the Pacific Northwest.”

CAISO noted that it is unique among Western grid operators in its technical capability for managing congestion in the day-ahead time frame.

“As a result, CAISO cannot ignore transmission constraints; it must avoid sending energy to areas where it cannot be received,” it wrote.

In a March 1 message to RTO Insider, Lauren Tenney Denison, PPC director of market policy and grid strategy, said her organization recognizes that CAISO distributes the congestion rents it collects to CRR holders within the ISO.

“While entities outside of the CAISO BAA can hold CRRs, it is our understanding that to the extent that Northwest load-serving entities were able to meaningfully hedge against the congestion charged over the California-Northwest Interties during the cold snap, they would need to have purchased CRRs from the CAISO via auction for the portion of the path within CAISO’s BAA,” Tenney Denison said.

The issue, she said, is that Northwest LSEs with ownership or capacity rights on the northern half of the interties will not receive any of the congestion revenue.

“We would like to emphasize that these assets were built based on regional coordination and with the historical mission to create benefits for both the Northwest and Southwest,” Tenney Denison said.

The PPC is asking that the value created by AC and DC interties between California and the Northwest — “as manifested here by congestion rent allocation” — be “shared equitably” by those who have invested in the lines, she said.

Tenney Denison said the PPC also understands CAISO reasons for re-dispatching around system constraints during the event.

“We look forward to additional discussion on where those constraints were observed and whether those constraints were the result of physical flows or CAISO modeling assumptions,” she said.

She added that “it is unclear when CAISO took actions to re-dispatch around these constraints whether those actions were taken as a balancing authority area, or the market operator based on CAISO’s comments.”

‘It Came from Everywhere’

Fred Heutte is a senior policy associate with the Northwest Energy Coalition (NWEC), which has been a vocal advocate for Northwest participation in a single Western market based on EDAM. In an interview, Heutte emphasized caution about reading too much into the EIA interchange data cited by the PPC and WPP, contending the numbers don’t provide sufficient insight into how power actually flowed across the system during the cold snap.

“Because all the interchange data just really does is say, ‘How much generation did you have inside your balancing authority? How much demand did you have? And, therefore, what’s the net difference?’ It doesn’t tell you that much,” Heutte said. “And especially in the Northwest, where things are very complicated. We have lots of different balancing areas.”

Heutte said the WEIM collects a “tremendous amount” of data that will take time to examine to identify exactly how power flowed during the event. But he also downplayed the importance of where the energy originated.

“I think a couple of things are really clear: that the AC intertie brought us a lot of power when we desperately needed it, and the Energy Imbalance Market was really crucial to that,” he said. “Because the market doesn’t just provide power from Point A to Point B, it optimizes the dispatch over a very wide area.”

“To me, personally, the notion of ‘where does the energy come from’ is it came from everywhere,” Heutte said.

Heutte additionally pointed to the “load and resource diversity” benefit of a market as broad as the WEIM is now.

“Because when it’s super cold up here, it’s not as cold in Southern California and Phoenix [and] Las Vegas,” he said. “If it’s really hot there, it might not be so hot here. So, load diversity helps provide some of the additional resources that the transmission in the market can then move around.”

But the PPC has drawn a different conclusion about the role of the WEIM during the freeze.

“Over the week of the cold event, CAISO’s public data shows they were a net importer during the evening peak when electricity demand is the highest,” Tenney Denison said in the March 1 email. “Other public analysis performed by the Western Power Pool and Energy GPS reaches the same conclusion. CAISO also publishes EIM transfer data that shows while the EIM did facilitate transfers to the [Pacific Northwest], comparing to the level of transmission flows published by BPA demonstrates most of the energy flowed outside of the EIM market.”

CAISO told RTO Insider it is close to issuing a “comprehensive” report on the winter event, which should be out as early as this week.

“The report will cover the dynamics of the WEIM and will provide a detailed analysis hour-by-hour of how the WEIM was able to economically re-dispatch resources to find the least-cost solution considering all the physical constraints on the system to move power across the West,” ISO spokesperson Anne Gonzales said. “That will include analysis of power flowing through California from the Desert Southwest to serve the high demand in the Northwest. The report will provide detailed information showing the actual transfers through the WEIM across the region.”

For its part, BPA has only obliquely weighed in publicly on the issues around the cold snap. In a Jan. 31 news release, the agency described how it helped keep the region powered through sophisticated maneuvers that managed to maintain targeted water levels while meeting a level of demand not seen since the time when energy-hungry aluminum smelters dominated the economy of the Columbia River region.

When asked to comment on the ongoing dispute about the winter event, including CAISO’s response, BPA spokesperson Nick Quinata said, “We’re aware of the situation and have no comment.”

Delayed Decision Urged

BPA’s reluctance to weigh in on the debate is understandable, given that its day-ahead market decision is at the heart of the larger conflict around whether the West will end up with one or two organized electricity markets.

Multiple industry sources not authorized to speak for attribution on behalf of their organizations have told RTO Insider that BPA has been favoring Markets+ throughout its public exploration of day-ahead markets, launched last July. During day-ahead market workshops hosted by BPA, agency officials themselves have expressed a preference for SPP’s approach to market governance.

And while BPA has emphasized that it has not yet identified a preferred day-ahead market — or whether it will join one at all — it has been a key participant in the process for developing Markets+. It has also been conspicuously absent as an active contributor to the West-Wide Governance Pathways Initiative, an effort kicked off by state regulators last year to create the framework for a single Western market that builds on the WEIM and EDAM.

Sources also say Northwest utilities Idaho Power, Portland General Electric (PGE) and Seattle City Light — the PPC’s largest member by customer base — are leaning toward commitments to EDAM.

Asked to comment, Idaho Power spokesperson Brad Bowlin said, “We don’t have a schedule for a public announcement. No recommendation has been made to our board of directors yet. Once that happens, depending on the outcome, we will have some work to do communicating with our regulators prior to any formal announcement.”

PGE spokesperson Andrea Platt responded that the utility “recognizes the potential value in a day-ahead market, as well as the barriers to achieving a full RTO for the West.”

“While PGE continues to evaluate participation in both the Extended Day-Ahead Market (EDAM) and Markets+, we are also actively engaged and support the West-Wide Governance Pathway[s] Initiative, which continues to explore ways to build on the benefits of the Western Energy Imbalance Market and realize the potential for a broader footprint in EDAM and enable a path forward for a potential West-wide market,” Platt said. PGE Director of Transmission and Market Services Pam Sporborg is co-chair of the Pathways Initiative’s Launch Committee.

Regarding City Light, utility Regional Affairs Manager Josh Walter also is a member of the Launch Committee. The utility, which manages its own BAA, told RTO Insider Feb. 28 that it backs BPA’s exploration of day-ahead market participation but “does not support endorsing Markets+ at this time” due to “the lack of essential information and the number of unknown variables.”

“City Light urges BPA to give careful consideration prior to making any market leaning. Doing so now would be premature, given undetermined and unresolved critical foundational issues including market footprint, transmission connectivity and governance,” spokesperson Jenn Strang said in an email. “City Light remains committed to creating a pathway to independent governance for the West and urges BPA to include the work of the West-Wide Governance Pathways Initiative in their market determination.”

With six-state utility PacifiCorp already committed to EDAM, a Markets+ consisting of just BPA and British Columbia’s Powerex in the Northwest and possibly a few entities in the Desert Southwest risks isolation and fragmentation. Under those conditions, it would not be as effective as the WEIM is in managing stressed conditions like the January cold snap, according to Heutte, who also recommends that BPA delay its decision.

“If Markets+ succeeds in moving forward with a lot of support across the West, [there will be] a Northwest zone and a Southwest zone with no direct connection from transmission,” he said. “It’ll have to transfer power across the grid of other entities that are not in Markets+, and that dramatically shrinks the load and resource diversity that’s actually available” in the West.

Along with BPA, Arizona Public Service has been a visible participant in developing Markets+ but, Heutte warned, “We have yet to see how enthused the Southwest utilities are really going to be about” the SPP market.

“One possibility is we’ll end up with something that doesn’t really come close to the performance of a much bigger market, and I think that’s a pretty legitimate issue here,” he said.